Evaluation of Sustainability Practices in Small and Medium-Sized Manufacturing Enterprises in Southern Brazil

, and

, and

Abstract

1. Introduction

2. Materials and Methods

3. Findings and Results

4. Final Remarks

Author Contributions

Funding

Conflicts of Interest

References

- Cazeri, G.T.; Anholon, R.; da Silva, D.; Ordoñez, R.E.C.; Quelhas, O.L.G.; Leal Filho, W.; de Santa-Eulalia, L.A. An assessment of the integration between corporate social responsibility practices and management systems in Brazil aiming at sustainability in enterprises. J. Clean. Prod. 2018, 182, 746–754. [Google Scholar] [CrossRef]

- Faller, C.M.; Zu Knyphausen, A.D. Does equity ownership matter for corporate social responsibility? A literature review of theories and recent empirical findings. J. Bus. Eth. 2018, 150, 15–40. [Google Scholar] [CrossRef]

- Bansal, P. Envolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- Gladwin, T.N.; Kennelly, J.J.; Krause, T.S. Shifting paradigms for sustainable development: Implications for management theory and research. Acad. Manag. Rev. 1995, 20, 874–907. [Google Scholar] [CrossRef]

- Sachs, I. Transition Strategies for the 21st Century: Development and Environment; Studio Nobel and Foundation for Administrative Development: São Paulo, Brazil, 1993. [Google Scholar]

- Anser, M.; Zhang, Z.; Kanwal, L. Moderating effect of innovation on corporate social responsibility and firm performance in realm of sustainable development. Wiley Corp. Soc. Responsib. Environ. Manag. 2018, 1–24. [Google Scholar] [CrossRef]

- Ashley, P.A. Ethics and Social Responsibility in Business; Saraiva: São Paulo, Brazil, 2002; Volume 153. [Google Scholar]

- Tinoco, J.E. Social Balance: An Approach to Transparency and Public Accountability of Organizations; Atlas: São Paulo, Brazil, 2006. [Google Scholar]

- Anholon, R.; Quelhas, O.L.G.; Leal Filho, W.; de Souza Pinto, J.; Feher, A. Assessing corporate social Responsibility concepts used by a Brazilian manufacturer of airplanes: A case study at Embraer. J. Clean. Prod. 2016, 135, 740–749. [Google Scholar] [CrossRef]

- Zylbersztajn, D.; Lins, C. Sustainability and Value Generation; Editora Campus: Rio de Janeiro, Brasil, 2010. [Google Scholar]

- Milne, M.J.; Gray, R.W. Whither ecology? The triple bottom line, the global reporting initiative, and corporate sustainability reporting. J. Bus. Eth. 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Reverte, C.; Gómez-Melero, E.; Cegarra-Navarro, J.G. The influence of corporate social responsibility practices on organizational performance: Evidence from eco-responsible Spanish firms. J. Clean. Prod. 2016, 112, 2870–2884. [Google Scholar] [CrossRef]

- El Baz, J.; Laguir, I.; Marais, M.; Staglianò, R. Influence of national institutions on the corporate social responsibility practices of small- and medium-sized enterprises in the food-processing industry: Differences between France and Morocco. J. Bus. Eth. 2016, 134, 117–133. [Google Scholar] [CrossRef]

- Lee, L.; Chen, L. Boosting employee retention through CSR: A configurationally analysis. Corp. Soc. Responsib. Environ. Manag. 2018, 20, 874–907. [Google Scholar] [CrossRef]

- Vilke, R. Corporate social responsibility as innovation: Recent developments in Lithuania. Econ. Bus. 2014, 26, 119–125. [Google Scholar] [CrossRef]

- Agyemang, O.S.; Ansong, A. Corporate social responsibility and firm performance of Ghanaian SMEs: Mediating role of access to capital and firm reputation. J. Glob. Responsib. 2017, 8, 47–62. [Google Scholar] [CrossRef]

- Hahn, R. ISO 26000 and the standardization of strategic management processes for sustainability and corporate social responsibility. Bus. Strategy Environ. 2013, 22, 442–455. [Google Scholar] [CrossRef]

- Madzik, P.; Budaj, P.; Chocholáková, A. Practical experiences with the application of corporate social responsibility principles in a higher education environment. Sustainability 2018, 10, 1736. [Google Scholar] [CrossRef]

- Arruda, L.R.; De Jesus Lameira, V.; Quelhas, O.L.G.; Pereira, F.N. Sustainability in the Brazilian heavy construction industry: An analysis of organizational practices. Sustainability 2013, 5, 4312–4328. [Google Scholar] [CrossRef]

- Batista, A.A.D.S.; Francisco, A.C.D. Organizational sustainability practices: A study of the firms listed by the corporate sustainability index. Sustainability 2018, 10, 226. [Google Scholar] [CrossRef]

- Lalangui, P.S.; Garcia, J.A.; Rio-Rama, M.C. Sustainable practices in small and medium-sized enterprises in Ecuador. Sustainability 2018, 10, 2105. [Google Scholar] [CrossRef]

- Aguado, E.; Holl, A. Differences of corporate environmental responsibility in small and medium enterprises: Spain and Norway. Sustainability 2018, 10, 1877. [Google Scholar] [CrossRef]

- Fethallah, W.; Chraibi, L. SMI’s and CSR: A new approach for measuring social responsibility performance. Index Res. Gate 2017, 22, 115–128. [Google Scholar]

- Hosoda, M. Management control systems and corporate social responsibility: Perspectives from a Japanese small company. Int. J. Bus. Soc. 2018, 18, 68–80. [Google Scholar] [CrossRef]

- Lun-Thomsen, P.; Lindgreen, A.; Vanhamme, J. Industrial clusters and corporate social responsibility in developing countries: What we know, what we do not know, and what we need to know. J. Bus. Eth. 2016, 133, 9–24. [Google Scholar] [CrossRef]

- Pantani, D.; Peltzer, R.; Cremonte, M.; Robaina, K.; Babor, T.; Pinsky, I. The marketing potential of corporate social responsibility activities: The case of the alcohol industry in Latin America and the Caribbean. Addiction 2017, 112, 74–80. [Google Scholar] [CrossRef] [PubMed]

- Choi, J.H.; Kim, S.; Yang, D.H. Small and medium enterprises and the relation between social performance and financial performance: Empirical evidence from Korea. Sustainability 2018, 10, 1816. [Google Scholar] [CrossRef]

- Martinez-Conesa, I.; Soto-Acosta, P.; Palacios-Manzano, M. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. J. Clean. Prod. 2017, 142, 2374–2383. [Google Scholar] [CrossRef]

- Chun, H.M.; Shin, S.Y. The impact of labor union influence on corporate social responsibility. Sustainability 2018, 10, 1922. [Google Scholar] [CrossRef]

- Dey, P.K.; Petridis, N.E.; Petridis, K.; Malesios, C.; Nixon, J.D.; Ghosh, S.K. Environmental management and corporate social responsibility practices of small and medium-sized enterprises. J. Clean. Prod. 2018, 195, 687–702. [Google Scholar] [CrossRef]

- Voss, C.; Tsikriktsis, N.; Frohlich, M. Case research in operations management. Int. J. Op. Prod. Manag. 2002, 22, 195–219. [Google Scholar] [CrossRef]

- Brazilian Service to Support Micro and Small Enterprises. Available online: http://www.sebrae.com.br/sites/PortalSebrae/estudos_pesquisas/quem-sao-os-pequenos-negociosdestaque5,7f4613074c0a3410VgnVCM1000003b74010aRCRD (accessed on 2 May 2018).

- Ethos Institute of Companies and Social Responsibility. Ethos Indicators of Corporate Social Responsibility. 2018. Available online: https://www3.ethos.org.br/conteudo/indicadores (accessed on 1 April 2018).

- Ethos Institute of Companies and Social Responsibility. Self-Assessment Tool and Planning: Ethos-SEBRAE Indicators of Corporate Social Responsibility for Micro and Small Companies. 2018. Available online: https://www3.ethos.org.br/conteudo/indicadores-ethos-publicacoes (accessed on 1 April 2018).

- Fischer, T.M.; Sawczyn, A.A. The relationship between corporate social performance and corporate financial performance and the role of innovation: Evidence from German listed firms. J. Manag. Control 2013, 24, 27–52. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.B. Strategic corporate social responsibility and value creation. Manag. Int. Rev. 2009, 49, 781–793. [Google Scholar] [CrossRef]

- Rodriguez, F.M. Social responsibility and financial performance: The role of good corporate governance. BRQ Bus. Res. Q. 2016, 19, 137–151. [Google Scholar] [CrossRef]

- Levick, R. Corporate Social Responsibility for Profit. Available online: https://www.forbes.com/sites/richardlevick/2012/01/11/corporate-social-responsibility-for-profit (accessed on 18 April 2018).

- Moore, S.B.; Manring, S.L. Strategy development in small and medium sized enterprises for sustainability and increased value creation. J. Clean. Prod. 2009, 17, 276–282. [Google Scholar] [CrossRef]

- Fernández-Guadaño, J.; Sarria-Pedroza, J.H. Impact of corporate social responsibility on value creation from a stakeholder perspective. Sustainability 2018, 10, 1352. [Google Scholar] [CrossRef]

- Elgammal, W.; El-Kassar, A.N.; Canaan Messarra, L. Corporate ethics, governance and social responsibility in MENA countries. Manag. Decis. 2018, 56, 273–291. [Google Scholar] [CrossRef]

- Lee, S.; Yoon, J. Does the authenticity of corporate social responsibility affect employee commitment? Soc. Behav. Personal. Int. J. 2018, 46, 617–632. [Google Scholar] [CrossRef]

- Martínez-Marínez, D.; Herrera Madueno, J.; Larran Jorge, M.; Lechuga Sancho, M.P. The strategic nature of corporate social responsibility in SMEs: A multiple mediator analysis. Ind. Manag. Data Syst. 2017, 117, 2–31. [Google Scholar] [CrossRef]

{kind=link}

| Enterprises | Annual Gross Revenue | Number of Employees | Company Years |

|---|---|---|---|

| E1 | US$302,113.00 | 68 | 27 |

| E2 | US$928,543.00 | 109 | 22 |

| E3 | US$780,101.00 | 100 | 18 |

| E4 | US$401,021.00 | 74 | 20 |

| E5 | US$498,011.00 | 76 | 25 |

| E6 | US$562,629.00 | 88 | 10 |

| E7 | US$813,000.00 | 95 | 25 |

| E8 | US$488,921.00 | 77 | 29 |

| E9 | US$397,026.00 | 70 | 11 |

| E10 | US$765,917.00 | 90 | 10 |

| E11 | US$389,012.00 | 71 | 20 |

| E12 | US$503,842.00 | 85 | 14 |

| E13 | US$345,099.00 | 70 | 17 |

| E14 | US$651,946.00 | 86 | 16 |

| E15 | US$787,009.00 | 93 | 7 |

| E16 | US$381,134.00 | 69 | 15 |

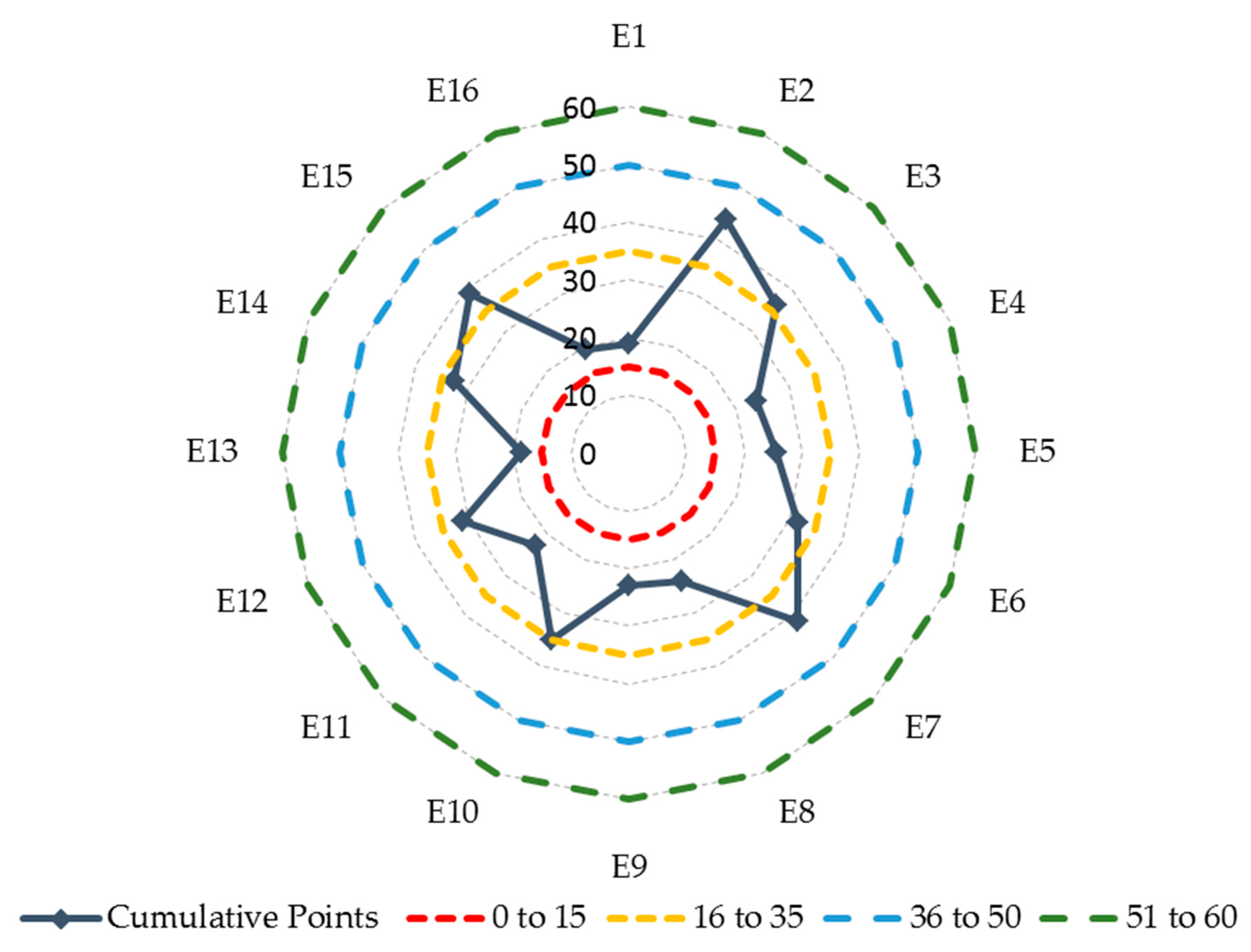

| Points | Corporate Social Responsibility Position |

|---|---|

| From 0 to 15 points | The company has great opportunities for improvement, as it does not yet have a management focused on corporate social responsibility. The tool will aim to plan a more structured way to increase the quality and the extent of the actions focused on corporate social responsibility. |

| From 16 to 35 points | The company already carried out corporate social responsibility actions. Analyze in detail the tool used, checking the topics with the highest score, and what contributed to this result. |

| From 36 to 50 points | The company has already assimilated the concepts of corporate social responsibility and has clarity of the commitments necessary for a socially responsible performance. These commitments should bring positive aspects to the business, through a closer and productive relationship with the parties involved (government and society, community, employees, customers, suppliers). At this stage, the company has matured some aspects of this action. |

| From 51 to 60 points | The company dominates emerging management concepts and uses corporate social responsibility to achieve its goals. At this stage, it is clear the feasibility to develop partnerships and intersectoral alliances, seeking to enhance the company’s performance, besides giving relevance to the systematization of knowledge through collaborative actions. |

| Enterprises | Values and Transparency | Internal Audience | Environment | Suppliers Relationship | Customers and/or Consumers Relationship | Community Relationship | Cumulative Points |

|---|---|---|---|---|---|---|---|

| E1 | 0.00 | 5.18 | 2.22 | 0.67 | 10.0 | 0.83 | 18.90 |

| E2 | 7.50 | 7.40 | 8.88 | 5.41 | 7.50 | 7.08 | 43.77 |

| E3 | 8.33 | 6.66 | 5.55 | 4.06 | 10.00 | 1.66 | 36.26 |

| E4 | 2.50 | 6.29 | 3.33 | 1.35 | 7.50 | 2.91 | 23.88 |

| E5 | 10.0 | 2.96 | 2.22 | 4.06 | 5.00 | 1.24 | 25.48 |

| E6 | 0.83 | 4.44 | 7.77 | 5.41 | 9.16 | 4.16 | 31.77 |

| E7 | 5.83 | 7.77 | 7.77 | 6.09 | 10.0 | 3.75 | 41.21 |

| E8 | 1.66 | 2.96 | 4.44 | 4.06 | 7.50 | 3.33 | 23.95 |

| E9 | 2.49 | 5.18 | 3.33 | 4.06 | 6.66 | 1.25 | 22.97 |

| E10 | 5.83 | 5.18 | 8.88 | 3.38 | 8.33 | 3.33 | 34.93 |

| E11 | 3.33 | 3.33 | 6.66 | 0.67 | 6.66 | 2.08 | 22.73 |

| E12 | 6.66 | 5.92 | 6.66 | 0.67 | 10.0 | 1.25 | 31.16 |

| E13 | 6.66 | 5.92 | 3.33 | 0.67 | 0.83 | 1.25 | 18.66 |

| E14 | 1.66 | 6.66 | 6.66 | 2.03 | 10.0 | 5.83 | 32.84 |

| E15 | 5.83 | 5.44 | 7.77 | 5.41 | 8.33 | 6.25 | 39.03 |

| E16 | 0.83 | 3.70 | 4.44 | 0.00 | 7.50 | 2.91 | 19.38 |

| Average | 4.37 | 5.31 | 5.62 | 3.00 | 7.81 | 3.07 | 29.18 |

| Standard Deviation | 3.07 | 1.51 | 2.31 | 2.10 | 2.39 | 1.94 | 8.26 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schmidt, F.C.; Zanini, R.R.; Korzenowski, A.L.; Schmidt Junior, R.; Xavier do Nascimento, K.B. Evaluation of Sustainability Practices in Small and Medium-Sized Manufacturing Enterprises in Southern Brazil. Sustainability 2018, 10, 2460. https://doi.org/10.3390/su10072460

Schmidt FC, Zanini RR, Korzenowski AL, Schmidt Junior R, Xavier do Nascimento KB. Evaluation of Sustainability Practices in Small and Medium-Sized Manufacturing Enterprises in Southern Brazil. Sustainability. 2018; 10(7):2460. https://doi.org/10.3390/su10072460

Chicago/Turabian StyleSchmidt, Fabricio Carlos, Roselaine Ruviaro Zanini, André Luis Korzenowski, Reno Schmidt Junior, and Karl Benchimol Xavier do Nascimento. 2018. "Evaluation of Sustainability Practices in Small and Medium-Sized Manufacturing Enterprises in Southern Brazil" Sustainability 10, no. 7: 2460. https://doi.org/10.3390/su10072460

APA StyleSchmidt, F. C., Zanini, R. R., Korzenowski, A. L., Schmidt Junior, R., & Xavier do Nascimento, K. B. (2018). Evaluation of Sustainability Practices in Small and Medium-Sized Manufacturing Enterprises in Southern Brazil. Sustainability, 10(7), 2460. https://doi.org/10.3390/su10072460