Abstract

The focus of this study looks at the motivations and rationale from a national survey of over 7200 Canadians in November 2020 into why they use online services to purchase food. As a result of the global COVID-19 pandemic, food supply chains have been significantly altered. Consumers are purchasing foods with different dynamics, including when they buy in-person at groceries, at restaurants or at food service establishments. Elements of the food supply chain will be permanently altered post-pandemic. The study looks at a specific set of factors, captured in the survey, namely, consumer price sensitivity to the costs of online food purchasing, growing sustainability-related concerns over food packaging and waste, and product sensory experience related to how online purchasing changes from in-person food selection. The end goal, emerging from a case study, is insight into the strategies and preparedness with which CPGs, food services, and retailers can better manage the supply chain in their food product offerings in the post-pandemic era.

1. Introduction

In Canada, we estimate that over CAD 12 billion have been committed to online interface services in the food industry, over the next 5 years, as several companies have made commitments to invest further in digital distribution projects and e-commerce. As e-commerce is most likely to persist, this is a rough estimation from knowing the budgets of the top leading Canadian grocery chains, which include Loblaws, Sobeys, and Metro [1,2,3]. Online services have improved significantly across the country as Canadians have now more options online than ever [4].

This article focuses on three determinants examined in a Canadian national survey, each having a lasting impact on food supply chains and how they can be addressed post-pandemic. These categories are (i) price sensitivity to online purchasing, (ii) sustainability-motivated factors for consumers, and how retail and food service can reduce their supply chain impact, and (iii) product sensory experience lost, especially in the context of online purchasing. These are often ‘middle mile’ logistical challenges. We postulate in this study what this means for supply chains, and for digital food products marketing. The uniqueness of this study is based on the fact that the survey was conducted in the middle of the pandemic, and that perceptions are likely impacted by how respondents perceive systemic risks related to the virus. The objective of this study is namely to look at how the acceleration of e-commerce and online food shopping under the pandemic will have lasting elements post-pandemic, and food supply chains will need to take account to meet consumer concerns, or their hesitations towards using e-commerce for food purchases.

2. Food’s Virtual Market

CPG (consumer packaged goods) brands need to think critically about their products in new ways, and especially about the online experience, how information is conveyed, and how people are interacting with physical food products. Many consumers are increasingly using mobile devices, and food companies need to think carefully about the online customer experience, whether on smart phones or laptops. Online shopping (and the associated experience), driven during the pandemic, is likely to persist to some degree post-pandemic, and will continue to be a major introduction source for food products and services. According to NielsenIQ [5], food groceries from online purchases grew 55% in 2020, up from 44% growth in 2019. A 2020 study from Indonesia about online grocery shopping points out the ‘factors influencing consumer intention to switch to online shopping include perceived risk, price-search intention, mobility, and delivery time, adding that ‘gender moderates the influences of attitude, design and site image variables with online shopping interest’ [6].

Online food retailers are focusing on price, assortment, convenience, and service to ease the transition between online and offline purchases, adding that innovation with online shopping creates uncertainty from known and routine behaviours, and can result in increased levels of risk, skepticism, and distrust, something that brands, and food product marketers need to be very aware of [7]. The authors refer to studies where time, physical constraints, and risk concerns are only a very minor role, and where major lifestyle changes, such as having children, are big factors for consideration of online groceries. Women are still usually the main household member responsible for grocery shopping, and therefore a relevant target group for the online grocery channel, and ‘consumer motivations to adopt online grocery shopping in fact lie at the household level’, while ‘studies relying solely on personal-level sociodemographics may fail to detect the whole picture and may even make incorrect inferences’ [8].

Establishing trust is a very important factor for new consumers adopting online grocery channels, whereas a 2020 study reiterates that ‘turning to online grocery shopping often coincides with major life events, and transitions, such as caring for a sick relative or the birth of a child’ [9]. Additional studies on online food shopping patterns have found that consumer concerns about freshness, bruising, and food safety [10,11,12] may make consumers less likely to purchase fresh and perishable foods online such as fruits, vegetables, and meat that are essential for a balanced diet [13,14]. Consumers living in an urban food desert who were given a voucher for online grocery shopping used at least some of the voucher on fresh and perishable foods [15]. Online grocery shopping may also help to promote healthier eating by decreasing impulse purchases while ‘online shopping is both a technology decision and a consumer decision and needs to be examined as such’, and ‘online induced retailer cross-purchasing is increasing over time’ [16,17,18,19,20]. People are buying in store from what they learned about online.

The positive relationship between e-commerce capability, market capitalizing agility, operational adjustment agility, and the moderating role of environmental dynamism providing good value for thinking about supply chains emphasizes that consumers have many, context-specific sensitivities to online shopping platforms and preferences [21]. Research on market leaders such as Amazon, fulfilled by Whole Foods, were forced to suspend certain services during the pandemic, delivery times were in short supply, and delivery delays were to be expected [22,23]. In stark contrast was the demand for goods supplied by local food retailers whose logistics for fulfilling online orders had not been established pre-COVID-19.

Before the pandemic, Nielsen and the Food Marketing Institute estimated that online grocery sales were expected to constitute 20% of the market by 2025 [24]. Furthermore, ‘as demand for online food purchases [has] surged, fulfillment, and distribution centers were left overwhelmed’, adding that ‘based on the observed interest in grocery delivery and pick-up services, there is an opportunity for retailers to sustain market share if they offer these programs or partner with existing services. Retailers that have more robust [supply chain] logistics in place may be more prepared to seamlessly integrate grocery delivery, offering it as a permanent service, as delivery and pick-up services continue to grow in popularity as a shopping mode for many consumers… because of channel agnosticism among consumers, brand continuity is crucial, hence, food manufacturers would need to build a flexible back end to offer products more ubiquitously’ [25].

2.1. Price Sensitivity

In 2021, constrained food shoppers continue seeking out more affordable alternatives to the product options they would normally buy, opting for more value offerings and private label products, at least for their everyday staples. Tiering products and pricing will become increasingly important as the year progresses. For consumers with greater disposable income (as a result of deferred travel-dining-entertainment costs), ‘since COVID-19, 24% of Canadian consumers are willing to pay more for food products that claim ease of home preparation’, and a shift towards higher-priced, and premium products and specialty goods is suggested by a NielsenIQ study [26]. Money matters to shoppers in relation to their openness to online shopping. While time saving is an advantage for online groceries, most households are also convinced of the cost savings. Management and supply chain messaging implications for grocers figure into the convenience and cost factors contributing to the ‘adoption’ vs. ‘non-adoption’ tipping point for new online food shoppers [27].

Online food prices during the pandemic, have led to asking questions such as ‘how did online grocers react to this extreme surge in demand? Did they use the opportunity to increase prices, especially for highly demanded products? Did they offer fewer sales promotions because of less need to attract customers? The research provides a lesson from Amazon’s online grocery presence in the USA, and notes that Amazon Fresh’s meat and seafood prices decreased compared with 2019, most strongly in the lockdown phase in April–May 2020, with median prices 2.5% lower than in the previous year [28]. This finding suggests that Amazon Fresh’s pricing decisions must depend on factors other than general US price trends and the supply situation. Amazon seems to apply its low-price strategy, for which the company is known in other sectors, also to its grocery business and in unusual times of high demand’, adding that ‘customer obsession’ and the demand surge during the COVID-19 pandemic will push Amazon into a leading position in the food retail sector [29]. If they succeed, Amazon Fresh with its low prices, will become a challenging competitor to other food retailers both online and offline. This is especially true because unlike pure grocery retailers, Amazon can cross-subsidize its low-margin grocery business with profits from the high-margin Amazon Web Services business unit [30].

2.2. Sustainability Concerns

Amidst the pandemic, and especially over the past decade, there has been a growing consumer consciousness about food packaging waste, and the impact of single-use plastics from grocery and food service. According to a 2020 study by NielsenIQ, ‘consumers [insulated during the pandemic] will shift to sustainability-focused products, to re-invigorate eco-friendly practices, an opportunity for sustainability’ [31]. FMCG (fast-moving consumer goods) are moving towards sustainability initiatives along with pressure to address all elements of the product footprint from ingredients, packaging, waste, carbon and resource footprint of manufacturing operations. According to the supply chain director at General Mills Foods, 2021 is the year of the supply chain, making sustainability an integral part of their decision making [32]. Contrastingly, according to Sustainable Brands, brands should focus on the solutions, rather than dramatizing the problem, making actions tangible and solvable, for example, with good reusable packaging.

NielsenIQ notes ‘health-minded buying will remain beyond the pandemic’. According to a recent survey, 36% of North American consumers plan to purchase health-wellness products online after the pandemic, and 24% are willing to switch their current products for those that offer natural-sustainable ingredients. For NielsenIQ, developing a sustainability mindset in FMCG will require understanding the size of the (sustainability) prize, zeroing in on the consumers who value it most, and what they specifically care about, and knowing how to thread the needle. The year 2021 can translate to a major year for FMCGs, and sustainability-oriented consumer spending growth is expected to exceed general spending by Canadians overall. A May 2020 NielsenIQ panel found that consumers are most personally concerned about plastic waste (73%), and the action companies should most take includes ‘reducing plastic packaging’ as the number one choice at 78% of respondents. The panel findings also add that beyond sustainability, in-store execution, consumer engagement, brand marketing, 3rd party logo verification, and addressing supply chain logistics to address sustainability concerns, including issues with returning packaging for store credits, remain practical planning challenges for retailers and CPG brands.

Consumers may be less interested in certain credence (sustainable or ethical) attributes, and these general shifts imply that consumers may have shifted their food values during the pandemic [33,34,35]. The pandemic and its aftermath may improve household skills and management practices in a manner that reduces day-to-day household food waste [36]. However, pandemic-driven disruptions may induce larger intermittent purges of food due to changes in work patterns and food service and food retailing availability. Contrastingly, the (pandemic) lockdown has fostered e-commerce, resulting in significant consumption of materials for containment and packaging [37].

Consider the supply chain, and concern over packaging sustainability in online grocery and food service delivery by adding, ‘the calculated cost of a material cannot be only that of the raw material, but should consider the impact on the environment’ [38]. To do so, the whole production system must be considered, including waste generation, collection, transport, recycling and treatment, use of recovered resource and disposal of remains. The circular approach allows for both reducing dependency on resource markets and decreasing disposal costs. The COVID-19 pandemic is expected to spur a transition to new models of circular economy; however, this is conditional on many factors. This raises important considerations, not only in terms of consumer response to concern over packaging waste, but to supply chains in general. In the post-pandemic world, some COVID-19 habits will probably hang on for a long time. E-commerce sales may continue to grow, as many consumers will not give up on the benefits of convenience and choice, potentially leading to an increase in packaging material and associated problems of treatment and recycling. Incentives can help companies reduce the use of raw materials in favor of those coming from recycling. The psychological aspects of consumers and encouraging sustainable products and processes can help achieve sustainable development. Plastics are important because they provide many advantages, yet instead of demonizing, we should learn to use plastics responsibly.

An important contribution towards understanding consumer behaviour related to sustainability is that ‘managers see pandemics as catalysts to prepare and respond more effectively’ [39]. In addition, firms must strategically build e-commerce platforms and operate in conjunction with offline methods for supplies because consumers turn to online sources to avoid infectious diseases and are increasingly engaging in sustainable consumption behaviors. Overall, this study provides new perspective on the critical role of e-commerce platforms and economic benefits and sets a supplementing point for future research to further explore sustainable consumption behavior of customers in the boundary condition of pandemic fear.

2.3. Loss of In-Person Food Sensory Experience/Concern over Food Substitutions and Safety

From the 2020 Dalhousie–Caddle survey on e-commerce, questions posed about what concerns people have in regard to their online grocery/food purchases included the following: ‘I cannot see the food before purchase’, ‘I am concerned about the quality of the food’, ‘unconfirmed product substitutions’, and ‘contact by others’. A major element in addressing all of this is building trust with the consumer, and also making tangible changes in building trust by addressing these concerns. For example, packaging with information clearly addressing these concerns is a step towards helping consumer confidence. Consumers during the pandemic have also been concerned with their immune systems, and brands can help with this concern, as it will remain a big issue post-pandemic. Some companies have, throughout their supply chain, used digital data gathering to detect anomalies and, in turn, alter or fix course. To address the Dalhousie–Caddle survey question ‘contact by others’, some coffee retailers offer contactless delivery, just as fast and quick service restaurants are as well. While a post-pandemic return to in-store shopping will most likely resume, there is something missed in the ‘touch and feel’ with online shopping. Brands need to be aware of this, with product descriptions, enhanced visuals, content, storytelling, emotional engagement, and addressing pain points. Interestingly, nutritional goals and healthy eating play a minor role in consumer choice, only 2% of US participants mentioned this aspect of motivation, while nearly 11% of German respondents stated that they engage in online grocery shopping to improve their…nutritional goals’ [40].

A concern amongst respondents to the Dalhousie–Caddle survey was ‘contact by others’, highlighting that ‘the use of e-wallet and digital payments’ saw an increase during the pandemic, while in developing countries, digital payment or credit card payment is encouraged to limit contact with delivery partners [41,42]. Online food delivery services (OFD) can provide attractive cashback offers or reward points, for digital payments, which motivates customers to use e-wallet and digital payments and increase the perceived benefits of OFD usage.

A case study from China echos the concerns from the Dalhousie–Caddle Canadian survey, and Chinese government policy on the safety of food sold on the Internet, and ‘protecting the carrier from becoming infected’ [43]. These also have managerial implications, and logistical questions that are relevant to consider in relation to the supply chain. An OECD study notes that online delivery ‘logistics and postal services have been slowed in many countries, due to the new COVID-19 related safety guidelines and government recommendations’ [44]. OECD ‘service providers have reacted by fostering contact-less delivery options in several countries, including via parcel lockers or by replacing signatures with alternative proofs of delivery’. In terms of supply chain innovation for e-commerce, ‘in some cases, it might also be necessary to regulate how grocery stores can identify vulnerable shoppers in the context of online shopping, with current approaches often being ad-hoc and heterogeneous, such as through loyalty schemes and customer accounts.

One of the Dalhousie–Caddle survey questions addressed concern over ‘ingredient substitution’/food fraud. Lack of adequate e-commerce-specific regulations and rules highlight the need for international standards covering online marketing, differences between local consumers’ understanding of food, and the different control methods used by the competent authority [45]. Supply chains are important and relevant to food fraud, and increasing e-commerce poses considerable challenges to food control. Adaptations of current food-control systems are required to allow for effective oversight of food retail through alternative channels such as the Internet and, given the increased numbers of online traders and consumers, increased trade across borders implies a high risk of buying illegal products [46]. Therefore, e-commerce activities should focus on quality management system principles that reduce the chances of an adverse event occurring, as well as on prevention and on reducing or eliminating vulnerability.

Important in regard to e-commerce and supply chains is ‘comparing different decision models of agri-food e-supply chains, showing that the decentralized decision model is better than the centralized model from the view of quality protection’, adding that the farmers willingness to supply high-quality agri-foods increases with the increase in the consumers’ consciousness of their rights and the government’s supervision intensity [47].

There is regional variation in the degree to which people use online shopping compared to regions that do less so. In North America, this can depend on Internet access, or proximity to grocers/food service establishments. In the EU, there is big variation in online grocery use in 2018 between countries, from 37% use in the Netherlands, down to as low as 6% in Croatia [48]. Online grocers have experienced a large boost in sales during the pandemic. Spending at online grocers has increased 79%, which is the highest percentage increase in US credit and debit card data categories, higher than gaming and food delivery [49,50].

According to a case study of the largest online platform selling agri-food products in Taiwan, Ubox, factor considerations are important for supply chains, and e-commerce is important for food. For example, grain products experienced the largest surge in demand, which could be due to the storable nature of raw grain and an increase in home production of grain-based foods such as breads and bakery items. In a typical week, sales from grain increased approximately 42% due to COVID-19 [51]. The valuable lesson here is that awareness depends on the different supply chains as well, for example, comparing fruits, vegetables and grains, making an important point about supply chains and e-commerce for food retail: ‘many food retailers have in fact invested heavily in online platforms due to COVID-19 but struggle to make a profit from online sales due to the high cost of developing new systems’ [52]. This is more challenging in the Canadian context, with an oligopoly in the grocery retail sector. An increase in demand for locally grown products from small farms during COVID is an important supply chain response, and offering for the e-commerce platform.

If online food retailing during the pandemic has concentrated with the growing dominance of Amazon (and other dominant e-commerce platforms), there are concerning implications for competitiveness from smaller retailers [53]. The momentum created towards online sales dominance will likely be maintained post-pandemic [54].

Some considerations and concerns regarding implications of the COVID-19 pandemic on food shopping, the growth of online platforms, and implications for small businesses include opportunities for smaller CPGs, and food providers to by-pass large retailers directly to consumers. This has been the case with the Best of Calgary Foods out of Alberta, Canada. However, the prospects of large e-commerce platforms, such as Amazon, continue to dominate and take over the food distribution system with advanced powers of scale [55,56].

Contrastingly, ‘efforts could be made to improve the food product attributes related to the important food choice motives for consumer choices of food products in different e-commerce modes. For example, they could improve consumers’ taste impressions of food products for delivery, in-store and new retail platforms, either through advertisements claiming ‘better flavour’ or working with the owners of these platforms to produce and promote tastier food. They should improve consumer impressions of ’good value for money’ for their food products only for business-to-consumer platforms. The authors findings can also help food producers and policy-makers to target the right consumers for their products. For example, focus on female consumers when selling and promoting food products through business-to-consumer platforms and direct their efforts to male consumers for online-to-offline delivery platforms. Thirdly, helping food producers, marketers and policy-makers to sell and promote the right food products within the different e-commerce modes. For instance, they should sell and promote packaged food products through business-to-consumer platforms and fresh food products through New Retail platforms and stores’ [57].

3. Methodology

Quantitative descriptive data were collected through a cross-sectional consumer survey in Canada. Participants were the main person responsible for food purchasing in the household and a balanced age distribution was strived for. Total sample size was almost 7290 respondents (79% female, 19% male). Participants were randomly selected from the representative of the Caddle omni access panel. All contact and questionnaire administration procedures were electronic. Data collection was performed across Canada in early November 2020.

Gender distribution reflects the selection of the main person responsible for food purchasing with mostly females. Age was equally spread within age groups. The sample varies in terms of household size, income level, education level, presence of children and regional distribution in line with population census distributions in each of the provinces involved.

The master questionnaire was developed in English and translated into French using the procedure of back-translation to ensure linguistic equivalence. Following back-translation, the questionnaire was extensively pre-tested by the researchers in order to identify and eliminate potential problems. Data collection started after editing, correcting, electronic programming and additional pre-testing of the electronic version of the questionnaire.

Participants were asked to complete the structured electronic questionnaire on their own, i.e., all data were self-administered by the participants without interference from an interviewer.

4. Survey Results

The following is a descriptive analysis of the survey at large, which involved 12 questions and was also organized into 3 sub-sections of further analysis: (i) consumer price sensitivity to e-commerce for food; (ii) sustainability concerns of consumers; and (iii) loss of sensory product experience (e.g., food adulteration, safety concern) with online purchasing. Responses to all 12 questions are provided, along with responses to the 3 sub-sections as part of deeper analysis in the discussion to follow. In total, 7290 respondents completed the survey, of whom 5734 (79%) were female, and 1388 (19%) were male. Response options to each question are provided, along with a breakdown of the leading response (the most popular response by percentage from each age category). Respondents were asked to answer the 12 questions from 5 age categories, and these were as follows: (i) Greatest Generation (born between 1900 and 1945); (ii) Baby Boomers (born between 1946 and 1964); (iii) Generation X (born between 1965 and 1980); (iv) Generation Y or Millennials (born between 1981 and 1996); (v) Generation Z (born between 1997 and 2005). Survey responses where weighted more to some age groups than others. The following is the breakdown of responses by age category. In total, 23 females and 11 males responded from the ‘Greatest Generation’ category; 872 females and 241 males responded from the ‘Boomers’ category; 1979 females and 480 males responded from the ‘Generation X’ category; 2585 females and 582 males responded from the ‘Generation Y’ category; 275 females and 74 males responded from the ‘Generation Z’ category.

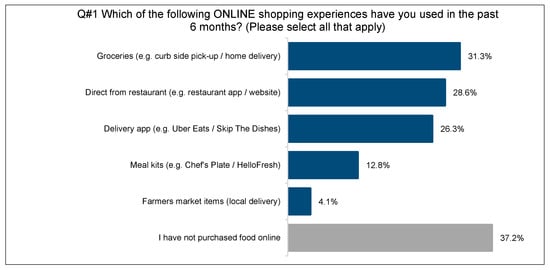

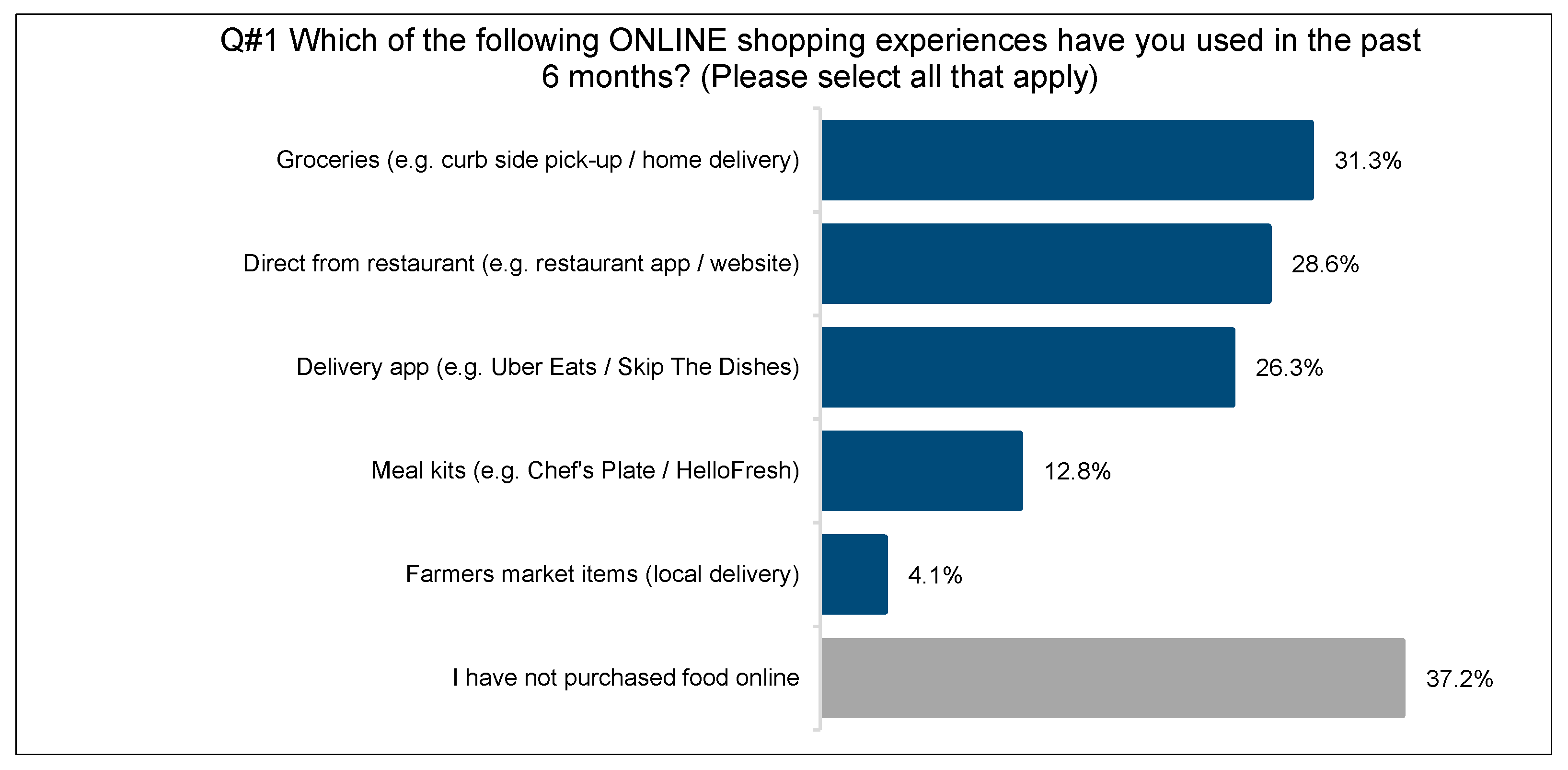

The first survey question asked, ‘Which of the following ONLINE shopping experiences have you used in the past 6 months? (Please select all that apply)’. The most popular choice was ‘I have not purchased food online’ at 37.2%, with the following in order of popular response: ‘Groceries (e.g., curb side pick-up/home delivery)’ at 31.3%, ‘Direct from restaurant (e.g., restaurant app/website)’ at 28.6%, ‘Delivery app (e.g., Uber Eats/Skip the Dishes)’ at 26.3%, ‘Meal Kits (e.g., Chef’s Plate/HelloFresh) at 12.8%, and ‘Farmers market items (local delivery) at 4.1%. From an age group perspective, 52.8% of the ‘Greatest Generation’, 57.1% of ‘Boomers’, and 39.9% of ‘Generation X’ responded with ‘I have not purchased food online’. A total of 35.3% of ‘Generation Y’ responded with ‘Groceries’, while 35.8% of ‘Generation Z’ responded with ‘Delivery app’ (See Figure 1).

Figure 1.

Online shopping experience.

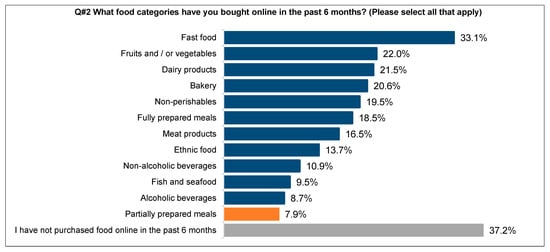

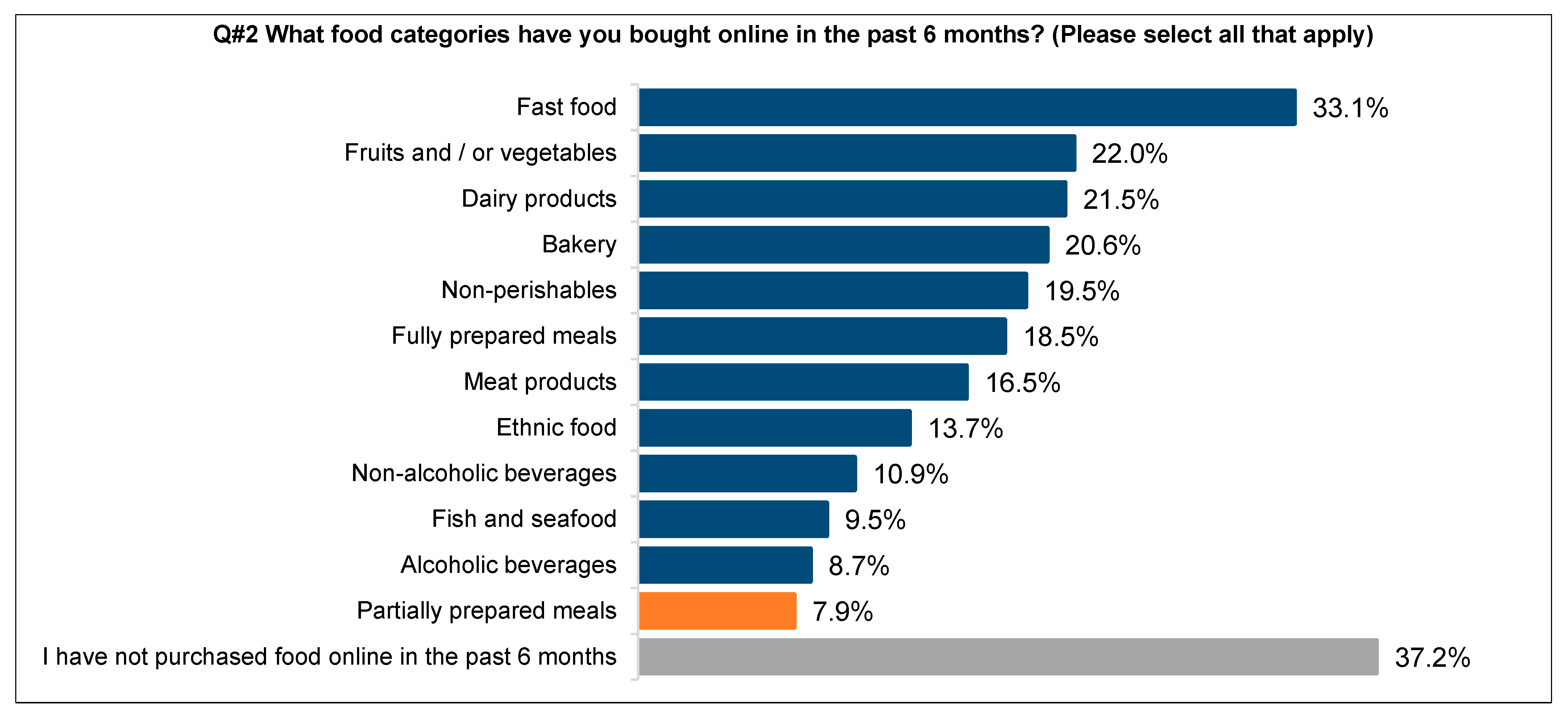

The second survey question asked, ‘What food categories have you bought online in the past 6 months? (Please select all that apply) (see Figure 2)’. The most popular choice was ‘I have not purchased food online in the past 6 months’ at 37.2%, with the following in order of popular response: ‘Fast food’ at 33.1%, ‘Fruits and/or vegetables’ at 22.0%, ‘Dairy products’ at 21.5%, ‘Bakery’ at 20.6%, ‘Non-perishables’ at 19.5%, ‘Fully prepared meals’ at 18.5%, ‘Meat products’ at 16.5%, ‘Ethnic food’ at 13.7%, ‘Non-alcoholic beverages’ at 10.9%, ‘Fish and seafood’ at 9.5%, ‘Alcoholic beverages’ at 8.7%, ‘Partially prepared meals’ at 7.9%. From an age group perspective, 52.8% of the ‘Greatest Generation’, 57.1% of ‘Boomers’, and 39.9% of ‘Generation X’ responded with ‘I have not purchased food online in the past 6 months’. A total of 39.7% of ‘Generation Y’, and 35.3% of ‘Generation Z’ responded with ‘Fast food’.

Figure 2.

Popular food categories.

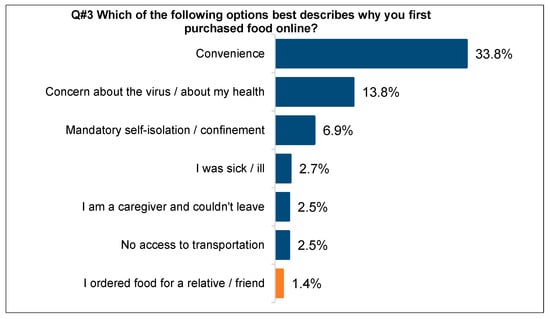

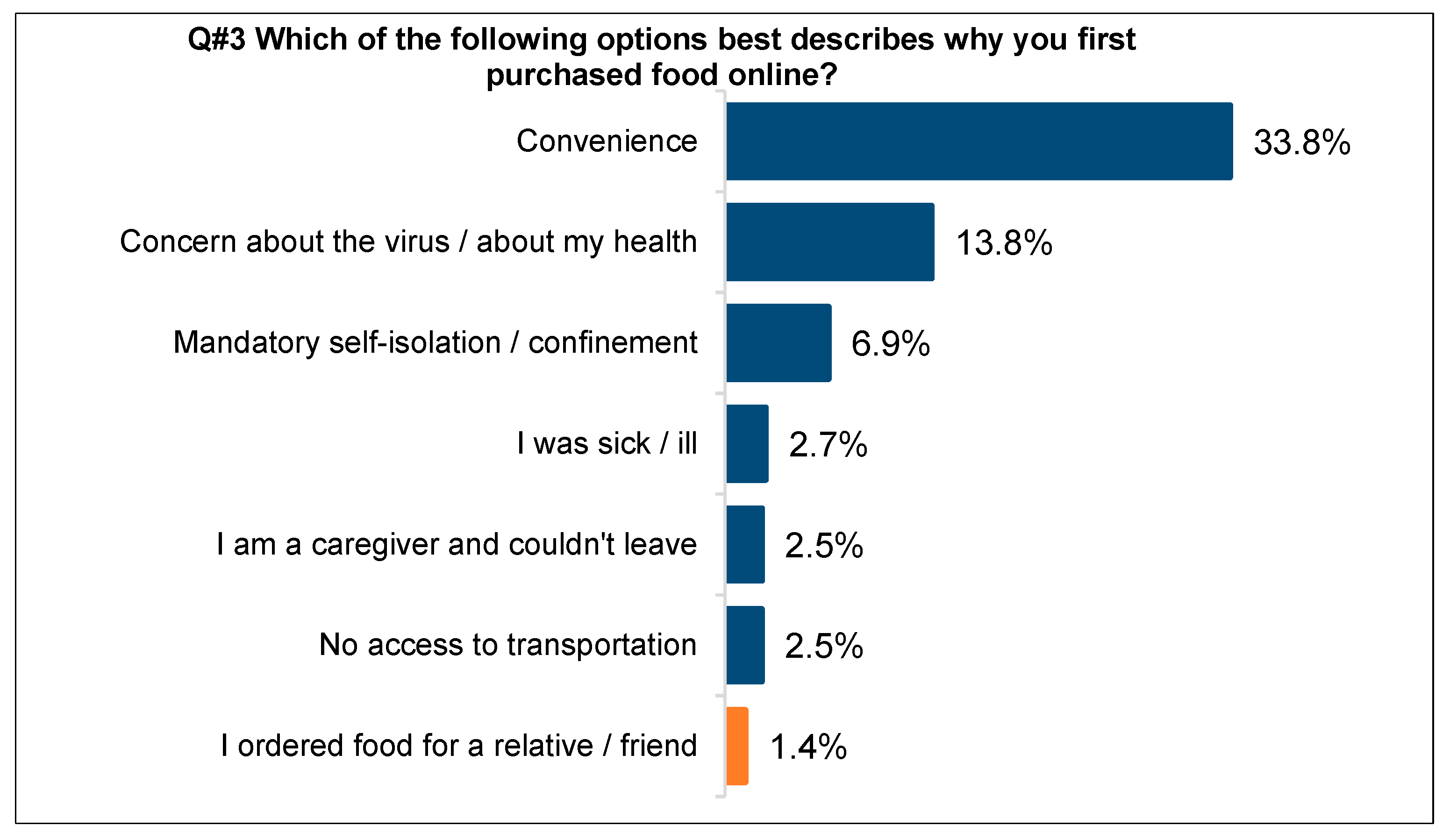

The third survey question asked, ‘Which of the following options best describes why you first purchased food online?’ (see Figure 3). The most popular choice was ‘Convenience’ at 33.8%, with the following in order of popular response: ‘Concern about the virus/about my health’ at 13.8%, ‘Mandatory self-isolation/confinement’ at 6.9%, ‘I was sick/ill’ at 2.7%, ‘I am a caregiver and couldn’t leave’ at 2.5%, ‘No access to transportation’ at 2.5%, and ‘I ordered food for a relative/friend’ at 1.4%. From an age group perspective, all groups responded that ‘convenience’ was the best description as to why they first purchased food online, with 22.2% from the ‘Greatest Generation’, 19.4% from ‘Boomers’, 31.9% from ‘Generation X’, 40.4% from ‘Generation Y’, and 35.3% from ‘Generation Z’.

Figure 3.

First purchase online.

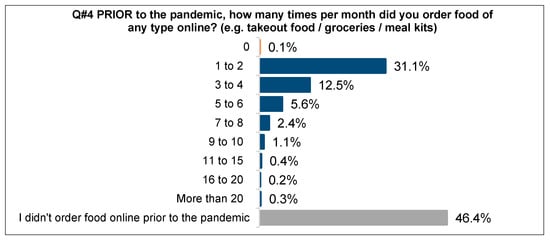

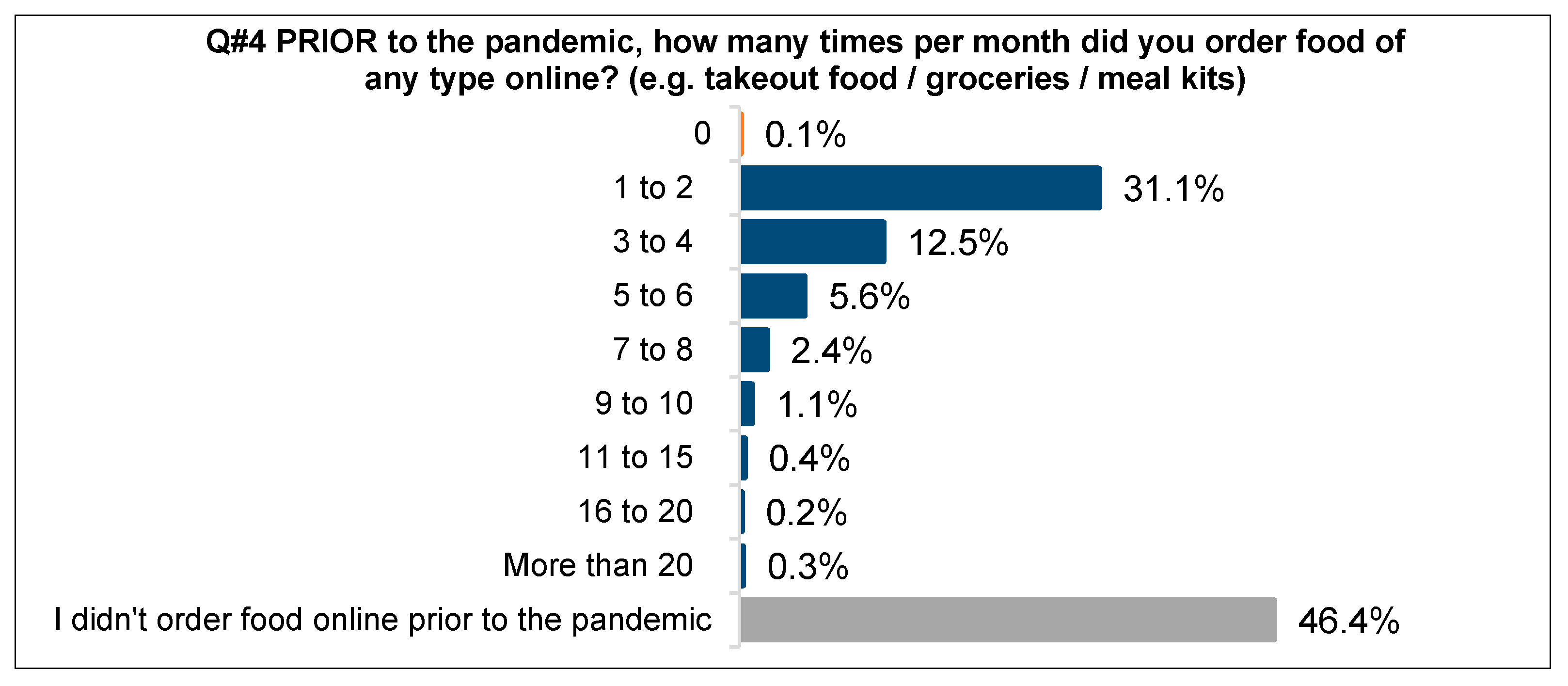

The fourth survey question asked, ‘PRIOR to the pandemic, how many times per month did you order food of any type online? (see Figure 4) (e.g., takeout food/groceries/meal kits)’. The most popular choice was ‘I didn’t order food online prior to the pandemic’ at 46.4% with the following in order of popular responses: ‘1 to 2’ at 31.1%, ‘3 to 4’ at 12.5%, ‘5 to 6’ at 5.6%, ‘7 to 8’ at 2.4%, ‘9 to 10’ at 1.1%, ‘11 to 15’ at 0.4%, and ‘More than 20’ at 0.3%. From an age group perspective, the most popular response with all age categories was ‘I didn’t order food online prior to the pandemic’. There was some variation in the age-related degree of response, with 66.7% of the ‘Greatest Generation, 67.9% of ‘Boomers’, 50.0% of ‘Generation X’, 36.9% of ‘Generation Y’, and 36.1% of ‘Generation Z’ answering this response.

Figure 4.

Online purchases before the pandemic.

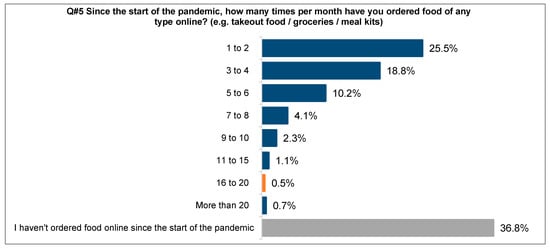

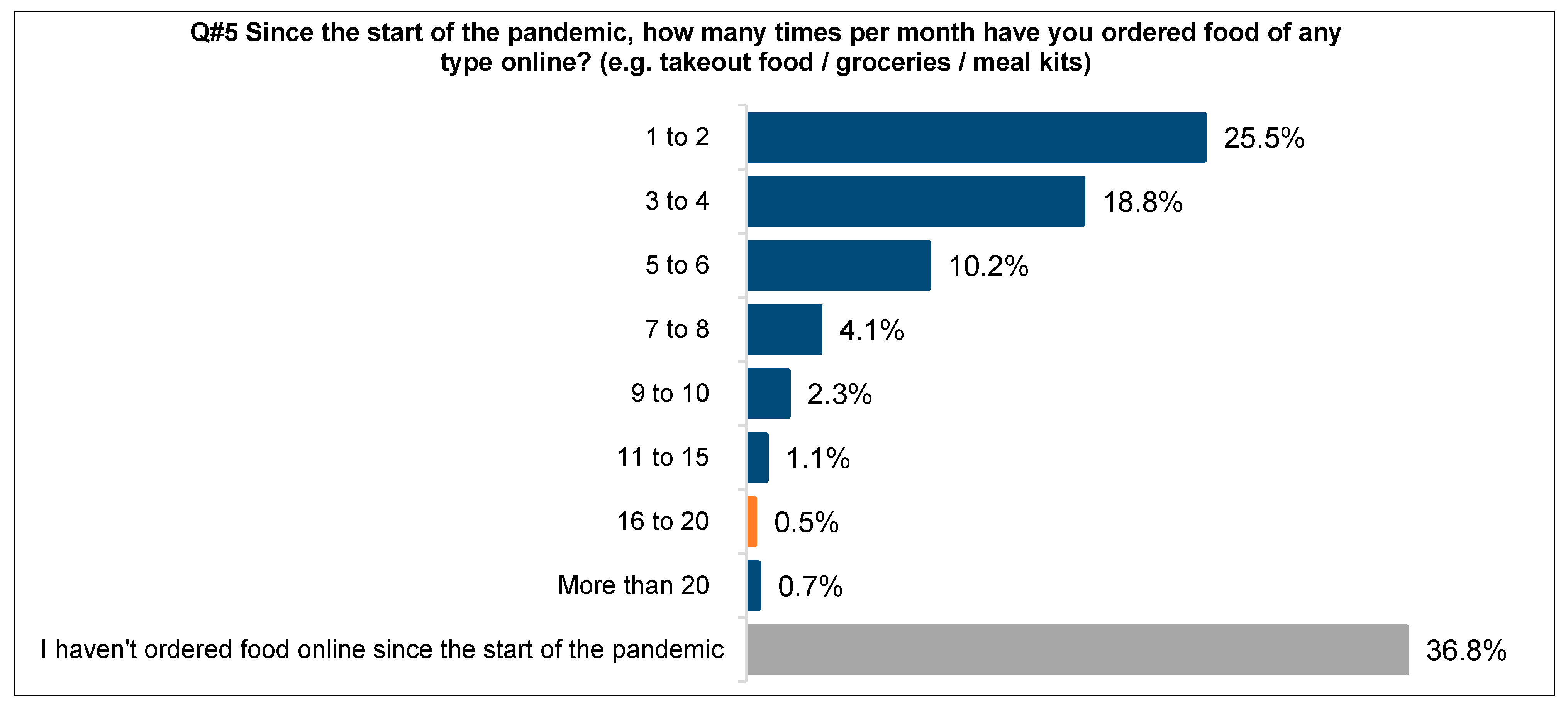

The fifth survey question asked, ‘Since the start of the pandemic, how many times per month have you ordered food of any type online? (e.g., takeout food/groceries/meal kits)’ (see Figure 5). The most popular choice was ‘I haven’t ordered food online since the start of the pandemic’ at 36.8%, with the following in order of popular responses: ‘1 to 2’ at 25.5%, ‘3 to 4’ at 18.8%, ‘5 to 6’ at 10.2%, ‘7 to 8’ at 4.1%, ‘9 to 10’ at 2.3%, ‘11 to 15’ at 1.1%, ’16 to 20’ at 0.5%, and ‘More than 20’ at 0.7%. From an age group perspective, the most popular response with all age categories was ‘I haven’t ordered food online since the start of the pandemic’. There was some variation in the age-related degree of response, with 50% of the ‘Greatest Generation’, 56.7% of ‘Boomers’, 39.7% of ‘Generation X’, 28% of ‘Generation Y’, and 32.5% of ‘Generation Z’ answering with this response.

Figure 5.

Times a month ordering food online.

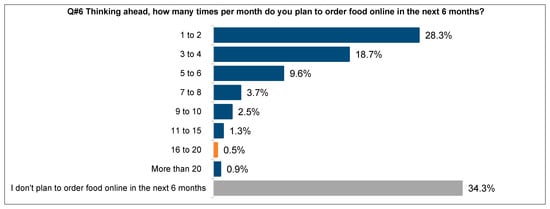

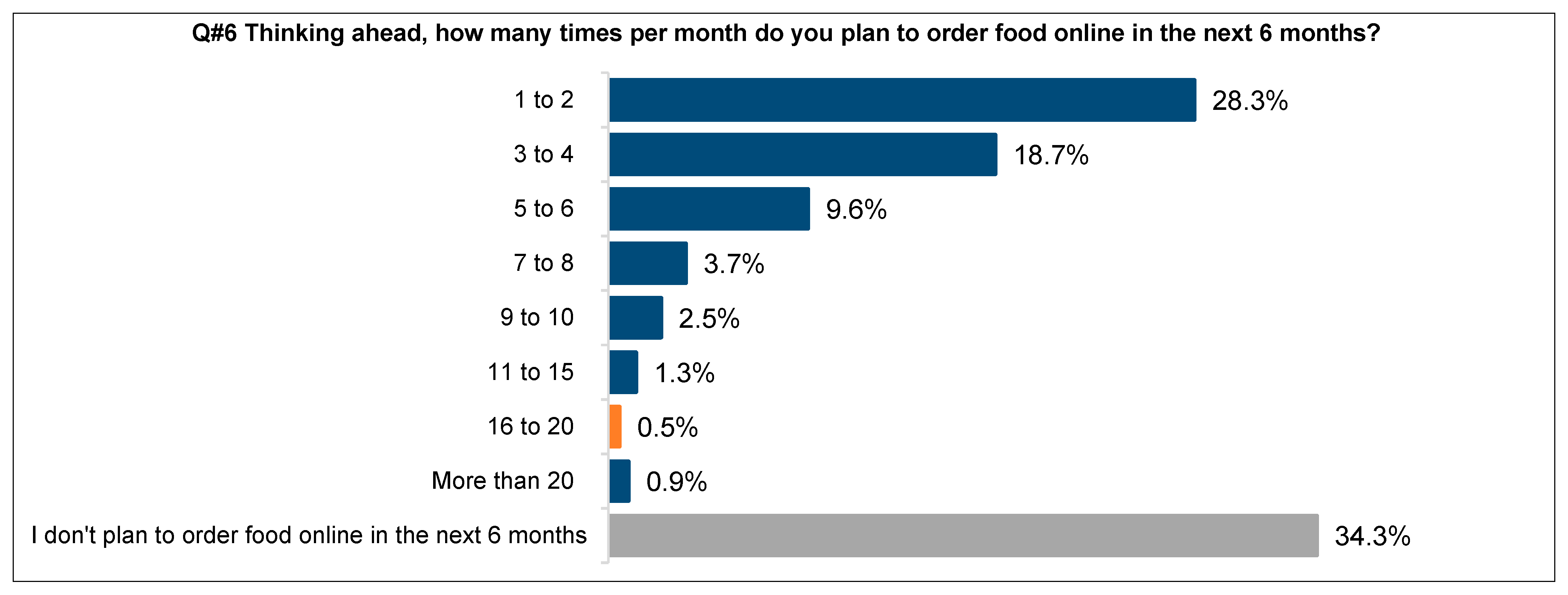

The sixth question asked, ‘Thinking ahead, how many times per month do you plan to order food online in the next 6 months?’ (see Figure 6). The most popular choice was ‘I don’t plan to order food online in the next 6 months’ at 34.3%, with the following in order of popular responses: ‘1 to 2’ at 28.3%, ‘3 to 4’ at 18.7%, ‘5 to 6’ at 9.6%, ‘7 to 8’ at 3.7%, ‘9 to 10’ at 2.5%, ’11 to 15’ at 1.3%, and ’16 to 20’ at 0.5%. From an age group perspective, the most popular response for all age categories was ‘I don’t plan to order food online in the next 6 months’ with the ‘Greatest Generation’ at 47.2%, 52.8% for ‘Boomers’, 37.5% for ‘Generation X’, and 28.9% for ‘Generation Z’. The one exceptional response was from ‘Generation Y’, where the most popular response in this age group was ‘1 to 2’ times per month where food is expected to be ordered online.

Figure 6.

Future online purchasing.

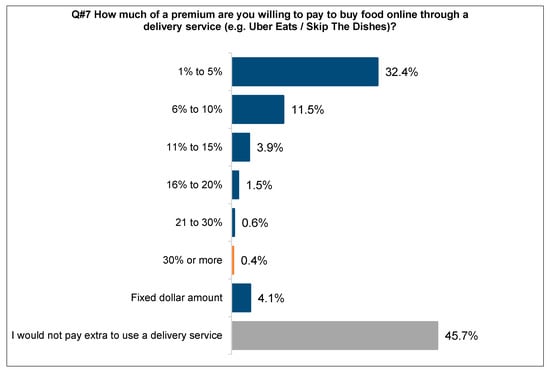

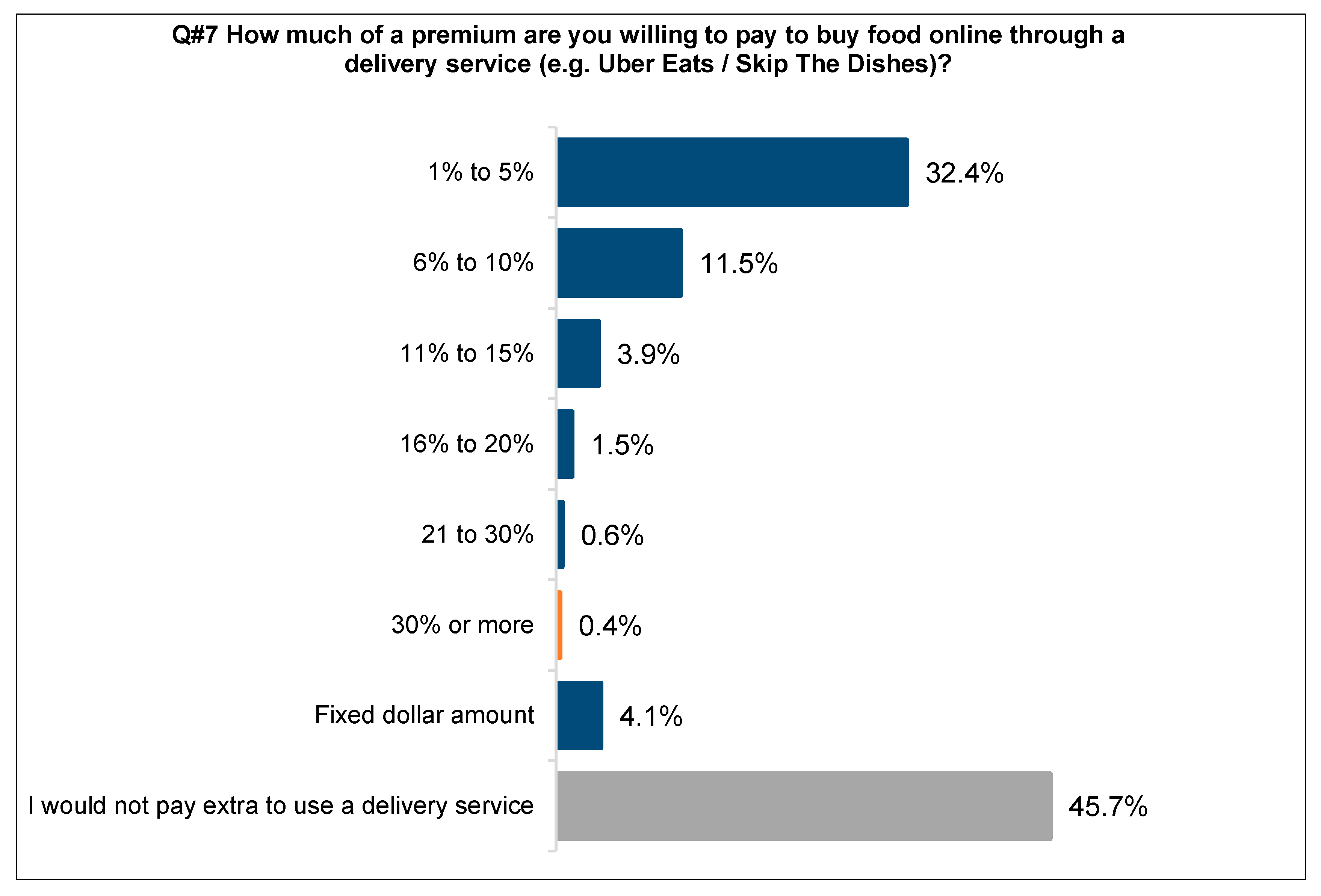

The seventh question asked ‘How much of a premium are you willing to pay to buy food online through a delivery service (e.g., Uber Eats/Skip The Dishes)?’ (see Figure 7). The most popular choice was ‘I would not pay extra to use a delivery service’ at 45.7%, with the following in order of popular responses: ‘1% to 5%’ at 32.4%, ‘6% to 10%’ at 11.5%, ‘11% to 15%’ at 3.9%, ‘16% to 20%’ at 1.5%, ‘21% to 30%’ at 0.6%, and ‘30% or more’ at 0.4%. From an age group perspective, the most popular response with all age categories was ‘I would not pay extra to use a delivery service’, with 58.3% of the ‘Greatest Generation’, 64% of ‘Boomers’, 48.7% of ‘Generation X’, 38% of ‘Generation Y’, and 34.4% of ‘Generation Z’ providing this answer.

Figure 7.

Willingness to pay a fee.

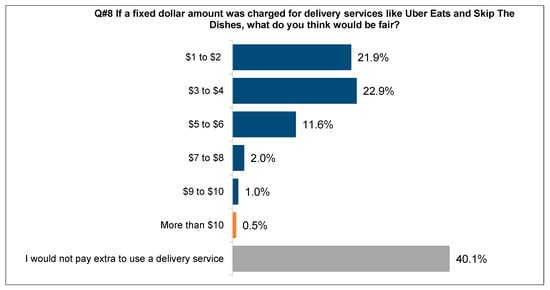

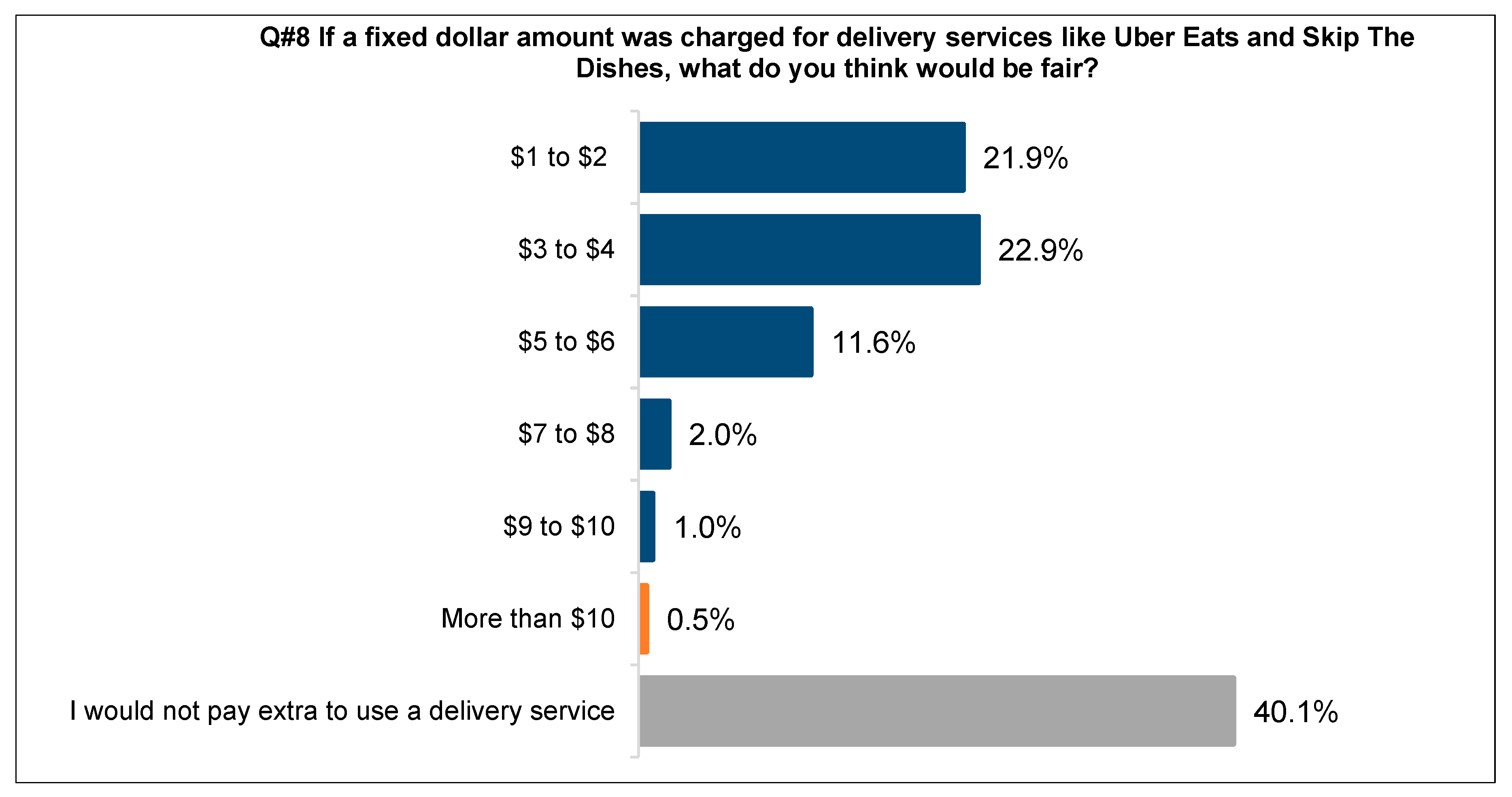

The eighth question asked ‘If a fixed dollar amount was charged for delivery services like Uber Eats and Skip The Dishes, what do you think would be fair?’ (see Figure 8). The most popular choice was ‘I would not pay extra to use a delivery service’ at 40.1%, with the following in order of popular responses: ‘$1 to $2’ at 21.9%, ‘$3 to $4’ at 22.9%, ‘$5 to $6’ at 11.6%, ‘$7 to $8’ at 2.0%, ‘$9 to $10’ at 1.0%, and ‘More than $10’ at 0.5%. From an age group perspective, the most popular response with all age categories was ‘I would not pay extra to use a deliver service’, with 52.8% of the ‘Greatest Generation’, 58.1% of ‘Boomers’, 42.9% of ‘Generation X’, 32.3% of ‘Generation Y’, and 32.8% of ‘Generation Z’ providing this answer.

Figure 8.

Fair delivery fee.

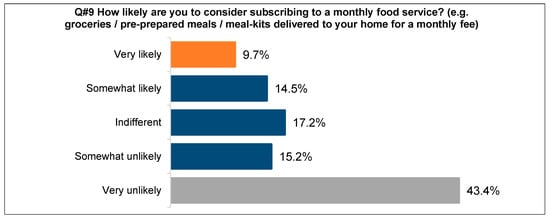

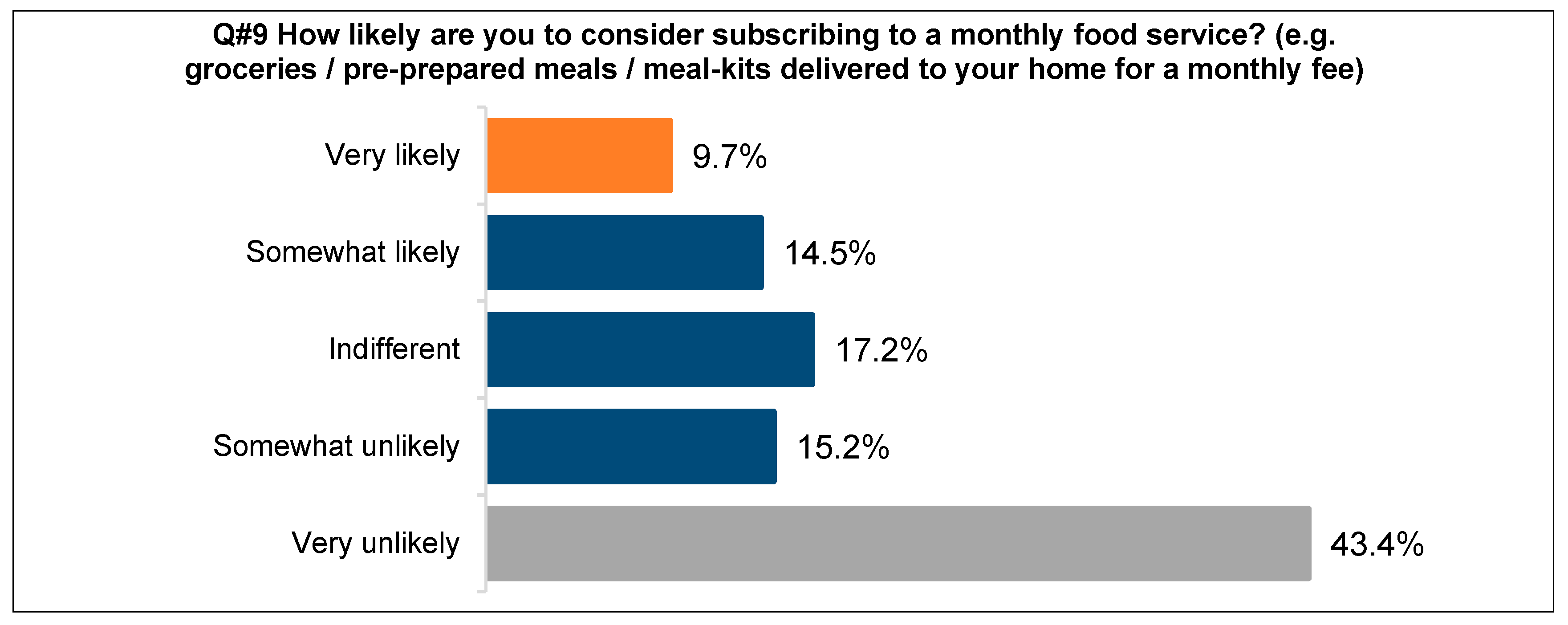

The ninth question asked, ‘How likely are you to consider subscribing to a monthly food service? (e.g., groceries/pre-prepared meals/meal-kits delivered to your home for a monthly fee) (see Figure 9)’. The most popular choice was ‘Very unlikely’ at 43.4%, with the following in order of popular responses: ‘Indifferent’ at 17.2%, ‘Somewhat unlikely’ at 15.2%, ‘Somewhat likely’ at 14.5%, and ‘Very likely’ at 9.7%. From an age group perspective, the most popular response with all age categories was ‘Very unlikely’. What is interesting is that the degree of this corresponds with age, where 69.4% of the ‘Greatest Generation’, 63.4% of ‘Boomers’, 47.5% of ‘Generation X’, 34.3% of ‘Generation Y’, and 31.7% of ‘Generation Z’ provided this answer.

Figure 9.

Wllingness to suscribe.

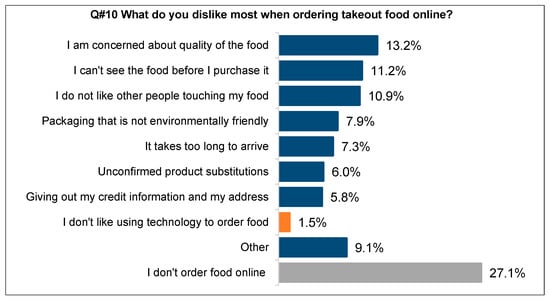

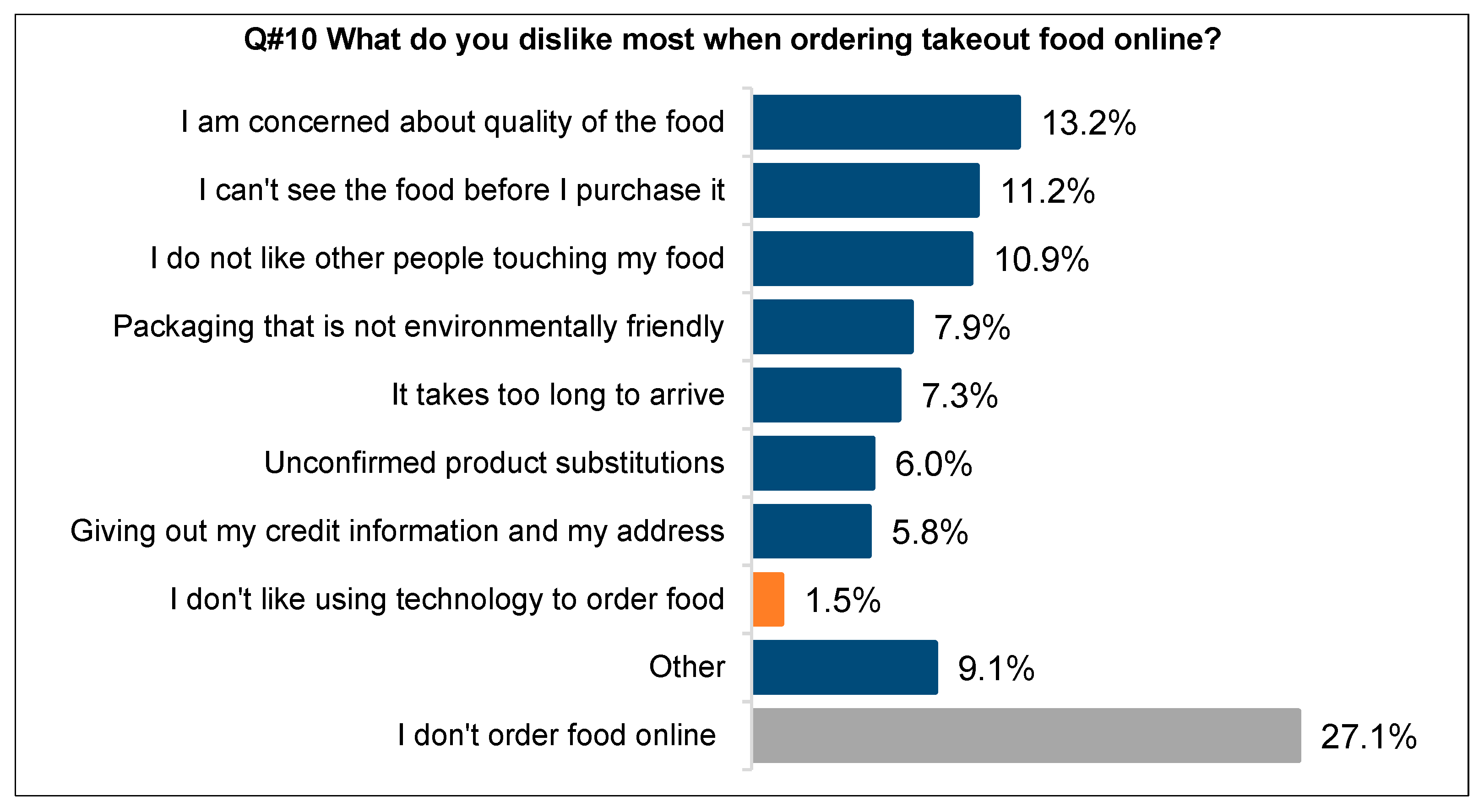

The tenth question asked, ‘What do you dislike most when ordering takeout food online?’ (see Figure 10). The most popular response was ‘I don’t order food online’ at 27.1%, with the following in order of popular responses: ‘I am concerned about the quality of the food’ at 13.2%, ‘I can’t see the food before I purchase it’ at 11.2%, ‘I do not like other people touching my food’ at 10.9%, ‘Packaging that is not environmentally friendly’ at 7.9%, ‘It takes too long to arrive’ at 7.3%, ‘Unconfirmed product substitutions’ at 6.0%, ‘Giving out my credit information and my address’ at 5.8%, and ‘I don’t like using technology to order food’ at 1.5%. From an age group perspective, the most popular response with all age categories was ‘I don’t order food online’, with 44.4% of the ‘Greatest Generation’, 45.9% of ‘Boomers’, 29% of ‘Generation X’, 19.6% of ‘Generation Y’, and 21.9% of ‘Generation Z’ providing this answer.

Figure 10.

Dislikes with ordering food online (takeout food).

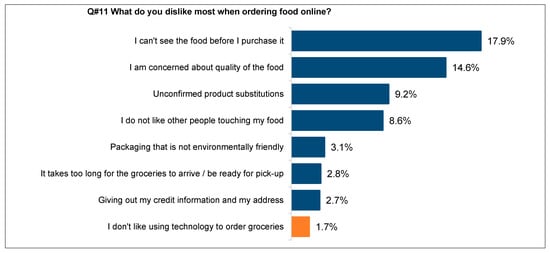

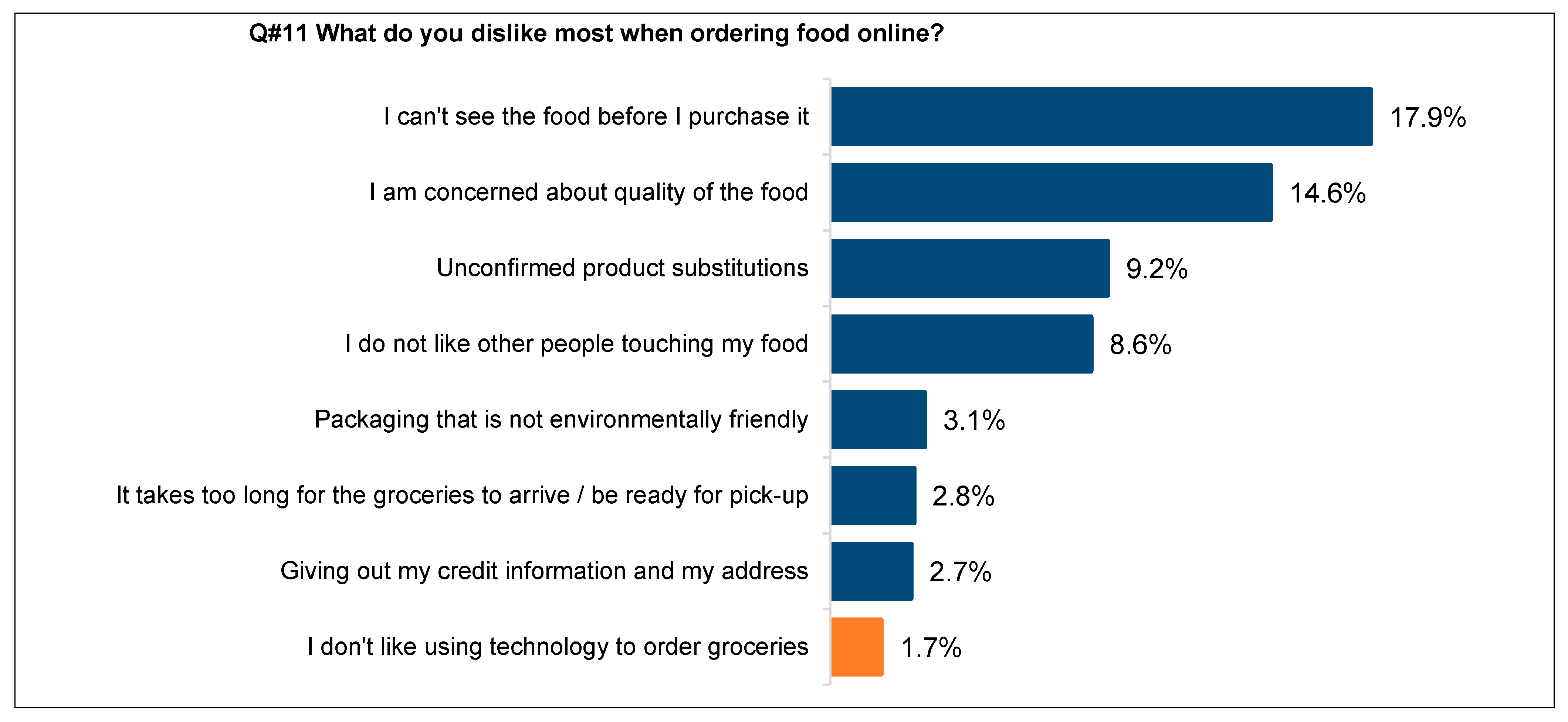

The eleventh question asked, ‘What do you dislike most when ordering food online?’ (see Figure 11). The distinction between question ten and eleven being between takeout food and groceries. The most popular response was ‘I can’t see the food before I purchase it’ at 17.9%, with the following in order of popular responses: ‘I am concerned about the quality of the food’ at 14.6%, ‘Unconfirmed product substitutions’ at 9.2%, ‘I do not like other people touching my food’ at 8.6%, ‘Packaging that is not environmentally friendly’ at 3.1%, ‘It takes too long for the groceries to arrive/be ready for pick-up’ at 2.8%, ‘Giving out my credit information and my address’ at 2.7%, and ‘I don’t like using technology to order groceries’ at 1.7%. From an age group perspective, the most popular response with all age categories was ‘I can’t see the food before I purchase it’, with 22.2% of the ‘Greatest Generation’, 14.1% of ‘Boomers’, 18.1% of ‘Generation X’, and 19.3% of ‘Generation Y’ providing this answer, with the exception of ‘Generation Z’ that answered ‘I am concerned about the quality of the food’ as the most popular answer with 16.7%.

Figure 11.

Popular food categories (groceries).

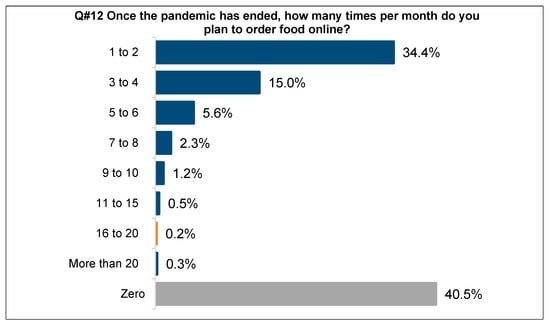

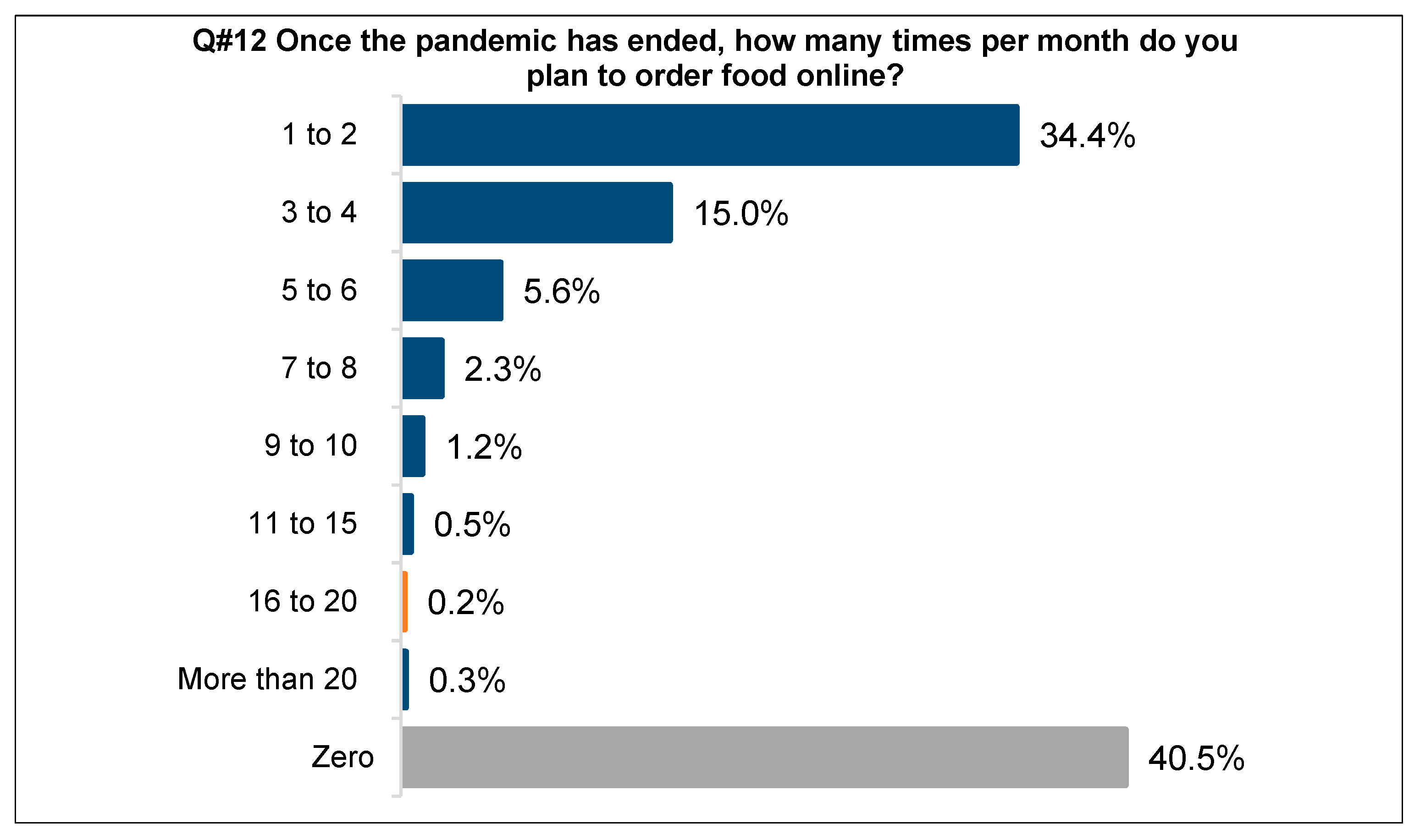

The twelfth and final question asked, ‘Once the pandemic has ended, how many times per month do you plan to order food online?’ (see Figure 12). The most popular response was ‘Zero’ at 40.5%, with the following in order of popular responses: ‘1 to 2’ at 34.4%, ‘3 to 4’ at 15%, ‘5 to 6’ at 5.6%, ‘7 to 8’ at 2.3%, ‘9 to 10’ at 1.2%, ’11 to 15’ at 0.5%, ’16 to 20’ at 0.2%, and ‘More than 20’ at 0.3%. From an age group perspective, the most popular response was somewhat divided. The ‘Greatest Generation’, ‘Boomers’, and ‘Generation X’ all indicated ‘Zero’, at 55.6%, 63.1%, and 43.6%, respectively. While the younger age groups of ‘Generation Y’ and ‘Generation Z’ responded with ‘1 to 2’ times per month in ordering food online.

Figure 12.

Intent after pandemic is over.

5. Discussion-Analysis

There are distinct patterns of responses in the survey that are worth addressing and analysing from the responses to the twelve questions as of over 7200 Canadians in November 2020. For the response to the first question, it is notable that between 40 and 60% of respondents between 40 and 60 years of age had ‘not purchased foods online during the pandemic’. This is in contrast to those under 40 years of age, where over 30% had either purchased ‘groceries’ or ‘food delivery’ online. ‘Groceries’ are also more popular than ‘direct from restaurant’ or from a ‘delivery app’. A generational openness to online shopping with a younger audience is evident from the start of the survey.

A second question determined that between 40 and nearly 60% of respondents aged over 40 ‘have not purchased a food category online during the pandemic’; however, what is in contrast to this is that, for the respondents aged under 40, between 35 and 40% had had ‘fast food’ as a leading food category which they had purchased in the past 6 months. Question three identified motivtions for purchasing food online, and ‘Convenience’ is the leading and dominant factor among all respondents from all age groups. It is interesting to observe that in the age group with the most significant number of respondents, ‘Generation Y’ or Millennials, over 40% were driven by convenience to purchase food online. It could also be argued that currently Millennial respondents are households during the pandemic with young children, between the ages of 24 and 40, and often balancing work and home life.

Question four revealed that, prior to the pandemic, nearly half (46.4%) of all respondents had not ‘ordered food online’, and about 31% had ordered a modest ‘1 to 2’ times per month. What is evident from the responses is that the under 40 respondents were again those who had ordered online food prior to the pandemic, even if again only modestly. Question five turned attention to the frequency of online food purchases, and the survey showed that ‘Boomers’ (between 55 and 75 years of age) were the most e-commerce averse, while again ‘Generation Y’ were most likely to have ordered more frequently online. Question six asked respondents to provide a forecast of how many times per month one expected to order food online, and the similar pattern of aversion from ‘Boomers’ and more openness from ‘Generation Y’ is evident from responses.

Question seven was specifically focused on determining price sensitivities amongst respondents to online food purchasing, and the aspect of willingness to pay a premium for a food delivery service. Nearly two thirds of Boomers were averse to this, while only one third of Generation Z were avese to this. From all respondents overall, the ‘1 to 5%’ premium rate resonates with the largest number of people, at 32.4% of all who answered. Question eight ask about the perceived fairness of a ‘fixed dollar amount’ being charged for a food delivery service. Interestingly, more respondents overall found ‘$3 to $4’ to be fair, rather than ‘$1 to $2’. As was a pattern among respondents, younger generations were more receptive to this than older generations. Specific to question nine, nearly 60% of all respondents were unlikely (combining ‘somewhat unlikely’ with ‘very unlikely’) to consider subscribing to a monthly food service; however, younger generations were more receptive to this.

Questions ten and eleven asked respondents to identify what categories of ordering ‘takeout food’ or ‘food’ in general they disliked. Consistent across categories and age groups is ‘concern about food quality’ and ‘not being able to see the food before purchase’ as what is disliked about online food purchasing.

In terms of sustainability concerns with the rise of e-commerce and online food purchasing, questions ten and eleven both had a category regarding dislike of ‘packaging that is not environmentally friendly’. Interestingly, 7.9% of respondents identified this with ‘ordering takeout food’, compared to 3.1% of respondents for ‘ordering food’. The distinction being that single-use plastics seem to increasingly have a negative perception among consumers, even during the pandemic, when concerns with food safety have often ensured that single-use packaging became food-service-standard industry practice. Food companies can partner with recycling companies to reduce their waste, or develop packaging products that can be reused by consumers. These types of initiatives are underway across Canada, most notably with TerraCycle and Canada’s largest grocer, Loblaws, and Canada’s largest coffee chain, Tim Hortons.

In terms of respondents’ concerns about loss of food product sensory experiences from online food purchasing, there are some common themes in the responses worth noting. The leading categories of concern for consumers, in both ‘ordering takeout food’ and ‘ordering food’ are: (i) concern over food quality; (ii) not being able to see food before purchasing it; (iii) people touching my food; and (iv) unconfirmed product substitutions. All of these elements have varied degrees of challenges for CPGs, food service companies, and retailers throughout the supply chain. Food companies can go a long way to ensuring that food quality meets consumer, freshness and safety requirements. ‘Not being able to see food before purchase’ is somewhat tricky; however, very detailed, accurate, high-resolution images can go a long way towards familiarizing consumers with foods and products they intend to purchase. Food companies can also implement systems to reduce the amount of hands that come into contact with foods, as well as cleaning systems, which can then be advertised and promoted to distinguish from competitors. In addition, food companies, whether food service, retailers or CPGs, can explicitly identify the ingredients going into their products, and have third party assurances confirming strict protocols against ingredient and product substitutions. This can gain favour among more frequent online food ordering consumers.

It is important to note here that now knowing (a) the literature on e-commerce/online buying of food service/groceries and (b) the results of a Canadian national survey on the topic, we can turn to what is the contribution from this survey to the scholarship, and importantly to the field of food product marketing. What do the results of the survey across Canada mean for supply chains? What are supply chain impact results, captured in our survey? What can supply chains do to respond? There is not, at least according to the survey, a big major growth happening in e-commerce according to respondents. However, there is a sizable core of online food purchasers, and from the survey this is namely people between the ages of 25 and 40 in Canada, Generation Y, also referred to as Millennials. This age category throughout the survey was at once more frequently using online food services, and open to innovation in the space. This generation is particularly unique in having households that are raising young children while also handling full time jobs.

Wherever in the supply chain food companies are located, their part in e-commerce needs to be strategic and responsive. Whether this is action towards sustainable packaging, reusable containers with incentives for returning to retailers and partnerships across value chains, or greater price sensitivity for consumer budgeting, or explicit food quality and safety communications, the opportunity and the need for clear and attentive e-commerce planning is especailly important. Food brands that have been able to establish some semblance of continuity during the pandemic for consumers, with consistency in delivery times, food quality, freshness, and convenience have likely earned a degree of loyalty with consumers. For smaller companies, whether they are consumer packaged goods providers, food service establishments, or restaurants with takeout options, having a clear, easy-to-navigate e-commerce platform with vivid images, product and ingredient descriptions, and operating policies, is more important than ever, especially in light of growing consumer-centric, and rapid service platforms offered by major e-commerce companies such as Amazon, and the leading grocery retailers in Canada.

6. Conclusions and Managerial Implications

How can CPG manufacturers respond with reshaping capabilities and cost structure, acting boldly to reshape their business structure, investing in their workforce and preparing for the growth of e-commerce [58]. The switching strategy (from pre- to post-COVID) depends on the challenge to meet the surge in orders and the amount of time, resources, and engineering required [59]. Questions to ask in creating a blueprint of e-commerce new reality include: What will the new e-commerce consumer care most about in the future: convenience, price, expanded assortment, speed, or something else? Which grocers and e-commerce services will be most popular with consumers and which will fade away? Where will category e-commerce penetration level off after the lockdown? How will brand loyalty be a factor in online markets? How will customer business models and requirements from CPG partners change as the e-commerce tipping point is reached, and what do CPGs need to do in order to prepare for this shift [60]?

Of the over 6000 food processing companies in Canada in 2019, 26% have less than 5 employees, 62% have between 5 and 99, 9% between 100 and 500, and only 1% have more than 500 employees [61,62]. Canada’s CPG (food processing) SMEs make up 90%. For many SMEs, with higher liquidity risk and limited working capital, the survival rate may only be counted in days or weeks [63]. Evident from recent research on the e-commerce food economy since the start of the pandemic is the rising dominance of established brands, in particular Amazon in the USA. This will have implications for Canadian CPGs and food service providers that seek to offer e-commerce platforms.

Author Contributions

Conceptualization, S.C., M.J.; methodology, S.C., M.J., J.M.; validation, S.C., M.J., J.M.; formal analysis, S.C.; investigation, M.J.; resources, J.M.; data curation, J.M.; writing—original draft preparation, S.C.; writing—review and editing, S.C.; visualization, S.C.; supervision, S.C.; project administration, M.J.; funding acquisition, J.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Caddle and Dalhousie University.

Institutional Review Board Statement

The study was conducted according to the guidelines of the Declaration of Helsinki, and approved by the Institutional Review Board (or Ethics Committee) of Dalhousie University (REB 2021-0956).

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Loblaws Companies Ltd. Live Life Well: 2020 Annual Report. 2020. Available online: https://www.loblaw.ca/en/investors-reports/ (accessed on 23 May 2021).

- Empire Company Ltd. Our Heroes: Annual Report 2020. 2020. Available online: https://www.empireco.ca/wp-content/uploads/2020/07/2020-Empire-AR-English-SEDAR.pdf (accessed on 23 May 2021).

- Metro. 2020 Annual Report. 2020. Available online: https://corpo.metro.ca/userfiles/file/PDF/Rapport-Annuel/2020/en/2020-annuel-10Q-EN-FINAL.pdf (accessed on 23 May 2021).

- Vividata. Survey of the Canadian Consumer, Vividata, Toronto. 2020. Available online: https://vividata.ca/product/survey-of-the-canadian-consumer/ (accessed on 23 May 2021).

- Nielsen, I.Q. Recalibrating for Diminished Growth: Resolutions for 2021. 14 December 2020. Available online: https://nielseniq.com/global/en/insights/analysis/2020/recalibrating-for-diminished-growth-resolutions-for-2021/ (accessed on 23 May 2021).

- Handayani, P.W.; Nurahmawati, R.A.; Pinem, A.A.; Azzahro, F. Switching Intention from Traditional to Online Groceries Using the Moderating Effect of Gender in Indonesia. J. Food Prod. Mark. 2020, 26, 425–439. [Google Scholar] [CrossRef]

- Frank, D.-A.; Peschel, A.O. Sweetening the Deal: The Ingredients that Drive Consumer Adoption of Online Grocery Shopping. J. Food Prod. Mark. 2020, 26, 1–10. [Google Scholar] [CrossRef]

- Van Droogenbroeck, E.; Van Hove, L. Adoption of Online Grocery Shopping: Personal or Household Characteristics? J. Internet Commer. 2017, 16, 255–286. [Google Scholar] [CrossRef]

- Blitstein, J.L.; Frentz, F.; Pitts, S.B.J. A Mixed-method Examination of Reported Benefits of Online Grocery Shopping in the United States and Germany: Is Health a Factor? J. Food Prod. Mark. 2020, 26, 212–224. [Google Scholar] [CrossRef]

- Hand, C.; Riley, F.D.; Harris, P.; Singh, J.; Rettie, R. Online grocery shopping: The influence of situational factors. Eur. J. Mark. 2009, 43, 1205–1219. [Google Scholar] [CrossRef]

- Lennon, S.J.; Ha, Y.; Johnson, K.K.P.; Jasper, C.R.; Damhorst, M.L.; Lyons, N. Rural Consumers’ Online Shopping for Food and Fiber Products as a Form of Outshopping. Cloth. Text. Res. J. 2008, 27, 3–30. [Google Scholar] [CrossRef] [Green Version]

- The Neilsen Group. The Future of Grocery: E-Commerce, Digit Technology, and Changing Shopping Preferences Around the World. 2015. Available online: nielsen.com/content/dam/nielsenglobal/vn/docs/Reports/2015/Nielsen%20Global%20E-Commerce%20and%20The%20New%20Retail%20Report%20APRIL%202015%20(Digital).pdf (accessed on 23 May 2021).

- Clark, L.; Wright, P. Off their trolly—understanding online grocery shopping behavior. In IFIP International Federation for Information Processing; Vankatesh, A., Gonsalves, T., Monk, A., Buckner, K., Eds.; Springer: Boston, MA, USA, 2007; pp. 157–170. [Google Scholar]

- Elms, J.; de Kervenoael, R.; Hallsworth, A. Internet or store? An ethnographic study of consumers’ internet and store-based grocery shopping practices. J. Retail. Consum. Serv. 2016, 32, 234–243. [Google Scholar] [CrossRef] [Green Version]

- Appelhans, B.M.; Lynch, E.B.; Martin, M.A.; Nackers, L.M.; Cail, V.; Woodrick, N. Feasibility and Acceptability of Internet Grocery Service in an Urban Food Desert, Chicago, 2011–2012. Prev. Chronic Dis. 2013, 10, E67. [Google Scholar] [CrossRef] [Green Version]

- Campo, K.; Breugelmans, E. Buying Groceries in Brick and Click Stores: Category Allocation Decisions and the Moderating Effect of Online Buying Experience. J. Interact. Mark. 2015, 31, 63–78. [Google Scholar] [CrossRef]

- Gorin, A.; Raynor, H.; Niemeier, H.M.; Wing, R.R. Home grocery delivery improves the household food environments of behavioral weight loss participants: Results of an 8-week pilot study. Int. J. Behav. Nutr. Phys. Act. 2007, 4, 58. [Google Scholar] [CrossRef] [Green Version]

- Huyghe, E.; Verstraeten, J.; Geuens, M.; Van Kerckhove, A. Clicks as a Healthy Alternative to Bricks: How Online Grocery Shopping Reduces Vice Purchases. J. Mark. Res. 2017, 54, 61–74. [Google Scholar] [CrossRef]

- Loketkrawee, P.; Bhatiasevi, V. Elucidating the Behavior of Consumers toward Online Grocery Shopping: The Role of Shopping Orientation. J. Internet Commer. 2018, 17, 418–445. [Google Scholar] [CrossRef]

- Dawes, J.; Nenycz-Thiel, M. Comparing retailer purchase patterns and brand metrics for in-store and online grocery purchasing. J. Mark. Manag. 2014, 30, 364–382. [Google Scholar] [CrossRef]

- Lin, J.; Li, L.; Luo, X.; Benitez, J. How do agribusinesses thrive through complexity? The pivotal role of e-commerce capability and business agility. Decis. Support Syst. 2020, 135, 113342. [Google Scholar] [CrossRef] [PubMed]

- Herrman, J. Amazon’s Big Breakdown. 2020. Available online: nytimes.com/interactive/2020/05/27/magazine/amazon-coronavirus.html (accessed on 23 May 2021).

- Schoolov, K. As Amazon Orders Surge, Coronavirus Delays Deliveries and Threatens to Put Sellers out of Business. 2020. Available online: cnbc.com/2020/03/20/coronavirus-delays-amazon-orders-and-could-put-sellers-out-of-business.html (accessed on 23 May 2021).

- Daniels, J. Online Grocery Sales Set to Surge, Grabbing 20 Percent of Market by 2025, CNBC. 2017. Available online: https://www.cnbc.com/2017/01/30/online-grocery-sales-set-surgegrabbing-20-percent-of-market-by-2025.html (accessed on 23 May 2021).

- Chenarides, L.; Grebitus, C.; Lusk, J.L.; Printezis, I. Food consumption behavior during the COVID-19 pandemic. Agribusiness 2021, 37, 44–81. [Google Scholar] [CrossRef] [PubMed]

- Mullins, L.; Charlebois, S.; Finch, E.; Music, J. Home Food Gardening in Canada in Response to the COVID-19 Pandemic. Sustainability 2021, 13, 3056. [Google Scholar] [CrossRef]

- Van Droogenbroeck, E.; Van Hove, L. Triggered or evaluated? A qualitative inquiry into the decision to start using e-grocery services. Int. Rev. Retail. Distrib. Consum. Res. 2019, 30, 103–122. [Google Scholar] [CrossRef]

- Hillen, J. Online food prices during the COVID-19 pandemic. Agribusiness 2021, 37, 91–107. [Google Scholar] [CrossRef]

- Tou, Y.; Watanabe, C.; Moriya, K.; Naveed, N.; Vurpillat, V.; Neittaanmäki, P. The transformation of R&D into neo open innovation- a new concept in R&D endeavor triggered by amazon. Technol. Soc. 2019, 58, 101141. [Google Scholar] [CrossRef]

- Aversa, P.; Haefliger, S.; Reza, D.G. How to assess the value of a business model portfolio? MIT Sloan Manag. Rev. 2017, 58, 49–54. Available online: http://openaccess.city.ac.uk/16947/ (accessed on 23 May 2021).

- Charlebois, S.; Music, J.; Faires, S. The Impact of COVID-19 on Canada’s Food Literacy: Results of a Cross-National Survey. Int. J. Environ. Res. Public Health 2021, 18, 5485. [Google Scholar] [CrossRef] [PubMed]

- Byington, L.; Doering, C.; Poinski, M. 5 Trends Fueling Food and Beverage Innovation in 2021, FoodDive. 2021. Available online: https://www.fooddive.com/news/5-trends-fueling-food-and-beverage-innovation-in-2021/592588/ (accessed on 23 May 2021).

- Ellison, B.; McFadden, B.; Rickard, B.J.; Wilson, N.L.W. Examining Food Purchase Behavior and Food Values During the COVID -19 Pandemic. Appl. Econ. Perspect. Policy 2021, 43, 58–72. [Google Scholar] [CrossRef]

- Cranfield, J.A.L. Framing consumer food demand responses in a viral pandemic. Can. J. Agric. Econ. Can. d’Agroecon. 2020, 68, 151–156. [Google Scholar] [CrossRef]

- Lusk, J.L.; Briggeman, B.C. Food Values. Am. J. Agric. Econ. 2009, 91, 184–196. [Google Scholar] [CrossRef]

- Roe, B.E.; Bender, K.; Qi, D. The Impact of COVID-19 on Consumer Food Waste. Appl. Econ. Perspect. Policy 2021, 43, 401–411. [Google Scholar] [CrossRef]

- Gorrasi, G.; Sorrentino, A.; Lichtfouse, E. Back to plastic pollution in COVID times. Environ. Chem. Lett. 2021, 19, 1–4. [Google Scholar] [CrossRef] [PubMed]

- Silva, A.L.P.; Prata, J.C.; Walker, T.R.; Duarte, A.C.; Ouyang, W.; Barcelò, D.; Rocha-Santos, T. Increased plastic pollution due to COVID-19 pandemic: Challenges and recommendations. Chem. Eng. J. 2021, 405, 126683. [Google Scholar] [CrossRef]

- Tran, L.T.T. Managing the effectiveness of e-commerce platforms in a pandemic. J. Retail. Consum. Serv. 2021, 58, 102287. [Google Scholar] [CrossRef]

- Charlebois, S.; Chamberlain, S.; Herian, A. Pre-shopping habits and consumer vulnerability in food retailing. J. Food Res. 2018, 7, 24–35. [Google Scholar] [CrossRef]

- Mehrolia, S.; Alagarsamy, S.; Solaikutty, V.M. Customers response to online food delivery services during COVID-19 outbreak using binary logistic regression. Int. J. Consum. Stud. 2021, 45, 396–408. [Google Scholar] [CrossRef]

- Nguyen, T.H.D.; Vu, D.C. Food Delivery Service During Social Distancing: Proactively Preventing or Potentially Spreading Coronavirus Disease–2019? Disaster Med. Public Health Prep. 2020, 14, e9–e10. [Google Scholar] [CrossRef]

- Gao, X.; Shi, X.; Guo, H.; Liu, Y. To buy or not buy food online: The impact of the COVID-19 epidemic on the adoption of e-commerce in China. PLoS ONE 2020, 15, e0237900. [Google Scholar] [CrossRef]

- OECD. Tackling Coronavirus (COVID-19): Contributing to a Global Effort—E-Commerce in the Times of COVID-19; OECD: Paris, France, 2020; pp. 1–10. Available online: oecd.org/coronavirus (accessed on 23 May 2021).

- Pinto, A.; Mottola, A.; Marchetti, P.; Savarino, A.; Tantillo, G. Fraudulent species substitution in e-commerce of protected denomination origin (pdo) products. J. Food Compos. Anal. 2019, 79, 143–147. [Google Scholar] [CrossRef]

- Food Chain Evaluation Consortium (FCEC). Delivering on EU Food Safety and Nutrition in 2050—Scenarios of Future Change and Policy Responses: Final Report DG SANCO. 2013. Available online: forum-synergies.eu/docs/fcec_dg_sanco_scoping_study_eu_food_safety_nutrition_2050_-_final_repo....pdf (accessed on 23 May 2021).

- Jing, X.; Guanxin, Y.; Panqian, D. Quality Decision-Making Behavior of Bodies Participating in the Agri-Foods E-Supply Chain. Sustainability 2020, 12, 1874. [Google Scholar] [CrossRef] [Green Version]

- Charlebois, S.; Somogyi, S.; Music, J.; Caron, I. Planet, Ethics, Health and the New World Order in Proteins. J. Agric. Stud. 2020, 8, 171–192. [Google Scholar] [CrossRef]

- Music, J.; Finch, E.; Gone, P.; Toze, S.; Charlebois, S.; Mullins, L. Pandemic Victory Gardens: Potential for local land use policies. Land Use Policy 2021, 109, 105600. [Google Scholar] [CrossRef]

- Leatherby, L.; Gelles, D. How the Virus Transformed the Way Americans Spend Their Money. The New York Times. 11 April 2020. Available online: nytimes.com/interactive/2020/04/11/business/economy/coronavirus-us-economy-spending.html (accessed on 23 May 2021).

- Chang, H.; Meyerhoefer, C.D. COVID-19 and the Demand for Online Food Shopping Services: Empirical Evidence from Taiwan. Am. J. Agric. Econ. 2021, 103, 448–465. [Google Scholar] [CrossRef]

- Eley, J.; McMorrow, R. Why Supermarkets Are Struggling to Profit from the Online Grocery Boom. Financial Times. 22 July 2020. Available online: ft.com/content/b985249c-1ca1-41a8-96b5-0adcc889d57d (accessed on 23 May 2021).

- Leone, L.A.; Fleischhacker, S.; Anderson-Steeves, B.; Harper, K.; Winkler, M.; Racine, E.; Baquero, B.; Gittelsohn, J. Healthy Food Retail during the COVID-19 Pandemic: Challenges and Future Directions. Int. J. Environ. Res. Public Health 2020, 17, 7397. [Google Scholar] [CrossRef]

- Goddard, E. The impact of COVID-19 on food retail and food service in Canada: Preliminary assessment. Can. J. Agric. Econ. Can. d’Agroecon. 2020, 68, 157–161. [Google Scholar] [CrossRef]

- Oncini, F.; Bozzini, E.; Forno, F.; Magnani, N. Towards food platforms? An analysis of online food provisioning services in Italy. Geoforum 2020, 114, 172–180. [Google Scholar] [CrossRef]

- Rushe, D.; Sainato, M. Amazon posts 75bn first-quarter revenues but expects to spend 4bn in Covid-19 costs. Guardian 2020, 30, 4. [Google Scholar]

- Wang, O.; Somogyi, S.; Charlebois, S. Food choice in the e-commerce era. Br. Food J. 2020, 122, 1215–1237. [Google Scholar] [CrossRef]

- PwC. Canadian Consumer Insights 2020: Accelerating Shifts Driving a Radical Rethink of the Customer Journey, PwC Canada. 2020. Available online: https://www.pwc.com/ca/en/industries/retail-consumer/consumer-insights-2020.html (accessed on 23 May 2021).

- Hailu, G. Economic thoughts on COVID-19 for Canadian food processors. Can. J. Agric. Econ. 2020, 68, 163–169. [Google Scholar] [CrossRef]

- Boston Consulting Group. CPG Companies Face an E-Commerce Tsunami, Boston Consulting Group. 2020. Available online: https://www.bcg.com/publications/2020/cpg-companies-face-increased-e-commerce (accessed on 23 May 2021).

- Government of Canada, Summary-Canadian Industry Statistics. 2020. Available online: https://www.ic.gc.ca/app/scr/app/cis/summary-sommaire/311 (accessed on 23 May 2021).

- Government of Canada, Key Small Business Statistics—January 2019. 2020. Available online: https://www.ic.gc.ca/eic/site/061.nsf/eng/h_03090.html (accessed on 23 May 2021).

- Charlebois, S. Why COVID-10 Will Change Canadian Grocery Industry Forever? Retail Insider E-News, 26 March 2020. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).