Abstract

In this paper, we investigate rewards-based crowdfunding as an innovative financing form for startups and firms. Based on game-theory models under asymmetric information, we test research hypotheses about the positive effects of two main campaign features: funding target and number of rewards. Furthermore, we examine how and when these characteristics are effective in attracting crowdfunders, by signaling high-quality projects (target) and by pricing according to backers’ preferences (rewards). Conditional process analysis is applied to a dataset of 1613 projects launched on the Spanish platform Verkami from 2015 to 2018. As expected, our study shows that market size is positively influenced by the target and the number of rewards, separately. Further analysis gives some interesting findings. Firstly, we find significant and positive mediating roles of social networks (in the relationship between target and market size) and of backers’ preferences (between rewards and market size). Secondly, the main orientation of a campaign, commercial or social, is relevant to explain previous relationships. While high funding targets are more effective in commercial projects, a high number of rewards is more effective in the social projects. This research provides new insights into the design of optimal crowdfunding, with theoretical and empirical implications.

1. Introduction

Crowdfunding has experienced a dramatic growth in the past decade as a ground-breaking funding tool for startups and small- and medium-sized firms. This growing phenomenon enables entrepreneurs to kick off innovative projects by raising funds from large crowds through digital platforms.

While there are several kinds of crowdfunding in practice, in this paper, we examine the prominent type of rewards-based crowdfunding, where funders/backers are compensated with a particular reward. The definition of a “reward” can be very broad: it may consist of a physical product, such as a smartwatch; an information good, such as a movie or software; or even simple thanks for the patronage. At the beginning of a campaign, an entrepreneur posts the description of his/her project, sets a funding target necessary to carry out the project, and offers a relatively wide set of rewards to potential funders. Each reward corresponds to a particular price/bid. In this regard, the project is funded with the monetary bids of backers for rewards. When the raised amount reaches the funding target, the crowdfunding campaign ends successfully. Therefore, the study of the conditions in which a campaign design (defined mainly by target and reward level) is effective in attracting large heterogeneous crowds is determinant for explaining campaign success. This is the main purpose of our paper.

In particular, we investigate the role of social networks as a mediator in the association between the target and market size, the role of backers’ preferences as a mediator between the reward level and the market size and, for both associations, the role of the project nature as a moderator. We answer these questions, using a mediation regression analysis and a moderated mediation regression analysis. Because our interest is to analyze those effects for projects that are more likely to be undertaken, we consider only successful projects (the raised amount during the campaign is beyond the target level).

A key feature of a crowdfunding campaign is that the interaction between the entrepreneurs and the potential future backers develops in a context of asymmetric information. On the one hand, the entrepreneur is typically better informed about the value or quality of the project than the backers. The backers usually receive signals (informative or not) and decide how much to pledge to the project. On the other hand, entrepreneurs face a high uncertainty about market demand and backers’ valuations given to their products. In this regard, rewards-based crowdfunding is considered an information aggregation mechanism that is extremely valuable for innovative startups (next to raising money). For instance, even an entrepreneur with no credit constraints may use rewards-based crowdfunding as an advertising tool, and for estimating the future demand of his/her product.

The nature of projects may also play a relevant role to explain crowdfunding success. As such, we refer to the entrepreneur’s main purpose with the project: whether his/her goal is to produce a product to maximize profits (namely, commercial projects) or, by contrast, he/she is a non-profit entrepreneur whose main goal is to benefit social community (namely, social projects). The impact of campaign design on capturing backers’ support may crucially depend on their main motivations, that is, the type of projects. Therefore, we are also interested in studying the mechanisms through which heterogeneous backers direct their support toward projects with different goals (commercial versus social community).

Therefore, our research aim is twofold: firstly, we analyze the effects of campaign design features on market size (number of backers). We focus particularly on two main design variables: the funding target and the reward level. Secondly, we examine how and when these two variables can be defined by entrepreneurs to successfully attract large crowds. The question regarding how is answered by studying the impact of two mediators (social networks and backers’ preferences), while the question regarding when is analyzed using the project nature as a moderator. Based on the theoretical literature on crowdfunding, we design and estimate an empirical model to explain the strategic relationships between entrepreneurs and backers.

Academic research on crowdfunding has very rapidly developed in recent years. Agrawal et al. [1] and Belleflamme et al. [2] surveyed early empirical and theoretical approaches. Kuppuswamy and Bayus [3] and Moritz and Block [4] provided also a detailed review of crowdfunding literature. Theoretical models of crowdfunding analyze the effectiveness of different design mechanisms under asymmetric information.

Rewards-based crowdfunding can be conceived as both a financing and selling instrument. Theoretical works show that funding is not fundamental for crowdfunding to be attractive for not-for-profit and for-profit entrepreneurs. Focusing on the selling role of crowdfunding, we find two main strands of research. Firstly, some studies analyze crowdfunding as an incentive-compatible market test that permits to adapt production to demand conditions (Strausz [5], Chemla and Tinn [6], Chang [7] and Chakraborty and Swinney [8]). Here, a common assumption is that backers’ behavior depends on both their preferences and their beliefs about the quality of the project (signaling games) and the entrepreneurs’ reputation (moral hazard models). In the present study, we are interested in the use of informative signals about the quality of the project. Thus, based on this line of research, we select the funding target as the key campaign variable for signaling high project quality and, thus, for attracting more backers. In particular, we test whether there is a positive association between target and market size.

Secondly, a smaller number of studies assess whether rewards-based crowdfunding can be also strategically used to discriminate pricing (Cornelli [9] and Ellman and Hurkens [10]). The design of an optimal reward level will allow entrepreneurs to extract rent from consumer surplus by charging high prices to consumers/backers with high valuations and low prices to consumers who value the product less. Empirical research provides strong evidence that crowdfunding success is related to the ability of entrepreneurs to convince backers to pledge to their projects (Mollick [11]). Thus, the reward level is chosen as the key design variable to test our second main hypothesis about the positive effect of the number of rewards on market size.

We also examine how and when both the quality signaling role of the target and the price discrimination role of reward levels are expected to be effective. Extant empirical literature has documented the importance of social networks in crowdfunding. Therefore, in the present study, we explore the influential mechanism underlying the association between the target and market size by looking at the interaction level of entrepreneurs with their supporters in the platform network. In addition, researchers have found empirical evidence that backers’ pledged amounts differ considerably among projects, which may depend on the reward level designed by entrepreneurs. Thus, regarding the association between reward level and market size, we study the mediating role of willingness-to-pay (WTP, hereafter) of backers in this relationship. Lastly, we test whether the project nature (commercial and social) moderates the conditions underlying the influence of the target and rewards on market size.

The present research contributes to a burgeoning literature on crowdfunding by examining the empirical conditions (associated to social networks, backers’ valuations and project nature) under which two main theoretically studied drivers (funding target and reward level) influence investment decisions in rewards-based crowdfunding.

The effectiveness of rewards-based crowdfunding as a mechanism to obtain feedback on demand is partly determined by the number of people who know of the existence of the crowdfunding campaign. In this paper, we analyze the data of one of the most important crowdfunding platforms in Spain, Verkami. The total sample consists of 1613 projects (1175 social projects and 438 commercial projects) launched between 2015 and 2018. All projects were successfully financed and reached a total monetary amount beyond their initial targets.

Our research allows to confirm the predictions based on game-theory models, and provides new insights into the crowdfunding design. The empirical findings show significantly positive effects of the target and rewards on market size, with notable differences between project types. In particular, we find that the effectiveness of the funding target (as a quality signal) to attract backers is higher in market-oriented projects (with commercial purposes) than in community-oriented projects (with social purposes). The mediating role of social networks helps to explain these relationships. On the contrary, the attraction capacity of rewards is stronger in the social projects than in the commercial projects. The mediating role of backers’ preferences (WTP) for paying more for social projects sheds light on these associations.

The remainder of the paper is structured as follows. Section 2 deals with the related literature and research hypotheses. Section 3 describes the project sample, the variables and the empirical models. Section 4 outlines the main findings which then are discussed in Section 5. Finally, Section 6 concludes.

2. Related Literature and Research Hypotheses

2.1. Game-Theoretic Models of Asymmetric Information in Rewards-Based Crowdfunding

Researchers have developed different theoretical approaches to model rewards-based crowdfunding. Models with private value about the project’s quality were firstly studied by Cornelli [9]. More recently, a line of research studies analyzed a moral hazard problem, where backers are not certain whether the entrepreneur will actually deliver the rewards or run away with the money raised from the campaign (Strausz [5], Chemla and Tinn [6], and Chang [7]). Two funding schemes were compared: a fixed funding mechanism (all-or-nothing, in practice), where money is refunded if the target is not met; and an alternate funding mechanism, called flexible (or keep-it-all) funding, where there is no refund. These studies reveal that fixed funding is superior in controlling entrepreneurial incentive problems. By reducing demand uncertainty, Strausz [5] found that crowdfunding promotes welfare and complements traditional entrepreneurial financing. Chemla and Tinn [6] showed that the value of learning the uncertain demand is high enough to overcome moral hazard by choosing fixed funding with a high target. In a setting with greater heterogeneity in backers’ values, Chang [7] showed that the optimal campaign uses fixed funding, being attractive to both small and large entrepreneurs. Belavina et al. [12] studied the interaction between performance opacity (i.e., backers do not observe the product quality) and funds misappropriation (i.e., the entrepreneur may not deliver the reward), and proposed some designs to mitigate these risks, such as stopping the campaign once the target is reached.

Models with private values have also been developed to study issues other than moral hazard. Belleflamme et al. [2] studied crowdfunding with asymmetric information about quality. They developed a signaling model with a unique price and continuous crowd. The backers are heterogeneous in their valuations and there is no demand uncertainty. In this context, the authors claimed that the community benefits or warm-glow is the justification for the high valuations of backers. Ellman and Hurkens [10] proposed a crowdfunding model with multiple prices, where warm-glow is unnecessary for (but compatible with) high-type backers to pay a crowdfunding premium. A key result is that a finite crowd is required to achieve a pivotal motive to implement price discrimination. Sayedi and Baghaie [13] considered a model in which creators signal their marginal cost of quality via their campaign design. Chakraborty and Swinney [8] incorporated the way creators can use target funding levels to help mitigate the impact of demand uncertainty as well as signal product quality. In their model, heterogeneity derives from intrinsic quality levels, rather than from quality marginal costs as in that of Sayedi and Baghaie [13]. While Sayedi and Baghaie [13] assumed that total market size is deterministic but valuations are a stochastic function of quality, Chakraborty and Swinney [8] assumed that market size (the number of backers interested in the product) is itself stochastic. Other theoretical works that examined the optimal properties of crowdfunding are Parker [14] (information cascades), Schwienbacher [15] (entrepreneurs’ risk taking) and Hakenes and Schlegel [16] (costly signals).

In the present research, we focus on two main aspects of rewards-based crowdfunding: the signaling of project quality and price discrimination. We next present the main elements of two theoretical models, which support the basis for our main research hypotheses: (i) a signaling model, which tackles the information asymmetry problem about project quality and, (ii) a price discrimination model, which analyses the effective learning of demand through multiple prices/rewards.

2.1.1. A Signaling Model about the Quality of Crowdfunding Projects

Here, we describe the main features of the crowdfunding model developed by Chakraborty and Swinney [8]. An entrepreneur launches a new product/project via a campaign on a rewards-based crowdfunding platform. The model is developed considering a single unit of the product as the only reward. The entrepreneur thus sets the reward price p and the funding target T: denotes the design parameters of the campaign, namely, the strategies chosen by the entrepreneur.

The authors consider a fixed funding mechanism or aggregate fund threshold with refunds: the campaign is deemed successful as long as the backers’ total pledges meet the funding target; in that case, the entrepreneur receives the aggregate funding and is obliged to deliver rewards. Otherwise, the campaign fails, backers are refunded their pledges, and the entrepreneur does not deliver any rewards. This is the funding mechanism implemented by the Verkami platform: all-or-nothing.

The project is assumed to be of either high or low quality. For simplicity, H-type is used to refer to a high-quality project and its entrepreneur, while L-type refers to a low-quality project and its entrepreneur. Backers have homogeneous valuations, and , for the H-type and L-type projects, respectively, where .

The difference in quality can arise in multiple ways. First, there could be diversity of attributes in the reward delivered by the entrepreneur, which is common with the type of innovative products typically launched via crowdfunding platforms. Such uncertainty in quality may directly lead to differences in utility derived from the projects offered by the entrepreneur types. Second, heterogeneity in project quality could be also due to the capabilities of the entrepreneur to successfully deliver the reward to backers after the campaign meets its target. In practice, most campaign promoters on crowdfunding platforms are amateur entrepreneurs, making their ability to fulfill contractual obligations uncertain for backers. In this regard, differences between an entrepreneur’ abilities could generate differences in backers’ expected valuations, and . Backers could assign a higher probability of successfully delivering rewards to the H-type entrepreneur than to the L-type entrepreneur. Therefore, heterogeneous valuations can be explained by heterogeneity in the chance that an entrepreneur fails to deliver the promised reward.

Although backers are homogeneous in their valuations, they are heterogeneous in their knowledge about the entrepreneur’s type. For instance, they are heterogeneous in their skill to determine whether the entrepreneur is more or less likely to deliver the reward or to accurately assess the characteristics of the project. Backers do not know the entrepreneur’s true type and must determine this information based on the design of the campaign and their common prior belief of the probability that a project is of H-type. After observing the design parameters of the campaign, backers update their belief that the project is H-type, and pledge to the campaign as long as their expected valuation exceeds the selling/offer price, that is, if .

Thus, the backers’ strategy set consists of supporting a campaign or not. A backer will support a campaign as long as his/her expected utility from pledging is non-negative (reservation utility), given his/her prior beliefs about the quality of the entrepreneur’s project and any information learned by observing the entrepreneur’s campaign.

A common approach used in much of the signaling literature consists of deriving an optimal strategy that separates the H-type entrepreneur from the L-type entrepreneur based purely on information conveyed in the design of the campaign. Thus, the strategic setting is defined by a signaling game with incomplete information in which an entrepreneur chooses appropriately the parameters of his/her campaign, T and p, to maximize his/her total profits at the end of the campaign. The solution concept is given by a perfect Bayesian equilibrium, and analyzes two possible types of equilibria: a separating equilibrium, in which the backers can distinguish the two types perfectly (that is, their posterior belief that the project is of high quality, , is either 0 or 1), and a pooling equilibrium, where the backers do not learn any new information from the entrepreneur’s campaign design (i.e., where the posterior belief is the same as their prior belief ).

The expected profit of an entrepreneur of type is as follows:

where the total number of backers interested in investing in the project, N, is a random variable with density function given by . is the fixed cost required to undertake the entrepreneur i’ project. It is assumed that . As can be seen, the expected profit depends positively on the number of backers, as N determines total revenues, .

The timing of the signaling game is as follows:

- t = 0: nature chooses the type of entrepreneur, H or L.

- t = 1: entrepreneur designs the contract or campaign .

- t = 2: agent observes and calculates his/her posterior beliefs that the entrepreneur is H-type, .

- t = 3: agent either pledges to the campaign or not according to expected valuations and selling price: .

- t = 4: campaign outcome and payments are determined.

It is worth noting that for an entrepreneur’s decision to be a signal, it must involve some cost. Under complete information, an entrepreneur of type sets the lowest possible funding target, given his/her fixed startup costs () and price , his/her project valuation. Consequently, in the presence of information asymmetry, the L-type sets target and price in any separating equilibrium. The choice of how to separate (i.e., by varying the target or by varying the price) depends only on the H-type entrepreneur.

Chakraborty and Swinney [8] showed that the funding target is a more effective signal of quality than the reward price, or than any combination of the two campaign parameters. Indeed, these authors concluded that separation by varying the campaign target is the H-type’s dominant strategy.

A second important result indicates that, though a high target will signal high quality, as the entrepreneur increases his/her target (while keeping price constant) the probability of failure increases, and expected profits decreases. However, the authors claimed that, if demand is high and success occurs (the funding target is reached), a high target does not affect the entrepreneur’s profits. This is because the risk of failure is higher with a high target, but once achieved, revenues received from backers compensate costs. This result is particularly important for our purposes, as our sample is composed only of successful campaigns.

In addition to the theoretical work on signaling in crowdfunding, there is also limited but growing empirical research on the topic, with somewhat conflicting results: Frydrych et al. [17] found that a lower target signals the legitimacy of a campaign (see also Mollick [11] and Dikaputra et al. [18]), while Devaraj and Patel [19] found that a higher target signals higher quality (supported also by Chung et al. [20]). Chakraborty and Swinney [8] added to this stream by providing theoretical support for the use of a higher target level to signal a higher-quality product.

Therefore, we will posit our first main hypothesis on the positive signaling effect of target for the project quality and, therefore, for increasing market size.

Hypothesis 1 (H1).

Target is positively associated with market size.

2.1.2. A Crowdfunding Model with Price Discrimination

Multiple rewards are a salient feature of crowdfunding platforms, where every reward is typically associated with a price. Multiple prices are relevant in practice, and matter in theory. Here, we describe the main elements of the optimal crowdfunding mechanism developed by Ellman and Hurkens [10]. This is the only paper to address multiple prices; all previous studies imposed a unique price for all backers of a campaign. In particular, Belleflamme et al. [2], Sayedi and Baghaie [13] and Kumar et al. [21] developed models where entrepreneurs discriminate between the price paid by backers of a crowdfunding campaign and that which would be paid by consumers of the future spot market in the case that the entrepreneur decides to produce and sell the product after the crowdfunding campaign. These authors showed that price discrimination proves necessary for effective learning of demand, substantial efficiency gains, even with relatively large crowds, and reduction in the need for credit. However, multiple prices also introduce the risk of excessive rent extraction, which yields the value of limiting reward quantities.

The timing of the game is as follows:

- t = 1: entrepreneur designs his/her campaign .

- t = 2: backers learn their private values and simultaneously choose their bids from .

- t = 3: campaign outcome determines production, consumption and payments.

Therefore, the strategies chosen by the entrepreneur are defined in terms of the target level, T, and the pricing options, p. Likewise, backers’ strategies are given by their particular bids/pledges for the project.

Ellman and Hurkens [10] characterized the optimal reward-based crowdfunding mechanism for a binary type space and any crowd size. Namely, it is assumed that there is a finite number of backers with private heterogeneous valuations that are either high () or low (). These authors showed that crowdfunding fully implements the general optimum, where bidding strategies are given by a unique Pareto undominated Bayesian Nash equilibrium.

With a profit-maximizer entrepreneur, optimal crowdfunding design hinges on whether the high-type frequency exceeds the ratio of low to high valuations (). When the frequency of high-type backers is higher than this critical value (high frequency), the price is set at the high valuation, , which implies that low-type backers are excluded (E). However, when the frequency of high-type backers is below the critical value (low frequency), the price is set at the low valuation, , and low-type backers are included (I).

In the high-frequency (full exclusion) case, only high-type backers buy the product. Crowdfunding adapts production to demand via a threshold set at cost () to preclude losses. This induces production when the number of high types exceeds a cutoff (the pivot, ).

In the low-frequency (full inclusion) case, both high and low types buy the product. Crowdfunding again adapts production, but now sets to extract rent from high-type backers by making them sometimes pivotal for production. The optimal threshold trades off higher rents against lower success rates. Each high-type backer pays less than with exclusion but thanks to the payments from low-type backers under inclusion, the pivotal number of highs needed for production is lower (). So, production is more likely, despite the higher threshold. Therefore, a for-profit entrepreneur will choose higher targets (above cost) in order to extract higher consumer surplus under the low frequency case.

Ellman and Hurkens [10] also derived an interesting partial inclusion case, where crowdfunding must offer a menu of rewards and minimum prices. The entrepreneur may implement optimal design by offering a limited number of standard rewards at the low price, and an unlimited number of rewards at a higher price. This is a standard practice and our main focus in this paper. In our sample, a high number of rewards is observed in all campaigns, which suggests that entrepreneurs pervasively choose to implement a high degree of price discrimination to include a higher number of bidders. Empirical studies found that offering a number of reward levels broad enough to cater to a wide crowdfunder group increases the likelihood of reaching the fundraising target (Thürridl and Kamleitner [22], and Hu et al. [23]). Additionally, projects that offer a greater reward structure motivate backer participation (Crosetto and Regner [24], Koch [25], and Dikaputra et al. [18]).

Therefore, we measure the discrimination degree as the number of rewards offered by entrepreneur. Based on theoretical predictions, it would be expected that more backers (with different valuations under the partial inclusion case) are attracted when more rewards are offered. As shown below, our second main hypothesis anticipates a positive effect of the number of rewards on market size.

Hypothesis 2 (H2).

The number of rewards is positively associated with market size.

Once the main research hypotheses are established on the basis of theoretical models, we will next present the subsequent hypotheses to test how and when those main effects are expected to be observed.

2.2. The Mediating Role of Social Networks and Backers’ Preferences (WTP)

To answer the question about how market size is positively influenced by the funding target (H1) and the number of rewards (H2), we study the role of social networks in signaling the project quality and the role of backers’ preferences (WTP) in response to multiple prices/rewards.

Social networks play a fundamental role in success of crowdfunding campaigns. One of the pioneering empirical studies on reward crowdfunding is that of Mollick [11]. His research showed how personal networks and project quality signals are associated with campaign success. Furthermore, Bi et al. [26] found that the quality of the project and word of mouth are among the most relevant factors determining backers’ participation. To measure these variables, they considered project characteristics, such as the number of words, videos on the project or the number of “likes”. Many other works provide evidence that news or updates posted on the crowdfunding platform during the campaign are crucial for reaching the target, and also increase the amount raised beyond the target (for instance, Ahlers et al. [27], André et al. [28] and Kuppuswamy and Bayus [29]).

Updates provide visibility to the project. Some of the variables commonly considered to measure internal social capital are the successful projects that entrepreneurs have previously supported by creating an internal community with other members or the number of connections on LinkedIn that reflect their contacts with professionals and potential backers (Butticè et al. [30], Kuppuswamy and Bayus [31]). Crowdfunding platforms foster these internal connections through forums, messaging, founder’s profile pages, etc. The idea of creating a community through the use of crowdfunding networks is fundamental (Kromidha and Robson [32], Skirnevskiy et al. [33], and Gerber et al. [34]). Having experience in previous projects and sharing such information with potential investors can be considered a quality signal, which will attract more backers.

Therefore, as the mediating process in Hypothesis 1, we assume that social networks are one key channel to communicate information about the quality of the project. If the campaign target is an effective signal for high-quality projects, it is expected that communication between entrepreneurs and backers through social networks will reinforce/mediate the positive association between the target and market size.

Hypothesis 1.a (H1.a).

Social networks act as a mediator of the association between the target and market size.

Regarding the rewards–market relationship (H2), according to Ellman and Hurkens [10], a higher degree of price discrimination (a higher number of rewards) may help to expand the market size by including low-type backers. This means that there exists a positive relationship between rewards and market size because the frequency of low-type backers (who value the project less) increases, and therefore, the number of low-type pledges increases. However, an optimal design may be implemented by limiting the number of rewards at the low price without limiting the number of rewards at higher prices. In this sense, it could be expected that average pledge to the project will increase. Empirical evidence shows a relationship between the number of reward options and crowdfunding success. Indeed, Cai et al. [35] found positive associations between the number of rewards and market size (number of backers), and between the number of rewards and the average pledge. Therefore, we anticipate that the average pledge will mediate the positive association between price discrimination and market size. An average pledge can be considered a proxy for backers’ preferences elicited through their WTP or bids (on average).

Hypothesis 2.a (H2.a).

Backers’ WTP acts as a mediator of the association between rewards and market size.

2.3. The Moderating Role of Project Nature: Social Projects versus Commercial Projects

Though rewards-based crowdfunding can generally respond to an entrepreneur’s needs for both financing and reducing demand uncertainty, the nature of a project (social versus commercial) may crucially determine the design of a crowdfunding campaign. That is, entrepreneurs of commercial innovative projects are expected to be more worried about demand level in a post-crowdfunding market. Even an entrepreneur with no credit constraints may use crowdfunding for adapting production to demand and extracting rents from consumers (for-profit entrepreneurs). By contrast, entrepreneurs of social projects may be more concerned about how to benefit the community (non-for-profit entrepreneurs). Therefore, while securing sufficient financing may be decisive in social projects, it may be not so decisive in commercial projects.

To further understand the previously hypothesized associations, we introduce the project nature (commercial versus social) as a potential moderator of such associations and compare campaign performance of non-for-profit entrepreneurs (social projects) to that of for-profit entrepreneurs (commercial projects).

Empirical studies have shown robust evidence that project type is related to quality, founders’ goals, funding target or backers’ pledges (Agrawal et al. [1], Mollick [11]). Furthermore, some researchers have revealed the importance of offering information or updates on the project in specific sectors, such as educational technology startups, creative industries, etc. (Hobbs et al. [36], Antonenko et al. [37], and André et al. [28]).

We, thus, make one assumption regarding how the project nature affects the association between target and market size as well as the association between target and networks. In particular, we anticipate that the effectiveness of a target as a quality signal will be higher in the commercial projects than in the social projects. We also predict that social networks will be more active in commercial projects than in social projects since entrepreneurs of innovative products are more concerned about signaling their quality through networks than are entrepreneurs of social projects. In this regard, the positive effect of target on the use of social networks is conditional on the project nature (commercial versus social).

Hypothesis 1.b (H1.b).

Project nature (social versus commercial) simultaneously moderates the positive association between target and market size and the association between target and networks.

Lastly, we make a second assumption regarding whether the project nature moderates the association between rewards and market size, and the association between WTP and market size.

Extant literature provides strong support for the moderating effect of the project nature in the association between the number of reward levels and market size. In fact, backers with distinct motivations pledge to different types of projects (Ryu and Kim [38]). More product-seeking backers appear in the commercial projects, motivated by personal gains and tangible rewards. By contrast, other kind of incentives motivate backers interested in social projects, such as being part of a community, or supporting a social benefit related to environmental issues, social goals, education, disadvantaged groups, etc. (Younkin and Kashkooli [39], Gerber and Hui [20,40,41], Rodriguez-Ricardo et al. [42], Lin et al. [43], Dai and Zhang [44], Hong et al. [45], and Allison et al. [46]).

In particular, some studies suggest that the project nature influences the reward level. Calic and Mosakowski [47] found a lower number of rewards for some project categories, such as technology. From a theoretical viewpoint, warm-glow or social community benefits could explain the use of more rewards in social projects by expanding crowdfunders’ interest toward other-regarding motivations (see Belleflamme et al. [2]). Yet, non-for-profit entrepreneurs may well attract purely self-interested crowdfunders by promoting inclusion via low minimum prices (Ellman and Hurkens [10]). The empirical evidence is consistent with both explanations. Bürger and Kleinert [41] showed that backers of commercial projects are motivated by pecuniary rewards, while rewards that engage backers with their community matter more for cultural projects; backers of cultural projects are not altruistic in response to symbolic rewards.

However, evidence about how project nature influences backers’ WTP is mixed. Pitschner and Pitschner-Finn [48] observed that the average pledge is higher in social projects than in commercial projects, which suggests that backers are willing to pay (WTP) higher prices for projects with social goals. By contrast, Bürger and Kleinert [41] obtained that, on average, the reward price is higher in the projects developed by commercial entrepreneurs, compared to cultural entrepreneurs.

Based on previous research, we formulate the following hypothesis.

Hypothesis 2.b (H2.b).

Project nature (social versus commercial) simultaneously moderates the positive association between rewards and market size and the association between WTP and market size.

The next section describes the research design that we used to test our hypotheses.

3. Methodology

3.1. Sample and Measures

We analyze data collected from the Spanish platform Verkami. This digital platform was created in 2010; nowadays, it has become the main rewards-based crowdfunding platform in Spain (González and Ramos [49]). It stands out not only for the large number of projects, but also for the high success rate of its campaigns (with the highest rate of 74% in the world). Through this platform, a total of EUR 48.5 million has been raised to date and 9527 projects have been financed, with the participation of 1.3 million backers (data consulted on www.verkami.com on 24 August 2021). The market for alternative financing through rewards is at a maturity stage in Spain (Roodink and Kleverlaan [50]). The platform uses a fixed fundraising model, known as all-or-nothing, in practice.

The total sample has 5547 projects launched on the platform from 2015 to 2018. Data were collected in an automated way in September 2018 with a web crawling algorithm programmed in Python. From this total sample, we select representative categories of projects to test our hypotheses. Our data analysis is based on a total of 1613 projects, having the fundraising campaign successfully completed at the data collection date. We rely upon the public information provided on Verkami’s website as being indicative of the information potential backers used to make their pledging decisions.

The Verkami platform classifies projects very broadly by category. The category of a project is directly decided by the entrepreneur at the moment of registering his/her project on the platform. For each primary category, the Verkami platform also uses tags for providing further information about the project nature. Following Bürger and Kleinert [41], we take the primary categories displayed on the platform to classify projects as a part of the entrepreneur’s campaign strategy. Furthermore, a crowdfunding project is usually supported by backers with different profiles and motivations but, depending on the project nature, a particular profile predominates in each category. In line with our hypotheses, we distinguish between projects with a main orientation towards the market, and those with a main orientation toward the social community. Thus, projects are regrouped into two types: commercial and social. We have collected information for 1175 social projects and 438 commercial projects.

As commercial projects, we include the Verkami categories: science and technology, design, games and art. These types of projects are characterized by a greater presence of backers with high self-interest motivations, looking for a knowledge-intensive or creative product (Ryu and Kim [38], and Bürger and Kleinert [41]). Other empirical studies that considered these categories or similar as commercial are the following: Thürridl and Kamleitner [22], André et al. [28] and Parhankangas and Renko [51]. Using the Verkami tags, we can distinguish between commercial projects with a small social component. In our database, there are only 39 of the 438 commercial projects with a “Community” tag or an “Ecology” tag (8.9%). This represents a very small proportion. Likewise, the art category represents only a 17.35% of the commercial projects (76 projects), and only 4 projects are performances.

As social projects, we consider the Verkami categories: community and film. In these types of projects, there is a greater presence of backers whose main motivations are philanthropic, and the projects benefit social community (Ryu and Kim [38], Thürridl and Kamleitner [22], and Younkin and Kashkooli [39]). Some examples of social projects are the making of cultural documentaries to enhance the visibility of historical events or places, charity, or paying tribute to someone.

We next describe the variables used in our statistical analysis (see Table A1 in Appendix A).

3.1.1. Dependent Variable

To measure market size, we define the variable Backers, which captures the total number of backers who have pledged to each successfully completed project. Numerous studies have previously used the number of backers as a dependent variable since the individual decision to participate in a project will depend on the backers’ motivations and the characteristics of the project (Bi et al. [26], Bürger and Kleinert [41], Allison et al. [46], and Ahlers et al. [27]).

3.1.2. Independent Variables

The independent variables considered in this study are the funding target, the reward levels, updates, average WTP and the project nature. The Target variable measures the minimum amount of funding that entrepreneurs request at the beginning of the campaign. This variable is expressed in euros for each project. In our database, all projects raised a total monetary amount equal to or higher than the Target which means that, under the “all-or-nothing” scheme implemented by Verkami, all backers of a campaign effectively made their contributions (no refunds). Target represents the main explanatory variable for testing the role of quality signaling for attracting backers.

The Rewards variable captures for each project the number of reward options from which backers can choose. Each reward option is associated to a different price/bid. In most cases, as the price increases, the type of offered reward will include additional items, though it will depend on the project nature. A game project, for instance, may increase its price by offering either expansions of the game itself or several copies of the game in the same reward package. Rewards represents the main explanatory variable for testing the role of pricing discrimination for attracting backers.

The interaction between entrepreneurs and backers through social networks is measured with Updates. This variable refers to the number of updates posited on the Verkami platform during the fundraising campaign of a project. With this measure, we attempt to capture the frequency with which entrepreneurs provide information and receive feedback from potential funders to attract their attention. As mentioned in the hypotheses section, Updates will be used as a mediator of the relationship between Target and Backers.

To measure the average WTP of backers for the project, we use the average price paid for it. To do this, the total raised amount is divided by the total number of backers at the end of the campaign. This variable will act as a mediator of the relationship between Rewards and Backers in our statistical analysis.

Finally, the type of project is defined by a dummy variable, Project Nature, which takes a value of 1 when the project is commercial and 0 when it is social. This variable is of great interest for our data analysis because it defines the different paths through which the explanatory variables affect the dependent variable.

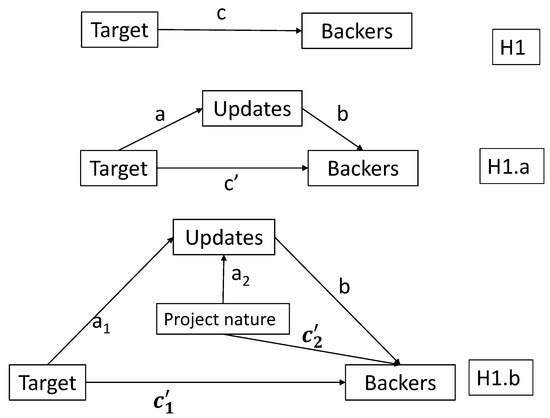

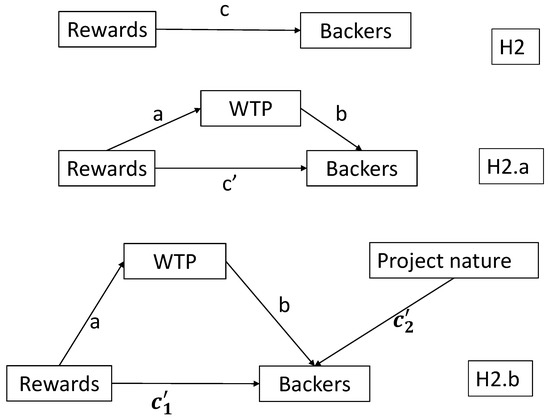

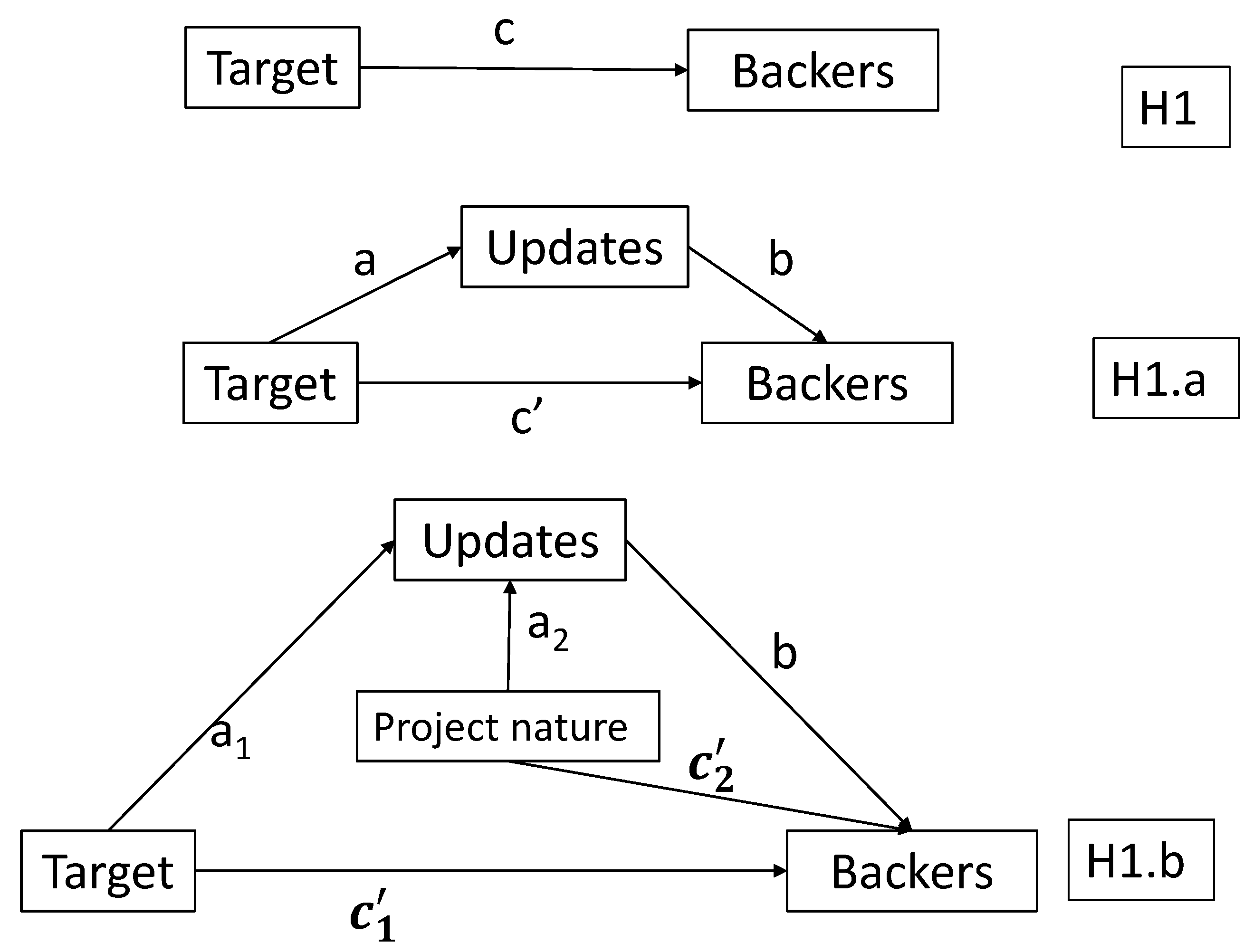

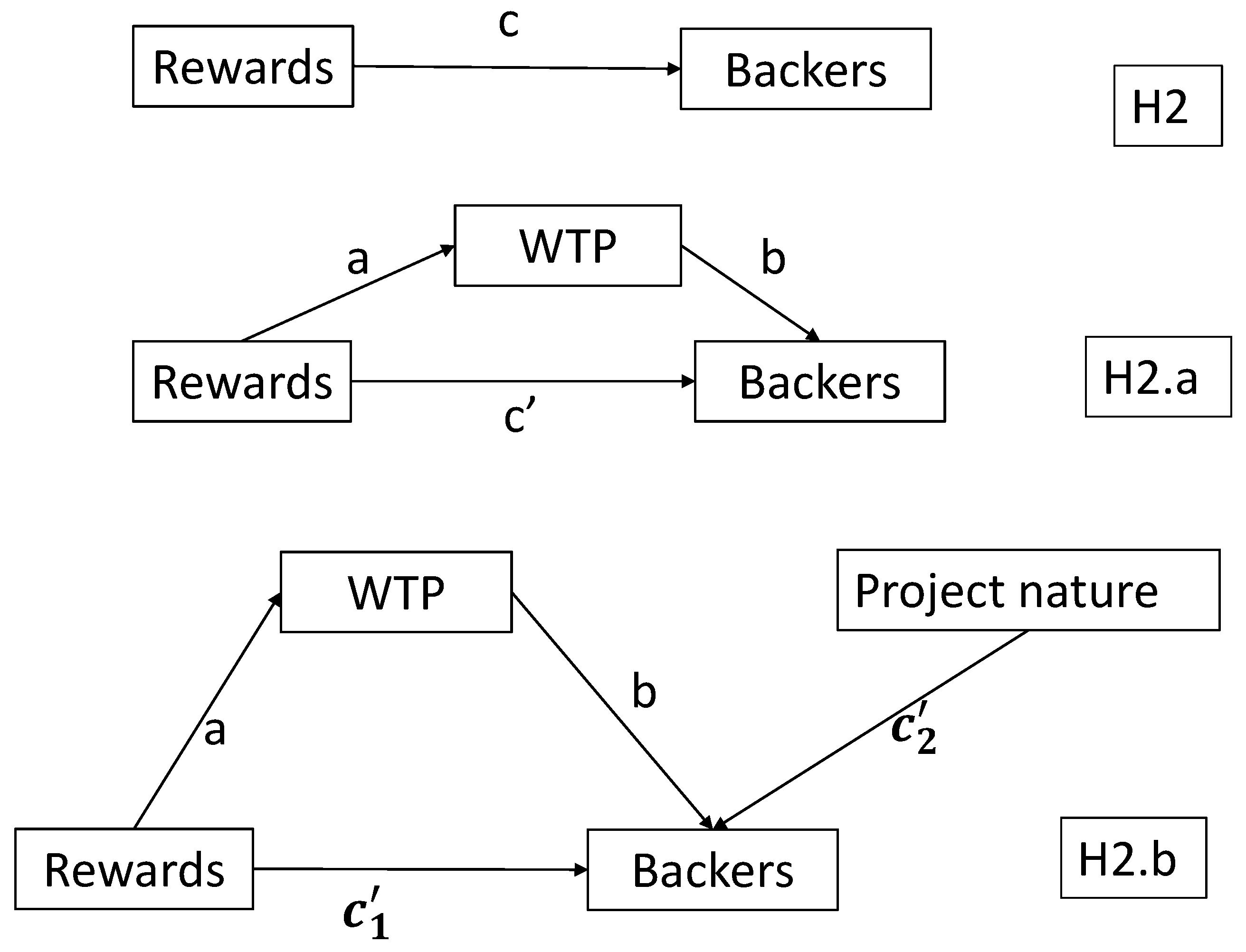

As we explain in the next subsection, Figure 1 and Figure 2 illustrate the conceptual diagrams to test Hypotheses H1, H1.a, H1.b, and Hypotheses H2, H2.a, H2.b, respectively.

Figure 1.

Basic, mediated and moderated mediation models of Target and Updates on Backers.

Figure 2.

Basic, mediated and moderated mediation models of Rewards and WTP on Backers.

3.1.3. Control Variables

As control variables, we consider the existence of video and entrepreneurs’ cooperation in other crowdfunding campaigns. Video is a dummy variable with a value of 1 if there is a video posted on the campaign’s website, and 0 otherwise. Researchers have widely studied the importance of this variable for success in rewards-based crowdfunding (Bi et al. [26], Mollick [11], Gorbatai and Nelson [52], Bi et al. [26], and Barbi and Bigelli [53]). Apart from providing general information about the project, the content of a video also shows the entrepreneurs’ abilities in preparing the campaign. Although the video content will clearly depend on the product/project, it may be a relevant campaign feature to reduce information asymmetry about the quality of the project (Courtney et al. [54]).

Lastly, the variable Entrepreneurs’ cooperation level (ECL) measures the number of crowdfunding campaigns that entrepreneurs of a project have previously supported. The fact that entrepreneurs have previously funded other projects may help to create internal social networks and build a community on the platform (Colombo et al. [55]). The projects whose creators have collaborated in other projects are more likely to be supported by the online community (Lin et al. [43], Zheng et al. [56]).

3.2. Statistical Models: Mediation Analysis and Moderated Mediation Analysis

As explained in Section 2, we explore the effect of Target on Backers (market size) at three levels: firstly, from a single linear regression model (direct path); secondly, quantifying the direct and indirect pathways through the intermediation of the number of Updates of campaigns; and thirdly, exploring how such mediation is conditioned by Project Nature (social or commercial). Figure 1 shows the conceptual diagrams that link the variables and the relationships between them for each level. Thus, means that X affects Y, and the letter on the arrow represents the regression coefficient of X in the regression equation of X on Y. Diagram H1 in Figure 1 represents the global relationship between Target and Backers through c. Diagram H1.a not only represents whether Target affects Backers (through ), but also how this effect exists through the mediation of Updates (through a and b). Then, we will talk of a direct effect of Target on Backers when Updates are constant, and of an indirect effect when the number of updates is taking into account (mediation analysis). Finally, diagram H1.b tells when the direct/indirect effects estimated in the previous model can be conditioned by Project Nature (moderated mediation analysis). That is, does the nature of the project lead to statistical differences in the direct/indirect effects of Target on Backers? For instance, when both direct and indirect effects are positive, a larger target will increase the market size (Backers) directly and indirectly through a higher number of updates. Yet, as expected, such effects may also depend on whether the project is commercial or social.

In the same line, we examine the effect of Rewards on Backers, from a basic model to a more complete one: including first WTP as a mediating variable and, afterwards, exploring whether such a mediation can be also conditioned by the project nature. Figure 2 contains the conceptual diagrams that summarize these steps.

To test the mediation models and the moderated mediation models, a conditional process analysis is performed (Hayes [57]) by using the macro PROCESS 3.5 for SPSS (freely available in www.processmacro.org). This methodology is particularly adequate to estimate, not only the direct/indirect effects of Target on Backers via the mediation of Updates, but also to examine when such effects are conditional on the type of projects funded through rewards-based crowdfunding. In all OLS regressions, the variables Video and ECL are included as control variables.

Although previous research in psychology and organizational behavior has widely used the (moderated) mediation analysis to explain associations between variables (Pollack et al. [58], Liu et al. [59], and Wu et al. [60]), a few number of studies can be found in the literature on crowdfunding (one exception is Calic and Mosakowski [47]).

4. Analysis

The statistical analysis of the dataset is carried out at a descriptive level in the first stage. Secondly, in a deeper study, a mediation regression analysis and a moderated mediation regression analysis are performed to determine the effects of the target and rewards on market size, using and as mediators, and taking the project nature (social and commercial) as a moderator in the rewards-based crowdfunding campaigns.

4.1. Descriptive Analysis

The number of campaigns considered for our study is 1613, of which 1175 are social projects and 438 are commercial projects. The summary of descriptive statistics for the whole sample and for each subsample is shown in Table 1. Some relevant findings are found: (i) commercial projects attract a mean value of 192.21 backers, whereas in the social projects, the attraction of funders decreases to 109.95, on average (although the most attractive project is social, with 3589 crowdfunders); (ii) the average target is quite similar in both types of projects, EUR 4781 for commercial projects and EUR 4598 for social projects, but the maximum value differs considerably, from EUR 60,000 (commercial projects) to EUR 200,000 (social projects); (iii) the offered number of rewards ranges from 98 (social projects) to 39 (commercial projects), which is consistent with the previous research (see, for example, Calic and Mosakowski [47]); and (iv) differences are also found with respect to the number of updates at the end of campaigns, in absolute and mean values, clearly in favor of commercial projects (maximum of 205 versus 109). Lastly, WTP is slightly higher for social projects than for commercial projects. On average, one backer of a social project pledges EUR 49.07, while one commercial backer pledges EUR 45.99.

Table 1.

Summary statistics.

Table 2 presents correlation results for the whole sample and the two project subsamples. As explained above, each conceptual diagram in Figure 1 is directly connected with hypotheses H1, H1.a and H1.b. The displayed relationships are supported by the positive correlation found between Target and Backers (), the positive correlation between Target and Updates (), the positive correlation between Updates and Backers (), and the fact that there exist notable differences between commercial and social projects.

Table 2.

Cross correlations between variables.

Likewise, the conceptual diagrams plotted in Figure 2 are used to test Hypotheses H2, H2.a and H2.b, and are based on correlation analysis. The positive correlation found between Rewards and Backers supports H2 (), the extant positive correlation between Rewards and WTP () and the negative correlation between WTP and Backers (). Again, these associations differ considerably between social and commercial projects.

The next subsection presents the statistical analysis of the effects (direct and indirect) of Target and Rewards on Backers, and examines (i) the connection of those effects with Updates and WTP, and (ii) whether such effects are dependent on the project type.

4.2. Results

Column 1 in Table 3 shows the results of the OLS regression analysis to estimate coefficients on Target to Backers with Video and ECL as control variables. Columns 2 and 3 include the regression coefficients of the two-step OLS regression analysis needed to include Updates as a mediating variable, and columns 4 and 5 are the corresponding results when Project Nature is additionally included as a moderating variable. This last analysis is called moderated mediation analysis. Notice that the total effect of Target on Backers is positive, units, after controlling by Video and ECL, which confirms Hypothesis H1. However, when Updates acts as a mediating variable, the total effect is decomposed into two parts: a direct effect of Target on Backers (Target’s coefficient in Equation (3), ), and an indirect effect through Updates (equal to Target’s coefficient in Equation (2) × Updates’ coefficient in Equation (3), ). In other words, if Updates takes a fixed value and Target increases by EUR 10, the number of backers increases by 0.155 units; if both Updates and Target increase by one unit each, the effect on Backers is increased by 0.0006 units. This result supports Hypothesis H1.a.

Table 3.

Results of the effects of Target, Updates and Project Nature on Backers.

Lastly, Table 3 also shows that the effects of Target on Backers are also moderated by the nature of the project. Thus, the impact of Target will not be the same for social and commercial projects. The results of Equations (4) and (5) allow us to obtain a significant total effect of Target on Backers, for social projects, while for commercial projects, this total effect is , where and are the regression coefficients of the interaction Target*Project Nature in Equations (4) and (5), respectively. As for the mediation model, the total effects can be decomposed into direct/indirect effects depending on whether Updates (mediator) is constant or not. The direct effect is obtained when Updates is fixed. Thus, Backers increases when Target adds one unit at rate of in social projects, while in commercial projects, such an direct effect is (both are statistically significant, ). However, in the indirect relationship between Target and Backers mediated by Updates, the indirect effects are reduced to in social projects and in commercial projects. To evaluate whether the indirect effects are significant, bootstrap confidence intervals at are performed with 5000 replications. The results show for social projects and for commercial projects. These findings agree with Hypothesis H1.b. With respect to the OLS regression model, it can be highlighted the acceptable explanatory capacity of the models with from to .

In sum, our findings show that the effectiveness of the target as a quality signal to attract backers is higher in the commercial projects than in the social projects: the total effect (direct and indirect effects) is 0.0196 in commercial projects and 0.0154 in social projects. Therefore, the project type (social versus commercial) becomes a relevant feature to explain the relationship between the funding target and market size in rewards-based crowdfunding.

Regarding the impact of the reward level, in Table 4, column 1 includes the coefficients of the OLS regression linked to diagram H2 in Figure 2, while columns 2 and 3 present the regression coefficients of the two-step OLS regression needed to incorporate WTP as a mediating variable. Lastly, columns 4 and 5 summarize the results of the inclusion of the nature of the project as a moderator in the mediation model. Again, in all the regressions, Video and ECT are included as control variables. Looking at Table 4, several findings can be highlighted. The first one allows to confirm hypothesis H2 since we obtain a significant and positive total effect of Rewards on Backers, . This effect implies that for each additional reward offered in a project, 10 additional backers support that project. Secondly, WTP acts as a mediator and allows to decompose the total effect into two parts: a direct effect with value and an indirect effect , both with statistical significance. This result supports Hypothesis H2.a. Notice that the negative value of the indirect effect means that one additional reward induces a reduction of backers as a result of the effect of Rewards on WTP which, in turn, negatively affects Backers.

Table 4.

Results of the effects of Rewards, WTP and Project Nature on Backers.

However, the inclusion of Project Nature as a moderator allows us to explore whether the direct relationship between Rewards and Backers and its indirect relationship mediated by WTP are different between social and commercial projects. For social projects, the direct effect of Rewards on Backers (when WTP is fixed) is , while for commercial projects, this value is . A direct implication of these results is that one additional reward is less effective for commercial projects than for social projects in the attraction of backers (more than half). On the contrary, regarding the indirect relationship, the indirect effect is for social projects, which is lower than the corresponding one for commercial projects, . Notice that although the number of reward options affects positively WTP, we also obtain that the higher WTP the lower number of backers. Thus, as expected, the indirect (mediated) effects of Rewards on Backers are negative in both types of projects. To determine if these indirect effects are significant, bootstrap confidence intervals at were built with 5000 replications. The results show for social projects and for commercial ones, which confirms Hypothesis H2.b. As can be seen, both indirect effects are statistically significant. Thus, when WTP is included as a mediator, the reduction in the number of backers (caused by an additional reward) is less intensive in a social project than in a commercial project, due to the different intensity of the effect of Rewards on WTP in each type of project. With respect to the OLS regression models, it is worth mentioning the acceptable explanatory capacity of the models with from to .

Therefore, our findings show that the effectiveness of rewards in attracting backers is lower in the commercial projects than in the social projects: the total effect (direct and indirect effects) is 11.3122 in social projects and 5.7991 in commercial projects. Therefore, the project type (social versus commercial) becomes a distinguishing feature to explain the relationship between the reward level and market size in rewards-based crowdfunding.

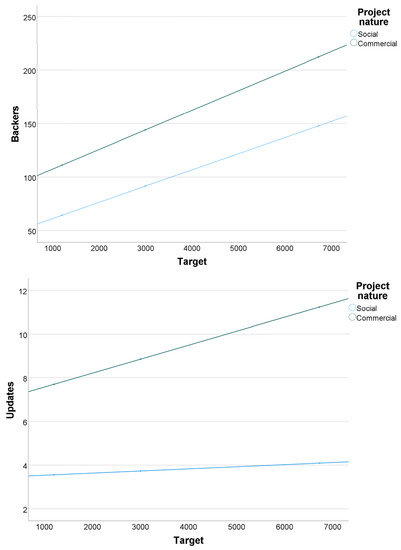

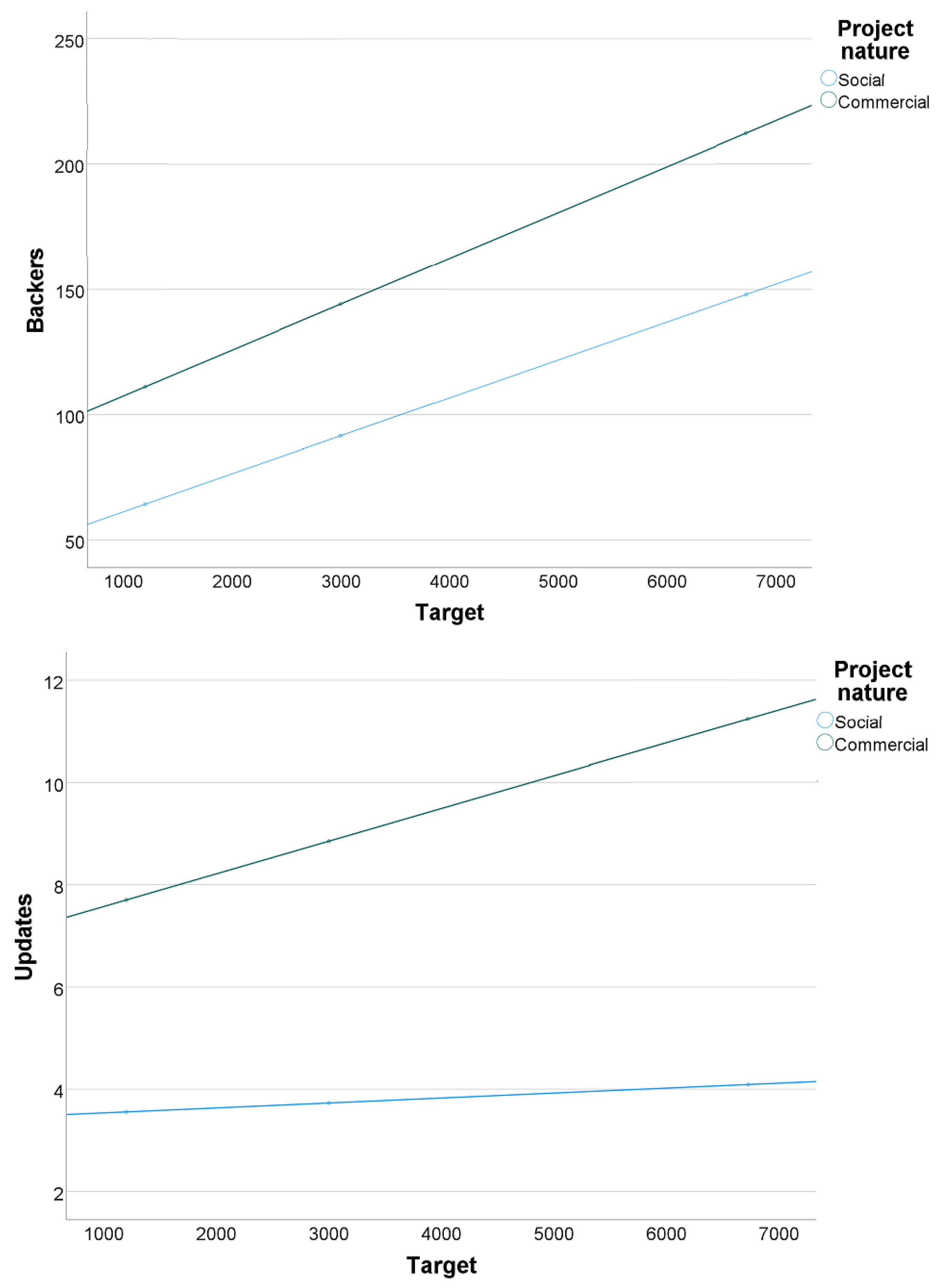

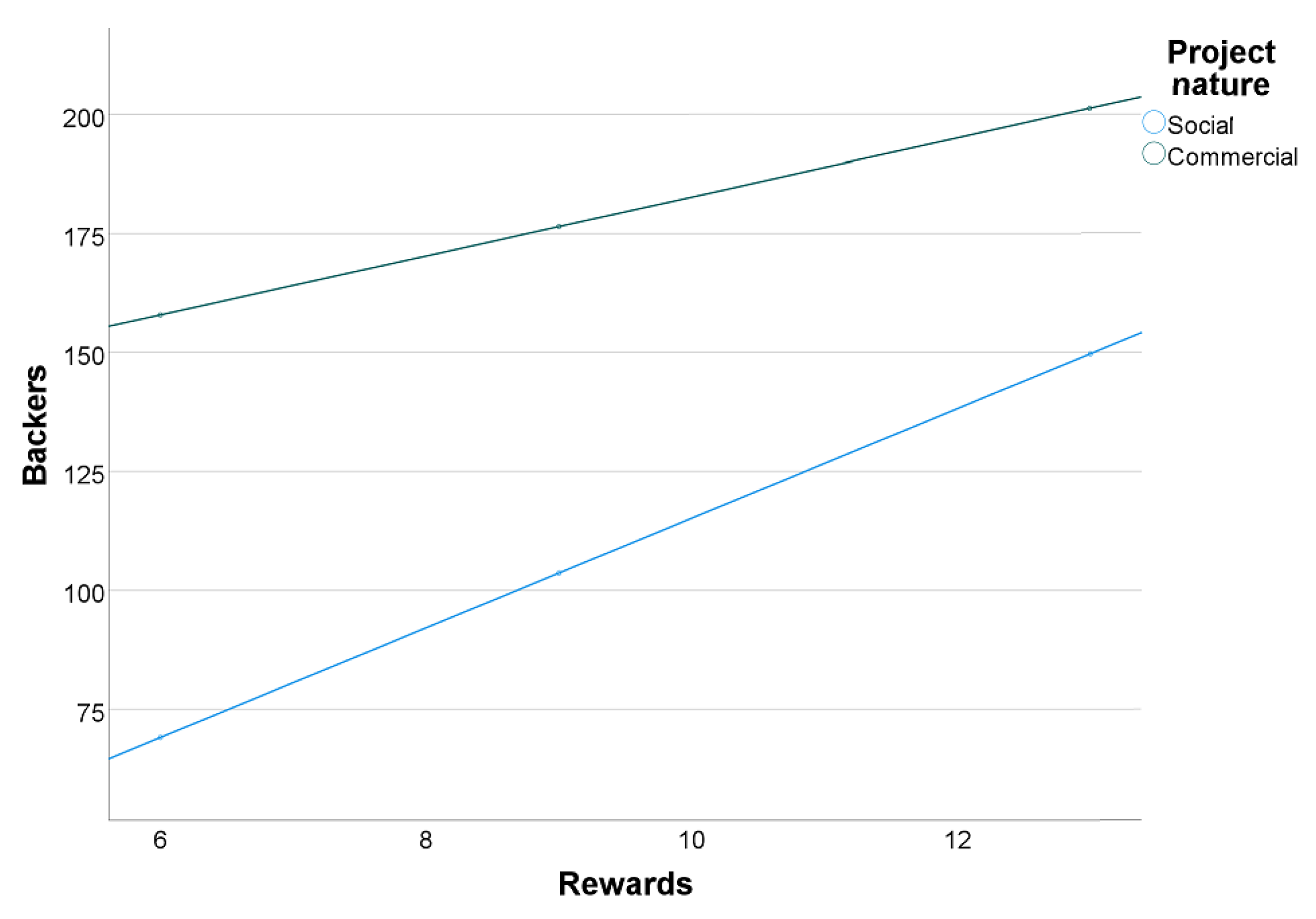

Finally, to illustrate the moderating effects of Project Nature more intuitively, we develop graphs to exhibit the distinguishing effects in Figure 3 and Figure 4. All the graphs shown in Figure 3 and depict three specific values of the variables: the 16th, 50th and 84th percentiles (Hayes [57]). The left graph in Figure 3 displays that the market size of commercial projects is larger than that of social projects, this difference being more pronounced as the target increases. Thus, increasing the funding amount requested will attract crowdfunders to a greater extent in commercial projects, compared to social projects. Furthermore, as shown in the right graph in Figure 3, the increase in the number of updates due to a higher target is much greater in the commercial projects than in the social projects. In other words, the communicating interactions between entrepreneurs and backers become considerably more intense in those commercial projects requesting high funding targets.

Figure 3.

Relationships of Target-Backers and Target-Updates by project type.

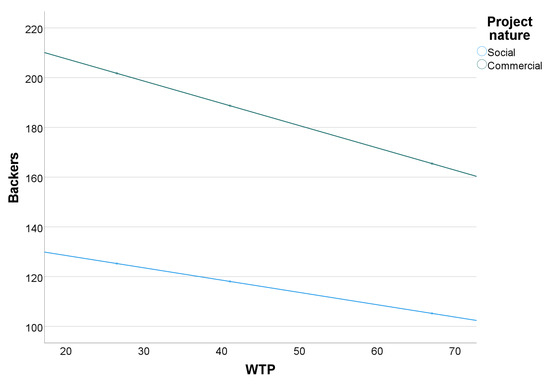

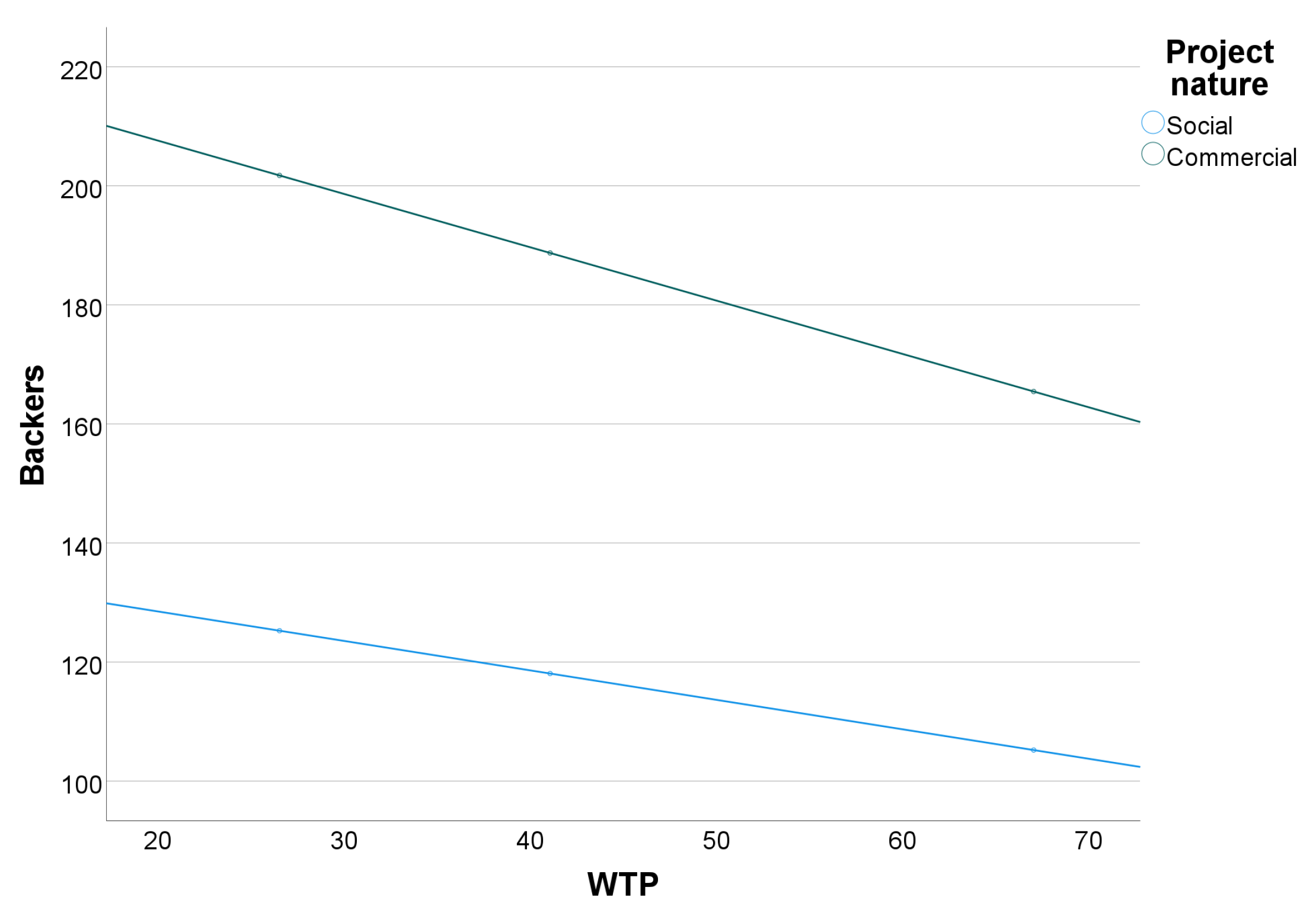

Figure 4.

Relationships of Rewards-Backers and WTP-Backers by project type.

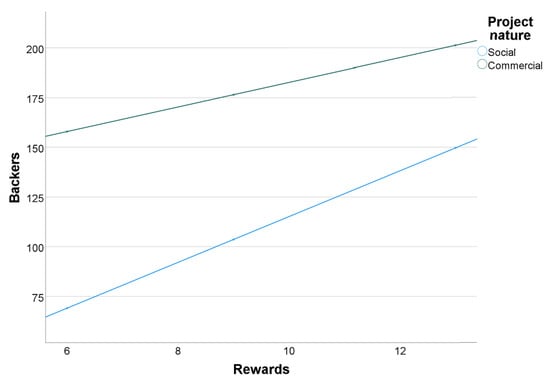

Analogously, the left graph in Figure 4 depicts how the difference in market size between commercial and social projects reduces as the number of reward options increases. Additionally, the rate at which the market size increases as the reward level broadens is much higher in the social projects. Lastly, if we consider the (negative) effect of WTP on Backers plotted on the right graph, it can seen that the market size decreases more quickly in the commercial projects as WTP increases. Notice that the differences in market size between social and commercial projects gradually decrease as projects offer a greater number of rewards and the backers’ WTP is higher.

5. Discussion

In this paper, we focused our attention on the twofold use of rewards-based crowdfunding as a market test for adaptation of production to demand, and as a financing tool. In particular, after analyzing the impact of two campaign features chosen by entrepreneurs (funding target and number of reward options), we studied how (the mediating role of updates and WTP) and when (the moderating role of project nature) these features may determine the success of a fundraising campaign in terms of the number of crowdfunders who support it (market size). This research adds several novel findings to the literature on crowdfunding.

The role of funding target to attract crowdfunders, typically found in previous studies (Devaraj and Patel [19], Chung et al. [20] and Chakraborty and Swinney [8]), is mediated by the level of communication between entrepreneurs and backers. In this regard, part of the increase in market size due to a high target seems to be explained by the positive relationship between the target and the number of updates posted on the campaign website. Furthermore, we also find that such effects do not occur equally in all projects. In projects of a social nature, the attracting role of the target is smaller than in those projects of a commercial nature. This result suggests that the updates may contribute to reduce backers’ uncertainty about the quality of projects. Backers who support commercial projects face the risk of not receiving the product or of delivery delays. Thus, publishing updates during a campaign allows entrepreneurs to provide backers with information to reduce their perceived risk. On the contrary, although backers of projects of a social nature also expect entrepreneurs to fulfill their contractual obligations, their main objective is that the idea or project raises funding enough to be developed, thereby benefiting the social community. Yet, the updates also help backers to reduce their fear of being cheated in social projects; for instance, when there is no real project and the entrepreneur runs away with money.

Our results are consistent with the idea that price discrimination facilitates rent extraction from consumers and increases market size, as the theory predicts. Taking the number of reward options as a proxy for pricing strategy, we have found a positive relationship between the number of rewards and market size. Offering a wider variety of rewards allows to attract low-value backers through low prices and high-value backers through high prices (Ellman and Hurkens [10]). As a novelty, we have also found that such a relationship is mediated by backers’ WTP. While a higher number of rewards increases the WTP, holding all other variables constant, the higher the WTP, the smaller the market size. Therefore, the total effect of an increase in the number of rewards on market size is slightly reduced. Furthermore, our study shows that the negative impact of WTP is more intense for commercial backers than for social backers. As Bürger and Kleinert [41] posited, backers of commercial projects behave similarly to consumers of a product in a market. In this regard, social backers may be less sensitive to prices when they value reward attributes other than a product. These results suggest that, although the market size may be smaller in a social project than in a commercial project (as in our study), the crowd of a social project may value the community impact more highly and, thereby, may be willing to choose highly priced rewards. This is also in line with our previous result regarding that, as the reward level increases, the difference in market size between commercial and social projects reduces. Higher rewards may attract more pro-social people willing to support a social project.

6. Conclusions

This research has also practical implications for the crowdfunding design. Preferences of backers and structure of the crowdfunding industry have moving targets (Calic and Mosakowski [47]). In this regard, our results may facilitate the creation of specific instruments or rules in a platform for the development of social and commercial projects. Our study may also help entrepreneurs who wish to launch a rewards-based crowdfunding campaign. Knowing how the backers’ profile interacts with the campaign features is of great interest for the design of a successful campaign.

Finally, the current study has several limitations, which may support avenues for future research. First, we selected only two types of projects and only one crowdfunding platform. In practice, there exist a great variety of mixed projects in which backers’ profiles are very diverse. It would be interesting to study the behavioral patterns of different profiles that support the same project in order to define optimal funding/commercial strategies in rewards-based crowdfunding. Second, our database is limited in terms of the variables available. In particular, we do not have information on the price range of each project. Another potentially fruitful avenue for future work lies in studying how price dispersion influences the response to funding/commercial strategies by the crowd. Likewise, we only considered campaigns using a fixed funding scheme (the scheme used by Verkami). Yet, understanding how the funding scheme (fixed or flexible) determines the use of a target to attract crowds may provide promising future research on optimal campaign design.

Author Contributions

Conceptualization, F.J.-J. and M.V.A.-F.; methodology, F.J.-J. and M.V.A.-F.; software, C.M.-G., M.V.A.-F. and F.J.-J.; validation, C.M.-G., F.J.-J. and M.V.A.-F.; formal analysis, F.J.-J. and M.V.A.-F.; investigation, F.J.-J., M.V.A.-F. and C.M.-G.; resources, C.M.-G.; data curation, C.M.-G. and F.J.-J.; writing–original draft preparation, F.J.-J. and M.V.A.-F.; writing–review and editing, F.J.-J., M.V.A.-F. and C.M.-G. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Spanish Ministry of Science, Innovation and Universities grant number RTI2018-097620-B-I00 and by University of Jaén (Spain) grant number EI_SEJ05_2021.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon request.

Acknowledgments

The authors thank Susana Torres Moreno for her technical support in the data collection. The authors also acknowledge two anonymous referees for their valuable comments.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Description of variables.

Table A1.

Description of variables.

| Variable | Definition |

|---|---|

| Backers | Market size: number of crowdfunders who support a project |

| Target | Minimum funding target set by the entrepreneurs of a project (in euros) |

| Rewards | Number of reward options offered by the entrepreneurs in a project |

| Updates | Social networks: number of updates published on the campaign’s website |

| WTP | Backers’ willingness-to-pay: total raised amount (in euros) divided by total number of backers |

| Project Nature | Binary where 1 = commercial project; 0 = social project |

| Video | Binary where 1 = the campaign shows a video of the project; 0 = the opposite |

| ECL | Entrepreneurs’ cooperation level: number of other campaigns supported by entrepreneurs |

References

- Agrawal, A.; Catalini, C.; Goldfarb, A. Some Simple Economics of Crowdfunding. Innov. Policy Econ. 2014, 14, 63–97. [Google Scholar] [CrossRef] [Green Version]

- Belleflamme, P.; Lambert, T.; Schwienbacher, A. Crowdfunding: Tapping the right crowd. J. Bus. Ventur. 2014, 29, 585–609. [Google Scholar] [CrossRef] [Green Version]

- Kuppuswamy, V.; Bayus, B.L. A review of crowdfunding research and findings. In Handbook of Research on New Product Development; Golder, P.N., Mitra, D., Eds.; Edward Elgar: Cheltenham, UK, 2018; pp. 361–373. [Google Scholar] [CrossRef]

- Moritz, A.; Block, J.H. Crowdfunding: A Literature Review and Research Directions. In Crowdfunding in Europe: State of the Art in Theory and Practice; Brüntje, D., Gajda, O., Eds.; Springer International Publishing: Cham, Switzerland, 2016; pp. 25–53. [Google Scholar] [CrossRef]

- Strausz, R. A Theory of Crowdfunding: A Mechanism Design Approach with Demand Uncertainty and Moral Hazard. Am. Econ. Rev. 2017, 107, 1430–1476. [Google Scholar] [CrossRef] [Green Version]

- Chemla, G.; Tinn, K. Learning Through Crowdfunding. Manag. Sci. 2020, 66, 1783–1801. [Google Scholar] [CrossRef] [Green Version]

- Chang, J.W. The Economics of Crowdfunding. Am. Econ. J. Microecon. 2020, 12, 257–280. [Google Scholar] [CrossRef]

- Chakraborty, S.; Swinney, R. Signaling to the Crowd: Private Quality Information and Rewards-Based Crowdfunding. Manuf. Serv. Oper. Manag. 2021, 23, 155–169. [Google Scholar] [CrossRef]

- Cornelli, F. Optimal Selling Procedures with Fixed Costs. J. Econ. Theory 1996, 71, 1–30. [Google Scholar] [CrossRef]

- Ellman, M.; Hurkens, S. Optimal crowdfunding design. J. Econ. Theory 2019, 184, 104939. [Google Scholar] [CrossRef] [Green Version]

- Mollick, E. The Dynamics of Crowdfunding: An Exploratory Study. J. Bus. Ventur. 2014, 29, 1–16. [Google Scholar] [CrossRef] [Green Version]

- Belavina, E.; Marinesi, S.; Tsoukalas, G. Rethinking Crowdfunding Platform Design: Mechanisms to Deter Misconduct and Improve Efficiency. Manag. Sci. 2020, 66, 4980–4997. [Google Scholar] [CrossRef]

- Sayedi, A.; Baghaie, M. Crowdfunding as a Marketing Tool. SSRN Electron. J. 2017. [Google Scholar] [CrossRef]

- Parker, S.C. Crowdfunding, cascades and informed investors. Econ. Lett. 2014, 125, 432–435. [Google Scholar] [CrossRef] [Green Version]

- Schwienbacher, A. Entrepreneurial risk-taking in crowdfunding campaigns. Small Bus. Econ. 2018, 51, 843–859. [Google Scholar] [CrossRef]

- Hakenes, H.; Schlegel, F. Exploiting the Financial Wisdom of the Crowd—Crowdfunding as a Tool to Aggregate Vague Information. SSRN Electron. J. [CrossRef]

- Frydrych, D.; Bock, A.J.; Kinder, T.; Koeck, B. Exploring entrepreneurial legitimacy in reward-based crowdfunding. Ventur. Cap. 2014, 16, 247–269. [Google Scholar] [CrossRef]

- Dikaputra, R.; Sulung, L.A.K.; Kot, S. Analysis of Success Factors of Reward-Based Crowdfunding Campaigns Using Multi-Theory Approach in ASEAN-5 Countries. Soc. Sci. 2019, 8, 293. [Google Scholar] [CrossRef] [Green Version]

- Devaraj, S.; Patel, P.C. Influence of number of backers, goal amount, and project duration on meeting funding goals of crowdfunding projects. Econ. Bull. 2016, 36, 1242–1249. [Google Scholar]

- Chung, Y.; Li, Y.; Jia, J. Exploring embeddedness, centrality, and social influence on backer behavior: The role of backer networks in crowdfunding. J. Acad. Mark. Sci. 2021, 49, 925–946. [Google Scholar] [CrossRef]

- Kumar, P.; Langberg, N.; Zvilichovsky, D. (Crowd)Funding Innovation: Financing Constraints, Price Discrimination and Welfare. SSRN Electron. J. 2016. [Google Scholar] [CrossRef]

- Thürridl, C.; Kamleitner, B. What Goes Around Comes Around? Rewards as Strategic Assets in Crowdfunding. Calif. Manag. Rev. 2016, 58, 88–110. [Google Scholar] [CrossRef]

- Hu, M.; Li, X.; Shi, M. Product and Pricing Decisions in Crowdfunding. SSRN Electron. J. 2014, 34, 331–345. [Google Scholar] [CrossRef]

- Crosetto, P.; Regner, T. It’s never too late: Funding dynamics and self pledges in reward-based crowdfunding. Res. Policy 2018, 47, 1463–1477. [Google Scholar] [CrossRef] [Green Version]

- Koch, J.A. The Phenomenon of Project Overfunding on Online Crowdfunding Platforms—Analyzing the Drivers of Overfunding. In Proceedings of the Twenty-Fourth European Conference on Information Systems, Istanbul, Turkey, 12–15 June 2016. [Google Scholar]

- Bi, S.; Liu, Z.; Usman, K. The influence of online information on investing decisions of reward-based crowdfunding. J. Bus. Res. 2017, 71, 10–18. [Google Scholar] [CrossRef]

- Ahlers, G.K.; Cumming, D.; Günther, C.; Schweizer, D. Signaling in Equity Crowdfunding. Entrep. Theory Pract. 2015, 39, 955–980. [Google Scholar] [CrossRef]

- André, K.; Bureau, S.; Rubel, O.; Gautier, A. Beyond the Opposition between Altruism and Self-Interest: Reciprocal Giving in Reward-Based Crowdfunding. J. Bus. Ethics 2017, 146, 313–332. [Google Scholar] [CrossRef]

- Kuppuswamy, V.; Bayus, B. Crowdfunding Creative Ideas: The Dynamics of Project Backers in Kickstarter. SSRN Electron. J. 2013, 151–182. [Google Scholar] [CrossRef] [Green Version]

- Butticè, V.; Colombo, M.G.; Wright, M. Serial Crowdfunding, Social Capital, and Project Success. Entrep. Theory Pract. 2017, 41, 183–207. [Google Scholar] [CrossRef]

- Kuppuswamy, V.; Bayus, B.L. Does my contribution to your crowdfunding project matter? J. Bus. Ventur. 2017, 32, 72–89. [Google Scholar] [CrossRef]

- Kromidha, E.; Robson, P. Social identity and signalling success factors in online crowdfunding. Entrep. Reg. Dev. 2016, 28, 605–629. [Google Scholar] [CrossRef] [Green Version]

- Skirnevskiy, V.; Bendig, D.; Brettel, M. The Influence of Internal Social Capital on Serial Creators’ Success in Crowdfunding. Entrep. Theory Pract. 2017, 41, 209–236. [Google Scholar] [CrossRef]

- Gerber, E.; Hui, J.; Kuo, P.Y.P. Crowdfunding: Why People are Motivated to Post and Fund Projects on Crowdfunding Platforms. In Proceedings of the International Workshop on Design, Influence, and Social Technologies: Techniques, Impacts and Ethics; ACM: New York, NY, USA, 2012; Volume 10. [Google Scholar]

- Cai, Z.; Zhang, P.; Han, X. The inverted U-shaped relationship between crowdfunding success and reward options and the moderating effect of price differentiation. China Financ. Rev. Int. 2020. [Google Scholar] [CrossRef]

- Hobbs, J.; Grigore, G.; Molesworth, M. Success in the management of crowdfunding projects in the creative industries. Internet Res. 2016, 26, 146–166. [Google Scholar] [CrossRef] [Green Version]

- Antonenko, P.P.; Lee, B.R.; Kleinheksel, A.J. Trends in the crowdfunding of educational technology startups. TechTrends 2014, 58, 36–41. [Google Scholar] [CrossRef]

- Ryu, S.; Kim, Y.G. A typology of crowdfunding sponsors: Birds of a feather flock together? Electron. Commer. Res. Appl. 2016, 16, 43–54. [Google Scholar] [CrossRef]

- Younkin, P.; Kashkooli, K. A Crowd or a Community? Comparing Three Explanations for the Decision to Donate to a Crowdfunding Project. In Proceedings of the Berkeley Crowdfunding Conference, Berkeley, CA, USA, 9 June 2013. [Google Scholar]

- Gerber, L.; Hui, J. Crowdfunding: How and Why People Participate. In International Perspectives on Crowdfunding; Emerald Group Publishing Limited: Bingley, UK, 2016; pp. 37–64. [Google Scholar] [CrossRef]

- Bürger, T.; Kleinert, S. Crowdfunding cultural and commercial entrepreneurs: An empirical study on motivation in distinct backer communities. Small Bus. Econ. 2020, 57, 667–683. [Google Scholar] [CrossRef]

- Rodriguez-Ricardo, Y.; Sicilia, M.; López, M. What drives crowdfunding participation? The influence of personal and social traits. Span. J. Mark.-ESIC 2018, 22, 163–182. [Google Scholar] [CrossRef] [Green Version]

- Lin, Y.; Lee, W.C.; Chang, C.C. Analysis of rewards on reward-based crowdfunding platforms. In Proceedings of the 2016 IEEE/ACM International Conference on Advances in Social Networks Analysis and Mining (ASONAM), San Francisco, CA, USA, 18–21 August 2016; pp. 501–504. [Google Scholar] [CrossRef]

- Dai, H.; Zhang, D.J. Prosocial Goal Pursuit in Crowdfunding: Evidence from Kickstarter. J. Mark. Res. 2019, 56, 498–517. [Google Scholar] [CrossRef]

- Hong, Y.; Hu, Y.; Burtch, G. Embeddedness, prosociality, and social influence: Evidence from online crowdfunding. MIS Q. Manag. Inf. Syst. 2018, 42, 1211–1224. [Google Scholar] [CrossRef]

- Allison, T.; Davis, B.; Short, J.; Webb, J. Crowdfunding in a Prosocial Microlending Environment: Examining the Role of Intrinsic Versus Extrinsic Cues. Entrep. Theory Pract. 2014, 39, 53–73. [Google Scholar] [CrossRef]

- Calic, G.; Mosakowski, E. Kicking Off Social Entrepreneurship: How A Sustainability Orientation Influences Crowdfunding Success. J. Manag. Stud. 2016, 53, 738–767. [Google Scholar] [CrossRef]

- Pitschner, S.; Pitschner-Finn, S. Non-profit differentials in crowd-based financing: Evidence from 50,000 campaigns. Econ. Lett. 2014, 123, 391–394. [Google Scholar] [CrossRef] [Green Version]

- González, A.; Ramos, J. Financiación Participativa (Crowdfunding) en España 2020. El Año de la Gran Prueba; Technical Report. Universo Crowdfunding. Available online: https://www.universocrowdfunding.com/datos-crowdfunding-espana/ (accessed on 15 August 2021).

- Roodink, C.; Kleverlaan, R. Current State of Crowdfunding in Europe an Overview of the Crowdfunding Industry in More Than 25 Countries: Trends, Volumes y Regulations; Technical Report; CrowdfundingHub: Amsterdam, The Netherlands, 2016. [Google Scholar]

- Parhankangas, A.; Renko, M. Linguistic style and crowdfunding success among social and commercial entrepreneurs. J. Bus. Ventur. 2017, 32, 215–236. [Google Scholar] [CrossRef]

- Gorbatai, A.; Nelson, L. The Narrative Advantage: Gender and the Language of Crowdfunding. Acad. Manag. Annu. Meet. Proc. 2015, 1. [Google Scholar] [CrossRef]

- Barbi, M.; Bigelli, M. Crowdfunding practices in and outside the US. Res. Int. Bus. Financ. 2017, 42, 208–223. [Google Scholar] [CrossRef]

- Courtney, C.; Dutta, S.; Li, Y. Resolving Information Asymmetry: Signaling, Endorsement, and Crowdfunding Success. Entrep. Theory Pract. 2017, 41, 265–290. [Google Scholar] [CrossRef]

- Colombo, M.G.; Franzoni, C.; Rossi-Lamastra, C. Internal Social Capital and the Attraction of Early Contributions in Crowdfunding. Entrep. Theory Pract. 2015, 39, 75–100. [Google Scholar] [CrossRef]

- Zheng, H.; Li, D.; Wu, J.; Xu, Y. The role of multidimensional social capital in crowdfunding: A comparative study in China and US. Inf. Manag. 2014, 51, 488–496. [Google Scholar] [CrossRef]

- Hayes, A. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach, 2nd ed.; The Guildford Press: New York, NY, USA, 2018. [Google Scholar]

- Pollack, J.; VanEpps, E.; Hayes, A. The Moderating Role of Social Ties on Entrepreneurs’ Depressed Affect and Withdrawal Intentions in Response to Economic Stress. J. Organ. Behav. 2012, 3, 76–86. [Google Scholar] [CrossRef]

- Liu, J.; Kwan, H.K.; Wu, L.z.; Wu, W. Abusive supervision and subordinate supervisor-directed deviance: The moderating role of traditional values and the mediating role of revenge cognitions. J. Occup. Organ. Psychol. 2011, 83, 835–856. [Google Scholar] [CrossRef]

- Wu, J.; Ma, Z.; Liu, Z. The moderated mediating effect of international diversification, technological capability, and market orientation on emerging market firms’ new product performance. J. Bus. Res. 2019, 99, 524–533. [Google Scholar] [CrossRef]