Abstract

This study aimed to provide a comprehensive analysis of the factors that determine and shape consumers’ behavioral intention to adopt mobile commerce (m-commerce). By integrating the core constructs from the Unified Theory of Acceptance and Use of Technology (UTAUT), together with the trust-building mechanisms, this study explored the importance of the institutional mechanisms and their moderating effects between trust in the vendors and intention to adopt m-commerce. Traditionally, the effects of institutional mechanisms on trust and adoption intention have been considered separately in different study contexts. The purpose of this study was to extend the literature by simultaneously exploring two institutional mechanisms that are conceptually highly similar to each other, namely, structural assurance (SA) and perceived effectiveness of e-commerce institutional mechanisms (PEEIM). A self-administered survey was used to collect data, which were analyzed using partial least squares structural equation modelling (PLS-SEM). The results revealed that most of the constructs examined have significant relationships with the intention to adopt m-commerce. Additionally, PEEIM exhibits a significant moderating effect but SA does not. This study delineates how trust-building mechanisms play important roles in increasing consumers’ confidence in order to promote m-commerce adoption.

1. Introduction

The use of Internet-based commerce has rapidly increased due to the recent advancement of mobile technology [1]. This includes the use of smartphones to perform mobile commerce (m-commerce) [2,3,4]. Global m-commerce sales tripled from USD 1 trillion in 2016 to USD 3 trillion in 2020 and are expected to reach USD 3.56 trillion in 2021 [5]. In Malaysia, the e-commerce market is valued at USD 4 billion, of which, USD 1.9 billion is from m-commerce. The mobile connection penetration per 100 inhabitants is 127, meaning that, on average, each Malaysian subscribes to more than one mobile broadband service [6]. Recently, the usage of mobile payments, particularly in the e-wallet segment, has increased significantly. E-wallets had a transaction value of USD 3.4 billion in 2019, compared to USD 2.7 billion in 2018 [7].

M-commerce transactions are undertaken by 39 percent of consumers [8]. Compared to the mobile connection penetration rate, significant potential exists for an increase in the use of m-commerce. Hence, this study examined the influential factors that potentially impact the growth of m-commerce. Prior studies showed that consumers perceive significant uncertainty and risk when interacting with online vendors or sellers [9,10,11,12]. In the online marketplace, it is common for consumers to routinely interact with new sellers. This leads to greater risk of opportunistic seller behavior. Because consumers may be unfamiliar with online vendors, building trust in the early relationships is vital to induce initial purchasing intention [13,14].

In Malaysia, online consumers are highly concerned about issues related to security and privacy. In general, about 53 percent of consumers are concerned with fraudulent online vendors and identity theft. Furthermore, 59 percent of consumers are worried about privacy issues, such as misuse of personal information, and 63 percent are concerned with online retailers’ reputation, trust payment gateways and guaranteed delivery times [15]. These data show that, despite widespread smartphone penetration in Malaysia, significant concern exists regarding issues of security and privacy in m-commerce transactions. The presence of trust and institutional mechanisms plays an important role in the facilitation of m-commerce activities. The effects of trust mechanisms on innovation acceptance have been extensively examined [11,14,16]. Similarly, the effectiveness of institutional mechanisms in influencing consumers’ intention to make an initial purchase was also studied previously [11,17].

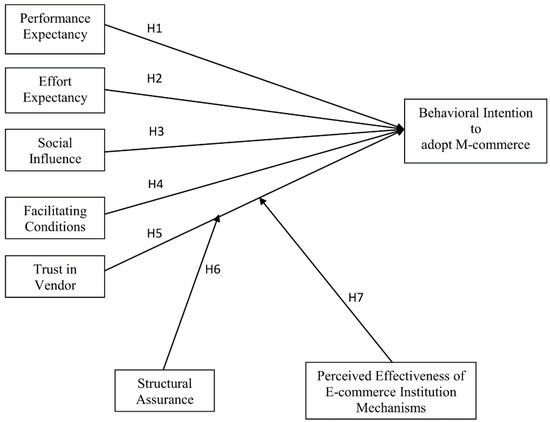

This study incorporated the constructs of performance expectancy (PE), effort expectancy (EE), social influence (SI), facilitating conditions (FC) and trust in vendor (TV) and explored their relationships with the behavioral intention (BI) to adopt m-commerce. Furthermore, the online trust building mechanisms, namely, perceived effectiveness of e-commerce institutional mechanisms (PEEIM) and structural assurance (SA), were examined in this study. Specifically, the moderating effects of PEEIM and SA on the relationship between TV and BI in m-commerce adoption were investigated.

PEEIM and SA were previously utilized as moderators in several studies. Fang et al. studied the effect of PEEIM as the moderator in satisfaction–trust–repurchase intention relationships [9]. Chen et al. demonstrated the differences in moderating effects on the trust transfer process when comparing PEEIM with the perceived website quality of the seller (PWQS) [18]. In the study conducted by Chong et al. [19], in addition to using PEEIM as the moderator, the effects of interactivity and presence on PEEIM were examined. McCole et al. investigated the moderating effect of SA in an online betting context [20]. Huang et al. revealed an interesting paradoxical effect of PEEIM on social and economic satisfaction [21]. A major distinction exists between the current study and the previous research in using PEEIM and SA as the moderators. In previous studies, PEEIM and SA were separately examined in different contexts. In the current study, the moderating effects of PEEIM and SA on the same relationship were considered simultaneously in a similar research model. To the best of our knowledge, this study is among the first to combine both institutional mechanisms with a substantial degree of conceptual similarity in the same framework [9]. In general, both PEEIM and SA are mechanisms that provide assurance that security and safety are in place and thus may convince consumers to perform online transactions. However, SA focuses on protection and assurance, whereas PEEIM highlights risk reduction [9]. Despite the similarity of their functions, our results reveal that both PEEIM and SA behave differently in terms of moderating effects in the context of m-commerce adoption.

2. Literature Review and Hypotheses Development

2.1. UTAUT

Venkatesh et al. presented the Unified Theory of Acceptance and Use of Technology (UTAUT) to address the limitations of previous behavioral theories [22]. It was asserted that the development of a specific behavioral theory is challenging because the use of one theory may possibly ignore the pertinence of another useful constructs developed in other theories. To address this issue, UTAUT was developed by integrating different constructs that were considered to have similarities from different behavioral theories. One of the most significant contributions provided by UTAUT is its capability in achieving 70% amount of variance in predicting BI and actual usage behavior of technology that surpassing other theories.

This study selects PE, EE, SI and FC as the foundation to explore the determinants of BI to accept m-commerce adoption in Malaysia.

2.2. Trust Transfer Theory

Trust is a key factor in maintaining sustained relationship between two parties. Trust is undeniably important in both transacting parties due to increased uncertainty in online environment. In order to initiate commerce between parties, sufficient trust need to be accelerated [23]. Initial trust is a prominent application in order to fulfil the online commerce potential. For instance, to establish and enhance consumers’ trustworthiness and positive judgements towards online vendors, initial trust protection should be leveraged adequately and efficiently [13,24].

Trust transfer process can build trust, particularly in online commerce platform [25]. A consumer’s trust in an uncertain entity could be transferred to another context virtually through the association between them [23,26]. A safe and reliable online commerce environment should be accelerated to support and convince consumers in transacting on e-marketplaces and avoid problematic online vendors at the same time. In a trust transfer process, three parties are involved. There is a trustor who evaluate if he/she decides to trust other. Next, a trustee who is assessed by the trustor. Finally, the third-party who is usually referred to as the broker [27]. It is believed that when the trustor decides to trust the third-party (particularly when the third-party is closely related to the trustee), the trust on the third-party will be shifted to the trustee [25]. Based on the similar rationale, a consumer’s trust can be transferred from the institution-mechanism to the online vendor and thereby encourage purchasing intention. Institutional mechanism plays the role as a third-party where trust is transferred from it to the trustee (online vendor).

2.3. Institutional-Based Mechanism

Institutional-based mechanisms are impersonal structure that protect transaction success by creating certain terms and conditions [28]. These institutional-based mechanisms play important roles in mitigating any possible risks during transactions by providing safe online environment through third-party safeguarding [9]. Examples of safeguarding are privacy protections, credit card guarantees, escrow services and assurance seals [17]. Such mechanisms yield assurances from the aspects of rules, regulations, policy and standard of operating procedures for customers’ benefit [9]. Moreover, this structure allows entities from different social and cultural backgrounds rely and build trust due to the assurances of the strong institutions and regulation.

In online marketplace where consumer has no prior experience, institution-based trust is created when the trust is transferred to institutional mechanisms, thereby set conditions to facilitate transaction success in the marketplace [29]. Likewise, the belief that online marketplace has regulative protections for consumers will inevitably generate the establishment of mechanism-based trust among consumers to foster online commerce. For instant, the third-party online payment service organizations such as Paypal and Alipay offer escrow services to safeguard the monetary transactions [28]. It serves as a buffer between the buyers and the online vendors thus reduce the possibility of faulty monetary transaction. Similarly, credit card companies like Visa and Mastercard offer online payments guarantees to reduce potential fraudulent risks [28]. Two significant institution-based mechanisms are introduced in this study to tailor with the scope of m-commerce research, namely perceived effectiveness of e-commerce institutional mechanisms (PEEIM) and structural assurance (SA). These two trust-transfer mechanisms could play an important role in safeguarding today’s m-commerce environment.

2.4. Performance Expectancy

Performance expectancy (PE) measures the degree to which one’s belief in using a system will assist him/her to perform certain task or function [22]. PE is one of the strongest determinants in predicting an innovation adoption. Individuals tend to be more willing to accept an innovation of technology if they believe it is useful for them [30]. In a study adopted integrated model of UTAUT and task-technology fit, PE was discovered to have positive effect on the consumers’ BI to use healthcare wearable devices [31]. In another study related to medical system, Shiferaw and Mehari examined the effect of PE on the intention to use electronic medical record system and the result was significant [32].

Mousa and Al Rababaa performed a study to assess the key factors that have influences in the acceptance of m-commerce among Jordanian consumers [33]. This is very similar to our context of study. In their study, it was proven that PE has significant effects towards adoption of m-commerce in Jordan [33]. In this study, PE is indicated as the extent on how m-commerce can be beneficial to individuals when conducting transactions. As such, the study hypothesized that:

Hypothesis 1 (H1).

Performance expectancy positively influences users’ behavioral intention in adopting m-commerce.

2.5. Effort Expectancy

Past study posited that the barriers in adopting mobile system could be reduced by improving its ease of use capability [34,35]. Additionally, the research found that effort expectancy (EE) significantly influenced the adoption of m-commerce in Jordan [33]. Researchers in Taiwan also found that mobile-phone navigation is widely accepted as compared to web browser because of the user-friendliness design of mobile phone’s interface [36]. A study on citizens’ e-government services adoption was conducted recently by using extended UTAUT model [37]. Li observed that most of the constructs of UTAUT, including EE, exhibited positive effects on the services adoption [37].

On the other hand, there were also studies reported that EE has no significant effect on the intention to use innovative technology. For example, a statistical meta-analysis discovered a weak relationship between EE and intention constructs [38]. In the study conducted in Mauritius, Lallmahomed et al. concluded that EE was not significantly related to BI to adopt e-Government services [39]. Similarly, Herrero et al. discovered that EE did not have any influence on the intention to use social network sites to share content [40].

In this study, EE referred to one’s ability in conducting m-commerce activities with minimal efforts. Hence, the study hypothesized that:

Hypothesis 2 (H2).

Effort expectancy positively influences users’ behavioral intention in adopting m-commerce.

2.6. Social Influence

The studies of m-commerce services like mobile payments also denoted significant impact in the relationship between social influence (SI) and acceptance worldwide which include UK [41], Portugal [42], Qatar [43] and Taiwan [44]. The consumers were highly responded to social pressure in their decision to adopt particular new technology. Even so, Venkatesh and Davis commented that when one’s experience with system grows, SI tends to be lesser [45]. In a study related to sharing economy service experience, the moderating effects of SI on two relationships were examined [44]. Tsou et al. discovered that SI exerted positive moderating effects on the relationship between utilitarian value and BI, as well as the relationship between hedonic value and BI [44]. In Cameroon, smartphone applications were deployed by top e-commerce companies to facilitate m-commerce business. By integrating perceived risk and perceived trust into the UTAUT2 model, Verkijika examined the factors influencing the adoption of m-commerce applications in Cameroon [46]. SI was found to positively influence the BI to adopt m-commerce.

On the contrary, Prayoonphan and Xu revealed that SI did not impact passengers’ intention to use smartcard ticket in Thailand [47]. Mensah observed interesting results on the study related to e-government services in China. SI exhibited significant effect on trust in the internet but was not significant in forecasting the trust in government [48].

Looking at the vary views from researchers, this study takes into the consideration that individuals will be influenced by their social networks. The opinions given by them will serve as the guidance in making decision to accept m-commerce adoption. Therefore, the study hypothesized that:

Hypothesis 3 (H3).

Social Influence positively influences users’ behavioral intention in adopting m-commerce.

2.7. Facilitating Conditions

Facilitating conditions (FC) refers to the situation where an individual perceive that resources are in place to facilitate ones to conduct a certain behavior, where in this case, m-commerce activities [30]. In other words, when consumers have sufficient supporting resources or someone is willing to provide guidance and facilities to access the particular technology, the individual will perceive that adapting to new innovation takes less effort and are more ready to use it [49].

Even though a number of previous studies indicated significant outcomes in the relationship between FC and acceptance [39,50], there are some that failed to find the association between them [40,42]. In fact, the initial UTAUT framework by Venkatesh considered FC as the predictor only when “Use of Behavior” exists, but the constructs were added into the later theory of UTAUT2 that it has impact towards behavioral intention in adopting a certain technology [30].

Given the mixed findings from the previous studies, this study follows UTAUT2 that FC have significant effect towards behavioral intention in m-commerce adoption. The FC here referred to the knowledge or proper guidance that are available. At the same time, facilities like smartphone and mobile internet are needed to equip an individual to use m-commerce. Thus, the study hypothesized that:

Hypothesis 4 (H4).

Facilitating conditions positively influences users’ behavioral intention in adopting m-commerce.

2.8. Trust in Vendor

Trust in vendor (TV) is an interpersonal trust of online vendors/sellers that able to serve consumers’ interest and have ability to hold honest, sincerity and reliability in transaction process [13]. Indeed, TV is prevalent when the transaction environment is uncertain. For example, consumers might not interact with online vendors face-to-face and touch the products physically [51]. Prior studies have reported that trust has significant impact towards intention to utilize m-commerce services [52,53]. Specifically, in a study that utilized SEM-neural network approach, trust was proven to be a significant predictor of BI [52]. Liébana-Cabanillas et al. concluded that since mobile payment was not a regular practice in Republic of Serbia, customer trust in the services was critical [52].

Chong et al. performed an interesting study by forming a prediction model based on two different cultural settings [54]. In their study, the consumers’ intention to adopt m-commerce from Malaysia and China was investigated. The trust in the usage of m-commerce was found to be significant in both regions [54]. Giovanis et al. conducted a study to identify the factors influencing the use of mobile self-service retail banking technologies in Greece [55]. Perceived trust was discovered to be positively affecting BI to use mobile banking services in this study.

Based on the findings from previous studies, this study hypothesized that:

Hypothesis 5 (H5).

Trust in vendor positively influences users’ behavioral intention in adopting m-commerce.

2.9. Perceived Effectiveness of E-Commerce Institutional Mechanisms (PEEIM) and Structural Assurance (SA)

Both PEEIM and SA are considered as impersonal mechanism structure that functioned to provide security and safeguard so that online transactions can be conducted safely. While both PEEIM and SA shared the similarity of concept in providing protection and security, PEEIM conceptualized its role in mitigating risks in a more explicit manner [9]. Several studies examined the institution-based trust towards intention to accept new technology. For example, Wei et al. [16] have proven the significant relationship between institution-based trust and intention to perform transaction in e-marketplaces. Consumers’ trust was successfully built and their transaction intention was increased with the accessibility of the legal binding mechanisms [56]. Furthermore, a ridesharing study has been conducted and found that consumers’ trust in ridesharing platform were influenced by perceived effectiveness of payment security. This in turn will also indirectly affect their trust in the driver [57].

E-commerce institution structure tends to create a less risky online transaction environment because regulatory assurance could reduce contextual uncertainties. Eventually, this enables consumers rely less on trust during initial purchase with no prior purchasing experience. With proper institution mechanisms in place, trust in vendor plays a lesser significant role because clear and useful signals allow consumer to access other’s behavior [9,58]. Trust is not the main determinant for a community that has little uncertainty because the contextual uncertainties could be diminished by imposing increased mechanism assurance [59]. In this situation, the need for TV in promoting purchasing intention is lessened and community rely on certain mechanism assurance to perform purchasing activities [9]. Conversely, consumers will rely heavily on TV in a context with high uncertainties [58].

In the previous study, it was found that SA has positive moderation effect in continuation to use in a pure e-service context [20]. Given the limited moderation studies in the domain of SA, the need for this aspect of investigation is highlighted. In this study, SA exists to assure customers that m-commerce activities will be performed securely. Therefore, it is hypothesized that:

Hypothesis 6 (H6).

Structural assurance will positively moderate the relationship between trust in vendor and users’ behavioral intention in adopting m-commerce such that relationship is stronger when the users perceive that structural assurance are highly in place.

PEEIM is defined as the consumer perception that in the e-commerce environment, there exist a measure to safeguard him/her from the risks that could happen during online transactions [9]. The moderation effects between TV and repurchase intention in online shopping were analyzed and it was discovered that the relationship between TV and customer repurchasing intention was moderated by PEEIM negatively. On the other hand, a study examined the consumer-to-consumer (C2C) online shopping platform discovered that PEEIM acted as a positive moderator [18]. Given the inconsistent results from previous research as well as limited moderation studies in the domain of PEEIM and SA, the need for this aspect of investigation is highlighted. This study focused mainly from the perspective of purchase intention in the m-commerce marketplaces and follows findings from Fang et al. [9]. Accordingly, this study hypothesized that:

Hypothesis 7 (H7).

PEEIM will negatively moderate the relationship between trust in vendor and users’ behavioral intention in adopting m-commerce such that relationship is weaker when the users perceive that PEEIM are highly in place.

The proposed research model is depicted in Figure 1.

Figure 1.

The research model.

3. Research Methodology

3.1. Data Collection and Sampling Procedure

In this study, the target population was adult citizens of Malaysia, who were at least 18 years of age who could speak and read English. The purposive sampling technique under non-probability sampling category was adopted for this research. The research site for this study is Terminal Bersepadu Selatan (TBS), an integrated transport terminal at Bandar Tasik Selatan, which is about 17 km south from the city center of Kuala Lumpur. It is an integrated transportation hub for passengers travelling to more than 150 destinations in Malaysia. Therefore, there are passengers from every part in the country and not limited to local residences. This could represent the target population of this study. The data were collected by using method which self-administered surveys were hand-delivered to the participants. This is commonly known as the Drop-Off/Pick-Up (DOPU) method. As compared to other survey techniques, DOPU method has higher completion rates [60]. There is a screening question included in our questionnaire. Participants who did not have smartphones were excluded from the survey. When the questionnaires were distributed, each participant was given approximately 20 min to complete the questions. 280 questionnaires were distributed but only 248 were retrieved as 32 of the participants just walked away without returning to us. From the 248 returned questionnaires, 16 of them were discarded. These include incomplete questionnaires, participants who did not have smartphones and those questionnaires having the same answers (for example, only “7” was selected for all questions). Therefore, 232 was the number of responses used for data analysis. In order to compute the required sample size, G Power software package was used. For input parameters, the recommended effect size of medium (f 2 = 0.15) was used, along with the power level of 0.95 (significance level of 0.05). Predictors are set to value of 7. The analysis revealed that the sample size of 153 is required to achieve the statistical power of 0.95. Thus, the sample size of 232 used for data analysis was deemed appropriate for this study.

3.2. Instrument Development

The survey questionnaire introduces the research briefly at the beginning. In the first section, the respondents are directed to complete the demographic section. In the second section, respondents are required to complete the questions that are related to the intention to adopt m-commerce. The questions utilized a seven-point Likert scale format. In total, 33 measurement items which are revised from the previous literature were utilized to investigate the consumer’s behavior with respect to m-commerce. The measurements of PE, EE, SI, FC and BI are adopted from Venkatesh et al. [30]. Meanwhile, PEEIM and TV are adopted from Fang et al. [9]. Lastly, SA is adopted from Gefen et al. [61] (Appendix A–Table A1).

3.3. Demographic Characteristic of Respondents

Table 1 summarizes the respondents’ profiles which include gender, age, highest level of academic qualification obtained and occupation. Among the respondents, about 42.7% were males and 57.3% were females. The largest age group in the survey sample was the 21–25 at 30.2%. Statistics on the highest level of academic qualification obtained showed that majority of the respondents (41.8%) possessed a bachelor’s degree or equivalent (professional qualification). All respondents owned a smartphone equipped with internet access capability and built-in applications.

Table 1.

Respondents’ demographic.

4. Analysis of Data

4.1. Analysis of Measurement Model

In this study, the Kolmogorov–Smirnov test and Shapiro–Wilk test were performed as the data normality test. The results from these two tests reveal that all variables have significant values of less than 0.001. Additionally, the Web Power analysis tool were used to determine the multivariate kurtosis and skewness of Mardia for examination of the multivariate normality. As a result, the p-values for skewness and kurtosis were below 0.001, indicating that non-normality exist in the data. In PLS-SEM, data are not required to be normally distributed since it is a non-parametric statistical method [62]. Unlike maximum likelihood (ML)-based method CB-SEM, normal distribution is required. Harman’s single factor test was conducted to check for the potential common method bias. The result revealed that factor one accounts for only 38.523% of the variance which is less than the 50% threshold value, indicating that common method bias is not an issue in this study.

As shown in Table 2, the values of composite reliability (CR) for the constructs are in the range of 0.860 to 0.937, which are above the cut off value of 0.6 [63], indicating that the internal consistency reliability of the model is acceptable. Even though the outer loadings above 0.708 are preferable, the cut off value of 0.5 is considered practically significant [64]. Two indicators which have loadings below 0.708 are FC4 (0.6850) and TV4 (0.6720). However, indicator with outer loadings between 0.40 and 0.70 should be removed only if the removal of these indicators will contribute to the raise of CR and AVE above their cut-off values [62]. The values of CR and AVE for the constructs FC and TV are already above the threshold values of 0.6 and 0.5, respectively. Therefore, the indicator FC4 and TV4 are retained in our study. The loadings for all items in the measurement model are in the range of 0.6720 to 0.9334, demonstrating satisfactory indicator reliability. Next, it is also shown in Table 2 that average variance extracted (AVE) for the constructs are having values in the range of 0.607 to 0.833, which are above the cut-off value of 0.5 [62,65], demonstrating an adequate convergent validity in this study.

Table 2.

Loading, composite reliability and average variance extracted.

In order to evaluate the discriminant validity of the model, Fornell–Larcker’s criterion and heterotrait–monotrait (HTMT) ratio of correlations are used [65,66]. Based on Fornell–Larcker’s criterion [65], the square root value of the AVE should be greater than the correlations for other constructs. Table 3 shows that the diagonal (in bold) elements signify the square root of the AVE and the off-diagonal values signify the intercorrelation values between other constructs. Based on the results, the square root of AVE is greater than all off-diagonal elements, demonstrating a satisfactory discriminant validity of the measurement model.

Table 3.

Fornell–Larcker criterion for testing discriminant validity.

Based on HTMT ratio of correlations technique [66], all the values fulfil the criterion of HTMT.85 (value lower than 0.85) and HTMT.90 (value lower than 0.90) [67,68], as shown in Table 4. In addition, HTMT inference was performed using a bootstrapping technique. It can be observed that all the values of the upper and the lower ends of the confidence interval with 95% (values in the brackets) are below one. This indicates that discriminant validity has been ascertained.

Table 4.

Heterotrait–monotrait assessment for testing discriminant validity.

4.2. Analysis of Structural Model

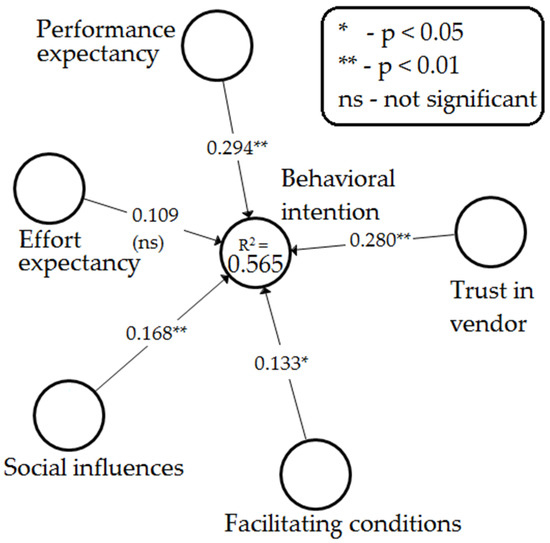

Firstly, the baseline model without the moderating effects was evaluated (Appendix A–Figure A1). All inner variance inflator factor (VIF) values for the variables varied from 1.383 to 2.080 are less than cut-off value of 3.3. This signifies that there is no lateral collinearity issue in the study [62,69]. The path coefficient should have a value above 0.1 to be deemed acceptable [70]. A bootstrapping function with 5000 subsamples was conducted using SmartPLS 3 to generate t-statistics for all paths [71]. One-tailed test was selected because each hypothesis is directional [72]. The results are summarized according to the sequence of hypotheses, as shown in Table 5.

Table 5.

Structural model assessment.

Based on the analysis, the predictors of PE (β = 0.294, t = 4.824, p < 0.01), SI (β = 0.168, t = 3.021, p < 0.01), FC (β = 0.133, t = 1.962, p < 0.05) and TV (β = 0.280, t = 3.877, p < 0.01) were positively related to BI. However, EE (β = 0.109, t = 1.445, p > 0.05) was not significant predictors of BI. Therefore, hypotheses H1, H3, H4 and H5 were supported while hypothesis H2 was not supported. The value of R2 represents the amount of variance in an endogenous variable that is explained by all the exogenous variables associated to it. From Figure A1, PE, EE, SI, FC and TV are able to explain 56.5% of variances in BI. This is above the value of 0.26 which indicates substantial level of predictive accuracy [73].

Table 6 shows the level of effect size for each predictor construct on the endogenous constructs. From the table, it can be observed that PE, SI, FC and TV have small effect in yielding the R2 for BI. For EE, the effect size is smaller than the threshold value of 0.02 for small size effect [73].

Table 6.

Effect size.

In examining the predictive relevance (Q2), blindfolding procedure was performed with the parameter of omission distance set to 7. The value between 5 and 10 for omission distance is recommended [74]. The cross-validated redundancy (CVR) approach was adopted in this analysis [62]. The model is deemed to have predictive relevance if the value of Q2 is above zero [75]. From Table 7, it can be observed that the values of Q2 for BI (Q2 = 0.460) is considerably above zero. Therefore, the model has sufficient predictive relevance.

Table 7.

Construct cross-validated redundancy.

4.3. Moderating Analysis

For the evaluation of a moderating effect, the baseline model was extended to include the moderator in this study. The two-stage approach is utilized in this study for moderation analysis. This approach is recommended if the purpose of the study is to determine if the moderator exerts a significant effect on the relationship [62]. Additionally, the two-stage approach has comparatively higher statistical power than product-indicator approach or orthogonalizing approach.

4.3.1. SA as the Moderator

Firstly, the moderation effect of SA was evaluated. With additional constructs included in the path model (i.e., SA and interaction term), the properties of other constructs (PE, EE, SI, FC, TV and BI) will be slightly altered. Reanalyzing the measurement model confirms the reliability and validity of the model. Table 8 shows the assessment of structural model with inclusion of SA as the moderator. The path coefficient of the interaction path (TV × SA) is −0.080 (t = 1.832). According to Lohmöller [70], the minimum value of path coefficient (β value) should be 0.10 to be statistically significant in the hypothesized path relationship between two variables. Therefore, this interaction path is not significant and thus, hypothesis H6 is not supported.

Table 8.

Structural model assessment with inclusion of SA as the moderator.

4.3.2. PEEIM as the Moderator

Similarly, the measurement model was reanalyzed to confirm the reliability and validity of the model when the moderation effect of PEEIM was evaluated. Table 9 shows the assessment of structural model with inclusion of PEEIM as the moderator. The path coefficient of the interaction path (TV × PEEIM) is −0.106 (t = 2.142) which is significant at p < 0.05.

Table 9.

Structural model assessment with inclusion of PEEIM as the moderator.

The new value of R2 is calculated as 0.580, which is slightly higher (2.65%) as compared to the R2 of the baseline model (0.565). The effect size of the interaction is calculated using the formula given below:

The term “R2 with moderator included” is the R2 obtained from the structural model with the interaction term evaluated and the term “R2 with moderator excluded” is the R2 of the baseline model. Therefore, the effect size is calculated as:

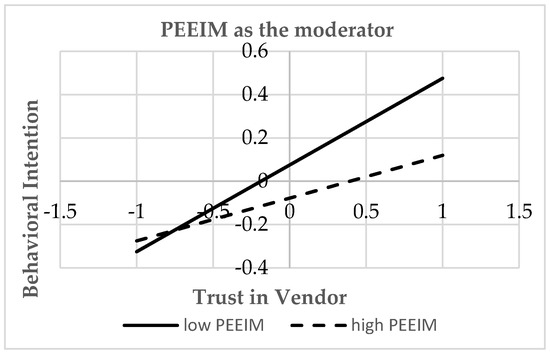

The trend and intensity of the moderating effect can be inspected from the interaction plot shown in Figure 2. In this figure, the two lines represent the relationship between TV (x-axis) and BI (y-axis). The solid and dotted lines represent the relationship for the lower and higher level of the moderator PEEIM, respectively. As can be seen in Figure 2, when the level of TV is high, the tendency of the BI in m-commerce adoption is higher, both in the cases of high and low PEEIM. The direction of the relationship between TV and BI in m-commerce adoption for both high PEEIM and low PEEIM are similar. In addition, it can be observed that the low PEEIM has a steeper gradient compared to the high PEEIM. This suggests that the effect of TV on users’ BI in adopting m-commerce is weaker when PEEIM is highly in place. Thus, hypothesis H7 is supported with the indication of the significant result of the interaction path (β = −0.106, t = 2.142, p < 0.05).

Figure 2.

Moderation effect of PEEIM on the relationship between TV and BI in m-commerce adoption.

5. Discussion

By comparing the relative importance of the independent constructs in predicting BI to adopt m-commerce, PE is the most important predictor. Based on the result, it shows that the benefits offered by m-commerce are vital for consumers. Online vendors of m-commerce should emphasis the convenience, good pricing feature and promotions to the consumers who are utilizing m-commerce services. This study echoes previous works that have also found association between PE and intention to adopt innovation technology [31,32,76]. It could be confirmed that if the benefits and advantages of using an innovation technology are presented adequately, users’ intention to use the new technology might be improved as well.

The study showed that EE does not significantly influence BI to accept m-commerce adoption. Since the penetration of smartphone usage in Malaysia is high, consumers nowadays have a lot of experience in using smartphone. Hence, it is likely that the consumers can use smartphone to handle m-commerce activities without much effort. Furthermore, if m-commerce could offer functions that are important to them, consumers would accept more efforts in applying it. Since PE served as the most vital factor in the current research, consumers appreciate the functions and benefits that m-commerce can provide; hence, EE would not be an obstacle when using m-commerce. Several recent studies reported that EE was not associated with the intention to adopt innovation technology, which is in agreement with our findings [39,40,46].

SI was also found to positively influence individual decision in accepting m-commerce. Consumers’ social networks such as family members, friends or colleagues play important roles in influencing an individual to use m-commerce. In line with our findings, previous studies have discovered SI significantly influence BI to adopt technologies within their context of studies [31,32,46]. In fact, Bawack and Kala Kamdjoug discovered that SI has the most significant effect on BI to use health information system in their model [76].

Next, FC such as technical knowledge and facilities are available and well-equipped to support consumers for developing intention to accept m-commerce adoption. For example, when consumers have mobile devices that are connected to the internet, with the knowledge to conduct m-commerce activities, they are more likely to use m-commerce. Our study echoes the similar outcome by Verkijika who deduced that FC positively influences the BI to adopt m-commerce in Cameroon [46]. In addition, Lallmahomed et al., Morosan and Defranco have observed a significant relationship as well [39,50]. However, Shaw and Sergueeva, Oliveira et al. and Herrero et al. did not find significant association between FC and BI in their studies [40,42,77].

From the analysis, H5 is supported, indicating that TV positively influences users’ BI in adopting m-commerce. Consumers are willing to follow online vendors or online sellers’ advice and purchase items from their sites. Additionally, consumer’s trusting beliefs towards a specific vendor is correlated with the purchasing intention with the vendor. The result of this study is in line with the findings of numerous past studies [18,28,61,78]. All the researchers agree that consumers’ trust in vendor is significantly related to their adoption behaviors. The well-known researchers in the context of trust-related studies—Pavlou and Gefen—explained that trust in vendor tends to reduce social uncertainty [28].

By assessing the boundary on how trust influences adoption intention, this study enhances the insight of conditional effect of trust. In this case, the outcome provides insight that trust could be much less important if a high level of PEEIM are in place. The perception of positive PEEIM will ease the evaluation process of consumers towards vendors’ trustworthiness (to the extent that it might diminish the establishment of trust in vendors) in adopting m-commerce. In other words, when trust development could be transferred to PEEIM, the rely on TV is weaken in adoption situation. Fang et al. [9] explored the moderation of PEEIM in terms of repurchase situation and discovered that the relationship between TV and repurchasing intention was affected negatively by PEEIM. This study further proves that during the initial purchasing process, PEEIM negatively moderate the relationship between TV and BI to adopt m-commerce. On the other hand, our results revealed that the moderation effect of SA on the same relationship is not significant. When PEEIM is more strongly framed from the perspective of lost reduction mechanisms, consumers are more likely to appreciate this type of value and, hence, attach to such lost reduction functions. If the transaction phenomenon is framed negatively by stressing on reducing loss, this would lead to a higher opportunity for consumers in conducting risk-taking behavior than it is framed positively. Therefore, our results imply that consumers are more desire for overall risk reducing functions during m-commerce transactions.

6. Conclusions

6.1. Theoretical Implications

Our study provides notable implications for theory. Firstly, one of the main and vital findings of this study is the discrepancy observed in the moderating effects of two institutional mechanisms (PEEIM and SA) which are conceptually very similar to each other. Previous studies have considered either PEEIM or SA as moderators in a separate manner and in different contexts of study [9,18,19,20,21]. Researchers may not recognize that PEEIM and SA can be combined and be examined simultaneously within the same framework. This is probably due to the assumption that the outcomes will be similar for two mechanisms that bear high degree of resemblance conceptually, in this case, PEEIM and SA. However, our findings reveal that the moderating effects of PEEIM and SA on the relationship between TV and BI in m-commerce adoption are different. Specifically, on the same relationship, PEEIM has a negative moderation effect, whereas for SA, the moderation effect is not significant. Therefore, it could be concluded that PEEIM has significantly more influential role than SA in the context of this study. By comparison, SA emphasizes on the effect of mechanisms in assuring safety and protection when performing online business, whereas PEEIM is highlighting that the risk of loss from conducting online transaction is diminished [9]. This implies that in an online transaction environment, assuring safety, protection and success in performing online business alone is no longer adequate. In other words, the relationship between trust in vendor and intention to adopt m-commerce is not significantly affected even though the mechanism of SA is highly in place. As m-commerce is getting more prevalent today, online consumers would consider that having safety and protection assured when performing online business is only meeting bare-minimum expectations. On the other hand, PEEIM negatively moderates the relationship between TV and BI to adopt m-commerce. This implies that if there exists a mechanism to protect one against any potential risks such as credit card fraud and leaking of personal information, the importance of trust in a vendor is weakened. As we can see from the results, the other implication is that consumers are paying considerably more attention to the overall risk reducing functions, as compared to assurance of safety and protection during m-commerce transactions.

This study is among the first to explore this assertion and our findings provide theoretical improvement in the existing literature by showing that two institutional mechanisms with almost similar function could exhibit distinctive influences on the trust transfer process. As compared to previous studies, it was found that SA has positive moderation effect in continuance intention in a pure e-service context [20]. Fang et al. and Chong et al. discovered negative moderating effects of PEEIM on repurchase intention in their studies [9,19], whereas Chen et al. concluded that PEEIM exert positive moderation effect on purchase intention [18]. This shows that the varying effects of PEEIM and SA are subjected to different contextual conditions.

Secondly, the present study is set to integrate the constructs of PE, EE, SI, FC, TV and trust transfer mechanisms together to evaluate individual acceptance of m-commerce. The R2 of this integrated model has accounted for 58.0 percent (for PEEIM as the moderator)—a noticeable value of coefficient determination that proved how well the regression predicts estimation of the integrated model. In previous studies, some researches took trust as a whole concept and integrated it into UTAUT/UTAUT2 [34,79,80]. Manrai and Gupta incorporated trust in service and trust in service provider into their research framework and the direct relationships with the BI to adopt mobile payments were examined [81]. In another recent study, Li explore how trust and perceived risk influence citizens’ e-government adoption using extended UTAUT model [37]. It was revealed that perceived risk exhibited moderating effects on the relationship between trust of the government and e-government adoption. In addition, by using modified UTAUT model, He et al. succeeded to improve the overall research model by integrating interpersonal trust and institutional trust variables [82]. By comparison, our current study not only investigates the direct relationship between trust (trust in vendor) and BI, but also delves into the moderating effects of the institutional mechanisms (PEEIM and SA). This study has filled the literature gap by including the institution-based trust (trust in vendor), institutional mechanisms (PEEIM and SA) and explore the moderating effects (trust transfer mechanism) simultaneously. To be more specific, how the aspects in security, protection and risk mitigation can affect the trust-intention relationships in the context of m-commerce acceptance are emphasized and investigated. As far as we are aware, this is the specific part which were not previously explored in UTAUT related models. In general, this study shows that trust in online vendors could be transferred to PEEIM. As for SA, consumers would expect this to be the minimum requirement for m-commerce environment. By strengthening the implications of the institutional mechanisms (PEEIM), on top of the mandatory features of SA, this will influence the trust towards online vendors and, hence, increase the adoption of m-commerce. The results also prove that by incorporating the trust transfer mechanisms into the model, it has increased the overall prediction estimation.

6.2. Managerial Implications

In terms of practical implication, this study may suggest some useful guidelines. First and foremost, our study indicates that while it remains imperative to establish the mechanism to assure safety and protection when performing online business, online vendors or platform owners should convince the consumers that the risk reduction mechanism is always in place. For example, when a consumer is performing online business with an online vendor, the first thing to be concerned could be related to the risk of credit card fraud. The consumer may ask: If my credit card is used fraudulently during this transaction, will the vendor refund my money? The implication is: when consumers perceive that the e-commerce institutional mechanism is considerably effective (risk mitigation), they will feel safe to conduct online transaction with the respective online vendor without relying too much on their trust alone (the trust in vendor). In general, our study indicates that it is mandatory for administrators to implement legally privacy protection and establish genuine security policy on m-commerce platforms (the existence of SA is the bare-minimum requirement). When there is an adequate security measure in the m-commerce platform, particularly in risk reduction aspects such as monetary transactions protection or faulty return policy, consumers will gain trust to conduct online transaction activities. Adequate initial trust to induce consumers for first time purchase can only be created if a well-established institutional infrastructure is in place for the whole m-commerce ecosystem. Next, mobile service providers also need to realize that trust transfer can exists between online vendors and institution-mechanisms (PEEIM). Therefore, the trust transfer mechanism requires service providers to execute effective institutional mechanisms so that a trustworthy environment for m-commerce activities could be established. The trustworthy environment is indeed a strong trust especially for customers to try and adopt m-commerce without prior experience.

Secondly, this study emphasizes the importance of PE, EE, SI, FC and TV in facilitating and increase the likelihood of m-commerce adoption. Our study reveals that mobile service providers need to leverage the m-commerce benefits efficiently to consumers so that they are aware of the m-commerce services provided in online platforms. As PE appeared to be the most influential predictors, m-commerce service providers should proactively highlight the advantages that m-commerce can offer. For example, the conveniences of using m-commerce services through mobile apps. Furthermore, online vendor providers should also emphasize that m-commerce tends to save time and money without the need to go to stores physically. Additionally, price comparison among online vendors could be done easily and efficiently. If service providers devote their attention to alleviate these benefits, it will certainty encourage more consumers to try and access m-commerce services. M-commerce could be more widely accepted if ample of facilities and incentives are provided. This includes initiatives such as smartphone can be sold in a cheaper price with lower tax, internet data is more affordable, delivery service is fast and on time. Moreover, m-commerce services providers may consider providing tips on how to conduct m-commerce transactions. Some short and simple tutorials about shopping tips and safety precautions can be provided to enhance the overall shopping experiences.

6.3. Limitations and Future Research

Firstly, the smartphone is used as the sole platform for m-commerce transactional activities in this study. The appropriateness of m-commerce as the transaction platform highly depends on the characteristics of the product or the service required. Therefore, product category could probably be included as the moderating variable in the future research to investigate their moderating effect that exist in product-acceptance relationship. Secondly, this study utilized the original UTAUT constructs (PE, EE, SI and FC). It is recommended to include the other variables from UTAUT2 to test the overall prediction estimation in the future studies. Lastly, this study focused mainly on the general perspectives of institution mechanism rather than specifying a vendor-specific companies. Future research could empirically explore the PEEIM and SA mechanisms within a specific online vendor category or online platform to provide a more in-depth view of distinct m-commerce environment.

Author Contributions

Conceptualization, J.J.S., S.H.L., K.L.W. and C.K.C.; methodology, J.J.S., S.H.L., K.L.W. and C.K.C.; software, J.J.S., S.H.L. and C.K.C.; validation, J.J.S., S.H.L., K.L.W. and C.K.C.; formal analysis, J.J.S., S.H.L., K.L.W. and C.K.C.; data curation, J.J.S., S.H.L., K.L.W. and C.K.C.; writing—original draft preparation, J.J.S. and S.H.L.; writing—review and editing, J.J.S., S.H.L., K.L.W. and C.K.C.; supervision, K.L.W. and C.K.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

The study was conducted according to the Ethical Principles and Guidelines for the Protection of Human Subjects of Research (Belmont Report) and approved by the Institutional Review Board (UTAR Scientific and Ethical Review Committee—SERC) of Universiti Tunku Abdul Rahman.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Figure A1.

Structural model (baseline model without moderating effects).

Table A1.

Questionnaire design (constructs and sources of items).

Table A1.

Questionnaire design (constructs and sources of items).

| Constructs | Items |

|---|---|

| Performance expectancy adapted from Venkatesh et al. (2012) | |

| PE1 | I find mobile commerce useful in my daily life. |

| PE2 | Using mobile commerce increases my chances of achieving things that are important to me. |

| PE3 | Using mobile commerce helps me accomplish things more quickly. |

| PE4 | Using mobile commerce increases my productivity. |

| Effort expectancy adapted from Venkatesh et al. (2012) | |

| EE1 | Learning how to use mobile commerce is easy for me. |

| EE2 | My interaction with mobile commerce is clear and understandable. |

| EE3 | I find mobile commerce easy to use. |

| EE4 | It is easy for me to become skillful at using mobile commerce. |

| Social influences adapted from Venkatesh et al. (2012) | |

| SI1 | People who are important to me think that I should use mobile commerce. |

| SI2 | People who influence my behavior think that I should use mobile commerce. |

| SI3 | People whose opinions that I value prefer that I use mobile commerce. |

| Facilitating conditions adapted from Venkatesh et al. (2012) | |

| FC1 | I have resource necessary to use mobile commerce. |

| FC2 | I have the knowledge necessary to use mobile commerce. |

| FC3 | Mobile commerce is compatible with other technologies I use. |

| FC4 | I can get help from others when I have difficulties using mobile commerce. |

| Perceived effectiveness of e-commerce institutional mechanisms adapted from Fang et al. (2014) | |

| PEEIM1 | When buying through smartphone, I am confident that there are mechanisms in place to protect me against any potential risks (eg. leaking of information, credit card fraud, goods not received, etc.) of online shopping if something goes wrong with my online mobile purchase. |

| PEEIM2 | I have confidence in third parties (eg. SafeTraders, TRUSTe) to protect me against any potential risks (eg. leaking of information, credit card fraud, goods not received, etc.) of online shopping if something goes wrong with my online mobile purchase. |

| PEEIM3 | I am sure that I cannot be taken advantage of (eg. leaking of information, credit card fraud, goods not received, etc.) of online shopping if something goes wrong with my online mobile purchase. |

| Trust in vendor adapted from Fang et al. (2014) | |

| TV1 | I believe that the online vendor is consistent in quality and service. |

| TV2 | I believe that the online vendor is keen on fulfilling my needs and wants. |

| TV3 | I believe that the online vendor is honest. |

| TV4 | I believe that the online vendor wants to be known as one that keeps promises and commitments. |

| TV5 | I believe that the online vendor has my best interests in mind. |

| TV6 | I believe that the online vendor is trustworthy. |

| TV7 | I believe that the online vendor has high integrity. |

| TV8 | I believe that the online vendor is dependable. |

| Structural assurance adapted from Gefen et al. (2003) | |

| SA1 | I feel safe conducting business with the online vendor because the authority will protect me. |

| SA2 | I feel safe conducting business with the online vendor because of it provides a 1-800 number. |

| SA3 | I feel safe conducting business with the online vendor because of its statements of guarantees. |

| SA4 | I feel safe conducting business with the online vendor because I accessed its site through a well-known, reputable portal. |

| Behavioral intention adapted from Venkatesh et al. (2012) | |

| BI1 | I intend to continue using mobile commerce in the future. |

| BI2 | I will always try to use mobile commerce in my daily life. |

| BI3 | I plan to continue to use mobile commerce frequently. |

References

- Xu, T. Development Analysis of O2O Model Based on Mobile Electronic Business. In Proceedings of the Fourth International Forum on Decision Sciences; Li, X., Xu, X., Eds.; Uncertainty and Operations Research; Springer: Singapore, 2017; pp. 507–516. ISBN 978-981-10-2919-6. [Google Scholar]

- Dabija, D.-C.; Lung, L. Millennials Versus Gen Z: Online Shopping Behaviour in an Emerging Market. In Applied Ethics for Entrepreneurial Success: Recommendations for the Developing World; Văduva, S., Fotea, I., Văduva, L.P., Wilt, R., Eds.; Springer Proceedings in Business and Economics; Springer International Publishing: Cham, Switzerland, 2019; pp. 1–18. ISBN 978-3-030-17214-5. [Google Scholar]

- Moorthy, K.; Johanthan, S.; Tham, C.; Xuan, K.X.; Yan, L.L.; Xunda, T.; Sim, T.C. Behavioural Intention to Use Mobile Apps by Gen Y in Malaysia. J. Inf. 2019, 5, 1–15. [Google Scholar] [CrossRef]

- Moorthy, K.; Chun T’ing, L.; Chea Yee, K.; Wen Huey, A.; Joe In, L.; Chyi Feng, P.; Jia Yi, T. What Drives the Adoption of Mobile Payment? A Malaysian Perspective. Int. J. Fin. Econ. 2020, 25, 349–364. [Google Scholar] [CrossRef]

- Global Mobile eCommerce Statistics, Trends & Forecasts (2020). Available online: https://www.merchantsavvy.co.uk/mobile-ecommerce-statistics/ (accessed on 3 September 2021).

- Digital 2020. Available online: https://wearesocial.com/digital-2020 (accessed on 5 July 2021).

- Hooi, R.T.S. E-Wallets to Carve up More Market. Available online: https://www.thestar.com.my/news/nation/2020/01/02/e-wallets-to-carve-up-more-market (accessed on 5 July 2021).

- Ecommerce in Malaysia in 2019. Available online: https://datareportal.com/reports/digital-2019-ecommerce-in-malaysia (accessed on 5 July 2021).

- Fang, Y.; Qureshi, I.; Sun, H.; McCole, P.; Ramsey, E.; Lim, K.H. Trust, Satisfaction, and Online Repurchase Intention: The Moderating Role of Perceived Effectiveness of E-Commerce Institutional Mechanisms. MIS Q. 2014, 38, 407–427. [Google Scholar] [CrossRef] [Green Version]

- Gao, L.; Waechter, K.A. Examining the Role of Initial Trust in User Adoption of Mobile Payment Services: An Empirical Investigation. Inf. Syst. Front. 2017, 19, 525–548. [Google Scholar] [CrossRef]

- Liu, Y.; Tang, X. The Effects of Online Trust-Building Mechanisms on Trust and Repurchase Intentions: An Empirical Study on EBay. Inf. Technol. People 2018, 31, 666–687. [Google Scholar] [CrossRef]

- Stouthuysen, K.; Teunis, I.; Reusen, E.; Slabbinck, H. Initial Trust and Intentions to Buy: The Effect of Vendor-Specific Guarantees, Customer Reviews and the Role of Online Shopping Experience☆. Electron. Commer. Res. Appl. 2018, 27, 23–38. [Google Scholar] [CrossRef]

- McKnight, D.H.; Chervany, N.L. What Trust Means in E-Commerce Customer Relationships: An Interdisciplinary Conceptual Typology. Int. J. Electron. Commer. 2001, 6, 35–59. [Google Scholar] [CrossRef]

- Huang, P.-C.; Hou, C.-C.; Chen, J.-S. Analyzing the Trust Mechanism of the Sharing Economy Based on Innovation Diffusion Theory and Innovation Resistance Theory. Manag. Rev. 2017, 36, 123–137. [Google Scholar] [CrossRef]

- E-Commerce Consumers Survey 2018. Available online: https://www.mcmc.gov.my/skmmgovmy/files/2c/2c7d733b-e086-43f1-9254-97cf0740c733/files/assets/basic-html/page-1.html# (accessed on 5 July 2021).

- Wei, K.; Li, Y.; Zha, Y.; Ma, J. Trust, Risk and Transaction Intention in Consumer-to-Consumer e-Marketplaces: An Empirical Comparison between Buyers’ and Sellers’ Perspectives. IMDS 2019, 119, 331–350. [Google Scholar] [CrossRef]

- Özpolat, K.; Gao, G.; Jank, W.; Viswanathan, S. Research Note—The Value of Third-Party Assurance Seals in Online Retailing: An Empirical Investigation. Inf. Syst. Res. 2013, 24, 1100–1111. [Google Scholar] [CrossRef]

- Chen, X.; Huang, Q.; Davison, R.M.; Hua, Z. What Drives Trust Transfer? The Moderating Roles of Seller-Specific and General Institutional Mechanisms. Int. J. Electron. Commer. 2015, 20, 261–289. [Google Scholar] [CrossRef]

- Chong, A.Y.L.; Lacka, E.; Boying, L.; Chan, H.K. The Role of Social Media in Enhancing Guanxi and Perceived Effectiveness of E-Commerce Institutional Mechanisms in Online Marketplace. Inf. Manag. 2018, 55, 621–632. [Google Scholar] [CrossRef] [Green Version]

- McCole, P.; Ramsey, E.; Kincaid, A.; Fang, Y.; Li, H. The Role of Structural Assurance on Previous Satisfaction, Trust and Continuance Intention: The Case of Online Betting. ITP 2019, 32, 781–801. [Google Scholar] [CrossRef] [Green Version]

- Huang, Q.; Chen, X.; Ou, C.X.; Davison, R.M.; Hua, Z. Understanding Buyers’ Loyalty to a C2C Platform: The Roles of Social Capital, Satisfaction and Perceived Effectiveness of e-Commerce Institutional Mechanisms: The Impact of Social Capital on Buyer Satisfaction. Inf. Syst. J. 2017, 27, 91–119. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Kim, D.J. A Study of the Multilevel and Dynamic Nature of Trust in E-Commerce from a Cross-Stage Perspective. Int. J. Electron. Commer. 2014, 19, 11–64. [Google Scholar] [CrossRef]

- Mcknight, D.H.; Kacmar, C.J.; Choudhury, V. Shifting Factors and the Ineffectiveness of Third Party Assurance Seals: A Two-Stage Model of Initial Trust in a Web Business. Electron. Mark. 2004, 14, 252–266. [Google Scholar] [CrossRef]

- Wang, N.; Shen, X.-L.; Sun, Y. Transition of Electronic Word-of-Mouth Services from Web to Mobile Context: A Trust Transfer Perspective. Decis. Support. Syst. 2013, 54, 1394–1403. [Google Scholar] [CrossRef]

- Pop, R.-A.; Săplăcan, Z.; Dabija, D.-C.; Alt, M.-A. The Impact of Social Media Influencers on Travel Decisions: The Role of Trust in Consumer Decision Journey. Curr. Issues Tour. 2021, 1–21. [Google Scholar] [CrossRef]

- Stewart, K.J. Trust Transfer on the World Wide Web. Organ. Sci. 2003, 14, 5–17. [Google Scholar] [CrossRef]

- Pavlou, P.A.; Gefen, D. Building Effective Online Marketplaces with Institution-Based Trust. Inf. Syst. Res. 2004, 15, 37–59. [Google Scholar] [CrossRef] [Green Version]

- Zucker, L.G. Production of Trust: Institutional Sources of Economic Structure, 1840–1920. Res. Organ. Behav. 1986, 8, 53–111. [Google Scholar]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Q. 2012, 36, 157. [Google Scholar] [CrossRef] [Green Version]

- Wang, H.; Tao, D.; Yu, N.; Qu, X. Understanding Consumer Acceptance of Healthcare Wearable Devices: An Integrated Model of UTAUT and TTF. Int. J. Med. Inform. 2020, 139, 104156. [Google Scholar] [CrossRef] [PubMed]

- Shiferaw, K.B.; Mehari, E.A. Modeling Predictors of Acceptance and Use of Electronic Medical Record System in a Resource Limited Setting: Using Modified UTAUT Model. Inform. Med. Unlocked 2019, 17, 100182. [Google Scholar] [CrossRef]

- Mousa Jaradat, M.-I.R.; Al Rababaa, M.S. Assessing Key Factor That Influence on the Acceptance of Mobile Commerce Based on Modified UTAUT. IJBM 2013, 8, 102. [Google Scholar] [CrossRef] [Green Version]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-Related Factors in Extended UTAUT Model for NFC Based Mobile Payment in the Restaurant Industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Zhou, T. Examining Users’ Switch from Online Banking to Mobile Banking. Int. J. Netw. Virtual Organ. 2018, 18, 51–66. [Google Scholar] [CrossRef]

- Yeh, Y.-S.; Li, Y.-M. Design-to-Lure in the e-Shopping Environment: A Landscape Preference Approach. Inf. Manag. 2014, 51, 995–1004. [Google Scholar] [CrossRef]

- Li, W. The Role of Trust and Risk in Citizens’ E-Government Services Adoption: A Perspective of the Extended UTAUT Model. Sustainability 2021, 13, 7671. [Google Scholar] [CrossRef]

- Dwivedi, Y.K.; Rana, N.P.; Chen, H.; Williams, M.D. A Meta-analysis of the Unified Theory of Acceptance and Use of Technology (UTAUT). In Governance and Sustainability in Information Systems. Managing the Transfer and Diffusion of IT; Nüttgens, M., Gadatsch, A., Kautz, K., Schirmer, I., Blinn, N., Eds.; IFIP Advances in Information and Communication Technology; Springer: Berlin/Heidelberg, Germany, 2011; Volume 366, pp. 155–170. ISBN 978-3-642-24147-5. [Google Scholar]

- Lallmahomed, M.Z.I.; Lallmahomed, N.; Lallmahomed, G.M. Factors Influencing the Adoption of E-Government Services in Mauritius. Telemat. Inform. 2017, 34, 57–72. [Google Scholar] [CrossRef]

- Herrero, Á.; San Martín, H.; del Mar Garcia-De los Salmones, M. Explaining the Adoption of Social Networks Sites for Sharing User-Generated Content: A Revision of the UTAUT2. Comput. Hum. Behav. 2017, 71, 209–217. [Google Scholar] [CrossRef] [Green Version]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust: CONSUMERS’ ADOPTION INTENTIONS OF REMOTE MOBILE PAYMENTS. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile Payment: Understanding the Determinants of Customer Adoption and Intention to Recommend the Technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Musa, A.; Khan, H.U.; AlShare, K.A. Factors Influence Consumers’ Adoption of Mobile Payment Devices in Qatar. IJMC 2015, 13, 670. [Google Scholar] [CrossRef]

- Tsou, H.-T.; Chen, J.-S.; Chou, Y.; Chen, T.-W. Sharing Economy Service Experience and Its Effects on Behavioral Intention. Sustainability 2019, 11, 5050. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Davis, F.D. A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef] [Green Version]

- Verkijika, S.F. Factors Influencing the Adoption of Mobile Commerce Applications in Cameroon. Telemat. Inform. 2018, 35, 1665–1674. [Google Scholar] [CrossRef]

- Prayoonphan, F.; Xu, X. Factors Influencing the Intention to Use the Common Ticketing System (Spider Card) in Thailand. Behav. Sci. 2019, 9, 46. [Google Scholar] [CrossRef] [Green Version]

- Mensah, I.K. Factors Influencing the Intention of University Students to Adopt and Use E-Government Services: An Empirical Evidence in China. SAGE Open 2019, 9, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Chen, K.; Chan, A.H.S. Gerontechnology Acceptance by Elderly Hong Kong Chinese: A Senior Technology Acceptance Model (STAM). Ergonomics 2014, 57, 635–652. [Google Scholar] [CrossRef]

- Morosan, C.; DeFranco, A. It’s about Time: Revisiting UTAUT2 to Examine Consumers’ Intentions to Use NFC Mobile Payments in Hotels. Int. J. Hosp. Manag. 2016, 53, 17–29. [Google Scholar] [CrossRef]

- Jarvenpaa, S.L.; Tractinsky, N.; Saarinen, L. Consumer Trust in an Internet Store: A Cross-Cultural Validation. J. Comput.-Mediat. Commun. 2006, 5. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Marinković, V.; Kalinić, Z. A SEM-Neural Network Approach for Predicting Antecedents of m-Commerce Acceptance. Int. J. Inf. Manag. 2017, 37, 14–24. [Google Scholar] [CrossRef]

- Zhang, L.; Zhu, J.; Liu, Q. A Meta-Analysis of Mobile Commerce Adoption and the Moderating Effect of Culture. Comput. Hum. Behav. 2012, 28, 1902–1911. [Google Scholar] [CrossRef]

- Chong, A.Y.-L.; Chan, F.T.S.; Ooi, K.-B. Predicting Consumer Decisions to Adopt Mobile Commerce: Cross Country Empirical Examination between China and Malaysia. Decis. Support. Syst. 2012, 53, 34–43. [Google Scholar] [CrossRef]

- Giovanis, A.; Assimakopoulos, C.; Sarmaniotis, C. Adoption of Mobile Self-Service Retail Banking Technologies: The Role of Technology, Social, Channel and Personal Factors. IJRDM 2019, 47, 894–914. [Google Scholar] [CrossRef]

- Chang, M.K.; Cheung, W.; Tang, M. Building Trust Online: Interactions among Trust Building Mechanisms. Inf. Manag. 2013, 50, 439–445. [Google Scholar] [CrossRef]

- Shao, Z.; Yin, H. Building Customers’ Trust in the Ridesharing Platform with Institutional Mechanisms: An Empirical Study in China. Internet Res. 2019, 29, 1040–1063. [Google Scholar] [CrossRef]

- Chiu, C.-M.; Hsu, M.-H.; Lai, H.; Chang, C.-M. Re-Examining the Influence of Trust on Online Repeat Purchase Intention: The Moderating Role of Habit and Its Antecedents. Decis. Support. Syst. 2012, 53, 835–845. [Google Scholar] [CrossRef]

- Luhmann, N. Trust and Power; English edition; Polity: Malden, MA, USA, 2017; ISBN 978-1-5095-1945-3. [Google Scholar]

- Steele, J.; Bourke, L.; Luloff, A.E.; Liao, P.-S.; Theodori, G.L.; Krannich, R.S. The Drop-Off/Pick-Up Method For Household Survey Research. Community Dev. Soc. J. 2001, 32, 238–250. [Google Scholar] [CrossRef]

- Gefen; Karahanna; Straub Trust and TAM in Online Shopping: An Integrated Model. MIS Q. 2003, 27, 51. [CrossRef]

- Hair, J.F. (Ed.) A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Los Angeles, CA, USA, 2017; ISBN 978-1-4833-7744-5. [Google Scholar]

- Bagozzi, R.P.; Yi, Y. On the Evaluation of Structural Equation Models. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Hair, J.F. (Ed.) Multivariate Data Analysis: Pearson New International Edition, 7th ed.; Pearson: Harlow, UK, 2014; ISBN 978-1-292-02190-4. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A New Criterion for Assessing Discriminant Validity in Variance-Based Structural Equation Modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Kline, R.B. Principles and Practice of Structural Equation Modeling, 4th ed.; Methodology in the social sciences; The Guilford Press: New York, NY, USA, 2016; ISBN 978-1-4625-2335-1. [Google Scholar]

- Gold, A.H.; Malhotra, A.; Segars, A.H. Knowledge Management: An Organizational Capabilities Perspective. J. Manag. Inf. Syst. 2001, 18, 185–214. [Google Scholar] [CrossRef]

- Diamantopoulos, A.; Siguaw, J.A. Formative Versus Reflective Indicators in Organizational Measure Development: A Comparison and Empirical Illustration. Br. J. Manag. 2006, 17, 263–282. [Google Scholar] [CrossRef]

- Lohmöller, J.-B. Latent Variable Path Modeling with Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 1989; ISBN 978-3-642-52512-4. [Google Scholar]

- Ringle, C.M.; Wende, S.; Becker, J.-M. SmartPLS 3 2015; SmartPLS GmbH: Boenningstedt, Germany, 2015. [Google Scholar]

- Ramayah, T.; Cheah, J.; Chuah, F.; Ting, H.; Memon, M.A. Partial Least Squares Structural Equation Modeling (PLS-SEM) Using SmartPLS 3.0: An. Updated Guide and Practical Guide to Statistical Analysis, 2nd ed.; Pearson Malaysia Sdn Bhd: Kuala Lumpur, Malaysia, 2018; ISBN 978-967-349-750-8. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; L. Erlbaum Associates: Hillsdale, NJ, USA, 1988; ISBN 978-0-8058-0283-2. [Google Scholar]

- Chin, W.W. The partial least squares approach for structural equation modeling. In Modern Methods for Business Research; Quantitative Methodology Series; Lawrence Erlbaum: Mahwah, NJ, USA, 1988; pp. 295–336. [Google Scholar]

- Fornell, C.; Cha, J. Partial Least Squares. In Advanced Methods of Marketing Research; Blackwell Business: Cambridge, UK, 1994; pp. 52–78. ISBN 978-1-55786-549-6. [Google Scholar]

- Bawack, R.E.; Kala Kamdjoug, J.R. Adequacy of UTAUT in Clinician Adoption of Health Information Systems in Developing Countries: The Case of Cameroon. Int. J. Med. Inform. 2018, 109, 15–22. [Google Scholar] [CrossRef]

- Shaw, N.; Sergueeva, K. The Non-Monetary Benefits of Mobile Commerce: Extending UTAUT2 with Perceived Value. Int. J. Inf. Manag. 2019, 45, 44–55. [Google Scholar] [CrossRef]

- Hong, I.B.; Cho, H. The Impact of Consumer Trust on Attitudinal Loyalty and Purchase Intentions in B2C E-Marketplaces: Intermediary Trust vs. Seller Trust. Int. J. Inf. Manag. 2011, 31, 469–479. [Google Scholar] [CrossRef]

- Oh, J.-C.; Yoon, S.-J. Predicting the Use of Online Information Services Based on a Modified UTAUT Model. Behav. Inf. Technol. 2014, 33, 716–729. [Google Scholar] [CrossRef]

- Rodrigues, G.; Sarabdeen, J.; Balasubramanian, S. Factors That Influence Consumer Adoption of E-Government Services in the UAE: A UTAUT Model Perspective. J. Internet Commer. 2016, 15, 18–39. [Google Scholar] [CrossRef]

- Manrai, R.; Gupta, K.P. Integrating UTAUT with Trust and Perceived Benefits to Explain User Adoption of Mobile Payments. In Strategic System Assurance and Business Analytics; Kapur, P.K., Singh, O., Khatri, S.K., Verma, A.K., Eds.; Asset Analytics; Springer: Singapore, 2020; pp. 109–121. ISBN 9789811536465. [Google Scholar]

- He, K.; Zhang, J.; Zeng, Y. Households’ Willingness to Pay for Energy Utilization of Crop Straw in Rural China: Based on an Improved UTAUT Model. Energy Policy 2020, 140, 111373. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).