Pricing and Emission Reduction Strategies of Heterogeneous Automakers Under the “Dual-Credit + Carbon Cap-and-Trade” Policy Scenario

Abstract

1. Introduction

2. Materials and Methods

2.1. Research on Dual-Credit and Cap-and-Trade Policies

2.2. Impacts of Low-Carbon Policies on Automotive Supply Chains

2.3. Production and Emission Reduction Decisions of Automakers in Monopoly Markets

3. Problem Description and Model Assumptions

3.1. Problem Description

3.2. Model Assumptions

4. Model Construction and Solution

4.1. Model 1: Monopoly Model Under the Single Dual-Credit Policy

4.2. Model 2: Monopoly Model Under the “Dual-Credit + Carbon Cap-and-Trade” Policy

5. Model Analysis

5.1. Impact Analysis of Dual-Credit Policy Factors

- (1)

- Impact of an increase in the NEV credit ratio requirement on fuel vehicle pricing:

- (2)

- Impact of an increase in the NEV credit ratio requirement on profits:

- (3)

- Impact of dual-credit policy factors on emission reduction investment strategies:

- (a)

- When , ; When , ;

- (b)

- When , ; When , ;

- (c)

- ; .

5.2. Impact Analysis of Carbon Trading Policy Factors

- (1)

- Impact of an increase in the unit carbon trading price on optimal pricing:

- (2)

- Impact of carbon trading policy factors on profits:

- (3)

- Impact of carbon trading policy factors on emission reduction investment strategies

5.3. Comparative Analysis of Two Carbon Policy Combinations

6. Numerical Simulations

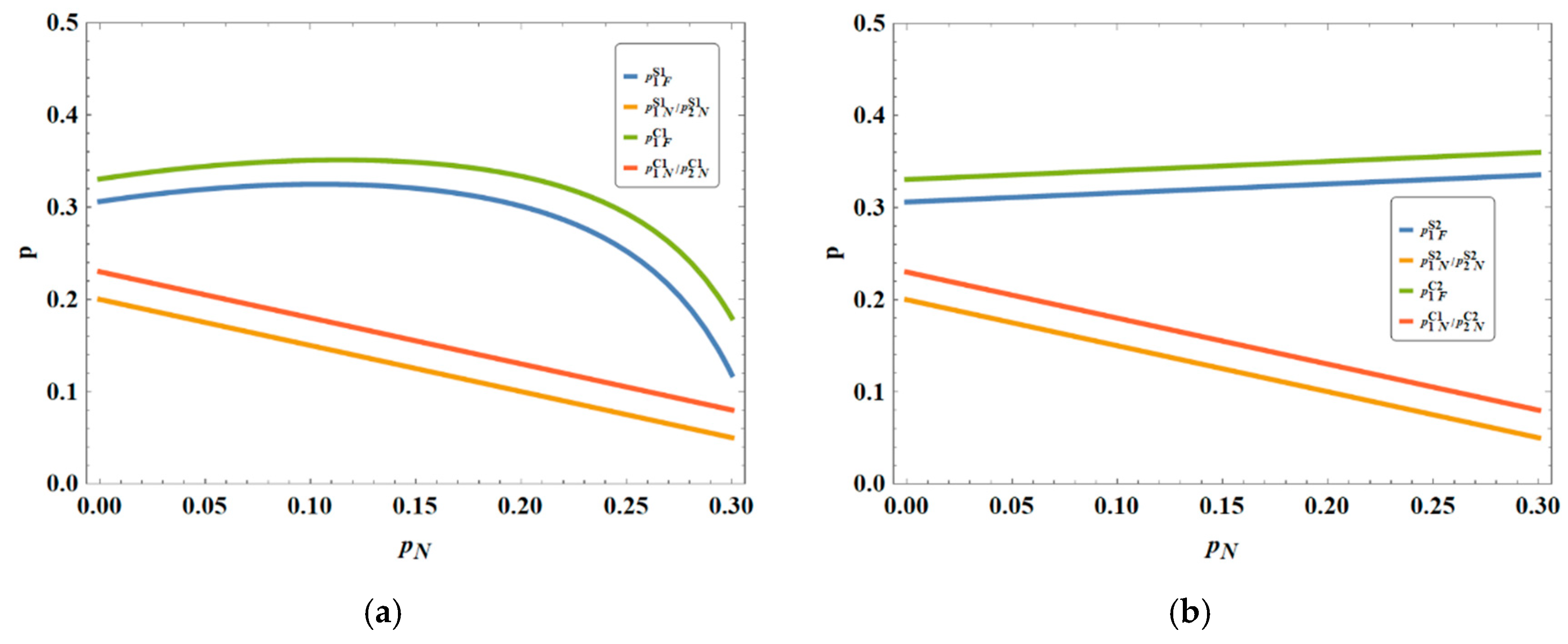

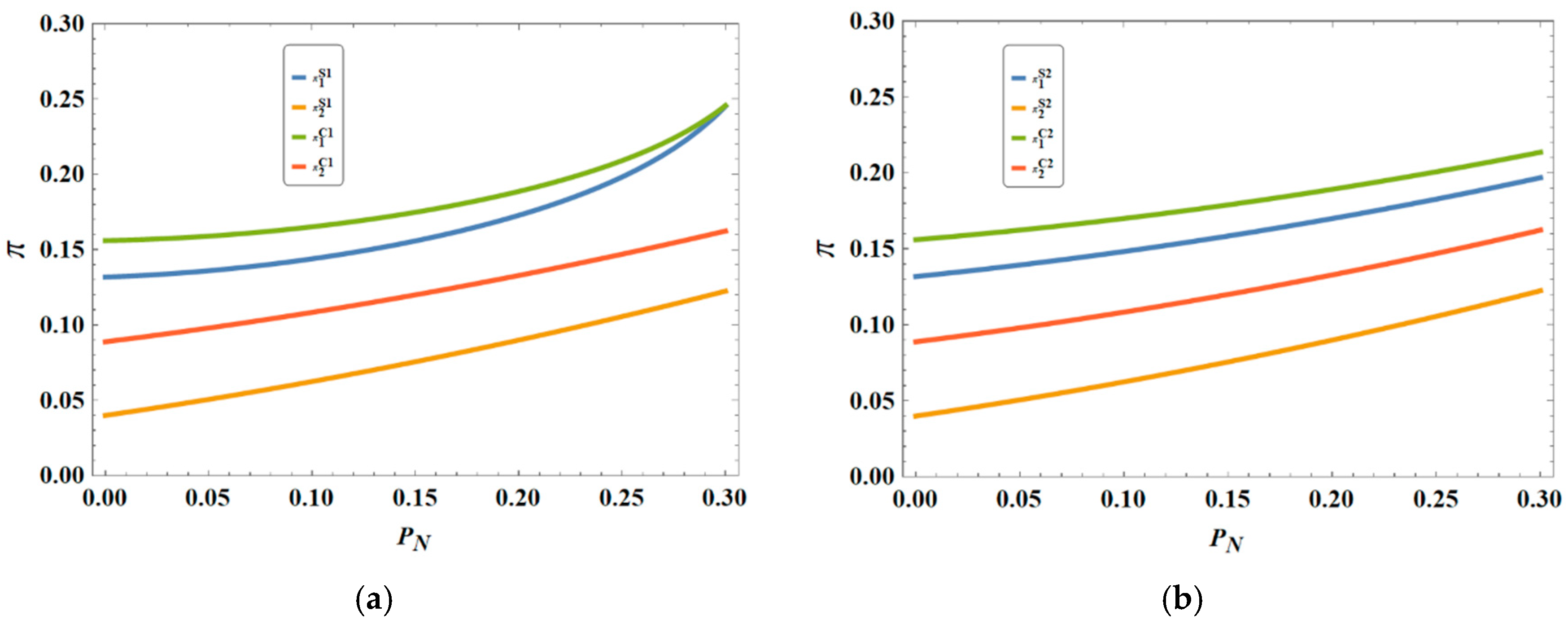

6.1. Impact of NEV Credit Trading Price

6.2. Impact of NEV Credit Ratio Requirement

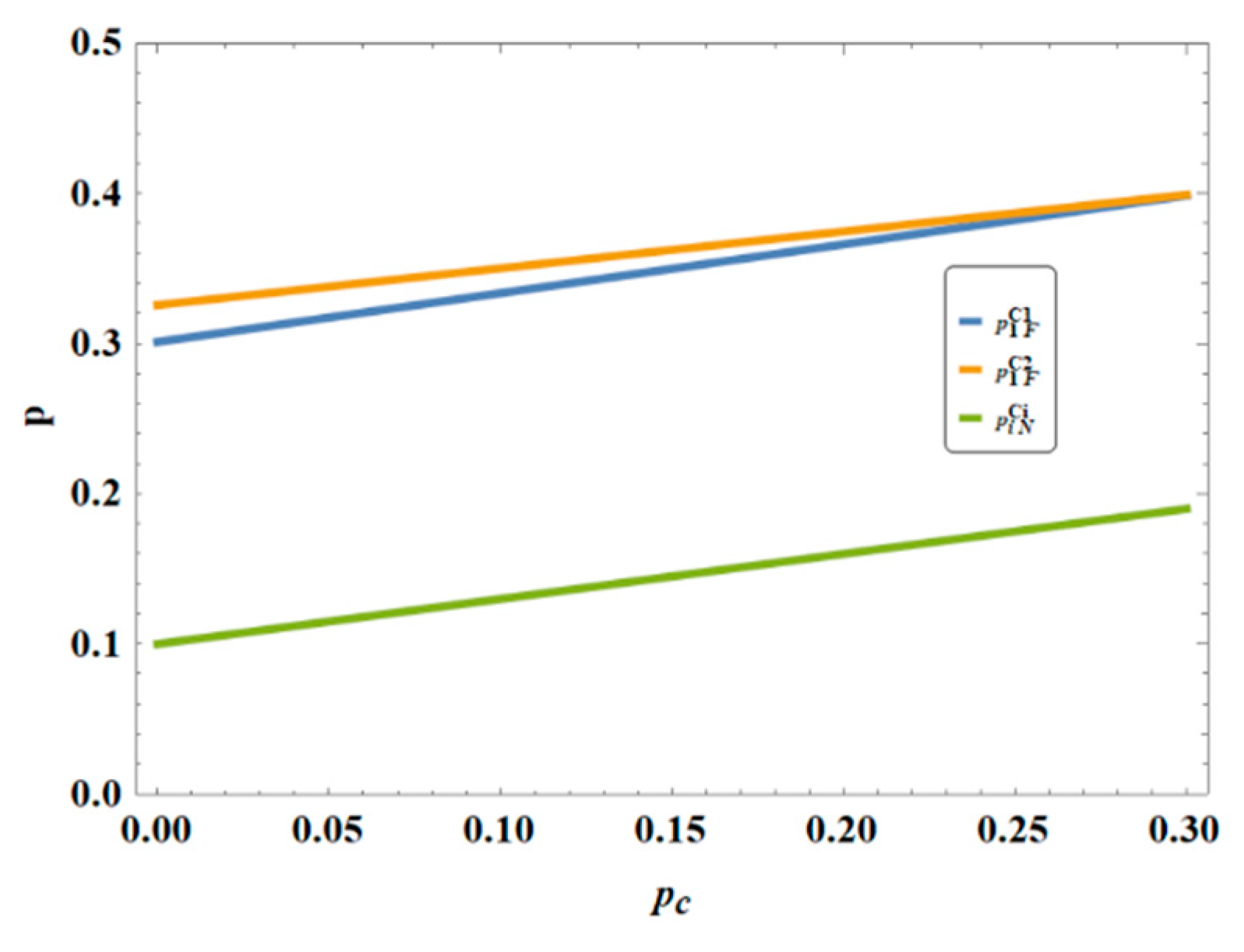

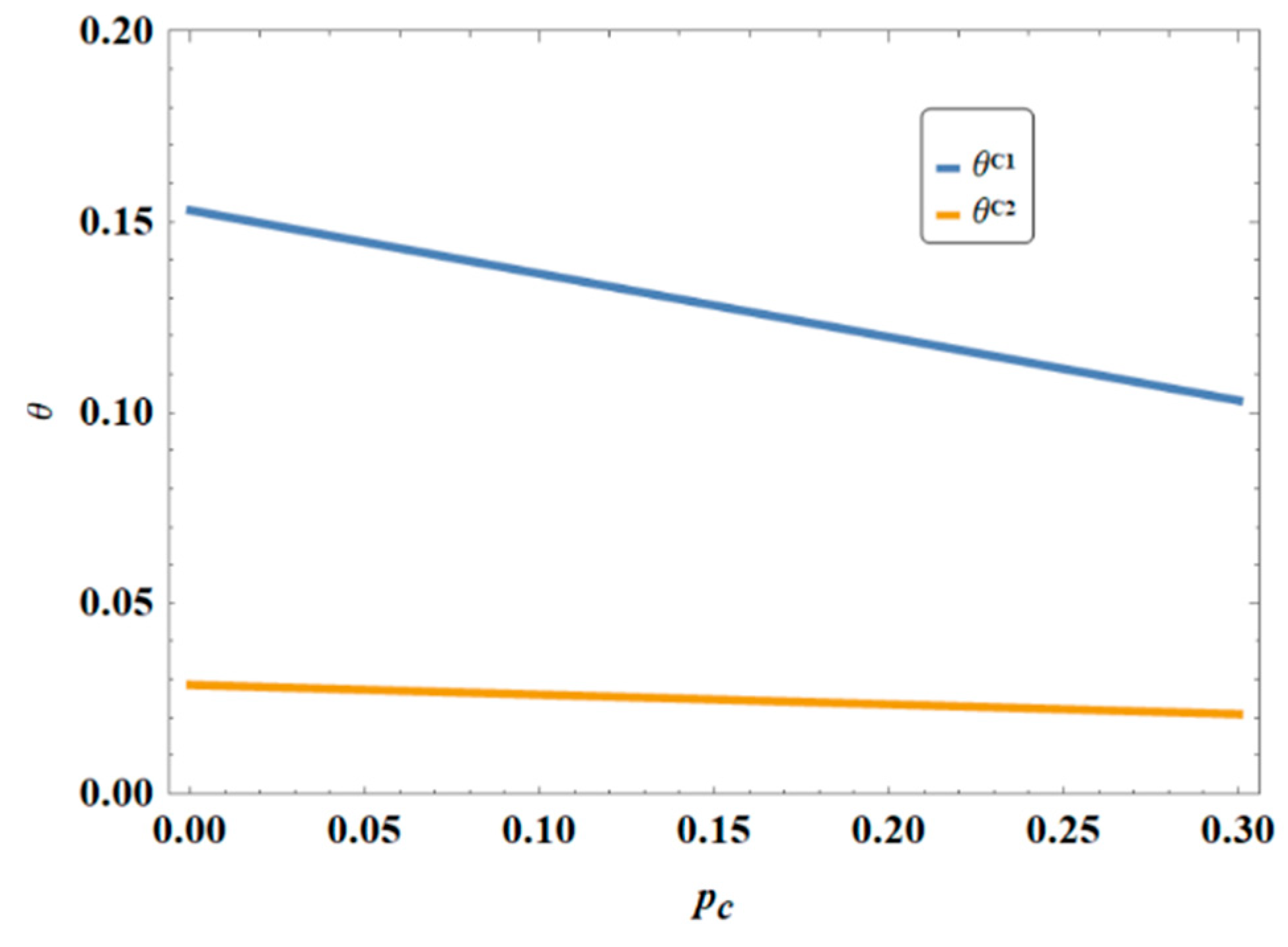

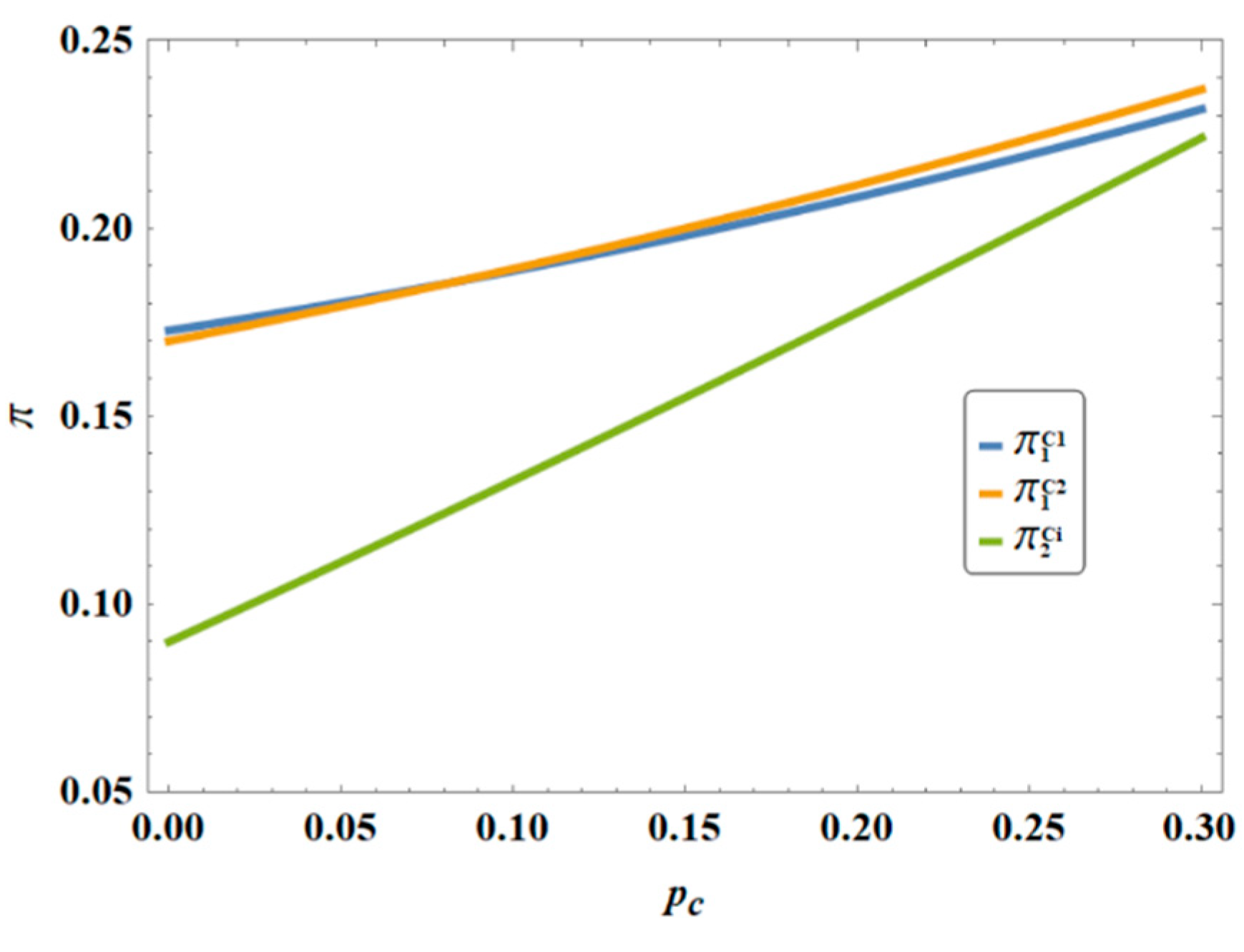

6.3. Impact of Carbon Trading Price

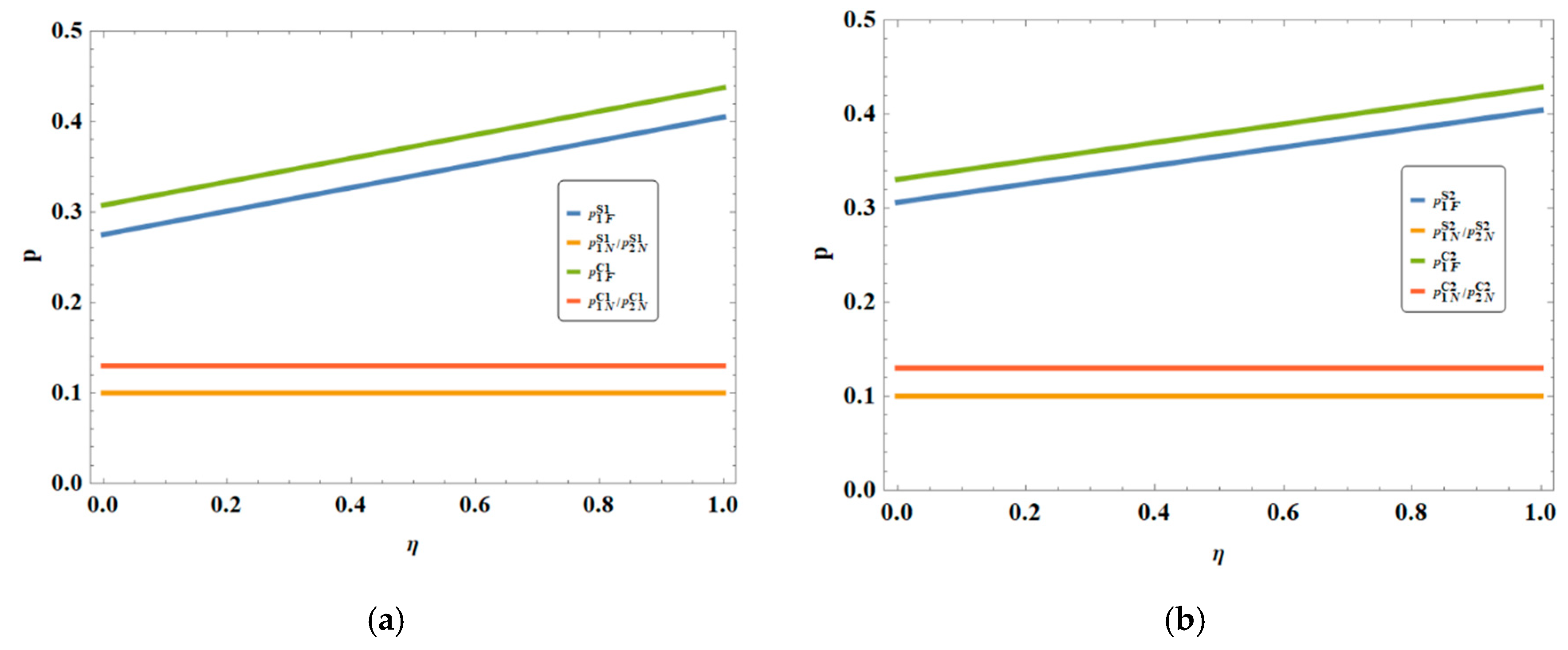

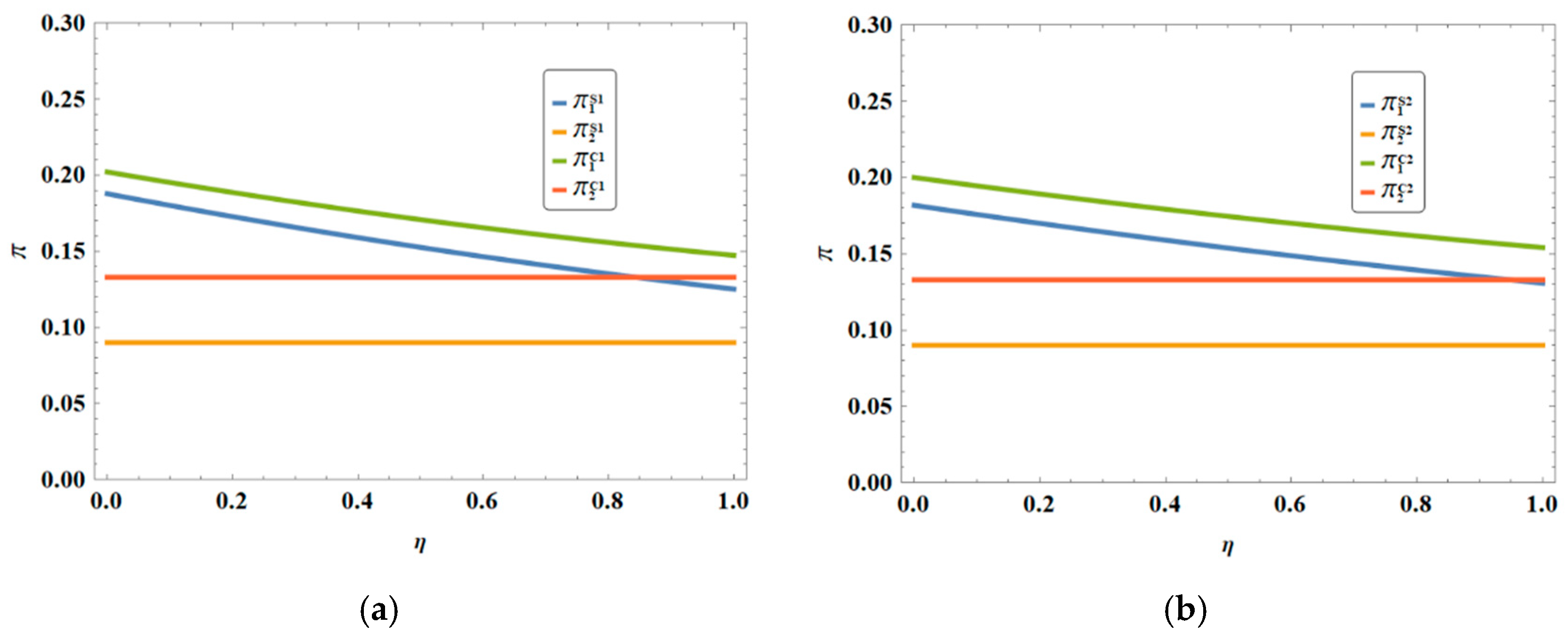

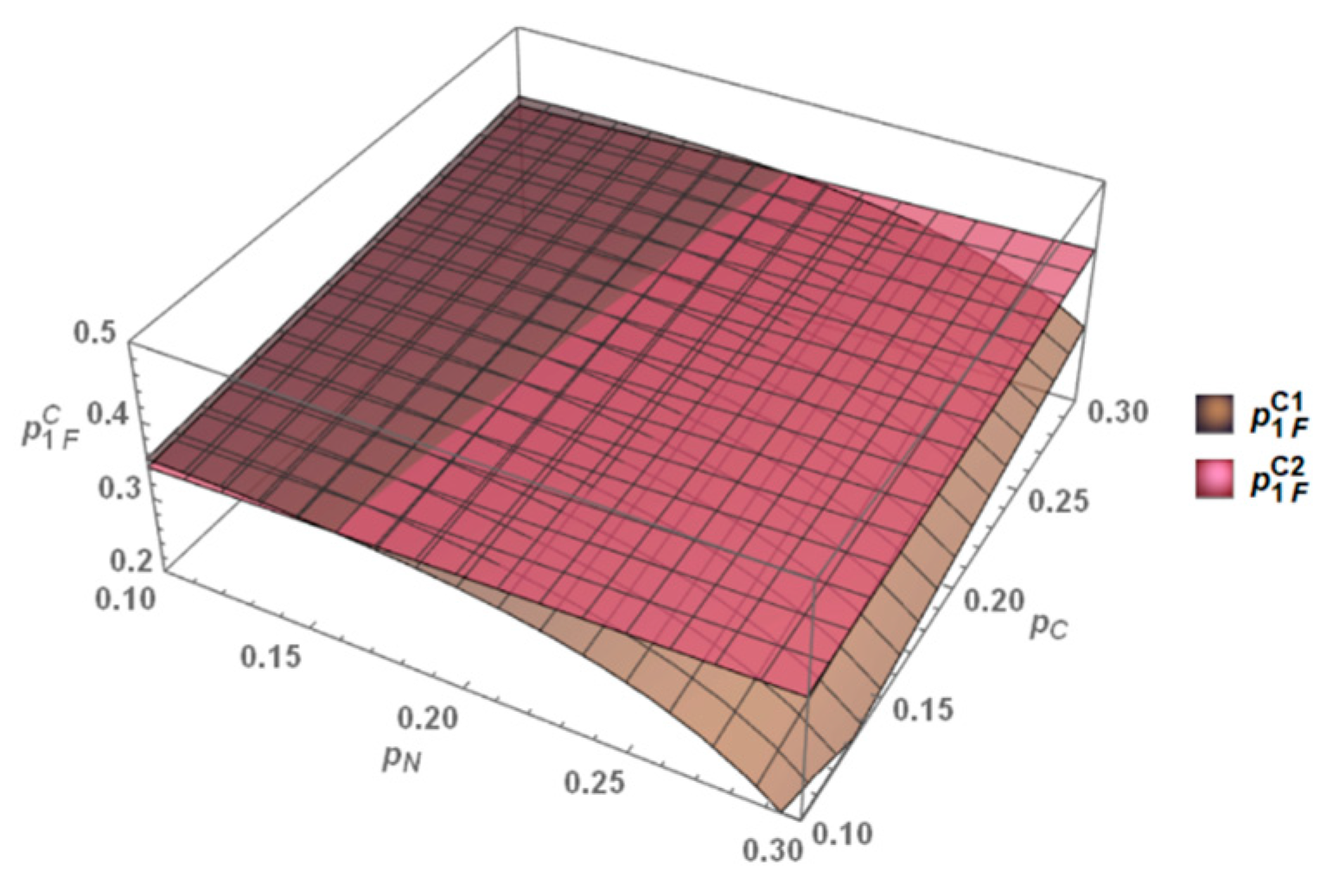

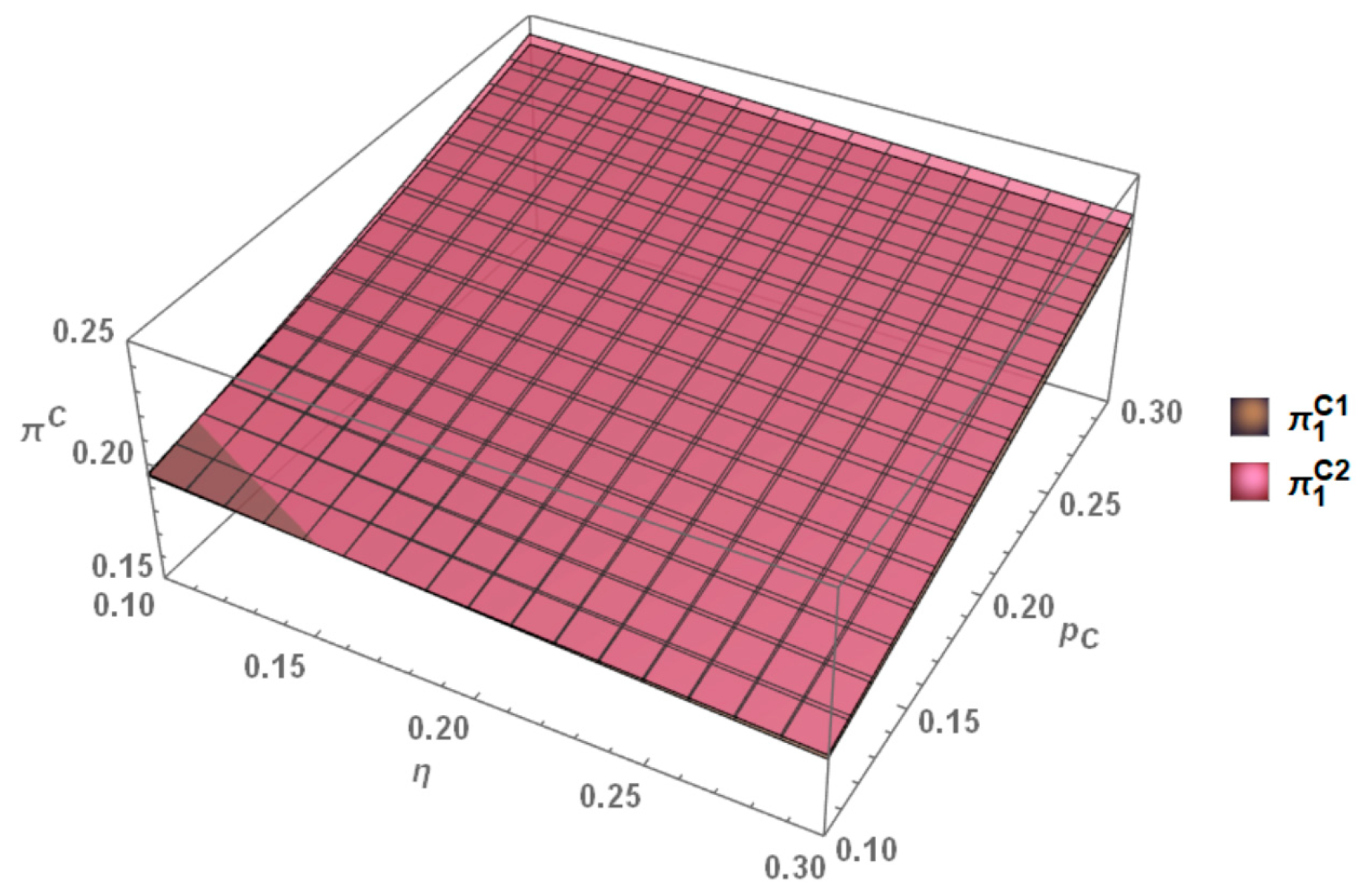

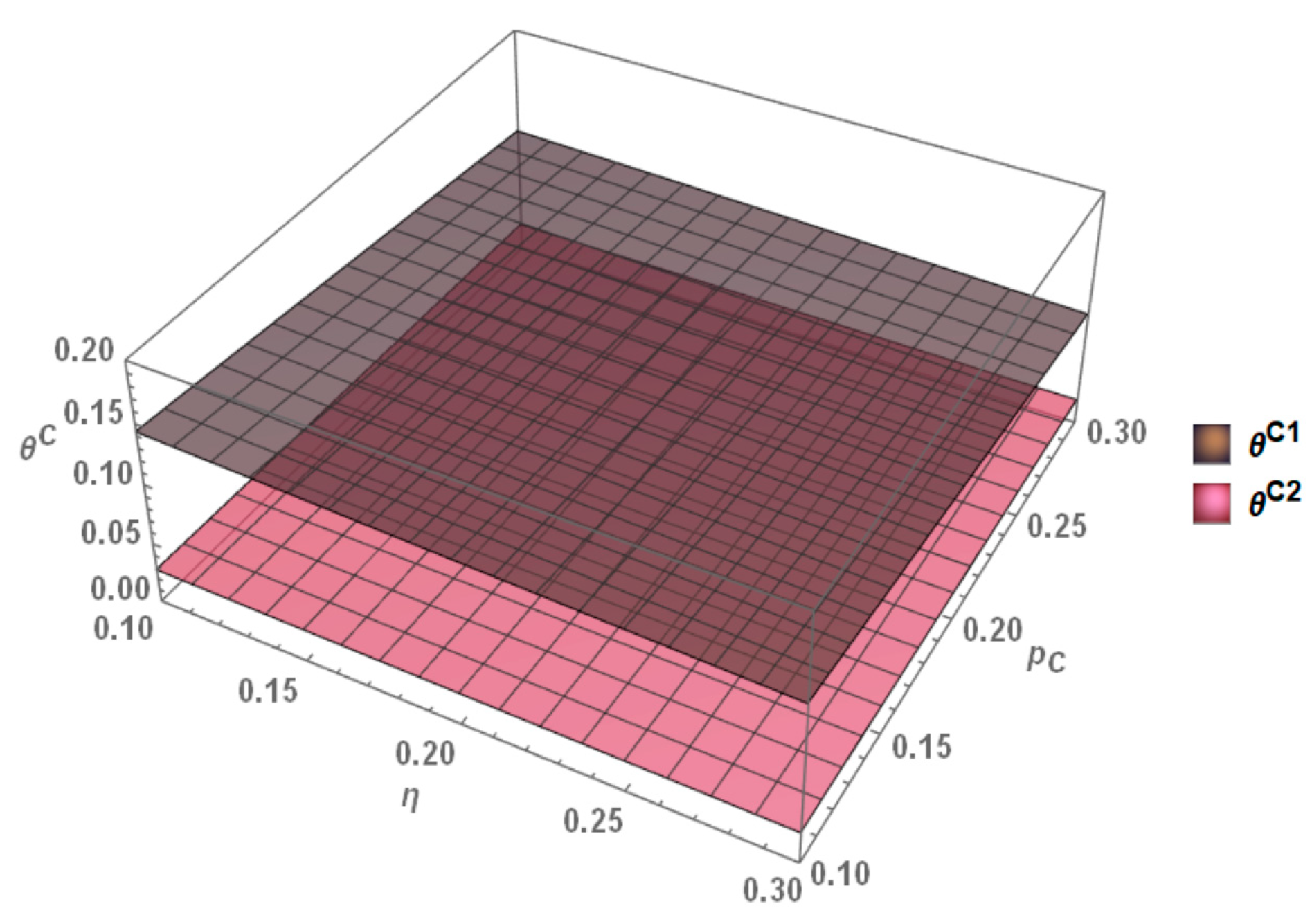

6.4. Interaction Effects of Policy Factors

- (1)

- Interactive Impact of Policy Factors on Pricing

- (2)

- The Interaction Effects of Policy Factors on Profits

- (3)

- The Interaction Effects of Policy Factors on Emission Reduction Effort Level

7. Discussion and Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. The Value of

Appendix B. The Value of

Appendix C. The Value of

Appendix D. Proof of Proposition 5

Appendix E. Proof of Proposition 6

Appendix F. Proof of Proposition 7

Appendix G. Proof of Proposition 8

Appendix H. Proof of Proposition 9

Appendix I. Proof of Proposition 10

Appendix J. Proof of Proposition 11

Appendix K. Proof of Proposition 12

Appendix L. Proof of Proposition 13

Appendix M. Proof of Proposition 14

Appendix N. Proof of Proposition 15

Appendix O. Proof of Proposition 16

References

- Jia, T.; Li, C.; Wang, H.; Hu, Y.-J.; Wang, S.; Xu, G.; Hoang, A.T. Subsidy policy or dual-credit policy? Evolutionary game analysis of green methanol vehicles promotion. Energy 2024, 293, 130763. [Google Scholar] [CrossRef]

- He, H.; Li, S.; Wang, S.; Zhang, C.; Ma, F. Value of dual-credit policy: Evidence from green technology innovation efficiency. Transp. Policy 2023, 139, 182–198. [Google Scholar] [CrossRef]

- Yu, H.; Li, Y.; Wang, W. Optimal innovation strategies of automakers with market competition under the dual-credit policy. Energy 2023, 283, 128403. [Google Scholar] [CrossRef]

- Shi, L.; Lin, B. The dual-credit policy effectively replaces subsidy from the perspective of R&D intensity. Environ. Impact Assess. Rev. 2023, 102, 107160. [Google Scholar]

- Pu, J.; Chun, W.; Yang, H. Low carbon strategy and coordination for a two-echelon automotive supply chain considering dual credit policy. Comput. Ind. Eng. 2024, 192, 110229. [Google Scholar] [CrossRef]

- Goulder, L.H.; Schein, A.R. Carbon taxes versus cap and trade: A critical review. Clim. Change Econ. 2013, 4, 1350010. [Google Scholar] [CrossRef]

- Li, Y.; Zhang, L.; Liu, J.; Qiao, X. Can the dual-credit policy help china’s new energy vehicle industry achieve corner overtaking? Sustainability 2023, 15, 2406. [Google Scholar] [CrossRef]

- Peng, L.; Li, Y. Policy evolution and intensity evaluation of the Chinese new energy vehicle industry policy: The angle of the dual-credit policy. World Electr. Veh. J. 2022, 13, 90. [Google Scholar] [CrossRef]

- Ou, S.; Lin, Z.; Qi, L.; Li, J.; He, X.; Przesmitzki, S. The dual-credit policy: Quantifying the policy impact on plug-in electric vehicle sales and industry profits in China. Energy Policy 2018, 121, 597–610. [Google Scholar] [CrossRef]

- Cheng, Y.; Mu, D. Optimal production decision of vehicle manufacturer based on double-score system. Syst. Eng. Theory Pract. 2018, 38, 2817–2830. [Google Scholar]

- Chen, K.; Zhao, F.; Hao, H.; Liu, Z. Synergistic impacts of China’s subsidy policy and new energy vehicle credit regulation on the technological development of battery electric vehicles. Energies 2018, 11, 3193. [Google Scholar] [CrossRef]

- Cheng, L.; Huang, P.; Zhang, M.; Yang, R.; Wang, Y. Optimizing Electricity Markets Through Game-Theoretical Methods: Strategic and Policy Implications for Power Purchasing and Generation Enterprises. Mathematics 2025, 13, 373. [Google Scholar] [CrossRef]

- Chaabane, A.; Ramudhin, A.; Paquet, M. Design of sustainable supply chains under the emission trading scheme. Int. J. Prod. Econ. 2012, 135, 37–49. [Google Scholar] [CrossRef]

- Drake, D.; Kleindorfer, P.R.; Van Wassenhove, L.N. Technology choice and capacity portfolios under emissions regulation. Prod. Oper. Manag. 2016, 25, 1006–1025. [Google Scholar] [CrossRef]

- Song, J.; Leng, M. Analysis of the single-period problem under carbon emissions policies. In Handbook of Newsvendor Problems: Models, Extensions and Applications; Springer: New York, NY, USA, 2012; pp. 297–313. [Google Scholar]

- Wang, Z.; Wu, Q. Carbon emission reduction and product collection decisions in the closed-loop supply chain with cap-and-trade regulation. Int. J. Prod. Res. 2021, 59, 4359–4383. [Google Scholar] [CrossRef]

- Zhang, T.; Hao, Y.; Zhu, X. Consignment inventory management in a closed-loop supply chain for deteriorating items under a carbon cap-and-trade regulation. Comput. Ind. Eng. 2022, 171, 108410. [Google Scholar] [CrossRef]

- Gong, B.; Xia, X.; Cheng, J. Supply-chain pricing and coordination for new energy vehicles considering heterogeneity in consumers’ low carbon preference. Sustainability 2020, 12, 1306. [Google Scholar] [CrossRef]

- Yi, Y.; Fu, A.; Zhang, S.; Li, Y. Dynamic pricing and joint carbon reduction strategies at the production and consumption end in a dual-channel fuel vehicle supply chain. Energy Econ. 2024, 131, 107396. [Google Scholar] [CrossRef]

- Yi, Y.; Fu, A.; Zhang, M.; Li, Y. Dynamic gaming strategies about fuel consumption reduction and mileage range between two heterogeneous automotive supply chains. Environ. Dev. Sustain. 2025, 1–30. [Google Scholar] [CrossRef]

- Cheng, Y.; Fan, T.; Zhou, L. Optimal strategies of automakers with demand and credit price disruptions under the dual-credit policy. J. Manag. Sci. Eng. 2022, 7, 453–472. [Google Scholar] [CrossRef]

- Li, Y.; Zhang, Q.; Tang, Y.; Mclellan, B.; Ye, H.; Shimoda, H.; Ishihara, K. Dynamic optimization management of the dual-credit policy for passenger vehicles. J. Clean. Prod. 2020, 249, 119384. [Google Scholar] [CrossRef]

- Ma, M.; Meng, W.; Huang, B.; Li, Y. The influence of dual credit policy on new energy vehicle technology innovation under demand forecast information asymmetry. Energy 2023, 271, 127106. [Google Scholar] [CrossRef]

- Yi, Y.; Zhang, M.; Zhang, A.; Li, Y. Can “dual credit” replace “subsidies” successfully? -based on analysis of vehicle supply chain decisions under the digital transformation of technology. Energy Econ. 2024, 130, 107303. [Google Scholar] [CrossRef]

- Zhang, X.; Sun, H.; Liu, K.Y.; Liu, S. Dual credit policy, product line decisions, and CO2 emission reduction. Ann. Oper. Res. 2023, 1–25. [Google Scholar] [CrossRef]

- Xu, X.; He, P.; Xu, H.; Zhang, Q. Supply chain coordination with green technology under cap-and-trade regulation. Int. J. Prod. Econ. 2017, 183, 433–442. [Google Scholar] [CrossRef]

- Luo, Z.; Chen, X.; Wang, X. The role of co-opetition in low carbon manufacturing. Eur. J. Oper. Res. 2016, 253, 392–403. [Google Scholar] [CrossRef]

- Chen, X.; Wang, X.; Xia, Y. Low-carbon technology transfer between rival firms under cap-and-trade policies. IISE Trans. 2021, 54, 105–121. [Google Scholar] [CrossRef]

- Chai, Q.; Li, Y.; Xiao, Z.; Lai, K.-H. Optimal carbon abatement strategy for manufacturers under cap-and-trade. Int. J. Environ. Res. Public Health 2022, 19, 10987. [Google Scholar] [CrossRef]

- Tong, W.; Liu, H.; Du, J. Does the carbon trading mechanism affect social and environmental benefits of the retailer-led supply chain: Strategic decisions of emissions reduction and promotion. Front. Environ. Sci. 2022, 10, 971214. [Google Scholar] [CrossRef]

- Xu, X.; Zhang, W.; He, P.; Xu, X. Production and pricing problems in make-to-order supply chain with cap-and-trade regulation. Omega 2017, 66, 248–257. [Google Scholar] [CrossRef]

- Bai, Q.; Xu, J.; Zhang, Y. Emission reduction decision and coordination of a make-to-order supply chain with two products under cap-and-trade regulation. Comput. Ind. Eng. 2018, 119, 131–145. [Google Scholar] [CrossRef]

- Yu, L.; Jiang, X.; He, Y.; Jiao, Y. Promoting the diffusion of new energy vehicles under dual credit policy: Asymmetric competition and cooperation in complex network. Energies 2022, 15, 5361. [Google Scholar] [CrossRef]

- Shao, J.; Yang, H.; Zhang, A. Adoption of electric vehicles: Manufacturers’ incentive and government policy. J. Transp. Econ. Policy (JTEP) 2019, 53, 175–198. [Google Scholar]

- Yu, M.; Cruz, J.M.; Li, D.; Masoumi, A.H. A multiperiod competitive supply chain framework with environmental policies and investments in sustainable operations. Eur. J. Oper. Res. 2022, 300, 112–123. [Google Scholar] [CrossRef]

- Liu, L.; Wang, Z.; Liu, Y.; Zhang, Z. Vehicle product-line strategy under dual-credit and subsidy back-slope policies for conventional/new energy vehicles. Comput. Ind. Eng. 2023, 177, 109020. [Google Scholar] [CrossRef]

- Wang, Y.; Zhang, Z.; Zhu, M. Optimal subsidy policy for new energy vehicles based on the influence of multiple factors and consumers’ green preference. Manag. Decis. Econ. 2024, 45, 2868–2891. [Google Scholar] [CrossRef]

- Zhou, J.; Li, Y.; Ye, F.; Zhao, X.; Tong, Y.; Guo, H. Single rollover or dual rollover: How a monopoly NEV manufacturer responds to NEV credit policy. Transp. Res. Part E Logist. Transp. Rev. 2024, 191, 103739. [Google Scholar] [CrossRef]

- Stepanova, A.; Tesoriere, A. R&D with spillovers: Monopoly versus noncooperative and cooperative duopoly. Manch. Sch. 2011, 79, 125–144. [Google Scholar]

- Ishikawa, N.; Shibata, T. R&D competition and cooperation with asymmetric spillovers in an oligopoly market. Int. Rev. Econ. Financ. 2021, 72, 624–642. [Google Scholar]

- Cheng, L.; Yu, F.; Huang, P.; Liu, G.; Zhang, M.; Sun, R. Game-theoretic evolution in renewable energy systems: Advancing sustainable energy management and decision optimization in decentralized power markets. Renew. Sustain. Energy Rev. 2025, 217, 115776. [Google Scholar] [CrossRef]

- Jiang, Y.; Liu, C. Research on carbon emission reduction and blockchain investment under different dual-channel supply chains. Environ. Sci. Pollut. Res. 2022, 29, 65304–65321. [Google Scholar] [CrossRef] [PubMed]

- Xiao, L.; Chen, Z.S.; Hou, R.; Mardani, A.; Skibniewski, M.J. Greenness-based subsidy and dual credit policy to promote new energy vehicles considering consumers’ low-carbon awareness. Comput. Ind. Eng. 2023, 185, 109620. [Google Scholar] [CrossRef]

- Zhao, D.; Wang, J.; Li, W.-W.; Tang, J.-H.; Huang, S. Consider payoff or emphasize learning? Exploring the effect of new dual-credit policy on electric vehicle diffusion in complex network. Energy Econ. 2025, 148, 108622. [Google Scholar] [CrossRef]

- Pu, J.; Chun, W. How does dual-credit policy regulate competitive fuel vehicle and new energy vehicle manufacturers? based on operational decision analysis under multiple scenarios. Comput. Ind. Eng. 2025, 203, 111076. [Google Scholar] [CrossRef]

- Qi, X.; Han, Y. The impact of technological innovation for emission reduction on decision-making for intertemporal carbon trading. Comput. Ind. Eng. 2023, 186, 109739. [Google Scholar] [CrossRef]

- Zhu, Z.; Cheng, L.; Shen, T. Spontaneous Formation of Evolutionary Game Strategies for Long-Term Carbon Emission Reduction Based on Low-Carbon Trading Mechanism. Mathematics 2024, 12, 3109. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Literature | Market Structure | Strategy | Dual-Credit | Cap-and-Trade | Mixed Carbon Policy |

|---|---|---|---|---|---|

| Yu H (2023) [24] | Oligopoly manufacturers | Optimal innovation | ✓ | ✗ | ✗ |

| Pu J (2024) [5] | Monopoly manufacturers | Emission reduction | ✓ | ✗ | ✗ |

| Wang Z (2021) [16] | Duopoly manufacturers | Emission reduction and product | ✗ | ✓ | ✗ |

| Zhang T (2022) [17] | / | Inventory | ✗ | ✓ | ✗ |

| Yi Y (2024) [19] | A manufacturer and a retailer | Pricing | ✓ | ✗ | ✗ |

| Cheng Y (2022) [21] | A manufacturer and government | Pricing and production | ✓ | ✗ | ✗ |

| Li Y (2020) [22] | Duopoly manufacturers | Production and credit | ✓ | ✗ | ✗ |

| Wang Y (2024) [38] | A manufacturer and government | Subsidy policy | ✓ | ✓ | ✓ |

| Zhou J (2024) [39] | Monopoly manufacturers | Pricing and rollover | ✓ | ✓ | ✗ |

| This paper | Monopoly manufacturers | Pricing and emission reduction | ✓ | ✓ | ✓ |

| Notations | Definition |

|---|---|

| denotes the single dual-credit policy, and denotes the “cap-and-trade + dual-credit” policy. | |

| and refer to the actual fuel consumption of Manufacturer 1 after emission reduction exceeds and is lower than the standard value under the single dual-credit policy, respectively. and denote the actual fuel consumption of Manufacturer 1 after emission reduction exceeds and is lower than the standard value under the “cap-and-trade + dual-credit” policy, respectively. | |

| The fuel vehicle production quantity of M1 | |

| The NEV production quantity of Manufacturer , | |

| M1’s emission reduction effort cost coefficient | |

| CAFC compliance value | |

| Actual CAFC value for fuel vehicles | |

| Positive NEV credit generated by producing one NEV | |

| NEV credit ratio requirement | |

| Trading price of NEV credits | |

| Proportion of consumers preferring NEVs | |

| Low-carbon preference awareness of fuel vehicle consumers | |

| Unit carbon trading price | |

| Total carbon allowance of Manufacturer , | |

| Per unit carbon emissions from producing NEVs | |

| Per unit carbon emissions from producing fuel vehicles | |

| Total carbon emissions of Manufacturer , | |

| Profit of M1 | |

| Profit of M2 | |

| Decision Variable | Definition |

| The price of fuel vehicles by M1 | |

| The price of NEVs by Manufacturer, | |

| M1’s emission reduction effort level |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, C.; Zhang, Y.; Zhao, J.; Wang, C.; Chun, W. Pricing and Emission Reduction Strategies of Heterogeneous Automakers Under the “Dual-Credit + Carbon Cap-and-Trade” Policy Scenario. Mathematics 2025, 13, 2262. https://doi.org/10.3390/math13142262

Wu C, Zhang Y, Zhao J, Wang C, Chun W. Pricing and Emission Reduction Strategies of Heterogeneous Automakers Under the “Dual-Credit + Carbon Cap-and-Trade” Policy Scenario. Mathematics. 2025; 13(14):2262. https://doi.org/10.3390/math13142262

Chicago/Turabian StyleWu, Chenxu, Yuxiang Zhang, Junwei Zhao, Chao Wang, and Weide Chun. 2025. "Pricing and Emission Reduction Strategies of Heterogeneous Automakers Under the “Dual-Credit + Carbon Cap-and-Trade” Policy Scenario" Mathematics 13, no. 14: 2262. https://doi.org/10.3390/math13142262

APA StyleWu, C., Zhang, Y., Zhao, J., Wang, C., & Chun, W. (2025). Pricing and Emission Reduction Strategies of Heterogeneous Automakers Under the “Dual-Credit + Carbon Cap-and-Trade” Policy Scenario. Mathematics, 13(14), 2262. https://doi.org/10.3390/math13142262