Legal Pathways to Coal Phase-Out in Italy in 2025

Abstract

1. Introduction

2. Methodology

- The current state-of-the-art of the use of coal-fired generation for electricity in Italy, as reported from international official national sources;

- The main outcomes of the first implementation of the capacity mechanism, the RES auctions and the PPAs;

- The advancement of the permitting procedures with regard to the relevant energy infrastructures in the context of the NECP.

3. De-Carbonization of the Energy Sector and Coal-Phase Out: The Italian Context

3.1. The Evolution of the Italian Energy Mix and Italian Energy Policy

3.2. The Current Italian Policy Context for Coal Phase-Out Between Ambitious Objectives and EU Constraints

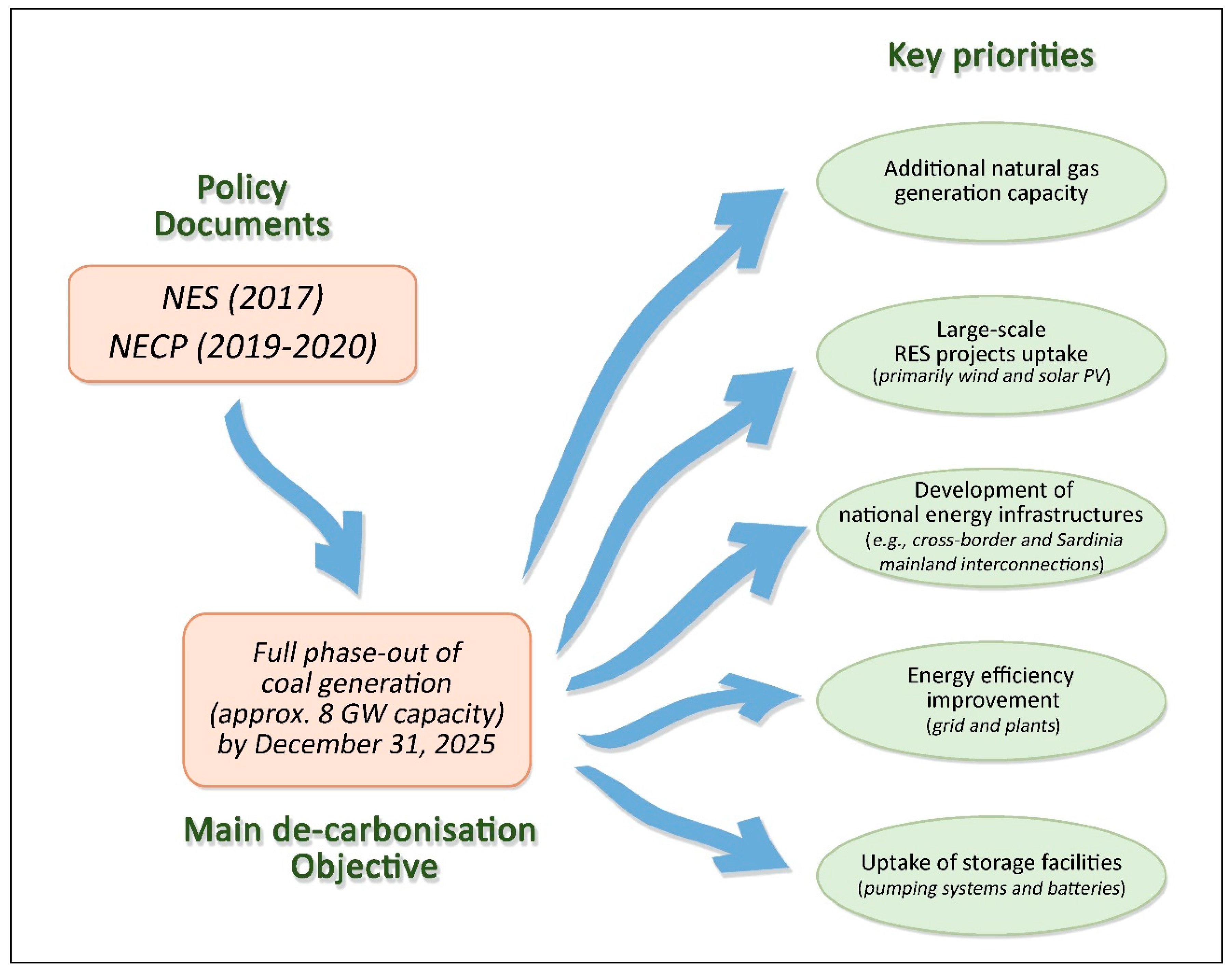

- A massive increase of RES electricity generation—up to 184 TWh in 2030, with a total of at least 52 GW (solar PV) and 19.3 GW (wind) generation capacity [8];

- The full development of key energy infrastructures, primarily with regard to insulated areas (i.e., large islands such as Sicily and Sardinia); for example, a new electricity interconnection between Sardinia, Sicily, and the continent is being looked into, along with new capacity for gas generation or storage capacity of 400 MW located on the island and the installation of condensers for at least 250 MVAR [8];

- The wide deployment of gas-fuelled power stations to ensure flexibility and security of energy supply against peak demand and wide ranges of electrical loads (especially in summer and winter) and to offset for intermittency of RES generation.

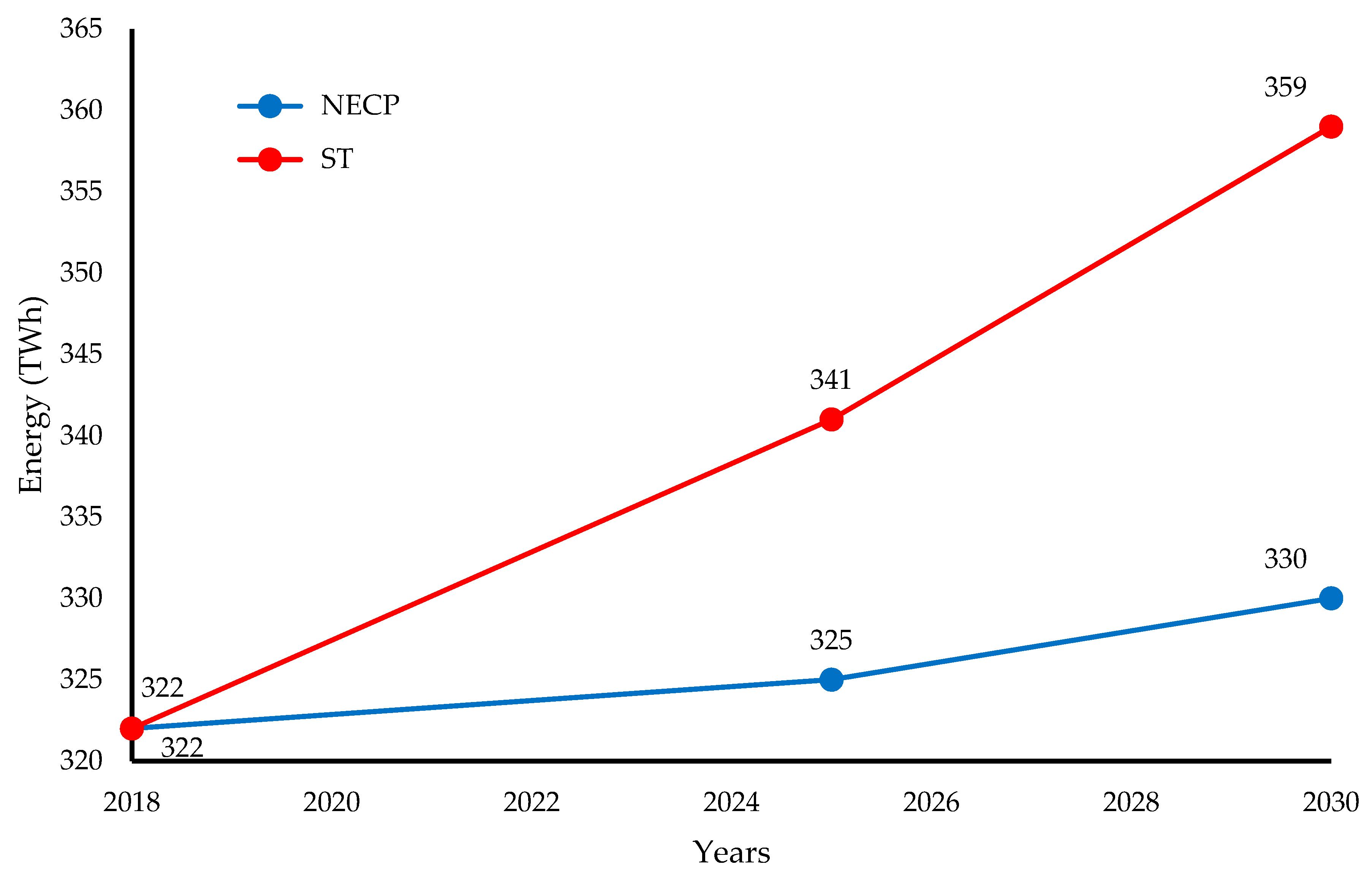

- The NECP 2025 scenario, developed by the Italian Transmission System Operator (TSO), Terna S.p.A., based on the Italian NECP [19]. This scenario envisages a total phase-out of coal power plants as pledged in the same NECP and therefore in a total 9.3 GW capacity reduction (7.9 GW) with a total of 43 GW additional RES (wind and solar PV) capacity through 2030. Accordingly, a 3 TWh demand increase in 2025 (325 TWh) as compared to 2018 (322 TWh) is foreseen, with a total of 54 GW thermal capacity needed as back-up, a total required addition of 3 GW aggregation/storage, and 5.4 GW new generation capacity (mostly acquired through natural gas) [19]. This additional capacity should be mostly (60%) allocated in Northern Italy, whereas storage capacity should be mostly allocated in the central and southern areas. Importantly, without such additional capacity, the loss of load expectation (LOLE) value would result in a ten-fold value (30 h) greater than the standard value adopted at the European and national level (3 h) [19];

- The Sustainable Transition (ST) scenario, elaborated by the European Network of Transmission System Operators for Electricity (ENTSO—E) [20]. This scenario is based on a rapid and steady reduction of coal generation (and related GHG emissions) as coupled with a 37 GW increase of RES generation (wind and solar PV) through 2030. Accordingly, a 19 TWh demand increase in 2025 (341 TWh) as compared to 2018 (322 TWh) is expected, with a total 56 GW thermal capacity needed as back-up and 5.4 GW new capacity (most entirely through natural gas) [20], although with hardly any increase in storage capacity.

4. Legal Pathways to Coal Phase-Out in Italy

4.1. Capacity Mechanism

4.2. RES Auctions and Power Purchase Agreements (PPAs) for RES Generation Capacity

4.3. Siting of Energy Infrastructures and RES Installations

5. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- European Commission. Communication, COM/2018/773 Final, a Clean Planet for All. A European Strategic Long-Term Vision for a Prosperous, Modern, Competitive and Climate Neutral Economy; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Caldecott, B.; Tulloch, D.J.; Bouveret, G.; Pfeiffer, A.; Kruitwagen, L.; McDaniels, J.; Dericks, G. The fate of european coal-fired power stations planned in the Mid-2000s: Insights for policymakers, companies, and investors considering new coal. Ssrn Electron. J. 2017. [Google Scholar] [CrossRef]

- Heinrichs, H.U.; Schumann, D.; Vögele, S.; Biß, K.H.; Shamon, H.; Markewitz, P.; Többen, J.; Gillessen, B.; Gotzens, F.; Ernst, A. Integrated assessment of a phase-out of coal-fired power plants in Germany. Energy 2017, 126, 285–305. [Google Scholar] [CrossRef]

- European Environmental Agency. Greening the Power Sector: Benefits of an Ambitious Implementation of Europe’s Environment and Climate Policies, Briefing no. 18/2018. Available online: https://www.eea.europa.eu/themes/industry/industrial-pollution-in-europe/benefits-of-an-ambitious-implementation (accessed on 31 July 2020).

- King, L.C.; van der Bergh, J.C. Implications of net energy-return-on-investment for a low-carbon energy transition. Nat. Energy 2018, 3, 334–340. [Google Scholar] [CrossRef]

- European Commission. Communication, COM (2020) 564 Final, an EU-Wide Assessment of National Energy and Climate Plans; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- Farfan, J.; Breyer, C. Structural changes of global power generation capacity towards sustainability and the risk of stranded investments supported by a sustainability indicator. J. Clean. Prod. 2017, 141, 370–384. [Google Scholar] [CrossRef]

- Italian Integrated National Energy and Climate Plan. Available online: https://ec.europa.eu/energy/sites/ener/files/documents/it_final_necp_main_en.pdf (accessed on 2 August 2020).

- RSE. Decarbonizzazione Dell’economia Italiana: Scenari di Sviluppo del Sistema Energetico Nazionale. Available online: https://www.minambiente.it/sites/default/files/archivio/allegati/rse_decarbonizzazione_web.pdf (accessed on 24 July 2020).

- Kittel, M.; Goeke, L.; Kemfert, C.; Oei, P.Y.; von Hirschhausen, C. Scenarios for coal-exit in Germany—A model-based analysis and implications in the European context. Energies 2020, 13, 2041. [Google Scholar] [CrossRef]

- Rentier, G.; Lelieveldt, H.; Kramer, G.J. Varieties of coal-fired power phase-out across Europe. Energy Policy 2019, 132, 620–632. [Google Scholar] [CrossRef]

- SDSN–IDDRI. Deep Decarbonization Pathways Project, Pathways to Deep Decarbonization 2015 Report. Available online: https://www.iddri.org/en/publications-and-events/report/pathways-deep-decarbonization-2015-report-executive-summary (accessed on 18 August 2020).

- Bellantuono, G. Legal pathways of decarbonisation in the EU: The case of coal phase-out. Oil Gas. Energy Law 2019, 17, 1–24. Available online: www.ogel.org/article.asp?key=3830 (accessed on 20 July 2020). [CrossRef]

- International Energy Agency, Country Profile: Italy. Available online: https://www.iea.org/countries/italy (accessed on 20 September 2020).

- Website of Italian Ministry of Environment, Land and Sea, Environmental Assessments and Permits Portal (AIA-SEA-EIA). Available online: https://va.minambiente.it/it-IT (accessed on 6 August 2020).

- Alved Dias, P.; Kanellopoulus, K.; Mederac, H.; Kapetaki, Z.; Miranda-Barbosa, E.; Shortall, R.; Czako, V.; Telsnig, T.; Vasquez-Hernandez, C.; Lacal Arantegui, R.; et al. EU Coal Regions: Opportunities and Challenges Ahead, EUR 29292 EN.; Publications Office of the European Union: Luxembourg, 2018. [Google Scholar] [CrossRef]

- ISPRA. National Inventory Report 2020. Available online: http://www.sinanet.isprambiente.it/it/sia-ispra/serie-storiche-emissioni/national-inventory-report/view (accessed on 5 August 2020).

- Ministry of Economic Development and Ministry of Environment, Land and Sea. Strategia Energetica Nazionale. 2017. Available online: https://www.mise.gov.it/images/stories/documenti/Testo-integrale-SEN-2017.pdf (accessed on 31 July 2020).

- Terna S.P.A. Rapporto Adeguatezza Italia 2019. Available online: https://download.terna.it/terna/Rapporto%20Adeguatezza%20Italia%202019_8d71cb7ff32ad37.pdf (accessed on 5 August 2020).

- ENTSO-E. Mid-Term Adequacy Forecast. 2019 Edition, Appendix 1; ENTSO-E: Brussels, Belgium. Available online: https://eepublicdownloads.entsoe.eu/clean-documents/sdc-documents/MAF/2019/MAF%202019%20Appendix%201%20-%20Detailed%20Results%2C%20Sensitivities%20and%20Input%20Data.pdf (accessed on 2 August 2020).

- SNAM; Terna S.P.A. La Transizione Energetica in Italia e il Ruolo del Settore Elettrico e del Gas. 2019. Available online: https://download.terna.it/terna/Transizione_Energetica_8d75215ad40fffa.pdf (accessed on 5 August 2020).

- Terna S.P.A. Mercato Della Capacità—Rendiconto degli Esiti Asta Madre. 2022. Available online: https://download.terna.it/terna/2019_12_06_Rendiconto%20EsitiAsta%202022_PUBBLICATO_8d7c06cc9f8470b.pdf (accessed on 30 July 2020).

- Terna S.P.A. Mercato Della Capacità—Rendiconto Degli Esiti Asta Madre. 2023. Available online: https://download.terna.it/terna/Rendiconto%20EsitiAsta%202023_8d78adbacbbe508.pdf (accessed on 30 July 2020).

- International Energy Agency. World Energy Outlook 2019; IEA: Paris, France, 2020; p. 270. [Google Scholar]

- European Commission. Staff Working Document, SWD (2020) 911 Final, Assessment of the Final National and Energy Climate Plan of Italy; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- ACER. Capacity Remuneration Mechanisms and the Internal Market for Electricity; ACER: Ljubljana, Slovenia, 2013. [Google Scholar]

- ISPRA. Fattori di Emissione Atmosferica di Gas a Effetto Serra nel Settore Elettrico Nazionale e Nei Principali Paesi Europei, Edizione 2020. Available online: https://www.isprambiente.gov.it/files2020/pubblicazioni/rapporti/Rapporto317_2020.pdf (accessed on 24 July 2020).

- European Commission. Staff Working Document, SWD (2013) 438 Final, Generation Adequacy in the Internal Electricity Market—Guidance on Public Interventions; European Commission: Brussels, Belgium, 2013; p. 3. [Google Scholar]

- Pototschnig, A.; Godfried, M. Capacity Mechanisms and the EU Internal Electricity Market. The Regulators’ View; ACER: Ljubljana, Slovenia, 2013. [Google Scholar]

- Meulman, L.; Méray, N. Capacity Mechanisms in Northwest Europe. Between a Rock and a Hard Place. Clingendael International Energy Programme; Nederlands Institut voor Internationale Betrekkingen: The Hague, The Netherlands, 2012. [Google Scholar]

- European Commission. Report COM (2016) 752 Final, Final Report of the Sector Inquiry on Capacity Mechanisms; European Commission: Brussels, Belgium, 2016. [Google Scholar]

- Gestore dei Servizi Energetici (GSE). Sintesi Rapporto Delle Attività. 2019. Available online: https://www.gse.it/documenti_site/Documenti%20GSE/Rapporti%20delle%20attività/RA2019.pdf (accessed on 2 August 2020).

- Bruck, M.; Sandborn, P.; Goudarzi, N. A levelized cost of energy (LCOE) model for wind farms that include power purchase agreements (PPAs). Renew. Energy 2018, 122, 131–139. [Google Scholar] [CrossRef]

- Energy Strategies Group. Renewable Energy Report 2020; Politecnico di Milano: Milan, Italy, 2020. [Google Scholar]

- Bloomberg NEF. New Energy Outlook 2020; Bloomberg NEF: New York, NY, USA, 2020. [Google Scholar]

- PPA Committee. Final Report 2019; PPA Committee: Milan, Italy, 2020. [Google Scholar]

- Cafaro, C.; Ceci, P.; Fardelli, A.; Zazzu, E. La trasformazione del settore energetico in Italia. Ing. Ambiente 2020, 7, 1–13. [Google Scholar]

- Maestroni, A. La questione della localizzazione di impianti di produzione di energie rinnovabili a valle delle linee guida ministeriali. Corte costituzionale e Corte di giustizia arbitri tra esigenze di tutela paesistica e di sviluppo economico. Riv. Giuridica Ambiente 2012, 5, 569. [Google Scholar]

- Gestore dei Servizi Energetici (GSE). Regolazione Regionale: Generazione Elettrica da Fonti Rinnovabili. 2018. Available online: http://enerweb.casaccia.enea.it/enearegioni/UserFiles/Regolazione_regionale_2018.pdf (accessed on 20 July 2020).

- Braaksma, L.; Fleming, R. Phasing out coal-fired power plants in the European Union: Examples from the Netherlands and Germany. In European Energy Law Report; Roggenkamp, M.M., Banet, C., Eds.; Intersentia: Cambridge, UK, 2020; Volume 13, pp. 261–288. [Google Scholar]

- European Commission. Document C (2018) 617 Final, State Aid SA.42011 (2017/N)-Italy-Italian Capacity Mechanism; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Spees, K.; Newell, S.A.; Pfeifenberger, J.P. Capacity markets—Lessons learned from the first decade. Econ. Energy Env. Policy 2013, 2, 1–26. [Google Scholar] [CrossRef]

- Gonzalez-Diaz, F.E. EU Policy on capacity mechanisms. In Capacity Mechanisms in the EU Energy Market: Law, Policy and Economics; Hancher, L., de Hauteclocque, A., Sadowska, M., Eds.; OUP: Oxford, UK, 2015. [Google Scholar]

- Mastropietro, P.; Fontini, F.; Rodilla, P.; Batlle, C. The Italian capacity remuneration mechanism: Critical review and open questions. Energy Policy 2018, 123, 659–669. [Google Scholar] [CrossRef]

- Ludwigs, M. Germany’s nuclear phase out and the right to property. Eur. Netw. Law Regul. Q. 2016, 1, 44. [Google Scholar]

- Carbon Tracker Initiative. The $2 Trillion Stranded Assets Danger Zone: How Fossil Fuels Firms Risk Destroying Investor Returns, London, United Kingdom. Available online: www.carbontracker.org/wp-content/uploads/2015/11/CAR3817_Synthesis_Report_24.11.15_WEB2.pdf (accessed on 13 October 2020).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 1990 | 2000 | 2010 | 2011 | 2013 | 2015 | 2017 | 2018 | ||

|---|---|---|---|---|---|---|---|---|---|

| Total | TWh | 218.59 | 275.30 | 301.19 | 301.61 | 289.06 | 282.39 | 295.79 | 289.12 |

| % | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | |

| Fossil Fuel | TWh | 180.19 | 217.76 | 218.78 | 214.58 | 172.85 | 169.63 | 186.98 | 170.53 |

| % | 82 | 79 | 73 | 71 | 60 | 60 | 63 | 59 | |

| Coal | TWh | 37.76 | 30.52 | 44.43 | 50.14 | 48.49 | 45.39 | 35.10 | 30.96 |

| % | 17.27 | 11.09 | 14.75 | 16.62 | 16.78 | 16.07 | 11.87 | 10.71 | |

| Natural Gas | TWh | 39.71 | 101.36 | 152.74 | 144.55 | 108.88 | 110.86 | 140.35 | 128.54 |

| % | 18.17 | 36.82 | 50.71 | 47.93 | 37.67 | 39.26 | 47.45 | 44.46 | |

| Oil | TWh | 102.72 | 85.88 | 21.71 | 19.89 | 15.48 | 13.38 | 11.53 | 11.03 |

| % | 46.99 | 31.20 | 7.21 | 6.59 | 5.36 | 4.74 | 3.90 | 3.82 | |

| Nuclear | TWh | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| % | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Total Renewables | TWh | 38.40 | 57.54 | 82.41 | 87.03 | 116.21 | 112.76 | 108.81 | 118.59 |

| % | 18 | 21 | 27 | 29 | 40 | 40 | 37 | 41 | |

| Hydro | TWh | 35.08 | 50.90 | 54.41 | 47.58 | 54.67 | 46.97 | 38.03 | 50.50 |

| % | 16.05 | 18.49 | 18.07 | 15.78 | 18.91 | 16.63 | 12.95 | 17.47 | |

| Biofuels | TWh | 0.01 | 0.99 | 7.39 | 8.63 | 14.89 | 17.05 | 17.00 | 16.78 |

| % | 0 | 0.36 | 2.45 | 2.86 | 5.15 | 6.04 | 5.75 | 5.80 | |

| Waste | TWh | 0.09 | 0.92 | 4.19 | 4.51 | 4.50 | 4.77 | 4.86 | 4.83 |

| % | 0.04 | 0.33 | 1.39 | 1.50 | 1.56 | 1.69 | 1.64 | 1.67 | |

| Geothermal | TWh | 3.22 | 4.71 | 5.38 | 5.65 | 5.66 | 6.19 | 6.20 | 6.11 |

| % | 1.47 | 1.71 | 1.79 | 1.87 | 1.56 | 2.19 | 2.10 | 2.11 | |

| Solar PV | TWh | 0 | 0.02 | 1.91 | 10.80 | 21.59 | 22.94 | 24.98 | 22.65 |

| % | 0 | 0.01 | 0.63 | 3.58 | 7.47 | 8.12 | 8.45 | 7.83 | |

| Solar Thermal | TWh | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| % | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Wind | TWh | 0 | 0.56 | 9.13 | 9.86 | 14.90 | 14.84 | 17.74 | 17.72 |

| % | 0 | 0.20 | 3.03 | 3.27 | 5.15 | 5.26 | 6.00 | 6.13 |

| Coal-Fired Combustion Plant | Thermal Capacity (MWt) | Electrical Capacity (MWe) |

|---|---|---|

| Torrevaldaliga Nord Civitavecchia (RM) | 4260 | 1980 |

| Brindisi | 6560 | 2640 |

| Monfalcone (GO) | 851 | 336 |

| Fusina Porto Marghera (Venice) | 2431 | 976 |

| Lamarmora (Brescia) | 200 | 72 |

| La Spezia | 1540 | 600 |

| Sulcis, Portoscuso (SU) | 1470 | 700 |

| Fiume Santo (SS) | 1600 | 960 |

| Total Installed Capacity | 18912 | 8264 |

| Coal-Fired Combustion Plant | Power Generation Unit | Operating Hours | ||||

|---|---|---|---|---|---|---|

| 2014 | 2015 | 2016 | 2017 | 2018 | ||

| Torrevaldaliga Nord Civitavecchia (RM) | TN2 1420 MWt TN3 1420 MWt TN4 1420 MWt | 6867 6944 6389 | n/a n/a n/a | 6484 6195 6001 | 6791 5344 5941 | 5353 4676 4367 |

| Brindisi | GR1 1640 MWt GR2 1640 MWt GR3 1640 MWt GR4 1640 MWt | 5880 7136 7616 7223 | 6330 7620 7988 7891 | 5031 3392 6276 6669 | 5173 4798 4874 3412 | 4132 4682 4152 3924 |

| Monfalcone (GO) | GR1 418 MWt GR2 433 MWt | 6303 6693 | n/a n/a | 7619 7794 | 7390 6230 | 6062 7118 |

| Fusina Porto Marghera (Venice) | GR1 415.2 MWt GR2 430.8 MWt GR3 792.8 MWt (co-combust. coal/CSS) GR4 792.8 MWt (co-combust. coal/CSS) | 6809 6625 6638 - 7586 - | 7762 8192 7479 - 8153 - | n/a n/a n/a - n/a - | n/a n/a n/a - n/a - | n/a n/a n/a - n/a - |

| Lamarmora (Brescia) | GR3 200 MWt | 3421 | 3537 | 3516 | 3384 | 3330 |

| La Spezia | SP3 1540 MWt | 6425 | 5740 | 6803 | 5057 | n/a |

| Sulcis Portoscuso (SU) | SU2 800 MWt SU3 670 MWt | 6196 5011 | n/a n/a | 3511 1469 | 5221 2601 | 4142 3437 |

| Fiume Santo (SS) | GR3 800 MWt GR4 800 MWt | 7597 7116 | 4939 5273 | 6618 4454 | 7105 8034 | 6147 7564 |

| Coal-Fired Combustion Plant | Years | ||||

|---|---|---|---|---|---|

| 2014 | 2015 | 2016 | 2017 | 2018 | |

| Torrevaldaliga Nord Civitavecchia (RM) | 10,892.368 | 10,736.213 | 10,181.950 | 9747.838 | 8081.026 |

| Brindisi | 11,972.979 | 13,115.643 | 8275.345 | 6485.120 | 5477.190 |

| Monfalcone (GO) | 1775.700 | 2037.300 | 2145.200 | 1920.400 | 1876.600 |

| Fusina Porto Marghera (Venice) | 4838.368 | 5779.412 | 4665.440 | 3682.847 | 3556.557 |

| Lamarmora (Brescia) | 193.653 | 219.311 | 204.505 | 212.964 | 205.652 |

| La Spezia | 2741.860 | 2532.872 | 2831.877 | 2019.990 | 1928.640 |

| Sulcis, Portoscuso (SU) | 1648.011 | 1294.928 | 679.581 | 1074.077 | 1001.932 |

| Fiume Santo (SS) | 3188.000 | 2404.000 | 2535.000 | 3514.000 | 3160.000 |

| Total | 37,250.939 | 38,119.679 | 31,518.898 | 28,657.236 | 25,287.597 |

| Area (Geographic) | Existing | New Capacity | Non-Domestic Capacity | |||

|---|---|---|---|---|---|---|

| Capacity (MW/y) | Premium (€/MW/y) | Capacity (MW/y) | Premium (€/MW/y) | Capacity (MW/y) | Premium (€/MW/y) | |

| North | 21,465 | 33,000 | 1276 | 75,000 | 4241 | 4400 |

| Center—North | 1272 | 33,000 | 49 | 75,000 | - | - |

| Center—South | 4233 | 33,000 | 305 | 75,000 | 104 | 3449 |

| South | 2581 | 33,000 | 84 | 75,000 | 49 | 4000 |

| Calabria | 3185 | 33,000 | 0 | 75,000 | - | - |

| Sicily | 1878 | 33,000 | 53 | 75,000 | - | - |

| Sardinia | 144 | 33,000 | 0 | 75,000 | - | - |

| Total | 34,758 | - | 1767 | - | 4394 | - |

| Area (geographic) | Existing | New Capacity | Non-Domestic Capacity | |||

|---|---|---|---|---|---|---|

| Capacity (MW/y) | Premium (€/MW/y) | Capacity (MW/y) | Premium (€/MW/y) | Capacity (MW/y) | Premium (€/MW/y) | |

| North | 21,284 | 33,000 | 2631 | 75,000 | 4241 | 4400 |

| Center—North | 1308 | 33,000 | 65 | 75,000 | − | − |

| Center—South | 4651 | 33,000 | 804 | 75,000 | 104 | 4949 |

| South | 2927 | 33,000 | 162 | 75,000 | 49 | 3999 |

| Calabria | 2891 | 33,000 | 0 | 75,000 | − | − |

| Sicily | 1797 | 33,000 | 342 | 75,000 | − | − |

| Sardinia | 155 | 33,000 | 0 | 75,000 | − | − |

| Total | 35,013 | − | 4004 | − | 4394 | − |

| Fuels | Years | ||

|---|---|---|---|

| 1990 | 2013 | 2017 | |

| Solids | 28,100 | 39,900 | 28,600 |

| Natural Gas | 21,000 | 48,500 | 60,700 |

| Derived Gases | 6700 | 5900 | 4500 |

| Oil Products | 70,200 | 12,400 | 8800 |

| Other Fuels | 100 | 3400 | 3500 |

| Total | 126,100 | 110,100 | 106,100 |

| Off-Taker | Developer/Generator | Duration (Years) | RES Technology | Power/Energy | Date |

|---|---|---|---|---|---|

| Wienerberger | Engie | 5 | Solar PV | n/a | Feb. 2018 |

| EGO | Octopus | 5 | Solar PV | 40 MW | Mar. 2018 |

| EGO | Octopus | 5 | Solar PV | 63 MW | Dec. 2018 |

| Trailstone | Canadian Solar, Manny Energy | 10 | Solar PV | 18 MW | Dec. 2019 |

| Shell | Octopus | 5 | Solar PV | 71 | Dec. 2020 |

| Axpo | European Energy (Framework PPA) | 12 | Solar PV | 150 (+150) MW | Jan. 2019 |

| Audax Renovables | Base FV | 10 | Solar PV | 20 MW | Jan. 2020 |

| DXT Commodities | Fera | 7 | Wind (Onshore) | 200 GWh | Apr. 2019 |

| Coal-Fired Combustion Plant | Existing IED (AIA) Permit for Coal Generation (To Expire on 31 December 2025) | EIA Permit (Natural Gas Repowering Projects) |

|---|---|---|

| Torrevaldaliga Nord Civitavecchia (RM) | Ministerial Decree no. 284/2019 (30 September 2019) | Pending |

| Brindisi | Ministerial Decree no. 84/2020 (21 April 2020) | Pending |

| Monfalcone (GO) | Ministerial Decree no. 50/2020 (27 February 2020) | Pending |

| Fusina Porto Marghera (Venice) | In progress | Pending |

| Lamarmora (Brescia) | In progress | n/a |

| La Spezia | Ministerial Decree no. 351/2019 (6 December 2019) | Pending |

| Sulcis, Portoscuso (SU) (Sardinia) | Ministerial Decree no. 37/2020 (13 February 2020) | n/a |

| Fiume Santo (SS) | Ministerial Decree no. 85/2020 (22 April 2020) | n/a |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fermeglia, M.; Bevilacqua, P.; Cafaro, C.; Ceci, P.; Fardelli, A. Legal Pathways to Coal Phase-Out in Italy in 2025. Energies 2020, 13, 5605. https://doi.org/10.3390/en13215605

Fermeglia M, Bevilacqua P, Cafaro C, Ceci P, Fardelli A. Legal Pathways to Coal Phase-Out in Italy in 2025. Energies. 2020; 13(21):5605. https://doi.org/10.3390/en13215605

Chicago/Turabian StyleFermeglia, Matteo, Paolo Bevilacqua, Claudia Cafaro, Paolo Ceci, and Antonio Fardelli. 2020. "Legal Pathways to Coal Phase-Out in Italy in 2025" Energies 13, no. 21: 5605. https://doi.org/10.3390/en13215605

APA StyleFermeglia, M., Bevilacqua, P., Cafaro, C., Ceci, P., & Fardelli, A. (2020). Legal Pathways to Coal Phase-Out in Italy in 2025. Energies, 13(21), 5605. https://doi.org/10.3390/en13215605