Abstract

While China’s economic development has made tremendous progress, it has also caused serious environmental pollution problems. This paper uses the date of the Chinese Private Enterprise Survey (CPES) to empirically investigate the impact of Confucianism on corporate environmental investment and its internal mechanism. The results show that: (1) Confucianism plays a significant role in corporate environmental investment. (2) In the areas where environmental regulation is relatively weak, Confucianism has a more significant effect on promoting corporate environmental investment. (3) The positive influence of Confucianism on corporate environmental investment is more obvious in heavy polluting industries. This paper’s conclusions deepen the theoretical cognition of the economic consequences of Confucianism and enrich the relevant literature on the subject of Confucianism. At the same time, this paper also expands the understanding of the determinants of corporate environmental investment from the perspective of the informal institution.

1. Introduction

Sustainability is an important part of global governance. As the main force driving economic development, enterprises are duty-bound to take the initiative to assume social responsibility. It is an important measure for enterprises to fulfill their social responsibilities by implementing environmental investment actively. While China’s economic development has made significant contributions to the world, Chinese enterprises are also being asked to pay more attention to environmental issues. In recent years, the Chinese government has introduced a number of environmental protection policies, in order to urge enterprises to implement environmental protection activities actively [1]. Although these measures have achieved some success, the status of environmental governance and investment is still not optimistic. Therefore, how to urge enterprises to actively participate in environmental protection behavior has become a hot topic in the field of corporate decision making.

Existing researches have carried out in-depth discussions on the main factors influencing corporate environmental behavior. Many external factors have been investigated by scholars. Liu et al. [2] divide corporate environmental practices into two categories, basic and proactive, and find that a perception of clear political commitment is positively correlated with the basic environmental practice of enterprises, but not with proactive environmental practices. Conversely, confusing regulatory standards and enforcement is negatively associated with corporate efforts in both basic and proactive environmental practices. Market pressures emanating from consumers, investors, and competing firms may also motivate corporate environmental management, which can help firms improve market share or charge premium prices from green consumers [3]. Yang et al. [4] found the effect of public pressure on corporate environmental behavior. When there are more environmental non-governmental organizations in the vicinity of an enterprise, they are more likely to provide close-up supervision and relevant public services (e.g., media exposure, events), which will help enterprises to fulfill their environmental responsibilities. Liao and Si [5] find that the public environmental appeals have a positive effect on increasing green investment in China. The channel analysis suggests that public appeals promote local governments’ enforcement of environmental regulation, thereby encouraging firms to increase their green investment. As for the impact of internal factors, Earnhart and Lizal [6] analyzed the effect of ownership structure on corporate environmental performance, and found that more concentrated ownership, as measured by the single largest shareholder, improves environmental performance, in the Czech Republic. Testa et al. [7] found that small and micro firms with managers with a greater environmental awareness are more likely to adopt an environmental proactive strategy. Wei et al. [8] found that when the number of female directors on the board reached more than three, female directors had a significant positive impact on the scale of enterprise environmental investment.

In recent years, more and more researchers have begun to pay attention to the influence of culture on environmental behavior. For instance, Arbuckle and Konisky [9] found that people affiliating with Judeo Christian traditions tend to express weaker environmental attitudes than individuals that do not affiliate with an established denomination. Similarly, using a large sample of data on U.S. firms, Cui et al. [10] found that the religiosity of a firm’s local region is negatively associated with the environmental decisions made by the firm’s management. However, the data they used came from the United States, where the majority of those persons who claim to be religious are Christian, therefore the result cannot extrapolate to other populations. Du [11] found that Buddhism can serve as social norms to evoke the consciousness of social responsibility, and therefore strengthens corporate environmental responsibility.

Nevertheless, little is known about the relationship between Confucianism and corporate environmental investment. Confucianism is the core traditional culture in China, and after years of dissemination, also has a strong influence on East Asia, South Asia, and Southeast Asian countries. The relationship between Confucianism and business decision making has been widely discussed. Ip [12] thinks that firms influenced by Confucianism are essentially de-based firms that treat their major stakeholders—shareholders, employees, customers, suppliers, communities, and government—as well as the environment with compassion and rightness. Lin and Huang [13] think that Confucianism leads to a strong perception of Collectivism. Confucianism and collectivism are positively related to Chinese management’s moral judgment, and also positively related to ethical leadership in Chinese management. Du [14] found that Confucianism is significantly negatively associated with minority shareholder expropriation, which indicates that Confucianism mitigates agency conflicts between the controlling shareholders and minority shareholders. Using a sample of Chinese listed firms during the period of 2001–2011, Du [15] suggests that Confucianism is significantly negatively associated with board gender diversity. Moreover, GDP per capita attenuates the negative association between Confucianism and board gender diversity. These studies provide us with ideas for further exploration of the relationship between Confucianism and corporate decision making.

Different from previous studies, we mainly focus on the relationship between Confucianism and corporate environmental investment. Theoretically, Confucianism should have a positive effect on the corporate environmental investment. Confucianism advocates “humanism (人本主义 ren ben zhu yi)”, “integration of man and nature (天人合一 tian ren he yi)”, and sustainable development, which is consistent with China’s ecological environmental strategy and the development direction of enterprises. “Humanism” advocates benevolence, ecology, and nature. “Integration of man and nature” requires people to live in harmony with nature. Sustainable development advocates that the use of natural resources should be timely, moderate, and appropriate, so as to ensure the sustainable use of natural resources. Corporate decisions should conform to social ethical behaviors. Therefore, influenced by the advocacy spirit of Confucianism on environment, enterprises may pay more attention to reduce environmental pollution and increase investment in environmental protection, so as to form a more sustainable business situation. In addition, Confucianism’s advocacy of “ morality and profit (义利 yi li)” and “ worshipping the mean and valuing the harmony (尚中贵和 shang zhong gui he)” may also affect corporate environmental investment. Based on this, we use the date of the Chinese Private Enterprise Survey (CPES) from 2010 to 2014 as the research sample to explore the relationship between Confucianism and corporate environmental investment.

We contribute to the extant literature in several ways. First, to my knowledge, it is the first empirical study of the relationship between Confucianism and corporate environmental investment. Although previous studies focused on the relationship between Confucianism and corporate decision making, they mainly addressed the concerns about the impact of Confucianism on business ethics [12,13], equity structure [14], executives’ characteristics [15], and so on. At the same time, although some studies have discussed the relationship between culture and corporate environmental behavior [9,10,11], they are mainly focused on Western culture (i.e., religion) but ignore the role of Confucianism on corporate environmental investment. Therefore, this paper fills that gap.

Second, our research provides new evidence for the relationship between informal institutions and corporate behavior and verifies a substitution effect between formal institutions and informal institutions. The existing literature has made many achievements about the influence of informal institutions (e.g., religion, culture, tradition, etc.) on corporate behavior. Our study finds that when environmental regulation is weak, Confucianism has a stronger positive impact on corporate environmental investment. It proves that informal institutions can assist formal institutions to regulate enterprises’ behaviors under specific conditions, which echoes and deepens the views of existing literatures [14,15,16,17].

Third, consistent with existing literature [18,19,20], we identify the moderating effect of industry type. Specifically, our study finds that the influence of Confucianism on corporate environmental investment is more pronounced in heavily polluting industries, which means that industry type moderates the relationship between Confucianism and corporate environmental investment.

The remainder of this paper is organized as follows. In the “Theory and Hypotheses Development” section, we put forward three hypotheses and expounded them theoretically. In the “Data and Methodology” section, we report the sample, data source, and variable measure method of this paper, and we also built a regression model for testing hypotheses in this section. In the “Empirical Results” section, we conduct descriptive statistical analysis, univariate mean difference test, regression result analysis, and robustness test. In the last part of the article, Conclusions, Implications, Limitations, and Future Research, we summarize the main findings of this paper, and on this basis, summarize the theoretical and practical significance of the research, from the perspective of the country and the enterprise, putting forward some useful suggestions for them to improve. In addition, we also put forward the shortcomings of this study, and point out the future research direction.

2. The Theoretical Analysis and Hypotheses Development

2.1. Confucianism and Corporate Environmental Investment

Individuals under social norms carry out activities in a way acceptable to the society unconditionally or without interest drive, which is mainly realized through the supervision or self-supervision of other social individuals [21,22]. Confucianism is one of the most core social norms in ancient and modern China. We think that the Confucian concept of ecological, “morality and profit (义利 yi li)” and “worshipping the mean and valuing the harmony (尚中贵和 shang zhong gui he)” can influence corporate decisions making on environmental investment.

First, the ecological concept contained in Confucianism may affect the level of environmental investment of enterprises. According to the theory of planned behavior [23], individuals and cultural factors in society (such as gender, personality, experience, cultural atmosphere, belief, etc.) will indirectly produce different behavioral attitudes and subjective norms through their behavioral concepts, which will eventually affect their intentions and behaviors. Confucianism contains many ecological concepts [24,25,26,27], such as “humanism”, “integration of man and nature”, and sustainable development. Humanism advocates benevolence, ecology, and nature, and “integration of man and nature” demands that man and nature live together in harmony. Sustainable development advocates that the use of natural resources should be timely, moderate, and appropriate, so as to ensure the sustainable use of natural resources. These ecological and environmental protection concepts of Confucianism guide people or groups in society to treat nature and environment harmoniously and play a certain role in motivating them to actively protect the environment, realize the harmony between man and nature, and achieve sustainable development. Therefore, we believe that the level of environmental investment by enterprises will be driven by Confucianism’s value proposition on ecological environment. In other words, influenced by the Confucian concept of ecological environment, enterprises will take the initiative to improve the level of environmental investment.

Second, the concept of “morality and profit” advocated by Confucianism will make enterprises obtain their own interests on the premise of environmental protection. The traditional Confucianism commerce spirit of “Morality brings profit, so it is our responsibility to contribute to the society (义以生利, 博施济众 yi yi sheng li, bo shi ji zhong)” has developed the corporate value orientation of “Gentlemen love fortune, in a proper way (君子爱财, 取之有道 jun zi ai cai, qu zhi you dao)” in modern enterprises. Confucianism believes that in the face of interests, the choice should be made by “moral principles (道义, dao yi)” [14]. Interests that conform to the moral standards can be obtained, while those that do not conform to the moral standards cannot be pursued [28]. Confucianism commerce spirit advocates righteousness and profit, because enterprises undertake social responsibility and contribute to social development, and at the same time, it can also create a good harmonious environment for enterprises to obtain profits. In fact, the ultimate beneficiaries are enterprises themselves. Enterprises undertake environmental responsibility and make environmental investment, not only to fulfill the moral obligation of protecting the environment, but also to make enterprises enjoy a higher reputation and popularity in the society. From the perspective of resource-based theory [29], environmental protection, as a key factor for enterprises to fulfill social responsibility, can also be regarded as a key material resource of enterprises. The participation in environmental governance by corporate environmental investment is conducive to improving their social benefits, increasing the government’s recognition of enterprises and their legitimacy, improving their financing ability, obtaining tax reduction, and exemption support. Based on the above situation, enterprises will take the initiative to invest in environmental protection. Therefore, we think that the Confucian concept of “morality and profit” is also conducive to promoting enterprises to invest in environmental protection.

Third, the Confucian concept of “worshipping the mean and valuing the harmony” makes enterprises dare to assume their environmental responsibility to stakeholders and resolve environmental conflicts. “Worshipping the mean (尚中 shang zhong)” refers to an impartial and conciliatory attitude towards thing while “valuing the harmony (贵和 gui he)” is the pursuit of “Harmony is most precious (以和为贵 yi he wei gui)”, and it advocated to coordinate interpersonal relations with a harmonious and tolerant attitude from the heart [30,31,32,33]. In fact, the pollution and destruction of the environment caused by enterprises have caused conflicts with the society and the public, such as industrial pollution, chemical fertilizer and pesticide pollution, household waste pollution, and so on, poisoning people’s physical and mental health and destroying the beautiful homeland. The concept of “ worshipping the mean and valuing the harmony “ will make corporate executives less self-interested, pay attention to the interests of stakeholders in the process of corporate management decisions and implementation of corporate activities, dare to assume the environmental responsibility of the enterprise to stakeholders, and try to avoid environmental conflicts or solve such conflicts. Therefore, we believe that the concept of “valuing the harmony” will also promote the investment of enterprises in environmental protection. In conclusion, we propose hypothesis 1:

H1:

Ceteris paribus, Confucianism is conducive to enhancing the level of environmental investment.

2.2. The Moderating Effect of Environmental Regulation

Institutions can be divided into formal and informal institutions [16]. Formal institutions are explicit and codified, consisting of the political rules, economic rules, and contracts that govern property rights and transactions in a society [34]. Informal institutions are tacit, usually unwritten, and exist outside the legal system [35]. Environmental regulation refers to the sum of policies and measures formulated and implemented by governments for the purpose of environmental protection [36]. Therefore, it belongs to formal institution. Confucianism is the core component of Chinese traditional culture and belongs to informal institution. We support that environmental regulation as a formal institution and Confucianism as an informal institution both have certain effects on the level of corporate environmental investment. But the two institutions can complement each other, mainly in areas where environmental regulation is weak.

From the content of institutional theory [37], organizations are regarded as institutionalized organizations because they are rooted in the institutional environments. The institutionalization of an organization is a process in which, in order to obtain political or social legitimacy, it will maintain a high degree of consistency with legal norms, cultural traditions, and social effects. At present, China has made a lot of efforts in environmental regulation. It has gradually established systematic laws and regulations on environmental protection in terms of natural resources protection and pollution prevention and control, hoping to urge enterprises or individuals to fulfill their responsibilities in environmental issues [1]. However, it cannot be ignored that China has a vast territory and there are obvious differences in environmental regulation intensity among provinces. In regions with relatively weak environmental regulations, enterprises are subject to relatively weak environmental supervision, they are under less administrative pressure from environmental protection, and the illegal cost of environmental violations incurred by enterprises is relatively low.

According to the resource-based theory [29], environmental investment by enterprises will consume some resources. Therefore, when the cost of environmental investment by enterprises is greater than the cost of environmental violations, enterprises will often choose environmental violations. That is to say, the lax environmental regulation will lead to a decrease in enterprises’ compliance rate of environmental standards and environmental expenditure [38]. At this time, Confucianism will not only reduce the motivation of enterprises to carry out environmental violations with its implied environmental protection concept, but also may replace environmental regulation to produce a certain regulatory role from the outside of enterprises.

Specifically, the stronger the Confucianism atmosphere in the region, the easier it is to form strong public opinion, causing pressure on enterprises. If an enterprise reduces its reputation because it does not fulfill its environmental responsibility and does not make environmental investment, it will be difficult to obtain social recognition and national policy support. Therefore, in regions with weak environmental regulations, the motivation of enterprises to make the decision of environmental investment is more likely to come from the supervisory role of Confucianism. At this time, Confucianism not only affects entrepreneurs’ spontaneous investment in environmental protection, but also influences corporate stakeholders to play a supervisory role to promotes entrepreneurs to increase the level of environmental investment indirectly. In regions with strong environmental regulation, the formal institution plays a more important role than the informal institution because of its mandatory characteristics. In this way, the positive influence of Confucianism on enterprise environmental investment may be less obvious. Therefore, we propose the following hypothesis:

H2:

In the case of weak environmental regulation, Confucianism plays a more obvious role in promoting corporate environmental investment.

2.3. The Moderating Effect of the Industry Type

The investment decision behavior of enterprises cannot avoid being restricted by the characteristics of industry [39]. Heavy polluting industries produce large pollution in the daily production process. Compared with other industries, stakeholders of heavily polluting industries, driven by Confucianism, attach great importance to environmental investment measures of heavily polluting industries, which may be manifested as requiring enterprises to have a higher level of environmental investment or paying more pollution control fees to the government. Confucianism, as an informal institution, plays an active role in supervising and controlling heavily polluting industries. Heavy polluting industries face more pressure from corporate stakeholders on environmental protection and may take the initiative to assume more social responsibilities for environmental protection and improvement, and improve the level of investment in environmental protection. Thus, the subordination of enterprises to heavy polluting industries may well stimulate Confucianism as a supervisory role of the informal institution, making its influence on the level of corporate environmental investment more prominent. Then, we propose hypothesis 3:

H3:

The effect of Confucianism on corporate environmental investment is more obvious in heavy polluting industries.

3. Data and Methodology

3.1. Sample and Data Sources

From 2009 to 2017, the number of private enterprises in China increased from 7.40 million to 27.26 million. Private enterprises have become an indispensable force to promote China’s development. The data used in this paper are from the Chinese Private Enterprise Survey (CPES) conducted in 2010, 2012, and 2014. The data are collected every two years by the private enterprise research group, which is composed of the United Front Work Department of the Central Committee of the Communist Party of China, All China Industry and Commerce Federation, the State Administration for Industry and Commerce, and the China Society of Private Economy at the Chinese Academy of Social Sciences. The survey covered all 31 provincial-level units (provinces, autonomous regions, and municipalities directly under the central Chinese government) of the People’s Republic of China. It has been carried out 12 times in a row, with a time span of more than 20 years, and the survey of 2018 is ongoing. However, so far, the data that the research group has made available to users are only up to 2014. In previous surveys, the data obtained each time can accurately reflect the basic situation of China’s private economy and the difficulties and problems encountered in its development. It contains key information of 15,831 firm-year observations of different industries and sizes across China. These data also contain samples of listed and unlisted companies, which to some extent better represent the survival status of private enterprises of all sizes in China. Some data needed in this paper, such as Confucianism, were not reflected in the questionnaire, so we also collected data through the Chinese Academy Dictionary, Chinese Environmental Yearbook (2010–2014), and Chinese Marketization Index (2010–2014). According to the research needs, the sample data are sorted as follows: (1) Data with missing values in variables are eliminated. (2) There are some differences about financial statements in the financial industry and the non-financial industry, so samples of financial enterprises are excluded. (3) The insolvent and zero-sales companies were excluded. Finally, we retained 8509 valid observations. In addition, we also sorted out the number of Confucian academies in the province where the enterprise was registered by hand. In order to avoid interference caused by extreme outliers, the Winsorize of 1% quantile is also used for all continuous variables.

3.2. Variables

3.2.1. Environmental Investment

In the survey data used in this paper, indicators related to corporate environmental investment include the amount invested by enterprises for pollution control and the expenses paid to the government for pollution control. Therefore, using the method of Askildsen et al. [40], this paper takes the pollution control investment of private enterprises sorted out from the survey data as the data source of corporate environmental investment and sets up the dummy variable of environmental protection investment (DEPI). When pollution control investment occurs, DEPI is 1, otherwise, it is 0. At the same time, the variable EPI is set up, and the natural logarithm is taken after adding 1 to the total pollution control input. In addition, we take the annual environmental protection fee (EPF) paid by enterprises to the government as an alternative variable of DEPI to test the robustness of the research conclusions.

3.2.2. Confucianism

Few studies have focused on the relationship between Confucianism and business management decisions, and the reason may be that it is difficult to find appropriate indicators to measure Confucianism. The existing literature mainly uses a questionnaire survey [41,42] and distance measurement [15] to measure Confucianism. Du [15] uses the distance between Confucian academies and the registered place of enterprises to represent the Confucianism index of listed companies in China, which effectively overcomes the problem that some scholars’ conclusions brought by questionnaire surveys are too subjective. As the sample of enterprises in this paper comes from the questionnaire survey and contains a large number of non-listed companies, the distance between enterprises and Confucian academies cannot be accurately obtained in this study, so the method of Du [15] cannot be used to measure Confucianism.

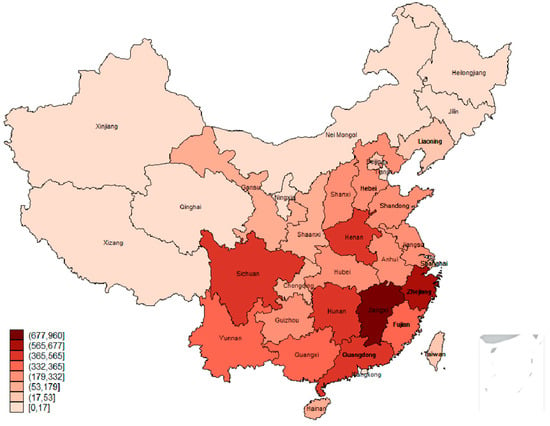

The influence of Confucianism on Chinese people and enterprises cannot be achieved overnight. It has continuously influenced the values and codes of conduct of common people and enterprises in the course of thousands of years of history. Therefore, it is feasible, reliable, and objective to use historical data to measure Confucianism. The Confucian academy is the main place for the education and publicity of the Confucianism, and it is the place with the strongest Confucianism. The Confucian academy can be regarded as the main birthplace of the dissemination of the Confucianism. Therefore, we select the natural logarithm of the number of Confucian academies recorded in historical documents to measure Confucianism (CONF). According to the records of Confucian academies in the Qing dynasty recorded in the Chinese Academy Dictionary, this paper manually collects the number of Confucian schools and academies in provincial regions established in the Qing dynasty and discusses their influence on corporate environmental investment. As the specific address of enterprises in the survey data is not clear, we match the number of Confucian academies according to their provinces as the measurement proxy variable of Confucianism. The final data show that China has 7081 Confucian academies, with an average of 208 in each province. Jiangxi has 960 Confucian academies, the largest number of Confucian academies in the province. Figure 1 shows the distribution of Confucian academies in China.

Figure 1.

Map of Confucian academies in China.

3.2.3. Moderating Variables

Environmental Regulation: Based on a large number of literature studies and the development of environmental regulation in China, Ren et al. [1] conceive that environmental regulation can be classified into three types: Command-and-control regulation, voluntary regulation, and market-based regulation. The conventional command-and-control approach to environmental. management like discharge standards, emission permits, emission quotas, etc., is to establish laws and regulations requiring polluters to cut emissions. Voluntary regulation, such as public opinion, consultation, negotiation, citizen participation, etc., in contrast to command-and-control regulation, provides incentives—but not mandates—for pollution control. Market-based regulation, such as pollution charges, emission taxes, emission subsidies, emissions trading, etc., is aimed at encouraging polluters to reduce pollution emissions. With reference to their research, we selected the number of local laws and regulations recorded in China Environmental Yearbook(2010–2014) to establish indicators of environmental administrative supervision (GOV), so as to measure the level of environmental regulation in the location of enterprises. In addition, in the robustness test, we use the ratio of the total sewage charges paid by each region to the regional industrial output value, namely the environmental economic regulation (EER), as a surrogate indicator of GOV, to measure the robustness of the test results.

Industry Type: In 2003, the Ministry of Ecology and Environment of the People’s Republic China issued Provisions on Environmental Protection Verification for Listed Enterprises and Listed Enterprises Applying for Refinancing and issued the Environmental Information Disclosure of Listed Company Guidelines in 2010; these two documents clearly define the classification of heavily polluting industry. In combination with the above two documents and The Guidelines on Industrial Classification of Listed Companies issued by the China Securities Regulatory Commission (CSRC) in 2001, we have formed the classification standards for heavy polluting industries of private enterprises. The industry attribute variable (Pollute) in this paper is a dummy variable, which is 1 when the sample company’s business involves heavy polluting industries; otherwise, it is 0.

3.2.4. Control Variables

Extant studies [6,43,44,45] recognize that an entrepreneur’s personal characteristics, enterprise scale, growth, and corporate governance will affect enterprise’s business decisions. So, we control for entrepreneurs’ gender (Male), age (Age), and education level (Edu). Meanwhile, we also control the internal characteristics of the enterprise, such as owner’s equity (Ownership), profitability (Profit), financial leverage (Lev), sales (Sales), board of shareholders (Board), board of supervisors (Supervisors), and chairman (Chairman). Considering that Confucianism and environmental regulations are measured at the provincial level, we also control the development level of each province, including Mkt and Law. Finally, in the empirical test, we also control the Industry. The variables and their definitions are described in detail in Table 1.

Table 1.

Variable definitions.

3.3. Empirical Models

In order to verify the influence of Confucianism on corporate environmental investment, we build the following regression model:

The dependent variable DEPI in the model represents the environmental investment of enterprises, which is represented by two measurement methods. The first is to use dummy variables to reflect (DEPI). When the input of enterprise pollution control is greater than 0, DEPI is 1; otherwise 0. The second method is to use the natural logarithm of the total investment of enterprise pollution treatment plus 1 (EPI). With reference to previous literatures, we also chose the following variables in the model to control: Entrepreneur’s gender (Male), age (Age), education level (Edu), owner’s equity (Ownership), profitability (Profit), sales (Sales), financial leverage (Lev), board of shareholders (Board), board of supervisors (Supervisors), chairman (Chairman), the Market environment (Mkt), the legal system environment index (Law), and the Industry (Industry). ɛ is the random error term. According to the above theoretical and research hypotheses, we expect the regression coefficient α1 of the independent variable to be positive.

4. Empirical Results

4.1. Descriptive Statistics

After descriptive statistics of key variables in the model, the results are shown in Table 2. It can be seen in Table 2 that the average of DEPI was 0.385, with the minimum values of 0 and the maximum value of 1. EPI had an average value of 4.398, a minimum of 0, and a maximum of 15.979. This indicates that there are some differences in the level of environmental investment among enterprises, and a large number of enterprises have not made environmental investment. The mean and standard deviation of CONF were 2.075 and 0.815, with a minimum value of 0 and a maximum value of 2.983. The mean value of GOV was 1.914, the standard deviation was 2.754, the minimum value was 0, and the maximum value was 18, indicating that there are also differences in the strength of environmental regulation in regions where private enterprises are located. The mean value and standard deviation of Pollute were 0.465 and 0.499, respectively, which means that nearly half of the enterprises are engaged in heavy polluting industries.

Table 2.

Descriptive statistics.

4.2. Univariate Test

According to the strength of Confucianism’s atmosphere, we divide the sample into two groups. A sample will be classified as firms with strong (weak) Confucianism atmosphere if the value of CONF is higher (lower) than the median of all samples. On this basis, the univariate test was carried out for the environmental investment of enterprises. The test results are shown in Table 3. Compared with the sample group with “Weak Confucianism”, the sample group with “Strong Confucianism” had a significantly higher level of environmental investment. When the dependent variables were DEPI and EPI, the Univariate test results were consistent. This showed that Confucianism promotes the level of corporate environmental investment, and hypothesis 1 was preliminarily verified.

Table 3.

Univariate comparisons.

4.3. Hypotheses Test

The empirical studies in this paper mainly adopt the Tobit regression. Given that DEPI is a dummy variable, the Logit regression method is used for the empirical test involving this variable.

4.3.1. The influence of Confucianism on enterprise investment in environmental protection

Table 4 reports the regression results of the influence of Confucianism on corporate environmental investment. The dependent variable in models (1) and (2) is whether enterprises have environmental investment (DEPI). The regression coefficients of CONF before and after the addition of control variables in the model were 0.226 and 0.225, respectively, which were significant at the 1% level. The models (3) and (4) change the dependent variable to EPI. When there was only the independent variable in the model, the CONF regression coefficient was 1.415 and the significance level was 1%. When the control variable was added into the model, the coefficient of CONF was 1.215, and the significance level was still 1%. It indicates that controlling the personal characteristics of business owners, internal characteristics of enterprises, market environment, and legal environment of the registered area, and the more Confucian academies in the province where the enterprise is registered, the greater the total amount of environmental investment made by the enterprise. Therefore, the regression results of models (1), (2), (3), and (4) well support hypothesis 1. From the regression results of control variables, it can be seen that the regression coefficients of Male, Ownership, Profit, Sales, and Supervisors in column models (2) and (4) were all significantly positive. This suggests that companies led by male entrepreneurs, with greater owners’ equity, better profitability, higher sales, and a board of directors, have higher levels of environmental investment. The regression coefficients of Board and Law were significantly negative, which indicates that enterprise with board of shareholders will reduce the level of environmental investment of enterprises to some extent, and a strong legal system environment is also not conducive to improving the level of environmental investment of enterprises. The internal conduction path that leads to this result needs to be verified by targeted design and empirical research.

Table 4.

The Influence effect of Confucianism on corporate environmental investment.

4.3.2. The Moderating Effect of environmental regulation

Both formal and informal institution can regulate the behavior of individuals or enterprises. Based on the above theoretical analysis, Confucianism and environmental regulation should both have positive effects on enterprises’ social environmental responsibility, and Confucianism and environmental regulation play an alternative role in influencing enterprises’ environmental investment. That is to say, in regions with weak environmental regulations, Confucianism should play a more significant role in enterprises’ environmental investment. In order to test hypothesis 2, the moderating effect of environmental regulation on the relationship between Confucianism and corporate environmental investment, we divided the samples into “strong environmental regulation group” and “weak environmental regulation group” according to the mean value of environmental regulation and conducted regression. As shown in Table 5, the regression coefficients of the independent variable CONF for DEPI and EPI were significantly positive at the 1% level in the areas with weak environmental regulation levels (models 1 and 3). However, in regions with high levels of environmental regulation (models 2 and 4), the coefficients of independent variables on DEPI and EPI were negative and not significant. This shows that Confucianism has a substitution effect on environmental regulation. In regions with strong environmental regulation, Confucianism does not play a significant role in promoting the investment level of enterprises’ environmental protection. However, in regions with weak environmental regulations, Confucianism plays a significant role in promoting enterprises’ environmental investment levels to replace the influence of environmental regulations. This regression result provides empirical support for hypothesis 2.

Table 5.

The moderating effect of environmental regulation.

4.3.3. The Moderating Effect of Industry Attribute

The above theoretical analysis shows that when the industry attribute of an enterprise is heavily polluting industry, it will be more supervised by Confucianism, so the enterprise will be more active in environmental investment. Therefore, this paper divided the samples into a heavily polluting industry group and non-heavily polluting industry group according to the industry type of enterprises and then groups them for regression. Table 6 reports the regression results. In the heavily polluting industry group (models 2 and 4), the regression coefficients of the independent variables Confucian for DEPI and EPI were both significantly positive at the 1% level. However, in the non-heavily polluting industry group (models 1 and 3), the regression coefficients of the independent variable Confucian for DEPI and EPI were positive, significant at the levels of 5% and 10%, respectively, and had lower significance compared with the regression results of the heavily polluting industry. This shows that when the industry attribute of an enterprise is heavy on polluting industries, its own ethical requirements have a stronger effect on its environmental investment behavior. That is to say, there are industrial differences in the influence of Confucianism on enterprises’ investment in environmental protection, and the positive relationship between the two is more obvious in heavy polluting industries. The regression results provide empirical support for hypothesis 3.

Table 6.

The regulatory effects of industry type.

4.4. Robustness Test

In order to further verify our main hypothesis, the robustness test was carried out by replacing key variables and solving endogenous problems. It included the replacement of dependent variables, independent variables, and environmental regulation variables and the application of the PSM matching method to explore the endogeneity of the model.

4.4.1. Replace the dependent variable

The questionnaire data used in this paper include the total amount of pollution control investment and the total amount of pollution control fee paid by enterprises to the state. Therefore, we took the total amount of environmental protection fees (EPF) paid by enterprises as an alternative variable of DEPI, put variables into the model for regression, and obtained the empirical results as shown in Table 7. As can be seen from the table, when the dependent variable was EPF, the regression coefficient of CONF was always significant at the level of 1% before and after adding the control variable. The regression results are consistent with the main effect results, which proves that Confucianism promotes the level of environmental investment of enterprises. Therefore, after replacing the measuring method of the dependent variable, the empirical conclusion of this paper is still valid.

Table 7.

Confucianism and corporate environmental protection fees.

4.4.2. Replace the independent variable

Confucianism put forward “Three Obedience and Four Virtues (三从四德 san cong si de)” to regulate the behavior and moral standards of women. Ancient Chinese Ministry of Rites also selects and honors outstanding women in this respect according to the ethical standards of women in the Confucianism and builds chastity archways to circulate it for setting up a custom. Therefore, the number of chastity archways built can reflect the influence of Confucianism on the common people or society. The more chastity archways there are in a region, the higher the Confucian cultural atmosphere there will be. We sorted out the number of chastity archways at the province level as an alternative variable of Confucianism, put the variable into the regression model, and obtained the regression results as shown in Table 8. According to the table, when the independent variable was Chastity, the regression coefficients of (1) to (4) were all significantly positive at the level of 1%. The regression results were consistent with the main effect results, indicating that Confucianism promotes the level of environmental investment of enterprises. Therefore, after replacing the measuring method of the independent variable, the empirical conclusion of this paper is still valid.

Table 8.

Chastity archways and corporate environmental investment.

4.4.3. Replace Environmental Regulation

In order to better explain the substitution effect of Confucianism and environmental regulation on corporate environmental investment, this paper adopts environmental economic regulation (EER) to evaluate the strictness of environmental regulation. The specific measurement method has been elaborated on in the definition and measurement of variables. We took the mean value of EER as the benchmark. Those higher than the mean value belonged to the group with strong environmental regulation, while those lower than the mean value belonged to the group with weak environmental regulation. Regression was performed on the variables again, and the results are shown in Table 9. Under different measures of environmental regulation, the independent variables in the models of environmental regulation weak groups (models 1 and 3), are significantly positive at the level of 1%. However, the regression coefficients of CONF in the strong environmental regulation group (models 2 and 4) were significantly positive only at the level of 10%. This indicates that Confucianism plays a better role in promoting the level of corporate environmental investment in enterprises with weak environmental regulation. The regression results provide further empirical support for hypothesis 2.

Table 9.

The moderating effect of environmental economic regulation (EER).

4.4.4. Endogenous Problems

In order to alleviate the interference of endogenous problems to the empirical conclusions, we adopted the propensity score matching (PSM) method. First, we constructed a new variable Confucian A, when the number of Confucian academies was greater than the mean takes 1, otherwise 0. Second, we took Confucianism as the dependent variable and take Male, Age, Edu, Sales, Profit, Lev, Ownership, Board, Supervisors, Chairman, Mkt, and Law as independent variables to conduct regression. At last, according to the propensity scores estimated by the logistic model, we chose an enterprise with low Confucianism as the matching sample for the enterprise with high Confucianism in the region according to the principle of similar scores. In order to make the PSM results more robust, we also generated a new variable Confucian B based on the median of Confucian academies and then conducted PSM matching. The above sample matching passed the balance test. The T-test results of the PSM paired samples on the corporate environmental investment show that compared with the control group (low Confucianism group), the treatment group (high Confucianism group) had a higher level of environmental investment. The results of multiple linear regression of PSM paired samples are reported in Table 10. The regression coefficients of CONF in model 1 to 4 were both significantly positive at the level of 1%. These findings are consistent with the above main effect regression results.

Table 10.

The effect of Confucianism on corporate environmental investment based on propensity score matching (PSM).

5. Conclusions, Implications, Limitations, and Future Research

5.1. Conclusions

In recent years, while China has made great progress in economic development, it has also produced serious environmental pollution problems. In order to deal with environmental problems and build a sound ecological and natural environment, the Chinese government has formulated and promulgated a series of laws and regulations on environmental protection and governance to regulate the behavior of enterprises. Different enterprises differ in how to fulfill their environmental responsibility and whether to comply with relevant laws and regulations. The decision and behavior of enterprises in environmental protection, especially the investment in environmental protection, has become the focus of academic circles. As one of the traditional Chinese cultures, Confucianism has nurtured a wealth of environmental and ecological concepts, including ecological environment concept, “morality and profit”, and “worshipping the mean and valuing the harmony”, which are in line with China’s environmental and ecological strategy and the way for enterprises to survive. It can be seen that the decision of enterprises to invest in environmental protection will be influenced by Confucianism to some extent. Therefore, this paper examines the impact of Confucianism on corporate environmental investment and its internal mechanism.

Based on the literature research achievements and progress in Confucianism and corporate environmental investment, this paper puts forward research hypotheses and constructs research models. Then, we use the empirical analysis method to take the sampling survey data of Chinese private enterprises as samples, referring to the existing literature to establish the measurement dimensions of enterprise environmental protection investment, Confucian culture, and other variables and form indicators. Finally, we used Excel and Stata15.0 to conduct data sorting and analysis and used multiple linear regression equation to empirically test whether Confucianism has an impact on corporate environmental investment, so as to produce empirical evidence for literature theoretical analysis.

The empirical research results show that: (1) There is a significant positive correlation between Confucianism and corporate environmental investment. The greater the strength of Confucianism in the region where the enterprise is located, the higher the level of corporate environmental investment is significant. (2) Confucianism as an informal institution, and government environmental regulations as a formal institution, have a certain substitution effect on corporate environmental investment behavior. The promotion effect of Confucianism on corporate environmental investment is more prominent in regions with weak government environmental regulations. (3) There are industry differences in the promotion effect of Confucianism on corporate environmental investment, and the positive relationship between Confucianism and corporate environmental investment is more obvious in heavy polluting industries.

5.2. Implications

The theoretical significance of this article lies in that it deepens the theoretical cognition of the influence of Confucianism on enterprise behavior from the micro-enterprise level and enriches the relevant literature on the research topic of Confucianism [12,13,14,15]. At the same time, it also expands the understanding of the determinants of corporate environmental investment from the perspective of informal institution, supporting the view of Crossland and Hambrick [16], Du [14,15], and Jiang et al. [17], which emphasize that researchers should notice the influence of informal institution (such as religion, culture, tradition, etc.) on corporate behavior. Finally, this article provides new evidence for the moderating role of industry type, expands the views of Jung et al. [18], Semenova and Hassel [19], and Sin et al. [20].

In terms of practical significance, based on the above research conclusions, this paper puts forward the following suggestions, hoping to provide beneficial suggestions for improving the environmental governance level of enterprises. First of all, this paper provides a meaningful reference for relevant departments in the improvement of the regulatory mechanism scheme. In developing countries such as China, which has a market of transitional economy and a legal environment with imperfect rules and regulations, the role of Confucianism in the moral supervision of enterprises should be given full attention. The government and enterprises can actively organize Confucian activities and put the abundant ecological theory of Confucianism into the potential consciousness of entrepreneurs and employees. Secondly, this paper provides an alternative space for Chinese enterprises to improve their own governance mechanisms. Confucianism as an informal institution has a positive effect on corporate environmental investment and business performance, thus this article suggested that when countries and the area of environmental regulation level is weak, in addition to constantly improve the intensity of environmental regulation, they should also strengthen the study and inheritance of Confucianism, and thus improve the overall environment of the local regulatory level, achieving the goal of promoting enterprise to take the initiative to improve the level of environmental investment. Finally, for heavily polluting industries, Confucianism plays a stronger regulatory role. Therefore, for countries or provinces with more developed heavily polluting industries, appropriate attention should be paid to the publicity of Confucianism, so as to improve the enthusiasm of enterprises to assume social responsibilities.

5.3. Limitations and Future Research Directions

This empirical research examines the influence of Confucianism on corporate environmental investment and the moderating effect of environmental regulation and industry on the relationship between them. However, due to some subjective and objective reasons, there are still some deficiencies in the research. Firstly, Confucianism spreads widely in East Asia, South Asia, and Southeast Asia, so the conclusions of this paper may not apply to other Eastern and Western countries. In addition, due to data limitations, we only use Chinese private enterprises as our research sample and lack samples from other East Asian, South Asian, and Southeast Asian countries, which makes our conclusions limited. Secondly, the data used in this paper are from the questionnaire survey, and the content of the questionnaire has some limitations, so the city name where the enterprise is located cannot be known. Therefore, the measurement of Confucianism can only focus on the level of the province. If the number of Confucian academies at the municipal level can be used to measure the Confucian culture, the empirical results will be more robust. Thirdly, this paper only uses the PSM method to solve the endogenous problem between variables. If appropriate instrumental variables can be found to solve this problem, it will be more conducive to verify the research conclusions of this paper. In the end, this paper discusses the influence of the informal institution on corporate environmental investment from the perspective of Confucianism. In fact, the influence of the informal institution on corporate business decisions is not limited to Confucianism. It would be more meaningful to study the influence of informal institution on enterprises’ environmental investment from the perspective of an expanded informal institution.

Therefore, in future research directions, researchers can try to use data from other Asian countries to verify the impact of Confucianism on corporate environmental investment. Researchers can also focus on finding more specific measures of Confucianism, finding appropriate instrumental variables to solve endogenous problems, and deepening the research scope of the informal institution.

Author Contributions

Conceptualization, X.X.; data curation, L.D.; formal analysis, L.D.; funding acquisition, X.X.; investigation, Y.Y.; methodology, L.D.; writing—original draft, L.D.; writing—review and editing, Y.Y.

Funding

This research was funded by Graduate Research and Innovation Foundation of Chongqing, grant number CYB19026, Philosophy and Social Sciences of Ministry of Education of China, grant number 18JHQ079, Humanities and Social Sciences of Ministry of Education of China, grant number 17YJA630017 and Fundamental Research Funds for the Central Universities, grant number 2019 CDJSK 02 XK 11. And the APC was funded by all of them.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Ren, S.G.; Li, X.L.; Yuan, B.L.; Li, D.Y.; Chen, X.H. The effects of three types of environmental regulation on eco-efficiency: A cross-region analysis in China. J. Clean. Prod. 2018, 173, 245–255. [Google Scholar] [CrossRef]

- Liu, N.; Tang, S.Y.; Zhan, X.Y.; Lo, C.W.H. Political Commitment, Policy Ambiguity, and Corporate Environmental Practices. Policy Stud. J. 2018, 46, 190–214. [Google Scholar] [CrossRef]

- Khanna, M.; Anton, W.R.Q. Corporate Environmental Management: Regulatory and Market-Based Incentives. Land Econ. 2002, 78, 539. [Google Scholar] [CrossRef]

- Yang, Z.J.; Liu, W.H.; Sun, J.; Zhang, Y.L. Corporate Environmental Responsibility and Environmental Non-Governmental Organizations in China. Sustainability 2017. [Google Scholar] [CrossRef]

- Liao, X.C.; Shi, X.P. Public appeal, environmental regulation and green investment: Evidence from China. Energy Policy 2018, 119, 554–562. [Google Scholar] [CrossRef]

- Earnhart, D.; Lizal, L. Effects of ownership and financial performance on corporate environmental performance. J. Comp. Econ. 2006, 34, 111–129. [Google Scholar] [CrossRef]

- Testa, F.; Gusmerottia, N.M.; Corsini, F.; Passetti, E.; Iraldo, F. Factors Affecting Environmental Management by Small and Micro Firms: The Importance of Entrepreneurs’ Attitudes and Environmental Investment. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 373–385. [Google Scholar] [CrossRef]

- Wei, F.; Ding, B.; Kong, Y. Female Directors and Corporate Social Responsibility: Evidence from the Environmental Investment of Chinese Listed Companies. Sustainability 2017, 9, 2292. [Google Scholar] [CrossRef]

- Arbuckle, M.B.; Konisky, D.M. The Role of Religion in Environmental Attitudes. Soc. Sci. Q. 2015, 96, 1244–1263. [Google Scholar] [CrossRef]

- Cui, J.; Jo, H.; Velasquez, M.G. The Influence of Christian Religiosity on Managerial Decisions Concerning the Environment. JOBE 2015, 132, 203–231. [Google Scholar] [CrossRef]

- Du, X.Q.; Jian, W.; Zeng, Q.; Du, Y.J. Corporate Environmental Responsibility in Polluting Industries: Does Religion Matter? JOBE 2014, 124, 485–507. [Google Scholar] [CrossRef]

- Ip, P.K. Is Confucianism Good for Business Ethics in China? J. Bus. Ethic 2009, 88, 463–476. [Google Scholar] [CrossRef]

- Lin, K.W.; Huang, K.P. Moral judgment and ethical leadership in Chinese management: the role of Confucianism and collectivism. Qual Quant 2014, 48, 37–47. [Google Scholar] [CrossRef]

- Du, X.Q. Does Confucianism Reduce Minority Shareholder Expropriation? Evidence from China. JOBE 2015, 132, 661–716. [Google Scholar] [CrossRef]

- Du, X.Q. Does Confucianism Reduce Board Gender Diversity? Firm-Level Evidence from China. JOBE 2016, 136, 399–436. [Google Scholar] [CrossRef]

- Crossland, C.; Hambrick, D.C. Differences in managerial discretion across countries: how nation-level institutions affect the degree to which ceos matter. Strat. Manag. J. 2011, 32, 797–819. [Google Scholar] [CrossRef]

- Jiang, W.; Lin, B.; Liu, Y.; Xu, Y. Chairperson collectivism and the compensation gap between managers and employees: Evidence from China. Corp. Gov. Int. Rev. 2019, 27, 261–282. [Google Scholar] [CrossRef]

- Jung, H.S.; Seo, K.H.; Lee, S.B.; Yoon, H.H. Corporate association as antecedents of consumer behaviors: The dynamics of trust within and between industries. J. Retail. Consum. Serv. 2018, 43, 30–38. [Google Scholar] [CrossRef]

- Semenova, N.; Hassel, L.G. The moderating effects of environmental risk of the industry on the relationship between corporate environmental and financial performance. J. Appl. Account. Res. 2016, 17, 97–114. [Google Scholar] [CrossRef]

- Sin, L.Y.; Tse, A.C.; Yau, O.H.; Chow, R.P.; Lee, J.S. Market Orientation, Relationship Marketing Orientation, and Business Performance: The Moderating Effects of Economic Ideology and Industry Type. J. Int. Mark. 2005, 13, 36–57. [Google Scholar] [CrossRef]

- Baumeister, R.F.; Leary, M.R. The need to belong: Desire for interpersonal attachments as a fundamental human motivation. Psychol. Bull. 1995, 117, 497–529. [Google Scholar] [CrossRef] [PubMed]

- Shulman, H.C.; Rhodes, N.; Davidson, E.; Ralston, R.; Borghetti, L.; Morr, L. The State of the Field of Social Norms Research. Int. J. Commun. 2017, 11, 1192–1213. [Google Scholar]

- Ajzen, I. The Theory of Planned Behavior. ORGAN BEHAV HUM DEC 1991, 5, 179–211. [Google Scholar] [CrossRef]

- Jenkins, T. Chinese traditional thought and practice: lessons for an ecological economics worldview. Ecol. Econ. 2002, 40, 39–52. [Google Scholar] [CrossRef]

- Nuyen, A.T. Ecological education: what resources are there in Confucian ethics? Environ. Educ. Res. 2008, 14, 187–197. [Google Scholar] [CrossRef]

- Li, M.L.; Jin, X.S.; Tang, Q.S. Policies, Regulations, and Eco-ethical Wisdom Relating to Ancient Chinese Fisheries. J. Agric. Environ. Ethics 2012, 25, 33–54. [Google Scholar] [CrossRef]

- Chen, H.Y.; Bu, Y.H. Anthropocosmic vision, time, and nature: Reconnecting humanity and nature. Educ. Philos. Theory 2019, 51, 1130–1140. [Google Scholar] [CrossRef]

- Liu, T.Q.; Stening, B.W. The contextualization and de-contextualization of Confucian morality: Making Confucianism relevant to China’s contemporary challenges in business ethics. Asia Pac. J. Manag. 2016, 33, 821–841. [Google Scholar] [CrossRef]

- Wernerfelt, B. A Resource-Based View of the Firm. STRATEGIC MANAGE J 1984, 5, 171–180. [Google Scholar] [CrossRef]

- Chen, T.; Leung, K.; Li, F.; Ou, Z. Interpersonal harmony and creativity in China. J. Organ. Behav. 2015, 36, 648–672. [Google Scholar] [CrossRef]

- Joshanloo, M. Eastern Conceptualizations of Happiness: Fundamental Differences with Western Views. J. Happiness Stud. 2014, 15, 475–493. [Google Scholar] [CrossRef]

- Kim, H.S.; Plester, B.A. Harmony and Distress: Humor, Culture, and Psychological Well-Being in South Korean Organizations. Front. Psychol. 2019, 9, 9. [Google Scholar] [CrossRef] [PubMed]

- Wang, S.Y.; Wong, Y.J.; Yeh, K.H. Relationship Harmony, Dialectical Coping, and Nonattachment: Chinese Indigenous Well-Being and Mental Health. Couns. Psychol. 2016, 44, 78–108. [Google Scholar] [CrossRef]

- North, D.C. Institutions, Institutional Change and Economic Performance: Institutions; Cambridge University Press: New York, NY, USA, 1990; pp. 37–42. [Google Scholar]

- Helmke, G.; Levitsky, S. Informal Institutions and Democracy: Lessons from Latin America; Johns Hopkins University Press: Baltimore, MD, USA, 2006; pp. 26–39. [Google Scholar]

- Liu, X.H.; Wang, E.X.; Cai, D.T. Environmental Regulation and Corporate Financing-Quasi-Natural Experiment Evidence from China. Sustainability 2018. [Google Scholar] [CrossRef]

- Zucker, L.G. Institutional Theories of Organization. Annu. Rev. Sociol. 1987, 13, 443–464. [Google Scholar] [CrossRef]

- Gray, W. Compliance and Enforcement: Air Pollution Regulation in the U.S. Steel Industry. J. Environ. Econ. Manag. 1996, 31, 96–111. [Google Scholar] [CrossRef]

- Chiasson, M.W.; Davidson, E. Taking industry seriously in information systems research. Mis Q. 2005, 29, 591–605. [Google Scholar] [CrossRef]

- Askildsen, J.E.; Jirjahn, U.; Smith, S.C. Works councils and environmental investment: Theory and evidence from German panel data. J. Econ. Behav. Organ. 2006, 60, 346–372. [Google Scholar] [CrossRef]

- Lin, L.H. Cultural and Organizational Antecedents of Guanxi: The Chinese Cases. J. Bus. Ethics 2011, 99, 441–451. [Google Scholar] [CrossRef]

- Sun, Y.; Garrett, T.C.; Kim, K.H. Do Confucian principles enhance sustainable marketing and customer equity? J. Bus. Res. 2016, 69, 3772–3779. [Google Scholar] [CrossRef]

- Ahn, J.M.; Minshall, T.; Mortara, L. Understanding the human side of openness: the fit between open innovation modes and CEO characteristics. R&D Manag. 2017, 47, 727–740. [Google Scholar]

- Ho, S.S.M.; Li, A.Y.; Tam, K.S.; Zhang, F.D. CEO Gender, Ethical Leadership, and Accounting Conservatism. J. Bus. Ethics 2015, 127, 351–370. [Google Scholar] [CrossRef]

- Huang, Q.; Chen, X.; Zhou, M.; Zhang, X.; Duan, L. How Does CEO’s Environmental Awareness Affect Technological Innovation? Int. J. Environ. Res. Public Heal. 2019, 16, 261. [Google Scholar] [CrossRef] [PubMed]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).