Abstract

Nowadays, listed companies around the world are shifting from short-term goals of maximizing profits to long-term sustainable environmental, social, and governance (ESG) goals. People have come to realize that ESG has become an important source of the corporate risk and may affect the company’s financial performance and profitability. Recent research shows that good ESG performance could improve the financial performance in some countries. Yet, the question of “how does ESG affect financial performance” has not been thoroughly discussed and studied in China. In this article, we study China’s listed power generation groups to explore the relationship between ESG performance and financial indicators in the energy power market based on the panel regression model. The results show that good ESG performance can indeed improve financial performance, which has significant meanings for investors, company management, decisionmakers, and industry regulators.

1. Introduction

Environmental, social, and governance (ESG) refers to the environmental, social, and corporate governance performance that is considered in corporate decision-making. ESG information disclosure refers to the legal system in which the issuer of securities releases the company’s environmental, social, governance, and financial management information in a comprehensive, timely, and accurate manner for the market to have a rational judgement for the value of the investment in order to safeguard the legitimate rights and interests of the shareholders or creditors. Since 1992, the United Nations Environmental Programme Financial Initiative (UNEP FI) has been advocating for financial institutions to integrate ESG factors into the decision-making process. Since then, ESG has gradually become one of the three main dimensions for the international community to measure the ability of the sustainable development of economic entities.

The need for ESG research in China’s energy power market is urgent at present. In the next decade, China’s carbon dioxide emissions will continue to increase, and the pressure for emission reductions will continue to increase [1]. As investment in coal-fired power continues to rise, operating efficiency will continue to deteriorate [2]. As a result, development will continue in most provinces in China in 2020. Yields are lower than the national average, and there are even negative values, which are destructive to the development of the entire industry [3]. China has begun to take action in this area. The “Integrated Reform Plan for Promoting Ecological Progress” released by the CPC Central Committee and State Council at the end of 2015 declares that “A mechanism will be established for the mandatory release of environmental protection information by listed companies” in the capital market, following the “13th five-year plan”, which pointed out that it is necessary to move the industry towards the mid- to high-end level and raise the “eco-friendly development” concept to a strategic goal. In the energy sector, the primary policy is to “adjust inventory, make incremental improvements and actively resolve excess capacity”. The formulation of these policies and regulations means that the traditional energy industry can no longer take the old path of “the extensive style of economic growth”. Because the large power generation groups in China are affecting China’s energy trends, the orientation of its development then would be the key to determining whether they could achieve those macro goals. This forced China’s power generation groups to rethink their strategic approach and adjust their profit model. Moreover, how to achieve sustainable development while maintaining profits has become a problem that has to be faced.

At the international or regional level, according to the Schroeder investment survey results, emerging market investors place more emphasis on the concept of ESG investment than do investors in developed countries. Global investment in ESG-related companies has increased from 17 trillion dollars to 28 trillion dollars [4] from 2012 to 2014. Thus, it can be seen that the concept of ESG investment has become one of the hot spots in the world. In addition, the importance of ESG disclosure has been recognized by more and more regulatory agencies, exchanges, and investors. Many stock exchanges in the world have launched listed company ESG disclosure requirements or guidelines in countries, such as the United Kingdom, Brazil, Canada, India, Malaysia, Norway, South Africa, Sri Lanka, Thailand, Germany, the Philippines, Poland, Singapore, Turkey, and so on [5]. On 21 December 2015, the Hong Kong Stock Exchange (HKSE) amended the “Guidelines for ESG Reporting” and added the “Comply or Explain” clause. This clause requires listed companies to disclose specific ESG information or explain the reason why this information is not disclosed.

With the continuous progress of China’s “One Belt and One Road” initiative and the continuous deepening of international energy cooperation, the construction of the ESG system will help China’s energy companies gain more international recognition and facilitate their “going global” strategy. For China, ESG is still a relatively new concept. China’s ESG construction started late. A considerable number of listed companies have only started issuing ESG special disclosures in recent years, but there are still many listed companies that have adopted the production of ESG disclosure as a future plan and that have not really implemented it to date. Due to the weak awareness of corporate managers and the lack of supervision by the supervisors, their development is also slow. At present, there are few studies on the relationship between ESG and financial performance and the construction and rating of China’s ESG evaluation index system. The construction and rating of the ESG evaluation index system for China’s power industry and its relationship with ESG and financial performance are rare. The inquiry is almost nonexistent.

The textual structure of this paper is explained as follows: The Introduction in Section 1 discusses the background of ESG research and emphasizes the urgency and importance of studying ESG in large-scale power generation listed companies in China. In Section 2, a literature review is presented regarding the disclosure of corporate social responsibility information and the research results of ESG in China and abroad. Section 3 is about the research objectives of this research. In Section 4, the methodology, the construction, and evaluation process of the ESG evaluation system is explained, and the panel regression model is explained too. The empirical analysis is carried out at the end of Section. Finally, in Section 5, we discuss our conclusions and make policy suggestions according to the significance of the conclusions.

2. Literature Review

Experts and scholars around the world have produced relevant research and discussion on the disclosure of corporate social responsibility information. Braametal [6] noted that “legality” in corporate social responsibility disclosure is an important consideration for companies in choosing to disclose social responsibility information and also emphasized the role of the regulatory agencies by exploring the relationship between the level and nature of voluntary corporate environmental reporting (CER) practices, multiple corporate environmental performance metrics, and external assurance. The quality of social responsibility information disclosure depends on many aspects. First, the regulator as a supervisor can play an important role in disclosure. For example, a series of mandatory directives issued by the European Union (EU) has played an important role in standardizing the information disclosure of the domestic enterprises of the EU member states [7]. Secondly, the position of corporate managers in the disclosure of social responsibility information cannot be ignored. Fontana et al. [8] examined the documentation of listed firms and pointed out that in many cases, the lack of disclosure information is caused by the lack of relevant awareness of business managers. Grigoris Giannarakis [9] used the least-squares dummy variable model (LSDV) to examine the influence of plausible variables on the ESG disclosure score and its sub-categories and then pointed out that we should pay attention to the disclosure of information and, according to the industry, have a corresponding focus, which provides a basis for us to establish an ESG evaluation system for Chinese power companies. The size of the company [10] and the diversity of the Board of Directors [11] will also affect the quality of the information disclosure of the enterprise to some extent. For investors, the impact of information disclosure depends on the value of information disclosure [12].

Although, the development in the global ESG research field is still at an early stage, both domestic and foreign academics have achieved significant progress. In the research field of ESG valuation and regional studies, Achima et al. analyzed 65 selected companies listed on the Bucharest Stock Exchange (BSE) in Romania between 2011 and 2012. The research team found that the listed companies in Romania score higher in environmental and social aspects than in corporate governance [13]. Auer et al. [14] analyzed companies’ ESG performance and investor relations in the Asia-Pacific region, the United States (US), and Europe and found that in the Asia-Pacific region and the United States, investors can obtain relatively good returns by investing based on ESG performance, while in Europe this strategy tends to be less effective. Sassen et al. [15] studied the correlation between ESG performance and the systematic, specific, and total risks of 8752 listed companies in Europe between 2002 and 2014. The results show that the improvement of environmental performance significantly reduces the company’s risk, while governance performance has no significant influence on the three aforementioned types of risks. Rose et al. [16] analyzed the relationship between the financial performance of Danish companies and corporate governance and found a positive correlation. Sanches Garcia et al. [17] analyzed the relationship between ESG and financial performance in a total of 365 listed companies in sensitive industries in BRICS (Brazil, Russia, India, China, and South Africa) in the Thomson Reuters EikonTM database between 2010 and 2012. Panel data analysis shows that these listed companies in sensitive industries have a better performance in environmental governance, and the correlation between systematic risk and ESG performance of these companies shows an inverted U curve; that is, there is a maximum ESG performance. Chelawat et al. [18] used panel regression to study the correlation between the ESG performance and the financial performance of listed companies in India. Regression results show that companies with good ESG performance can improve financial performance.

Except for the correlation between ESG and the company-related factors mentioned above, experts and scholars have also studied the correlation between ESG and other factors. Duuren et al. [19] found that traditional managers are already considering incorporating ESG evaluation reports into investment due diligence processes, and financial analysts in the market emphasize that corporate governance has a positive effect on a company’s long-term financial performance and return on equity. Al-Tuwaijri et al. [20] comprehensively analyzed environmental information disclosure, environmental performance, and economic performance and concluded that good economic performance is positively correlated with good environmental performance. In addition to the environment, social performance also helps the financial stability of a company [21]. Fatemi et al. [22] studied the impact of ESG on a company’s valuation and discussed the impact of ESG disclosure. The research found that the environmental score was positively correlated with the corporate valuation, and lower scores in the social and governance sectors were correlated with lower valuation of the company, while a higher score had little effect on the valuation of the company. Capelle-Blancard et al. [23] analyzed 33,000 published ESG-related news articles from 2002 to 2010 in Covalence EthicalQuote and found that the market value of companies facing critical events dropped by 0.1%, while positive events had little impact on the company’s market value. Crifo et al. [24] studied the correlation between additional financial aspects of ESG factors and the sovereign bond market. Using panel data of 23 Organization for Economic Co-operation and Development (OECD) countries between 2007 and 2012, the paper shows that good ESG performance reduces government bond yield spread. In addition, corporate social responsibility also helps management to predict corporate financial income levels more accurately [25]. Through the above references, in general, enterprise ESG has a certain degree of influence on corporate financial-related indicators, which leads to the first hypothesis of our research as follows:

Hypothesis 1.

The environmental, social, and corporate governance of large-scale listed power generation companies in China will have a certain degree of impact on corporate financial performance.

For the relevant research on ESG in China, in terms of disclosure and content, Lee et al. [26] adopted data from manufacturing companies listed on the Shanghai and Shenzhen stock exchanges from 2008 to 2012 and found that the state subsidy is a determining factor for a company to decide whether to disclose ESG-related data or not. Dong et al. [27] started with mining companies listed in both stock exchanges mentioned above and emphasized the key role of industry oversight in controlling the quality of corporate responsibility; moreover, returning overseas talents will also help develop Chinese companies’ ESG [28].On the correlation between financial performance and social responsibility, Yin et al. [29] analyzed non-financial A-share listed companies that issued social responsibility reports in 2009 and 2010 and found that current corporate social responsibility has a significant positive impact on the financial performance of the current period. Zhang et al. [30], using system GMM method and empirical analysis of the interaction span effect between corporate social responsibility and financial performance on A-share listed companies in the Shanghai stock exchange from 2007 to 2011, showed that social responsibility from the previous period has a significant positive impact on financial performance on the current period, and current financial performance has a significant positive influence on current social responsibilities. However, Yang [31] and Dou et al. [32] found that the corporate social responsibility of listed companies has no positive effect on financial performance. Through the abovementioned ESG-related references for Chinese companies, combined with the research results of other countries in the world, it can be seen that ESG can have a positive impact on the financial performance of enterprises. Therefore, we assume the following here:

Hypothesis 2.

The environmental, social, and corporate governance of large-scale listed power generation companies in China can contribute to the improvement of corporate financial performance.

This study discusses the criteria and particularity of the ESG-related index in the power generation industry, combs out a series of ESG important indexes, constructs an ESG evaluation system of China’s large power generation listed companies, and further explores the relationship to financial performance through a sample company’s ESG performance level. This provides a reference for the ESG evaluation system of other industries in China and makes up for the vacancy of ESG and financial performance in China’s electric power industry, which has a certain value in the academic field.

3. Research Objectives

The ESG evaluation system, which is suitable for China’s own electric power group enterprises, is constructed by reference to international research and the actual situation in China. The performance level of ESG is determined by the comprehensive evaluation method, and the panel regression method is used to reveal the relationship between the ESG performance and the financial performance of China’s listed power generation corporations, which guides the government, enterprises, and investors to pay attention to the performance of ESG and enables regulators to introduce relevant policies and regulations to help decision makers make relevant investment choices. The objectives of this study are also to promote China’s rapid integration with large international exchanges, lay the foundation for the opening up of financial markets, develop corporate social responsibility standards, gain more international recognition, and reduce barriers to “going out”.

4. Methodology

4.1. Evaluation Methods and Data Sources

4.1.1. Explanation of Evaluation Indicators

A sample description and the establishment of an evaluation indicator system are as follows: Table 1 shows the groups and subordinate companies in the sample. The sample includes China’s five major power generation groups, and all sample companies account for more than half of China’s total installed capacity, so they are representative. Based on the pressure-state-response (PSR) concept model proposed jointly by the OECD and the UNEP from the perspective of coordination between the various business activities of the power generation group and social development [33], building a comprehensive ESG evaluation index system requires a comprehensive ESG assessment of the listed power generation groups at the goal level, the “stress”, “state”, and “response” at the rule level, and a number of specific evaluation indicators that can reflect the ESG performance of the listed power generation groups at the index level. Taking China Resources Power Holdings Company Limited as an example, the construction of an indicator evaluation system is shown in Table 2.

Table 1.

The Groups and Subordinate Companies in the Sample.

Table 2.

The Construction of the Index Evaluation System from China Resources Power Holdings Company Limited in 2016.

The determination of the standard value of the indicators is as follows: After the evaluation of the listed power generation company’s ESG, the actual values need to be compared with their standard values before they can be normalized or standardized. The actual values refer to the social responsibility reports disclosed by the power generation group companies in the year or the ESG report. The determination of the standard values of each indicator by referring to internationally recognized values and world averages, by consulting the experts in the field, or by adopting the average values of the indicators of each power generation group company during the research period. Taking China Resources Power Holdings Company Limited as an example, the distribution results of the indicator weights are shown in Table 2.

The determination of index weights is as follows: According to the relevant references and experts’ recommendations, the environment (E) has a significant impact on the financial performance of power companies. The investment in environmental aspects of power companies not only involves the surrounding environmental protection but also includes the improvement of the emission reduction performance of their own equipment and the transformation investment. With the improvement of relevant environmental laws and regulations and the strengthening of law enforcement, violations of power companies in this area will also affect the financial performance of enterprises. Social (S) indicators are mostly related to the enterprise system, which will directly affect the efficiency of enterprises, thus affecting financial performance. The impact of the corporate governance (G)-related indicators on the company’s financial performance has no significant environmental and social impacts, and the disclosure of information on corporate governance is limited, which limits the selection and governance of the indicators to some extent. To obtain the financial impact, therefore, of the environmental, social, and governance aspects, we will divide the weight by 6:3:1. In the weight ratio of the secondary and tertiary indicators, due to the wide coverage of various indicators, there is a lack of consensus in the opinions regarding weights allocation and relevant references, so this paper uses a combination of analytic hierarchy process (AHP) and ESG research literature to obtain index weights. It provides simple decision-making ideas for complex decision-making problems with multiple objectives, multiple criteria, or no-structure characteristics and can effectively analyze qualitative and quantitative indicators to analyze problems. Taking China Resources Power Holdings Company Limited as an example, the distribution results of the indicator weights are shown in Table 3.

Table 3.

China Resources Power Holdings Company Limited 2016 Index Evaluation.

The construction of a comprehensive measurement model is as follows: ESG evaluation indicators have a wide range and are complex and diverse. There are both positive and negative indicators and both quantitative and qualitative indicators. In order to unify various indicators with different meanings that are not comparable, it is necessary to non-dimensionalize various indicators. This paper uses the following non-dimensionalized model to calculate the sustainability index of each evaluation index. In the case of China Resources Power Holdings Company Limited, the non-dimensionalized results of the indicators are shown in Table 3.

4.1.2. Method of Data Processing

- (1)

- StandardizationPositive indicator:Negative indicator:where xi is the actual value of the ith index; yi is the standard value of the evaluation index; and p(xi) is the sustainability index of the evaluation index.

- (2)

- Comprehensive evaluationThe comprehensive evaluation index formula of the weighted summation is as follows:where E is the sustainability comprehensive evaluation index; Wi is the weight corresponding to each factor; and p(xi) is the sustainability index of the evaluation index.

Generally speaking, as part of the report, the listed companies’ corporate and social responsibility (CSR) reports or environmental, social, and governance report will list economic performance individually. This provides us with a method of selecting financial performance indicators that are comparable to those of ESG. The disclosed economic performance indicators include return on invested capital (ROIC), return on capital employed (ROCE), return on equity (ROE), return on asset (ROA), return on net assets (RONA), and so on. This article will measure the financial performance of a company based on accounting indicators—we choose ROCE as a financial performance indicator. The ROCE indicators of each corporate group in this article are sourced from the CSMAR.

4.2. Panel Regression Model

The main tools applied for data analysis are as follows:

The Levin–Lin–Chu (LLC) test—also known as the unit root test—was proposed by Levin, Lin, and Chu. This test checks the stationarity of the data and avoids spurious correlation to ensure the validity of the regression. It examines the existence of unit root in the panel data and is carried out before the regression.

The co-integration test was carried out to test whether there is a stable long-term correlation among the variables in the model. Under the circumstances, those independent variables and the dependent variables are on the same order in the unit root test.

Panel data here is a panel data set that contains both cross-sectional and time series data. Strictly speaking, it refers to a series of individuals (such as residents, countries, companies, etc.) that is continuously observed data obtained during a time frame.

Panel data could well solve the problem of the missing variables. The omitted variable bias is a common problem. Missing variables are often caused by unsolvable individual differences or “heterogeneity”. If this individual difference is “time-invariant”, the panel data, therefore, provides a tool to solve for missing variables. Because the panel data has both the cross-sectional and the time series dimensions, to some extent, it can solve the problem that cannot be solved by cross-section data or time series data separately; in addition, due to the cross-section dimension and the time dimension, the sample size of the panel data is usually larger. This can improve the accuracy of the evaluation.

There are three main methods for modeling panel data: fixed effect regression model (Fe); random effect regression model (Re), and mixed regression model (Me). The equation of the panel data regression model can be written as follows:

where Yit is the dependent variable, i and t respectively represent the dimension of the section and the time dimension, Xit represents the observed dependent variable of the i-th dimension in the t-th time period, the uit is the error term, the α is a scalar constant, and the β is the regression coefficient vector.

Fixed effect model (Fe)—for a particular individual i, it means that the factors that do not change with time, such as individual consumption habits, state social system, regional characteristics, gender, etc., we generally call it “individual effect”. If the “individual effect” is treated as a fixed factor that does not change over time, the corresponding model is called the “fixed effect” model. The fixed effect regression model is:

where i = 1, 2, ..., n; t = 1, 2, ..., T; X1 indicates the value of the first regression variable for individual i in period t; and X2 indicates the value of the second regression variable, and so on. α1, α2, …, αn are the intercepts for a particular individual.

The intercept of the random effect model (Re) is different from that of the fixed effect model. In the fixed effect model, αi is used as an explanatory variable to indicate the individual effect of the model. In the random effect model, the random error term is divided into two parts, one part is the error term αi that does not change with time, and the other part is the error term uit that changes with time as follows:

where,

The fixed effect model eliminates variables that do not change with time by using group dispersion method. This ensures the unbiasedness of the model, yet the model cannot estimate the impact of variables that do not change with time. This can be implemented in the random effect model.

The Hausman test is one of the tools to judge whether to select a fixed effect model or a random effect model for panel data. If Cov(αi,Xit) = 0, Re is more efficient. If Cov(αi,Xit) ≠ 0, Re is biased. In other words, if the null hypothesis, Cov(αi,Xit) = 0, is true, then the random effect model should be adopted, and if the null hypothesis is not true, then the fixed effect model should be adopted.

The White test is a common method for testing heteroskedasticity. This test method does not need to make any assumptions about the nature of the heteroskedasticity.

The model is as follows:

if,

Namely, for different sample points, the variances of the error terms are not constant, and they are different from each other; therefore, it is assumed that there is heteroskedasticity in the model. The heteroskedasticity will invalidate the model prediction.

If there is heteroskedasticity in the model, then new estimation models need to be used. The most common method is the weighted least-squares (WLS) method. The weighted least-squares method weights the original model to correct for heteroskedasticity in the new model and then uses an ordinary least-squares method to estimate its parameters.

4.3. Variables Explanation

The variables for analyzing are described below:

Return on capital employed (ROCE) is the ratio of earnings before interest and tax (EBIT) to the total capital employed by the company. It is one of the more commonly used indicators to measure corporate financial performance. ROCE eliminates the interference of tax rates in measuring corporate financial performance so that the horizontal comparisons between different companies can be conducted more equitably. As a dependent variable in the regression model, it is used as a financial performance indicator based on accounting indicators to assess the impact of ESG factors on financial performance.

Environmental, social, and governance performance of the company was used as an independent variable of the regression model to study its impact on financial performance. ESG performance builds index evaluation framework through the PSR-AHP index classification method and weight distribution, and they are all obtained nondimensionalized. The actual number of each listed company comes from the social responsibility report or environmental, social, and governance report disclosed each year.

The debt-to-equity ratio (D/E) reflects the company’s capital structure and the company’s default risk dimension. It is considered to be one of the key factors in the company’s financial performance. Because the debt-to-equity ratio of a company with good financial performance remains within a reasonable level, it is usually negatively correlated with financial performance. It is used as a control variable in the regression model in this study.

Size is another important factor in corporate financial performance. It can be measured in terms of assets or total sales. In the paper, the logarithm of total assets (Log TA) is used to represent the size of the company, which is used as a controllable variable in the regression model.

4.4. Empirical Analysis

In order to assess the impact of corporate ESG performance on financial performance, this paper uses ROCE to estimate regression models and measure corporate financial performance. The panel data for the study are from 20 large listed power generation companies in China, each of which includes observations for 10 years. Because many entities in the dataset have missing values and do not have the same number of observations, the dataset is unbalanced. The panel data must first be tested before proceeding to the panel regression analysis.

4.4.1. Tests for Data

Before the panel regression analysis, the Levin–Lin–Chu method is used to test the stationarity of the test data. The results of the LLC test are listed in Table 4. The results show that the null hypothesis of the presentation unit root can be rejected. Therefore, the dataset can be considered as stationary. Table 5 shows the co-integration test results. The p-value is less than the corresponding significance level, indicating that the variables are co-integrated. Table 6 lists the correlation matrix that contains all the variables. Because the correlations among the independent variables are not significant, we do not have to consider the problem of multicollinearity. However, using only the correlation matrix, the relationship between the company’s financial performance and the regression variables cannot be explained. Therefore, we must return to the panel regression results in order to explore the relationship between them.

Table 4.

Test Results of the Stationarity of the Panel Data.

Table 5.

Test Results of Co-Integration.

Table 6.

Correlation Matrix.

This article uses the Hausman test to determine whether to use a fixed effect model or a random effect model. The null hypothesis of Hausman’s test assumes that the generalized least-squares (GLS) estimation is consistent, which means that the random effect model should be preferred. The alternative hypothesis assumes that the GLS estimation is inconsistent, so the fixed effect model is a more suitable model. Table 7 shows the Hausman test results for the dependent variable ROCE regression model. The Hausman test results show that in those two models, the p-value is not significant at the 5% level. Therefore, the null hypothesis cannot be rejected, which means that the random effect model is the preferred model.

Table 7.

Test Results of the Hausman Test.

4.4.2. Panel Data Regression in the Random Effect Model

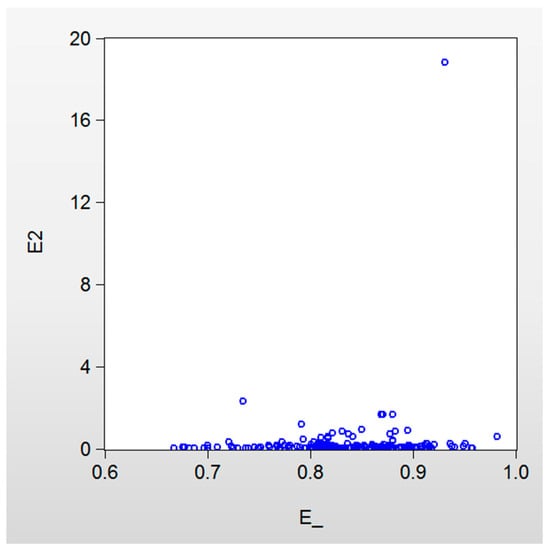

Table 8 shows the results of the panel regression of the random effects model for the dependent variable ROCE. The estimated coefficients, t-statistics, and p-values can be seen in the table. In this paper, we applied heteroskedasticity tests on the regression results and drew a scatter plot. It is shown that the scatter plot of the residual square term e2 against the explanatory variable ESG is mainly distributed at the bottom of Figure 1, which describes a marginal trend that residual square term e2 increases with the change of the ESG. Therefore, the model is likely to have heteroskedasticity, but whether or not heteroskedasticity does exist remains to be proven in further tests.

Table 8.

Panel Regression of the Random Effects Model for the Dependent Variable ROCE.

Figure 1.

Scatterplot of the Correlation Between e2 and ESG.

4.4.3. White Test

In this paper, the White test is carried out separately in the cases with cross product items and no cross product items. Table 9 shows that in the case with cross product items, the White’s statistic is nR2 = 187 × 0.241625 = 45.18, according to the χ2 distribution at a 5% significance level, and the critical value of the χ2 distribution with a degree of freedom of 5 is χ20.05 = 11.07. Because nR2 = 45.18 > χ20.05 = 11.07, the null hypothesis of homoskedasticity is rejected, indicating that heteroskedasticity exists. Under the condition with no cross product items (Table 10), White’s statistic is nR2 = 187 × 0.105907 = 19.8, under the 5% significance level, and the null hypothesis of homoskedasticity is still rejected, indicating that the model does have heteroskedasticity. In order to correct for heteroskedasticity, the WLS model is used in this study (Table 11). In this model, the weight of each value of the independent variables is inversely proportional to the error variance.

Table 9.

White Test with Cross Product Items.

Table 10.

White Test with No Cross Product Items.

Table 11.

Weighted Least-Squares (WLS) Regression for ROCE.

In order to achieve a better goodness of fit of the model, the difference between the predictions and the observations (i.e., the standard error) must be controlled within a reasonable range of values. It is generally believed that the smaller the standard error values, the closer the observations to the regression line, which means that the prediction is more accurate. A good model should have a significant and large F-statistic (the F-statistic is at least greater than 1). The R2 indicates the degree of explanatory value of the independent variable by the dependent variable, and the individual coefficients show the degree to which all the independent variables can explain the dependent variables. From the model output, it can be seen that the standard error after regression using WLS is small (0.000674), the F statistic is large and significant (11609.11), and R2 indicates that the independent variables can explain 99% of the changes of the dependent variable. In addition, the output shows that the standard error based on the original data is 0.089621; meanwhile, the standard error based on the WLS model is reduced to 0.000674. The decrease of the standard error indicates a significant improvement in the goodness of fit.

With impacts of other predictor values remaining the same, the individual coefficient values show how much each independent variable contributes to the dependent variables. Combining coefficient columns with p-values, we can see that the ESG coefficient is positive and is significant. The Log TA coefficient is negative, it contributes more to financial performance than does the DE coefficient, and the negative effect of the DE coefficient on the model is small. The abovementioned correlation between the independent variable and the dependent variable can be explained by the following equation:

From Table 12, we can see that the White’s statistic is nR2 = 187 × 0.030183 = 5.644, which is less than the critical value of χ20.05 = 12.59, under the 5% significance level and with the corresponding degree of freedom of 6, which does not reject the null hypothesis of homoskedasticity. Therefore, this model is very suitable for this group of panel data.

Table 12.

White Test after WLS.

5. Research Conclusions and Policy Implications

5.1. Research Conclusions and Academic Contribution

The conclusions of the study confirm the two aforementioned hypotheses that the ESG performance of large listed power generation companies has an impact on financial performance and that the impact is positive. The results of the equations above are basically in accordance with the research conducted by Chelawat et al. [18] on India. Regardless of whether in China or India, ESG performance contributes positively to financial performance. The reason why China is more prominent than India may be related to China’s earlier realization of the importance of ESG construction. In addition, the supervisory standards and enforcement of the supervisory authority will also affect the contribution of the two countries’ ESG indicators. From the perspective of developed countries, Sidhoum et al. [34] used the copula method to explore the correlation between the ESG performance of the US electric power company and its financial performance. The results are inconsistent with the conclusions of this study. All of the above suggests that strengthening the construction of corporate social responsibility standards will have a long-term and outstanding contribution to a company’s financial performance. As for the influence of the scale of the electrical power group on financial performance, Li et al. [35] explored the economies of scale of fire-powered electric power plants in China from 2003 to 2010 based on China’s actual condition using panel data and a translog cost model and found that the power generation plants’ economies of scale reduce with the increase of the scale of the power plants. The minimum efficient scale (MES) of power plants are declining year by year. While the research scope of this paper is from 2007 to 2016, according to the results of Li et al., it can be predicted that the economies of scale will further reduce. This conclusion is also consistent with the results of this article. From an international perspective, Angel et al. [36] studied the economies of scale for Spanish power generation companies and found that the economies of scale for Spanish power generation companies, which are supposed to be more developed than China’s, did not exist anymore at the end of the last century. The economic boost basically relies on the improvement of management and technical aspects.

With respect to academic value, this research creates a new ESG comprehensive evaluation system based on China’s large power generation listed companies, which provides important references for the disclosure of social responsibility information and the guidance of supervisors in the power industry. In the evaluation method, we extend the traditional qualitative description of social responsibility to more intuitive quantitative analysis. The conclusion of the study on scoring has laid a foundation for other related studies in the future. In addition, the study compensates for the gap between China’s ESG and financial performance correlation analysis and confirms the important contributions of ESG to the financial performance measurement index—ROCE. Thus, improving ESG can improve the corresponding financial performance, and excellent ESG performance can achieve excellence in the power generation industry. The financial results of this study have also produced good insights for emerging economies, such as that of China.

5.2. Conclusions and Implications

The research results in this article show that under the current market conditions, China’s large listed power generation group can improve their financial performance through good ESG performance. This can be confirmed by the financial performance indicator—ROCE. The results of this study have practical implications for investors, company management, and decisionmakers, as well as industry regulators.

This article will enable investors to pay more attention to the company’s ESG performance when making investment decisions. For example, investors can determine a company’s enterprise value and risk and select companies with investment potential by interpreting the company’s ESG report; meanwhile, companies will also focus on ESG improvement through the urging of their investors. Taking the US S&P 500 index as an example, from 2011 to 2015, the number of companies that released responsibility reports has increased from 20% to 81% [37]. The sharp increases in corporate sustainability disclosures have come from major customers’ requests for such information disclosure.

For a company’s management and decisionmakers, it is necessary to shift the focus from profit maximizing to corporate social responsibility in order to achieve a long-term profitability goal. This will help to improve the company’s societal impact and public relations and achieve long-term sustainable and healthy development of the company. The improvement of ESG performance also helps China’s listed power generation companies gain international recognition and remove unnecessary obstacles for “going out”.

For industry regulators, companies that pay attention to ESG development will help stabilize and stimulate the sustainable development of the capital market. An MSCI study showed that the S&P 500′s ESG index has a higher long-term return and lower volatility than the S&P 500 index [38]. This shows that the mandatory disclosure of ESG information can balance the interests between companies and external stakeholders, which benefit the stable development of the capital market.

5.3. Policy Proposal

Regulators must implement the principle of “Comply or Explain” in a corporate disclosure statement. Due to companies’ differences in business scale and industry-specific and corporate management experience, not all issuers can reach the same depth of information disclosure within the same time period. In the electric power industry, the companies’ sizes and the degree of ESG information collection and disclosures vary. Strictly following the principle of “Comply or Explain” will improve the level of disclosure.

China has not been successful in establishing an index system to evaluate listed companies’ ESGs. Compared with foreign ESG disclosures, China’s ESG disclosure system lacks standards. Most companies have released ESG reports, yet the quality of the reports has been uneven, and it is difficult to make industry-wide comparisons. The levels of disclosure on sensitive projects are not deep enough, the data are not clear enough, the scopes are not wide enough, and the problem of “great emphasis on quantity, little focus on quality” is prominent. All of these lower the value added by the ESG reports. It is recommended that stock exchanges and the relevant departments in charge of bonds approval and registration specify regulations and clarify the expected contents and templates for the disclosures. For key information, especially the major pollution emission indicators, disclosures should be significant and frequent. In this regard, EU standards should be used for reference: due to environmental and social externalities, the decision to disclose information should be based on environmental and social impacts rather than on financial criteria.

The agencies that provide environmental information analysis should be supported and developed to strengthen the evaluation, supervision, guidance, and incitation of corporate environmental information disclosure. Support from third-party consulting agencies to provide environmental information assessment and prepare environmental responsibility reports for some listed companies and debt-issuing companies should also be encouraged.

For regulators, it is necessary to strengthen the supervision and enforcement of environmental information disclosures. Stock exchanges should punish companies that are in violation of environmental information disclosure requirements via public denunciation. The environmental protection department should also consider similar methods to punish such behavior. It should provide supportive policies to companies with good ESG assessments, such as incentives in the areas of tendering, procurement, tax deductions, and so on, as well as facilitate the IPO process, refinancing, green credit, and so forth.

Author Contributions

J.Y. designed the research framework; Y.G. conducted the analysis and drafted the paper; and C.Z. gave a lot of practical recommendations for the construction of the index system. M.W. and D.L. made contributions in data collection and writing material; Y.Z. and J.K. analyzed the data and completed the paper in English.

Funding

This research was funded by the National Natural Science Foundation of China (71673085), the Fundamental Research Funds for the Central Universities (2018ZD14), the Beijing Social Science Fund (16YJB027) and the 111 Project (B18021). The authors also appreciate the funding by the Energy Foundation to support the work reported in this paper. The usual caveats apply.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Yuan, J.; Xu, Y.; Hu, Z.; Zhao, C.; Xiong, M.; Guo, J. Peak energy consumption and CO2 emissions in China. Energy Policy 2014, 68, 508–523. [Google Scholar] [CrossRef]

- Yuan, J.; Li, P.; Wang, Y.; Liu, Q.; Shen, X.; Zhang, K.; Dong, L. Coal power overcapacity and investment bubble in China during 2015–2020. Energy Policy 2016, 97, 136–144. [Google Scholar] [CrossRef]

- Hao, C.; Zhang, W.; Wang, Y.; Liu, Q.; Guo, J.; Xiong, M.; Yuan, J. The economics of coal power generation in China. Energy Policy 2017, 105, 1–9. [Google Scholar]

- Taiwanese Investors Pay Attention to the Global Ranking of Corporate Social Responsibility. 12 December 2016. Available online: http://www.chinatimes.com/cn/realtimenews/20161212002862-260410 (accessed on 23 July 2018).

- Listed Company ESG Disclosure Requirements around the World. 29 December 2015. Available online: http://www.syntaogf.com/Menu_Page_CN.asp?ID=21&Page_ID=167 (accessed on 23 July 2018).

- Braam, G.J.; de Weerd, L.U.; Hauck, M.; Huijbregts, M.A. Determinants of corporate environmental reporting: The importance of environmental performance and assurance. J. Clean. Prod. 2016, 129, 724–734. [Google Scholar] [CrossRef]

- Camilleri, M.A. Environmental, social and governance disclosures in Europe. Sustain. Account. Manag. Policy J. 2015, 6, 224–242. [Google Scholar] [CrossRef]

- Fontana, S.; D’Amico, E.; Coluccia, D.; Solimene, S. Does environmental performance affect companies’ environmental disclosure? Meas. Bus. Excell. 2015, 19, 42–57. [Google Scholar] [CrossRef]

- Giannarakis, G.; Konteos, G.; Sariannidis, N. Financial, Governance and Environmental determinants of Corporate Social Responsible Disclosure. Manag. Decis. 2014, 52, 1928–1951. [Google Scholar] [CrossRef]

- Wirth, H.; Kulczycka, J.; Hausner, J.; Koński, M. Corporate Social Responsibility: Communication about social and environmental disclosure by large and small copper mining companies. Resour. Policy 2016, 49, 53–60. [Google Scholar] [CrossRef]

- Hoang, T.C.; Abeysekera, I.; Ma, S. Board Diversity and Corporate Social Disclosure: Evidence from Vietnam. J. Bus. Ethics 2016. [Google Scholar] [CrossRef]

- Cho, C.H.; Michelon, G.; Patten, D.M.; Roberts, R.W. CSR Disclosure: The more things change …? Account. Audit. Account. J. 2015, 28, 14–35. [Google Scholar] [CrossRef]

- Achim, M.V.; Borlea, S.N. Developing of ESG Score to Assess the Non-financial Performances in Romanian Companies. Procedia Econ. Financ. 2015, 32, 1209–1224. [Google Scholar] [CrossRef]

- Auer, B.R.; Schuhmacher, F. Do socially (ir)responsible investments pay? New evidence from international ESG data. Q. Rev. Econ. Financ. 2016, 59, 51–62. [Google Scholar] [CrossRef]

- Sassen, R.; Hinze, A.K.; Hardeck, I. Impact of ESG factors on firm risk in Europe. J. Bus. Econ. 2016, 86, 867–904. [Google Scholar] [CrossRef]

- Rose, C. Firm performance and comply or explain disclosure in corporate governance. Eur. Manag. J. 2016, 34, 202–222. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R.J. Orsato.Sensitive industries produce better ESG performance: Evidence from emerging markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Chelawat, H.; Trivedi, I.V. The business value of ESG performance: The Indian context. Asian J. Bus. Ethics 2016, 5, 195–210. [Google Scholar] [CrossRef]

- Van Duuren, E.; Plantinga, A.; Scholtens, B. ESG Integration and the Investment Management Process: Fundamental Investing Reinvented. J. Bus. Ethics 2016, 138, 525–533. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K.E., II. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–472. [Google Scholar] [CrossRef]

- Bouslah, K.; Kryzanowski, L.; M’Zali, B. Social Performance and Firm Risk: Impact of the Financial Crisis. J. Bus. Ethics 2018, 149, 643–669. [Google Scholar] [CrossRef]

- Fatemi, A.; Glaum, M.; Kaiser, S. ESG performance and firm value: The moderating role of disclosure. Glob. Financ. J. 2017. [Google Scholar] [CrossRef]

- Capelle-Blancard, G.; Petit, A. Every Little Helps? ESG News and Stock Market Reaction. J. Bus. Ethics 2017. [Google Scholar] [CrossRef]

- Crifo, P.; Diaye, M.A.; Oueghlissi, R. The effect of countries’ ESG ratings on their sovereign borrowing costs. Q. Rev. Econ. Financ. 2017, 66, 13–20. [Google Scholar] [CrossRef]

- Lee, D. Corporate Social Responsibility and Management Forecast Accuracy. J. Bus. Ethics 2017, 140, 353–367. [Google Scholar] [CrossRef]

- Lee, E.; Walker, M.; Zeng, C.C. Do Chinese state subsidies affect voluntary corporate social responsibility disclosure? J. Account. Public Policy 2017, 36, 179–200. [Google Scholar] [CrossRef]

- Dong, S.; Xu, L. The impact of explicit CSR regulation: Evidence from China’s mining firms. J. Appl. Account. Res. 2016, 17, 237–258. [Google Scholar] [CrossRef]

- Wen, W.; Song, J. Can returnee managers promote CSR performance? Evidence from China. Front. Bus. Res. China 2017, 11, 12. [Google Scholar] [CrossRef]

- Yin, K.-G.; Liu, X.-Q.; Chen, H.-D. Study on the Relationship between Corporate Social Responsibility and Financial Performance from the Endogenous Perspective Evidence from Chinese Listed Companies. China Soft Sci. 2014, 6, 98–108. [Google Scholar]

- Zhang, Z.; Jin, X.; Li, G. An Empirical Study on the Interactive and Inter-temporal Influence between Corporate Social Responsibility and Corporate Financial Performance. Account. Res. 2013, 8, 32–39. [Google Scholar]

- Yang, W.; Yang, S. An Empirical Study on the Relationship between Corporate Social Responsibility and Financial Performance under the Chinese Contest—Based on the Contrastive Analysis of Large, Small and Medium-size Listed Companies. Chin. J. Manag. Sci. 2016, 24, 143–150. [Google Scholar]

- Dou, X. The Lagging Effects of the Influence of Corporate Social Responsibility on Corporate Financial Performance—Empirical Analysis Based on the Panel Data of Chinese Listed Companies. Ind. Econ. Res. 2015, 3, 74–81. [Google Scholar]

- Tong, C. Review on environmental indicator research. Res. Environ. Sci. 2000, 13, 53–55. [Google Scholar]

- Sidhoum, A.A.; Serra, T. Corporate social responsibility and dimensions of performance: An application to U.S. electric utilities. Util. Policy 2017, 48, 1–11. [Google Scholar] [CrossRef]

- Li, T.; Zhang, G. Does Competition Damage Scale Economies of Generation Side? Evidence on Thermal Power Plants. Financ. Trade Res. 2012, 23, 58–66. [Google Scholar]

- Arcos, A.; De Toledo, P.A. An analysis of the Spanish electrical utility industry: Economies of scale, technological progress and efficiency. Energy Econ. 2009, 31, 473–481. [Google Scholar] [CrossRef]

- Governance & Accountability Institute (“G&A Institute”).

- Ma, X.; Wang, J.; Qin, E. Listed company’s ESG information disclosure system. China Financ. 2016, 16, 33–34. [Google Scholar]

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).