Enhancing Bank Loyalty through Sustainable Banking Practices: The Mediating Effect of Corporate Image

Abstract

1. Introduction

2. Theoretical Framework

Socially Responsible Investment

3. Literature Review

3.1. Bank Loyalty

3.2. Sustainable Banking

3.3. Corporate Image

4. Methods

4.1. Measurement Validity

4.2. Discriminant Validity

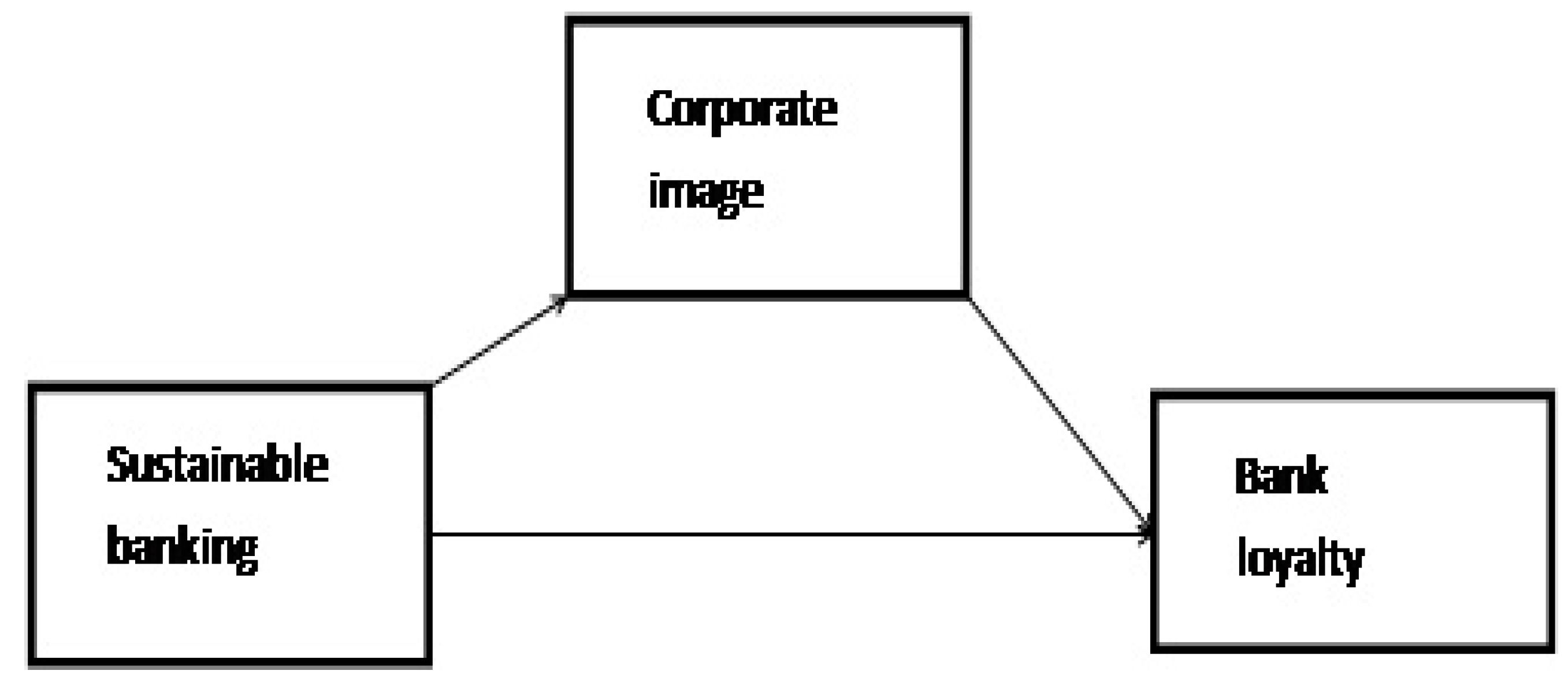

4.3. Test of Hypotheses

5. Discussion

Author Contributions

Funding

Conflicts of Interest

References

- Brundtland, G.H. Our common future—Call for action. Environ. Conser. 1987, 14, 291–294. [Google Scholar] [CrossRef]

- Renn, O.; Jager, A.; Deuschle, J.; Weimer-Jehle, W. A normative-functional concept of sustainability and its indicators. Int. J. Glob. Environ. Issues 2009, 9, 291–317. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Fisk, P. People Planet Profit: How to Embrace Sustainability for Innovation and Business Growth; Kogan Page Publishers: London, UK, 2010. [Google Scholar]

- Baldassarre, B.; Calabretta, G.; Bocken, N.M.; Jaskiewicz, T. Bridging sustainable business model innovation and user-driven innovation: A process for sustainable value proposition design. J. Clean Prod. 2017, 147, 175–186. [Google Scholar] [CrossRef]

- Bocken, N.; Short, S.; Rana, P.; Evans, S. A value mapping tool for sustainable business modelling. Corp. Gov. 2013, 13, 482–497. [Google Scholar] [CrossRef]

- Boons, F.; Lüdeke-Freund, F. Business models for sustainable innovation: State-of-the-art and steps towards a research agenda. J. Clean Prod. 2013, 45, 9–19. [Google Scholar] [CrossRef]

- Girotra, K.; Netessine, S. OM Forum—Business model innovation for sustainability. Manuf. Serv. Oper. Manag. 2013, 15, 537–544. [Google Scholar] [CrossRef]

- Hervani, A.A.; Sarkis, J.; Helms, M.M. Environmental goods valuations for social sustainability: A conceptual framework. Technol. Forecast. Soc. Chang. 2017, 125, 137–153. [Google Scholar] [CrossRef]

- Sueyoshi, T.; Yuan, Y.; Li, A.; Wang, D. Social sustainability of provinces in China: A data envelopment analysis (DEA) window analysis under the concepts of natural and managerial disposability. Sustainability 2017, 11, 2078. [Google Scholar] [CrossRef]

- Pitarch-Garrido, M.D. Social Sustainability in Metropolitan Areas: Accessibility and Equity in the Case of the Metropolitan Area of Valencia (Spain). Sustainability 2018, 2, 371. [Google Scholar] [CrossRef]

- Park, S.; Jun, S. Statistical Technology Analysis for Competitive Sustainability of Three Dimensional Printing. Sustainability 2017, 7, 1142. [Google Scholar] [CrossRef]

- Batista, A.A.; Francisco, A.C. Organizational sustainability practices: A study of the firms listed by the Corporate Sustainability Index. Sustainability 2018, 1, 226. [Google Scholar] [CrossRef]

- Jeong, J.; Park, N. Core Elements for Organizational Sustainability in Global Markets: Korean Public Relations Practitioners’ Perceptions of Their Job Roles. Sustainability 2017, 9, 1646. [Google Scholar] [CrossRef]

- Bocken, N.M.; Short, S.W.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Yip, A.W.; Bocken, N.M. Sustainable business model archetypes for the banking industry. J. Clean. Prod. 2018, 174, 150–169. [Google Scholar] [CrossRef]

- Weber, O. Sustainability benchmarking of European banks and financial service organizations. Corp. Soc. Responsib. Environ. Manag. 2005, 12, 73–87. [Google Scholar] [CrossRef]

- Sanfeliu, C.B.; Royo, R.C.; Clemente, I.M. Measuring performance of social and non-profit Microfinance Institutions (MFIs): An application of multicriterion methodology. Math. Comput. Model. 2013, 57, 1671–1678. [Google Scholar] [CrossRef]

- Daher, L.; Le Saout, E. Microfinance and financial performance. Strateg. Chang. 2013, 22, 31–45. [Google Scholar] [CrossRef]

- Oyegunle, A.; Weber, O. Development of Sustainability and Green Banking Regulations: Existing Codes and Practices; CIGI Paper No. 65; CIGI: Waterloo, ON, Canada, 2015. [Google Scholar]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development; Resolution adopted by the General Assembly; United Nations General Assembly: New York, NY, USA, 2015. [Google Scholar]

- Global Alliance for Banking on Values (GABV). Strong, Straight Forward and Sustainable Banking. A Report on Financial Capital and Impact Metrics of Values Based Banking. 2012. Available online: www.gabv.org/wp-content/uploads/Full-Report-GABV-v9d.pdf (accessed on 12 April 2018).

- Batchelor, S. Changing the Financial Landscape of Africa: An Unusual Story of Evidence-informed Innovation, Intentional Policy Influence and Private Sector Engagement. IDS Bull. 2012, 5, 84–90. [Google Scholar] [CrossRef]

- Yunus, M.; Moingeon, B.; Lehmann-Ortega, L. Building social business models: Lessons from the Grameen experience. Long Range Plan. 2010, 43, 308–325. [Google Scholar] [CrossRef]

- Climent, F. Ethical Versus Conventional Banking: A Case Study. Sustainability 2018, 10, 2152. [Google Scholar] [CrossRef]

- Ferreira, F.A.; Jalali, M.S.; Meidutė-Kavaliauskienė, I.; Viana, B.A. A metacognitive decision making based-framework for bank customer loyalty measurement and management. Technol. Econ. Dev. Econ. 2015, 2, 280–300. [Google Scholar] [CrossRef]

- Rebai, S.; Azaiez, M.N.; Saidane, D. A multi-attribute utility model for generating a sustainability index in the banking sector. J. Clean Prod. 2016, 113, 835–849. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of a Corporate Culture of Sustainability on Corporate Behavior and Performance; National Bureau of Economic Research: Cambridge, MA, USA, 2012. [Google Scholar]

- Miroshnychenko, I.; Barontini, R.; Testa, F. Green practices and financial performance: A global outlook. J. Clean Prod. 2017, 147, 340–351. [Google Scholar] [CrossRef]

- Arasli, H.; TuranKatircioglu, S.; Mehtap-Smadi, S. A comparison of service quality in the banking industry: Some evidence from Turkish-and Greek-speaking areas in Cyprus. Int. J. Bank Mark. 2005, 7, 508–526. [Google Scholar] [CrossRef]

- Şafakli, O. Assessing the need of TQM in the banking sector of the Northern Cyprus. J. Trans. Manag. 2005, 2, 59–72. [Google Scholar] [CrossRef]

- Harvey, B. Ethical banking: The case of the Co-operative bank. J. Bus. Ethics 1995, 12, 1005–1013. [Google Scholar] [CrossRef]

- Scholtens, B.; Cerin, P.; Hassel, L. Sustainable development and socially responsible finance and investing. Sustain. Dev. 2008, 3, 137–140. [Google Scholar] [CrossRef]

- Jeucken, M.; Bouma, J.J. The changing environment of banks. In Sustainable Banking; Routledge: Abingdon, UK, 2017; pp. 24–38. [Google Scholar]

- Renneboog, L.; Horst, J.; Zhang, C. Socially responsible investment funds. In A Handbook of Corporate Governance and Social; Aras, G., Crowthere, D., Eds.; Routledge: Abingdon, UK, 2010. [Google Scholar]

- Beerli, A.; Martin, J.D.; Quintana, A. A model of customer loyalty in the retail banking market. Eur. J. Mark. 2004, 38, 253–275. [Google Scholar] [CrossRef]

- Bloemer, J.; De Ruyter, K.; Peeters, P. Investigating drivers of bank loyalty: The complex relationship between image, service quality and satisfaction. Int. J. Bank Mark. 1998, 7, 276–286. [Google Scholar] [CrossRef]

- van Esterik-Plasmeijer, P.W.; van Raaij, W.F. Banking system trust, bank trust, and bank loyalty. Int. J. Bank Mark. 2017, 1, 97–111. [Google Scholar] [CrossRef]

- Makanyeza, C.; Chikazhe, L. Mediators of the relationship between service quality and customer loyalty: Evidence from the banking sector in Zimbabwe. Int. J. Bank Mark. 2017, 3, 540–556. [Google Scholar] [CrossRef]

- Erdem, T.; Swait, J. Brand credibility, brand consideration, and choice. J. Consum. Res. 2004, 1, 191–198. [Google Scholar] [CrossRef]

- Jeucken, M. Sustainable Finance and Banking: The Financial Sector and the Future of the Planet; Routledge: Abingdon, UK, 2010. [Google Scholar]

- Ramnarain, T.D.; Pillay, M.T. Designing Sustainable Banking Services: The Case of Mauritian Banks. Procedia-Soc. Behav. Sci. 2016, 224, 483–490. [Google Scholar] [CrossRef]

- Chesbrough, H. Business model innovation: Opportunities and barriers. Long Range Plan. 2010, 43, 354–363. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 1, 65–91. [Google Scholar] [CrossRef]

- Tyl, B.; Vallet, F.; Bocken, N.M.; Real, M. The integration of a stakeholder perspective into the front end of eco-innovation: A practical approach. J. Clean. Prod. 2015, 108, 543–557. [Google Scholar] [CrossRef]

- Schaltegger, S.; Hansen, E.G.; Lüdeke-Freund, F. Business models for sustainability: Origins, present research, and future avenues. Organ. Environ. 2016, 29, 3–10. [Google Scholar] [CrossRef]

- Jeucken, M. Sustainability in Finance: Banking on the Planet; EburonUitgeverij BV: Delft, The Netherlands, 2004. [Google Scholar]

- Walker, M. Building Sustainable Banking Architectures. Microsoft Developer Network, 2007. Available online: https://msdn.microsoft.com/enus/library/bb278105.aspx (accessed on 7 June 2017).

- Case, P. Managing Sustainability Risks and Opportunities in the Financial Services Sector—Non-Executive Directors Briefing. PriceWaterhouseCoopers. 2012. Available online: https://www.pwc.com/en_JG/jg/publications/ned-sustainability-presentation (accessed on 9 May 2017).

- Rebai, S. New Banking Performance Evaluation Approach: Sustainable Finance and Sustainable Banking Based. Ph.D. Dissertation, Higher Institute of Management, University of Tunis, Tunis, Tunisia, 2014. [Google Scholar]

- Global Alliance for Banking on Values (GABV). About Us—Our Principles. Global Alliance for Banking on Values. 2015. Available online: http://www.gabv.org/about-us/our-principles (accessed on 5 January 2018).

- Høgevold, N.M.; Svensson, G. A business sustainability model: A European case study. J. Bus. Ind. Mark. 2012, 2, 142–151. [Google Scholar] [CrossRef]

- Falcone, P.M.; Morone, P.; Sica, E. Greening of the financial system and fuelling a sustainability transition: A discursive approach to assess landscape pressures on the Italian financial system. Technol. Forecast. Soc. Chang. 2018, 127, 23–37. [Google Scholar] [CrossRef]

- Worcester, R.M. Managing the image of your bank: The glue that binds. Int. J. Bank Mark. 1997, 5, 146–152. [Google Scholar] [CrossRef]

- Fombrun, C.J. Reputation: Realizing Value from the Corporate Image; Harvard Business School Press: Boston, MA, USA, 1996. [Google Scholar]

- Herstein, R.; Mitki, Y.; Jaffe, E.D. Communicating a new corporate image during privatization: The case of El Al airlines. Corp. Commun. Int. J. 2008, 4, 380–393. [Google Scholar] [CrossRef]

- Van Riel, C.B.; Fombrun, C.J. Essentials of Corporate Communication: Implementing Practices for Effective Reputation Management; Routledge: Abingdon, UK, 2007. [Google Scholar]

- Flavián, C.; Guinaliu, M.; Torres, E. The influence of corporate image on consumer trust: A comparative analysis in traditional versus internet banking. Internet Res. 2005, 4, 447–470. [Google Scholar] [CrossRef]

- Kandampully, J.; Hu, H.H. Do hoteliers need to manage image to retain loyal customers? Int. J. Contemp. Hosp. Manag. 2007, 6, 435–443. [Google Scholar] [CrossRef]

- Heinberg, M.; Ozkaya, H.E.; Taube, M. Do corporate image and reputation drive brand equity in India and China?-Similarities and differences. J. Bus. Res. 2018, 86, 259–268. [Google Scholar] [CrossRef]

- Smith, D.; Harbisher, A. Building societies as retail banks: The importance of customer service and corporate image. Int. J. Bank Mark. 1989, 1, 22–27. [Google Scholar] [CrossRef]

- Bravo, R.; Montaner, T.; Pina, J.M. The role of bank image for customers versus non-customers. Int. J. Bank Mark. 2009, 4, 315–334. [Google Scholar] [CrossRef]

- Nguyen, N.; Leblanc, G. Corporate image and corporate reputation in customers’ retention decisions in services. J. Retail. Consum. Serv. 2001, 4, 227–236. [Google Scholar] [CrossRef]

- Hong, T.L.; Cheong, C.B.; Rizal, H.S. Service Innovation in Malaysian Banking Industry towards Sustainable Competitive Advantage through Environmentally and Socially Practices. Procedia Soc. Behav. Sci. 2016, 224, 52–59. [Google Scholar] [CrossRef]

- Karatepe, O.M.; Choubtarash, H. The effects of perceived crowding, emotional dissonance, and emotional exhaustion on critical job outcomes: A study of ground staff in the airline industry. J. Air Trans. Manag. 2014, 40, 182–191. [Google Scholar] [CrossRef]

- Hooper, D.; Coughlan, J.; Mullen, M. Structural equation modelling: Guidelines for determining model fit. Electron. J. Bus. Res. Methods 2008, 6, 53–60. [Google Scholar]

- Bagozzi, R.P.; Yi, Y. On the evaluation of structural equation models. J. Acad. Mark. Sci. 1988, 1, 74–94. [Google Scholar] [CrossRef]

- Cortina, J.M. What is coefficient alpha? An examination of theory and applications. J. Appl. Psychol. 1993, 78, 98. [Google Scholar] [CrossRef]

- Nunnally, J.C. Psychometric Theory, 2nd ed.; Mcgraw-Hill: Hillsdale, NJ, USA, 1978. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 1, 39–50. [Google Scholar] [CrossRef]

- Segars, A.H. Assessing the unidimensionality of measurement: A paradigm and illustration within the context of information systems research. Omega 1997, 1, 107–121. [Google Scholar] [CrossRef]

- To, W.M.; Lam, K.H.; Lai, T.M. Importance-performance ratings for environmental practices among Hong Kong professional-level employees. J. Clean. Prod. 2015, 108, 699–706. [Google Scholar] [CrossRef]

- Staub, S.; Kaynak, R.; Gok, T. What affects sustainability and innovation—Hard or soft corporate identity? Technol. Forecast. Soc. Chang. 2016, 102, 72–79. [Google Scholar] [CrossRef]

- Wang, C.Y. Service quality, perceived value, corporate image, and customer loyalty in the context of varying levels of switching costs. Psychol. Mark. 2010, 3, 252–262. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Rauter, R. Strategic perspectives of corporate sustainability management to develop a sustainable organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Ferreira, F.A.; Jalali, M.S.; Ferreira, J.J. Experience-focused thinking and cognitive mapping in ethical banking practices: From practical intuition to theory. J. Bus. Res. 2016, 11, 4953–4958. [Google Scholar] [CrossRef]

{kind=link}

| Construct | Description | Frequency |

|---|---|---|

| Gender | ||

| Male | 284 | 55.6 |

| Female | 227 | 44.4 |

| Age | ||

| 18–25 | 146 | 28.6 |

| 26–35 | 131 | 25.6 |

| 36–45 | 124 | 24.3 |

| 46 and above | 110 | 21.5 |

| Education | ||

| BSc | 328 | 64.2 |

| MSc | 95 | 18.8 |

| PhD | 11 | 2.2 |

| Others | 77 | 15.1 |

| Marital Status | ||

| Married | 265 | 51.9 |

| Single | 246 | 48.1 |

| Construct | Items | Standardized Factor Loading | Cronbach’s Alpha | Composite Reliability |

|---|---|---|---|---|

| Sustainable banking | SB8 | 0.911 | 0.943 | 0.953 |

| SB9 | 0.941 | |||

| SB10 | 0.949 | |||

| Corporate image | CI1 | 0.884 | 0.880 | 0.873 |

| CI2 | 0.855 | |||

| CI3 | 0.860 | |||

| CI4 | 0.565 | |||

| CI5 | 0.600 | |||

| Bank trust | BL2 | 0.953 | 0.879 | 0.967 |

| BL3 | 0.954 | |||

| BL4 | 0.970 | |||

| BL5 | 0.873 |

| Construct | M | SD | SB | CI | BL |

|---|---|---|---|---|---|

| SB | 2.921 | 1.103 | 0.934 | ||

| CI | 2.906 | 1.099 | 0.474 | 0.766 | |

| BL | 2.889 | 1.100 | 0.598 | 0.433 | 0.938 |

| Hypothesis | Path | Standardized Estimate | Remark |

|---|---|---|---|

| H1 | SB → CI | 0.498 | Supported |

| H2 | SB → BL | 0.744 | Supported |

| H3 | CI → BL | 0.112 | Supported |

| H4 | SB → CI → BL | 0.055 | Supported |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Igbudu, N.; Garanti, Z.; Popoola, T. Enhancing Bank Loyalty through Sustainable Banking Practices: The Mediating Effect of Corporate Image. Sustainability 2018, 10, 4050. https://doi.org/10.3390/su10114050

Igbudu N, Garanti Z, Popoola T. Enhancing Bank Loyalty through Sustainable Banking Practices: The Mediating Effect of Corporate Image. Sustainability. 2018; 10(11):4050. https://doi.org/10.3390/su10114050

Chicago/Turabian StyleIgbudu, Nicholas, Zanete Garanti, and Temitope Popoola. 2018. "Enhancing Bank Loyalty through Sustainable Banking Practices: The Mediating Effect of Corporate Image" Sustainability 10, no. 11: 4050. https://doi.org/10.3390/su10114050

APA StyleIgbudu, N., Garanti, Z., & Popoola, T. (2018). Enhancing Bank Loyalty through Sustainable Banking Practices: The Mediating Effect of Corporate Image. Sustainability, 10(11), 4050. https://doi.org/10.3390/su10114050