Deforestation as a Systemic Risk: The Case of Brazilian Bovine Leather †

Abstract

:1. Introduction

2. Conceptual Approach. Materials and Methods

2.1. Economic Analysis of Drivers of Deforestation

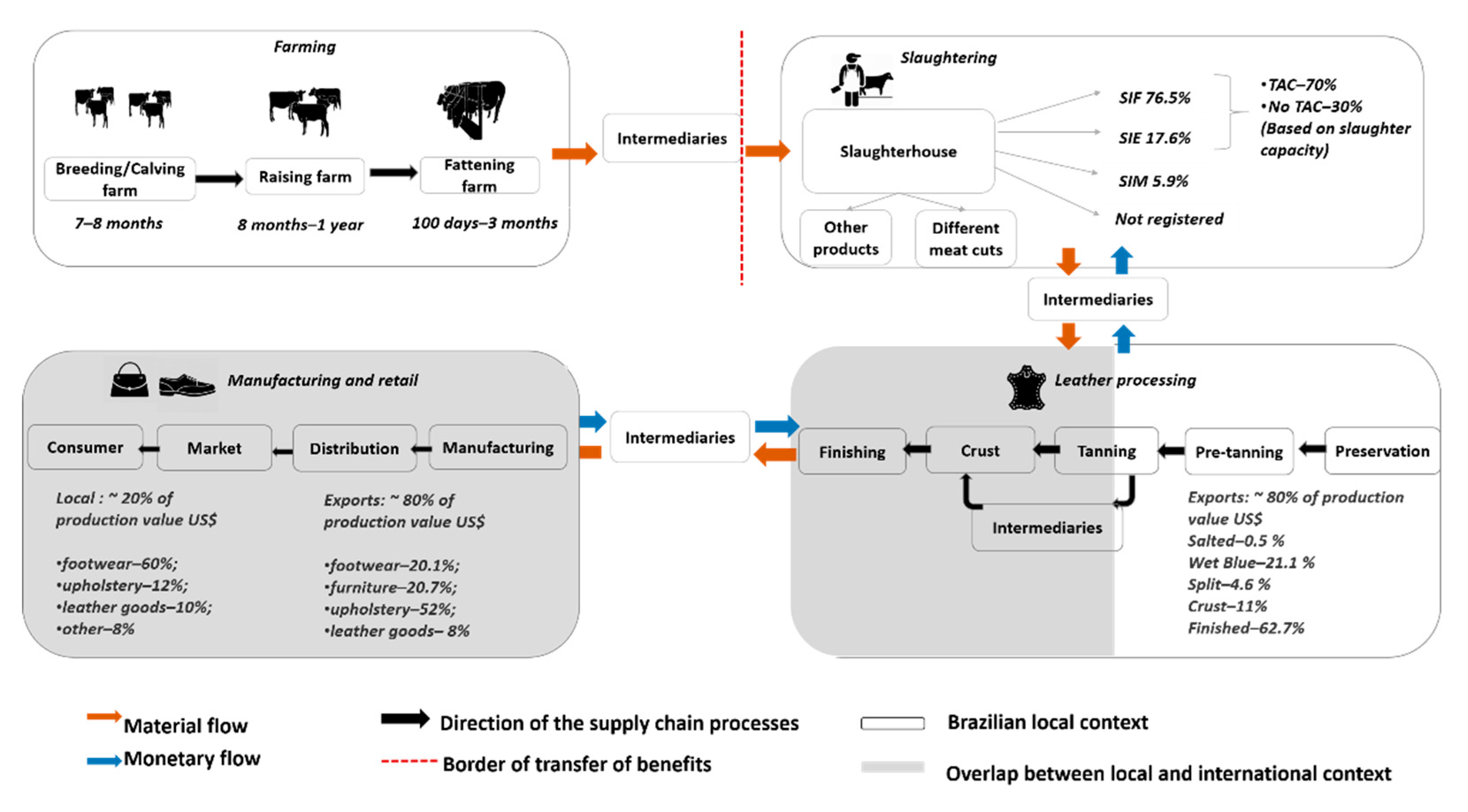

2.2. Supply Chains and Deforestation Risk

2.3. Materials

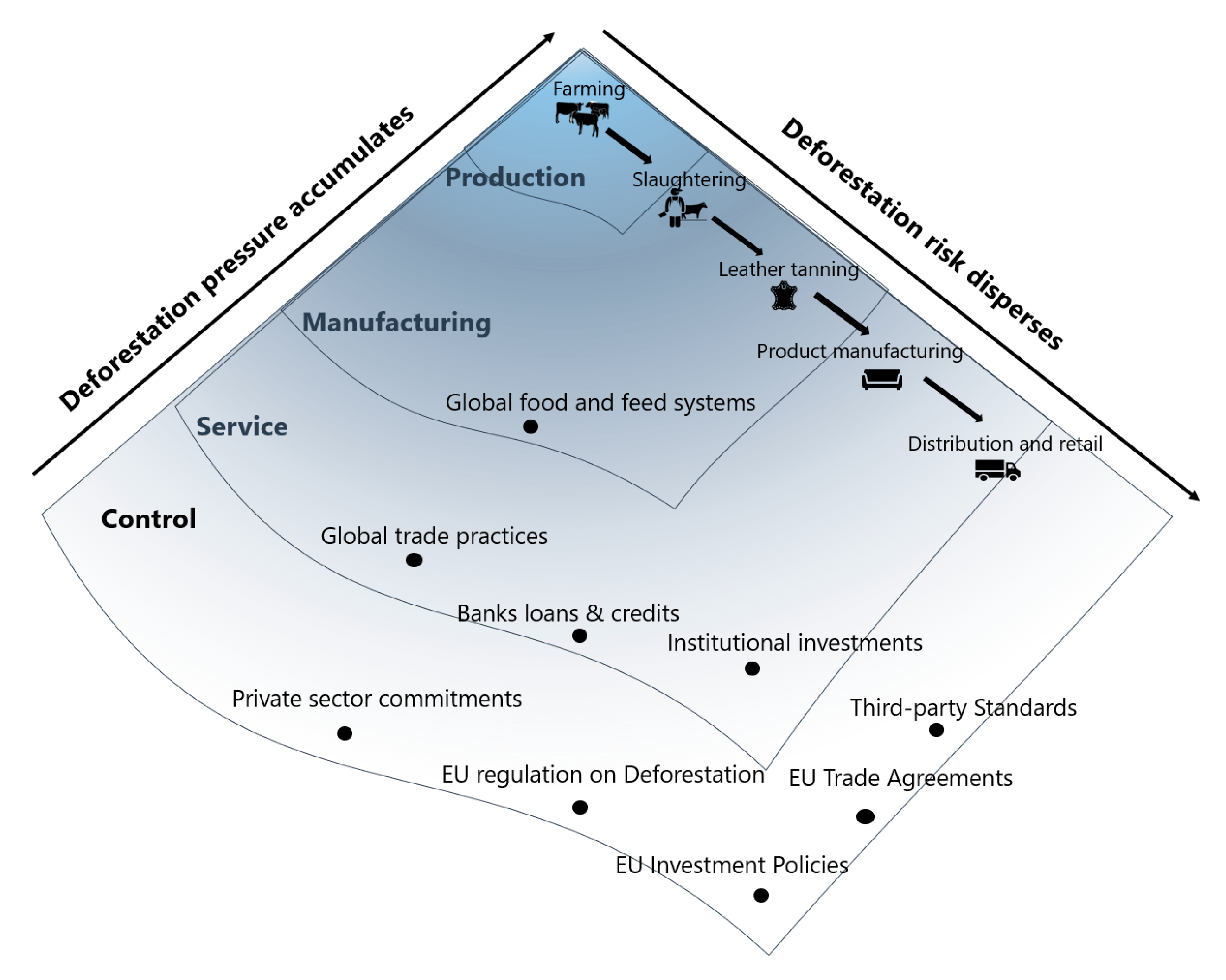

3. How Pressure for Deforestation Accumulates across Economic Sectors

3.1. Deforestation Pressures Coming from the Control Sector

3.2. The Deforestation Pressures Coming from Service Sector

3.3. Deforestation Pressures Coming from the Manufacturing Sector

3.4. Accumulated Pressure in the Production Sector: An Anchor Point?

4. How Traceability of Deforestation Risk Disperses across Supply Chains and Economic Sectors

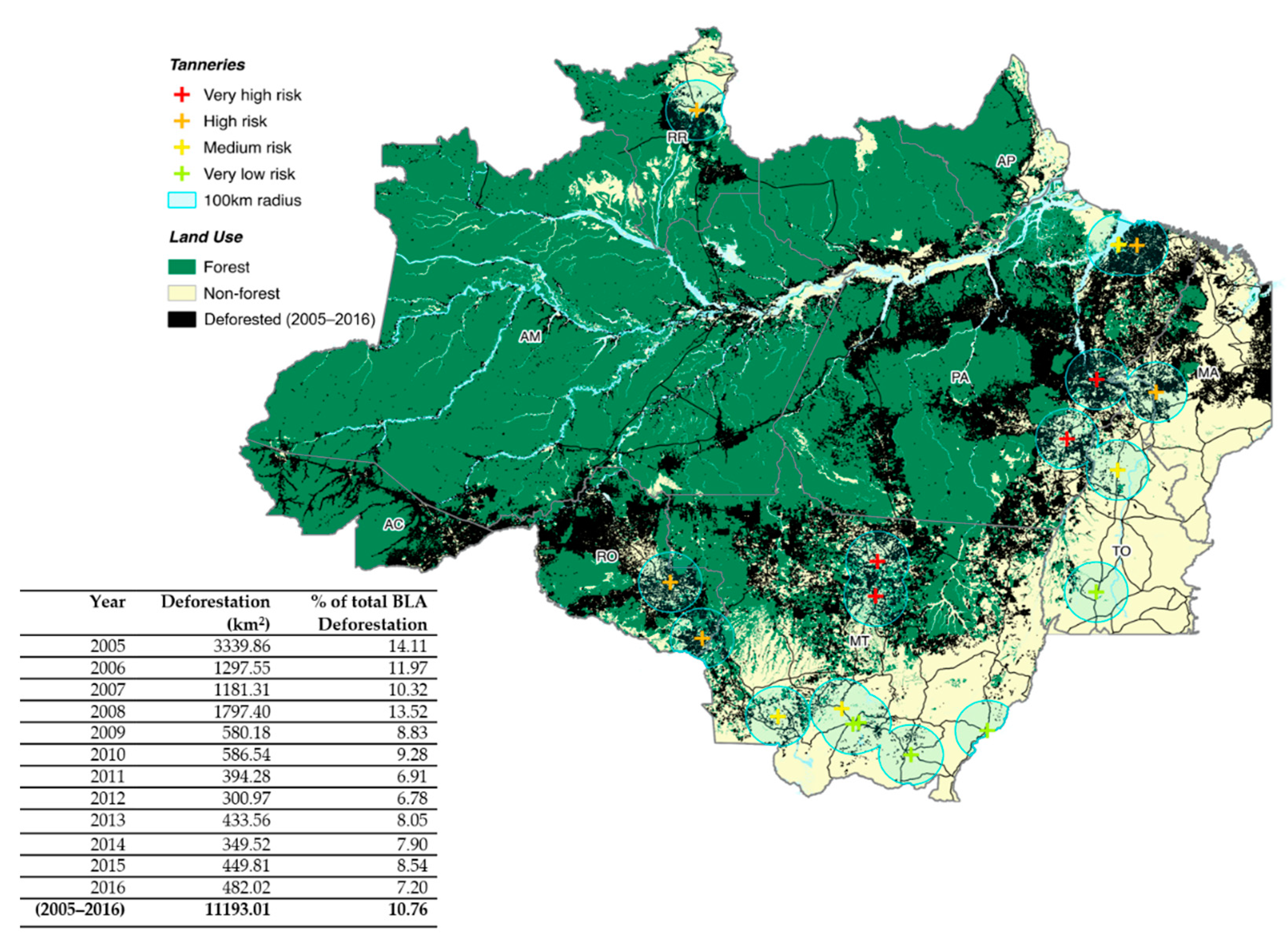

4.1. Dispersal of Deforestation Risk at Production Level. Farms and Slaughterhouses

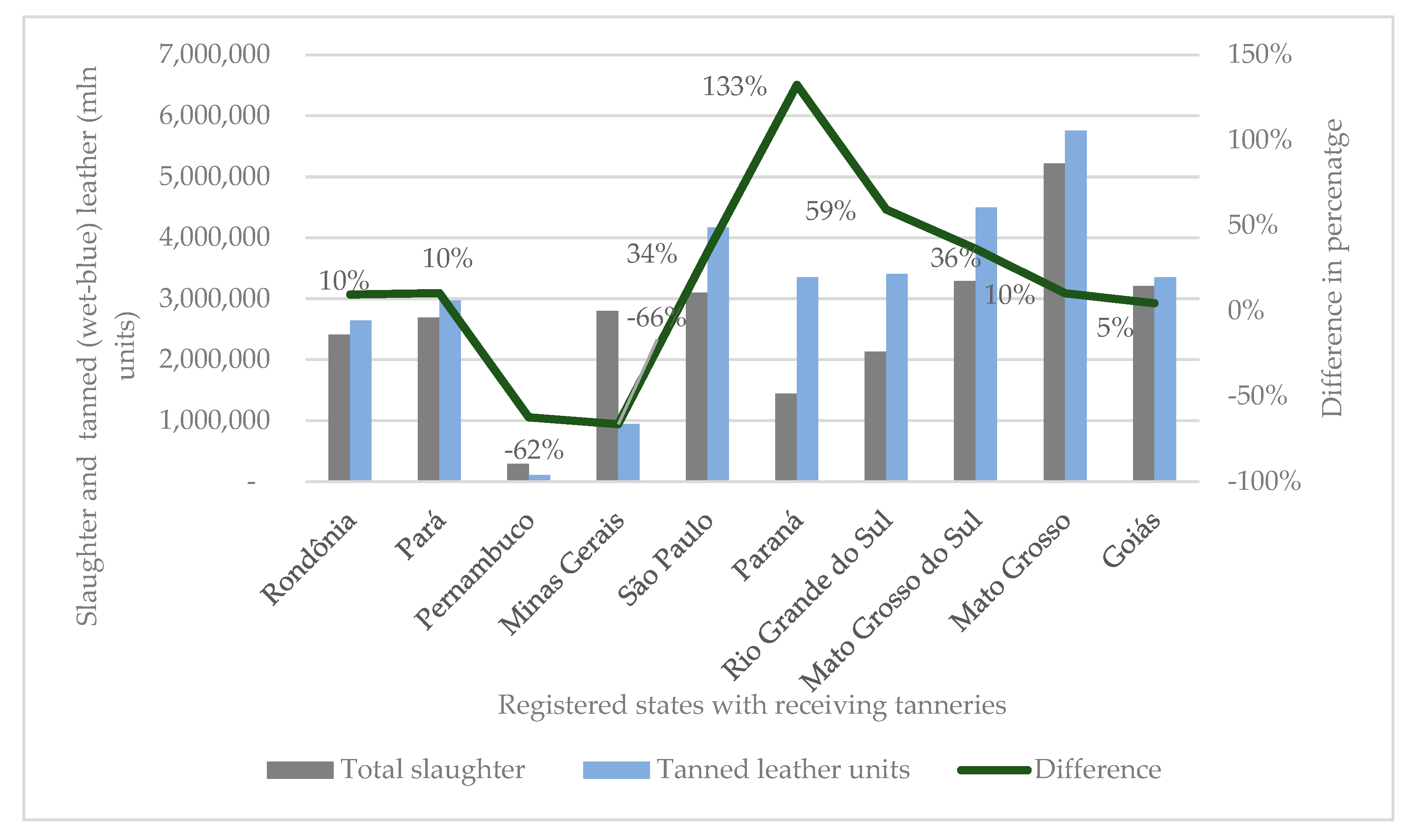

4.2. Dispersal of Deforestation Risk at Manufacturing Level: Leather Tanneries and Product Manufacturers

4.3. Dispersal of Deforestation Risk at Trade Level: Distribution and Retail

4.4. Dispersal of Deforestation Risk in Control Sector

5. Discussion

5.1. Deforestation As Embedded in All Economic Sectors

5.2. Dispersal of Deforestation Risk As a Systemic Quality

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

- -

- “Very high risk”: if Q3 ≤ DefArea ≤ Max

- -

- “High risk”: if Q2 ≤ DefArea < Q3

- -

- “Medium risk”: if Q1 ≤ DefArea < Q2

- -

- “Low risk”: if Min ≤ DefArea < Q1

Appendix C

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company | SIF Code | Deforestation 2005–2016 (km2) | Rank | State | City |

|---|---|---|---|---|---|

| Frigorfico Nosso Ltd.a | 386 | 4324.98 | 4 | RO | Porto Velho |

| T. M. Da Silva De Carvalho Frigorifico-Epp | 4686 | 3283.18 | 4 | PA | Novo Progresso |

| Frigol S. A. L | 4150 | 3124.02 | 4 | PA | São Félix do Xingu |

| Jbs S/A | 2011 | 2889.43 | 4 | MT | Juruena |

| Jbs S/A | 4393 | 2504.95 | 4 | MT | Vila Rica |

| Frigoari-Frigorifico Ariquemes S/A | 511 | 2297.57 | 4 | RO | Ariquemes |

| Jbs S/A | 1110 | 2207.89 | 4 | PA | Santana do Araguaia |

| Unibrax Alimentos E Participacoes S/A Ull | 3038 | 2073.91 | 4 | PA | Jacunda |

| Jbs S/A | 4149 | 1980.77 | 4 | RO | Porto Velho |

| Jbs S/A | 457 | 1976.36 | 4 | PA | Marabá |

| Frigorifico Fortefrigo Ltd.a | 372 | 1915.68 | 4 | PA | Paragominas |

| Jbs S/A | 3470 | 1837.84 | 4 | MT | Confresa |

| Jbs S/A | 3297 | 1723.31 | 4 | AC | Rio Branco |

| Frigorifico Redentor S/A. | 411 | 1716.93 | 4 | MT | Guarantã do Norte |

| Jbs S/A | 4323 | 1702.93 | 4 | MT | Matupá |

| Vale Grande Industria E Comercio De Alimentos S/A | 4490 | 1654.56 | 4 | MT | Matupá |

| Frigorifico Nosso Ltd.a | 4086 | 1537.98 | 4 | AC | Senador Guiomard |

| Jbs S/A | 4268 | 1489.89 | 4 | MT | Colíder |

| Jbs S/A | 4302 | 1475.95 | 4 | MT | Alta Floresta |

| Abatedouro De Bovinos Sampaio Ltd.a-Me | 2258 | 1412.57 | 4 | PA | Redenção |

| Agropam-Agricultura E Pecuaria Amazonas S/A | 2803 | 1388.68 | 4 | AM | Boca do Acre |

| Vale Grande Industria E Comercio De Alimentos S/A | 2937 | 1379.71 | 3 | MT | Nova Canaã Norte |

| Jbs S/A | 200 | 1332.41 | 3 | MT | Juara |

| Jbs S/A | 2350 | 1317.39 | 3 | PA | Tucumã |

| Mfb Marfrig Frigorficos Brasil S. A. | 1497 | 1304.80 | 3 | PA | Tucumã |

| Jbs S/A | 807 | 1280.55 | 3 | PA | Redenção |

| Masterboi Ltd.a | 2437 | 1247.85 | 3 | PA | São Geraldo do Araguaia |

| Frigorifico Rio Maria Ltd.a | 112 | 1245.37 | 3 | PA | Rio Maria |

| Mafripar Matadouro Frigorifico Paraense Ltd.a | 4413 | 1217.28 | 3 | PA | Xinguara |

| Xinguara Indstria E Comrcio S/A | 4398 | 1209.03 | 3 | PA | Xinguara |

| Frigorfico Vale Do Tocantins S/A | 2431 | 1194.13 | 3 | MA | Imperatriz |

| Mfb Marfrig Frigorficos Brasil S. A. | 3250 | 1118.22 | 3 | RO | Chupinguaia |

| Jbs S/A | 2942 | 1092.08 | 3 | MT | Juína |

| Frigomil Frigorfico Mil Ltd.a | 4510 | 1023.71 | 3 | RO | Pimenta Bueno |

| Jbs S. A. | 2880 | 1009.05 | 3 | RO | Pimenta Bueno |

| Vpr Brasil–Importações E Exportações Ltd.a | 3801 | 994.00 | 3 | MT | São José do Rio Claro |

| Matadouro Frigorifico Do Norte Ltd.a-Mafrinorte | 2801 | 986.39 | 3 | PA | Castanhal |

| Minerva Indstria E Comrcio De Alimentos S/A | 791 | 950.31 | 3 | RO | Rolim de Moura |

| Frigol S. A. | 2583 | 922.88 | 3 | PA | Água Azul do Norte |

| Companhia De Desenvolvimento De Roraima | 2040 | 921.74 | 3 | RR | Boa Vista |

| Industria De Carnes E Derivados Bonutt Ltd.a | 2852 | 906.52 | 3 | TO | Araguaína |

| Distriboi-Industria Comércio E Transporte De Carne Bovina Ltd.a | 4334 | 904.27 | 3 | RO | Rolim de Moura |

| Irmos Gonalves, Comrcio E Indstria Ltd.a | 2443 | 896.44 | 2 | RO | Jaru |

| Jbs S/A | 175 | 868.79 | 2 | RO | São Miguel do Guaporé |

| Matadouro E Frigorifico Extemo Norte Ltd.a | 4554 | 750.07 | 2 | PA | Castanhal |

| Distriboi-Ind, Com E Transporte De Carne Bovina | 4488 | 722.75 | 2 | RO | Cacoal |

| Frigoserve Cacoal Ltd.a | 1594 | 713.76 | 2 | RO | Cacoal |

| Jbs S/A | 4333 | 698.28 | 2 | RO | Vilhena |

| R. E. Ribeiro Soares-Me | 1367 | 682.17 | 2 | PA | Santarém |

| Frigorifico Tangar Ltd.a | 4267 | 503.79 | 2 | RO | Ji-Paraná |

| Distriboi-Industria, Comercio E Transporte De Carne Bovina Ltd.a | 4695 | 497.62 | 2 | RO | Ji-Paraná |

| Jbs S/A | 51 | 414.72 | 2 | MT | Pontes e Lacerda |

| L K J-Frigorifico Ltd.a | 723 | 406.87 | 2 | TO | Araguaína |

| Naturafrig Alimentos Ltd.a | 1811 | 406.25 | 2 | MT | Barra do Bugres |

| Minerva S. A. | 1940 | 397.50 | 2 | TO | Araguaína |

| Jbs S/A | 4001 | 389.31 | 2 | TO | Araguaína |

| Jbs S/A | 3000 | 378.82 | 2 | MT | Diamantino |

| Frigorifico Redentor S/A | 3826 | 370.82 | 2 | MT | Barra do Bugres |

| Comcarne Comercial De Carne Ltd.a | 1339 | 366.11 | 2 | MA | Igarapé do Meio |

| Marfrig Alimentos S/A | 1751 | 360.18 | 2 | MT | Tangará da Serra |

| Jbs S/A | 2979 | 336.02 | 2 | MT | Araputanga |

| Jbs S/A | 3031 | 319.93 | 2 | MT | São José dos Quatro Marcos |

| Brf-Brasil Foods S. A. | 2911 | 313.49 | 1 | MT | Mirassol d’Oeste |

| Masterboi Ltd.a | 860 | 263.49 | 1 | TO | Nova Olinda |

| Frigorifico 3m Ltd.a-Epp | 1777 | 213.97 | 1 | MT | Cáceres |

| Jbs S/A | 4121 | 88.39 | 1 | MT | Água Boa |

| Ifc International Food Company Ind De Alimentos S* | 2345 | 70.22 | 1 | MT | Nova Xavantina |

| Jbs S/A | 826 | 57.01 | 1 | MT | Cuiabá |

| Brf-Brasil Foods S. A. | 2015 | 56.32 | 1 | MT | Várzea Grande |

| Carnes Boi Branco Ltd.a | 2862 | 55.18 | 1 | MT | Várzea Grande |

| Frigovrzea Frigoriffico De Vrzea Grande Eireli | 4656 | 53.87 | 1 | MT | Várzea Grande |

| Pantaneira Ind. E Com De Carnes E Derivados Ltd.a | 1206 | 52.53 | 1 | MT | Várzea Grande |

| Agra Agroindustrial De Alimentos S/A | 3941 | 41.66 | 1 | MT | Rondonópolis |

| Mataboi Alimentos S. A. | 1886 | 40.59 | 1 | MT | Rondonópolis |

| Leandro Santos Carneiro Ltd.a-Epp | 3970 | 40.44 | 1 | MT | Rondonópolis |

| Jbs S/A | 2019 | 34.59 | 1 | MT | Pedra Preta |

| Marfrig Alimentos S/A | 2500 | 29.32 | 1 | MT | Paranatinga |

| Coop Dos Produtores De Carne E Derivados De Gurupi | 93 | 27.87 | 1 | TO | Gurupi |

| Jbs S/A | 42 | 6.01 | 1 | MT | Barra do Garças |

| Ind E Comer De Carnes E Derivados Boi Brasil | 1723 | 5.11 | 1 | TO | Alvorada |

| Hbc Ind E Com De Alimentos Imp E Exp Ltd.a | 1441 | 4.47 | 1 | TO | Araguaçu |

| Cesilio Agroindustrial Ltd.a | 4625 | 3.37 | 1 | TO | Paraíso do Tocantins |

| Plena Alimentos Ltd.a | 3215 | 2.30 | 1 | TO | Paraíso do Tocantins |

| Company | Deforestation 2005–2016 (km2) | Rank | State | City | LWG Certification |

|---|---|---|---|---|---|

| Jbs S/A Maraba | 2039.04 | 4 | PA | Marabá | Yes |

| Curtume Blubras | 1820.81 | 4 | MT | Sinop | Yes |

| Jbs Colider | 1522.88 | 4 | MT | Colíder | Yes |

| Durlicouros Indústria Comércio De Couros Exportação E Importação Ltd.a | 1223.11 | 4 | PA | Xinguará | Yes |

| Curtidora Ribeirãozinho Ltd.a | 1057.25 | 4 | MA | Governador Edison Lobão | No |

| Curtume Santa Maria Ltd.a | 1054.57 | 4 | MA | Governador Edison Lobão | Yes |

| Maranhão Indústria De Couro Ltd.a. | 1051.88 | 3 | MA | Governador Edison Lobão | Yes |

| Couros Boa Vista Ltd.a. | 976.97 | 3 | RR | Boa Vista | Yes |

| Mastercouros Comércio Importação E Exportação De Couros Ltd.a. | 961.14 | 3 | PA | Castanhal | Yes |

| Jbs S/A Colorado Do Oeste | 753.11 | 3 | RO | Colorado do Oeste | Yes |

| Jbs S/A Cacoal | 725.94 | 3 | RO | Cocal | Yes |

| Couro Do Norte Ltd.a | 601.07 | 2 | PA | Belém | No |

| Mj Novaes De Lima E Cia Ltd.a | 589.67 | 2 | PA | Belém | No |

| Curtume Araputangas S/A | 349.96 | 2 | MT | Araputanga | Yes |

| Curtidora Tocantins Ltd.a | 169.86 | 2 | TO | Colinas do Tocantins | Yes |

| Curtume Jangadas S/A | 65.55 | 2 | MT | Jangada | Yes |

| Viposa S/A | 61.80 | 1 | MT | Várzea Grande | Yes |

| Durlicourous Cuiba | 60.42 | 1 | MT | Cuiabá | Yes |

| Durlicouros Ind Com De Couros Ltd.a | 60.35 | 1 | MT | Cuiabá | Yes |

| Jbs Pedra Preta/Brazservice Wet Leather S/A | 36.63 | 1 | MT | Pedra Preta | Yes |

| Jbs S/A Gurupi | 36.08 | 1 | TO | Gurupi | No |

| Jbs S/A Barra Do Garcas | 6.01 | 1 | MT | Barra dos Garças | Yes |

References

- Curtis, P.G.; Slay, C.M.; Harris, N.L.; Tyukavina, A.; Hansen, M.C. Classifying drivers of global forest loss. Science 2018, 361, 1108–1111. [Google Scholar] [CrossRef] [PubMed]

- Arneth, A.; Barbosa, H.; Benton, T.; Intergovernmental Panel for Climate Change (IPCC). Summary for Policymakers. Climate Change and Land. An IPCC Special Report on Climate Change, Desertification, Land Degradation, Sustainable Land Management, Food Security, and Greenhouse Gas Fluxes in Terrestrial Ecosystems. 2019. Available online: https://www.ipcc.ch/site/assets/uploads/2019/08/Edited-SPM_Approved_Microsite_FINAL.pdf (accessed on 29 January 2022).

- Weisse, M.; Goldman, D.E. Just 7 Commodities Replaced an Area of Forest Twice the Size of Germany between 2001 and 2015. World Resour. Inst. Rev. 2021. Available online: https://www.wri.org/blog/2021/02/global-deforestation-agricultural-commodities?utm_medium=worldresources&utm_source=linkedin&utm_campaign=globalforestreview (accessed on 29 January 2022).

- Dummett, C.; Blundell, A.; Canby, K.; Wolosin, M.; Bodnar, E. Illicit Harvest, Complicit Goods. The State of Illegal Deforestation for Agriculture. Report Forest Trends. 2021. Available online: https://www.forest-trends.org/wp-content/uploads/2021/05/Illicit-Harvest-Complicit-Goods_rev.pdf (accessed on 29 January 2022).

- Lawson, S. Stolen Goods. In The EU’s Complicity in Illegal Tropical Deforestation; FERN: Gloucestershire, UK, 2015; ISBN 978-1-906607-40-1. Available online: https://www.fern.org/fileadmin/uploads/fern/Documents/Stolen%20Goods_EN_0.pdf (accessed on 29 January 2022).

- Henders, S.; Persson, U.M.; Kastner, T. Trading Forests: Land-Use Change and Carbon Emissions Embodied in Production and Exports of Forest-Risk Commodities. Environ. Res. Lett. 2015, 10, 125012. [Google Scholar] [CrossRef]

- Pendrill, F.; Persson, U.M.; Godar, J.; Kastner, T.; Moran, D.; Schmidt, S.; Wood, R. Agricultural and Forestry Trade Drives Large Share of Tropical Deforestation Emissions. Glob. Environ. Chang. 2019, 56, 1–10. [Google Scholar] [CrossRef]

- Gibbs, H.K.; Ruesch, A.S.; Achard, F.; Clayton, M.K.; Holmgren, P.; Ramankutty, N.; Foley, J.A. Tropical Forests Were the Primary Sources of New Agricultural Land in the 1980s and 1990s. Proc. Natl. Acad. Sci. USA 2010, 107, 16732–16737. [Google Scholar] [CrossRef] [Green Version]

- Mammadova, A.; Vasconcelos, A. Retailers Wake up to Deforestation Risk—Will Italy’s Leather Trade Raise Its Game? Global Canopy. 2019. Available online: https://medium.com/global-canopy/retailers-wake-up-to-deforestation-risk-will-italys-leather-trade-raise-its-game-4c8a8293175f (accessed on 29 January 2022).

- Garcia, T.M.; Rijk, G.; Piotrowski, M. Deforestation for Agricultural Commodities a Driver of Fires in Brazil, Indonesia in 2019. Chain Reaction Research, May. 2020. Available online: https://chainreactionresearch.com/wp-content/uploads/2020/05/Deforestation-driven20fires.pdf (accessed on 29 January 2022).

- Rudel, T.K.; Defries, R.; Asner, G.P.; Laurance, W.F. Changing Drivers of Deforestation and New Opportunities for Conservation. Conserv. Biol. 2009, 23, 1396–1405. [Google Scholar] [CrossRef]

- Boucher, D.; Elias, P.; Lininger, K.; May-Tobin, C.; Roquemore, S.; Saxon, E. The Root of the Problem: What’s Driving Tropical Deforestation Today? Union of Concerned Scientists: Cambridge, MA, USA, 2011. [Google Scholar]

- European Commission (EC). Guidance Document for the EU Timer Regulation. Brussels. 2016. Available online: https://ec.europa.eu/environment/forests/pdf/C_2016_755_F1_ACT_EN_V6_P1_831439.PDF (accessed on 29 January 2022).

- Mammadova, A.; Behagel, J.; Masiero, M. Making Deforestation Risk Visible. Discourses on Bovine Leather Supply Chain in Brazil. Geoforum 2020, 112, 85–95. [Google Scholar] [CrossRef]

- Zu Ermgassen, E.K.; Godar, J.; Lathuillière, M.J.; Löfgren, P.; Gardner, T.; Vasconcelos, A.; Meyfroidt, P. The Origin, Supply Chain, and Deforestation Risk of Brazil’s Beef Exports. Proc. Natl. Acad. Sci. USA 2020, 117, 31770–31779. [Google Scholar] [CrossRef]

- Pacheco, P.; Mo, K.; Dudley, N.; Shapiro, A.; Aguilar-Amuchastegui, N.; Ling, P.Y.; Anderson, C.; Marx, A. Deforestation Fronts: Drivers and Responses in a Changing World. WWF, Gland, Switzerland. 2021. Available online: https://wwfint.awsassets.panda.org/downloads/deforestation_fronts___drivers_and_responses_in_a_changing_world___full_report_1.pdf (accessed on 29 January 2022).

- Umunay, P.; Lujan, B.; Meyer, C.; Cobián, J. Trifecta of Success for Reducing Commodity-Driven Deforestation: Assessing the Intersection of REDD+ Programs, Jurisdictional Approaches, and Private Sector Commitments. Forests 2018, 9, 609. [Google Scholar] [CrossRef] [Green Version]

- Gibbs, H.K.; Munger, J.; L’Roe, J.; Barreto, P.; Pereira, R.; Christie, M.; Amaral, T.; Walker, N.F. Did Ranchers and Slaughterhouses Respond to Zero-Deforestation Agreements in the Brazilian Amazon? Conserv. Lett. 2016, 9, 32–42. [Google Scholar] [CrossRef]

- Barreto, P.; Marianno, B.; Valdiones, A.P.; Barreto, G. Os Frigoríficos vão Ajudar a Zerar o Desmatamento na Amazônia? Imazon and Instituto Centro da Vida. 2017. Available online: http://www.imazon.org.br/PDFimazon/Portugues/livros/Frigorificos%20e%20o%20desmatamento%20da%20Amaz%C3%B4nia.pdf (accessed on 29 January 2022).

- Greenpeace International. Destruction Certified. Report. 2021. Available online: https://www.greenpeace.org/international/publication/46812/destruction-certified/ (accessed on 29 January 2022).

- Brack, D. Illegal Logging and the Illegal Trade in Forest and Timber Products. Int. For. Rev. 2003, 5, 195–198. [Google Scholar] [CrossRef]

- Schloenhardt, A. The Illegal Trade in Timber and Timber Products in the Asia–Pacific Region. Australian Institute of Criminology. 2008. Available online: https://core.ac.uk/download/pdf/30687625.pdf (accessed on 29 January 2022).

- Miranda, J.; Börner, J.; Kalkuhl, M.; Soares-Filho, B. Land Speculation and Conservation Policy Leakage in Brazil. Environ. Res. Lett. 2019, 14, 045006. [Google Scholar] [CrossRef]

- Prager, A. Brazil’s Key Deforestation Drivers: Pasture, Cropland, Land Speculation. 2019. Mongabay, 19 March 2019. Available online: https://news.mongabay.com/2019/03/brazils-key-deforestation-drivers-pasture-cropland-land-speculation/ (accessed on 29 January 2022).

- Stabile, M.C.; Guimarães, A.L.; Silva, D.S.; Ribeiro, V.; Macedo, M.N.; Coe, M.T.; Pinto, E.; Moutinho, P.; Alencar, A. Solving Brazil’s Land Use Puzzle: Increasing Production and Slowing Amazon Deforestation. Land Use Policy 2019, 91, 104362. [Google Scholar] [CrossRef]

- Cuypers, D.; Geerken, T.; Gorissen, L.; Lust, A.; Peters, G.; Karstensen, J.; Prieler, S.; Fisher, G.; Hizsnyik, E.; Van Velthuizen, H. The Impact of EU Consumption on Deforestation: Comprehensive Analysis of the Impact of EU Consumption on Deforestation, Brussels: European Union (Technical Report—2013—063). 2013. Available online: http://ec.europa.eu/environment/forests/pdf/1.%20Report%20analysis%2of%20impact.pdf (accessed on 29 January 2022).

- Balogh, J.M.; Jámbor, A. The Environmental Impacts of Agricultural Trade: A Systematic Literature Review. Sustainability 2020, 12, 1152. [Google Scholar] [CrossRef] [Green Version]

- Heyl, K.; Ekardt, F.; Roos, P.; Stubenrauch, J.; Garske, B. Free Trade, Environment, Agriculture, and Plurilateral Treaties: The Ambivalent Example of Mercosur, CETA, and the EU–Vietnam Free Trade Agreement. Sustainability 2021, 13, 3153. [Google Scholar] [CrossRef]

- Balogh, J.M.; Mizik, T. Trade–Climate Nexus: A Systematic Review of the Literature. Economies 2021, 9, 99. [Google Scholar] [CrossRef]

- DeFries, R.S.; Rudel, T.; Uriarte, M.; Hansen, M. Deforestation Driven by Urban Population Growth and Agricultural Trade in the Twenty-First Century. Nat. Geosci. 2010, 3, 178–181. [Google Scholar] [CrossRef]

- Kissinger, G.M.; Herold, M.; De Sy, V. Drivers of Deforestation and Forest Degradation: A Synthesis Report for REDD+ Policymakers; Lexeme Consulting: Vancouver, Canada, 2012. [Google Scholar]

- Geist, H.J.; Lambin, E.F. Proximate Causes and Underlying Driving Forces of Tropical Deforestation Tropical Forests Are Disappearing as the Result of Many Pressures, Both Local and Regional, Acting in Various Combinations in Different Geographical Locations. BioScience 2002, 52, 143–150. [Google Scholar] [CrossRef]

- DeFries, R.; Herold, M.; Verchot, L.; Macedo, M.N.; Shimabukuro, Y. Export-Oriented Deforestation in Mato Grosso: Harbinger or Exception for Other Tropical Forests? Philos. Trans. R. Soc. B Biol. Sci. 2013, 368, 20120173. [Google Scholar] [CrossRef]

- Chang, J.; Symes, W.S.; Lim, F.; Carrasco, L.R. International Trade Causes Large Net Economic Losses in Tropical Countries via the Destruction of Ecosystem Services. Ambio 2016, 45, 387–397. [Google Scholar] [CrossRef] [Green Version]

- Clark, C. The Conditions of Economic Progress; MacMillan & Co.: London, UK, 1940. [Google Scholar]

- Kuznets, S. Toward a Theory of Economic Growth, with Reflections on the Economic Growth of Modern Nations; Norton Library: New York, NY, USA, 1968. [Google Scholar]

- Schafran, A.; McDonald, C.; Lopez Morales, E.; Akyelken, N.; Acuto, M. Replacing the Services Sector and Three-Sector Theory: Urbanization and Control as Economic Sectors. Reg. Studi. 2018, 52, 1708–1719. [Google Scholar] [CrossRef]

- Kim, H.D. Systems Thinking Tools: A User’s Reference Guide; Pegasus Communications, Inc.: Arcadia, CA, USA, 2000; ISBN 1-883823-02-1. Available online: https://thesystemsthinker.com/wp-content/uploads/2016/03/Systems-Archetypes-I-TRSA01_pk.pdf (accessed on 29 January 2022).

- Meadows, D. Leverage Points: Places to Intervene in a System; The Sustainability Institute: Hartland, WI, USA, 1999. [Google Scholar]

- Abson, D.J.; Fischer, J.; Leventon, J.; Newig, J.; Schomerus, T.; Vilsmaier, U.; Von Wehrden, H.; Abernethy, P.; Ives, C.D.; Jager, N.W.; et al. Leverage Points for Sustainability Transformation. Ambio 2017, 46, 30–39. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Blokland, P.; Reniers, G. Safety Science, a Systems Thinking Perspective: From Events to Mental Models and Sustainable Safety. Sustainability 2020, 12, 5164. [Google Scholar] [CrossRef]

- Nepstad, D.; McGrath, D.; Stickler, C.; Alencar, A.; Azevedo, A. Slowing Amazon Deforestation through Public Policy and Interventions in Beef and Soy Supply Chains. Science 2014, 344, 1118–1123. [Google Scholar] [CrossRef] [PubMed]

- Weber, A.K.; Partzsch, L. Barking up the Right Tree? NGOs and Corporate Power for Deforestation-Free Supply Chains. Sustainability 2018, 10, 3869. [Google Scholar] [CrossRef] [Green Version]

- Seuring, S.; Müller, M. From a Literature Review to a Conceptual Framework for Sustainable Supply Chain Management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Håkansson, H.; Persson, G. Supply Chain Management: The Logic of Supply Chains and Networks. Int. J. Logist. Manag. 2004, 15, 11–26. [Google Scholar] [CrossRef]

- Meijer, K.S. A Comparative Analysis of the Effectiveness of Four Supply Chain Initiatives to Reduce Deforestation. Trop. Conserv. Sci. 2015, 8, 583–597. [Google Scholar] [CrossRef]

- Lundy, M.; Amrein, A.; Hurtado, J.J.; Becx, G.; Zamierowski, N.; Rodriguez, F.; Mosquera, E.E. LINK Methodology: A Participatory Guide to Business Models That Link Smallholders to Markets. Version 2.0. Cali, Colombia: International Center for Tropical Agriculture. 2014. Available online: http://hdl.handle.net/10568/49606 (accessed on 29 January 2022).

- Newton, P.; Benzeev, R. The Role of Zero-Deforestation Commitments in Protecting and Enhancing Rural Livelihoods. Curr. Opin. Environ. Sustain. 2018, 32, 126–133. [Google Scholar] [CrossRef]

- Walker, N.; Patel, S.; Kalif, K. From Amazon Pasture to the High Street: Deforestation and the Brazilian Cattle Product Supply Chain. Trop. Conserv. Sci. 2013, 6, 446–467. [Google Scholar] [CrossRef] [Green Version]

- TRASE. How Trase Assesses ‘Commodity Deforestation’ and ‘Commodity Deforestation Risk’. Resources. 2020. Available online: http://resources.trase.earth/documents/data_methods/Trase_deforestation_risk_method_final%20Sept%202020.pdf (accessed on 29 January 2022).

- Malterud, K.; Siersma, V.D.; Guassora, A.D. Sample Size in Qualitative Interview Studies: Guided by Information Power. Qual. Health Res. 2016, 26, 1753–1760. [Google Scholar] [CrossRef]

- European Commission (EC). Policy. Accessing Markets. Investments. 2021. Available online: https://ec.europa.eu/trade/policy/accessing-markets/investment/ (accessed on 29 January 2022).

- Ferreira, S. Deforestation, Property Rights, and International Trade. Land Econ. 2004, 80, 174–193. [Google Scholar] [CrossRef]

- Faria, W.R.; Almeida, A.N. Relationship between Openness to Trade and Deforestation: Empirical Evidence from the Brazilian Amazon. Ecol. Econ. 2016, 121, 85–97. [Google Scholar] [CrossRef]

- Schmitz, C.; Kreidenweis, U.; Lotze-Campen, H.; Popp, A.; Krause, M.; Dietrich, J.P.; Müller, C. Agricultural Trade and Tropical Deforestation: Interactions and Related Policy Options. Region. Environ. Chang. 2015, 15, 1757–1772. [Google Scholar] [CrossRef]

- Abman, R.; Lundberg, C. Does Free Trade Increase Deforestation? The Effects of Regional Trade Agreements. J. Assoc. Environ. Resour. Econ. 2020, 7, 35–72. [Google Scholar] [CrossRef]

- FERN. Eu-Mercosur Deal Sacrifices Forests and Rights on the Altar of Trade. 2019. Available online: https://www.fern.org/news-resources/eu-mercosur-deal-sacrifices-forests-and-rights-on-the-altar-of-trade-1986/ (accessed on 29 January 2022).

- Kehoe, L.; Reis, T.; Virah-Sawmy, M.; Balmford, A.; Kuemmerle, T. Make EU Trade with Brazil Sustainable. Science 2019, 364, 341–342. Available online: https://www.researchgate.net/publication/332665154_Make_EU_trade_with_Brazil_sustainable (accessed on 29 January 2022). [CrossRef] [Green Version]

- Amazon Institute of People and the Environment (IMAZON). Is the EU-MERCOSUR trade agreement deforestation-proof?/Instituto do Homem e Meio Ambiente da Amazônia—Belém, PA. 2020. Available online: https://imazon.org.br/wp-content/uploads/2020/11/mercosulue_en_imazon.pdf (accessed on 29 January 2022).

- Arima, E.; Barreto, P.; Taheripour, F.; Aguiar, A. Dynamic Amazonia: The EU–Mercosur Trade Agreement and Deforestation. Land 2021, 10, 1243. [Google Scholar] [CrossRef]

- Follador, M.; Soares-Filho, B.S.; Philippidis, G.; Davis, J.L.; de Oliveira, A.R.; Rajão, R. Brazil’s Sugarcane Embitters the EU-Mercosur Trade Talks. Sci. Rep. 2021, 11, 1–10. [Google Scholar]

- European Commission (EC). Eu Market Access Flash Note. Brazil Removes Export Duties on Hides and Skins. 2018. Available online: https://trade.ec.europa.eu/doclib/docs/2018/october/tradoc_157430.pdf (accessed on 29 January 2022).

- Global Canopy. Time for Change: Delivering Deforestation-Free Supply Chains. Forests 500. 2021. Available online: https://forest500.org/sites/default/files/forest500_2021report.pdf (accessed on 29 January 2022).

- Baldock, C.; McLuckie, M.; Mosnier, F.; Willis, J. Exchange-Traded Deforestation. 2020. Available online: https://planet-tracker.org/tracker-programmes/food-and-land-use/food-and-agriculture/ (accessed on 29 January 2022).

- NYDF Assessment Partners. Balancing Forests and Development: Addressing Infrastructure and Extractive Industries, Promoting Sustainable Livelihoods. Climate Focus (Coordinator and Editor). 2020. Available online: www.forestdeclaration.org (accessed on 29 January 2022).

- United Nations Framework Convention on Climate Change (UNFCC). Glasgow Leaders’ Declaration on Forests and Land Use. 2021. Available online: https://ukcop26.org/glasgow-leaders-declaration-on-forests-and-land-use/ (accessed on 29 January 2022).

- Leblois, A.; Damette, O.; Wolfersberger, J. What Has Driven Deforestation in Developing Countries Since the 2000s? Evidence from New Remote-Sensing Data. World Dev. 2017, 92, 82–102. [Google Scholar] [CrossRef]

- Pendrill, F.; Persson, U.M.; Godar, J.; Kastner, T. Deforestation Displaced: Trade in Forest-Risk Commodities and the Prospects for a Global Forest Transition. Environ. Res. Lett. 2019, 14, 055003. [Google Scholar] [CrossRef]

- Richards, P.D.; Walker, R.T.; Arima, E.Y. Spatially Complex Land Change: The Indirect Effect of Brazil’s Agricultural Sector on Land Use in Amazonia. Glob. Environ. Chang. 2014, 29, 1–9. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- dos Reis, T.N.; Meyfroidt, P.; zu Ermgassen, E.K.; West, C.; Gardner, T.; Bager, S.; Croft, S.; Lathuilliere, M.J.; Godar, J. Understanding the Stickiness of Commodity Supply Chains Is Key to Improving Their Sustainability. One Earth 2020, 3, 100–115. [Google Scholar] [CrossRef]

- Fearnside, P.M. Soybean Cultivation as a Threat to the Environment in Brazil. Environ. Conserv. 2001, 28, 23–38. [Google Scholar] [CrossRef] [Green Version]

- Fearnside, P.M. Deforestation in Amazonia. In Encyclopedia of Earth; Cleveland, C.J., Ed.; Environmental Information Coalition, National Council of Science and the Environment: Washington, DC, USA, 2007. [Google Scholar]

- Morton, D.C.; DeFries, R.S.; Shimabukuro, Y.E.; Anderson, L.O.; Arai, E.; del Bon Espirito-Santo, F.; Freitas, R.; Morisette, J. Cropland Expansion Changes Deforestation Dynamics in the Southern Brazilian Amazon. Proc. Natl. Acad. Sci. USA 2006, 103, 14637–14641. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Greenpeace International. Eating up the Amazon. 2006. Available online: https://www.greenpeace.org/usa/wp-content/uploads/legacy/Global/usa/report/2010/2/eating-up-the-amazon.pdf (accessed on 29 January 2022).

- Walker, R.; Defries, R.; Vera-Diaz, M.D.C.; Shimabukuro, Y.; Venturieri, A. The Expansion of Intensive Agriculture and Ranching in Brazilian Amazonia. Amazonia and Global Change. 2009, pp. 61–81. Available online: https://ui.adsabs.harvard.edu/abs/2009GMS...186...61W/abstract (accessed on 29 January 2022).

- Gibbs, H.K.; Rausch, L.; Munger, J.; Schelly, I.; Morton, D.C. Brazil’s Soy Moratorium. Science 2015, 347, 377–378. [Google Scholar] [CrossRef]

- Godar, J.; Suavet, C.; Gardner, T.A.; Dawkins, E.; Meyfroidt, P. Balancing Detail and Scale in Assessing Transparency to Improve the Governance of Agricultural Commodity Supply Chains. Environ. Res. Lett. 2016, 11, 35015. [Google Scholar] [CrossRef] [Green Version]

- Junior, C.S.; Lima, M. Soy Moratorium in Mato Grosso: Deforestation Undermines the Agreement. Land Use Policy 2018, 71, 540–542. [Google Scholar]

- UN Comtrade Database. Available online: https://comtrade.un.org/ (accessed on 29 January 2022).

- TRASE. Trase Yearbook 2018. Assessing Deforestation Risk in Brazilian Soy Exports. 2018. Available online: https://yearbook2018.trase.earth/chapter5/ (accessed on 29 January 2022).

- Kröger, M. Extractivisms, Existences and Extinctions: Monoculture Plantations and Amazon Deforestation; Taylor & Francis: Abingdon, UK, 2022; p. 176. [Google Scholar]

- Global Witness. Money to Burn. More than 300 Banks and Investors Back Six of the World’s Most Harmful Agribusinesses to the Tune of $44bn; Global Witness: Washington, DC, USA, 2019; Available online: https://www.globalwitness.org/en/campaigns/forests/money-to-burn-how-iconic-banks-and-investors-fund-the-destruction-of-the-worlds-largest-rainforests/ (accessed on 29 January 2022).

- Orth, C.F.; Rios dos Santos, C.C.; Celeste, I.I.; de Melo, R.G.; Gusman, T.P. Bilateral Investment Map. Brazil-European Union. 2017. Available online: https://eeas.europa.eu/sites/default/files/mapa_de_investimentos_brasil-ue_eng_final_0.pdf (accessed on 29 January 2022).

- Central Bank of Brazil. Foreign Direct Investment Report. 2018. Available online: https://www.bcb.gov.br/Rex/CensoCE/ingl/FDIReport2016.pdf (accessed on 29 January 2022).

- European Commission (EC). Trade. Policy. Countries and Regions. Brazil. 2019. Available online: https://ec.europa.eu/trade/policy/countries-and-regions/countries/brazil/ (accessed on 29 January 2022).

- Slob, B.; Rijk, G.; Piotrowski, M. JBS, Marfrig, and Minerva: Material Financial Risk from Deforestation in Beef Supply Chains. Chain Reaction Research. 2020. Available online: https://chainreactionresearch.com/wp-content/uploads/2020/12/JBS-Marfrig-and-Minerva-Material-financial-risk-from-deforestation-in-beef-supply-chains-4.pdf (accessed on 29 January 2022).

- OECD/FAO. OECD-FAO Agricultural Outlook 2020–2029. 2020. Available online: https://www.oecd-ilibrary.org/ (accessed on 29 January 2022).

- European Commission. The EU Leather Industry. 2021. Available online: https://ec.europa.eu/growth/sectors/fashion/leather-industry/eu-leather-industry_en (accessed on 29 January 2022).

- Andreoni, M.; Tabuchi, H.; Sun, A. How Americans’ Appetite for Leather in Luxury SUVs Worsens Amazon Deforestation. New York Times. 17 November 2021. Available online: https://www.nytimes.com/2021/11/17/climate/leather-seats-cars-rainforest.html (accessed on 29 January 2022).

- Faminow, M.D. Cattle, Deforestation and Development in the Amazon: An Economic, Agronomic and Environmental Perspective; Cab International: New York, NY, USA, 1998; Volume 253. [Google Scholar]

- Kaimowitz, D.; Mertens, B.; Wunder, S.; Pacheco, P. Hamburger Connection Fuels Amazon Destruction; Center for International Forest Research: Bangor, Indonesia, 2004; pp. 1–10. [Google Scholar]

- Pereira, R.; Simmons, C.S.; Walker, R. Smallholders, Agrarian Reform, and Globalization in the Brazilian Amazon: Cattle versus the Environment. Land 2016, 5, 24. [Google Scholar] [CrossRef]

- Zu Ermgassen, E.K.; Ayre, B.; Godar, J.; Lima, M.G.B.; Bauch, S.; Garrett, R.; Green, J.; Lathuillière, M.J.; Löfgren, P.; MacFarquhar, C.; et al. Using Supply Chain Data to Monitor Zero Deforestation Commitments: An Assessment of Progress in the Brazilian Soy Sector. Environ. Res. Lett. 2020, 15, 035003. [Google Scholar] [CrossRef]

- MapBiomas. Map and Data, Land Use Change 1985–2017. 2018. Available online: http://mapbiomas.org/map#coverage (accessed on 29 January 2022).

- Moutinho, P.; Guerra, R.; Azevedo-Ramos, C. Achieving Zero Deforestation in the Brazilian Amazon: What Is Missing? Elem. Sci. Anthr. 2016, 4, 000125. [Google Scholar] [CrossRef] [Green Version]

- INPE/PRODES. Available online: http://www.obt.inpe.br/OBT/assuntos/programas/amazonia/prodes (accessed on 29 January 2022).

- Locatelli, P.; Aranha, A. JBS Compra Gado de Áreas Desmatadas Ilegalmente e Leva Multa de R$24 Milhões. Reporter Brasil. 2017. Available online: https://reporterbrasil.org.br/2017/03/jbs-compra-gado-de-areas-desmatadas-ilegalmente-e-leva-multa-de-r24-milhoes/ (accessed on 29 January 2022).

- Anonymous; Belém, Para, Brazil. Personal Communication, 24 May 2018.

- Barreto, P.; Pereira, R.; Baima, S. Os Potenciais Impactos de Fiscalizar Frigoríficos sem Compromissos contra o Desmatamento. Imazon: Belém, Brazil, 2018. [Google Scholar]

- Alix-Garcia, J.; Gibbs, H.K. Forest Conservation Effects of Brazil’s Zero Deforestation Cattle Agreements Undermined by Leakage. Glob. Environ. Chang. 2017, 47, 201–217. [Google Scholar] [CrossRef]

- Ministério Público Federal (MPF) do Brazil. Procuradoria da República no Pará. Auditorias Confirmam e Aprimoram Avanços no Controle da Origem da Carne no Pará. 2018. Available online: http://www.mpf.mp.br/pa/sala-de-imprensa/noticias-pa/auditorias-confirmam-e-aprimoram-avancos-no-controle-da-origem-da-carne-no-para (accessed on 29 January 2022).

- Mengardo, B. TACs da Carne no Pará Expõem Limitações do MP na Área Ambiental, Notícia de 10/05/2018. Jota/((o)) Eco. 2018. Available online: https://www.jota.info/especiais/tacs-da-carne-no-para-expoem-limitacoes-do-mp-na-area-ambiental-10052018 (accessed on 29 January 2022).

- Ministério Público Federal (MPF) do Brasil. Ações Penais—Operação Arquimedes. 2019. Available online: http://www.mpf.mp.br/grandes-casos/operacao-arquimedes/atuacao-do-mpf/acoes-penais (accessed on 29 January 2022).

- Investopedia. What Is Vertical Integration? 2021. Available online: https://www.investopedia.com/terms/v/verticalintegration.asp (accessed on 29 January 2022).

- Brazilian Leather Guide (BLG). Available online: http://www.guiabrasileirodocouro.com.br/ (accessed on 29 January 2022).

- The Centre for the Brazilian Tanning Industry (CICB). Available online: http://www.cicb.org.br/cicb (accessed on 29 January 2022).

- The Ministry of Agriculture, Cattle and Supply (MAPA). SIF Database. Available online: http://sigsif.agricultura.gov.br/sigsif_cons/%21ap_estabelec_nacional_rep (accessed on 29 January 2022).

- Leather Working Group (LWG). Available online: https://www.leatherworkinggroup.com/leather-manufacturers-and-traders/leather-manufacturers/our-rated-members?country=Brazil (accessed on 29 January 2022).

- Sartorato, S.F.C. Is Leather a Forest-Risky Commodity? Exploring Embodied Deforestation in the Brazilian Leather. Master Thesis, University of Padova, Padova, Italy, 2017. [Google Scholar]

- Textile Exchange. Leather Supply Chain Mapping and Traceability Guidelines. 2021. Available online: https://textileexchange.org/wp-content/uploads/2021/02/LIA-261-V0.1-Leather-Supply-Chain-Mapping-and-Traceability-Guidelines.pdf (accessed on 29 January 2022).

- Anonymous; Maraba, Para, Brazil. Personal Communication, 23 May 2018.

- Anonymous; Cuiaba, Mato Grosso. Personal Communication, 7 June 2018.

- Instituto Brasileiro de Geografia e Estatística (IBGE) (Brazilian Institute of Geography and Statistics). Sistema IBGE de Recuperação Automática—SIDRA. Pesquisa do Couro e Abate de Animais. 2018. Available online: https://sidra.ibge.gov.br/home/abate/brasil (accessed on 29 January 2022).

- Global Forest Watch (GFW). Available online: http://data.globalforestwatch.org/ (accessed on 29 January 2022).

- UFG—Image Processing Laboratory and Geo-LAPIG. Available online: http://maps.lapig.iesa.ufg.br/lapig.html (accessed on 29 January 2022).

- SECEX/MDIC. Available online: http://comexstat.mdic.gov.br/en/geral (accessed on 29 January 2022).

- Buljan, J.; Kráľ, I. The Framework for Sustainable Leather Manufacture, 2nd ed.; United Nations Industrial Development Organization (UNIDO), 2019; Available online: https://leatherpanel.org/sites/default/files/publications-attachments/the_framework_for_sustainable_leather_manufacturing_2nd_edition_2019_f.pdf#page=156 (accessed on 29 January 2022).

- Centro das Indústrias de Curtumes do Brasil (CICB). Sobre o Couro. 2021. Available online: http://www.cicb.org.br/cicb/sobre-couro (accessed on 29 January 2022).

- Mammadova, A.; Masiero, M.; Pettenella, D. Embedded Deforestation: The Case Study of the Brazilian–Italian Bovine Leather Trade. Forests 2020, 11, 472. [Google Scholar] [CrossRef] [Green Version]

- Institute of Quality Certification for the Leather Sector (ICEC). Certifications. Made in Italy of Leather Production. 2019. Available online: http://www.icec.it/en/certifications/product-economic-sustainability/made-in-italy-of-leather-production (accessed on 11 February 2020).

- Anonymous. Bresaola Della Valtellina. Raw Material. 2021. Available online: https://www.bresaolavaltellina.it/en/raw-material/ (accessed on 29 January 2022).

- De Rosa-Giglio, P.; Fontanella, A.; Gonzalez-Quijano, G.; Ioannidis, I.; Nucci, B.; Brugnoli, F. Product Environmental Footprint Category Rules (PEFCR). Leather. Final Version. 2018. Available online: https://ec.europa.eu/environment/eussd/smgp/pdf/PEFCR_leather.pdf (accessed on 29 January 2022).

- Faggin, J.; Drost, S.; Garcia, M. Driving Deforestation: The European Automotive Industry’s Contribution to Deforestation in Brazil. Report Commissioned by Rainforest Foundation Norway. Aidenvironment. 2021. Available online: https://www.regnskog.no/uploads/documents/Driving-Deforestation-A7.pdf (accessed on 29 January 2022).

- Italian Tanners Association (UNIC). Tales of Italian Leather. Sustainability Report 2017. 2017. Available online: http://s.unic.it/5/report-en.html#20-21 (accessed on 29 July 2019).

- Lin, L.; Sills, E.; Cheshire, H. Targeting Areas for Reducing Emissions from Deforestation and Forest Degradation (REDD+) Projects in Tanzania. Glob. Environ. Chang. 2014, 24, 277–286. [Google Scholar] [CrossRef]

- Di Lallo, G.; Mundhenk, P.; Zamora López, S.; Marchetti, M.; Köhl, M. REDD+: Quick Assessment of Deforestation Risk Based on Available Data. Forests 2017, 8, 29. [Google Scholar] [CrossRef]

- Ordway, E.M.; Asner, G.P.; Lambin, E.F. Deforestation Risk Due to Commodity Crop Expansion in Sub-Saharan Africa. Environ. Res. Lett. 2017, 12, 044015. [Google Scholar] [CrossRef]

- Global Forest Watch (GFW). Global Forest Watch Pro Online Management Tool. 2021. Available online: https://pro.globalforestwatch.org/about (accessed on 29 January 2022).

- Gaveau, D.L.; Locatelli, B.; Salim, M.A.; Yaen, H.; Pacheco, P.; Sheil, D. Rise and Fall of Forest Loss and Industrial Plantations in Borneo (2000–2017). Conserv. Lett. 2019, 12, e12622. [Google Scholar] [CrossRef]

- Godar, J.; Persson, U.M.; Tizado, E.J.; Meyfroidt, P. Towards more Accurate and Policy Relevant Footprint Analyses: Tracing Fine-Scale Socio-Environmental Impacts of Production to Consumption. Ecol. Econ. 2015, 112, 25–35. [Google Scholar] [CrossRef]

- Pelenc, J.; Ballet, J. Strong Sustainability, Critical Natural Capital and the Capability Approach. Ecol. Econ. 2015, 112, 36–44. [Google Scholar] [CrossRef] [Green Version]

- Institute for European Environmental Policy (IEEP). IEEP’s Response to the Public Consultation ‘Deforestation and Forest Degradation: Reducing the Impact of Products Placed on the EU Market’. IEEP, December. 2020. Available online: https://ieep.eu/uploads/articles/attachments/9a45e14a-e483-43c1-9be3-79fc3da940d9/IEEP's%20response%20to%20deforestation%20and%20forest%20degradation%20public%20consultation%20(Dec%202020).pdf?v=63774841886 (accessed on 29 January 2022).

- European Commission (EC). Proposal for a Regulation on Deforestation-Free Products. European Commission, November. 2021. Available online: https://ec.europa.eu/environment/publications/proposal-regulation-deforestation-free-products_en (accessed on 29 January 2022).

- Ingram, V.; Behagel, J.; Mammadova, A.; Verschuur, X. The Outcomes of Deforestation-Free Commodity Value Chain Approaches; Summary Discussion Paper; Wageningen University & Research: Wageningen, The Netherlands, 2020. [Google Scholar]

- Gupta, A.; Lövbrand, E.; Turnhout, E.; Vijge, M.J. In Pursuit of Carbon Accountability: The Politics of REDD+ Measuring, Reporting and Verification Systems. Curr. Opin. Environ. Sustain. 2012, 4, 726–731. [Google Scholar] [CrossRef]

- McDermott, C.L. REDDuced: From sustainability to legality to units of carbon—The search for common interests in international forest governance. Environ. Sci. Policy 2014, 35, 12–19. [Google Scholar] [CrossRef]

- Humphreys, D. Logjam—Deforestation and the Crisis of Global Governance; Earthscan: London, UK, 2006. [Google Scholar]

- Susanti, A.; Maryudi, A. Development Narratives, Notions of Forest Crisis, and Boom of Oil Palm Plantations in Indonesia. For. Policy Econ. 2016, 73, 130–139. [Google Scholar] [CrossRef]

- Weatherley-Singh, J.; Gupta, A. “Embodied Deforestation” as a New EU Policy Debate to Tackle Tropical Forest Loss: Assessing Implications for REDD+ Performance. Forests 2018, 9, 751. [Google Scholar] [CrossRef] [Green Version]

- Derous, M.; Verhaeghe, E. When P Stands for Politics. The Role of the EU in the VPAs: A Research Agenda. For. Policy Econ. 2019, 101, 81–87. [Google Scholar] [CrossRef]

- Lima, M.G.B.; Harring, N.; Jagers, S.C.; Löfgren, Å.; Persson, M.; Sjöstedt, M.; Brülde, B.; Langlet, D.; Steffen, W.; Alpízar, F. Large-Scale Collective Action to Avoid an Amazon Tipping Point-Key Actors and Interventions. Curr. Res. Environ. Sustain. 2021, 3, 100048. [Google Scholar] [CrossRef]

- Fischer, J.; Riechers, M. A leverage points perspective on sustainability. People Nat. 2019, 1, 115–120. [Google Scholar] [CrossRef] [Green Version]

- Picheta, R. Timberland, Vans and the North Face Will Stop Using Brazilian Leather in Amazon Protest. CNN Business. 30 August 2019. Available online: https://edition.cnn.com/2019/08/30/business/vf-corp-brazilian-leather-amazon-scli-intl/index.html (accessed on 29 January 2022).

- CEPEA. Available online: http://www.cepea.esalq.usp.br/br (accessed on 29 January 2022).

- Anonymous; Sao Paulo, Brazil. Personal communication, 11 May 2018.

- Goddard, L. Brazilian Beef: Inside the Supply Chain. Global Witness. 2020. Available online: https://www.globalwitness.org/en/blog/brazilian-beef-supply-chain/ (accessed on 29 January 2022).

- SIDRA. Available online: https://sidra.ibge.gov.br/home/pnadcm (accessed on 29 January 2022).

- IBGE. Available online: https://www.ibge.gov.br/estatisticas/economicas/agricultura-e-pecuaria.html (accessed on 29 January 2022).

- The Ministry of Agriculture, Cattle and Supply (MAPA). Dados de Rebanho Bovino e Bubalino no Brasil—2017. Obtained 08/08/2018. 2018. Available online: http://www.agricultura.gov.br/assuntos/sanidade-animal-e-vegetal/saude-animal/programas-de-saude-animal/febre-aftosa/documentos-febre-aftosa/DadosderebanhobovinoebubalinodoBrasil_2017.pdf (accessed on 29 January 2022).

- TRASE. Available online: https://www.trase.earth/ (accessed on 29 January 2022).

- da Silva Frasão, B.; de Mattos Nascimento MR, B.; de Oliveira Costa, H.C.; Morais, H.R.; de Fátima Carrijo, K.; Biase, N.G. Quantity, Location, and Description of Bruises in Beef Cattle Slaughtered under Sanitary Inspection. Acta Sci. Vet. 2014, 42, 1192. [Google Scholar]

- Bertoloni, W.; Silva, J.L.; de Abreu, J.S.; Andreolla, D.L. Bem-Estar e Taxa de Hematomas de Bovinos Transportados em Diferentes Distâncias e Modelos de Carroceria no Estado do Mato Grosso—Brasil. Rev. Bras. Saúde Produção Anim. 2012, 13, 850–859. [Google Scholar] [CrossRef]

- Neto, A.P.; Zanco, N.; Lolatto, D.C.J.; Moreira, P.S.A.; Dromboski, T. Perdas Econômicas Ocasionadas por Lesões em Carcaças de Bovinos Abatidos em Matadouro-Frigorífico do Norte de Mato Grosso. Pesquisa Vet. Bras. 2015, 35, 324–328. [Google Scholar] [CrossRef]

- Warris, P.D.; Brown, S.N.; Knowles, T.G.; Kestin, S.C.; Edwards, J.E.; Dolan, S.K.; Philips, A.J. Effects on Cattle of Transport by Road for up 15 Hours. Vet. Rec. 1995, 136, 319–323. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mammadova, A.; Behagel, J.; Masiero, M.; Pettenella, D. Deforestation as a Systemic Risk: The Case of Brazilian Bovine Leather. Forests 2022, 13, 233. https://doi.org/10.3390/f13020233

Mammadova A, Behagel J, Masiero M, Pettenella D. Deforestation as a Systemic Risk: The Case of Brazilian Bovine Leather. Forests. 2022; 13(2):233. https://doi.org/10.3390/f13020233

Chicago/Turabian StyleMammadova, Aynur, Jelle Behagel, Mauro Masiero, and Davide Pettenella. 2022. "Deforestation as a Systemic Risk: The Case of Brazilian Bovine Leather" Forests 13, no. 2: 233. https://doi.org/10.3390/f13020233

APA StyleMammadova, A., Behagel, J., Masiero, M., & Pettenella, D. (2022). Deforestation as a Systemic Risk: The Case of Brazilian Bovine Leather. Forests, 13(2), 233. https://doi.org/10.3390/f13020233