The Emerging Technologies of Digital Payments and Associated Challenges: A Systematic Literature Review

Abstract

1. Introduction

2. Research Background

2.1. Digital Payment and Digital Payment Technologies

2.2. Related Work

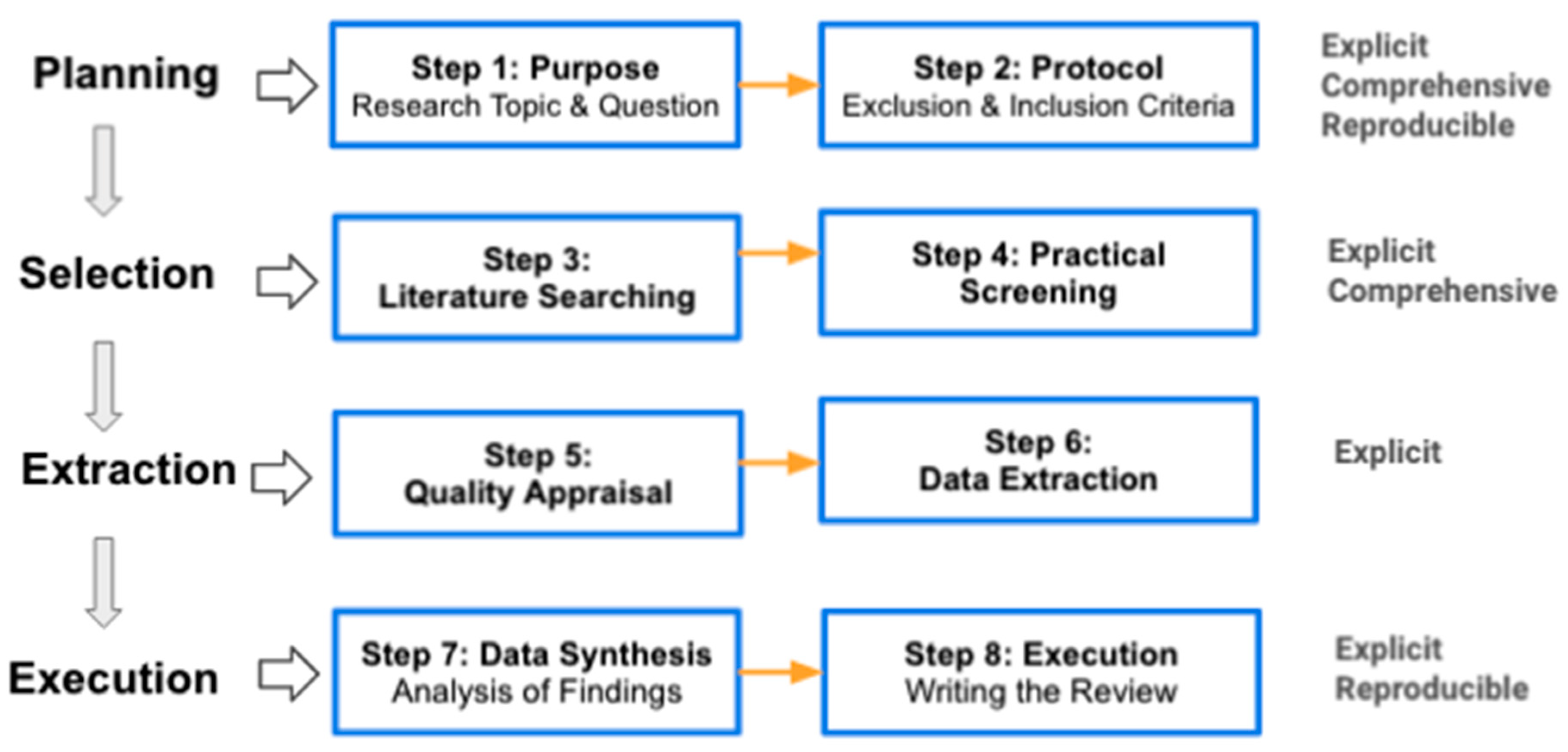

3. Methodology

4. Results and Discussion

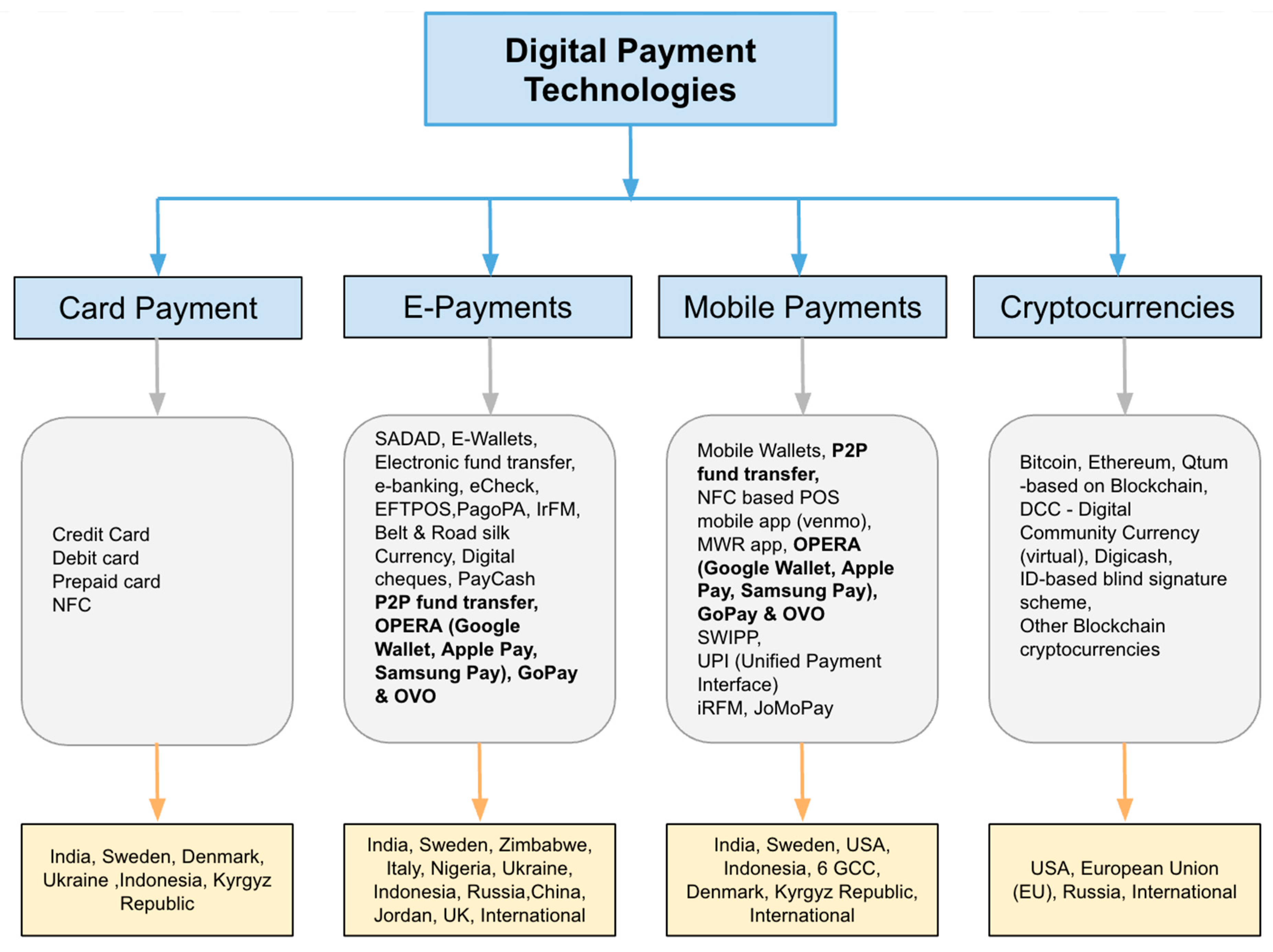

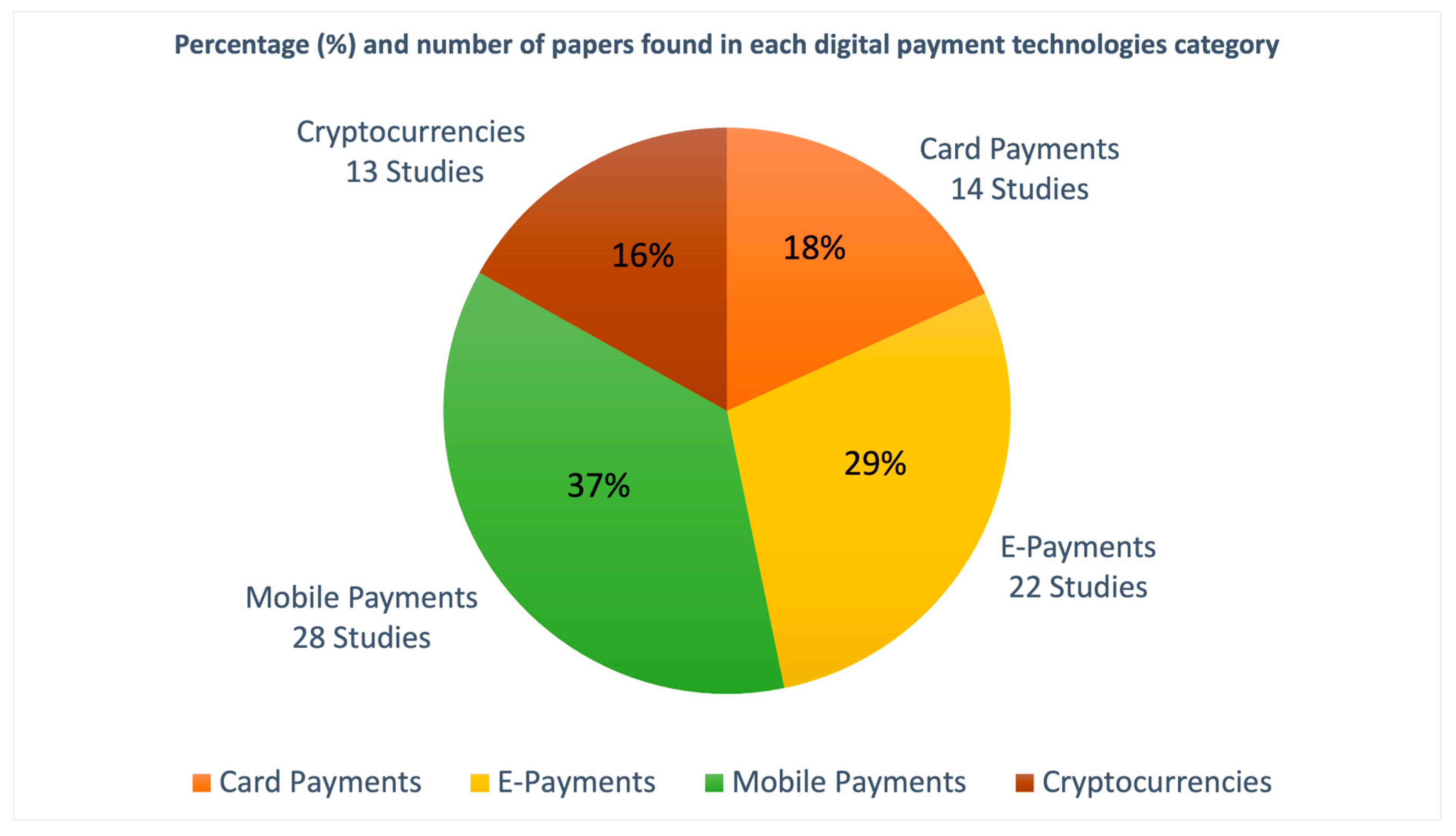

4.1. Emerging Digital Payment Technologies

4.1.1. Card Payments

4.1.2. E-Payments

4.1.3. Mobile Payments

4.1.4. Cryptocurrencies

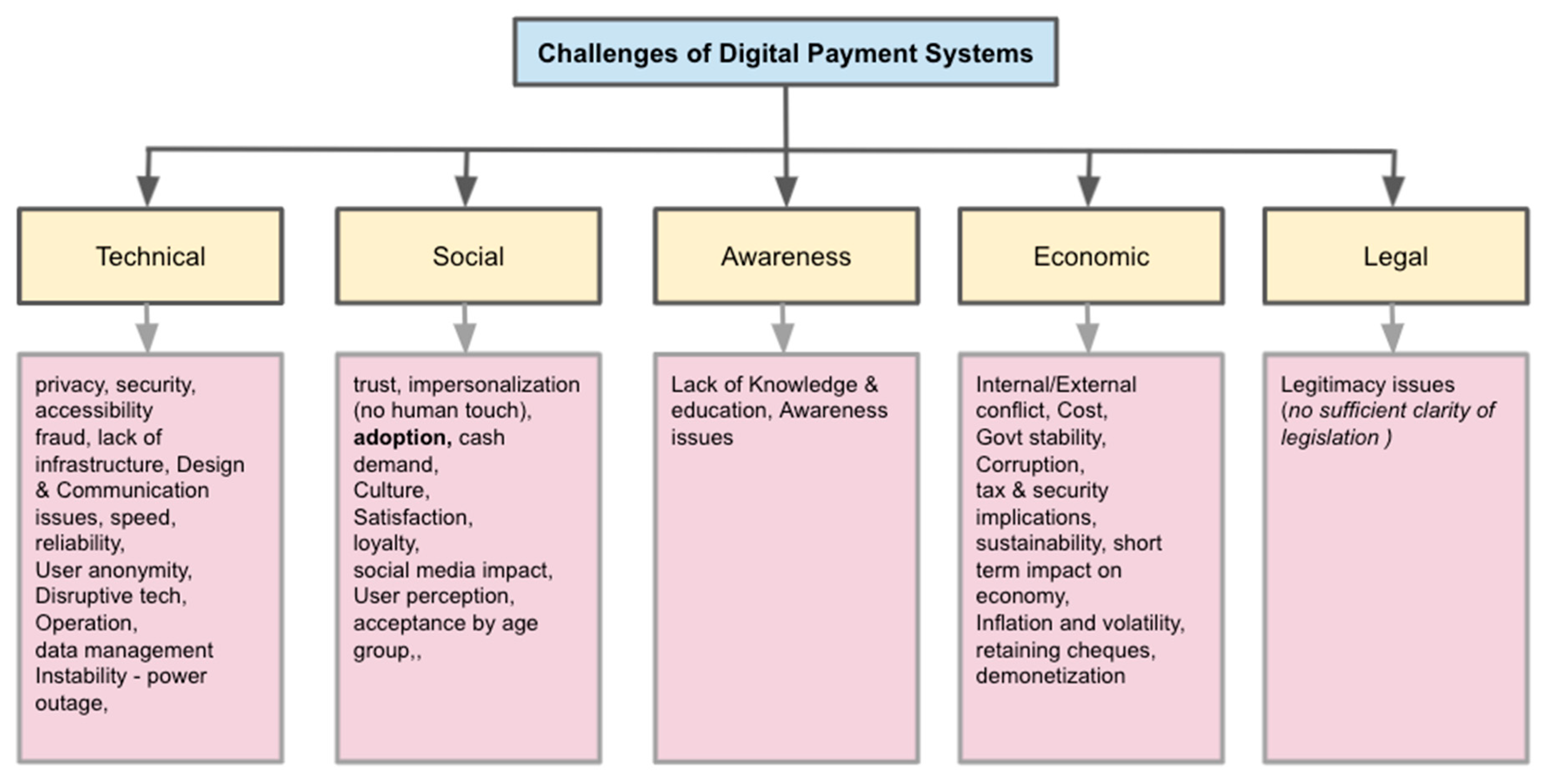

4.2. Challenges

4.2.1. Social Challenges

4.2.2. Technical Challenges

4.2.3. Economic Challenges

4.2.4. Awareness Challenges

4.2.5. Legal Challenges

4.3. Remarks on the Identified Challenges

5. Limitations

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Slozko, O.; Pelo, A. Problems and Risks of Digital Technologies Introduction into E-Payments. Transform. Bus. Econ. 2015, 14, 42–59. [Google Scholar]

- Premchand, A.; Choudhry, A. Future of Payments—ePayments. Int. J. Emerg. Technol. Adv. Eng. 2015, 5, 110–115. [Google Scholar]

- Capgemini. 2020 World Payments Report: Transforming into Digital Masters in the Next Normal; World Payments Report: 2020. Available online: https://www.sogeti.com/explore/reports/world-payments-report-2020/ (accessed on 8 November 2022).

- Statista. 2021 Digital Payments Report. Statista Digital Market Outlook. 2021. Available online: https://www.statista.com/study/41122/fintech-report-digital-payments/ (accessed on 8 November 2022).

- Khando, K.; Islam, M.S.; Gao, S. Factors Shaping the Cashless Payment Ecosystem: Understanding the Role of Participating Actors. In Proceedings of the 35th Bled eConference-Digital Restructuring and Human (Re) Action, Bled, Slovenia, 26–29 June 2022; University of Maribor University Press: Maribor, Slovenia, 2022; pp. 161–186. [Google Scholar]

- Visa School of Public Policy. (2 May 2018). Digital Payments & Economic Growth [Video]. YouTube. Available online: https://www.youtube.com/watch?v=EnzGI1yGcu0 (accessed on 8 November 2022).

- Goodell, G.; Al-Nakib, H.D.; Tasca, P. A digital currency architecture for privacy and owner-custodianship. Future Internet 2021, 13, 130. [Google Scholar] [CrossRef]

- Akanfe, O.; Valecha, R.; Rao, H.R. Assessing country-level privacy risk for digital payment systems. Comput. Secur. 2020, 99, 102065. [Google Scholar] [CrossRef]

- Singh, T.V.; Supriya, N.; Joshna, M.S. Issues and challenges of electronic payment systems. Int. J. Innov. Res. Dev. 2016, 2, 25–30. [Google Scholar]

- Khairun, N.K.; Yasmin, M.H. E-commerce Adoption in Malaysia: Trends, Issues and Opportunities. In ICT Strategic Review; PIKOM Publishers: Petaling Jaya, Malaysia, 2010; pp. 89–134. [Google Scholar]

- Najib, M.; Fahma, F. Investigating the adoption of digital payment system through an extended technology acceptance model: An insight from the Indonesian small and medium enterprises. Int. J. Adv. Sci. Eng. Inf. Technol. 2020, 10, 1702–1708. [Google Scholar] [CrossRef]

- Rana, N.P.; Luthra, S.; Rao, H.R. Developing a Framework using Interpretive Structural Modeling for the Challenges of Digital Financial Services in India. In Proceedings of the 22nd Pacific Asia Conference on Information Systems (PACIS 2018), Yokohama, Japan, 26–30 June 2018; Association for Information Systems: Atlanta, Georgia, 2018; p. 53. Available online: https://core.ac.uk/download/pdf/301375969.pdf (accessed on 8 November 2022).

- Kaleeth, A.B.L.; Chellammal, T. Adoption of Digital Payment Methods in Rural Areas of Ramanathapuram District. Ann. Rom. Soc. Cell Biol. 2021, 25, 7831–7837. [Google Scholar]

- Seethamraju, R.; Diatha, K.S. Adoption of Digital Payments by Small Retail Stores; UTS ePress: Ultimo, Australia, 2018. [Google Scholar]

- Ramli, F.A.A.; Hamzah, M.I. Mobile payment and e-wallet adoption in emerging economies: A systematic literature review. J. Emerg. Econ. Islam. Res. 2021, 9, 1–39. [Google Scholar] [CrossRef]

- Arango-Arango, C.A.; Suárez-Ariza, N. Digital payments adoption and the demand for cash: New international evidence. J. Paym. Strategy Syst. 2020, 14, 392–410. [Google Scholar]

- Casino, F.; Dasaklis, T.K.; Patsakis, C. A systematic literature review of blockchain-based applications: Current status, classification and open issues. Telemat. Inform. 2019, 36, 55–81. [Google Scholar] [CrossRef]

- Dahlberg, T.; Mallat, N.; Ondrus, J.; Zmijewska, A. Past, present and future of mobile payments research: A literature review. Electron. Commer. Res. Appl. 2008, 7, 165–181. [Google Scholar] [CrossRef]

- Kabir, M.A.; Saidin, S.Z.; Ahmi, A. Adoption of e-payment systems: A review of literature. In Proceedings of the International Conference on E-Commerce, Kuching, Malaysia, 20–22 October 2015; pp. 112–120. [Google Scholar]

- Adeoti, O.; Osotimehin, K. Adoption of point of sale terminals in Nigeria: Assessment of consumers’ level of satisfaction. Res. J. Financ. Account. 2012, 3, 1–6. [Google Scholar]

- DeVries, P.D. An analysis of cryptocurrency, bitcoin, and the future. Int. J. Bus. Manag. Commer. 2016, 1, 1–9. [Google Scholar]

- Insider Intelligence. Digital Payment Industry in 2021: Payment Methods, Trends, and Tech Processing Payments Electronically. 2021. Available online: https://www.insiderintelligence.com/insights/digital-payment-services/ (accessed on 8 November 2022).

- Rotolo, D.; Hicks, D.; Martin, B.R. What is an emerging technology? Res. Policy 2015, 44, 1827–1843. [Google Scholar] [CrossRef]

- Diniz, E.; Porto de Albuquerque, J.; Cernev, A. Mobile Money and Payment: A literature review based on academic and practitioner-oriented publications (2001–2011). Oriented Publications (2001–2011) (3 December 2011). In Proceedings of the SIG GlobDev Fourth Annual Workshop, Shanghai, China, 3 December 2011. [Google Scholar]

- Karsen, M.; Chandra, Y.U.; Juwitasary, H. Technological factors of mobile payment: A systematic literature review. Procedia Comput. Sci. 2019, 157, 489–498. [Google Scholar] [CrossRef]

- Patil, P.P.; Dwivedi, Y.K.; Rana, N.P. Digital payments adoption: An analysis of literature. In Conference on e-Business, e-Services and e-Society; Springer: Cham, Switzerland, 2017; pp. 61–70. [Google Scholar]

- Chitu, O.; Schabram, K. A Guide to Conducting a Systematic Literature Review of Information Systems Research; SSRN: Amsterdam, The Netherlands, 2010. [Google Scholar]

- Falagas, M.E.; Pitsouni, E.I.; Malietzis, G.A.; Pappas, G. Comparison of PubMed, Scopus, web of science, and Google scholar: Strengths and weaknesses. FASEB J. 2008, 22, 338–342. [Google Scholar] [CrossRef]

- Fink, A. Conducting Research Literature Reviews: From the Internet to Paper; Sage Publications: Thousand Oaks, CA, USA, 2019. [Google Scholar]

- Hart, C. Doing a Literature Review: Releasing the Social Science Research Imagination, 1st ed.; Sage Publications Ltd.: Thousand Oaks, CA, USA, 1999. [Google Scholar]

- Kitchenham Guidelines for Performing Systematic Literature Reviews in Software Engineering; Technical report, Ver. 2.3 EBSE Technical Report; EBSE: Goyang-si, Republic of Korea, 2007; Volume 5.

- Levy, Y.; Ellis, T.J. A systems approach to conduct an effective literature review in support of information systems research. Inf. Sci. 2006, 9, 181–212. [Google Scholar] [CrossRef]

- Webster, J.; Watson, R.T. Analyzing the past to prepare for the future: Writing a literature review. MIS Q. 2002, 26, xiii–xxiii. [Google Scholar]

- Boote, D.N.; Beile, P. Scholars before researchers: On the centrality of the dissertation literature review in research preparation. Educ. Res. 2005, 34, 3–15. [Google Scholar] [CrossRef]

- Balan, U.M.; Pal, A. Is Cash Still the Enemy? The Dampening of Demonetization’s Ripple Effect on Mobile Payments. In International Working Conference on Transfer and Diffusion of IT; Springer: Cham, Switzerland, 2020; pp. 529–540. [Google Scholar]

- Chakrabarty, M.; Jha, A.; Ray, P. Demonetization and digital payments in India: Perception and reality. Appl. Econ. Lett. 2021, 28, 319–323. [Google Scholar] [CrossRef]

- Dimitrova, I.; Öhman, P.; Yazdanfar, D. Challenges in the Limited Choice of Payment Methods in Terms of Cashless Society: Bank Customers’ Perspective (work in progress). In Proceedings of the 2019 3rd International Conference on E-Commerce, E-Business and E-Government, Lyon, France, 18–21 June 2019; pp. 45–48. [Google Scholar]

- Iqbal, R.; Ahmad, S.; Hashim, M. Evaluating Factors Affecting Communication in Wearable Internet of Things for Near Field. In Proceedings of the 2018 IEEE 87th Vehicular Technology Conference (VTC Spring), Porto, Portugal, 3–6 June 2018; pp. 1–4. [Google Scholar]

- Jain, K.; Chowdhary, R. A Study on Intention to Adopt Digital Payment Systems in India: Impact of COVID-19 Pandemic. Asia Pac. J. Inf. Syst. 2021, 31, 76–101. [Google Scholar] [CrossRef]

- Kantoroeva, A.K.; Toktomamatova, N.K. Some Aspects of the Development of Payment Innovations in the Kyrgyz Republic. Int. J. Criminol. Sociol. 2020, 9, 3007–3013. [Google Scholar]

- Ligon, E.; Malick, B.; Sheth, K.; Trachtman, C. What explains low adoption of digital payment technologies? Evidence from small-scale merchants in Jaipur, India. PLoS ONE 2019, 14, e0219450. [Google Scholar] [CrossRef] [PubMed]

- Pizzol, M.; Vighi, E.; Sacchi, R. Challenges in coupling digital payments data and input-output data to change consumption patterns. Procedia CIRP 2018, 69, 633–637. [Google Scholar] [CrossRef]

- Ravikumar, T.; Suresha, B.; Sriram, M.; Rajesh, R. Impact of Digital Payments on Economic Growth: Evidence from India. Int. J. Innov. Technol. Explor. Eng. 2019, 8, 553–557. [Google Scholar]

- Sharif, M.; Pal, R. Moving from cash to cashless: A study of consumer perception towards digital transactions. PRAGATI J. Indian Econ. 2020, 7, 1–13. [Google Scholar]

- Sivathanu, B. Adoption of digital payment systems in the era of demonetization in India: An empirical study. J. Sci. Technol. Policy Manag. 2019, 10, 143–171. [Google Scholar] [CrossRef]

- Thirupathi, M.; Vinayagamoorthi, G.; Mathiraj, S.P. Effect Of Cashless Payment Methods: A Case Study Perspective Analysis. Int. J. Sci. Technol. Res. 2019, 8, 394–397. [Google Scholar]

- Al-Okaily, M.; Lutfi, A.; Alsaad, A.; Taamneh, A.; Alsyouf, A. The determinants of digital payment systems’ acceptance under cultural orientation differences: The case of uncertainty avoidance. Technol. Soc. 2020, 63, 101367. [Google Scholar] [CrossRef]

- Datta, P.; Walker, L.; Amarilli, F. Digital transformation: Learning from Italy’s public administration. J. Inf. Technol. Teach. Cases 2020, 10, 54–71. [Google Scholar] [CrossRef]

- Dostov, V.; Shust, P. Cryptocurrencies: An unconventional challenge to the AML/CFT regulators? J. Financ. Crime 2014, 21, 249–263. [Google Scholar] [CrossRef]

- Huang, P.; Boucouvalas, A.C. Future personal” e-payment”: IRFM. IEEE Wirel. Commun. 2006, 13, 60–66. [Google Scholar] [CrossRef]

- Ilankumaran, G.; Darling Selvi, V. Customer Purview of Cashless Payment System in the Digital Economy of India. Int. J. Innov. Technol. Explor. Eng. 2019, 8, 87–93. [Google Scholar]

- Ivashchenko, A.; Britchenko, I.; Dyba, M.; Polishchuk, Y.; Sybirianska, Y.; Vasylyshen, Y. Fintech platforms in SME’s financing: EU experience and ways of their application in Ukraine. Investig. Manag. Financ. Innov. 2018, 15, 83–96. [Google Scholar] [CrossRef]

- Kumar, M.; Agrawal, S.; Mishra, R. User Behaviour and Digital Payment Ecosystem: An Audit of Connections between usage Attributes and Demographic Profile. Int. J. Emerg. Technol. 2020, 11, 935–938. [Google Scholar]

- Liu, F.; Lu, S.; Qin, S.; Shao, S. Research on the New Generation Electronic Payment System Applied in ‘The Belt and Road’. In Proceedings of the 2020 International Conference on E-Commerce and Internet Technology (ECIT), Zhangjiajie, China, 22–24 April 2020; pp. 5–9. [Google Scholar]

- Lakshmi, M.S.; Alamelumangai, R. Cashless Transactions: Opportunities and Challenges amongst MSME at Sivaganga District, Tamilnadu. Int. J. Sci. Technol. Res. 2020, 9, 4900–4902. [Google Scholar]

- Nwankwo, O.; Eze, O.R. Electronic payment in cashless economy of Nigeria: Problems and prospect. J. Manag. Res. 2013, 5, 138–151. [Google Scholar] [CrossRef]

- Selvakumar, D.S.; Sharma, A.K. A Study on Market Without Cash—Conventional to Digital. Int. J. Appl. Bus. Econ. Res. 2017, 15, 337–342. [Google Scholar]

- Simatele, M.; Mbedzi, E. Consumer payment choices, costs, and risks: Evidence from Zimbabwe. Cogent Econ. Financ. 2021, 9, 1875564. [Google Scholar] [CrossRef]

- Vines, J.; Dunphy, P.; Blythe, M.; Lindsay, S.; Monk, A.; Olivier, P. The joy of cheques: Trust, paper and eighty somethings. In Proceedings of the ACM 2012 Conference on Computer Supported Cooperative Work, Seattle, WA, USA, 11–15 February 2012; pp. 147–156. [Google Scholar]

- Vinitha, K.; Vasantha, S. Determinants of Customer intention to use Digital payment system. J. Adv. Res. Dyn. Control Syst. 2020, 12, 168–174. [Google Scholar]

- Alshubiri, F. The Impact of Financial Macroeconomic Indicators on Mobile Money: An Empirical Evidence of GCC Countries. In Proceedings of the 2019 International Conference on Digitization (ICD), Sharjah, United Arab Emirates, 18–19 November 2019; pp. 118–122. [Google Scholar]

- Bagla, R.K.; Sancheti, V. Gaps in customer satisfaction with digital wallets: Challenge for sustainability. J. Manag. Dev. 2018, 37, 442–451. [Google Scholar] [CrossRef]

- Chen, C.L.; Lin, Y.C.; Chen, W.H.; Chao, C.F.; Pandia, H. Role of Government to Enhance Digital Transformation in Small Service Business. Sustainability 2021, 13, 1028. [Google Scholar] [CrossRef]

- Garcia-Teruel, R.M. Legal challenges and opportunities of blockchain technology in the real estate sector. J. Prop. Plan. Environ. Law 2020, 12, 129–145. [Google Scholar] [CrossRef]

- Gupta, R.; Kapoor, C.; Yadav, J. Acceptance Towards Digital Payments and Improvements in Cashless Payment Ecosystem. In Proceedings of the 2020 International Conference for Emerging Technology (INCET), Belgaum, India, 5–7 June 2020; pp. 1–9. [Google Scholar]

- Park, K.W.; Baek, S.H. OPERA: A Complete Offline and Anonymous Digital Cash Transaction System with a One-Time Readable Memory. IEICE Trans. Inf. Syst. 2017, 100, 2348–2356. [Google Scholar] [CrossRef]

- Pradiatiningtyas, D.; Dewa, C.B.; Safitri, L.A.; Kiswati, S. The Effect of Satisfaction and Loyalty Towards Digital Payment System Users Among Generation Z in Yogyakarta Special Region. In Journal of Physics: Conference Series; IOP Publishing: Bristol, UK, 2022; Volume 1641, p. 012110. [Google Scholar]

- Sandeep, K.; Nidhi, W. Impact of Demonetization on Digital Payments in India—Event Study Methodology. Pac. Bus. Rev. Int. 2020, 13. Available online: http://www.pbr.co.in/2020/2020_month/October/2.pdf (accessed on 8 November 2022).

- Singh, A.K.; Mudang, T. Digital Payment System and the Millennial in a Smart City: An Antecedent to Technopreneurship. In Electronic Systems and Intelligent Computing; Springer: Singapore, 2020; pp. 109–118. [Google Scholar]

- Singh, G.; Kumar, B.; Gupta, R. The role of consumer’s innovativeness & perceived ease of use to engender adoption of digital wallets in India. In Proceedings of the 2018 International Conference on Automation and Computational Engineering (ICACE), Greater Noida, India, 3–4 October 2018; pp. 150–158. [Google Scholar]

- Staykova, K.S.; Damsgaard, J. The race to dominate the mobile payments platform: Entry and expansion strategies. Electron. Commer. Res. Appl. 2015, 14, 319–330. [Google Scholar] [CrossRef]

- Thiruvaazhi Arthi, R. Threats to Mobile Security and Privacy. Int. J. Recent Technol. Eng. 2018, 7, 407–412. [Google Scholar]

- Zhang, X.; Tang, S.; Zhao, Y.; Wang, G.; Zheng, H.; Zhao, B. Cold hard E-cash: Friends and vendors in the Venmo digital payments system. In Proceedings of the International AAAI Conference on Web and Social Media, Montreal, QC, Canada, 15–18 May 2017; Volume 11. [Google Scholar]

- Almarashdeh, I.; Bouzkraoui, H.; Azouaoui, A.; Youssef, H.; Niharmine, L.; Rahman, A.; Murimo, B.M. An overview of technology evolution: Investigating the factors influencing non-bitcoins users to adopt bitcoins as online payment transaction method. J. Theor. Appl. Inf. Technol. 2018, 96, 3984–3993. [Google Scholar]

- Alshamsi, A.; Andras, P. User perception of Bitcoin usability and security across novice users. Int. J. Hum.-Comput. Stud. 2019, 126, 94–110. [Google Scholar] [CrossRef]

- Androulaki, E.; Karame, G.O.; Roeschlin, M.; Scherer, T.; Capkun, S. Evaluating user privacy in bitcoin. In International Conference on Financial Cryptography and Data Security; Springer: Berlin/Heidelberg, Germany, 2013; pp. 34–51. [Google Scholar]

- Bello, G.; Perez, A.J. Adapting financial technology standards to blockchain platforms. In Proceedings of the 2019 ACM Southeast Conference, Kennesaw, GA, USA, 18–20 April 2019; pp. 109–116. [Google Scholar]

- Diniz, E.H.; Siqueira, E.S.; van Heck, E. Taxonomy of digital community currency platforms. Inf. Technol. Dev. 2019, 25, 69–91. [Google Scholar] [CrossRef]

- Elkamchouchi, H.; Abouelseoud, Y. Privacy protecting digital payment system using ID-based blind signatures with anonymity revocation trustees. In Proceedings of the 2008 International Conference on Computer Engineering & Systems, Cairo, Egypt, 25–27 November 2008; pp. 274–280. [Google Scholar]

- Mai, F.; Bai, Q.; Shan, Z.; Wang, X.; Chiang, R. From bitcoin to big coin: The impacts of social media on bitcoin performance. SSRN Electron. J 2015, 1–46. Available online: https://www.semanticscholar.org/paper/The-Impacts-of-Social-Media-on-Bitcoin-Performance-Mai-Bai/57344ccfe492af1ccfa05496ab2d4ef534ba632a (accessed on 8 November 2022). [CrossRef]

- Thawre, G.; Bahekar, N.; Chandavarkar, B.R. Use Cases of Authentication Protocols in the Context of Digital Payment System. In Proceedings of the 2020 11th International Conference on Computing, Communication and Networking Technologies (ICCCNT), Kharagpur, India, 1–3 July 2020; pp. 1–6. [Google Scholar]

- Wang, J.; Xue, Y.; Liu, M. An analysis of bitcoin price based on VEC model. In Proceedings of the 2016 International Conference on Economics and Management Innovations, Wuhan, China, 9–10 July 2016. [Google Scholar]

- Wijaya, D.A. Extending asset management system functionality in bitcoin platform. In Proceedings of the 2016 International Conference on Computer, Control, Informatics and its Applications (IC3INA), Tangerang, Indonesia, 3–5 October 2016; pp. 97–101. [Google Scholar]

- Experian. Credit Cards Matched to Your Credit Profile—Experian. 2021. Available online: https://www.experian.com/credit/credit-cards/ (accessed on 8 November 2022).

- Ankit, S. Factors influencing online banking customer satisfaction and their im- portance in improving overall retention levels: An Indian banking perspective. Inf. Knowl. Manag. 2011, 1, 45–54. [Google Scholar]

- Chen, L.D.; Nath, R. Determinants of mobile payments: An empirical analysis. J. Int. Technol. Inf. Manag. 2008, 17, 9–20. [Google Scholar]

- Lucarelli, S.; Sachy, M.; Brekke, K.J.; Bria, F.; Giuliani, A.; Gentilucci, E.; Idir, G. D3.4 Field Research and User Requirements Digital Social Currency Pilots; D-CENT: Seoul, Republic of Korea, 2014. [Google Scholar]

- Deng, R.; Ruan, N.; Zhang, G.; Zhang, X. FraudJudger: Fraud Detection on Digital Payment Platforms with Fewer Labels. In Proceedings of the International Conference on Information and Communications Security, Chongqing, China, 17–19 September 2019; Springer: Cham, Switzerland, 2019; pp. 569–583. [Google Scholar]

- Kolodiziev, O.; Mints, A.; Sidelov, P.; Pleskun, I.; Lozynska, O. Automatic Machine Learning Algorithms for Fraud Detection in Digital Payment Systems. East.-Eur. J. Enterp. Technol. 2020, 5, 107. [Google Scholar] [CrossRef]

- Shen, H.; Kurshan, E. Deep Q-network-based adaptive alert threshold selection policy for payment fraud systems in retail banking. arXiv 2020, arXiv:2010.11062. [Google Scholar]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Shah, P.; Dubhashi, M. Review Paper on Financial Inclusion-The Means of Inclusive Growth. Chanakya Int. J. Bus. Res. 2015, 1, 37–48. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Review by | No. of Papers | Focus of the Study |

|---|---|---|

| Our review (2021) | 58 | Emerging technologies of digital payment and challenges associated with them |

| Ahmad and Hamzah [15] | 77 | Mobile e-wallet in emerging economies |

| Kabir, Saidin and Ahmi [19] | 51 | Adoption of e-payment systems |

| Casino, Dasaklis and Patsakis [17] | 54 | Applications related to blockchain technology |

| Diniz, Porto and Cernev [24] | 192 | Mobile money and payment |

| Dahlberg et al. [18] | 73 | Past, present and future of mobile payment technology |

| Patil, Dwivedi and Rana [26] | 21 | Adoption of digital payment technologies |

| Karsen, Chandra and Juwitasary [25] | 54 | Technological factors of mobile payment |

| Selection Criteria | Eligibility Criteria |

|---|---|

| Inclusion |

Empirical studies only: Peer-reviewed research articles (final stage), conference proceedings and reviewed papers (in English language) Without time-frame restrictions |

| Exclusion |

During title screening and prior to downloading the article

|

| Keywords Searched | Database | Delimitation Criteria | No. of Papers |

|---|---|---|---|

| “digital payment” AND “digital payment system” OR “digital payment” AND emerging AND technology OR “digital payment”AND risks OR “digital payment”AND challenges | Web of Science | Publication stage: Final Publication years: No time-frame restrictions Document types: (Journal Articles and proceeding reviewed papers) Language: (english) | 37 |

| Scopus | 106 | ||

| Total | 143 | ||

| Subtracted “Papers with no full text access” | −21 | ||

| Subtracted “Duplications” | −22 | ||

| Total articles retrieved through the search process (downloaded for reading) | 100 | ||

| Article from Search Process | Practical Screening | Quality Screening | ||||

|---|---|---|---|---|---|---|

| Eligibility Criteria | Articles Screened- Out | Articles Selected | Eligibility Criteria | Article Screen- Out | Article Selected | |

| 100 | Inclusion criteria:

| 26 | 74 | Inclusion criteria:

| 22 | 52 |

| Articles selected through backward citation search | +6 | |||||

| Total No. of empirical studies used for the review | 58 | |||||

| Digital Payment Technologies | References |

|---|---|

| Card Payments (Credit/Debit card, Prepaid card) | [11,13,35,36,37,38,39,40,41,42,43,44,45,46] |

| E-Payments (SADAD, E-Wallets, Electronic fund transfer, e-banking, eCheck, EFTPOS, PagoPA, IrFM, Belt & Road silk Currency, Digital cheques, P2P fund transfer, Russian PayCash, OPERA (Google Wallet, Apple Pay, Samsung Pay), GoPay & OVO) | [11,13,16,37,41,44,45,46,47,48,49,50,51,52,53,54,55,56,57,58,59,60] |

| Mobile Payments (Mobile Wallets, P2P fund transfer, NFC based POS, mobile app (venmo), MWR app, OPERA (Google Wallet, Apple Pay, Samsung Pay), GoPay & OVO, SWIPP, UPI (Unified Payment Interface) iRFM, JoMoPay) | [8,11,12,13,35,36,37,38,40,41,45,46,61,62,63,64,65,66,67,68,69,70,71,72,73] |

| Cryptocurrencies (Bitcoin, Ethereum, Qtum -based on Blockchain, DCC—Digital Community Currency (virtual), Digicash, ID-based blind signature scheme, Other Blockchain cryptocurrencies) | [49,54,64,74,75,76,77,78,79,80,81,82,83] |

| Challenges | Studies Conducted |

|---|---|

| Social challenges—trust, impersonalization (no human touch), adoption, risks, cash demand, Culture, satisfaction, loyalty, social media impact, user perception, acceptance by age group, | [11,13,14,16,37,39,41,47,48,52,56,57,60,62,65,67,69,70,73,75,79,80] |

| Economic challenges—Internal/External conflict, Cost, Govt stability, Corruption, tax, cost implications & sustainability, short term impact on economy, inflation, volatility, retaining cheques, demonetization, | [8,13,35,36,43,56,59,61,62,68,82] |

| Technical challenges—privacy, security, access, fraud, lack of infrastructure, Design & Communication issues, speed, reliability, User anonymity, HR, Disruptive tech, operation, data management, Instability—power outage, | [8,11,12,13,37,38,40,41,44,45,46,47,50,51,52,56,57,58,59,63,66,69,71,72,76,79,81,82,83,88,89,90] |

| Awareness challenges (Lack of Knowledge & Awareness) | [11,12,13,42,44,45,51,53,55,57] |

| Legal challenges (Legitimacy problem—no sufficient clarity of legislation) | [49,52,64,74,76,77,78,79,82] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Khando, K.; Islam, M.S.; Gao, S. The Emerging Technologies of Digital Payments and Associated Challenges: A Systematic Literature Review. Future Internet 2023, 15, 21. https://doi.org/10.3390/fi15010021

Khando K, Islam MS, Gao S. The Emerging Technologies of Digital Payments and Associated Challenges: A Systematic Literature Review. Future Internet. 2023; 15(1):21. https://doi.org/10.3390/fi15010021

Chicago/Turabian StyleKhando, Khando, M. Sirajul Islam, and Shang Gao. 2023. "The Emerging Technologies of Digital Payments and Associated Challenges: A Systematic Literature Review" Future Internet 15, no. 1: 21. https://doi.org/10.3390/fi15010021

APA StyleKhando, K., Islam, M. S., & Gao, S. (2023). The Emerging Technologies of Digital Payments and Associated Challenges: A Systematic Literature Review. Future Internet, 15(1), 21. https://doi.org/10.3390/fi15010021