1. Introduction

With the development of economic globalization, the financial system has become more and more closely interconnected by investment networks, debtor–creditor and trade contacts [

1,

2,

3,

4]. Financial institutions such as depositories, broker-dealers and insurance companies permeate each other by related business and display significant complex network properties [

5,

6,

7]. The failure of several financial institutions may lead to a severe economic crisis [

8,

9,

10]. One of the typical examples is the global financial crisis triggered by the collapse of Lehman Brothers in 2008 [

11,

12,

13]. Therefore, how to accurately evaluate the systemic importance of financial institutions (SIFIs) so as to provide early warning and deal with the crisis effectively has become an emergent work [

14,

15,

16].

Usually, there are three ways to measure the SIFIs. The first way is to employ Pearson correlation coefficient to calculate the financial institutions’ default probabilities [

17,

18,

19]. Pearson correlation coefficient ignores the heterogeneity of financial data at different times [

20]. Adopting a tail-dependence method to measure the systemic risk contributions between financial institutions is the second method. Girardi and Ergün (2013) [

21] used the conditional value-at-risk (CoVaR) method to estimate systemic risk of each financial institution. Acharya et al. (2017) [

22] employed the systemic expected shortfall (SES) model to calculate financial institution’s losses by considering its leverage. Wang et al. (2019) [

23] proposed CSRISK model to investigate financial institutions’ capital shortfall under the market crash. The above two methods are based on the local correlation and disregard the interlinked among the financial institutions, which may underrate systemic risk contribution [

24]. The latest financial crisis manifests that intricate connections among financial markets can spread risk [

25,

26,

27,

28,

29]. Using the complex network theory to research SIFIs comes up to the third method. Billio et al. (2012) and Gong et al. (2019) [

30,

31] applied Granger causality model to build financial institution network and utilized the out degree to compute the total connectedness. Hautsch et al. (2014) [

24] proposed VaR model to set up financial institution network and adopted systemic risk betas to investigate the systemic risk contribution. Härdle et al. (2016) and Wang et al. (2018) [

32,

33] adopted CoVaR model to construct financial institution network and used the index of out degree to measure the system risk contribution.

Most of the literature evaluates the SIFIs by out degree [

31,

32,

33], which can reveal the range of risk contagion but restrict to the local information of the network [

34,

35]. Recently, considering financial institutions have the characteristics of deeper risk contagion extent, higher risk contagion efficiency and greater risk contagion degree after the outbreak of financial risk, some other indicators such as, clustering coefficient [

36], closeness centrality [

37] and Leaderrank value [

38] are also applied to measure the SIFIs. Although most of the above indicators have been investigated extensively and many findings on SIFIs have been reported recently, which only reflect one characteristic of the network [

36,

37,

38]. A comprehensive evaluation with respect to the entire network appears to be very few. Such studies are however essential to accurately evaluate SIFIs in practice. To deal with this issue, combining four indicators (out degree [

32], clustering coefficient [

36], closeness centrality [

37] and Leaderrank value [

38]) and assigning different weights to each indicator may give a better evaluation. However, the selection of weight is often based on the subjective experience of researchers, rather than sufficient scientific support, which may lead to inaccurate evaluation results. As we all known, entropy weight technique for ioder preference by similarities to ideal solution (TOPSIS) is a multiple criteria decision making method, and it bases on the conception that the selected alternative should have the shortest distance from the positive ideal solution and the farthest distance from the negative ideal solution. Entropy weight TOPSIS has been proved to be a good method in strategic decision making and successfully applied in some fields, such as coal mine safety [

39], multinational consumer electronics company [

40] and transport [

41]. Therefore, it seems that adopting entropy weight TOPSIS to comprehensively assess the SIFIs might be a better choice.

It should be pointed out that the all above mentioned literatures on measuring SIFIs have been greatly limited to low-frequency data. The low-frequency data with daily, weekly, monthly, quarterly or annual sampling frequency can not accurately measure the whole-day volatility information [

42]. Nowadays, more and more scholars have realized that the high-frequency data with the frequency of hours, minutes or even shorter includes the rich information of asset price, and it has been intensively studied in applied finance risk management [

43,

44,

45,

46]. On the other hand, with the unexpected changes of macroeconomic conditions, international events and economic policy in recent years, financial markets are increasingly volatile [

47]. Some researches detected jump volatility in the volatile process of financial assets based on high-frequency data [

48]. For example, Wright and Zhou (2007) [

49] found that jump volatility can explain much of the countercyclical movements in bond risk premium. Zhang et al. (2016) [

50] found that jump volatility is an important component of Dow Jones Industrial Average stocks’ volatility. Audrino and Hu (2016) [

51] found that jump volatility can improve the forecast of S&P 500’s volatility.

The jump volatility depicts an infrequent but a sharp change of asset price, and it can better describe violent volatility of financial market than continuous volatility [

52]. Measuring SIFIs associated with jump volatility spillover network and high-frequency data has not been reported yet and it still remains a challenging problem. Motivated by the above discussions, in this paper, we aim to employ high-frequency data of China’s financial institutions to construct jump volatility spillover network, and then utilize entropy weight TOPSIS to comprehensively assess the SIFIs. The innovations of this paper are as follows:

- (1)

Many scholars investigated the jump volatility of a single financial asset on its price fluctuation from the perspective of prediction. We first propose Granger-causality test to identify the jump volatility spillover among financial institutions.

- (2)

Financial markets are extremely volatile, and the low-frequency data might lose a lot of important information. By employing 5-min high-frequency data, we establish the jump volatility spillover network, which can capture the jump volatility spillover among financial institutions.

- (3)

We use entropy weight TOPSIS rather than a single indicator to comprehensively assess the SIFIs.

The reminder of this paper is arranged as follows. In

Section 2, we introduce the methodology. In

Section 3, we present the data. In

Section 4, we give an empirical analysis. Finally, we make conclusions and discuss our findings in

Section 5.

5. Conclusions and Discussion

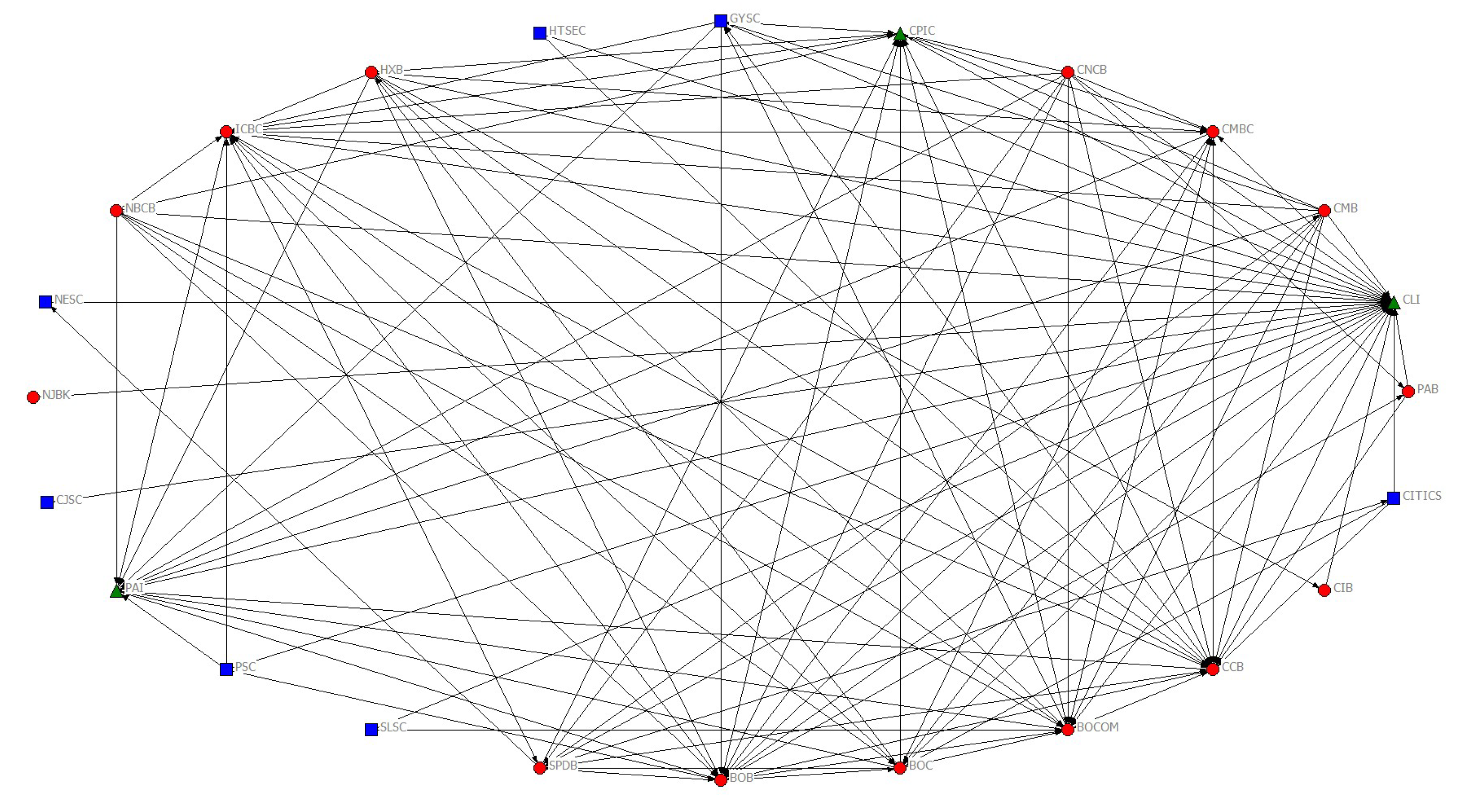

This paper adopts 5-min high-frequency data of China’s financial institutions to extract realized jump volatility. Then, we employ Granger-casuality test to construct the jump volatility spillover network. Furthermore, out degree, clustering coefficient, closeness centrality and leaderrank value are used to evaluate the SIFIs, respectively. In addition, we utilize entropy weight TOPSIS to comprehensively evaluate the SIFIs.

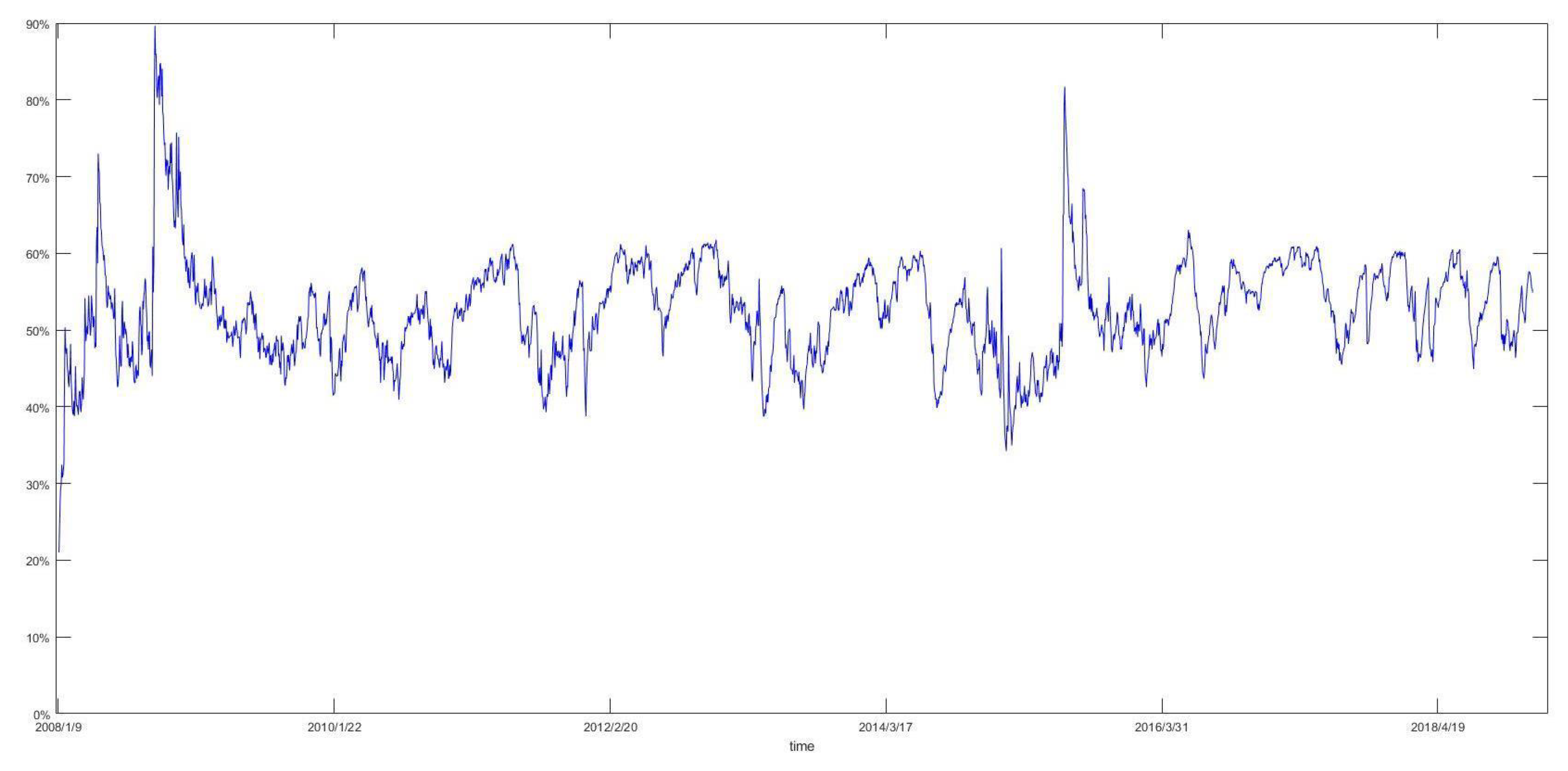

Some basic results of our research can be summed up as follows: (1) The highest frequency of jump volatility is 44.30% in 2008. This may be related to the outbreak of the subprime mortgage crisis in 2008. (2) We measure the SIFIs from four dimensions. In terms of risk contagion range, we can find that CMB, BOC and CNCB, which are all from depository sector, possess the highest out degree value of 10. One possible explanation is that China’s financial system is a depository-led system. In terms of risk contagion extent, one can see that SLSC and HTSEC, which are all from broke-dealer sector, have the highest clustering coefficient value. This indicates that broke-dealer sector’s risk contagion ability can not be neglected in China’s financial system. In terms of risk contagion efficiency, we discover that CJSC and PAI have the highest closeness centrality value, which means that some insurances have gradually become important departments. In terms of risk contagion degree, the results reveal that the greatest degree of risk contagion is insurance sector, followed by broke-dealer sector, and depository sector have the worst risk contagion degree. (3) Based on the comprehensive evaluation of the SIFIs, by the method of entropy weight TOPSIS, the obtained results show that CLI, CCB, BOB, ICBC and BOCOM are identified as the influential nodes. (4) According to highest values of total linkages in each period, we can find three prominent cycles. The first cycle started at January 2008 and ended at April 2008, which was in the period of the subprime crisis. The second cycle started at June 2008 and ended at October 2008, which was in the later period of the subprime crisis, and in the initial period of the European sovereign debt crisis. The third cycle began at May 2015 and ended at August 2015, which was in the period of China’s stock market disaster. (5) Total connectedness of financial institution networks reveal that large commercial banks and insurances play an important role when financial market is under pressure, especially during the subprime crisis, the European sovereign debt crisis and China’s stock market disaster. Meanwhile, some small financial institutions are also systemic importance, which may be related to their too much interconnection with other financial institutions.

By the way, the work presented in this article does not consider the following points: (1) The data do not contain all publicly listed financial institutions in China because we have deleted those for which we have experienced long suspension periods. Therefore, developing new tools that have limited sample for investigating SIFIs is a worthy target. (2) We just select 24 top financial institutions. Non-financial institutions may also play an important role as a result of their interactions with these financial ones. It would be interesting to research some financial institutions and non-financial institutions at the same time. We will leave this challenging yet interesting problem as future research. (3) It is important to measure SIFIs based on the network. This paper employs linear Granger-casuality test to construct the jump volatility spillover network. There is a nonlinear relationship between financial markets. The method of network construction could be extended by employing the Granger-casuality test. We have to leave these challenging yet interesting problems as future research.

{kind=link}

{kind=link}