1. Introduction

Since Bitcoin was invented in 2008 (

Nakamoto 2008), more than 10,707 new cryptocurrencies (

Investing 2022) have been created (as of March 2022). Generally, a cryptocurrency is a digital currency that is designed to work as a medium of intermediate exchange. Cryptocurrencies are decentralized digital currencies that are not issued by any jurisdictional authority. All transactions of cryptocurrencies are written in a big, distributed ledger that can be copied by every participant assigned to a node of the blockchain network. Cryptocurrencies are secured by encryption hash algorithms, signed with a digital signature, timestamped, and verified by participants to ensure security and prevent fraud (

Silvia 2019).

Blockchain technology is the supporting technology that underlies cryptocurrencies. Cryptocurrencies are crypto assets, which are digitized by blockchain technology. Crypto assets are the most important financial assets in modern financial markets. Crypto assets impact elements of modern finance including highways, mobile phones, and the Internet. Blockchain technology has led to a revolutionary change to potentially many service industries, including finance and banking. Blockchain technology has become an innovative medium and transaction system with high value (

Boring 2019).

On 5–6 March 2019, in London, the International Financial Reporting Standards (IFRS) Interpretations Committee (IFRSIC) held a meeting and discussed how the IFRS standards could apply to the holding of cryptocurrencies. A tentative agenda decision on holdings of cryptocurrencies was published. According to the tentative agenda decision, the

IFRSIC (

2019a) noted that cryptocurrencies are crypto assets.

A cryptocurrency is a digital currency that is recorded on a distributed ledger. For security, it is encrypted by a mathematical cryptography algorithm. A cryptocurrency is not as legal as a fiat currency issued by a jurisdictional authority or a central bank. Most cryptocurrencies are issued by private companies, which do not have any issuing permissions from the central government. The holders of cryptocurrencies do not have any legal contracts as they usually do in traditional financial markets (

IFRSIC 2019a).

Based on the tentative agenda decision,

IFRSIC (

2019a) proposed that the IAS 2 Inventories accounting standard is the accounting rule that best fits the holding of cryptocurrencies. As in the ordinary course of business, when holders want to sell their crypto assets, the best accounting rule is the IAS 2 Inventories. The

IFRSIC (

2019a) also proposed that if the IAS 2 Inventories accounting standard is not appropriate for holdings of cryptocurrencies, another good choice is the IAS 38 Intangible Assets accounting standard. In most cases, IAS 38 will be the best accounting standard for holdings of cryptocurrencies.

After the tentative agenda decision was published by the

IFRSIC (

2019a), many accounting bodies worldwide, including accounting firms and accountants, made comments to the IFRSIC. As of 15 May 2019, at least 20 comment letters had been received by the

IFRSIC (

2019b, Comment letters). These comments represent the major opinions of the accounting industry on holdings of cryptocurrencies. This was the first time that the issue of cryptocurrency holding had been a focus of accounting bodies.

However, there have not been any comments from Mainland China. Do the Chinese accounting bodies not care about the issues of cryptocurrency holding?

Actually, since Bitcoin was created in 2008, the trend of cryptocurrency holding by private companies and individuals has been rapidly increasing in China. However, in contrast to the enthusiasm from private companies and individuals about cryptocurrency holding, the Chinese government has set up a number of regulations to prevent the widespread purchase of cryptocurrencies in China. The conflict between the private holding of cryptocurrencies and the government regulations means that no Chinese accounting body has made a statement on the suggestions of the

IFRSIC (

2019a). Although the exchange of cryptocurrencies is prohibited by the Chinese government, holdings of cryptocurrencies by Chinese entities and individuals cannot be prevented. Although there are a number of governmental regulations to prevent the exchange of cryptocurrencies in China, when dealt with as a technical problem, it is necessary to consider how to record the holdings of cryptocurrencies in financial statements. As long as some Chinese entities and individuals still hold cryptocurrencies, this will continuously be a question related to accounting standards. On the other hand, even if Chinese accounting bodies do not care about this issue, many international accounting bodies do. If the Chinese accounting bodies do not consider the implications of this issue in China now, it will be a continuous issue in the future. Thus, the motivation of this study was to investigate this issue now in relation to the situation in China.

On 3 December 2013, five Chinese central government regulators, including The People’s Bank of China (PBOC), jointly issued a governmental document named A Circular on Preventing Risks Related to Bitcoin (

CSRC 2013) in which the Chinese central government regulators warn that no Chinese financial institution can offer its services to Bitcoin. The Chinese central government regulators noted that Bitcoin may be defined as a special virtual commodity in nature, but because it does not have any legal status as fiat currencies do, it must not be used or circulated in circulation markets as a currency in China. The Chinese central government regulators stated that Bitcoin has no central issuer, a limited total volume, no territory restrictions for its use, and anonymous users. In China, Bitcoin is not seen as a real currency although it is called a currency. Because it is not issued by monetary authorities, it does not have the characteristics of currency in terms of legal compensation and mandatory payment. For these reasons, the Chinese central government regulators have asked that the national financial institutions do not provide any bitcoin-related businesses or services. The Chinese central government regulators also require online Bitcoin exchanges to be filed as trading records, and measures must be taken to prevent speculative trading and money-laundering risks associated with bitcoin. The Chinese central government regulators have warned that if individuals use Bitcoin, then any risks related to Bitcoin will be taken by themselves (

Zhu 2013).

Although Bitcoin-related business is prohibited by the Chinese regulators, many cryptocurrencies were used in China. Along with the development of cryptocurrencies in China, further regulations were published by the Chinese government.

On 4 September 2017, seven Chinese central government regulators, including the PBOC (

CSRC 2017), again jointly issued a governmental document, named The Announcement on Preventing Financial Risks from Initial Coin Offerings (ICO Rules). Its purpose is to protect investors from financial risks. Under the ICO Rules, ICOs that raise cryptocurrencies are illegal in China. Cryptocurrencies, such as Bitcoin, Ethereum, and others, are considered illegal cryptocurrencies, and their issue and trading are prohibited in China by the Chinese government. If an investor tries to raise money by issuing cryptocurrencies on the black market or selling cryptocurrencies through an irregular trading channel, his or her illegal behavior is prohibited by the Chinese government. Because cryptocurrencies involved in ICOs are not issued by the Chinese official authorities, they are not legally accepted as a fiat currency in China (

LLC 2018).

On 3 September 2021, eleven top Chinese economic regulators, including the National Development and Reform Commission (

NDRC 2021), jointly issued a tightened regulation named the Notice on Regulating the Activities of Virtual Currency Mining. According to the notice, because virtual currency mining has many negative impacts on the economy, such as energy wastage and the creation of carbon emissions, which do not promote industrial development or technological improvements, industrial entities will be strictly punished if they engage in mining Bitcoin or other virtual currencies. The main punitive measures are the imposition of high electricity prices on state-owned and private companies undertaking virtual currency mining activities that would otherwise pay household electricity prices.

On 24 September 2021, ten Chinese central government regulators, including the

PBOC (

2021), jointly issued a more tightened regulation on virtual-currency trading and speculation, which is named The Notice on Further Preventing and Disposing of the Risk of Hype in Virtual Currency Trading. Based on the new notice, cryptocurrency trading in China was totally cracked down on. Because there was a concern that financial transactions of cryptocurrencies will have big negative impacts on the Chinese economic and financial order, these kinds of activities were made illegal and were banned in the country. According to the notice of the

PBOC (

2021), the main negative activities that may result from financial transactions of cryptocurrencies include financial gambling, illegal fund-raising, commercial fraud, pyramid scheme investments, money laundering, and serious threats to the safety of people’s property. Immediately, all cryptocurrency-related business activities were defined as illegal and strictly banned in China.

Although the mining of virtual currency and the trading of cryptocurrencies are banned based on the regulations announced by the Chinese government, in fact, some individuals and companies do hold cryptocurrencies in China. It is thus necessary to do a survey on holdings of cryptocurrencies in China. Except for the regulations, technically, it is necessary to discuss how transactions of cryptocurrencies should be recorded in financial statements. As China’s central bank is developing a digital currency electronic payment (DCEP) system (

Xinhua 2020), a survey of holdings of cryptocurrencies will provide some useful suggestions for policy makers.

Generally, under the reform and opening up policy, the Chinese government usually prefers to operate and test its new business policies in a special economic zone (SEZ) or in a pilot free trade zone (FTZ). For example, according to the 2020 annual report (

Meitu 2021), during the year ended 31 December 2021, the company of Meitu

1 had invested 940.88523 units of Bitcoin and 31,000 units of Ethereum, and were accounted as intangible assets approximately US

$45.1 million and US

$117.3 million when revaluated by using the prevailing market prices of fair values (

Meitu 2022). Moreover, on 12 October 2020, the PBOC issued CNY 10 million (about USD 1.47 million) of its first digital currency, known as Digital Renminbi, in Shenzhen (

Xinhua 2020). These were the first SEZs and FTZs in China. Because the Digital Renminbi is not a cryptocurrency like Bitcoin, we do not discuss it in this paper. However, if a cryptocurrency is used as a reference to the Digital Renminbi, the survey on cryptocurrencies can provide some reference suggestions for the government.

Since the first pilot free trade zone was set up in 2013, China has established 18 pilot FTZs (

CGTN 2019). Setting up new pilot FTZs is a strategic policy to improve the degrees of the Chinese reform and opening up in the new era. In China, the pilot FTZs are meant to serve as pioneers of the country’s reform and opening up. For better integration of the domestic economy with international practices, the Chinese government has given some special policies to the pilot FTZs. Before a new opening up policy is implemented in the country, it can be firstly implemented and tested in the pilot FTZs.

Xiamen City became a special economic zone (SEZ) in 1980 and a pilot free trade zone (FTZ) in 2015. Based on the support from the Xiamen City Federation of Social Science Associations (

XMSK 2020), we conducted survey focusing on the issue of whether it would be possible for the Chinese government to allow people within the SEZ and FTZ of Xiamen City to trade cryptocurrencies. If this is possible, how do we deal with holdings of cryptocurrencies in accounting? To answer these questions, we conducted a survey in Xiamen City. We discuss the majority opinions from the global accounting industry and present the results of the survey conducted in Xiamen City.

3. A Survey of the Accounting Industry on Holdings of Cryptocurrencies

3.1. Survey Results from the Xiamen City, China

In order to provide meaningful feedback on how to deal with holdings of cryptocurrencies in accounting, we conducted a survey of the industry in Xiamen City, China, from April to September 2020.

First, basic information of the respondents was collected.

During the survey, a total of 1013 valid questionnaires were collected. About 60% of the respondents were male, and the other 40% of the respondents were female (

Table A1).

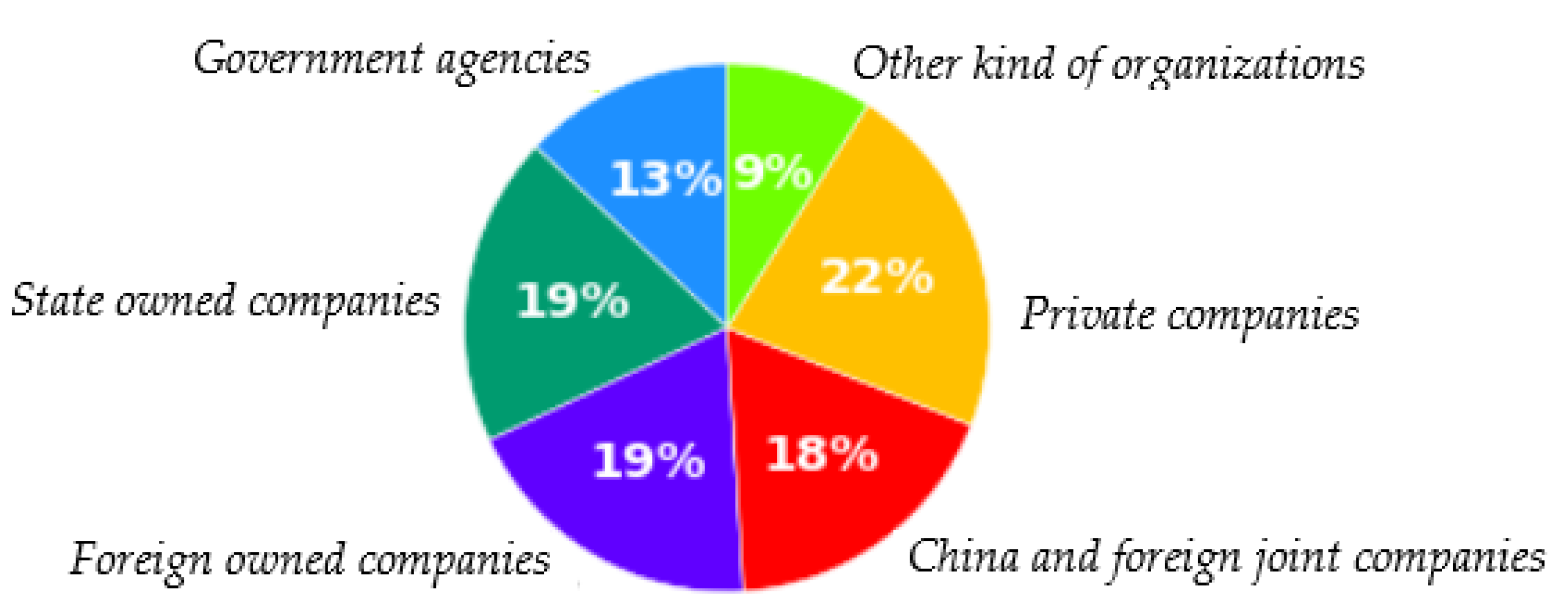

The total of 1013 respondents could be distributed into six different areas (

Figure 1): 13% were from government agencies and affiliated institutions, 19% were from state-owned companies, 19% were from foreign-owned companies, 18% were from China and foreign joint companies, 22% were from private companies, and 9% were from other organizations (

Table A2).

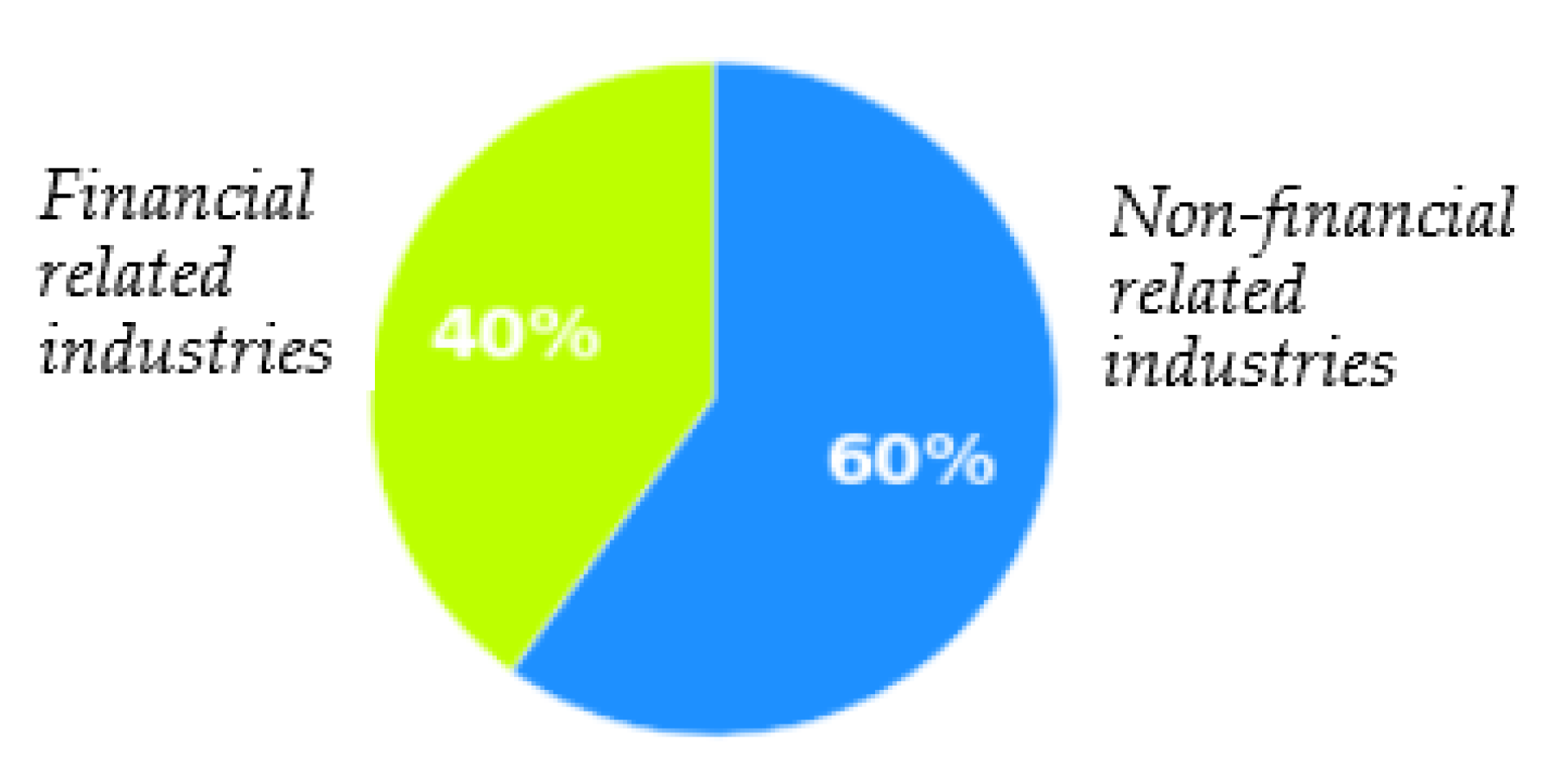

About 40% of the respondents were from financial-related industries, and the other 60% were from other industries (

Figure 2,

Table A3).

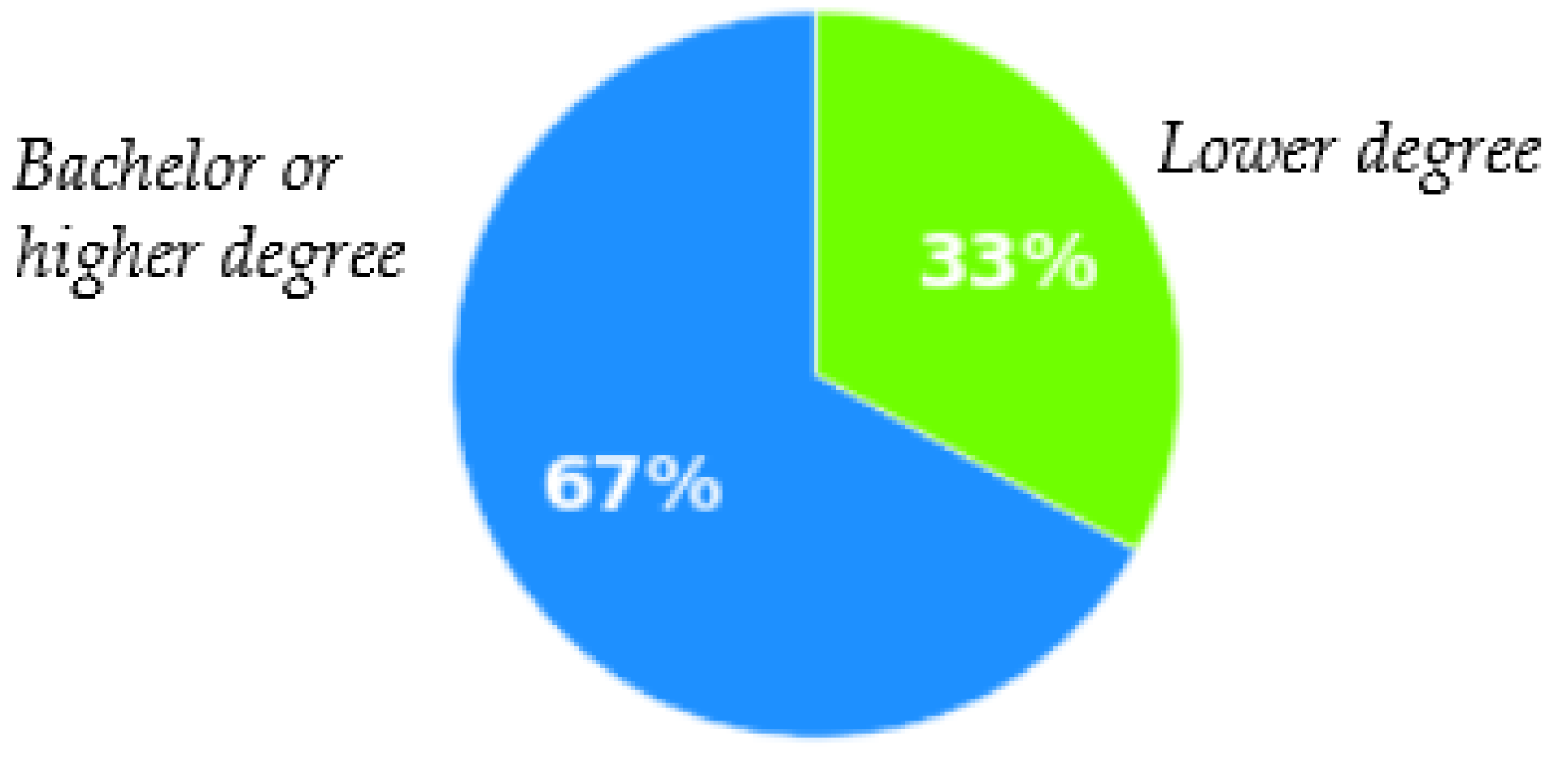

A total of 67% of the respondents held a bachelor’s degree or higher, while the other 33% held a lower degree (

Figure 3,

Table A4).

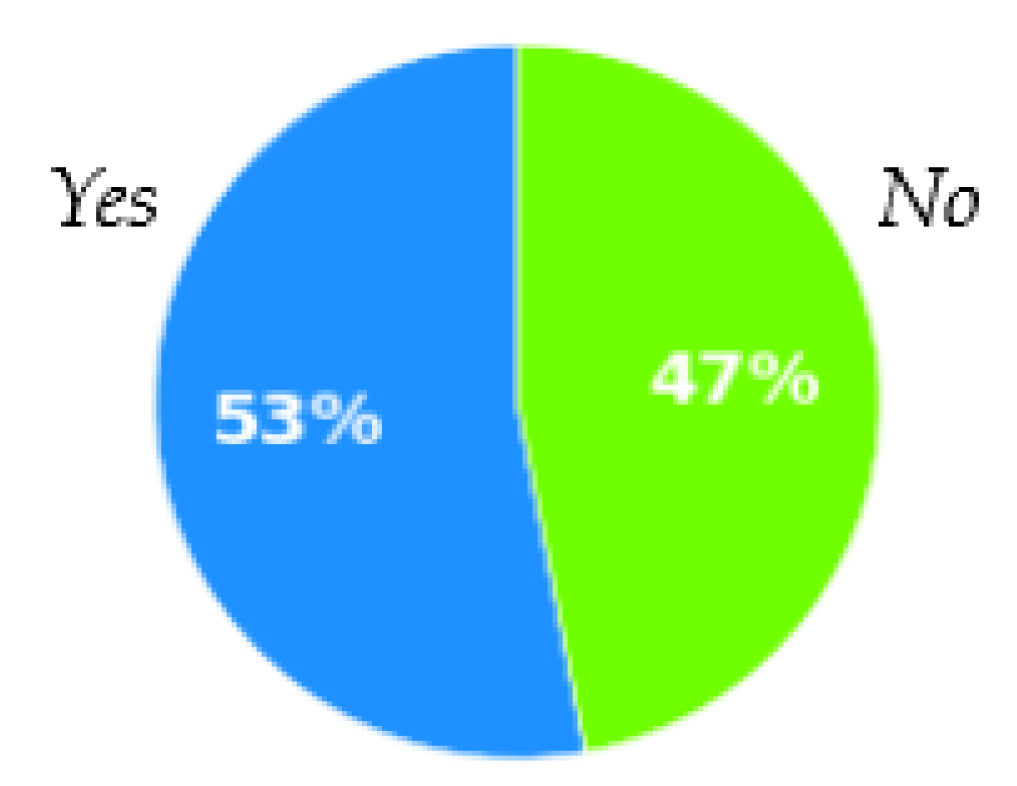

A total of 53% of the respondents have experience with operating financial derivatives, including stocks and options, while 47% of the respondents did not have this experience (

Figure 4,

Table A5).

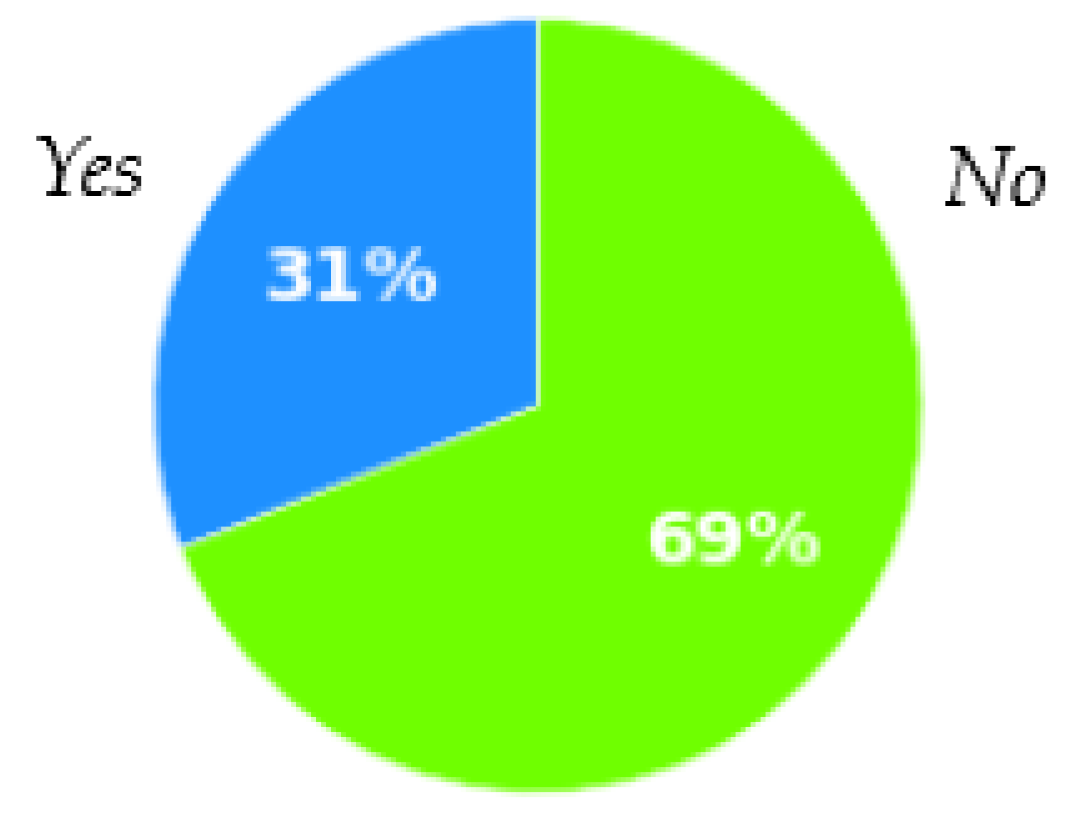

Only 31% of the respondents had experience with holdings of cryptocurrencies, while the other 69% did not (

Figure 5,

Table A6).

While 100% of the respondents already knew that Bitcoin is the first-ranking cryptocurrency in the world (

Table A7), only 38% of the respondents knew that the Ethereum is the second-ranking cryptocurrency in the world (

Table A8).

Second, the survey investigated the characteristics of holdings of cryptocurrencies in China.

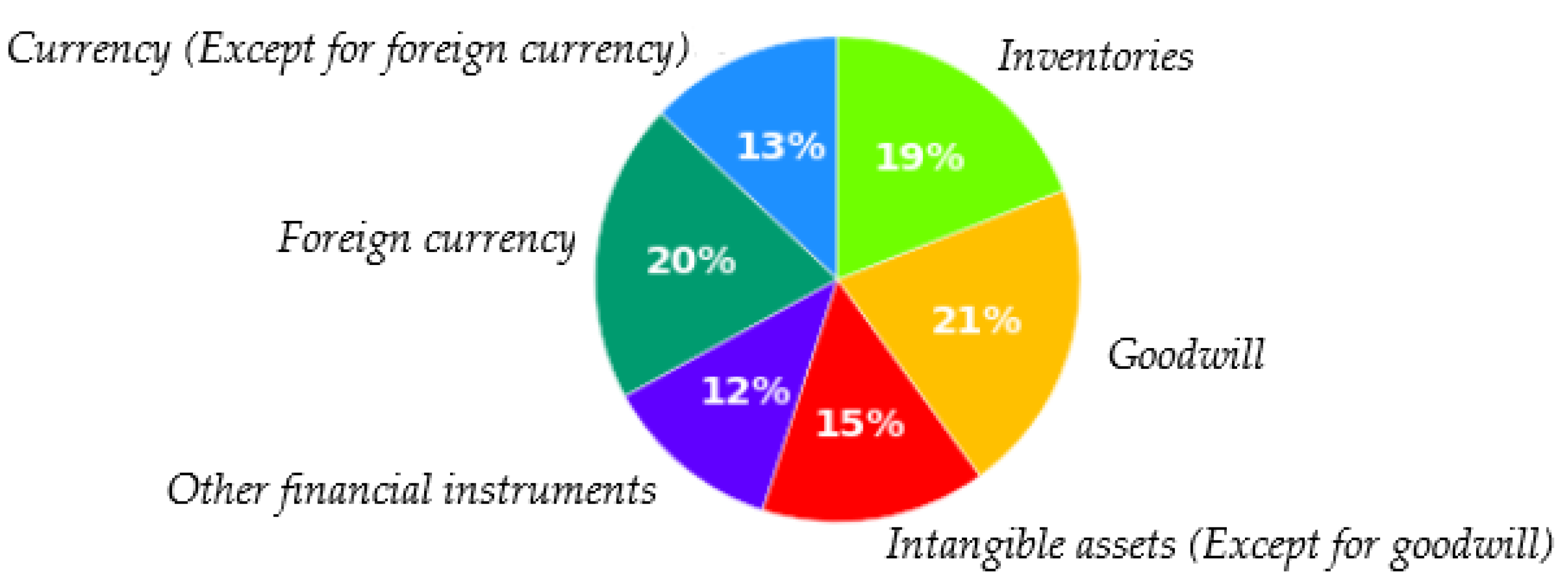

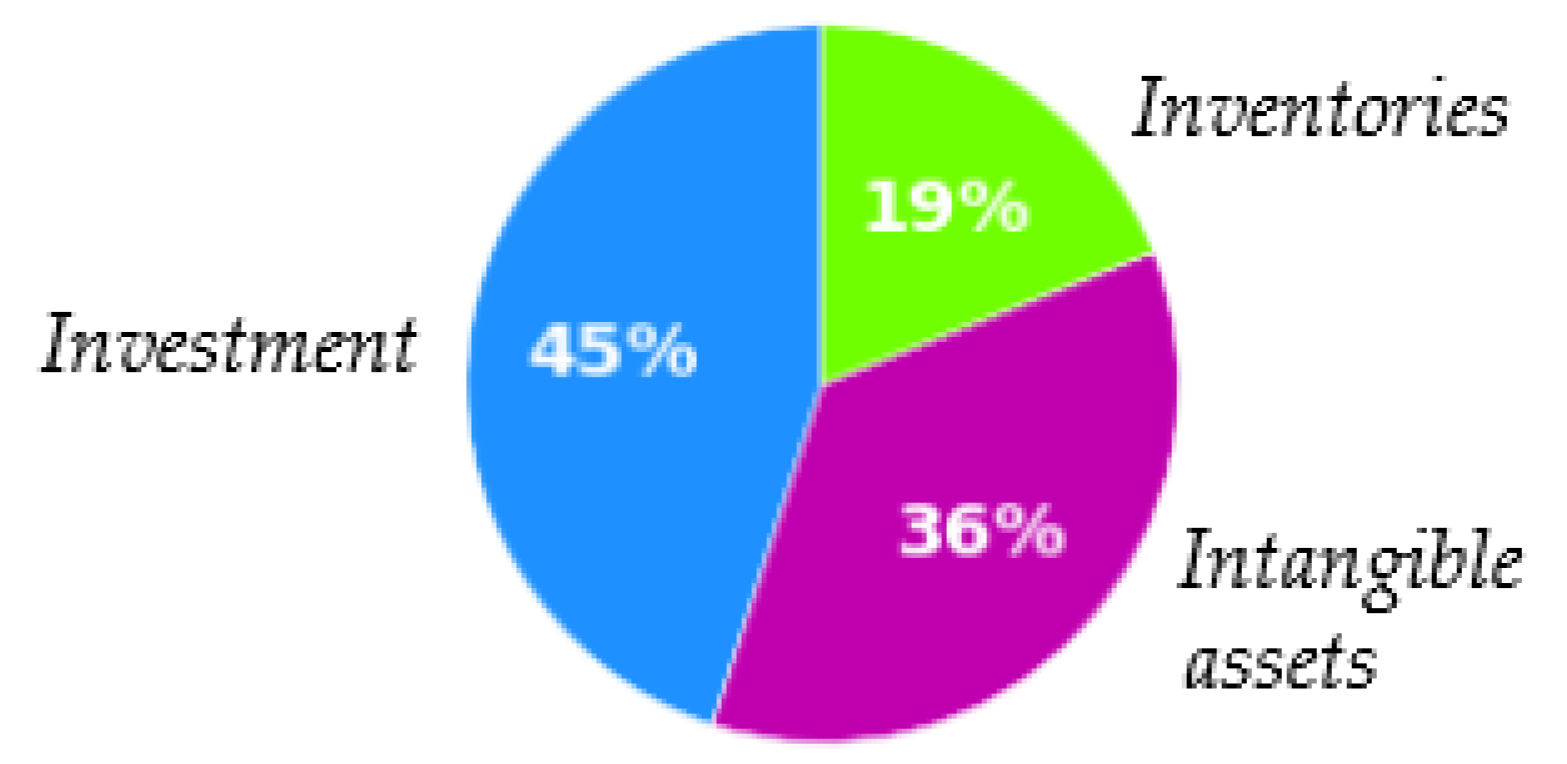

In answer to the question of how companies currently account for holdings of cryptocurrencies, 45% of the respondents stated that entities carry crypto assets as investments (13% as cash, 20% as foreign currencies, and 12% as other financial instruments), 36% of the respondents stated that entities carry crypto assets as intangible assets (15% as intangible assets except for goodwill, and 21% as goodwill), and 19% of the respondents stated that entities carry crypto assets as inventories (

Figure 6 and

Figure 7,

Table A9).

This survey result is similar to that of the DAAC, where 50% of the respondents answered that entities carry crypto assets as investments, 39% as inventories, and 19% as intangible assets (

Boring 2019). However, this result differs from the tentative agenda decision of the IFRSIC, because the conclusion of the IFRSIC does not include investments.

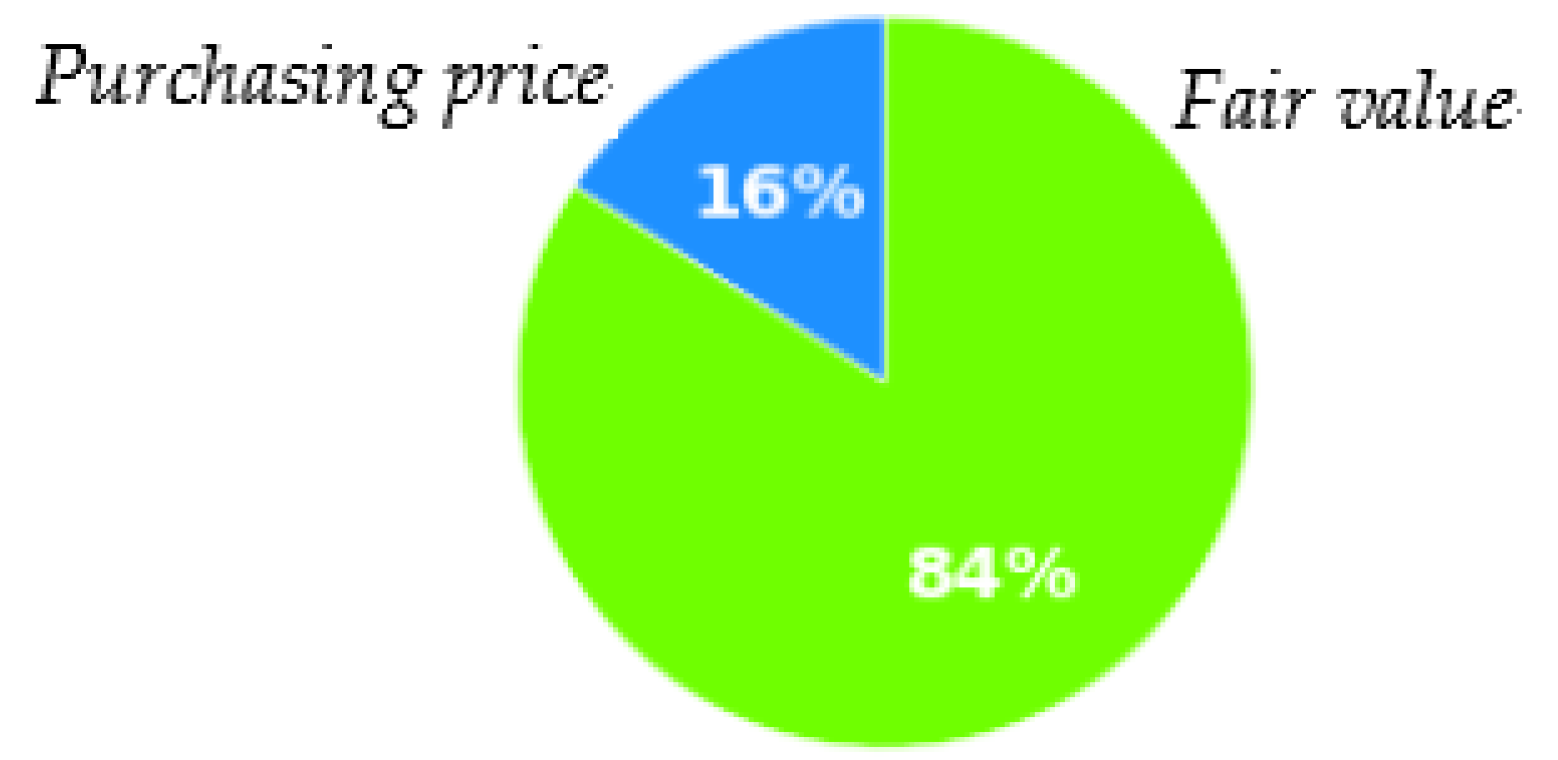

In answer to the question of how to disclose the value of the crypto assets held by entities in accounting, 84% of the respondents stated that entities holding cryptocurrencies should revaluate them at fair value through profit and loss (FVTPL) (

Figure 8,

Table A10).

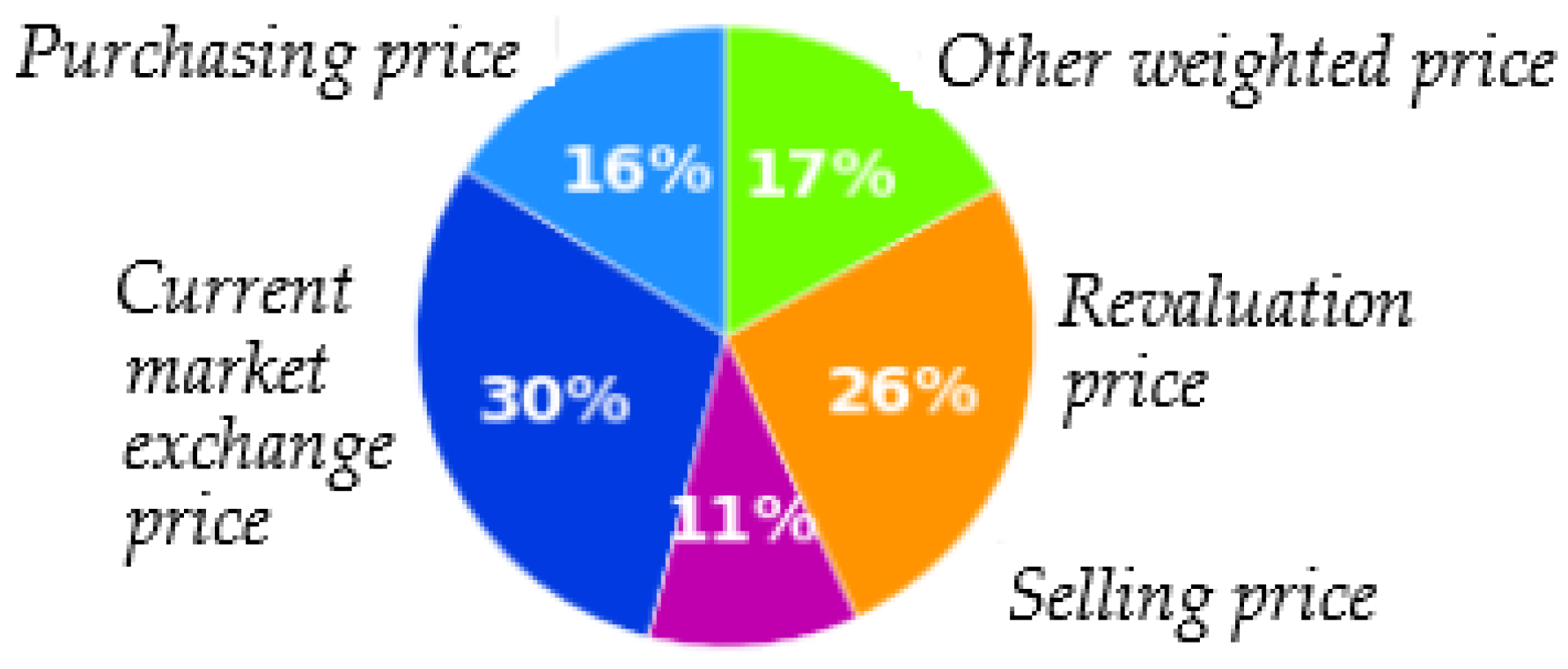

This survey result has also revealed that the 84% of fair value is composed by four different types of fair value, including 30% of current market exchange price, 11% of selling price, 26% of revaluation price and 17% or other weighted price (

Figure 9,

Table A10).

This percentage of the respondents stated that entities holding cryptocurrencies should revaluate them at FVTPL is much higher than those obtained in the Canadian Securities Administrators Chief Accountants Committee (76%) (

Hait et al. 2019) and the DAAC (75%) (

Boring 2019).

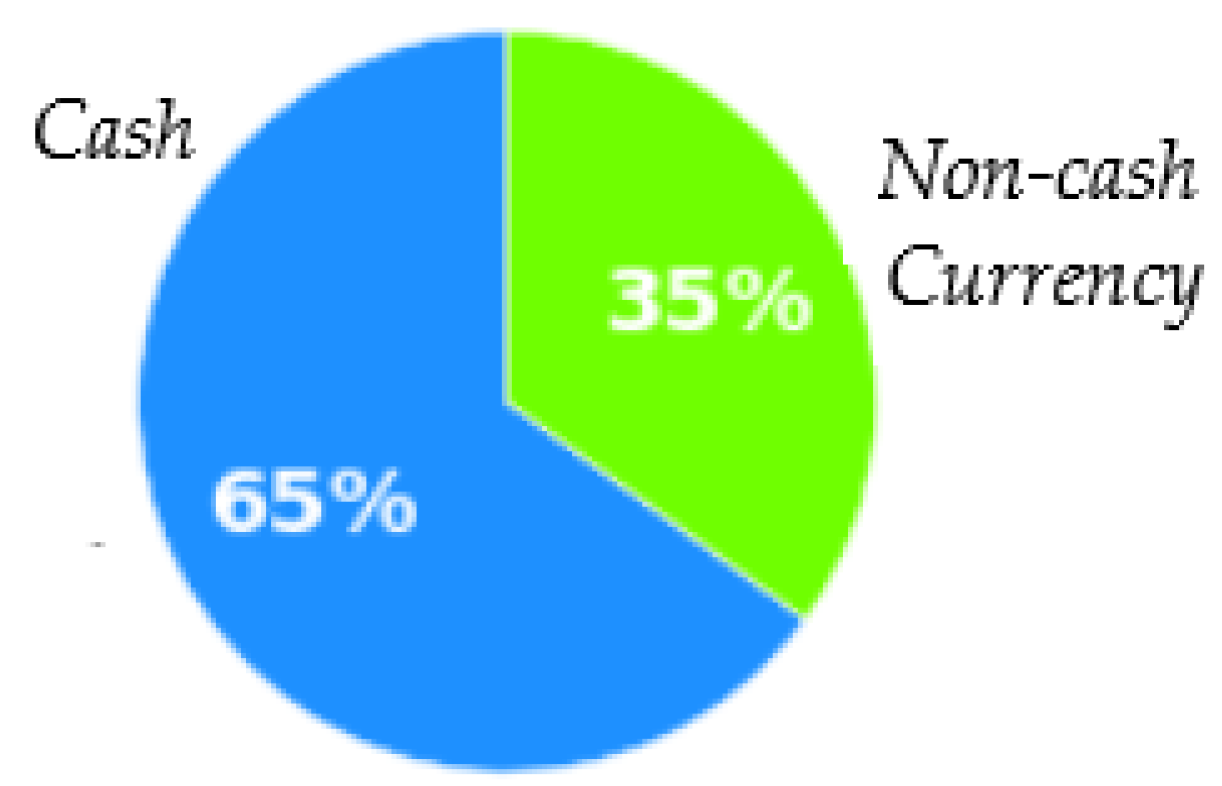

In answer to the question of whether cryptocurrencies are considered cash (currencies), 65% of the respondents stated that cryptocurrencies are cash, whereas 35% of the respondents stated that cryptocurrencies are not cash (

Figure 10,

Table A11).

This result is different to that of the tentative agenda decision of the IFRSIC, because the conclusion of the IFRSIC was that cryptocurrencies are not cash.

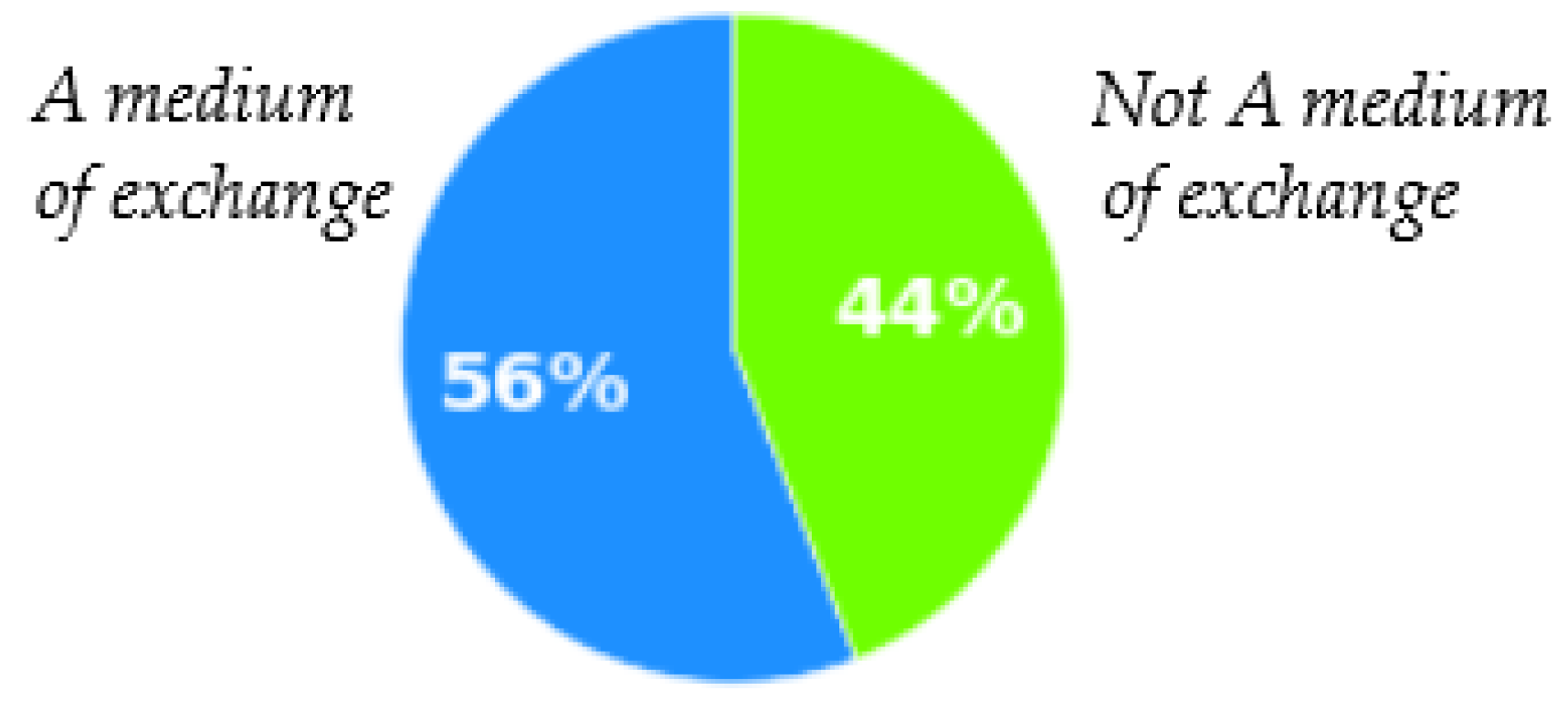

In answer to the question of what functions of a currency that cryptocurrencies have (if the respondent considers cryptocurrencies to be currencies), 56% of the 1013 respondents stated that cryptocurrencies can be used as a medium of exchange (

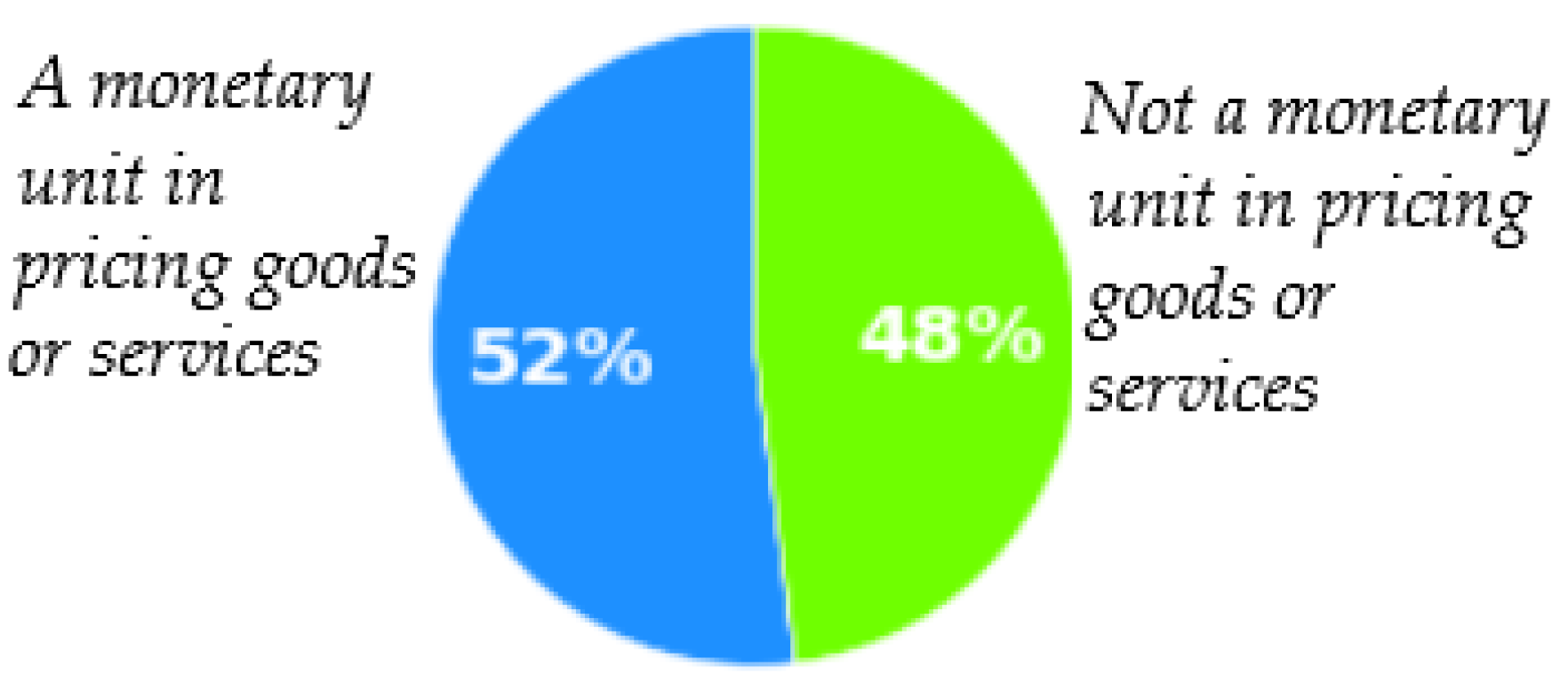

Figure 11), 52% stated that cryptocurrencies can be used as a monetary unit for pricing goods or services (

Figure 12), 36% stated that cryptocurrencies can be used to store currency value, and 18% stated that cryptocurrencies can be used as world currencies (

Table A12).

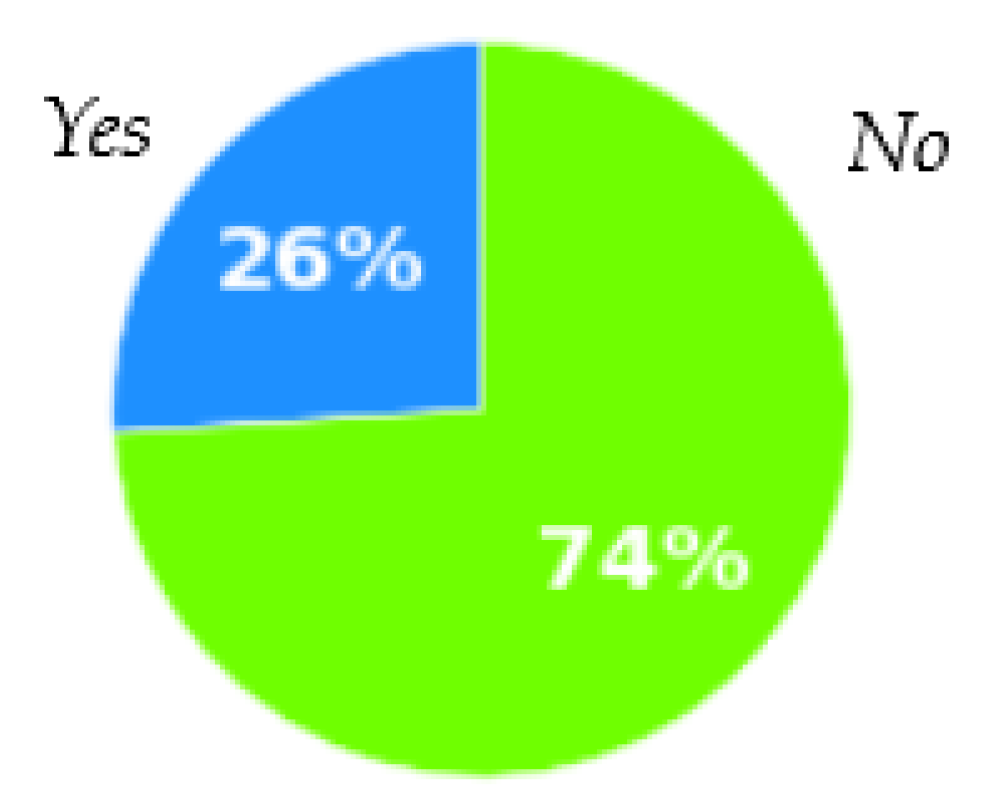

In answer to the question of whether the current accounting standards of the IFRS are appropriate for entities’ holdings of cryptocurrencies, 74% of the respondents answered no, and only 26% of the respondents answered yes (

Figure 13,

Table A13).

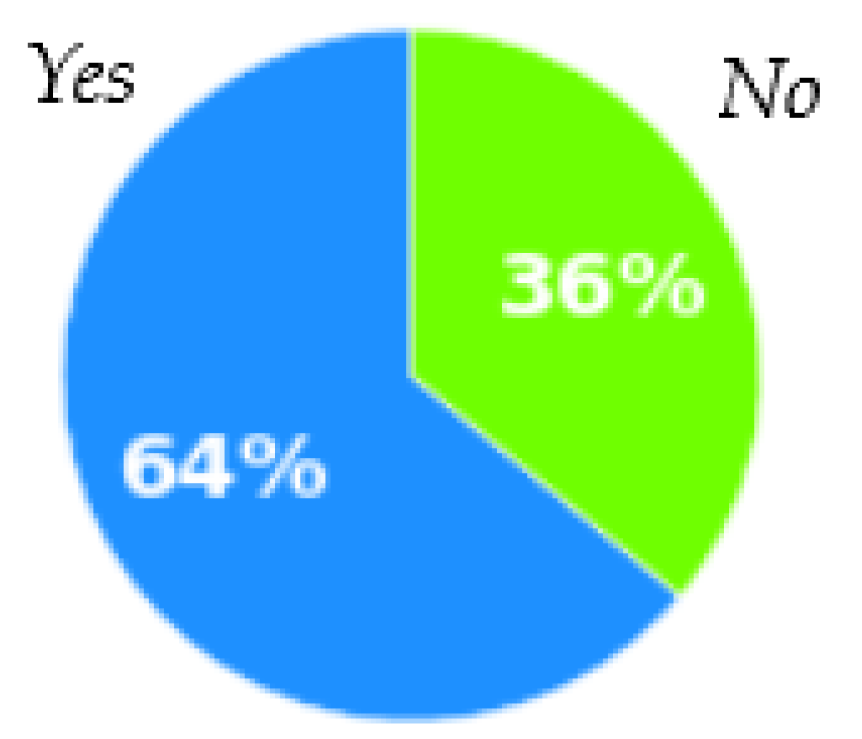

In answer to the question of whether it is essential to make additions to the current standards of the IFRS for holdings of cryptocurrencies, 64% of the respondents answered yes, and 36% of the respondents answered no (

Figure 14,

Table A14).

In answer to the question of whether the distribution ledger recording the trading of cryptocurrencies has greater advantages than the central ledger recording the trading of traditional currencies, 61% of the respondents answered yes, and 39% of the respondents answered no (

Table A15).

In answer to the question of whether the distribution ledger in the blockchain will become a trend that substitutes the central ledger in the future, 54% of the respondents answered yes, and 46% of the respondents answered no (

Table A16).

In answer to the question of whether the respondent would accept the use of cryptocurrencies by their partners when doing business with them, 58% of the respondents answered yes, while 42% of the respondents answered no (

Table A17).

Third, the survey asked questions about the future trends for holdings of cryptocurrencies in China.

In answer to the question of whether the respondent considered exchange platforms of cryptocurrencies on the Internet to be legal in China, 37% answered yes and 63% answered no (

Table A18).

In answer to the question of whether the respondent considered that the trading of cryptocurrencies, including Bitcoin, should be legally permitted in China, 52% answered yes and 48% answered no (

Table A19).

In answer to the question of whether the respondent thought holdings of cryptocurrencies would become legal in China in the future, 60% answered yes and 40% answered no (

Table A20).

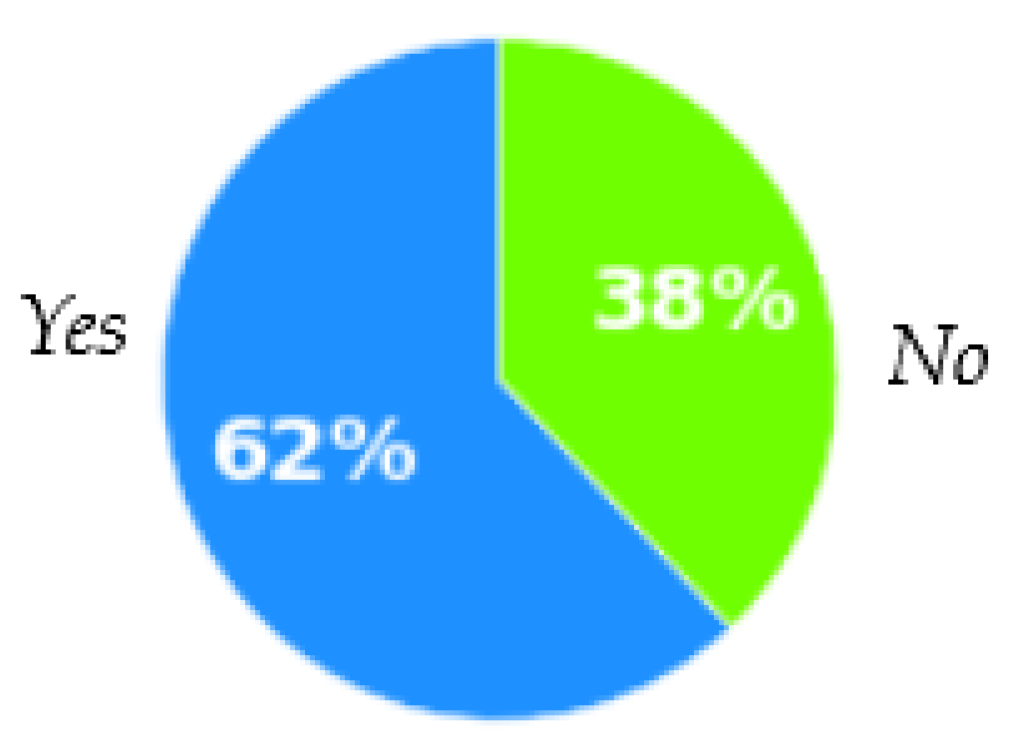

In answer to the question of whether the respondent considered it essential for legal exchange platforms to be set for cryptocurrencies and the management of these platforms to be enhanced in China, 62% answered yes and 38% answered no (

Figure 15,

Table A21).

Fourth, the survey asked questions about future trends for holdings of cryptocurrencies in China’s Xiamen pilot FTZs.

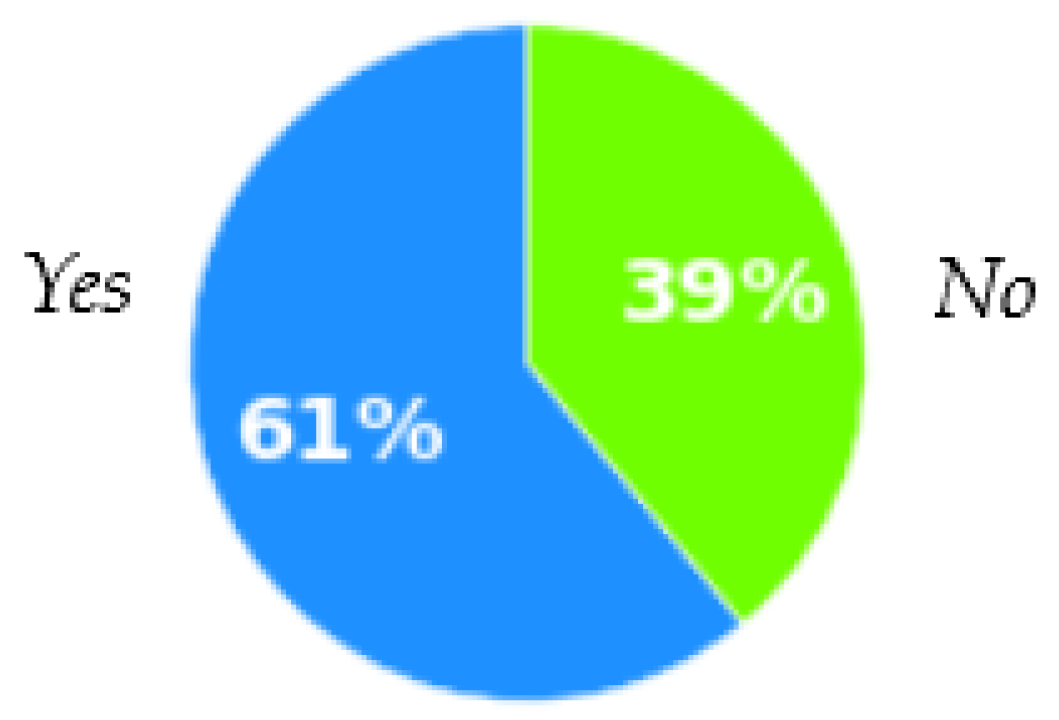

In answer to the question of whether the respondent thought that the legal trade of cryptocurrencies should first be operated and tested in China’s pilot FTZs, 61% answered yes and 39% answered no (

Figure 16,

Table A22).

In answer to the question about the areas that the legal trade of cryptocurrencies should be first operated and tested in China’s Xiamen pilot FTZs, 59% stated that this should occur and agreed to encourage the setup of platforms for the trading of cryptocurrencies, 55% suggested that the government should give permission to entities to hold and use cryptocurrencies, 51% stated that cryptocurrencies should become legal, and 50% stated that cryptocurrencies should be freely traded (

Table A23).

In answer to the question of which industry should be selected as the first to use cryptocurrencies in the pilot FTZs, 58% of the respondents chose the financial industry (

Table A24).

3.2. Analysis of the Survey Results and Policy Suggestions

When considering all respondents, this survey tended to collect questionnaires from people with higher educational degrees who had already learned about cryptocurrencies, particularly about the first-ranking cryptocurrency, Bitcoin. This survey is tended to collect questionnaires from people who had work experience in government agencies, state-owned companies, financial organizations, and Internet-related companies.

Because the first contractors and holders of cryptocurrencies preferred to access them via the Internet, and because the questionnaire was focused on the concepts of currency and accounting, it was reasonable to target the questionnaire to people with Internet experience and higher educational degrees in computing, banking, accounting, and some other majors.

Regarding the total number questionnaires received and the industries of the respondents, we consider the survey results to be representative in terms of both quantity and quality. Because the respondents were from many different industries, held higher educational degrees, and had good understanding of cryptocurrencies, including Bitcoin, the survey results give a good idea of the real situation of cryptocurrencies in China.

The survey results fit with the enthusiasms of private companies and individuals with holdings of cryptocurrencies in China. Most respondents responded positively when asked about the developing trend of cryptocurrencies and supported the legal operation and testing of holdings in China’s Xiamen pilot free trade zone.

Nearly one-third of the respondents had experience with holdings of cryptocurrencies, despite there being no legal exchange market or policy support in China.

Most of the respondents stated that they define holdings of cryptocurrencies as investments, inventories, or intangible assets and believe that the value of a cryptocurrency holding is best represented by its market fair value. Most of the respondents stated that they consider cryptocurrencies are currencies with two main functions: a medium of exchange and a monetary unit for pricing goods and services. Most of the respondents confirmed that the current IFRS standards do not satisfy the accounting requirements for holdings of cryptocurrencies. Thus, it is necessary to add to current IFRS standards to make them appropriate for holdings of cryptocurrencies. Most respondents stated the distributed decentralized ledger based on blockchain technology recording the transactions of cryptocurrencies has more advantages than the centralized ledger, which records the transactions of traditional currencies and believe that, in the future, the distributed ledger will replace the centralized ledger.

Although most of the respondents already knew that the trade of cryptocurrencies in China is illegal and strictly prohibited by the Chinese government, they still stated that, in the future, the trade of cryptocurrencies is likely to become legal and be permitted by the government; platforms for the exchange of cryptocurrencies will be set up and regulated by the government; and cryptocurrencies will be accepted and used by firms for business.

One-third of the respondents stated that, in Xiamen city, there are a few firms that record cryptocurrencies as assets in financial statements and use them as monetary units in business contracts to price goods and services. Most respondents estimated that, in Xiamen city, there are about 50–100 firms that are focused on doing business related to the development of cryptocurrencies.

Most respondents supported the setting up of exchange platforms for cryptocurrencies in the Xiamen pilot free trade zone, the holding and use of cryptocurrencies by entities, the trading of cryptocurrencies in a legal mode, and the initial operation and testing of legal trading in the financial industry.

From the survey results, we can see that although most respondents presented an optimistic attitude toward the holding, use, and trading of cryptocurrencies, a few respondents presented a negative attitude. This means that for an opening up policy for cryptocurrencies to be developed, namely, the operation and test exchange of cryptocurrencies in the Xiamen pilot FTZ, it is necessary to maintain a prudent attitude and conduct a complete analysis of policies, environments, and risks to avoid financial risks from the trading of cryptocurrencies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}