FinTech 2026, 5(2), 45; https://doi.org/10.3390/fintech5020045 - 21 May 2026

Abstract

This study examines the impact of artificial intelligence (AI) and the development of FinTech services on firms’ financial performance, with particular emphasis on the moderating role of dynamic capabilities. Drawing on the dynamic capabilities perspective, the study explains how organizations can effectively leverage

[...] Read more.

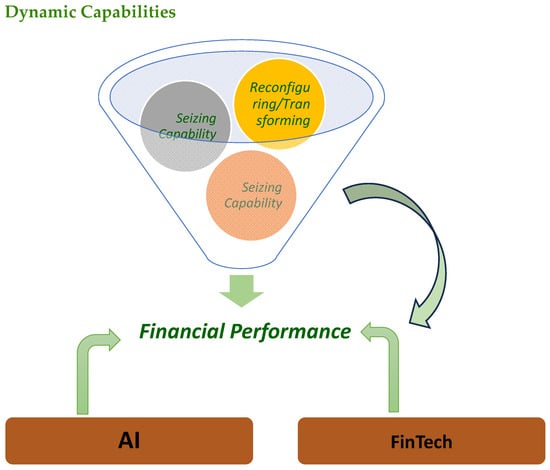

This study examines the impact of artificial intelligence (AI) and the development of FinTech services on firms’ financial performance, with particular emphasis on the moderating role of dynamic capabilities. Drawing on the dynamic capabilities perspective, the study explains how organizations can effectively leverage emerging digital technologies to enhance financial outcomes. The study is applied in purpose and adopts a descriptive correlational design. Data were collected using four structured questionnaires administered to 384 respondents, including senior executives, chief financial officers, and board members of companies listed on the Tehran Stock Exchange. A convenience sampling method was employed. The conceptual model and research hypotheses were tested using structural equation modeling based on the partial least squares structural equation modeling (PLS-SEM) approach, implemented using IBM SPSS Statistics version 29 and Smart PLS version 4. The results indicate that both artificial intelligence and FinTech have positive and statistically significant effects on firms’ financial performance. Although dynamic capabilities do not have a direct statistically significant effect on financial performance, they play a significant moderating role in the relationship between FinTech and financial performance. A disaggregated analysis of the dimensions of dynamic capabilities shows that only sensing capability has a positive and statistically significant moderating effect on the relationship between FinTech and financial performance, whereas seizing and reconfiguring capabilities do not show statistically significant moderating effects. By emphasizing the conditional and indirect role of dynamic capabilities, this study contributes to the growing literature on FinTech and artificial intelligence in emerging markets. The findings suggest that performance advantages from FinTech and AI stem less from the technologies themselves and more from firms’ ability to identify and interpret technological opportunities promptly. The study provides valuable practical insights for managers of publicly listed Iranian firms and clarifies how digital investments translate into improved financial performance.

Full article

(This article belongs to the Special Issue The Impact of AI in Business, Finance and Accounting)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}