Financial Risk Management Based on Corporate Social Responsibility in the Interests of Sustainable Development

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

- −

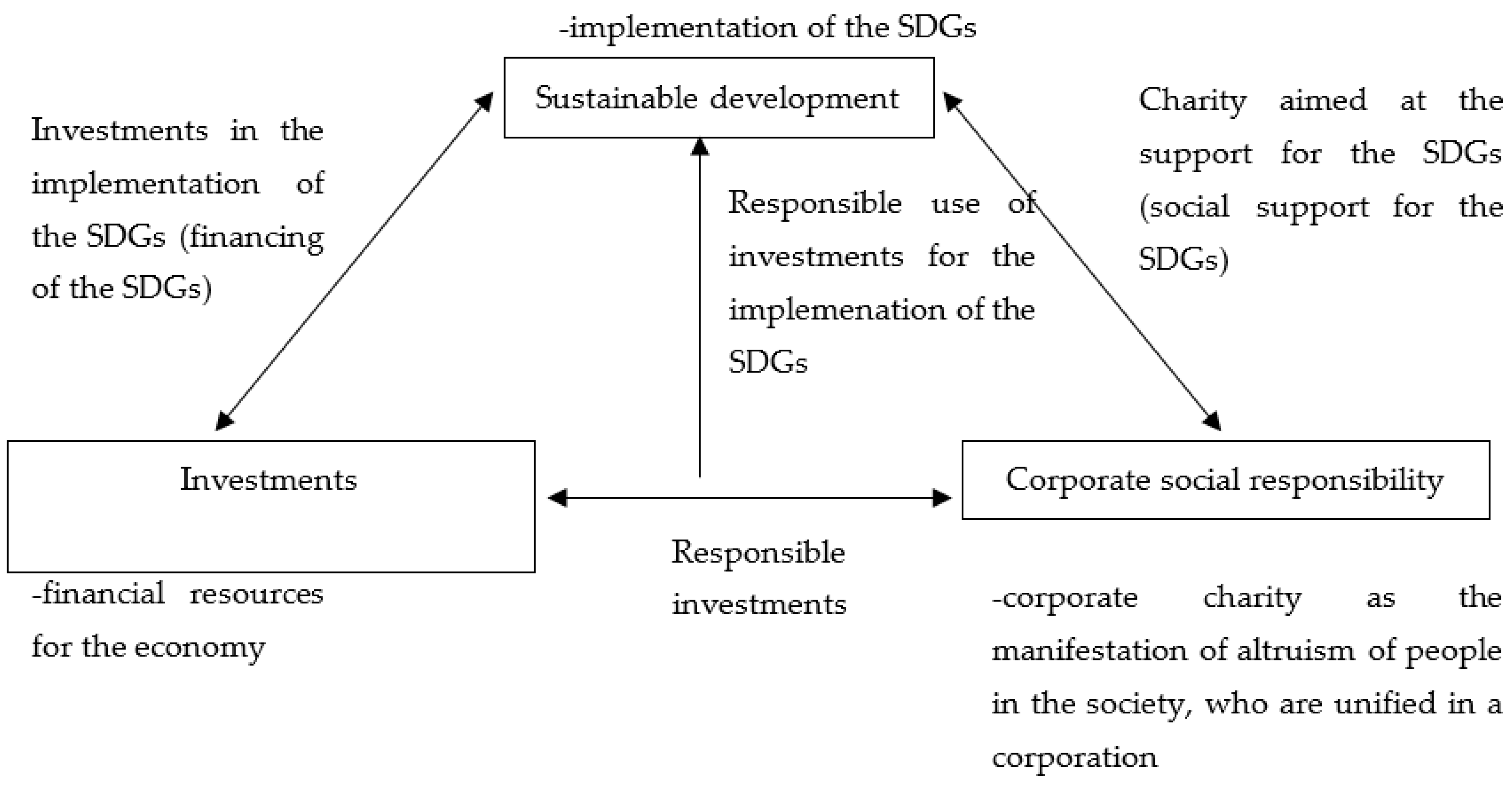

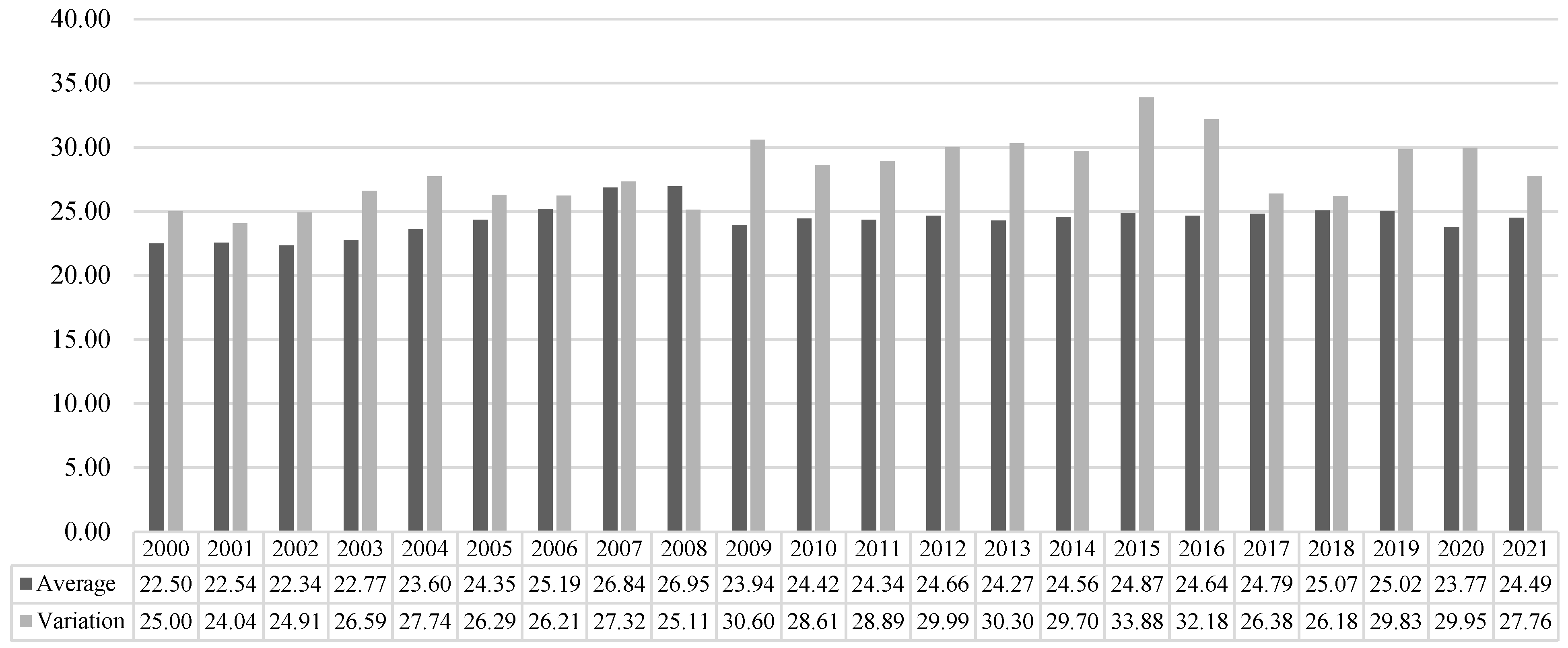

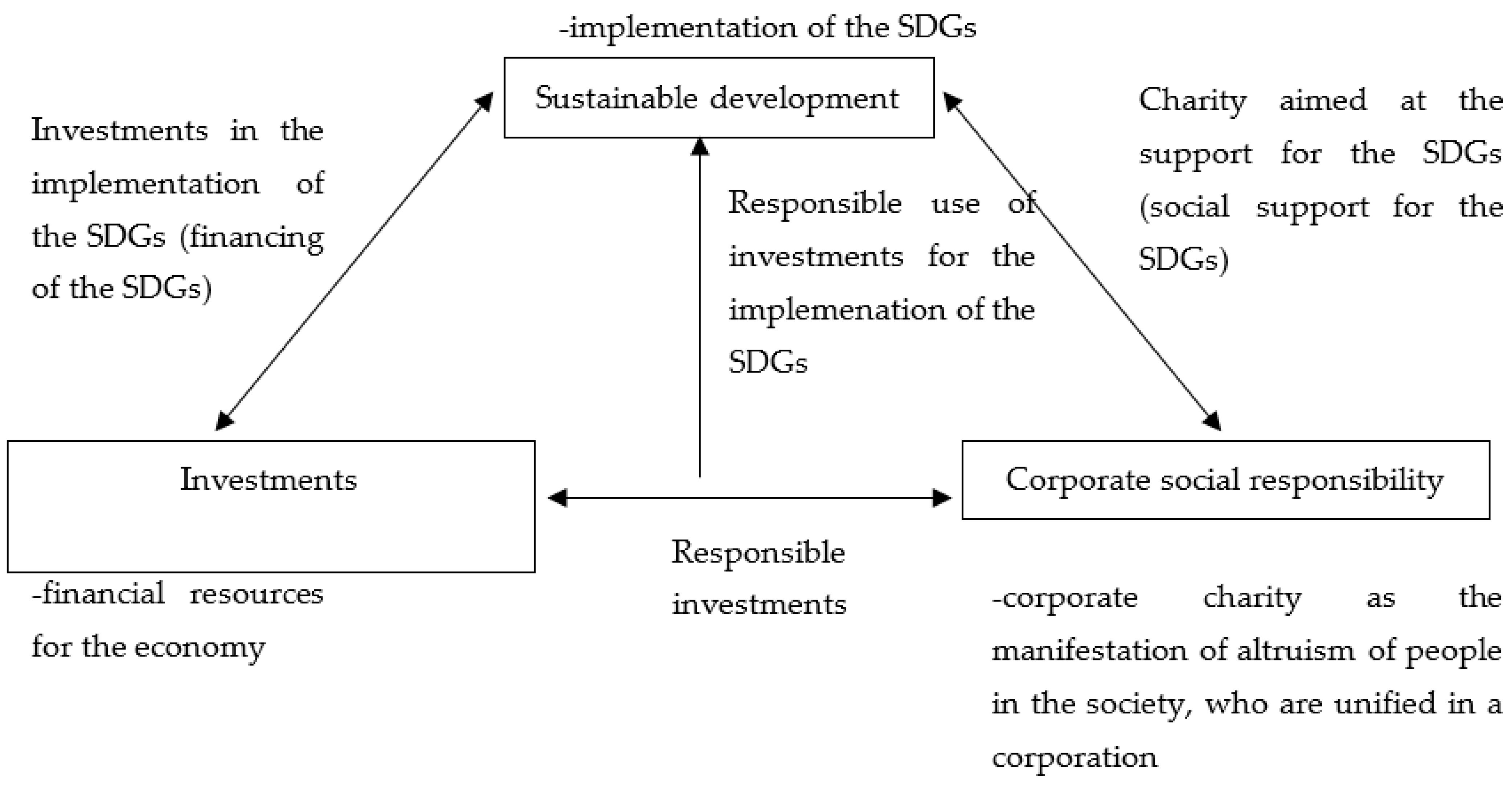

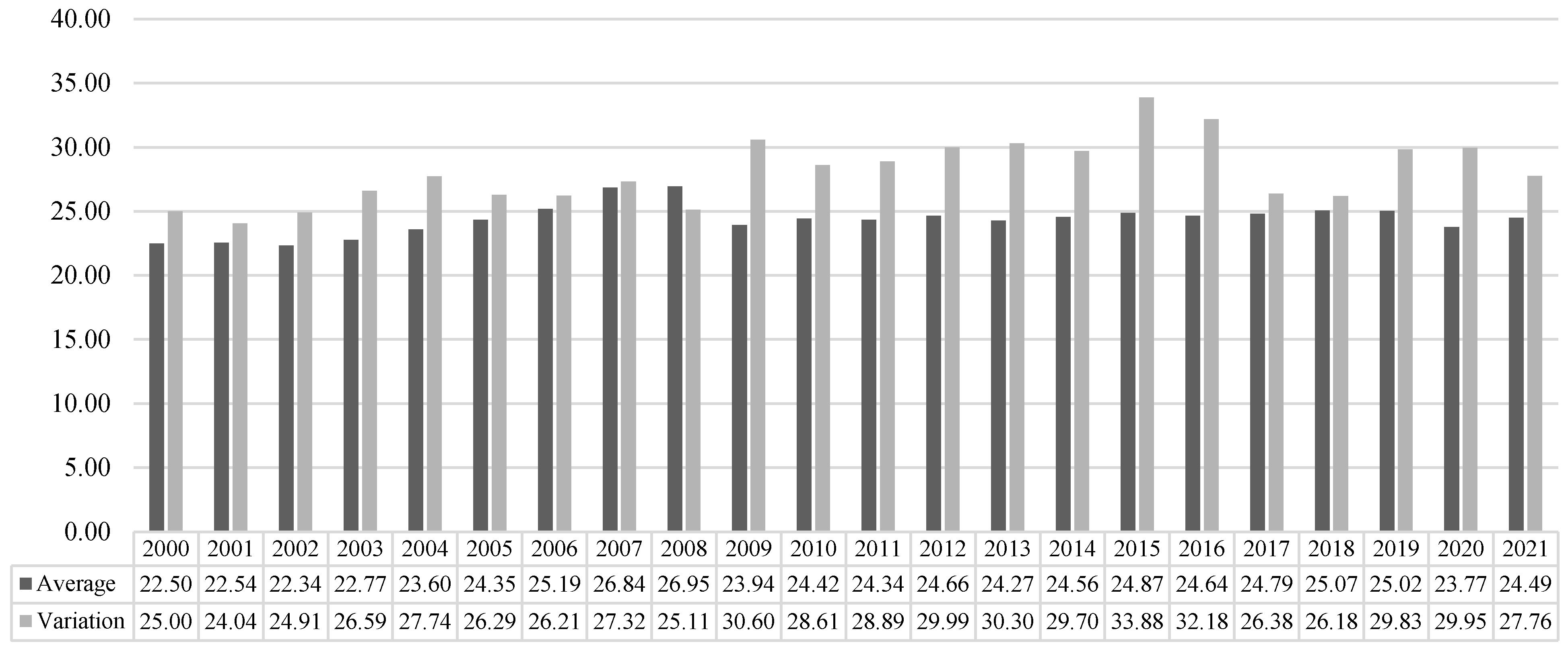

- Total investment, calculated by the International Monetary Fund (2021), which characterizes the availability of financial resources in the economy (we shall denote it as fr);

- −

- World giving index, calculated by Charities Aid Foundation (2021), which characterizes the level of corporate social responsibility (we shall denote it as cr);

- −

4. Results and Discussion

- −

- The analysis of multiple correlations has shown that the multiple correlation coefficient (R2) took the value 0.3745. This is a sign of the moderate connection between the indicators: the change of the sustainable development index by 37.45% is explained by the change of total investments in the economy and the world giving index (corporate social responsibility);

- −

- Variables multicollinearity test allowed obtaining the following results. Cross-correlation between the sustainable development index and total investments rsd,fr = −0.16. Cross-correlation between the sustainable development index and the world giving index rsd,cr = −0.35. Cross-correlation between the world giving index and total investments rcr,ft = 0.12. Therefore, multicollinear (duplicative) variables are absent;

- −

- F-test allowed obtaining the following results. At 105 observations in the sample and 2-factor variables (k1 = 2, k2 = 104 − 3 = 101), the table value F = 3.09. The observed value F = 8.32, i.e., it exceeds the table value (the test is passed);

- −

- The Student’s t-test allowed obtaining the following results. At the significance level df = 104, the table value F = 1.982. The observed value F = 20.65, i.e., it exceeds the table value (the test is passed).

- −

- Provision of tax preferences (e.g., tax subsidies or tax vacations) for the subjects of entrepreneurship, which are recipients of responsible investments;

- −

- Provision of attractive conditions for the inflow of responsible investments in the economy—e.g., based on special economic zones;

- −

- Setting requirements to the placement of responsible investments by private parties of the implemented and started projects of public-private partnership;

- −

- Compilation and publication in open access of the national ranking of responsible investors and responsible companies, which attract the largest total investments and use them with the largest contribution to the implementation of the SDGs.

- −

- absence of the necessity for the special attraction of investments in the economy amid a crisis;

- −

- the complicated structure of investments in the economy, in which responsible (and opposite—irresponsible) investments are distinguished.

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Adachi-Sato, Meg, and Chaiporn Vithessonthi. 2021. Bank risk-taking and corporate investment: Evidence from the Global Financial Crisis of 2007–2009. Global Finance Journal 49: 100573. [Google Scholar] [CrossRef]

- Ahmad, Munir, Abbas Ali Chandio, Yasir Ahmed Solangi, Syed Ahsan Ali Shah, Farrukh Shahzad, Abdul Rehman, and Gul Jabeen. 2021. Dynamic interactive links among sustainable energy investment, air pollution, and sustainable development in regional China. Environmental Science and Pollution Research 28: 1502–18. [Google Scholar] [CrossRef] [PubMed]

- Alshater, Muneer, Osama Atayah, and Allam Hamdan. 2021. Journal of Sustainable Finance and Investment: A bibliometric analysis. Journal of Sustainable Finance and Investment, 1–22. [Google Scholar] [CrossRef]

- Anderson, Carl, M. Denich, Manfred Warchold, J. Jürgen Kropp, and Pradhan Pradhan. 2021. A systems model of SDG target influence on the 2030 Agenda for Sustainable Development. Sustainability Science, 1–14. [Google Scholar] [CrossRef]

- Anis, Alan, Noonu Mary Jose, and Tess Jacob. 2019. Achieving sustainable development goals (Sdg’s) through Csr activities—A study on hindustan petroleum corporation limited (Hpcl) a major Navaratna company. Journal of Advanced Research in Dynamical and Control Systems 11: 844–50. [Google Scholar]

- Brundtland, Gro. 1987. Our Common Future. Report of the World Commission on Environment and Development. Available online: https://www.un.org/ru/ga/pdf/brundtland.pdf (accessed on 1 December 2021).

- Brzeszczyński, Janusz, Jerzy Gajdka, and Tomasz Schabek. 2021. How risky are the socially responsible investment (SRI) stocks? Evidence from the Central and Eastern European (CEE) companies. Finance Research Letters 42: 101939. [Google Scholar] [CrossRef]

- Buhmann, Karin, Jonas Jonsson, and Mette Fisker. 2019. Do no harm and do more good too: Connecting the SDGs with business and human rights and political CSR theory. Corporate Governance 19: 389–403. [Google Scholar] [CrossRef] [Green Version]

- Çamlibel, Mehmet Emre, Levent Sümer, and Ali Hepşen. 2021. Risk-return performances of real estate investment funds in turkey including the COVID-19 period. International Journal of Strategic Property Management 25: 267–77. [Google Scholar] [CrossRef]

- Castillo-Villar, Rosalia. 2020. Identifying determinants of CSR implementation on SDG 17 partnerships for the goals. Cogent Business and Management 7: 1847989. [Google Scholar] [CrossRef]

- Charities Aid Foundation. 2021. World Giving Index 2021: A Global Pandemic Special Report. Available online: https://www.sdgphilanthropy.org/system/files/2021-06/cafworldgivingindex2021_report_web2_100621.pdf (accessed on 1 December 2021).

- Choi, Bu-Kyung, Ji-Young Ahn, and Myeong-Cheol Choi. 2021. Corporate social responsibility, CEO compensation structure, and corporate innovation activities. Sustainability 13: 13039. [Google Scholar] [CrossRef]

- Costa, Antonio, Alessandra Tafuro, Marco Benvenuto, and Carmine Viola. 2021. Corporate Social Responsibility through SDGs: Preliminary Results from a Pilot Study in Italian Universities. Administrative Sciences 11: 117. [Google Scholar] [CrossRef]

- de SouzaCunha, Felipe Arias Fogliano, Erick Meira, and Renato Orsato. 2021. Sustainable finance and investment: Review and research agenda. Business Strategy and the Environment 30: 3821–38. [Google Scholar]

- Daniels, Lauren, Yves Stevens, and David Pratt. 2021. Environmentally friendly and socially responsible investment in and by occupational pension funds in the USA and the EU. European Journal of Social Security 23: 247–63. [Google Scholar] [CrossRef]

- Doni, Federica, and Lara Johannsdottir. 2021. COVID-19 and pandemic risk: The link to SDG 13, climate change and the finance context. In COVID-19: Paving the Way for a More Sustainable World. Cham: Springer, pp. 43–60. [Google Scholar] [CrossRef]

- Falato, Antonio, Itay Goldstein, and Ali Hortaçsu. 2021. Financial fragility in the COVID-19 crisis: The case of investment funds in corporate bond markets. Journal of Monetary Economics 123: 35–52. [Google Scholar] [CrossRef]

- Gambetta, Nicolas, Ines Garcia Fronti, Valeska V. Geldres-Weiss, Mauricio Gómez-Villegas, and Marcela Jaramillo Jaramillo. 2021. The Potential of Listed Companies to Finance the Sustainable Development Goals. Journal of Legal, Ethical and Regulatory Issues 24: 1–11. [Google Scholar]

- Ho, Shirley, and Cheng-Li Huang. 2018. Reply to “Modeling Managerial Altruism, CSR, and Donations: A Comment”. Managerial and Decision Economics 39: 591. [Google Scholar] [CrossRef]

- Huk, Katarzyna, and Mateusz Kurowski. 2021. The environmental aspect in the concept of corporate social responsibility in the energy industry and sustainable development of the economy. Energies 14: 5993. [Google Scholar] [CrossRef]

- Ikram, Muhammad, Marcos Ferasso, Robert Sroufe, and Qingyu Zhang. 2021. Assessing green technology indicators for cleaner production and sustainable investments in a developing country context. Journal of Cleaner Production 322: 129090. [Google Scholar] [CrossRef]

- Imanche, Sunday Adiyoh, Tian Ze, Salisu Gidado Dalibi, Taitiya Kenneth Yuguda, and Hassan Ali Kumo. 2021. The Role of Sustainable Finance in the Achievement of Sustainable Development Goals in Nigeria: A Focus on Chinese Foreign Direct Investment. In IOP Conference Series: Earth and Environmental Science. Bristol: IOP Publishing, vol. 793. [Google Scholar] [CrossRef]

- International Monetary Fund. 2021. World Economic Outlook Database: October 2021. Available online: https://www.imf.org/en/Publications/WEO/weo-database/2021/October (accessed on 1 December 2021).

- Ionescu, Luminita. 2021. Leveraging green finance for low-carbon energy, sustainable economic development, and climate change mitigation during the COVID-19 pandemic. Review of Contemporary Philosophy 20: 175–86. [Google Scholar] [CrossRef]

- Janowski, Marcin. 2021. CSR and Postal Service Sustainable Development and Its Impact on Urban Environment at the Example of Courier Service Operator Solutions in Europe. In Advanced Studies in Efficient Environmental Design and City Planning. Cham: Springer, pp. 513–19. [Google Scholar] [CrossRef]

- Jegers, Marc. 2018. Modeling managerial altruism, CSR, and donations: A comment. Managerial and Decision Economics 39: 425–26. [Google Scholar] [CrossRef]

- Ji, Xiangfeng, Xueqi Chen, Nawazish Mirza, and Muhammad Umar. 2021. Sustainable energy goals and investment premium: Evidence from renewable and conventional equity mutual funds in the Eurozone. Resources Policy 74: 102387. [Google Scholar] [CrossRef]

- Khuong, Mai Ngoc, Nguyen Khoa Truong An, and Tran Thi Thanh Thanh Hang. 2021. Stakeholders and Corporate Social Responsibility (CSR) programme as key sustainable development strategies to promote corporate reputation—Evidence from Vietnam. Cogent Business and Management 8: 1917333. [Google Scholar] [CrossRef]

- Kurniatama, Gandang Ardi, Robiyanto Robiyanto, Gatot Sasongko, and Adrian Dolfrianda Huruta. 2021. Determinants of corporate social responsibility: Empirical evidence from sustainable and responsible investment index. Quality—Access to Success 22: 55–61. [Google Scholar]

- Leal Filho, Walter. 2021. Non-conventional learning on sustainable development: Achieving the SDGs. Environmental Sciences Europe 33: 97. [Google Scholar] [CrossRef]

- Liyanage, Shantha Indrajith, Fulu Godfrey Netswera, and Abel Motsumi. 2021. Insights from EU policy framework in aligning sustainable finance for sustainable development in Africa and Asia. International Journal of Energy Economics and Policy 11: 459–70. [Google Scholar] [CrossRef]

- Lopata, Ewelina, and Krysztof Rogatka. 2021. CSR & COVID19—How do they work together? Perceptions of Corporate Social Responsibility transformation during a pandemic crisis. Towards smart development. Bulletin of Geography. Socio-economic Series 53: 87–103. [Google Scholar] [CrossRef]

- López-Concepción, Arelys, Anna Gil-Lacruz, and Isabel Saz-Gil. 2021. Stakeholder engagement, CSR development and SDGs compliance: A systematic review from 2015 to 2021. Corporate Social Responsibility and Environmental Management 29: 19–31. [Google Scholar] [CrossRef]

- Mach, Łukasz, Karina Bedrunka, Anna Kuczuk, and Marzena Szewczuk-Stępień. 2021. Effect of structural funds on housing market sustainability development—Correlation, regression and wavelet coherence analysis. Risks 9: 182. [Google Scholar] [CrossRef]

- Machokoto, Michael, Ngoza Ibeji, and Chimwemwe Chipeta. 2021. Investment–cash flow sensitivity around the crisis: Are African firms different? International Journal of Managerial Finance 17: 733–56. [Google Scholar] [CrossRef]

- Miralles-Quirós, Jose Luis, Maria Mar Miralles-Quirós, and Jose Manuel Nogueira. 2020. Sustainable development goals and investment strategies: The profitability of using five-factor fama-french alphas. Sustainability 12: 1842. [Google Scholar] [CrossRef] [Green Version]

- Nawrocki, Tomasz, and Danuta Szwajca. 2021. A multidimensional comparative analysis of involvement in CSR activities of energy companies in the context of sustainable development challenges: Evidence from Poland. Energies 14: 4592. [Google Scholar] [CrossRef]

- Nedopil Wang, Christoph, Mathias Lund Larsen, and Yu Wang. 2020. Addressing the missing linkage in sustainable finance: The ‘SDG Finance Taxonomy’. Journal of Sustainable Finance and Investment, 1–8. [Google Scholar] [CrossRef]

- Nobanee, Haitham, Maryam Alhajjar, Ghada Abushairah, and Safaa Al Harbi. 2021. Review reputational risk and sustainability: A bibliometric analysis of relevant literature. Risks 9: 134. [Google Scholar] [CrossRef]

- Quaranta, Cristina, and Emilliano Di Carlo. 2020. The Incentives of a Common Good-Based CSR for SDG’s Achievement: The Importance of Mission Statement. In Accountability, Ethics and Sustainability of Organizations. Cham: Springer, pp. 23–43. [Google Scholar] [CrossRef]

- Ragulina, Julia, Stanislav Prokofyev, and Tatyana Bratarchuk. 2021. Managing the risks of innovative activities focused on the consumer market: Competitiveness vs. corporate responsibility. Risks 9: 173. [Google Scholar] [CrossRef]

- Rehman, Mobeen Ur, Muhammad Kashif, Nader Naifar, and Syed Jawad Hussain Shahzad. 2021. Socially Responsible Funds and Traditional Energy Commodities: A Diversification Perspective for Investments. Frontiers in Environmental Science 9: 709990. [Google Scholar] [CrossRef]

- Rim, Hyejoon, and Dooti Song. 2017. Corporate message strategies for global CSR campaigns: The mediating role of perceived altruism. Corporate Communications 22: 383–400. [Google Scholar] [CrossRef]

- Rim, Hyejoon, Song-Un Yang, and Jaejin Lee. 2016. Strategic partnerships with nonprofits in corporate social responsibility (CSR): The mediating role of perceived altruism and organizational identification. Journal of Business Research 69: 3213–19. [Google Scholar] [CrossRef]

- Singh, Manjit, Manju Mittal, Pooja Mehta, and Himanshu Singla. 2021. Personal values as drivers of socially responsible investments: A moderation analysis. Review of Behavioral Finance 13: 543–65. [Google Scholar] [CrossRef]

- Sudirman, Faturachman Alputra, Ambo Upe, and Fera Tri Susilawaty La Ode Herman. 2021. Corporate social responsibility (CSR) contribution to achieving sustainable development goals (SDGs) in southeast Sulawesi. Paper presented at the International Conference on Industrial Engineering and Operations Management, Singapore, March 7–11; pp. 3408–16. [Google Scholar]

- Tan, Feifei, Hao Wan, Xiangjun Jiang, and Zhiyuan Niu. 2021. The impact of outward foreign direct investment on carbon emission toward china’s sustainable development. Sustainability 13: 11605. [Google Scholar] [CrossRef]

- Trzeciak, Mateusz. 2021. Sustainable risk management in IT enterprises. Risks 9: 135. [Google Scholar] [CrossRef]

- UN. 2021. Sustainable Development Report 2021The Decade of Action for the Sustainable Development Goals. Available online: https://sdgindex.org/reports/sustainable-development-report-2021/ (accessed on 1 December 2021).

- Unger, Eva-Maria, Rohan Mark Bennett, Christian Lemmen, and Jaap Zevenbergen. 2021. LADM for sustainable development: An exploratory study on the application of domain-specific data models to support the SDGs. Land Use Policy 108: 105499. [Google Scholar] [CrossRef]

- Vagin, Sergei, Elena Kostyukova, Natalia Spiridonova, and tatiana Vorozheykina. 2021. Financial risk management based on corporate social responsibility for sustainable development. Mendeley Data V1. [Google Scholar] [CrossRef]

- Vanwalleghem, Dieter, and Agata Mirowska. 2020. The investor that could and would: The effect of proactive personality on sustainable investment choice. Journal of Behavioral and Experimental Finance 26: 100313. [Google Scholar] [CrossRef]

- Wang, Lei, Chi-Wei Su, Shahid Ali, and Hsu-Ling Chang. 2020. How China is fostering sustainable growth: The interplay of green investment and production-based emission. Environmental Science and Pollution Research 27: 39607–18. [Google Scholar] [CrossRef]

- Xiong, Kai, and Yijun Yao. 2021. Research on China’s Green Finance Promoting Sustainable Economic Development. 2021 Paper presented at E3S Web of Conferences, International Conference on Economic Innovation and Low-carbon Development (EILCD 2021), Qingdao, China, May 28–30; p. 275. [Google Scholar]

- Yoshino, Naoyuki, Fahrad Taghizadeh-Hesary, and Miyu Otsuka. 2021. COVID-19 and Optimal Portfolio Selection for Investment in Sustainable Development Goals. Finance Research Letters 38: 101695. [Google Scholar] [CrossRef]

- Zhang, Bufan, and Yifeng Wang. 2021. The Effect of Green Finance on Energy Sustainable Development: A Case Study in Emerging Markets. China Finance and Trade 57: 3435–54. [Google Scholar] [CrossRef]

- Zhao, Hung, Wei Du, Hao Shen, and Xinting Zhen. 2021. Corporate social responsibility and bond price at issuances: U.S. evidence. Sustainability 13: 13123. [Google Scholar] [CrossRef]

- Ziogas, Ioannis, and Theodore Metaxas. 2021. Corporate social responsibility in south Europe during the financial crisis and its relation to the financial performance of Greek companies. Sustainability 13: 8055. [Google Scholar] [CrossRef]

- Ziolo, Magdalena, Iwona Bak, and Katarzyna Cheba. 2021. The role of sustainable finance in achieving sustainable development goals: Does it work? Technological and Economic Development of Economy 27: 45–70. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Criterion of Comparison | Financial Risk Management of Economic Growth (GDP) | Financial Risk Management of Sustainable Development |

|---|---|---|

| Manifestation of economic crisis | the slowdown of the rate of economic growth (reduction of GDP) | the slowdown of progress in implementing the SDGs (reduction of the sustainable development index) |

| Financial risks, which increase in the conditions of economic crises | deficit (an increase of demand with a less vivid increase or decrease of the offer of investments) of investments for economic growth | deficit of responsible investments due to the insufficient (low or reduced) level of corporate social responsibility |

| Structure of investments | simple—all investments are important and equally valuable | complex—only responsible investments are necessary and valuable |

| Approach to economic crisis management | the attraction of investments for the financial support for the vectors of economic growth | the attraction of responsible investments through the stimulation of corporate social responsibility |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vagin, S.G.; Kostyukova, E.I.; Spiridonova, N.E.; Vorozheykina, T.M. Financial Risk Management Based on Corporate Social Responsibility in the Interests of Sustainable Development. Risks 2022, 10, 35. https://doi.org/10.3390/risks10020035

Vagin SG, Kostyukova EI, Spiridonova NE, Vorozheykina TM. Financial Risk Management Based on Corporate Social Responsibility in the Interests of Sustainable Development. Risks. 2022; 10(2):35. https://doi.org/10.3390/risks10020035

Chicago/Turabian StyleVagin, Sergei G., Elena I. Kostyukova, Natalia E. Spiridonova, and Tatiana M. Vorozheykina. 2022. "Financial Risk Management Based on Corporate Social Responsibility in the Interests of Sustainable Development" Risks 10, no. 2: 35. https://doi.org/10.3390/risks10020035

APA StyleVagin, S. G., Kostyukova, E. I., Spiridonova, N. E., & Vorozheykina, T. M. (2022). Financial Risk Management Based on Corporate Social Responsibility in the Interests of Sustainable Development. Risks, 10(2), 35. https://doi.org/10.3390/risks10020035