Capacity Market and Investments in Power Generations: Risk-Averse Decision-Making of Power Producer

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

1.1. Background

1.2. Literature Review

1.3. Significance and Contribution

2. Methodology

2.1. Investment Problem to the Power Generator without the Capacity Market

2.2. Investment Problem to the Power Generator with the Capacity Market

3. Comparison of Optimal Investment Policies

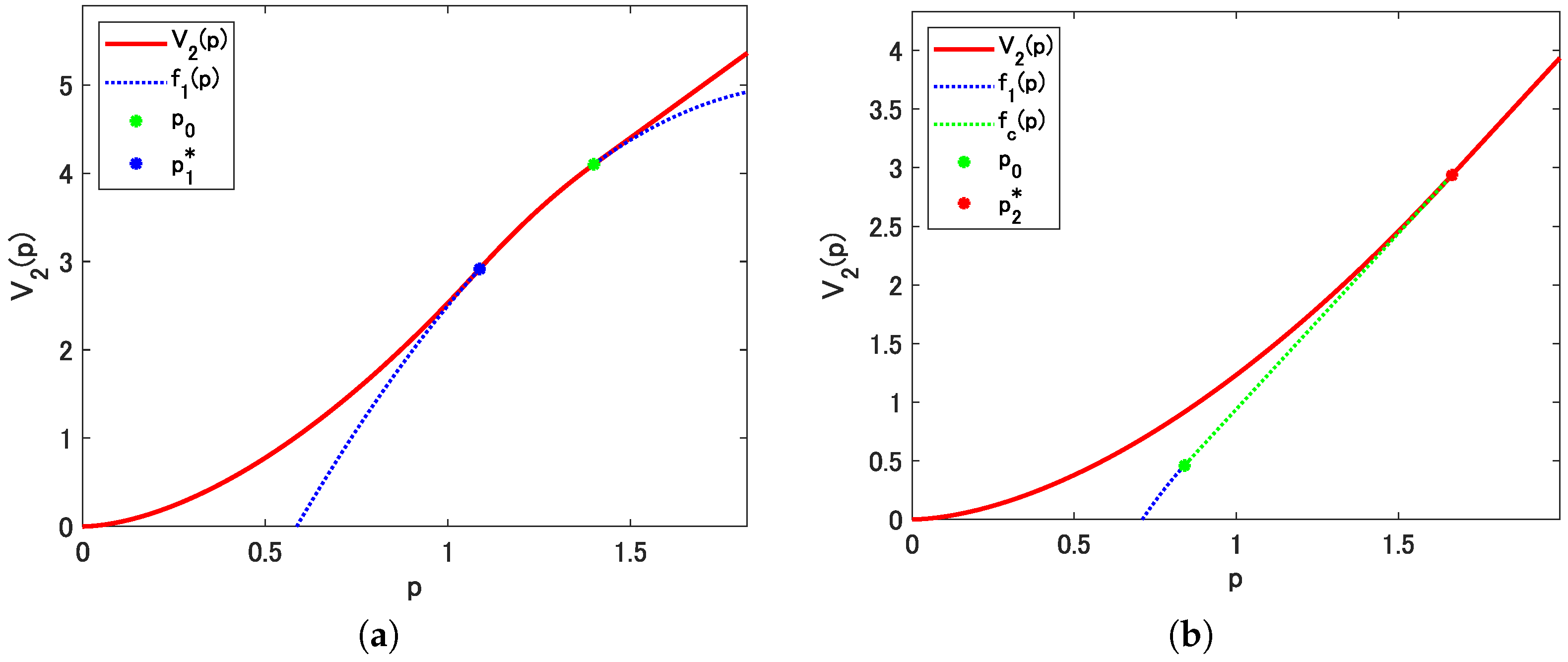

3.1. Optimal Investment Policies

3.2. Comparative Statics

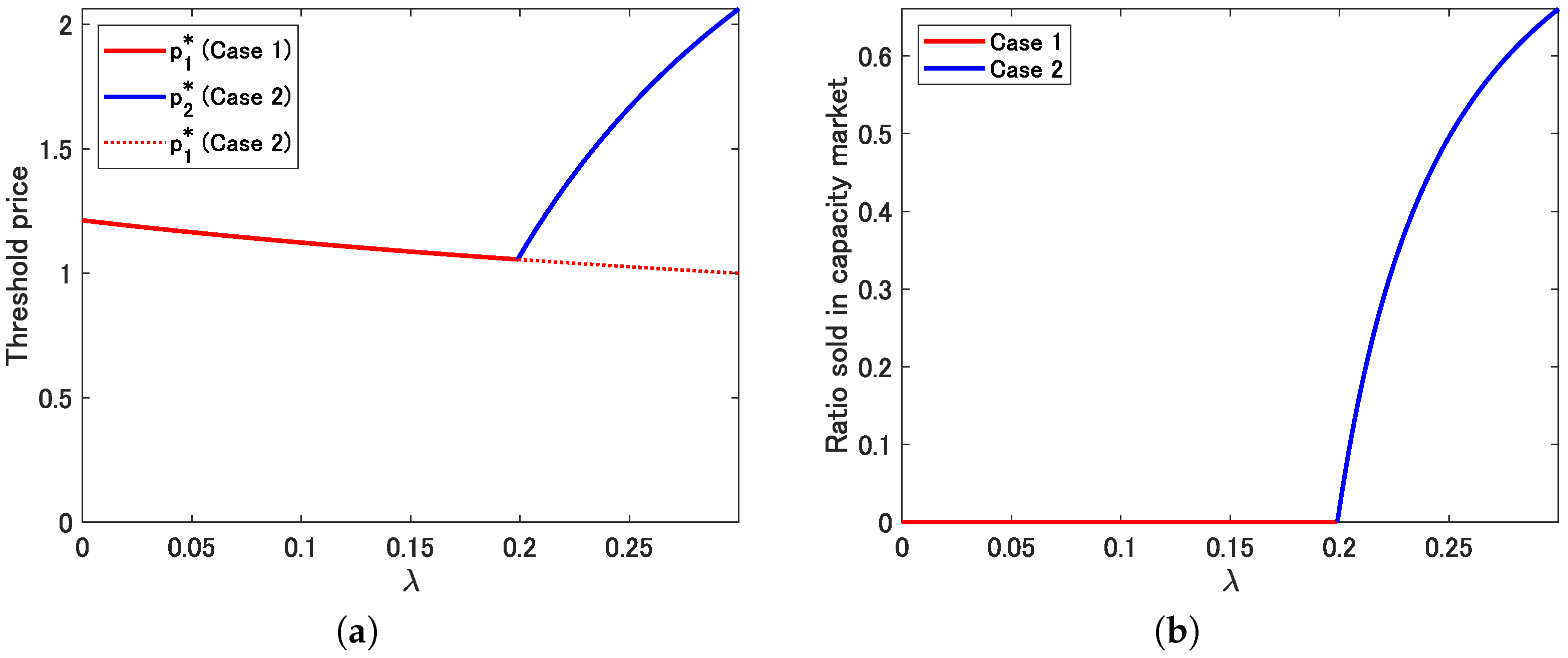

3.2.1. Risk Aversion Coefficient

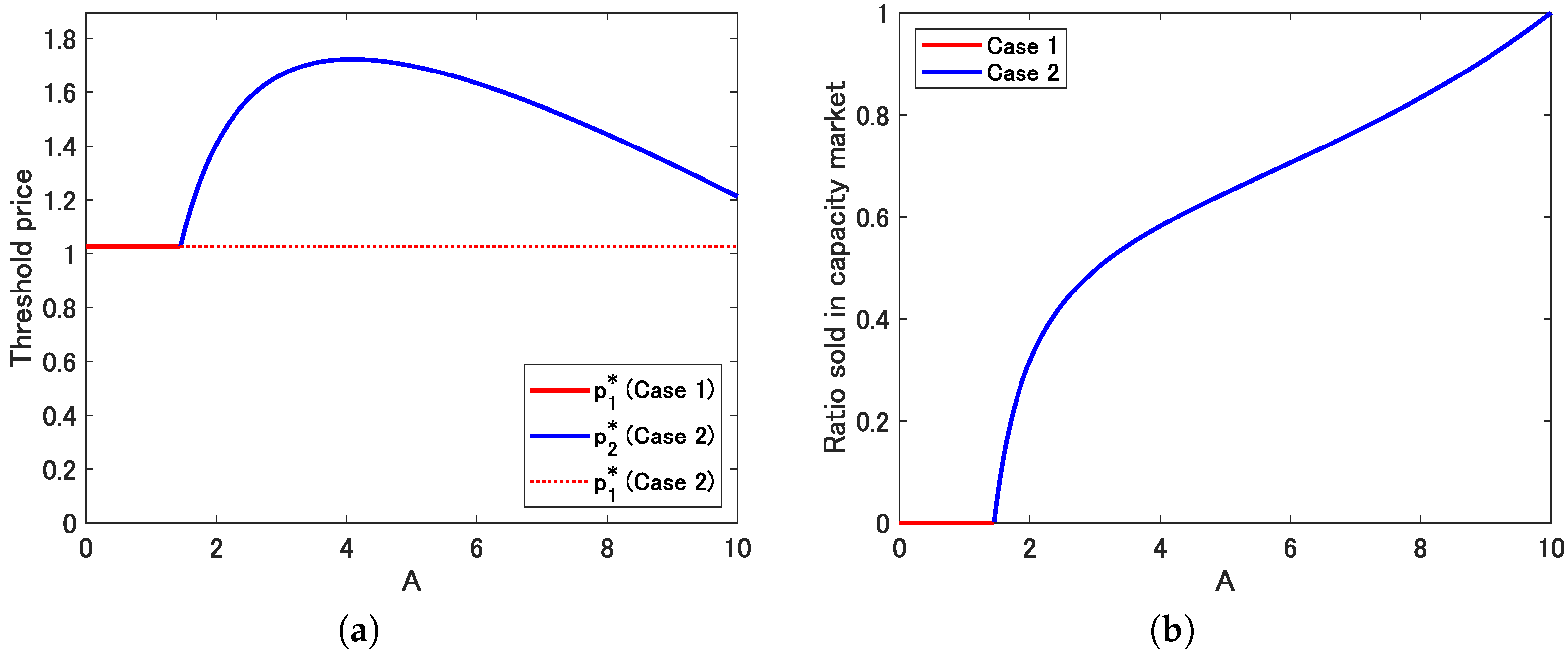

3.2.2. Profit Rate of Capacity Market A

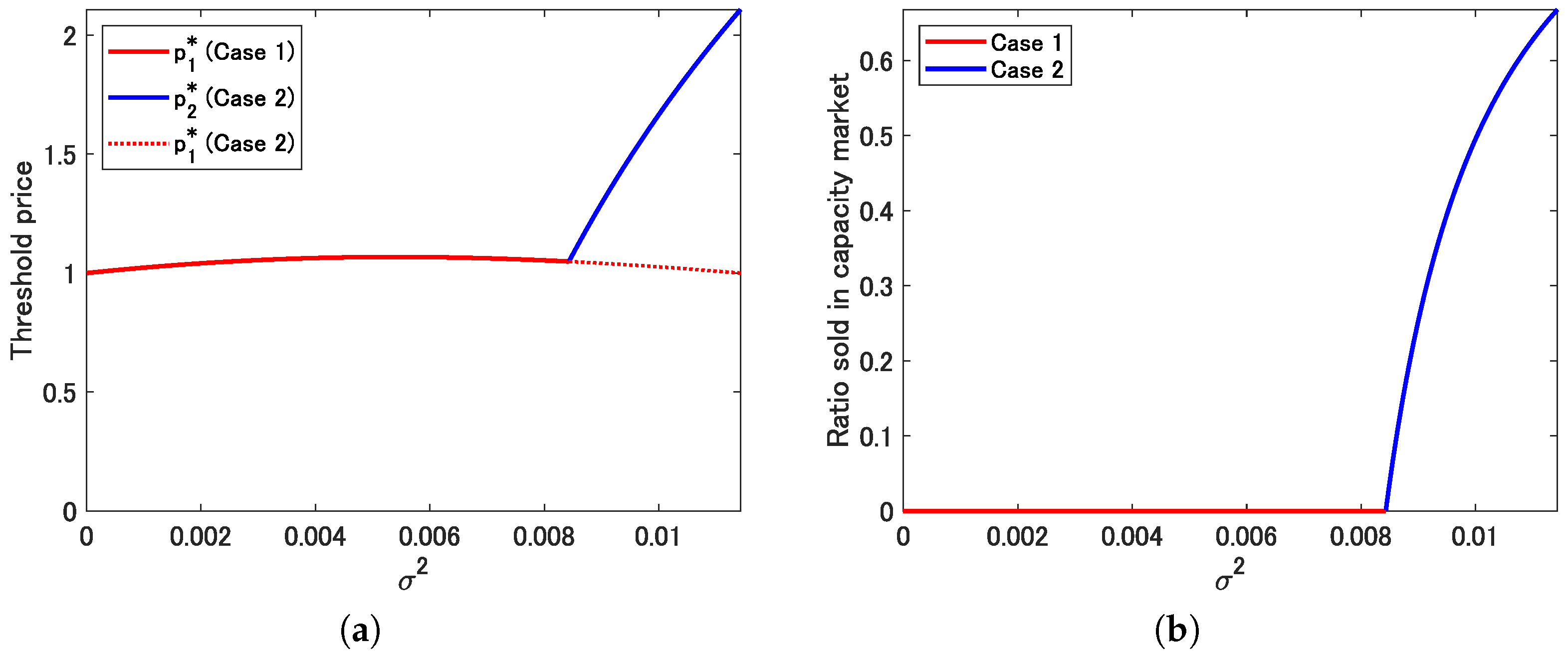

3.2.3. Electricity Price Volatility

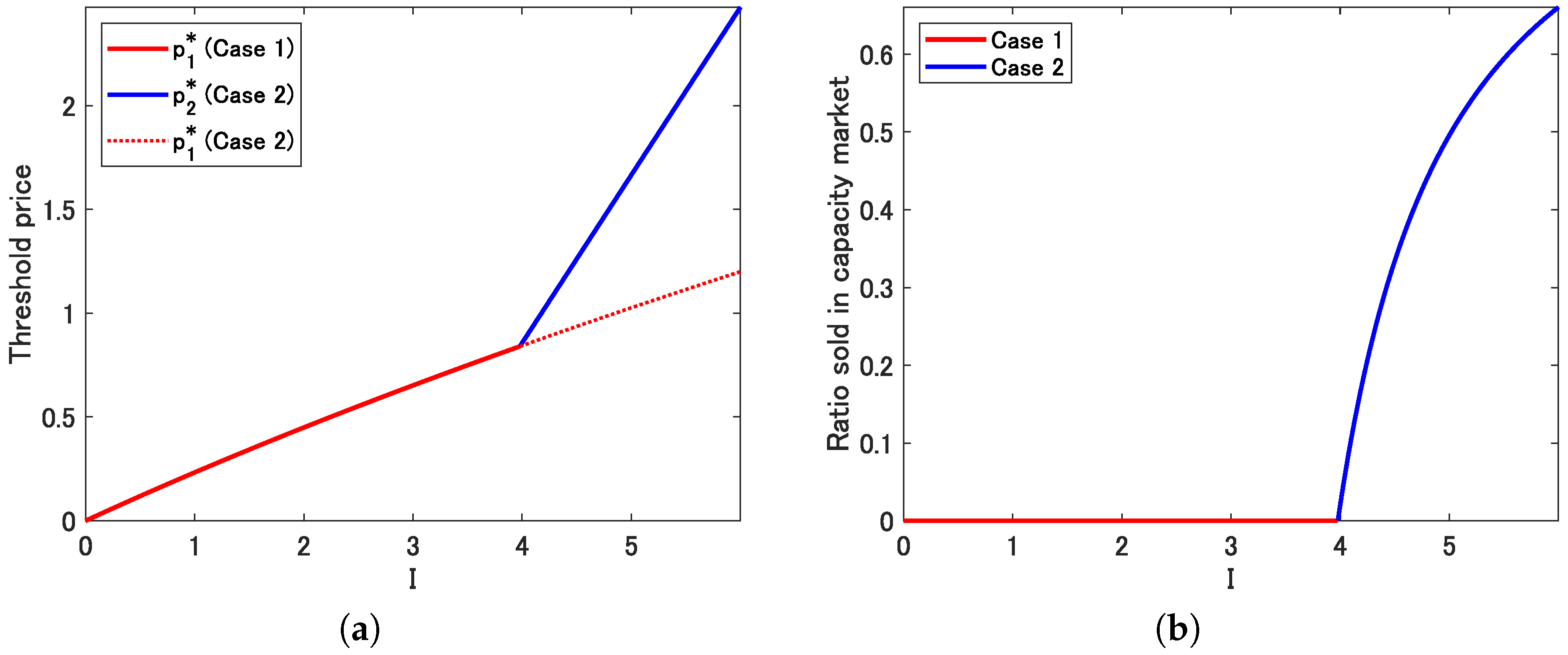

3.2.4. Investment Cost I

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| GBM | Geometric Brownian motion |

Appendix A. Proofs

Appendix A.1. Derivation of (6) and (7)

Appendix A.2. Proof of Theorem 1

Appendix A.3. Proof of Theorem 2

Appendix A.4. Proof of Theorem 3

References

- Joskow, P.L. Capacity payments in imperfect electricity markets: Need and design. Util. Policy 2008, 163, 159–170. [Google Scholar] [CrossRef]

- Green, R.; Staffell, I. Electricity in Europe: Exiting fossil fuels? Oxf. Rev. Econ. Policy 2016, 32, 282–303. [Google Scholar] [CrossRef]

- Woo, C.K.; Ho, T.; Zarnikau, J.; Olson, A.; Jones, R.; Chait, M.; Horowitz, I.; Wang, J. Electricity-market price and nuclear power plant shutdown: Evidence from California. Energy Policy 2014, 73, 234–244. [Google Scholar] [CrossRef]

- Newbery, D. Missing money and missing markets: Reliability, capacity auctions and interconnectors. Energy Policy 2016, 94, 401–410. [Google Scholar] [CrossRef]

- Bublitz, A.; Keles, D.; Zimmermann, F.; Fraunholz, C.; Fichtner, W. A survey on electricity market design: Insights from theory and real-world implementations of capacity remuneration mechanisms. Energy Econ. 2019, 80, 1059–1078. [Google Scholar] [CrossRef]

- Duggan, J.E., Jr. Capacity market mechanism analyses: A literature review. Curr. Sustain. Energy Rep. 2020, 7, 186–192. [Google Scholar] [CrossRef]

- De Vries, L.; Heijnen, P. The impact of electricity market design upon investment under uncertainty: The effectiveness of capacity mechanisms. Util. Policy 2008, 16, 215–227. [Google Scholar] [CrossRef]

- Hach, D.; Spinler, S. Capacity payment impact on gas-fired generation investments under rising renewable feed-in—A real options analysis. Energy Econ. 2016, 53, 270–280. [Google Scholar] [CrossRef]

- Höschle, H.; De Jonghea, C.; Le Cadre, H.; Belmans, R. Electricity markets for energy, flexibility and availability—Impact of capacity mechanisms on the remuneration of generation technologies. Energy Econ. 2017, 66, 372–383. [Google Scholar] [CrossRef]

- Hach, D.; Spinler, S. Robustness of capacity markets: A stochastic dynamic capacity investment model. OR Spectr. 2018, 40, 517–540. [Google Scholar] [CrossRef]

- Rios-Festner, D.; Blanco, G.; Olsina, F. Long-term assessment of power capacity incentives by modeling generation investment dynamics under irreversibility and uncertainty. Energy Policy 2020, 137, 111185. [Google Scholar] [CrossRef]

- de Maere d’Aertryckea, G.; Ehrenmanna, A.; Smeers, Y. Investment with incomplete markets for risk: The need for long-term contracts. Energy Policy 2017, 105, 571–583. [Google Scholar] [CrossRef]

- Petitet, M.; Finon, D.; Janssen, T. Capacity adequacy in power markets facing energy transition: A comparisonof scarcity pricing and capacity mechanism. Energy Policy 2017, 103, 30–46. [Google Scholar] [CrossRef]

- Ousman, A.A.; Hary, N.; Rious, V.; Saguan, M. The impact of investors’ risk aversion on the performances of capacity remuneration mechanisms. Energy Policy 2018, 112, 84–97. [Google Scholar] [CrossRef]

- Basak, S.; Chabakauri, G. Dynamic mean-variance asset allocation. Rev. Financ. Stud. 2010, 23, 2970–3016. [Google Scholar] [CrossRef]

- Dixit, A.K.; Pindyck, R.S. Investment under Uncertainty; Princeton University Press: Princeton, NJ, USA, 1994. [Google Scholar]

- Hugonnier, J.; Morellec, E. Real options and risk aversion. In Real Options, Ambiguity, Risk and Insurance; Bensoussan, A., Peng, S., Sung, J., Eds.; IOS Press: Amsterdam, The Netherlands, 2013; pp. 52–65. [Google Scholar]

- McDonald, R.L.; Siegel, D.S. The value of waiting to invest. Q. J. Econ. 1986, 101, 707–728. [Google Scholar] [CrossRef]

- Chronopoulos, M.; De Reyck, B.; Siddiqui, A. Optimal investment under operational flexibility, risk aversion, and uncertainty. Eur. J. Oper. Res. 2011, 213, 221–237. [Google Scholar] [CrossRef]

- Chronopoulos, M.; Lumbreras, S. Optimal regime switching under risk aversion and uncertainty. Eur. J. Oper. Res. 2017, 256, 543–555. [Google Scholar] [CrossRef]

- Barbosa, L.; Ferrão, P.; Rodrigues, A.; Sardinha, A. Feed-in tariffs with minimum price guarantees and regulatory uncertainty. Energy Econ. 2018, 72, 517–541. [Google Scholar] [CrossRef]

- Detemple, J.; Kitapbayev, Y. The value of green energy under regulation uncertainty. Energy Econ. 2017, 89, 104807. [Google Scholar] [CrossRef]

- Babich, V.; Lobel, R.; Yücel, S. Promoting solar panel investments: Feed-in-tariff vs. tax- rebate policies. Manuf. Serv. Oper. Manag. 2021, 22, 1148–1164. [Google Scholar] [CrossRef]

- Conejo, A.J.; Carrión, M.; Morales, J.M. Decision Making under Uncertainty in Electricity Markets; Springer: New York, NY, USA, 2010. [Google Scholar]

- Dayanik, S.; Karatzas, I. On the optimal stopping problem for one-dimensional diffusions. Stoch. Process. Their Appl. 2003, 107, 173–212. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Makimoto, N.; Takashima, R. Capacity Market and Investments in Power Generations: Risk-Averse Decision-Making of Power Producer. Energies 2023, 16, 4241. https://doi.org/10.3390/en16104241

Makimoto N, Takashima R. Capacity Market and Investments in Power Generations: Risk-Averse Decision-Making of Power Producer. Energies. 2023; 16(10):4241. https://doi.org/10.3390/en16104241

Chicago/Turabian StyleMakimoto, Naoki, and Ryuta Takashima. 2023. "Capacity Market and Investments in Power Generations: Risk-Averse Decision-Making of Power Producer" Energies 16, no. 10: 4241. https://doi.org/10.3390/en16104241

APA StyleMakimoto, N., & Takashima, R. (2023). Capacity Market and Investments in Power Generations: Risk-Averse Decision-Making of Power Producer. Energies, 16(10), 4241. https://doi.org/10.3390/en16104241