Abstract

The heterogeneous empirical evidence in the vast literature on capital structure determinants is puzzling to scholars and practitioners. Various leverage measurements, in conjunction with the inconclusiveness of the significant firm-related capital structure determinants, complicate comparability. Practitioners also find it challenging to determine optimal financing strategies with real precision. This paper provides an integrative position that consolidates firm-related capital structure determinants with their respective measurements and suggests a preferred proxy for capital structure. A qualitative design has been applied, which is rarely done in the context of capital structure. This paper also offers a methodological contribution by utilising a combination of documentary analysis with PRISMA and forward-looking citation analysis, named the adapted documentary analysis. Capital structure determinant studies were targeted from inception until 2023. The synthesis of the results from 335 articles identified the six most prominent capital structure determinants: profitability, tangibility, growth proxied by the market-to-book value of equity (MTB), firm size, non-debt tax shield (NDTS), and business risk. Capital structure book value measurements seem more reliable than market-based measures. Profitability, MTB, and tangibility are the key firm-related determinants informing practitioners’ financing decisions. A consolidated list of the most prominent capital structure determinants, with their associated measurements, and a reliable proxy for capital structure are novel contributions that enable comparability in capital structure research across companies, industries, and countries. It creates a consolidated, integrative platform that adds to the academic debate and assists practitioners in their capital structure decision-making.

1. Introduction

How firms finance their operations has always been important (Klestov & Jindřichovská, 2021). The current focus on sustainability propels managers to align their financing strategy with this goal (StatsSA, 2019). A business’s sustainable financing strategy is vital (Mokhova & Zinecker, 2014). It is crucial for future growth and an important tool for creating shareholder value. A financing strategy, however, that is not sustainable over the long term puts a firm’s longevity in jeopardy (Sisodia & Maheshwari, 2022). For this reason, many firms have ceased to exist, especially during periods of crisis (Kurznack et al., 2021; Moradi & Paulet, 2019).

The firm’s choice between debt and equity is a contentious issue that has spanned decades. The optimal capital structure was termed a puzzle by Myers for the first time in 1984 (Myers, 1984), but still, the literature has come up short with the answer to real-life capital structure behaviour (DeAngelo, 2022). The problem is that managers cannot precisely determine optimal capital structure decisions (DeAngelo, 2022). This is due to uncertainties that plague the financing decision-making. There is a tendency for managers to default to heuristic decision-making. This notion is evident in DeAngelo’s (2021) case study. This authoritative author on capital structure compared the financing strategies of two established corporations in the same industry. Based on interviews with the two CEOs, both agreed that they cannot determine optimal financing decisions with real precision.

Over the past few decades, various conflicting theories have attempted to explain the actual financing behaviour of companies, such as the irrelevance, pecking order, and trade-off theories (Boateng et al., 2022). The theorising of the corporate financing decision started with the seminal work of Modigliani and Miller in 1958. The Nobel Prize-winning economists initially proposed that no combination of debt and equity influences a firm’s value, a position that came to be known as the irrelevance theory. The authors’ work was widely criticised. Five years later, Modigliani and Miller (1963) accepted that their irrelevance theory’s initial assumptions were unrealistic since it was based on perfect market conditions (Vatavu, 2012). More theories followed, such as the agency, signalling, and market timing theories (Jensen & Meckling, 1976; Ross, 1977; Baker & Wurgler, 2002). However, the two dominant capital structure theories are the trade-off and pecking order theories (DeAngelo, 2021). The trade-off theory proposed by Kraus and Litzenberger (1973) postulates that the corporate financing decision is a balancing act between the costs and benefits associated with debt. The interest deductibility of debt creates tax savings for the firm. However, there is a point at which too much debt may endanger the business due to the threat of financial downturns and shocks. Therefore, the tax-saving benefit is balanced with the cost of financial distress to find the appropriate level of debt within the firm’s capital structure. On the contrary, the pecking order theory, initially proposed by Donaldson (1961) and refined by Myers and Majluf (1984), postulates that managers use a hierarchical order of financing options. The order of raising funds is prioritised: retained earnings are targeted first, followed by debt, and, as a last option, equity issuance. These two theories, with their distinct approaches, constitute the main debate within the field.

In 1988, Titman and Wessels seminally extended the range of theoretical attributes of the various capital structure theories to capture the effect they may have on the debt-equity choice. The authors identified a range of determinants of capital structure at the time as: ‘asset structure, non-debt tax shields, growth, uniqueness, industry classification, size, earnings volatility, and profitability’ (Titman & Wessels, 1988, p. 2). Over the years, additional firm-related determinants, such as liquidity, business risk, size, age, tangibility, and market-to-book ratio, have been identified and tested. Capital structure literature has been previously reviewed by Harris and Raviv (1991), Frank and Goyal (2009), and Graham and Leary (2011). However, Kumar et al. (2017) state that, at the time of publishing their meta-study, theirs was the first in the literature on capital structure determinants.

Study findings agree that various firm-related factors influence capital structure. Notwithstanding the coverage in the literature, the empirical evidence remains heterogeneous and inconclusive, since the significance and strength of these determinants vary across firms, industries, and countries (Roy & Sen, 2022). Additionally, the outcomes of studies, such as the meta-studies by Kumar et al. (2017) and Hang et al. (2018) on capital structure determinants and their associated measures, differ. This poses a problem for researchers in determining which firm-related factors to include, especially when more complex investigations are targeted, such as exploring new variables influencing firms’ financing decisions.

Furthermore, the literature on capital structure determinants is vast (Demirgüneş, 2017). This vastness makes it difficult to synthesise heterogeneous results, hindering managers’ ability to make financing decisions with greater precision. Furthermore, for researchers, there is uncertainty and bias when selecting capital structure determinants and their proxies for capital structure investigations (Graham & Leary, 2011; Demirgüneş, 2017). Graham and Leary (2011) scrutinised the empirical capital structure literature at the time and found that an additional problem lies in the variety of empirical leverage measures and proxies for firm characteristics used in the literature. The authors argued that this variety of capital structure measures may contribute to misspecification and, consequently, to inconclusive evidence in the capital structure literature. Furthermore, this variety hampers the comparability of the vast empirical capital structure evidence (Demirgüneş, 2017). The lack of consolidated results also hampers the exploration of underexplored determinants, as the literature calls for. Consolidated results will simplify matters, aiding researchers in their future investigations.

However, synthesising these heterogeneous findings is challenging, especially given the vastness of the capital structure literature. One way to navigate the vastness is to lean on the work of previous authors. To this end, studies such as systematic reviews, bibliometric analyses, and meta-studies can provide valuable insights, since these kinds of studies aim to determine a field’s status and make sense of the existing literature (Xiao & Watson, 2019). In such studies, a systematic approach is applied to scientifically and credibly harvest findings from the existing literature. These kinds of studies have been scarce in the capital structure literature for many years (Kumar et al., 2017), making it difficult to achieve consolidation of capital structure determinants. However, more recently, these kinds of studies, encompassing systematic reviews, bibliometric analysis, and meta-studies, have surfaced in the capital structure field, providing a renewed landscape to explore. In so doing, a set of prominent capital structure determinants can emerge, contributing to the scholarship and guiding managers with greater precision in their financial decision-making.

Therefore, the focus of this paper is to extend a consolidation to provide an integrative platform from which underexplored determinants can be investigated, thereby advancing the field of capital structure determinants. Additionally, this paper adopts a qualitative methodology, which is rarely done in the context of capital structure. It presents a novel, PRISMA-informed documentary and citation analysis to mitigate the risk of researcher bias. In this process, responsible simplicity is achieved, assisting future capital structure investigations. The rest of the paper will address this research methodology applied, followed by the results and findings. The conclusion is then presented, incorporating limitations, managerial implications, and suggestions for future research.

2. Materials and Methods

This study employed a qualitative approach that adopts an interpretivist epistemology, viewing knowledge as contextual. It proposed a novel method for consolidating findings from documentary analysis, incorporating PRISMA (Page et al., 2021) which adds rigour to the systematic interpretation of the most prominent capital structure determinants.

A documentary analysis may be criticised for bias, which threatens the trustworthiness of a study (Bowen, 2009). Quinlan et al. (2015) suggested that documentary analysis should be systematically divided into three stages: planning, conducting, and reporting. Xiao and Watson (2019) propose eight steps for the same three systematic stages as those described by Quinlan et al. (2015). However, the eight steps proposed by Xiao and Watson (2019) are in the context of a systematic review and not a documentary analysis. Still, one can lean on these steps to mitigate the previously mentioned criticism and enhance the transparency and credibility of documentary analyses. Therefore, for this study, the three-staged systematic approach prescribed by Quinlan et al. (2015) is scaffolded by consulting the eight steps for systematic reviews proposed by Xiao and Watson (2019), which provide granular detail. The eight steps of Xiao and Watson (2019) are as follows: (1) formulate the problem; (2) develop and validate the review protocol; (3) search the literature; (4) screen for inclusion; (5) assess the quality; (6) extract data; (7) analyse and synthesise the data; and (8) report findings. Steps 3 to 6 involve data extraction, which also requires an articulated method. To guide these steps, the revised Preferred Reporting Items for Systematic Reviews and Meta-Analyses 2020 statement (PRISMA) of Page et al. (2021) is incorporated. PRISMA provides a protocol in the form of a flowchart that sets out a more detailed step-by-step action plan for extracting documents, operationalising the steps suggested by Quinlan et al. (2015) or Xiao and Watson (2019). The PRISMA protocol helps researchers fully and transparently report their inclusion criteria (Priyan et al., 2023). This PRISMA flowchart outlines three stages of data extraction: identification, screening, and inclusion. According to the PRISMA flow diagram, documents from various sources are first identified. Then, unwanted documents, such as duplicates, must be removed. The PRISMA protocol underscores the need to clearly define eligibility criteria and provide detailed explanations for study selection decisions. For this study, the title of an article had to indicate that it is a systematic review, a bibliometric study, or a meta-analysis. Then the selected documents are screened. During the screening process, documents that specifically address the investigation’s aim are selected. For this study, a systematic review, bibliometric study, or meta-analysis had to address an analysis of capital structure determinants. An attempt is then made to retrieve the selected documents. If no access to the documents is possible, they are self-evidently excluded. The retrieved documents are then submitted for a full-text read-through to assess eligibility for inclusion. The data extraction process is concluded once the final list of eligible documents is determined. The eligible documents are then analysed. PRISMA is an improved data extraction protocol compared to Steps 3 to 6 of Xiao and Watson (2019).

Once the list of eligible documents is analysed, a forward-looking approach is necessary to ensure that the documentary analysis results are not dated. Such an approach is necessary because the review protocol’s search terms may not align with the articles’ keywords. Consequently, such articles will not be detected in the initial documentary analysis. Citation analysis helps mitigate these risks (Meho, 2007). Moreover, drawing from the updated PRISMA guidelines by Page et al. (2021), other methods, such as citation searching, are allowable. Therefore, a follow-up citation analysis of the identified documents from the initial analysis will verify that recently published articles not identified in the initial analysis are not excluded from the sample. Such a technique ensures that the documentary analysis findings are current and comprehensive. When searching for the cited articles, the PRISMA protocol should be followed again to maintain transparency and credibility.

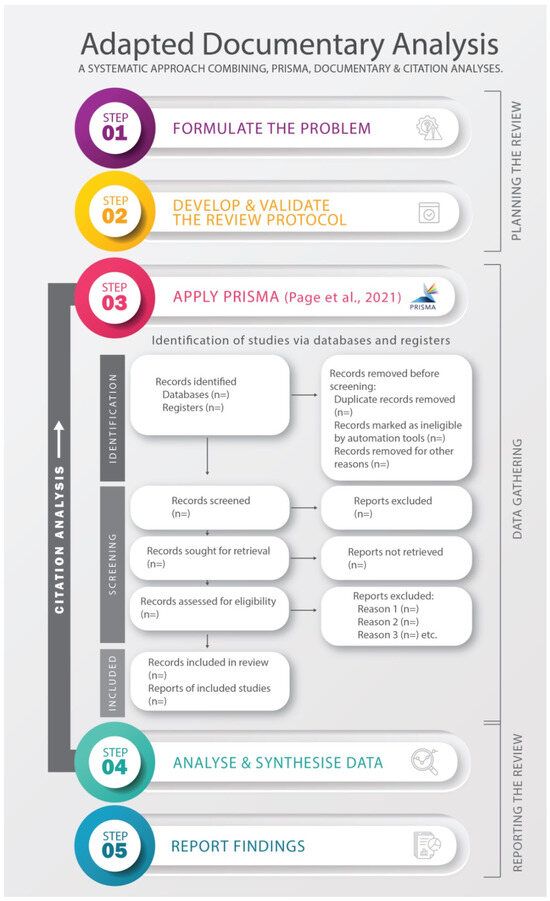

Therefore, this article followed an adapted, yet complementary, newly synthesised documentary analysis, incorporated with PRISMA, which respectively represent a different point of departure from the stand-alone methods already covered in this section. The adaptations provided a platform for presenting a step-by-step rationale for conducting robust, integrative documentary analysis, which, to the authors’ best knowledge, has not been done in the capital structure literature. The attention to systematisation was intended to mitigate bias and build credibility and transparency into the data extraction process, improving the trustworthiness of the results. The adaptation of documentary analysis, the PRISMA protocol, and citation analysis, as applied, is displayed in Figure 1.

Figure 1.

Adapted documentary and citation analyses informed by PRISMA (source: authors).

Secondary data were collected from publicly available databases. Ethical clearance was granted in writing by the applicable institution’s ethics committee, with ethical clearance number SAREC20230314/06.

In Figure 1, the planning stage is set out in Steps 1 and 2. In Step 1, the problem was formulated. The problem, as mentioned before, is the conflicting empirical evidence across a wide variety of determinants and proxies in the vast capital structure literature, which complicates comparability across companies, industries, and countries. To address this concern, this study targeted systematic reviews, bibliometric studies, and meta-analyses in the capital structure literature. In doing so, this research draws on scientific findings from previous authors who conducted wide-ranging studies to identify the most common and prominent capital structure determinants and proxies. Step 2 addresses the development and validation of the review protocol. To establish the protocol, well-chosen search terms were selected to inform the data collection. Based on the problem formulated in Step 1, the search terms were “capital structure” and “systematic review” or “bibliometric” or “meta” to locate systematic reviews, bibliometric studies, and meta-analyses on capital structure. The terms “determinant” and “variable” were explicitly omitted from the search terms to expand the search as broadly as possible.

Part of the protocol includes identifying the databases to be targeted and aligning with the required quality assurance. To bolster the quality of this research, SCOPUS is purposefully selected. SCOPUS is an internationally recognised database containing peer-reviewed literature from accredited scientific journals, conference proceedings, and books. It provides extensive coverage of sources and is regarded by some as one of the largest abstract and citation databases of peer-reviewed literature (Pinto et al., 2020; Priyan et al., 2023). It has also been used in the capital structure literature before (Bajaj et al., 2020; Priyan et al., 2023).

Africa has been identified as a geographical area where focused research with regard to capital structure is needed (Gajdosikova & Valaskova, 2022). Therefore, a database dedicated to African research, such as SABINET, was additionally explored to determine what has been done in the African context. The search in both databases was limited to peer-reviewed articles written in English.

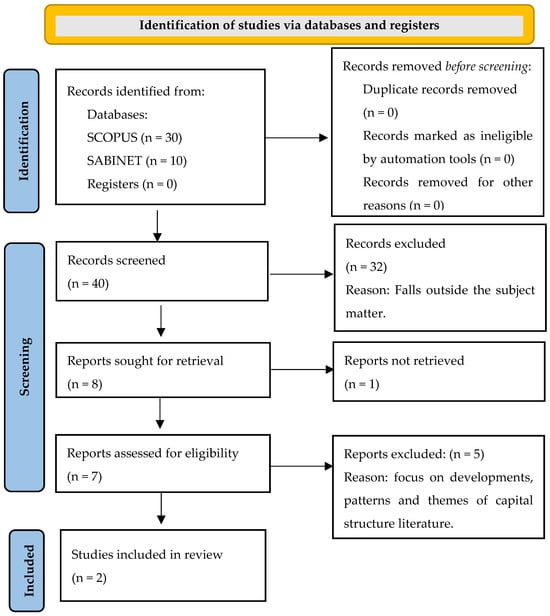

As shown in Figure 1, Step 3 addresses data extraction considerations, including searching the literature, screening for inclusion, assessing quality, and extracting data. The PRISMA protocol is apt for this purpose. For the identification stage, the following search terms were used: “capital structure” and “systematic review” or “bibliometric” or “meta”. The search was conducted on the SCOPUS and SABINET databases from 21 to 25 Aug 2023. In the SCOPUS database, the ‘TITLE-ABS-KEY’ function was used. This function executes full-text searches on titles, abstracts, and authors’ keywords. The search was not limited to document type or time horizon. Therefore, the search included journal articles, book chapters, and conference proceedings. This search produced 30 documents.

Consequently, the same search terms were used for the SABINET database. The advanced search function was used. Because the search functionality differed from SCOPUS, the search was conducted differently. Three searches were necessary—the first, “capital structure” and “systematic review,” returned two documents. The second, “capital structure” and “bibliometric”, returned one document; the third, “capital structure” and “meta”, returned seven documents. Therefore, 10 documents were identified in the SABINET database. In total, 40 documents were identified. There were no duplicates.

In the screening stage, the titles of the 40 identified documents were scanned, and 32 articles were excluded because they did not address the aim of the documentary analysis. The excluded studies were not systematic reviews, bibliometric studies, or meta-analyses of the capital structure literature. The remaining eight documents were identified for retrieval. One document could not be retrieved and was excluded. The remaining seven articles were submitted for a full-text review to determine the final list for analysis. It is evident that, even though no time horizon has been specified for the searches, the seven articles that received a full-text review were published between 2015 and 2023.

After the full-text review, five of the seven articles were excluded. Four of the five excluded articles focused solely on developments, patterns, and themes in the capital structure literature, without identifying the most prominent determinants. Next, as part of judging whether these articles are legible for analysis, a search for the word “determinant” was performed on each article. In doing so, the context could be interpreted. Even though references to “determinant” were detected, they did not include the identification of capital structure determinants through systematic review, bibliometric analysis, or meta-analysis studies. Furthermore, the terms “proxy”, “proxies”, and “measurement” were also searched for, with no mention surfacing. Thus, the decision to exclude these four articles was confirmed, as they did not address proxies for capital structure or its determinants.

The fifth and final excluded article did not identify capital structure determinants through a bibliometric review or meta-analysis. Instead, the capital structure determinants used for their meta-study were based on synthesising the outcomes of two previous studies by Harris and Raviv (1991) and Frank and Goyal (2009). Therefore, no primary identification process was used. This means that the authors did not employ their own investigation to establish the most prominent capital structure determinants until the time of publication. They used the determinants previously identified in articles published in 1991 and 2009.

After excluding five of the seven articles, the remaining two articles were included and submitted for analysis. PRISMA also provides a checklist for the process, and all requirements were met accordingly. The data extraction and final selection processes, according to the PRISMA approach, are depicted in Figure 2.

Figure 2.

PRISMA application to the adapted documentary analysis.

3. Results and Discussion

In Figure 1, Steps 4 and 5 analyse, synthesise, and report the data. To analyse the data, it needs to be organised into categories that relate to the central questions of the research (Bowen, 2009), which was done. The categories considered for improvement in synthesis were year of publication, citations, the time horizon of data collection, data analysis techniques, determinants of capital structure, proxies for identified determinants of capital structure, and proxies for capital structure.

The synthesis involves comparing the similarities and differences among the extracted studies using criteria such as study quality, findings, and context. According to Xiao and Watson (2019), there are many ways to synthesise data. The textual narrative synthesis method was deemed suitable for this research involving two articles, as it requires a standardised data extraction format supported by the PRISMA protocol. Details of the two articles included in the adapted documentary analysis are summarised in Table 1.

Table 1.

Articles included in documentary analysis (source: authors).

3.1. Year of Publication, Citations, and Time Horizon

The year of publication, number of citations, and the time horizon are identified to determine the possible value of Articles 1 and 2. In academia, it is assumed that ‘important works will be cited more frequently than others’ (Meho, 2007, p. 32). Therefore, Article 1, published in 2017, had 220 citations on 29 November 2023. Article 2, published in 2018, received 102 citations on the same date. The date of publication and the number of citations are also indicated in Table 1.

Equally important is the time horizon of the articles under review, as it indicates the extent of the search each review covers. The search in Article 1 started in 1958. The year 1958 marked the seminal work of Modigliani and Miller (1958). However, the authors of Article 1 established that the literature on capital structure determinants emerged only in 1972. Therefore, their data ranged from 1972 to 2013. Their sample comprised 167 peer-reviewed articles in the EBSCO, SSRN, and Google Scholar databases.

The literature search for Article 2 covered the ABI/INFORM Complete, Business Source Premier, EconLit, and GreenFILE through EBSCOhost and ProQuest databases. The authors also used the recursive RePEc Journal Impact Factor to perform the valuation of the journals as guidance for the inclusion of studies in their sample. The authors followed a unique sampling strategy. Apart from targeting high-end journals, they also search for unpublished work in the electronic database for working papers, SSRN, to search for dissertations, working papers, and conference papers. Their initial sample consisted of 591 primary empirical studies. Since statistical independence is required for the meta-analysis technique they had employed, a study was scrutinised to ensure statistical independence before it was included in the final sample. Therefore, if there were any indication of double-counting, such an article was excluded. The authors also complied with the established guidelines published by the Meta-Analysis of Economics Research Network. Their final sample comprised 100 studies, totalling 3890 observations. The data ranged from 1975 to the beginning of 2016.

There is some overlap between the two articles regarding databases and time horizons. The years covered by the two articles span from the initial emergence of the capital structure determinant literature in 1972 to the beginning of 2016. The end of the time horizon for Articles 1 and 2 leaves room for a forward-looking search. The forward-looking search can be executed by employing citation analysis. The exploration of this possibility will be discussed later in this paper. For now, the documentary data analysis is presented.

3.2. Data Analysis Techniques

Understanding the data analysis techniques used in the selected articles is important, as they relate to the validity of the findings. A systematic literature review and a meta-analysis were employed in Article 1. Additionally, to inform the validity of their findings, the authors did not perform the analysis to identify the determinants of capital structure by way of counting, since counting can produce errors in an analysis. Counting also gives equal weight to each study, regardless of the number of observations per study. The authors mitigated the error that can arise from counting by employing two quantitative procedures: the combined significance test and the effect size index. Furthermore, the Weighted Stouffer Test (WST) was applied to give greater weight to studies with more observations than to those with fewer.

A different approach was followed for Article 2. A multiple meta-regression analysis was employed. The funnel asymmetry test (FAT) and the precision effect test (PET) were used to detect publication bias and calculate the effect size. This mechanism allows for a detailed analysis of misspecification bias, which addresses the concern previously raised by Graham and Leary (2011).

Therefore, even though the data analysis techniques used in the two articles differ, both incorporated methods to ensure valid and reliable results in identifying the significant capital structure determinants.

3.3. Identified Capital Structure Determinants

Through a sample size of 167 articles, eight primary determinants were identified in Article 1. The determinants are profitability, tangibility, size, age, growth, liquidity, risk, and non-debt tax shield (NDTS). In comparison, in Article 2, the authors initially identified 14 frequently used capital structure determinants in their sample of 100 articles. The determinants include the following: tangibility, non-debt tax shield, firm growth, firm size, market-to-book ratio (growth opportunities), earning volatility (business risk), profitability, firm age, liquidity, dividend yield, corporate tax rate, advertising, research and development, and lastly, a lagged variable for capital structure. The authors then narrowed it to the seven most frequently used capital structure determinants: tangibility, NDTS, firm growth, firm size, market-to-book ratio (growth opportunities), earnings volatility (business risk), and profitability.

When the findings of Articles 1 and 2 are compared, nine different determinants are identified and are presented in Table 2. Both articles identified six of the nine determinants as primary or most frequently used, namely profitability, tangibility, firm size, firm growth, NDTS, and earnings volatility. The two studies differ in their views on the importance of liquidity, firm age, and growth opportunities. Liquidity and firm age were only identified as important determinants in Article 1, whereas growth opportunities, as a determinant, were only identified in Article 2.

Table 2.

Comparison of the most prominent firm-related capital structure determinants (source: authors).

In Article 2, a further elaboration by way of ranking was provided. The authors identified the three most important determinants in descending order as tangibility, growth opportunities, and profitability. No specific order of preference was provided in Article 1. However, in Article 1, profitability was identified as a prime explanatory capital structure determinant, and tangibility was also found to be an important determinant. Therefore, both articles agree on the prominence of profitability and tangibility as firm-related determinants of capital structure.

3.4. Proxies for Identified Determinants of Capital Structure

Regarding the nine identified determinants in Table 2, various proxies per determinant have been identified. Based on the explanations and proxy variations provided in each article, some proxies could be matched. The comparison of the proxies between Articles 1 and 2 is presented in Table 3. Six of the previously identified nine determinants have a matched proxy. Matched proxies are indicated in grey in Table 3.

Table 3.

Identified proxies per article (source: authors).

However, there is one exception. Article 1 used the market-to-book value of equity ratio (MTB) as a proxy for firm growth, whereas Article 2 used MTB as a proxy for growth opportunities. This match has been indicated in bold. In Article 2, it has been documented that MTB was the proxy (growth opportunities) ranked as the second most impactful determinant on capital structure, providing merit for inclusion. Therefore, even though there is a difference in what the proxy represents between Article 1 and Article 2, it is important to include the MTB of equity as a proxy. Based on this analysis, a clear indication of the firm-related proxies to be utilised has emerged.

3.5. Proxies for Capital Structure

Article 1 did not attempt to differentiate between different measurements of capital structure. However, important findings have been documented in Article 2. The authors of Article 2 distinguished between different measurements of capital structure. Capital structure proxies were analysed based on the debt-equity ratio. They accounted for measurement differences relating to market leverage, book leverage, and whether total debt was used as the proxy for capital structure.

The first distinction was between market-based measurements and book value measurements. Based on the number of extracted effect sizes, where equity is measured in book value, 712 effect sizes were documented. In comparison, only 329 effect sizes were documented when equity was measured in market value. However, when the authors compared the PET and FAT tests, they found remarkable differences between market leverage and book leverage results. Market leverage measurements suffered from publication selection, and therefore, the authors judged the book value-based capital structure ratios to be more reliable than market-based measurements.

The second distinction addressed by the authors was whether capital structure ratios accommodating total debt were more reliable than when long-term or short-term debt was utilised in the capital structure ratio. The number of effect sizes documented for total debt was 705, compared to 337 for long-term debt. More consistent effects were observed when total debt was used in the capital structure ratio. The authors do not provide a clear recommendation for the preferred measurement, leaving one to interpret the context of a particular study to establish the measurement of choice.

3.6. Going Beyond Documentary Analysis

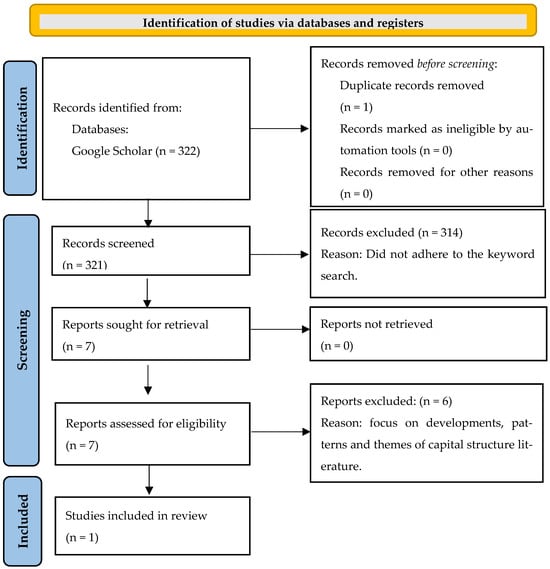

The outcome of the documentary analysis reflects what happened in past scholarship of the two selected articles’ reviews up to 2016. It provides a much-needed consolidation of the most prominent internal capital structure determinants across the vast capital structure literature. However, it is a concern that years have passed since 2016, hence emphasising the gaps that this article demonstrates. Additionally, if the search terms of the documentary analysis did not align with an article’s keywords, it would have caused a possible target article to be automatically excluded from the documentary analysis. As noted earlier, citation analysis is an effective tool to mitigate these concerns and to implement a forward-looking perspective, as illustrated in Figure 1.

To this end, a citation analysis limited to Articles 1 and 2 was performed on 29 November 2023 on Google Scholar. The number of citations of Articles 1 and 2 was 220 and 102, respectively. The total number of titles was 322. To determine which articles should be included in the citation analysis, the PRISMA approach was implemented again to provide a systematic process of identification, screening, and inclusion, in this case, of cited articles. To this end, the necessary keywords for the identification process were derived from the titles of Articles 1 and 2, which are: Article 1: “Research on capital structure determinants: a review and future directions” and Article 2: “Measurement matters—A meta-study of the determinants of corporate capital structure”.

As indicated in bold, the keywords “review” or “meta” combined with “capital structure” were deemed appropriate. One duplication was detected in the 322 citations identified on 29 November 2023. The same article was cited by both Articles 1 and 2. Therefore, the titles of the reduced list of 321 cited articles were scanned for the identified keywords. Seven articles were identified after 314 articles were excluded. These seven articles were then submitted for further investigation by reading the abstracts and scanning the articles. The results of the PRISMA approach followed for the citation analysis are shown in Figure 3.

Figure 3.

PRISMA application for the citation analysis.

It was found that of the seven articles, two articles conducted a review of capital structure theories; one conducted a review to detect the patterns in capital structure literature; another conducted a review on firm performance in relation to capital structure; one article reviewed the relationship between chief executive characteristics and capital structure which fell outside this study’s scope and will inform part of recommendation for further research; one article focused on the relationship between macroeconomic and institutional environment and firm-related capital structure determinants and the focus was not the exploration of identifying additional capital structure determinants and only used previously identified capital structure determinants from Harris and Raviv (1991) and Frank and Goyal (2009); in the last article, entitled ‘Influencing factors that determine capital structure decisions: A review from the past to present’ (Boateng et al., 2022), the authors addressed firm-related capital structure determinants. Therefore, this article was submitted for a full-text review and is hereafter referred to as Article 3. Article 3 covers a time horizon from 2014 to 2020.

Article 3 is of particular interest because it explicitly states that it was an extension of Article 1, as reported in the preceding documentary analysis. The authors of Article 3 specifically state that they have extended the time horizon of Article 1, which ended in 2013. Therefore, their time horizon stretched from 2014 to 2020. It was noted that they had applied the same methodology as in Article 1. They also expanded the number of sources to include additional databases such as ScienceDirect, JSTOR, and Sage. Based on the focus and execution, Article 3 is suitable for establishing whether further developments have occurred in identifying capital structure determinants. Their final sample consisted of 68 articles. Importantly, the authors did not identify any additional firm-related capital structure determinants in Article 3.

Since Article 3 is an article based on SCOPUS, it was puzzling why Article 3 was not part of the initial documentary analysis data search. Further analysis revealed that none of the chosen search terms for the documentary analysis were keywords for Article 3. Because the search terms and keywords did not align, Article 3 was not included in the initial documentary analysis sample. Therefore, this endorsed the need for a follow-up citation analysis and ensured that the findings from the current study were not dated.

Therefore, this research proposes a more refined list of the six most prominent capital structure determinants and their measurements to be used, summarised in Table 4. They are tangibility, growth proxied by the market-to-book ratio of equity, profitability, firm size, NDTS, and business risk. The first three most prominent determinants listed in Table 4 were also ranked in descending order by Article 2. The authors of Articles 1 and 2 agree that tangibility and profitability are the most important firm-related determinants of capital structure.

Table 4.

The consolidated list of the most prominent firm-related capital structure determinants and preferred measurements (source: authors).

4. Discussion

The list of six capital structure determinants takes on a specific dimension, underscoring their importance for firms’ financing decisions. Tangibility addresses the issue of firms with a larger proportion of fixed assets, which they use as collateral to negotiate better financing terms and thereby support value creation (Frank & Goyal, 2009). MTB is an interesting firm-related variable. It is viewed as a proxy for growth opportunities (Rajan & Zingales, 1995) and market mispricing (Baker & Wurgler, 2002). When stock prices are high, MTB is high. Under the market timing theory, firms will then tend to issue equity to raise capital. This can be ascribed to MTB being the sole determinant of the financing choice under this theory (Hang et al., 2018). If market timing drives the financing decision, firms will tend to exploit the overvalued mispricing by issuing equity (Frank & Goyal, 2009). Therefore, leverage should be lower in a bull market, suggesting a negative relationship between MTB and capital structure (Baker & Wurgler, 2002; Frank & Goyal, 2009; Hang et al., 2018). Conversely, this implies that low stock prices, which lower MTB, will support debt issuance as a preferred financing option (Frank & Goyal, 2009). In the case of MTB representing company growth, the pecking order theory supports a positive relationship, suggesting that as firms grow, they deplete their internal financing and turn to debt financing, while the trade-off theory indicates a negative relationship (Frank & Goyal, 2009). When a company uses debt financing to support its growth, it may lead to over-leveraging, especially if it is already operating at its optimal capital structure.

Profitability can be empirically supported by both the trade-off theory and the pecking order theory, but the relationship differs across the two theories. A positive relationship between capital structure and profitability is supported by the trade-off theory, since a firm’s profitability determines how much debt it can take on, consequently increasing the capital structure ratio (Frank & Goyal, 2009). In contrast, the negative relationship is supported by the pecking order, since firms will exercise financial flexibility to subsidise positive net present value projects (Rajan & Zingales, 1995; Kumar et al., 2017). Higher profits increase retained earnings, which is the preferred source of financing under the pecking order theory. Consequently, delaying debt financing affects the capital structure.

The same applies to size as a determinant. Larger firms typically find it easier to obtain debt financing, can often secure more favourable interest rates, and have a lower likelihood of bankruptcy (Delcoure, 2007). This observation supports the positive relationship between profitability and capital structure suggested by the trade-off theory. In contrast, the pecking order theory posits a negative relationship, arguing that larger and more profitable firms are more likely to prefer internal financing, such as retained earnings, as their first choice (Titman & Wessels, 1988). Then, NDTS includes depreciation and amortisation alongside debt financing. Therefore, this aligns with predictions from the pecking order theory. NDTS tax-saving potential will discourage firms from employing debt financing (Moradi & Paulet, 2019).

Then, the business risk associated with earnings volatility suggests that the trade-off theory supports a negative relationship between capital structure and earnings volatility. As earnings become more volatile, the likelihood of bankruptcy increases. This scenario will encourage companies to reduce their debt levels, thereby lowering their bankruptcy risk and decreasing the capital structure ratio. Additionally, the pecking order theory can also be seen as supporting a negative relationship between business risk and capital structure.

Together, these prominent capital structure determinants highlight the complex interplay shaping firms’ financing behaviour, underscoring the need for informed, theoretically grounded capital structure decisions. However, by identifying the six prominent capital structure determinants, greater simplicity is achieved.

5. Conclusions

The capital structure determinant literature is vast, and synthesising the conflicting empirical evidence is daunting, often leading to a biased selection of firm-specific capital structure determinants. Additionally, many managers apply rough heuristic decision-making, referring to the rule of thumb or reasonable financial decision-making (DeAngelo, 2022). Therefore, this study aimed to establish a more robust synthesis of the most prominent firm-related capital structure determinants and their appropriate measurements to foster consolidation within the vast capital structure literature.

For this endeavour, documentary and citation analyses were included as methodology. Since documentary analysis is qualitative, it may be criticised for being biased. Therefore, it was deemed necessary to establish a novel process. For this purpose, the three-staged systematic approach prescribed by Quinlan et al. (2015) is extended with eight steps provided by Xiao and Watson (2019) in conjunction with the data-extraction checklist proposed by the PRISMA approach, which provides a credible pathway to synthesise the existing literature. Due to the vastness of the literature on capital structure determinants, a novel approach was employed to focus on systematic reviews, bibliometric studies, and meta-analyses. To the best of the researchers’ knowledge, this approach has not been executed in the capital structure literature before.

The documentary analysis produced two articles, which can be viewed as a limitation. However, these two articles analysed 267 studies from 1972 until the beginning of 2016. Both articles applied a meticulous and rigorous process to produce valid and reliable results. The comparison between the two articles resulted in the six most prominent firm-related capital structure determinants. The most prominent measurements for these six firm-related capital structure determinants were also identified.

Since the data of the documentary analysis ended in 2016, it was deemed necessary to go beyond its findings and conduct a follow-up citation analysis, also informed by PRISMA, that extended to the end of 2023. A third article analysing a further 68 articles was identified. However, no additional capital structure determinants were identified.

The result was a list of the six most prominent firm-related capital structure determinants and their associated measurements, identified as a consolidation of 335 articles through a systematic approach. Considering the large number of articles, this rigorous process provides credibility to the outcome. Therefore, this attempt is a credible consolidation of firm-related capital structure determinants and associated measurements. The six most prominent firm-related determinants were confirmed as tangibility, growth proxied by MTB, profitability, firm size, NDTS, and business risk.

Notably, a ranking of the importance of capital structure determinants was established in Article 2. Tangibility was ranked the most prominent factor, followed by growth opportunities proxied by MTB and profitability. Article 1 used MTB, among others, to proxy firm growth, whereas Article 2 used it specifically to proxy growth opportunities. Nonetheless, MTB is an important proxy to include in capital structure studies. Regarding proxies for capital structure, the book value of leverage proved more reliable.

Reliance on SCOPUS and SABINET databases is a limitation; future studies focusing on other databases would be helpful. Additionally, a follow-up study will be beneficial, as more systematic reviews, bibliometric studies, and meta-analyses are foreseen to be published. Future studies identifying underexplored capital structure determinants, particularly in the context of emerging trends such as ESG considerations and digital transformation, can also offer fresh insights into firms’ financing decisions.

The consolidated list of the six most prominent firm-related capital structure determinants and their associated measurements creates an easy-to-use guide for researchers and managers. This consolidated list helps managers identify key determinants for financing decisions related to their firm, especially in an increasingly dynamic and complex business environment. It guides managers to prioritise tangibility, MTB, and profitability as the key focus areas when financing decisions arise. For researchers, it provides a credible, user-friendly foundation for further studies. Additionally, it provides an integrative platform that supports capital structure investigations aimed at identifying underexplored variables, as this list can serve as a solid foundation for control variables.

Additionally, qualitative research is rarely conducted in the context of capital structure, which is the focus of this paper. This paper also offers a methodological contribution through an adapted documentary analysis that combines documentary analysis with PRISMA and forward-looking citation analysis. The adapted documentary analysis provides an easy-to-use framework for conducting documentary analysis with enhanced credibility and transparency.

Author Contributions

Conceptualisation, M.M.; methodology, M.M.; validation, M.M. and I.B.; formal analysis, M.M.; investigation, M.M.; resources, M.M.; data curation, M.M.; writing—original draft preparation, M.M.; writing—review and editing, M.M. and I.B.; visualisation, M.M.; supervision, I.B.; project administration, M.M. and I.B. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Dataset available on request from the authors.

Acknowledgments

Our thanks are extended to Charmaine Williamson for her valuable feedback as an internal reviewer and to Lillian Gray Rabe for the artwork featured in the Adapted documentary analysis figure.

Conflicts of Interest

The authors declare no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| PRISMA | Preferred Reporting Items for Systematic Reviews and Meta-Analyses |

| MTB | market-to-book value of equity |

| NDTS | non-debt tax shield |

References

- Bajaj, Y., Kashiramka, S., & Singh, S. (2020). Application of capital structure theories: A systematic review. Journal of Advances in Management Research, 18(2), 173–199. [Google Scholar] [CrossRef]

- Baker, M., & Wurgler, J. (2002). Market timing and capital structure. Journal of Finance, 57(1), 1–32. [Google Scholar] [CrossRef]

- Boateng, P. Y., Ahamed, B. I., Soku, M. G., Addo, S. O., & Tetteh, L. A. (2022). Influencing factors that determine capital structure decisions: A review from the past to present. Cogent Business and Management, 9(1), 2152647. [Google Scholar] [CrossRef]

- Bowen, G. A. (2009). Document analysis as a qualitative research method. Qualitative Research Journal, 9(2), 27–40. [Google Scholar] [CrossRef]

- DeAngelo, H. (2021). Corporate financial policy: What really matters? Journal of Corporate Finance, 68, 101925. [Google Scholar] [CrossRef]

- DeAngelo, H. (2022). The capital structure puzzle: What are we missing? Journal of Financial and Quantitative Analysis, 57(2), 413–454. [Google Scholar] [CrossRef]

- Delcoure, N. (2007). The determinants of capital structure in transitional economies. International Review of Economics & Finance, 16, 400–415. [Google Scholar] [CrossRef]

- Demirgüneş, K. (2017). Capital structure choice and firm value: New empirical evidence from asymmetric causality test. International Journal of Financial Research, 8(2), 75–91. [Google Scholar] [CrossRef][Green Version]

- Donaldson, G. (1961). Corporate debt capacity: A study of corporate debt policy and the determination of corporate debt capacity. Beard Books. [Google Scholar]

- Frank, M. Z., & Goyal, V. K. (2009). Capital structure decisions around the world: Which factors are reliably important? Journal of Financial and Quantitative Analysis, 50(3), 301–323. [Google Scholar] [CrossRef]

- Gajdosikova, D., & Valaskova, K. (2022). A systematic review of literature and comprehensive bibliometric analysis of capital structure issue. Management Dynamics in the Knowledge Economy, 10(3), 210–224. [Google Scholar] [CrossRef]

- Graham, J. R., & Leary, M. T. (2011). A review of empirical capital structure research and directions for the future. Annual Review of Financial Economics, 3, 309–345. [Google Scholar] [CrossRef]

- Hang, M., Geyer-Klingeberg, J., Rathgeber, A. W., & Stöckl, S. (2018). Measurement matters—A meta-study of the determinants of corporate capital structure. Quarterly Review of Economics and Finance, 68, 211–225. [Google Scholar] [CrossRef]

- Harris, M., & Raviv, A. (1991). The theory of capital structure. Journal of Finance, XLVI(1), 297–355. [Google Scholar] [CrossRef]

- Jensen, C., & Meckling, H. (1976). Theory of the firm: Managerial behaviour, agency costs and ownership structure. Journal of Financial Economics, 3, 305–360. [Google Scholar] [CrossRef]

- Klestov, M., & Jindřichovská, I. (2021). The determinants of debt load for companies in emerging markets. Journal of Corporate Finance Research, 15(3), 39–59. [Google Scholar] [CrossRef]

- Kraus, A., & Litzenberger, R. H. (1973). A state-preference model of optimal financial leverage. The Journal of Finance, 28(4), 911–922. [Google Scholar] [CrossRef]

- Kumar, S., Colombage, S., & Rao, P. (2017). Research on capital structure determinants: A review and future directions. International Journal of Managerial Finance, 13(2), 106–132. [Google Scholar] [CrossRef]

- Kurznack, L., Schoenmaker, D., & Schramade, W. (2021). A model of long-term value creation. Journal of Sustainable Finance and Investment, 1–19. [Google Scholar] [CrossRef]

- Meho, L. I. (2007). The rise and rise of citation analysis. Physics World, 20(1), 32–36. [Google Scholar] [CrossRef]

- Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. The American Economic Review, 48(3), 261–297. [Google Scholar]

- Modigliani, F., & Miller, M. H. M. (1963). Corporate income taxes and the cost of capital: A correction. American Economic Review, 53(3), 433–443. [Google Scholar]

- Mokhova, N., & Zinecker, M. (2014). Macroeconomic factors and corporate capital structure. Procedia—Social and Behavioral Sciences, 110, 530–540. [Google Scholar] [CrossRef]

- Moradi, A., & Paulet, E. (2019). The firm-specific determinants of capital structure—An empirical analysis of firms before and during the Euro Crisis. Research in International Business and Finance, 47, 150–161. [Google Scholar] [CrossRef]

- Myers, S. C. (1984). Capital structure puzzle. Journal of Finance, 39, 575–592. [Google Scholar] [CrossRef]

- Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. [Google Scholar] [CrossRef]

- Page, M. J., McKenzie, J. E., Bossuyt, P. M., Boutron, I., Hoffmann, T. C., Mulrow, C. D., Shamseer, L., Tetzlaff, J. M., Akl, E. A., Brennan, S. E., Chou, R., Glanville, J., Grimshaw, J. M., Hróbjartsson, A., Lalu, M. M., Li, T., Loder, E. W., Mayo-Wilson, E., McDonald, S., … Moher, D. (2021). The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. The BMJ, 372, 1–12. [Google Scholar] [CrossRef]

- Pinto, G., Rastogi, S., Kadam, S., & Sharma, A. (2020). Bibliometric study on dividend policy. Qualitative Research in Financial Markets, 12(1), 72–95. [Google Scholar] [CrossRef]

- Priyan, P. K., Nyabakora, W. I., & Rwezimula, G. (2023). A bibliometric review of the knowledge base on capital structure decisions. Vision, 27(2), 155–166. [Google Scholar] [CrossRef]

- Quinlan, C., Babin, B., Carr, J., Griffin, M., & Zikmund, W. (2015). Business research methods. Cengage Learning. [Google Scholar]

- Rajan, R. G., & Zingales, L. (1995). What do we know about capital structure ? Some evidence from international data. The Journal of Finance, 50(5), 1421–1460. [Google Scholar] [CrossRef]

- Ross, S. A. (1977). The determination of financial structure: The incentive-signalling. The Bell Journal of Economics, 8(1), 23–40. [Google Scholar] [CrossRef]

- Roy, S., & Sen, C. (2022). Role of debt in emerging economies: A re-examination of the debt-growth nexus. Macroeconomics and Finance in Emerging Market Economies, 17(2), 227–248. [Google Scholar] [CrossRef]

- Sisodia, A., & Maheshwari, G. C. (2022). Capital structure study: A systematic review and bibliometric analysis. Vision, 2022, 09722629221130453. [Google Scholar] [CrossRef]

- StatsSA. (2019). Sustainable development goals: Country report. StatsSA.

- Titman, S., & Wessels, R. (1988). The determinants of capital structure choice. The Journal of Finance, 43(1), 1–19. [Google Scholar] [CrossRef]

- Vatavu, S. (2012). Trade-off versus pecking order theory in listed companies around The world. Annals of the University of Petroşani, Economics, 12(2), 285–292. [Google Scholar]

- Xiao, Y., & Watson, M. (2019). Guidance on conducting a systematic literature review. Journal of Planning Education and Research, 39(1), 93–112. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.