Abstract

With the frequent occurrence of financial risks, financial innovation supervision has become an important research issue, and excellent regulatory strategies are of great significance to maintain the stability and sustainable development of financial markets. Thus, this paper intends to analyze the financial regulation strategies through evolutionary game theory. In this paper, the delayed replication dynamic equation and the non-delayed replication dynamic equation are established, respectively, under different reward and punishment mechanisms, and their stability conditions and evolutionary stability strategies are investigated. The analysis finds that under the static mechanism, the internal equilibrium is unstable, and the delay does not affect the stability of the system, while in the dynamic mechanism, when the delay is less than a critical value, the two sides of the game have an evolutionary stable strategy, otherwise it is unstable, and Hopf bifurcation occurs at threshold. Finally, some numerical simulation examples are provided, and the numerical results show the correctness of the proposed algorithm.

Keywords:

digital financial innovation; digital financial supervision; static and dynamic mechanism; delayed replication dynamic equation; Hopf bifurcation MSC:

91A25; 34C23; 34K18

1. Introduction

Digital finance is a combination of internet information technology and traditional financial services. The emergence of digital finance is conducive to the development of social technology and industry [1,2]. However, when looking at the reality, not all digital financial innovations are compliant, and innovations using illegal digital technologies happen from time to time. On the one hand, financial innovation has given rise to accomplishments such as digital currency, technology finance, and big data risk control, thereby enhancing the operational efficiency of the financial industry and fostering the growth and prosperity of the financial market. Conversely, there have also emerged instances of financial turmoil like P2P online lending, shadow banking, and illegal fundraising that have resulted in frequent financial risks and widespread incidents, significantly impacting financial security and social order. The complexity and multifunctionality inherent in regulating financial innovation itself along with the imperfections and delays within the existing regulatory system may be identified as pivotal factors contributing to this issue.

While digital finance is beneficial to the development of various industries and economies, at the same time, it has presented significant regulatory challenges [3]. Compliance innovation can bring more opportunities to the development of the financial industry. If financial institutions choose illegal innovation, even if they will get temporary excess returns, various financial risks will come one after another, such as information technology risks, systematic financial risks, and trading reputation risks. Research on financial regulatory strategies is of great significance for preventing financial risks, maintaining market stability, and protecting investors’ rights and interests. In the supervision of financial innovation, government departments should not only strengthen supervision and maintain market stability, but also relax restrictions and promote financial innovation, while both will inevitably increase the complexity of supervision. Thus, to maintain a balance between financial innovation and stability, an effective regulatory system should be established as soon as possible [4,5,6]. Hanson et al. [7] discussed how to deal with many phenomena observed in the financial crisis between 2007 and 2009. Chao et al. [8] believed that the role of intelligent regulatory technology in financial regulation can be fully utilized. In [9], the authors made a thorough analysis of various strategies needed in the process of financial supervision. Zhou et al. [10] indicated that regulatory penalties can be effective in curbing irregularities in financial innovation. Most of these research results are derived from the perspective of static analysis.

As a dynamic game theory, evolutionary game theory provides a new method and perspective for the study of financial regulation strategies. Evolutionary game theory is a combination of game and evolution theory. It has been widely used in the analysis of practical problems in the financial field, such as internet finance, financial innovation and supervision [9], credit markets [11], blockchain [12], supply chains [13], and digital finance [14]. Evolutionary games focus on the dynamic adjustment process of players’ strategies, which can better explain the long-term evolution of the market and the interaction between players. In the field of financial regulation, applying evolutionary game theory can better reflect the dynamic characteristics of the market, predict the future development trend, and provide theoretical support for the formulation of more effective regulatory strategies.

In the existing research, many scholars have used this method to analyze the evolutionary process and game relationship of financial innovation and regulation, and obtained corresponding theoretical results. Liu et al. [15] analyzed the game model between the government, enterprises, and consumers, and discussed the evolution strategy between them. Deng et al. [16] constructed an evolutionary game model for government Internet regulation based on prospect theory and mental accounts. Xu et al. [17] demonstrated the behavioral strategies and game results of regulators and financial institutions based on the data of a commercial bank. Gunarso [18] found that reasonable benefits can be gained through cooperation between regulators and fintech companies. Song et al. [19] found that if the regulatory intensity of innovation is greater than a given threshold, both can achieve a win-win situation. If the dynamic balance between supervision and innovation is maintained, compliance innovation and effective regulation will evolve in tandem [20].

Although the innovation and regulation of digital finance have been analyzed by many scholars from various angles and methods, they have not considered the impact of time delay on evolutionary game analysis. In the evolution of the classical game theory, the interaction between individuals is generally considered to be instantaneous, but usually, it is not. Many biological and social processes need some time to complete. This fact leads to the emergence of time delay. Time delay affects replicator dynamics, so time delay should be taken into account in evolutionary game analysis [21,22,23,24,25,26]. Hu et al. [23] studied three models and found that the existence of delay has a significant effect on the stability of the studied system. Jan et al. [24] studied the stability of internal equilibrium points in discrete delay replication factor dynamics. Cheng et al. [25] considered delayed game models with three strategies. In [26], the stability of game models with fixed and random delay is analyzed.

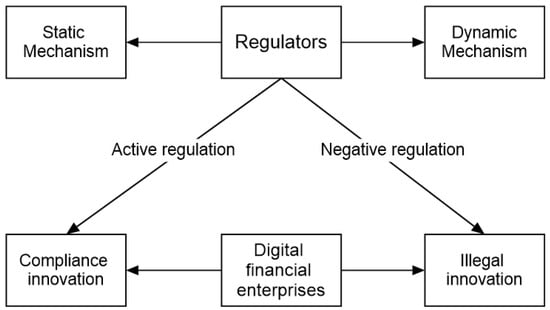

In general, although some scholars have conducted relevant studies on the innovation and regulation of digital finance, the objective existence of time delay is not considered, and its influence on the analysis of system stability is ignored. The introduction of time delay factors, first, makes the model analysis more consistent with the objective facts, and second, may make the originally stable system become unstable. Inspired by this, this paper establishes several evolutionary game models of financial innovation and regulation based on the introduction with and without delay under different reward and penalty mechanisms, illustrating their logical relationship in Figure 1. The stability analysis of models and properties of Hopf bifurcation is carried out, and the results are verified by numerical simulation examples. Finally, relevant suggestions are put forward.

Figure 1.

The relationship between regulators and digital financial enterprises.

The organization of this article is as follows. In Section 2, the basic hypotheses are presented and the payment matrix is obtained. The evolutionary game models are established and the stable strategies are discussed in Section 3 and Section 4. In Section 5, the direction of Hopf bifurcation and the stability of periodic solutions at critical values are analyzed. In Section 5, numerical examples are given and simulations are performed. In Section 6, relevant conclusions and suggestions are drawn.

2. Basic Assumptions and Payoff Matrix

This section mainly sets the corresponding parameters for the establishment of models and obtains the payment matrix. Before proceeding, the following assumptions are needed. The assumptions of some parameters are similar to the literature [27,28].

Hypothesis 1.

Game subject: digital financial enterprises and regulators.

Hypothesis 2.

Digital financial enterprises have two pure strategies: “compliance innovation” and “illegal innovation”, and the probability of selecting compliance innovation is p, and illegal innovation is . Regulators also have two pure strategies: “active regulation” and “negative regulation”, with a probability of q for active regulation and a probability of for negative regulation, and the trend of .

Hypothesis 3.

When enterprises choose compliance innovation, the income and cost are and , respectively, while when choosing illegal innovation, its excess income and cost are and , respectively.

Hypothesis 4.

If financial enterprises choose compliance innovation, the healthy development of the social economy will bring corresponding benefits, and the regulators will achieve . If the financial enterprises opt for illegal innovation, the loss of public interest caused by the financial enterprises is D, and the regulators obtain . The costs of active supervision and passive supervision by the regulators are and , respectively.

Hypothesis 5.

When the regulators are active in supervision, there will be a reward and punishment mechanism. If the financial enterprises choose compliance innovation, they will obtain a reward R; otherwise, they will be fined F. When the regulators are passive in supervision, there will be no reward and punishment.

Based on the above hypotheses, the following Table 1 can be obtained.

Table 1.

Payoff matrix.

3. Evolutionary Models under a Static Mechanism

3.1. Static Mechanism Evolutionary Model without Time Delay

From Table 1, we can obtain a two-dimensional replicated dynamic equation concerning the two-party game between digital financial enterprises and regulators,

In System (1), if and , we can obtain five equilibrium points for a replicated dynamical system, which are , , , where , . The ESS of system can be obtained according to its Jacobian matrix [29]. If the equilibrium point of Det > 0 and Tr, then this is an ESS. The Jacobian matrix of System (1) is

Because of Tr, is not an ESS. The values of Tr and Det for the other four points are shown in the following Table 2.

Table 2.

The values of Tr and Det in equilibrium.

From Table 2, if and , the ESS of system (1) is ; if and , the ESS is ; if and , the ESS is ; and if and , the ESS is .

indicates that the difference in supervision costs is greater than the amount of penalty received; means that the excess return is greater than the difference in cost required. The ESS is (illegal innovation, negative regulation), and System (1) will present the phenomenon of frequent security accidents in digital finance. shows that regulators can receive a large fine, but the excess income of financial firms is greater than the fine; means that they can receive a small reward for compliance innovation, and the ESS is (illegal innovation, active regulation). indicates that the excess return is less than the cost to be paid; shows that the incentive paid by regulators for compliance innovation is greater than the difference in supervision costs, and the ESS is (compliance innovation, negative regulation). means that the fines of digital financial firms are greater than the excess returns, and means that the cost of active supervision is less than negative regulation, so the ESS is (compliance innovation, active regulation), indicating that active regulation plays an important role in promoting compliance innovation.

3.2. Delayed Static Mechanism Evolutionary Model and Stability Analysis

The coordinated development and win-win cooperation between financial enterprises and regulators need to be based on information sharing. Only by establishing a sound information sharing platform to provide information exchange and separate supervision for financial regulators can coordination and cooperation be achieved. However, in reality, there is information asymmetry in the process of information sharing, the complexity of the regulatory objects and other objective factors. The regulators lag in the development of information updates for digital financial enterprises, and digital financial companies also lag in updating information on relevant policies and measures of government departments. The payoff of both parties at the present moment may depend on the strategy at delay .

Based on the above discussion, this paper assumes the payoff of the strategy adopted by the digital financial enterprises at the time t depends on the strategy adopted by the regulators at time ; if the strategy of “active regulation” is adopted by the regulators at time , then the financial enterprises will be fined F. Additionally, suppose regulators have a delay , if the illegal innovation is adopted at time , the profit of the regulators will increase by F. From System (1), the delayed static mechanism evolutionary model can be established as follows.

where , , , is an interior equilibrium point of system (2). Let , , , , then System (2) becomes

It is easy to see the linearized approximation of Equation (3) is

The characteristic equation of Equation (4) is

where , , .

Lemma 1

([30]). A sufficient and necessary condition for uniform asymptotic stability of the zero solution of is that all the roots of are distributed in the left half, i.e.,

According to Lemma 1, we can obtain the following result for System (2).

Theorem 1.

The internal equilibrium point of System (2) is unstable, and the stability of the system is not affected by a time delay.

Proof.

If ,

then based on , can be solved. This shows that when , all eigenvalues are distributed along the imaginary axis.

When increases slightly from 0, the change in can be judged according to the sign of . Taking the derivative of both ends concerning , we obtain

The eigenvalues passes through the imaginary axis into the right half plane, and continues to increase. At , the roots intersect the imaginary axis, and the corresponding roots are denoted by ; similar to Equation (7), we have

This indicates that the roots on the imaginary axis will again enter the right half plane as increases slightly from . □

Remark 1.

The proof process of Theorem 1 shows that when , the eigenvalues of Equation (5) fall on the imaginary axis, and when it increases gradually from 0, the roots enter the right half plane, and if it continues to increase from , the eigenvalues will not enter the left half plane, so no matter how much increases, the internal equilibrium of System (2) is not uniformly asymptotically stable.

Remark 2.

Remark 3.

The conclusion of Theorem 1 is mainly based on . A natural problem is that if , that is, under the static mechanism, if the delay time of the enterprises and regulators is basically the same, the stability of the equilibrium point is the above Theorem 1 of a special situation, and from the proof process of Theorem 1, it is easy to draw the following corollary.

Corollary 1.

4. Evolutionary Models under a Dynamic Mechanism

From the previous analysis, the equilibrium of System (1) and System (2) is not an ESS, so a dynamic mechanism with more realistic, flexible supervision and higher liquidity can be introduced to improve the stability of the system. Based on this, the non-delay and delay replication dynamic equations can be established, and their stability is analyzed, respectively.

4.1. Dynamic Mechanism Evolutionary Model without Time Delay

Suppose that the regulator’s reward for digital financial firms is and punishment is , then the replication dynamic equation is

The equilibrium points of the dynamic system (8) are , , , , . If , , , then the Jacobian matrix is

where . According to , the stability of System (8) can be analyzed, and the following table presents the relevant results.

It is evident from the results in Table 3, that is a unique ESS of System (8). From the values of and , the evolutionary stability strategy of financial enterprises and regulators is related to the difference between the supervision cost and the ceiling of reward and punishment of regulatory departments, and also to the difference between the cost and excess return of digital financial enterprises.

Table 3.

Stability of the equilibrium points in System (8).

4.2. Dynamic Mechanism Evolutionary Model with Time Delay and Stability Analysis

Based on System (8), which is similar to System (2), it is assumed that the payoff of the strategy adopted by the financial enterprises at time t depends on the strategy adopted by the regulators at time . Similarly, suppose that the benefits of the regulators are influenced by the financial enterprises at the time of , then the replicated dynamic system under the dynamic mechanism can be obtained.

Let , , , , then System (9) at equilibrium becomes

The linearization result of Equation (10) is

Theorem 2.

The sufficient and necessary condition for the equilibrium of System (9) to be uniformly asymptotically stable is

where , .

Proof.

If , , then by Vieta’s theorem, we can obtain

and therefore, . That is to say, when , all roots are distributed in the left half plane.

Suppose that when is further added, for equilibrium , the system becomes uniformly asymptotically unstable, and if is the minimum that makes the equilibrium points unstable, then has roots across the imaginary axis; that is, exists such that is true.

When , , so it does not go through the origin. If we substitute into Equation (12), we obtain

the sufficient and necessary condition for is

and this is equivalent to

It can be solved by Equation (14)

i.e., , and a further calculation can be obtained

and because of , then When , , so if , the equilibrium point of System (9) is stable.

As increases from and considering how the eigenvalues change in the complex plane, on both sides of the equation about derivative gain

from , this equation can be simplified to

and

This shows that as increases slightly from , the roots will enter the right half plane. Let continue to increase, then at corresponding roots back to the imaginary axis.

Similarly,

This means that when increases slightly from , the characteristic roots will again enter the right half plane. In general, when , the roots of Equation (12) never enter the left half plane again. □

Remark 4.

From the proof of Theorem 2.

Remark 5.

Theorem 2 shows that, under the dynamic mechanism, when the delay of financial enterprises and regulators is less than the threshold, they will eventually achieve evolutionary stability. The conclusion of Theorem 2 is mainly based on the fact that is not equal to . For a special case of Theorem 2, ; that is, when the delay time of financial enterprises and regulators is basically the same under the dynamic mechanism, the following corollary can be easily obtained from the proof process of Theorem 2.

Corollary 2.

5. Properties of Hopf Bifurcation

In this section, we focus on the condition of , applying the central manifold theorem and normal form to analyze the Hopf bifurcation direction of System (9) and the stability of periodic solutions.

By the Riesz representation theorem, there is a bounded variational function , such that

We define

System (17) is equivalent to

For , the adjoint operator of is defined as

and a bilinear form

According to the previous section, are the eigenvalues of and , so we can easily calculate the eigenvectors corresponding to the eigenvalues, respectively. Suppose that , by , and the definition of and , we obtain

By calculation we obtain or , or To make sure , it is necessary to compute N, and from (19), we have

Thus,

Then, by using the relevant algorithms in the literature [31,32] and similar calculation processes, we can come up with several coefficients for determining the direction of Hopf bifurcation and the stability of bifurcated periodic solutions.

Among them, the calculation results of and are

where , are constant vectors.

which leads to

In this way, the following formulas can be used to obtain the properties of bifurcation on the central manifold,

If , then the direction of bifurcation is supercritical, the bifurcated periodic solution is stable if and the period of the bifurcating periodic solution increases if .

6. Numerical Simulations

To visually and vividly reflect the evolutionary game behavior between two plays in the above models, we conduct numerical simulation analysis. Based on the parameter settings mentioned in the relevant literature [14], we set the parameters as , = 1, = 3, = 3 and = 4.

6.1. Numerical Analysis under Static Mechanism

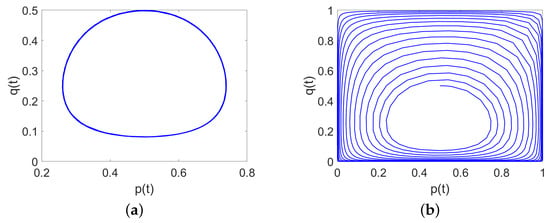

Given the set parameters, the equilibrium point in System (1) can be solved as . Assume that p and q are both 0.5, then the evolution curves of Systems (1) and (2) are shown in Figure 2a,b, respectively. Figure 2 shows that neither System (1) nor System (2) are evolutionarily stable at the equilibrium point . What is more, the curve of System (1) is a closed-loop line in Figure 2a, whereas System (2) is a time-delay replication dynamic system, and it does not evolve towards equilibrium, confirming that under the static mechanism, the stability of enterprises and regulators is not affected by the delay .

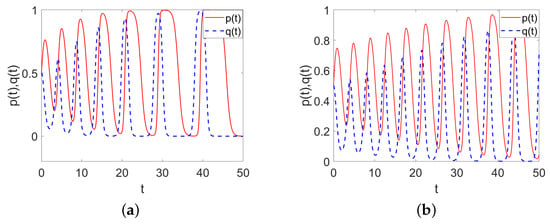

To analyze the effect of different delays on System (2), let and . In Figure 3, System (2) is unstable regardless of whether the time delay is the same or different, and the amplitude of the evolution curve’s fluctuation is roughly the same, but the frequency of the fluctuation is different. The larger the delay , the smaller the fluctuation frequency, and the smaller the delay , the larger the fluctuation frequency, indicating that although the stability strategies of enterprises and regulators are not affected by delay, it will affect the evolutionary process between them.

Figure 3.

(a) Evolution curve when , (b) Evolution curve when .

6.2. Numerical Analysis under Dynamic Mechanism

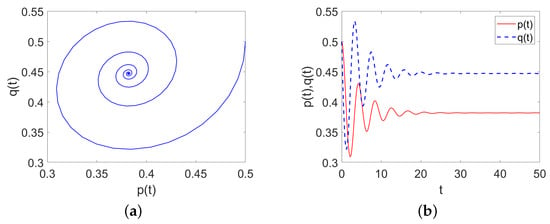

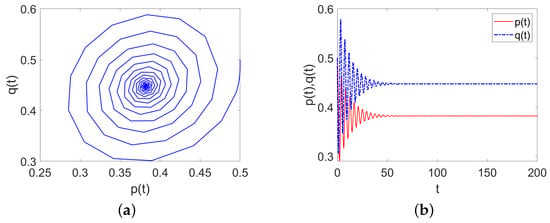

For Systems (8) and (9), the equilibrium and can be obtained by keeping the parameter settings unchanged. For System (9), it can be established from Theorem 2 that as long as holds, the dynamic System (9) is evolutionarily stable for any . When and , the evolution processes of Systems (8) and (9) are shown in Figure 4 and Figure 5, respectively. In the figures, the evolution curves between the enterprises and regulators in both the non-delayed dynamic system and the time delay dynamic system present a spiral convergence trend and finally reach stability.

Figure 4.

(a) Evolution curve of System (8) when , ; (b) The evolution progress of p and q as t changes.

Figure 5.

(a) Evolution curve of System (9) when ; (b) The evolution progress of p and q as t changes.

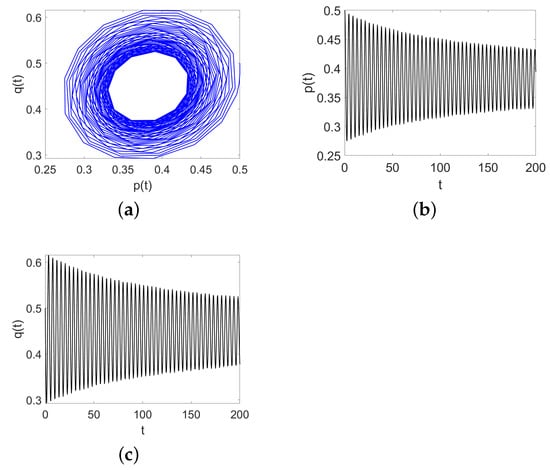

When , System (9) undergoes a Hopf bifurcation. Substituting numerical values for the formulas in Section 5, we obtain

where indicates that the Hopf bifurcation of the system (9) is supercritical; that is, the system is stable before bifurcation and unstable after bifurcation, which is reflected in Figure 5, Figure 6 and Figure 7. In this case, the stability change in the system is continuous, and according to the signs of and , it is concluded that the periodic solution of Hopf bifurcation is stable, and the period of the periodic solution increases gradually.

Figure 6.

(a) Evolution curve of System (9) when ; (b) The evolution progress of p as t changes; (c) The evolution progress of q as t changes.

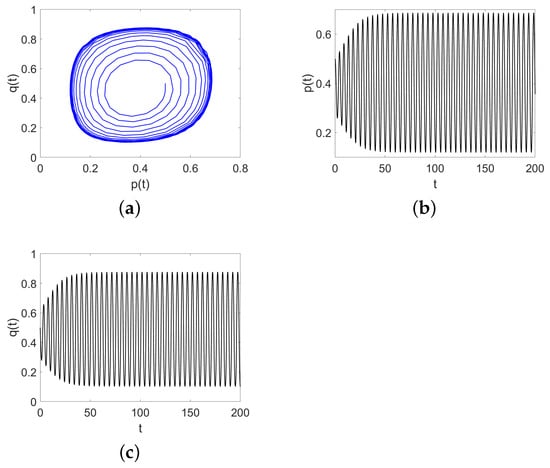

Figure 7.

(a) Evolution curve of System (9) when ; (b) The evolution progress of p as t changes; (c) The evolution progress of q as t changes.

Figure 7 is the evolution process of the delayed dynamic System (9) when . It is obvious from the figure that there is no ESS between the two sides, and the path is a closed-loop line around (0.38, 0.45). It is also known from the figure that the players of both sides present periodic behavior patterns. Figure 5, Figure 6 and Figure 7 prove the objective fact that time delay affects the stability of the system; when it is less than threshold, the system remains stable and goes through Hopf bifurcation at threshold, and when it is greater than the critical value, there is a qualitative change in the system. In real life, before reaching critical conditions, if players’ strategies can not be adjusted, that means digital financial enterprises and regulators need to control the delay of obtaining information and establish a good information sharing platform.

Effect of Initial Value on Amplitude of State Curve of System (9)

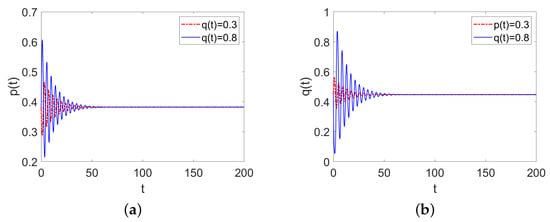

Based on the setting of the previous parameters, the impact of different initial values on the evolutionary curve of System (9) are compared. When the probability for enterprises to adopt compliance innovation, and are taken as the initial values of active supervision by the regulators; when and are taken as the initial values of financial enterprises. The corresponding evolution curves are shown in Figure 8.

Figure 8.

(a) The evolution process of p as t changes when q is set to 0.3 and 0.8; (b) The evolution process of q as t changes when p is set to 0.3 and 0.8.

p and q oscillate in the initial stage, and the larger the initial values of p and q, the larger the oscillation amplitude. It can be seen from the evolution curve that the greater the possibility of compliance innovation of financial enterprises in the initial stage, the greater the fluctuation of its evolutionary stability curve, and the smaller the possibility of regulators’ active regulation at the beginning, the smaller the fluctuation of its evolutionary stability curve. If the strategy in the initial stage is (illegal innovation, negative regulation), then both sides of the game can quickly achieve evolutionary stability, and market fluctuations will be relatively small, which is more conducive to market coordination and long-term development.

7. Conclusions and Recommendations

7.1. Conclusions

In this paper, from the establishment and analysis of the models, we draw the following conclusions.

Firstly, under the static condition, the internal equilibrium point is not ESS for Systems (1) and (2), and whether the delay exists or not does not affect its stability. It shows that regulators and digital financial enterprises cannot reach a stable state, and their evolution process shows a cyclical movement. According to the theoretical results, there are boundary stability strategies between them under certain conditions. Among them, if the fines of digital financial firms are greater than the excess returns, and the cost of active regulation is less than negative regulation, then (compliance innovation, active regulation) is ESS, indicating that active regulation plays an important role in promoting compliance innovation and can achieve this by increasing the penalties and reducing regulatory costs to regulate the behavior of innovation.

Secondly, under the dynamic mechanism, for Systems (8) and (9) ESS equilibrium exists, and its stability changes with the change in delay. The system is stable before the delay reaches the critical value, Hopf bifurcation occurs at threshold, the bifurcation direction is forward, the periodic solution of the bifurcation is stable and the period gradually increases, and the system becomes unstable if the delay exceeds the threshold. In the process of evolution, regulators and firms can achieve a stable state, which shows the superiority of dynamic mechanisms. However, this stable state only exist under certain conditions, so digital financial enterprises and regulators need to limit the delay of information acquisition to a certain range when making decisions.

7.2. Recommendations

A few suggestions can be made from the theoretical results of this paper.

For regulators, first, improve the financial regulatory framework and rules, and improve risk compensation, emergency response, service withdrawal, and other mechanisms. They must control financial industry overall risk, limit excess competition in the financial sector, and promote the healthy and stable financial sector in accordance with the law. Second, promote the idea of compliance innovation, and conduct reasonable guidance and constraints on innovation activities. Third, regulators can take the initiative to supervise financial institutions through technological means. Big data, cloud computing, artificial intelligence, and other technologies can be used to build data platforms and analysis platforms for financial regulation.The use of digital regulatory means to continuously and dynamically monitor the operation status of innovative applications can in a timely manner locate, track, prevent, and resolve risks and hidden dangers. Through the digital expression of regulatory policies and compliance requirements, the establishment of an information sharing platform can effectively solve the problem of information asymmetry, which is conducive to easing regulatory delays, improving regulatory penetration, and enhancing regulatory uniformity.

Digital financial enterprises should consciously innovate in compliance with regulations and improve their professional quality. They should establish and improve the self-supervision system, self-supervision management, and internal control management. Financial innovation is conducive to the improvement in financial efficiency, the effective allocation of resources, and the promotion of economic development, but the innovation of financial models, products, services, and tools must be carried out under certain institutional constraints to avoid the occurrence of financial risks and realize the healthy and sustainable development of financial innovation.

7.3. Weaknesses and Prospects

Although this paper introduces the delay factor and obtains the relevant theoretical results, the influencing factors of financial innovation are not comprehensively considered. In addition, this article focuses on a two-party evolutionary game, which has certain limitations. Future work can consider building a three-party evolutionary game model; for example, the public can be added into the game model. In addition, it will be interesting to explore the influence of different delay types on the system’s stability, and the addition of a delay feedback controller to control critical values, and we will conduct further research on these issues in the future.

Author Contributions

Conceptualization, M.X. and Z.L.; Methodology, M.X., Z.L., C.X. and N.W.; software, M.X.; formal analysis, M.X. and Z.L.; resources, C.X. and N.W.; Writing—original draft preparation, M.X.; Funding acquisition, Z.L. All authors have read and agreed to the published version of the manuscript.

Funding

This research was supported by the National Natural Science Foundation of China [grant number 62062018]; Guizhou Key Laboratory of Big Data Statistics Analysis [grant number BDSA20200102]; Guizhou University of Finance and Economics Project [grant number 2022ZCZX082]; and Guizhou Province University Science and Technology top talents project [grant number KY[2018]047].

Data Availability Statement

The data will be made available by the authors on request.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Durai, T.; Stella, G. Digital finance and its impact on financial inclusion. J. Emerg. Technol. Innov. Res. 2019, 6, 122–127. [Google Scholar]

- Peng, S.; Jiang, X.; Li, Y. The impact of the digital economy on Chinese enterprise innovation based on intermediation models with financing constraints. Heliyon 2023, 9, e13961. [Google Scholar] [CrossRef]

- Cao, S.; Nie, L.; Sun, H.; Sun, W.; Taghizadeh-Hesary, F. Digital finance, green technological innovation and energy-environmental performance: Evidence from China’s regional economies. J. Clean. Prod. 2021, 327, 129458. [Google Scholar] [CrossRef]

- Haonan, S.; Gaoyang, C.; Yutong, S.; Hu, W.; Wang, W. Building of a standard system for supervision over financial technology enterprises from the perspective of governmental regulation. J. Sociol. Ethnol. 2022, 4, 101–106. [Google Scholar]

- Zheng, C.; Wang, Z.; Pan, S.; Chen, X.; Jia, S. Does financial structure still matter for technological innovation when financial technology and financial regulation develop? Technol. Forecast. Soc. Change 2023, 194, 122747. [Google Scholar] [CrossRef]

- Ran, H.; Qun, F. Asymmetric evolutionary game between financial innovation and financial regulation: Punishment or encouragement. J. Financ. Account. 2017, 5, 102–106. [Google Scholar] [CrossRef]

- Hanson, S.G.; Kashyap, A.K.; Stein, J.C. A macroprudential approach to financial regulation. J. Econ. Perspect. 2011, 25, 3–28. [Google Scholar] [CrossRef]

- Chao, X.; Ran, Q.; Chen, J.; Li, T.; Qian, Q.; Ergu, D. Regulatory technology (reg-tech) in financial stability supervision: Taxonomy, key methods, applications and future directions. Int. Rev. Financ. Anal. 2022, 80, 102023. [Google Scholar] [CrossRef]

- An, H.; Yang, R.; Ma, X.; Zhang, S.; Islam, S.M.N. An evolutionary game theory model for the inter-relationships between financial regulation and financial innovation. N. Am. J. Econ. Financ. 2021, 55, 101341. [Google Scholar] [CrossRef]

- Zhou, X.; Chen, S. Fintech innovation regulation based on reputation theory with the participation of new media. Pac. Basin Financ. J. 2021, 67, 101565. [Google Scholar] [CrossRef]

- Wang, L.; Wang, Z.; Tian, L.; Li, C. Evolutionary game and numerical simulation of enterprises’ green technology innovation: Based on the credit sales financing service of supply chain. Sustainability 2022, 15, 702. [Google Scholar] [CrossRef]

- Tan, Y.; Huang, X.; Li, W. Does blockchain-based traceability system guarantee information authenticity? an evolutionary game approach. Int. J. Prod. Econ. 2023, 264, 108974. [Google Scholar] [CrossRef]

- Hu, Y.; Ghadimi, P. A review of blockchain technology application on supply chain risk management. IFAC-PapersOnLine 2022, 55, 958–963. [Google Scholar] [CrossRef]

- Fu, H.; Liu, Y.; Cheng, P.; Cheng, S. Evolutionary game analysis on innovation behavior of digital financial enterprises under the dynamic reward and punishment mechanism of government. Sustainability 2022, 14, 12561. [Google Scholar] [CrossRef]

- Liu, L.; Wang, Z.; Song, Z.; Zhang, Z. Evolutionary game analysis on behavioral strategies of four participants in green technology innovation system. Manag. Decis. Econ. 2023, 44, 960–977. [Google Scholar] [CrossRef]

- Deng, J.; Su, C.; Zhang, Z.; Wang, X.; Ma, J.; Wang, C. Evolutionary game analysis of chemical enterprises’ emergency management investment decision under dynamic reward and punishment mechanism. J. Loss Prev. Process. Ind. 2024, 87, 105230. [Google Scholar] [CrossRef]

- Xu, Y.; Bao, H. FinTech regulation: Evolutionary game model, numerical simulation, and recommendations. Expert Syst. Appl. 2023, 211, 118327. [Google Scholar] [CrossRef]

- Gunarso, G. Game theory of regulator, companies, and cooperation in Indonesian financial technology industry. Jinnah Bus. Rev. 2022, 10, 74–86. [Google Scholar] [CrossRef]

- Song, Y.; Xu, Y.; Zhang, Z. Win-win situation of Internet finance innovation and regulation: A game analysis of evasion and regulation. Soc. Sci. Res. 2018, 4, 25–31. [Google Scholar]

- Xu, Y.; Bao, H.; Zhang, W.; Zhang, S. Which financial earmarking policy is more effective in promoting fintech innovation and regulation? Ind. Manag. Data Syst. 2021, 121, 2181–2206. [Google Scholar] [CrossRef]

- Yi, T.; Zuwang, W. Effect of time delay and evolutionarily stable strategy. J. Theor. Biol. 1997, 187, 111–116. [Google Scholar] [CrossRef]

- Zhang, Z.; Kundu, S.; Tripathi, J.P.; Bugalia, S. Stability and Hopf bifurcation analysis of an SVEIR epidemic model with vaccination and multiple time delays. Chaos Solitons Fractals 2019, 131, 109483. [Google Scholar] [CrossRef]

- Hu, K.; Li, Z.; Shi, L.; Perc, M. Evolutionary games with two species and delayed reciprocity. Nonlinear Dyn. 2023, 111, 7899–7910. [Google Scholar] [CrossRef]

- Alboszta, J.; Mie, J. Stability of evolutionarily stable strategies in discrete replicator dynamics with time delay. J. Theor. Biol. 2004, 231, 175–179. [Google Scholar] [CrossRef]

- Cheng, H.; Meng, X. Multistability and hopf bifurcation analysis for a three-strategy evolutionary game with environmental feedback and delay. Phys. A Stat. Mech. Appl. 2023, 620, 128766. [Google Scholar] [CrossRef]

- Hu, L.; Qiu, X. Stability analysis of game models with fixed and stochastic delays. Appl. Math. Comput. 2022, 435, 127473. [Google Scholar] [CrossRef]

- Xie, C.; Li, H.; Chen, L. A Three-Party Decision Evolution Game Analysis of Coal Companies and Miners under China’s Government Safety Special Rectification Action. Mathematics 2023, 11, 4750. [Google Scholar] [CrossRef]

- Mou, S.; Zhong, K.; Ma, Y. Regulating the Big Data-Based Discriminatory Pricing in Platform Retailing: A Tripartite Evolutionary Game Theory Analysis. Mathematics 2023, 11, 2579. [Google Scholar] [CrossRef]

- Friedman, D. Evolutionary games in economics. Econom. J. Econom. Soc. 1991, 59, 637–666. [Google Scholar] [CrossRef]

- Toshiki, N.; Tadayuki, H.; Yoshiyuki, H.; Rinko, M. Differential Equations with Time Lag: Introduction to Functional Differential Equations; Makino Shoten: Tokyo, Japan, 2002. [Google Scholar]

- Hassard, B.D.; Kazarinoff, N.D.; Wan, Y.H. Theory and Applications of Hopf Bifurcation; CUP Archive; Cambridge University Press: Cambridge, UK; New York, NY, USA, 1981. [Google Scholar]

- Sun, C.; Cao, Z.; Lin, Y. Analysis of stability and Hopf bifurcation for a viral infectious model with delay. Chaos Solitons Fractals 2007, 33, 234–245. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).