1. Introduction

The rapidity and quality of the transmitted information and the related increasing pace of the spread of new information and communication technologies caused various changes in the economy. Deep social change and the accompanying digital revolution have meant that owned goods cease to be treated as the most important value [

1,

2]. As a result, a new business model based on the exchange of resources was created. The previous research shows that cooperation in interorganizational networks allows for generating benefits through sharing resources, knowledge, competence, which leads to the achievement of common goals and benefits [

3,

4,

5,

6].

Modern technologies and solutions available in the new industrial revolution allow for the implementation of a new business model based on the exchange of all the available assets and their optimal use [

7,

8,

9]. Connection of the network of entities and innovative information technology allow for an increase in the productivity of the company’s resources, as well as an increase in the efficiency of business processes [

10,

11]. This means the readiness to implement tasks associated with streamlining the flow of physical resources and exchange of information [

12], at the same time, expecting the increased production but with the same resources [

13,

14]. The exchange of resources is reasonably justified in the change in the production paradigm (

Table 1), i.e. the transition from mass production to individual production.

As far as mass production does not engage the customer at all, in the case of mass customization, it is the customer that decides on the final product. This stage corresponds with new goals and directions associated with a flexible market activity and assumes that no entity has all the resources necessary to achieve the indicated objectives of the market [

15,

16,

17,

18]. As a result, both in the vertical and horizontal value chain, an important part of the current functioning of the entity on the market is the effective management of assets [

19].

The paper is organized as follows.

Section 2 presents the objectives and challenges of the sharing economy in the contemporary economy, which are presented to the society and entrepreneurs.

Section 3 presents the results of the research into the implementation of the concept of sharing between enterprises. The discussion on the obtained results is held in

Section 4.

Section 5 includes the final conclusions and the directions of future research.

3. Research Methodology

Literature studies indicated that management of resources is an important part of the social and environmental policy. However, the limited research in this area does not indicate clearly what this phenomenon looks like in the economic practice and what its range is. As a result of the conducted research, the information on the use of resource exchange among the surveyed enterprises was collected. The primary objective of the empirical part was to respond to the question: Do companies possess redundant or unused assets? And if so, are they able to benefit from this? In order to search for the responses to these questions, in the first quarter of 2019, the nationwide survey was conducted, concerning the level and type of the redundant assets owned and the ways of their management in enterprises with a different type of activity.

The size of the research sample was 352 entities, among which the number of enterprises, broken down by the number of employees, was distributed evenly. In the research, broken down by the number of employees, a similar number of entities participated (26% of micro-enterprises; 25% of small ones; 24% of medium ones; and 25% of large ones). The data collection was carried out randomly using the CATI method (Computer Assisted Telephone Interviews). This method allowed for the rapid collection of necessary data and, simultaneously, the reduction in the number of possible errors committed by the respondents. During the ongoing telephone session, the questions are displayed on the interviewer’s computer screen, which enables the control of the accuracy of the record of responses. Consequently, the reliability of the responses obtained from the respondents increased [

61,

62].

The main hypothesis assumes:

The main hypothesis: Enterprises use the sharing economy in their activities depending on the assets possessed and fixed costs generated.

The verification of the main hypothesis consisted of a few stages:

Firstly, the assessment of the potential for resource exchange between enterprises ought to be made;

Secondly, it should be verified whether the surveyed enterprises exchange resources with each other;

Groups of enterprises broken down by the applied model of resource exchange should be identified;

Subsequently, it is necessary to examine the impact of the level of the resources possessed on the occurrence of the motivation to exchange them with other entities.

4. Results

4.1. The Assessment of the Potential for Resource Exchange Between Enterprises

Here, the exchange potential is understood as the level of assets which can be partially subject to exchange between different entities (

Table 3).

The preliminary research indicated that the vast majority of enterprises have less than 60% of fixed assets in total assets. In most cases, less than 20% of these assets are used seasonally or temporarily. The vast majority of these enterprises possess material resources which they use continuously in their activities. Fixed costs invariably remain at the same level per annum and, among others, they depend on the costs of maintenance of assets; therefore, the willingness to reduce fixed costs should also result from the disposal of redundant assets in the company. In the surveyed entities, the share of fixed costs per annum in total costs is most frequently at the level of not more than 60%. This means the possibilities of exchanging resources which are involved temporarily, which are redundant or unused. At the same time, 96% of the surveyed enterprises declared they had ever possessed redundant assets. The structure of material resources which remain unused most frequently in the company’s activity during the year is the following:

Machinery and equipment (40.1%);

Stocks of raw materials, materials, and intermediate goods (35.5%);

Ancillary and buffer stocks (21%).

Therefore, it can be observed that enterprises possess the potential to use the concept of the sharing economy, particularly in the area of machinery and equipment as well as stocks. As far as stocks constituting a part of current assets that can be efficiently liquidated and the related funds can be recovered, it is much harder to get rid of the equipment which is needed in the activity of the entity only in selected periods.

The preliminary analyses indicated that enterprises possess the physical potential to use the concept of the sharing economy since they own the assets, in particular, machinery and equipment, which are not fully used. Moreover, these enterprises indicate the possession of redundant assets which they most frequently sell (62%) or lend for fee or donate (36%). However, it should be assumed that this is only the assets which are not used in the enterprise at all. The remaining redundant assets are most often lent and they are unnecessary only temporarily.

4.2. The Level of Resource Exchange Between Enterprises

The exchange of resources between enterprises was considered in the category of the form and direction of their flow. The one-way and two-way flow, as well as the form of partial or temporary exchange, were taken into account. It was assumed that enterprises may exchange resources:

partially—to transmit only this part of the resources which they do not need at all; in this case, the most frequent form of transmission is sales;

temporarily—to transmit only this part of the resources which they do not need at a specific time; in this case, the most common form of transmission is lend for fee or donation;

one-way—only to share their resources or exclusively to use the resources of other companies;

two-way—to share their resources and use the resources of other companies simultaneously.

The possibility that enterprises do not show the willingness to exchange resources was also taken into consideration.

Table 4 presents habits concerning sharing resources in the surveyed enterprises.

Every third company does not decide on sharing its resources; however, they are already less reluctant to reach for the resources of other companies. In turn, every third company uses the external resources temporarily and shares them in this form slightly more often. Taking into account the possibility of partial transmission, enterprises more frequently reach for their own resources than those of others. The obtained indications are comparable with each other. At the same time, it can be observed that sharing resources based on the existing outsourcing relationship occurs only in few cases.

In the case of most enterprises, the flow of assets based on temporary or partial exchange can be observed. For the significant share of entities (every third one) there is no need to exchange resources in their activities.

The overwhelming number of companies which decide on the mutual transmission of assets allows the positive verification of the first part of the main hypothesis, which assumes that enterprises use the concept of the sharing economy in their activities.

4.3. The Identification of Groups of Enterprises Broken Down by the Applied Model of Resource Exchange

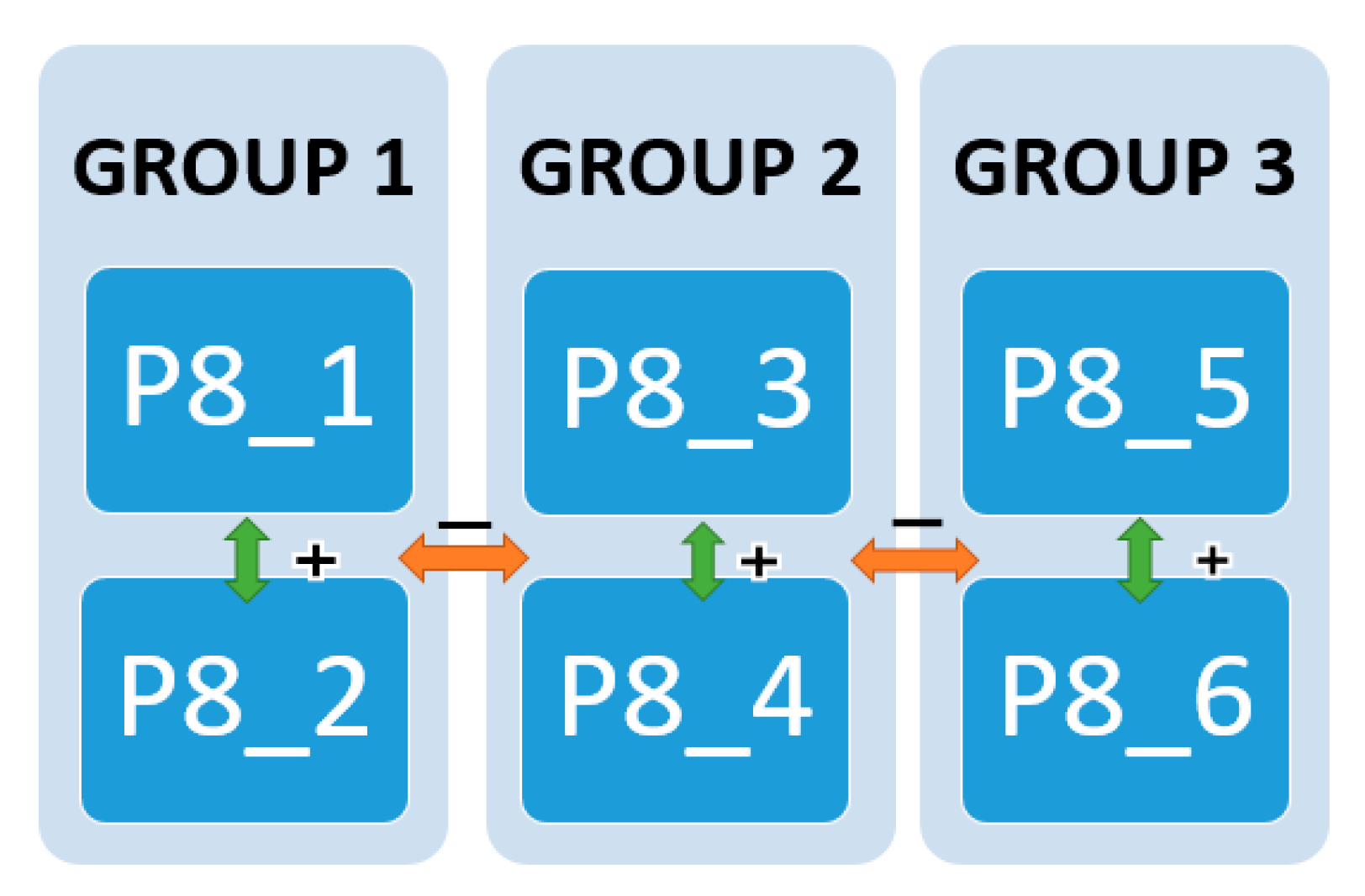

For the purpose of the assessment of the impact of the assets possessed and costs generated on the approach towards sharing resources, first of all, the groups of enterprises were isolated, broken down by the applied model of exchange of resources. In order to present some significant relationships between the possible ways of resource exchange (see:

Table 4), the Chi-square correlation analysis was carried out (

Table 5).

The results allowed for identification of the following significant pairs of variables, where:

- a)

χ2 (1, N = 352) = 0.389, p < 0.001 means that the entity which indicated P8_1, equally often indicated P8_2;

- b)

χ2 (1, N = 352) = −0.459, p < 0.001 and for χ2 (1, N = 352) = −0.325, p < 0.001 means that the company which indicated P8_1 simultaneously did not indicate P8_3 and P8_4;

- c)

χ2 (1, N = 352) = −0.458, p < 0.001 and for χ2 (1, N = 352) = −0.427, p < 0.001 means that the company which indicated P8_2 simultaneously did not indicate P8_3 and P8_4;

- d)

χ2 (1, N = 352) = 0.312, p < 0.001, means that the company which indicated P8_3, equally often indicated P8_4;

- e)

χ2 (1, N = 352) = 0.595, p < 0.001, means that the company which indicated P8_5 equally often indicated P8_6;

- f)

χ2 (1, N = 352) = −0.116, p < 0,001 and for χ2 (1, N = 352) = −0.115, p < 0.001 means that the company which indicated P8_5 simultaneously did not indicate P8_3 and P8_4;

- g)

χ2 (1, N = 352) = −0.199, p < 0,001 means that the company which indicated P8_6 simultaneously did not indicate P8_3 and P8_4.

Significant correlations between the selected pairs of variables allowed the isolation of specific groups of enterprises broken down by the practiced approach to the concept of sharing. The graphical illustration of the combinations is presented in

Figure 1.

Group 1. The enterprises which share resources temporarily:

A. share their resources B. use the resources of others C. simultaneously share and use

Group 2. The enterprises which share resources partially:

A. share their resources B. use the resources of others C. simultaneously share and use

Group 3. The enterprises which do not share resources:

A. do not share their resources B. do not use the resources of others C. simultaneously do not share and use

Subsequently, the results of indications based on new groups of the application of the concept of the sharing economy were examined. The results of these groups were presented as a percentage in

Table 6.

The most frequently practiced model in the case of entities which apply the concept of the sharing economy is the two-way resource exchange. In a situation where enterprises do not decide on exchange, they most often do not share their resources. This allows for the conclusion that, if enterprises implement the concept of the sharing economy, this is most frequently realized through mutual exchange of assets.

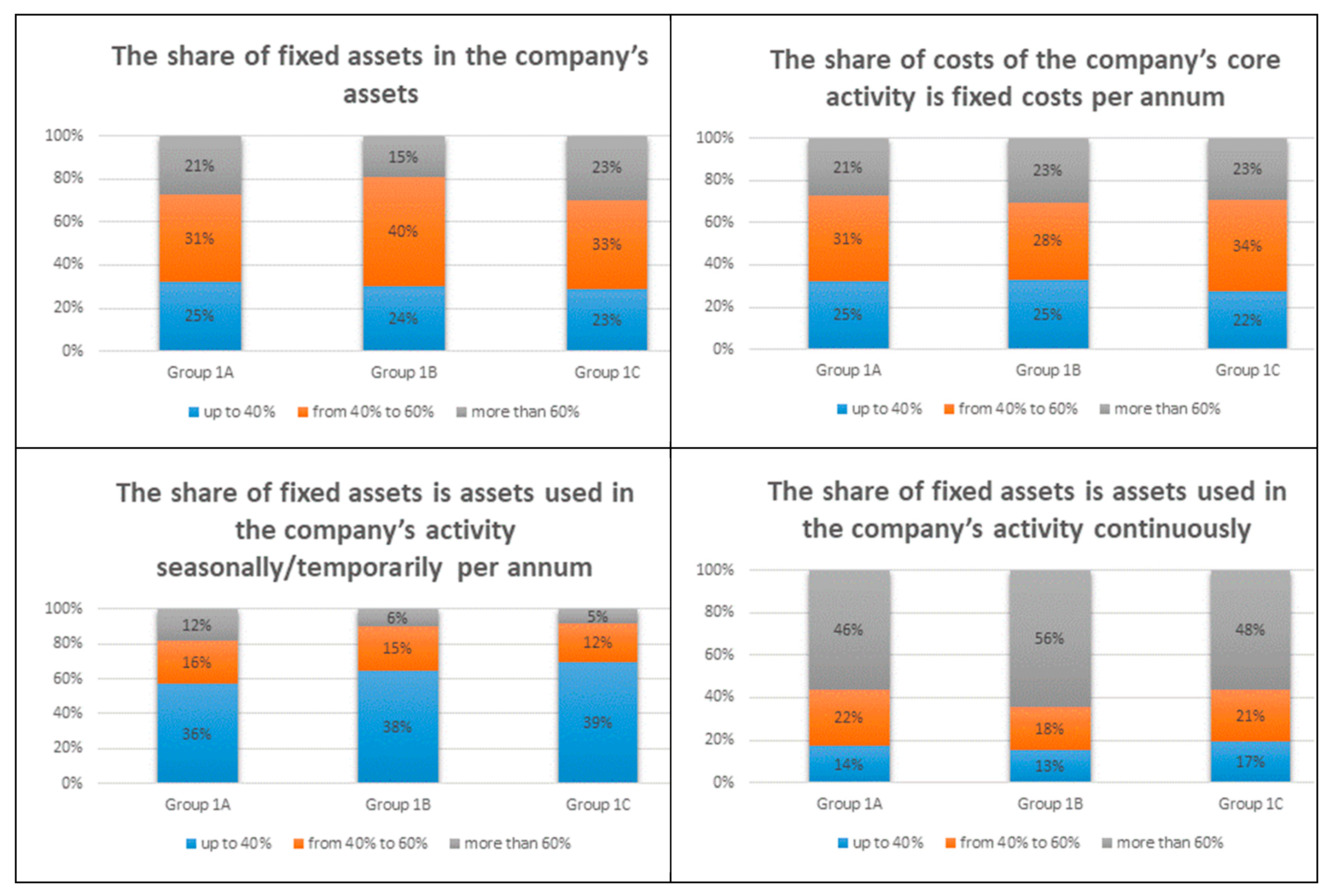

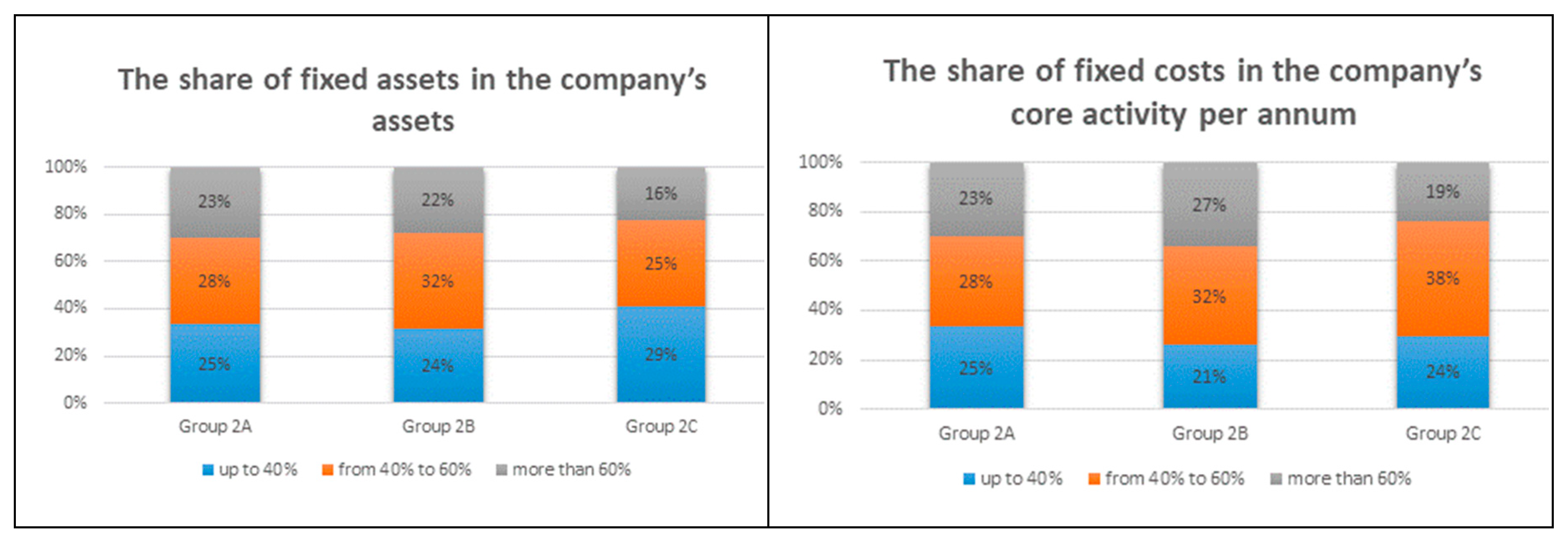

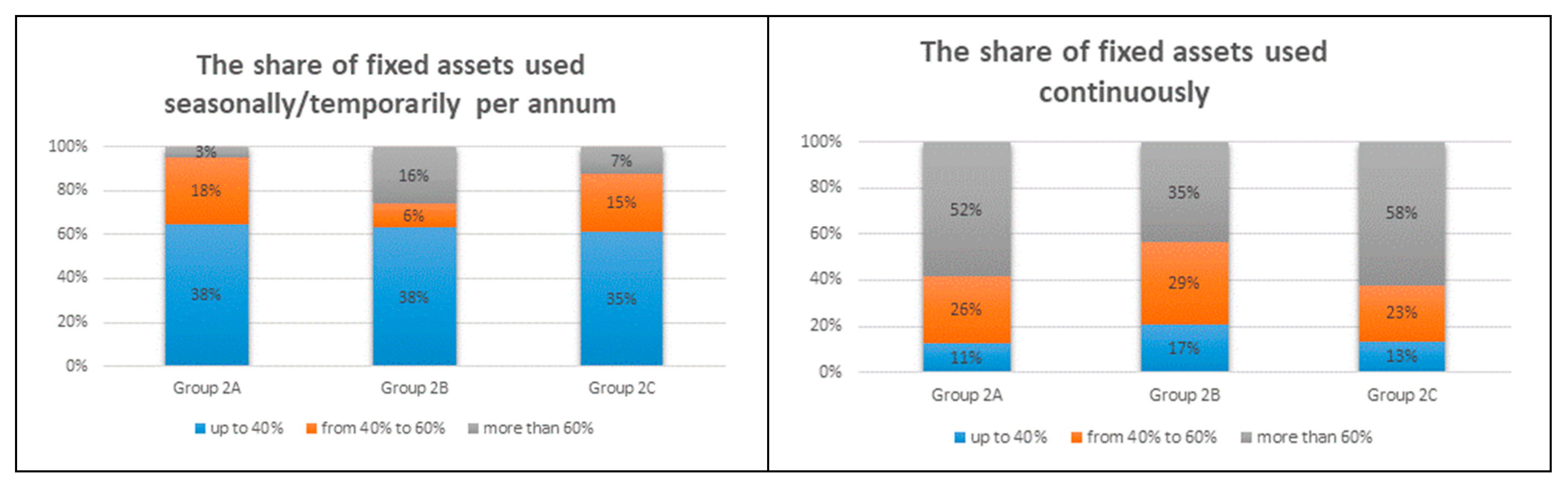

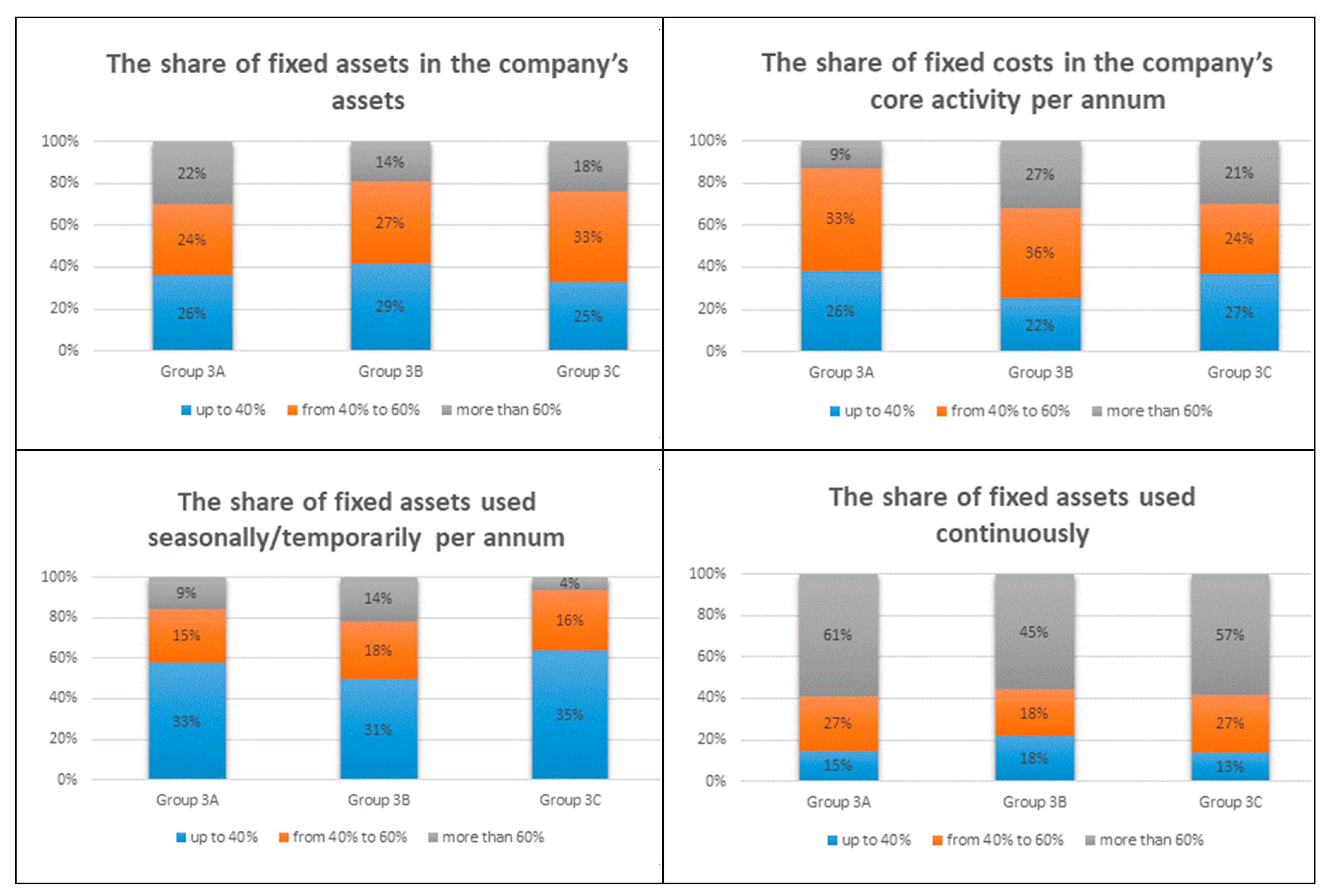

Subsequently, the detailed analysis of the structure of assets and fixed costs was conducted in relation to the applied model of resource exchange in the surveyed companies. The results were presented graphically for the three previously isolated groups (

Figure 2,

Figure 3 and

Figure 4).

When comparing the conditions for the company’s asset management for Group 1, the same trends are observed between the three subgroups. In each of the groups, the share of fixed assets in the company’s assets most often ranges from 40% to 60%; fixed costs are at the same level. The group of these enterprises has up to 40% of fixed assets which are used seasonally/temporarily; on the other hand, the majority of them have more than 80% of assets used in the company continuously.

Also, in Group 2, the same trends for the share of assets and fixed costs are observed. In each of the subgroups, the share of fixed assets in the company’s assets most frequently ranges from 40% to 60%, fixed costs are at the same level. The share of fixed assets most often amounts up to 40% of fixed assets which are used seasonally/temporarily and more than 80% of assets used continuously.

In Group 3, it can be observed that the share of fixed assets amounts to up to 40% for enterprises which operate following the two-way exchange. In turn, enterprises which share resources one-way possess from 40% to 60% of fixed assets. Fixed costs most commonly range from 40% to 60% of total costs. The differences due to the seasonal use of assets are not observed, where most frequently their share amounts to up to 40%. The group of these companies has more than 60% of fixed assets which are used continuously.

The graphical characterization of individual groups of enterprises broken down by the assets possessed and fixed costs generated indicated the lack of significant differences between the subgroups. Both the direction of exchange and its form do not result from the level of fixed assets and fixed costs. Therefore, in the subsequent part of the research, only the fact of resource exchange or its lack due to the assets possessed was verified.

4.4. Types of the Resources Possessed and the Willingness to Share Resources

In order to verify the second part of the main hypothesis, it was subsequently tested whether sharing resources in the surveyed entities is determined by the structure of the assets possessed and the share of fixed costs. For this purpose, the fact of resource exchange was coded using the binary system, where:

The relationship was verified using the Spearman’s rho nonparametric test. The results are presented in

Table 7.

It is observed that there is a relationship between the share of fixed assets in the company’s total assets and the willingness to exchange resources between the surveyed entities. The other variables do not significantly affect the approach to resource exchange. In order to verify the differences between the surveyed groups of enterprises which exchange resources and the companies which do not implement this approach and the share of fixed assets in total assets, the ANOVA test was subsequently carried out for the means of these groups(

Table 8).

The results of the obtained test F (2.338) = 2,427; p < 0.049 means that it is statistically significant. This means that it should be assumed that there are significant differences between the means in the groups compared. In order to assess how these means differ from each other, the data of the descriptive statistics were generated (

Table 9).

It is observed that, the larger the share of fixed assets in total assets, the greater the motivation indicated by enterprises to share and exchange the resources possessed. Based on this, it should be noted that the main hypothesis was verified positively only partially. This means that enterprises use the sharing economy in their activities more willingly if the share of fixed assets in total assets is higher. At the same time, it was not indicated that the use of assets in time (seasonally or continuously) and fixed costs generated were of great significance in the process of exchange.

The summary of the results of the four research stages is presented in

Table 10.

The collected results allow for the final conclusion that enterprises use the sharing economy in their activities depending on the level of the assets owned, regardless of their type and generated fixed costs.

5. Discussion

The conducted research in the field of the sharing economy among enterprises allowed for making a number of important observations. The vast majority of companies have material resources which they use in their activities continuously. Fixed costs remain stable per annum. At the same time, almost all the surveyed enterprises declared they had ever possessed some redundant assets, which are most frequently lent and which are redundant in their nature only temporarily or partially [

63]. According to the research by MarketplaceHUB, among tangible assets the most frequently exchanged between companies, there are primarily unused materials and raw materials [

64]. In order to manage the assets more effectively, P.N. Umoh [

65] and J. Pfeffer [

66] suggest conducting their systematic registry, the task of which is their proper use or release if they are not necessary any longer.

In the case of the majority of enterprises, the flow of assets was observed based on their temporary or partial exchange. The most frequently practiced model in the case of entities using the concept of the sharing economy is a two-way exchange of resources. This means that, most often, companies indicate the willingness to simultaneously exchange resources. According to S. Siitonen [

67] and D. Slagen [

68], the sharing economy between enterprises transmits the mentality of companies from possession to access. The research into individual groups of enterprises, broken down by the assets possessed and fixed costs generated, indicated the lack of significant differences between the subgroups identified in the research. Both the direction of exchange and its form do not result from the characteristics of fixed assets and fixed costs generated in enterprises. It was not indicated that the seasonality or continuity of the use of an asset influenced the willingness to share. This is confirmed by the research by D. Slagen [

68], according to which, it is the process of sharing resources that plays the main role in resource exchange and improves the operation of enterprises, which translates into faster operations and rapid responses to market changes. At the same time, the fact that there is a relationship between the share of fixed assets in total assets and the willingness to exchange resources between the surveyed entities was verified positively in the research. The larger the share of fixed assets in total assets, the greater the motivation indicated by enterprises to share and exchange the possessed resources [

69]. This means that the ownership of the excessive or temporarily or partially redundant assets itself is only one of the determinants of sharing one’s own resources with other forms. S.M. Ekayanti et al. [

70] supplement that the basis for the effective management of assets is the proper information system, which is simultaneously an important part of the fourth industrial revolution. B. Cohen [

71] confirms that, for the sharing economy in business, it is more important to select the transaction model and manage the flow of information than to possess common resources and technologies. C. Lemmens and C. Luebkeman [

72], as the most important role in the implementation of the sharing economy in business, also list the exchange of information. Modern IT solutions induces cost reduction and revenue growth, resulting in a real competitive advantage for the whole chain [

73,

74].

6. Conclusions and Recommendations

The sharing economy gives new meaning to the concept of consumption which, along with the technological and social progress, more and more frequently includes sharing, exchange, and lend of resources based on mutual cooperation. The “possession” loses its value, whereas sharing and sharing unused resources gains value. The task of such an approach is to develop a range of benefits associated with generating higher profits, cost reduction by limiting unnecessary investments, and overall improvement in business performance.

The research indicated that the possession of excessive material resources is only one of the reasons for resource exchange. The larger the share of fixed assets in total assets motivates the enterprises to share and exchange the resources possessed. However, after more thorough consideration, neither the type of resources nor the willingness to reduce costs constitute the motivation of the entity for conducting the sharing economy if there are no formal and technological solutions enabling its implementation. The surveyed companies do not differ from each other due to their assets and generated fixed costs, which means that the direction of exchange as well as its form do not result from the level of fixed assets and fixed costs.

The conducted research has some constraints, though. If the level and type of fixed assets do not constitute the main motivation for resource exchange, the main source of such behavior should be sought in the lack of appropriate technologies and information platforms, which enable the exchange of information in this field. Therefore, further research should include the analysis of opportunities and the level of technological development of companies. Moreover, there is a need to repeat the research including a larger number of samples in a few countries, in order to also take into consideration companies operating in a global network. Such extended research can also serve as the basis for responding to the question as to how the concept of Industry 4.0 is implemented in these enterprises. This should be another research step; therefore, the presented research in the field of the sharing economy in the era of the fourth industrial revolution can be found as the preliminary effort made towards this direction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}