Modified Block Bootstrap Testing for Persistence Change in Infinite Variance Observations

Abstract

1. Introduction

2. Materials and Methods

3. Results

4. Block Bootstrap Approximation

5. Numerical Results

5.1. Properties of the Tests under the H1, H0, and Near-Unit Root

5.2. Properties of the Tests under the H10 and H01

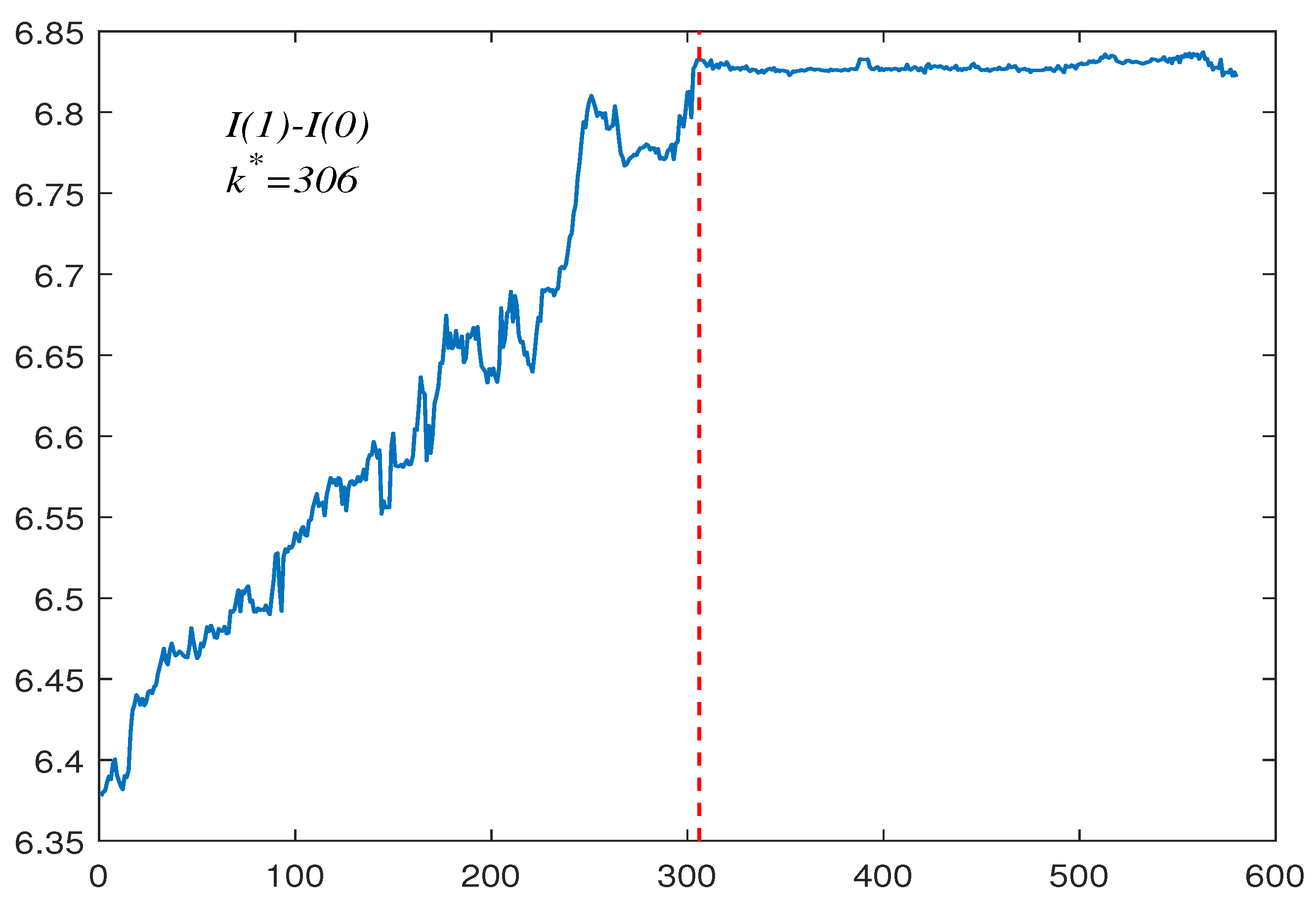

6. Empirical Applications

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Busetti, F.; Taylor, A.R. Tests of stationarity against a change in persistence. J. Econom. 2004, 123, 33–66. [Google Scholar] [CrossRef]

- Chen, W.; Huang, Z.; Yi, Y. Is there a structural change in the persistence of wti–brent oil price spreads in the post-2010 period? Econ. Model. 2015, 50, 64–71. [Google Scholar] [CrossRef]

- Belaire-Franch, J. A note on the evidence of inflation persistence around the world. Empir. Econ. 2019, 56, 1477–1487. [Google Scholar] [CrossRef]

- Sibbertsen, P.; Willert, J. Testing for a break in persistence under long-range dependencies and mean shifts. Stat. Pap. 2012, 53, 357–370. [Google Scholar] [CrossRef]

- Kim, J.Y. Detection of change in persistence of a linear time series. J. Econom. 2000, 95, 97–116. [Google Scholar] [CrossRef]

- Leybourne, S.; Kim, T.H.; Taylor, A.R. Detecting multiple changes in persistence. Stud. Nonlinear Dyn. Econom. 2007, 11. [Google Scholar] [CrossRef]

- Leybourne, S.; Taylor, R.; Kim, T.H. Cusum of squares-based tests for a change in persistence. J. Time Ser. Anal. 2007, 28, 408–433. [Google Scholar] [CrossRef]

- Cerqueti, R.; Costantini, M.; Gutierrez, L.; Westerlund, J. Panel stationary tests against changes in persistence. Stat. Pap. 2019, 60, 1079–1100. [Google Scholar] [CrossRef]

- Kejriwal, M. A robust sequential procedure for estimating the number of structural changes in persistence. Oxf. Bull. Econ. Stat. 2020, 82, 669–685. [Google Scholar] [CrossRef]

- Hao, J.; Si, Z. Spurious regression between long memory series due to mis-specified structural break. Commun.-Stat.-Simul. Comput. 2018, 47, 692–711. [Google Scholar]

- Hao, J.; Si, Z.; Jinsuo, Z. Modified tests for change point in variance in the possible presence of mean breaks. J. Stat. Comput. Simul. 2018, 88, 2651–2667. [Google Scholar]

- Wingert, S.; Mboya, M.P.; Sibbertsen, P. Distinguishing between breaks in the mean and breaks in persistence under long memory. Econ. Lett. 2020, 193, 1093338. [Google Scholar] [CrossRef]

- Grote, C. Issues in Nonlinear Cointegration, Structural Breaks and Changes in Persistence. Ph.D. Thesis, Leibniz Universität Hannover, Hannover, Germany, 2020. [Google Scholar]

- Mittnik, S.; Rachev, S.; Paolella, M. Stable paretian modeling in finance: Some empirical and theoretical aspects. In A Practical Guide to Heavy Tails; Birkhäuser: Boston, MA, USA, 1998; pp. 79–110. [Google Scholar]

- Han, S.; Tian, Z. Bootstrap testing for changes in persistence with heavy-tailed innovations. Commun. Stat. Theory Methods 2007, 36, 2289–2299. [Google Scholar] [CrossRef]

- Qin, R.; Liu, Y. Block bootstrap testing for changes in persistence with heavy-tailed innovations. Commun. Stat. Theory Methods 2018, 47, 1104–1116. [Google Scholar] [CrossRef]

- Chen, Z.; Tian, Z.; Zhao, C. Monitoring persistence change in infinite variance observations. J. Korean Stat. Soc. 2012, 41, 61–73. [Google Scholar] [CrossRef]

- Yang, Y.; Jin, H. Ratio tests for persistence change with heavy tailed observations. J. Netw. 2014, 9, 1409. [Google Scholar] [CrossRef]

- Hao, J.; Si, Z.; Jinsuo, Z. Spurious regression due to the neglected of non-stationary volatility. Comput. Stat. 2017, 32, 1065–1081. [Google Scholar]

- Hao, J.; Jinsuo, Z.; Si, Z. The spurious regression of AR(p) infinite variance series in presence of structural break. Comput. Stat. Data Anal. 2013, 67, 25–40. [Google Scholar]

- Wang, D. Monitoring persistence change in heavy-tailed observations. Symmetry 2021, 13, 936. [Google Scholar] [CrossRef]

- Chan, N.H.; Zhang, R.M. Inference for nearly nonstationary processes under strong dependence with infinite variance. Stat. Sin. 2009, 19, 925–947. [Google Scholar]

- Cheng, Y.; Hui, Y.; McAleer, M.; Wong, W.K. Spurious relationships for nearly non-stationary series. J. Risk Financ. Manag. 2021, 14, 366. [Google Scholar] [CrossRef]

- Paparoditis, E.; Politis, D.N. Residual-based block bootstrap for unit root testing. Econometrica 2003, 71, 813–855. [Google Scholar] [CrossRef]

- Chan, N.H.; Wei, C.Z. Asymptotic inference for nearly nonstationary AR(1) processes. Ann. Stat. 1987, 15, 1050–1063. [Google Scholar] [CrossRef]

- Leybourne, S.J.; Kim, T.H.; Robert Taylor, A. Regression-based tests for a change in persistence. Oxf. Bull. Econ. Stat. 2006, 68, 595–621. [Google Scholar] [CrossRef]

- Phillips, P.C.; Solo, V. Asymptotics for linear processes. Ann. Stat. 1992, 20, 971–1001. [Google Scholar] [CrossRef]

- Ibragimov, I.A. Some limit theorems for stationary processes. Theory Probab. Appl. 1962, 7, 349–382. [Google Scholar] [CrossRef]

- Resnick, S.I. Point processes, regular variation and weak convergence. Adv. Appl. Probab. 1986, 18, 66–138. [Google Scholar] [CrossRef]

- Chan, N.H. Inference for near-integrated time series with infinite variance. J. Am. Assoc. 1990, 85, 1069–1074. [Google Scholar] [CrossRef]

- Mandelbrot, B. The variation of some other speculative prices. J. Bus. 1967, 40, 393–413. [Google Scholar] [CrossRef]

- Arcones, M.A.; Giné, E. The bootstrap of the mean with arbitrary bootstrap sample size. Ann. IHP Probab. Stat. 1989, 25, 457–481. [Google Scholar]

- Chen, Z.; Jin, Z.; Tian, Z.; Qi, P. Bootstrap testing multiple changes in persistence for a heavy-tailed sequence. Comput. Stat. Data Anal. 2012, 56, 2303–2316. [Google Scholar] [CrossRef]

- John, P.N. Numerical calculation of stable densities and distribution functions. Commun. Stat. Stoch. Model. 1997, 13, 759–774. [Google Scholar]

- Cherstvy, A.G.; Vinod, D.; Aghion, E.; Chechkin, A.V.; Metzler, R. Time averaging, ageing and delay analysis of financial time series. New J. Phys. 2017, 19, 063045. [Google Scholar] [CrossRef]

- Yu, Z.; Gao, H.; Cong, X.; Wu, N.; Song, H.H. A Survey on Cyber-Physical Systems Security. IEEE Internet Things J. 2023, 10, 21670–21686. [Google Scholar] [CrossRef]

- Kantz, H.; Schreiber, T. Nonlinear Time Series Analysis; Cambridge University Press: Cambridge, UK, 2004. [Google Scholar]

- Knight, K. Limit theory for autoregressive-parameter estimates in an infinite-variance random walk. Can. J. Stat. 1989, 17, 261–278. [Google Scholar] [CrossRef]

- Amemiya, T. Regression analysis when the dependent variable is truncated normal. Econom. Econom. Soc. 1973, 41, 997–1016. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Q | Q | Q | Q | Q | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (a) Empirical Size | 0.0543 | 0.0480 | 0.0433 | 0.0503 | 0.0527 | 0.0487 | 0.0513 | 0.0443 | 0.0527 | 0.0437 | |

| (b) Power Values | |||||||||||

| 0.9517 | 0.7413 | 0.8653 | 0.5717 | 0.7507 | 0.4043 | 0.5907 | 0.2933 | 0.3923 | 0.0010 | ||

| 0.9170 | 0.6690 | 0.8133 | 0.5147 | 0.6943 | 0.3633 | 0.5307 | 0.2280 | 0.3637 | 0.0003 | ||

| 0.8247 | 0.5273 | 0.7170 | 0.3927 | 0.6003 | 0.2660 | 0.4480 | 0.1757 | 0.3060 | 0.0003 | ||

| 0.9977 | 0.9170 | 0.9750 | 0.7977 | 0.9167 | 0.6570 | 0.7843 | 0.4387 | 0.4957 | 0.0023 | ||

| 0.9910 | 0.8730 | 0.9567 | 0.7420 | 0.8727 | 0.5667 | 0.7177 | 0.3923 | 0.4270 | 0.0017 | ||

| 0.9400 | 0.7410 | 0.8860 | 0.5900 | 0.7777 | 0.4397 | 0.6160 | 0.3083 | 0.3763 | 0.0010 | ||

| 0.9973 | 0.9273 | 0.9860 | 0.8250 | 0.9597 | 0.6723 | 0.8603 | 0.4833 | 0.5407 | 0.0153 | ||

| 0.9860 | 0.8557 | 0.9707 | 0.7413 | 0.9127 | 0.5777 | 0.7793 | 0.4103 | 0.4667 | 0.0090 | ||

| 0.9280 | 0.6757 | 0.8793 | 0.5823 | 0.8027 | 0.4430 | 0.6443 | 0.2957 | 0.4057 | 0.0023 | ||

| 0 | 0 | 0 | 0 | 0 | 0 | 0.0043 | 0 | 0.0140 | 0 | 0.0310 | 0.0003 |

| 0.5 | 0 | 0 | 0 | 0 | 0 | 0 | 0.0010 | 0.0013 | 0.0013 | 0.0047 | |

| 0.9 | 0.0050 | 0 | 0.0047 | 0 | 0.0063 | 0.0037 | 0.0093 | 0.0050 | 0.0057 | 0.0167 | |

| 1.0 | 0.0543 | 0.0473 | 0.0433 | 0.0530 | 0.0527 | 0.0443 | 0.0513 | 0.0480 | 0.0527 | 0.0473 | |

| 0.6 | 0 | 0 | 0 | 0 | 0 | 0.0017 | 0 | 0.0080 | 0.0007 | 0.0593 | 0 |

| 0.5 | 0 | 0 | 0.0040 | 0 | 0.0603 | 0 | 0.2043 | 0.0010 | 0.5140 | 0.0007 | |

| 0.9 | 0 | 0 | 0 | 0 | 0 | 0 | 0.0023 | 0.0020 | 0.0100 | 0.0083 | |

| 1.0 | 0.0507 | 0.0263 | 0.0443 | 0.0180 | 0.0423 | 0.0227 | 0.0503 | 0.0467 | 0.0527 | 0.0403 | |

| −0.6 | 0 | 0 | 0 | 0 | 0 | 0.0053 | 0 | 0.0237 | 0.0003 | 0.0493 | 0.0017 |

| 0.5 | 0 | 0 | 0.0043 | 0 | 0.0287 | 0 | 0.0467 | 0 | 0.0040 | 0.0030 | |

| 0.9 | 0.0170 | 0 | 0.0147 | 0 | 0.0163 | 0.0003 | 0.0150 | 0.0020 | 0.0177 | 0.0083 | |

| 1.0 | 0.0540 | 0.0517 | 0.0550 | 0.0537 | 0.0527 | 0.0240 | 0.0570 | 0.0277 | 0.0450 | 0.0440 | |

| 0 | 1 | 0.0787 | 0.0367 | 0.0647 | 0.0343 | 0.0710 | 0.0430 | 0.0550 | 0.0487 | 0.0387 | 0.0463 |

| 3 | 0.0967 | 0.0153 | 0.0777 | 0.0160 | 0.0697 | 0.0297 | 0.0553 | 0.0303 | 0.0273 | 0.0320 | |

| 5 | 0.0983 | 0.0077 | 0.0727 | 0.0067 | 0.0592 | 0.0190 | 0.0380 | 0.0213 | 0.0237 | 0.0327 | |

| 0.6 | 1 | 0.0607 | 0.0053 | 0.0467 | 0.0050 | 0.0510 | 0.0133 | 0.0547 | 0.0157 | 0.0637 | 0.0287 |

| 3 | 0.0803 | 0.0003 | 0.0503 | 0.0007 | 0.0457 | 0.0033 | 0.0487 | 0.0097 | 0.0540 | 0.0203 | |

| 5 | 0.0480 | 0 | 0.0280 | 0 | 0.0313 | 0.0013 | 0.0373 | 0.0067 | 0.0417 | 0.0240 | |

| −0.6 | 1 | 0.0747 | 0.0293 | 0.0943 | 0.0330 | 0.0853 | 0.0163 | 0.0710 | 0.0233 | 0.0537 | 0.0353 |

| 3 | 0.1193 | 0.0137 | 0.1263 | 0.0210 | 0.0900 | 0.0077 | 0.0853 | 0.0167 | 0.0567 | 0.0250 | |

| 5 | 0.1203 | 0.0093 | 0.1127 | 0.0113 | 0.0907 | 0.0040 | 0.0870 | 0.0107 | 0.0433 | 0.0223 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0.0030 | 0 | 0.0107 | 0.0003 | 0.0273 | 0.0007 |

| 0.5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.0003 | 0.0003 | 0.0037 | |

| 0.9 | 0 | 0 | 0.0013 | 0 | 0.0043 | 0.0007 | 0.0073 | 0.0033 | 0.0033 | 0.0110 | |

| 1.0 | 0.0557 | 0.0470 | 0.0463 | 0.0587 | 0.0407 | 0.0583 | 0.0497 | 0.0453 | 0.0457 | 0.0507 | |

| 0.6 | 0 | 0 | 0 | 0 | 0 | 0.0017 | 0 | 0.0080 | 0 | 0.0480 | 0.0003 |

| 0.5 | 0 | 0 | 0.0063 | 0 | 0.0760 | 0 | 0.2173 | 0 | 0.5233 | 0.0003 | |

| 0.9 | 0 | 0 | 0 | 0 | 0 | 0 | 0.0007 | 0.0003 | 0.0050 | 0.0070 | |

| 1.0 | 0.0537 | 0.0370 | 0.0473 | 0.0277 | 0.0413 | 0.0323 | 0.0560 | 0.0470 | 0.0517 | 0.0490 | |

| −0.6 | 0 | 0 | 0 | 0 | 0 | 0.0040 | 0 | 0.0113 | 0.0007 | 0.0307 | 0.0010 |

| 0.5 | 0 | 0 | 0.0060 | 0 | 0.0243 | 0 | 0.0580 | 0 | 0.0030 | 0.0020 | |

| 0.9 | 0.0010 | 0 | 0.0047 | 0 | 0.0083 | 0.0003 | 0.0113 | 0.0017 | 0.0077 | 0.0090 | |

| 1.0 | 0.0553 | 0.0517 | 0.0563 | 0.0433 | 0.0537 | 0.0453 | 0.0560 | 0.0270 | 0.0447 | 0.0473 | |

| 0 | 1 | 0.0820 | 0.0323 | 0.0647 | 0.0353 | 0.0593 | 0.0507 | 0.0527 | 0.0380 | 0.0347 | 0.0493 |

| 3 | 0.0987 | 0.0143 | 0.0823 | 0.0157 | 0.0690 | 0.0267 | 0.0507 | 0.0310 | 0.0350 | 0.0470 | |

| 5 | 0.1053 | 0.0077 | 0.0763 | 0.0057 | 0.0720 | 0.0157 | 0.0413 | 0.0220 | 0.0190 | 0.0340 | |

| 0.6 | 1 | 0.0733 | 0.0180 | 0.0550 | 0.0077 | 0.0503 | 0.0117 | 0.0597 | 0.0193 | 0.0570 | 0.0313 |

| 3 | 0.0837 | 0.0013 | 0.0550 | 0 | 0.0517 | 0.0030 | 0.0523 | 0.0097 | 0.0593 | 0.0223 | |

| 5 | 0.0670 | 0 | 0.0370 | 0 | 0.0363 | 0.0007 | 0.0490 | 0.0060 | 0.0550 | 0.0183 | |

| −0.6 | 1 | 0.0850 | 0.0370 | 0.0830 | 0.0430 | 0.0737 | 0.0373 | 0.0690 | 0.0200 | 0.0490 | 0.0337 |

| 3 | 0.1187 | 0.0147 | 0.1200 | 0.0227 | 0.1010 | 0.0147 | 0.0943 | 0.0147 | 0.0487 | 0.0290 | |

| 5 | 0.1207 | 0.0070 | 0.1153 | 0.0160 | 0.0890 | 0.0043 | 0.0857 | 0.0117 | 0.0400 | 0.0227 | |

| 0 | 0.3 | 0.3 | 0.9517 | 0 | 0.8653 | 0 | 0.7507 | 0 | 0.6010 | 0 | 0.3923 | 0.0027 |

| 0.5 | 0.9170 | 0 | 0.8133 | 0 | 0.6943 | 0 | 0.5307 | 0.0007 | 0.3637 | 0.0030 | ||

| 0.7 | 0.8247 | 0 | 0.7170 | 0 | 0.6003 | 0 | 0.4480 | 0.0013 | 0.3193 | 0.0073 | ||

| 0.5 | 0.3 | 0.9977 | 0 | 0.9750 | 0 | 0.9167 | 0 | 0.7843 | 0 | 0.4957 | 0.0047 | |

| 0.5 | 0.9910 | 0 | 0.9567 | 0 | 0.8727 | 0 | 0.7177 | 0.0007 | 0.4390 | 0.0067 | ||

| 0.7 | 0.9400 | 0 | 0.8860 | 0 | 0.7827 | 0 | 0.6160 | 0.0017 | 0.3817 | 0.0087 | ||

| 0.7 | 0.3 | 0.9973 | 0 | 0.9907 | 0 | 0.9597 | 0 | 0.8603 | 0 | 0.5557 | 0.0080 | |

| 0.5 | 0.9860 | 0 | 0.9707 | 0 | 0.9127 | 0 | 0.7793 | 0.0007 | 0.4820 | 0.0083 | ||

| 0.7 | 0.9280 | 0 | 0.8793 | 0 | 0.8060 | 0.0003 | 0.6443 | 0.0030 | 0.4097 | 0.0107 | ||

| 0.6 | 0.3 | 0.3 | 0.5710 | 0 | 0.4923 | 0 | 0.4953 | 0 | 0.5487 | 0 | 0.6380 | 0.0023 |

| 0.5 | 0.5637 | 0 | 0.4947 | 0 | 0.5323 | 0 | 0.6337 | 0.0007 | 0.7150 | 0.0013 | ||

| 0.7 | 0.5437 | 0 | 0.4483 | 0 | 0.4503 | 0 | 0.5470 | 0.0003 | 0.6643 | 0.0020 | ||

| 0.5 | 0.3 | 0.8507 | 0 | 0.7693 | 0 | 0.7457 | 0 | 0.7347 | 0.0003 | 0.6463 | 0.0047 | |

| 0.5 | 0.8287 | 0 | 0.7290 | 0 | 0.7353 | 0 | 0.7497 | 0.0007 | 0.7000 | 0.0063 | ||

| 0.7 | 0.7520 | 0 | 0.6437 | 0 | 0.6317 | 0 | 0.6423 | 0.0020 | 0.6340 | 0.0063 | ||

| 0.7 | 0.3 | 0.8663 | 0 | 0.8067 | 0 | 0.7600 | 0 | 0.7430 | 0.0003 | 0.6177 | 0.0067 | |

| 0.5 | 0.8227 | 0 | 0.7207 | 0 | 0.6887 | 0 | 0.6617 | 0.0017 | 0.5940 | 0.0067 | ||

| 0.7 | 0.7303 | 0 | 0.6343 | 0 | 0.5740 | 0 | 0.5537 | 0.0020 | 0.5067 | 0.0137 | ||

| −0.6 | 0.3 | 0.3 | 0.9867 | 0 | 0.9420 | 0 | 0.8710 | 0 | 0.7827 | 0 | 0.6127 | 0.0023 |

| 0.5 | 0.9593 | 0 | 0.9067 | 0 | 0.8173 | 0 | 0.6867 | 0 | 0.4093 | 0.0017 | ||

| 0.7 | 0.8883 | 0 | 0.8100 | 0 | 0.6680 | 0 | 0.5193 | 0 | 0.3640 | 0.0043 | ||

| 0.5 | 0.3 | 0.9993 | 0 | 0.9903 | 0 | 0.9557 | 0 | 0.8803 | 0 | 0.6103 | 0.0040 | |

| 0.5 | 0.9963 | 0 | 0.9793 | 0 | 0.9043 | 0 | 0.7607 | 0 | 0.4693 | 0.0033 | ||

| 0.7 | 0.9677 | 0 | 0.9170 | 0 | 0.7907 | 0 | 0.6303 | 0.0007 | 0.3990 | 0.0047 | ||

| 0.7 | 0.3 | 0.9993 | 0 | 0.9940 | 0 | 0.9633 | 0 | 0.8703 | 0 | 0.5747 | 0.0033 | |

| 0.5 | 0.9957 | 0 | 0.9813 | 0 | 0.8983 | 0 | 0.7483 | 0 | 0.4750 | 0.0050 | ||

| 0.7 | 0.9573 | 0 | 0.9247 | 0 | 0.7837 | 0 | 0.6143 | 0.0007 | 0.3913 | 0.0080 | ||

| 0 | 0.3 | 0.3 | 0.9920 | 0 | 0.9217 | 0 | 0.8327 | 0 | 0.6577 | 0 | 0.4313 | 0.0017 |

| 0.5 | 0.9803 | 0 | 0.9073 | 0 | 0.7797 | 0 | 0.6040 | 0 | 0.3983 | 0.0030 | ||

| 0.7 | 0.9357 | 0 | 0.8263 | 0 | 0.7060 | 0 | 0.5520 | 0.0007 | 0.3457 | 0.0047 | ||

| 0.5 | 0.3 | 1 | 0 | 0.9870 | 0 | 0.9563 | 0 | 0.8573 | 0 | 0.5637 | 0.0030 | |

| 0.5 | 0.9990 | 0 | 0.9823 | 0 | 0.9237 | 0 | 0.7860 | 0.0007 | 0.4890 | 0.0067 | ||

| 0.7 | 0.9907 | 0 | 0.9570 | 0 | 0.8720 | 0 | 0.6993 | 0.0010 | 0.4280 | 0.0063 | ||

| 0.7 | 0.3 | 1 | 0 | 0.9990 | 0 | 0.9797 | 0 | 0.9230 | 0 | 0.6180 | 0.0023 | |

| 0.5 | 1 | 0 | 0.9927 | 0 | 0.9537 | 0 | 0.8567 | 0 | 0.5393 | 0.0060 | ||

| 0.7 | 0.9877 | 0 | 0.9633 | 0 | 0.8980 | 0.0007 | 0.7550 | 0.0007 | 0.4627 | 0.0107 | ||

| 0.6 | 0.3 | 0.3 | 0.7213 | 0 | 0.6367 | 0 | 0.5947 | 0 | 0.6173 | 0 | 0.6917 | 0.0020 |

| 0.5 | 0.7253 | 0 | 0.6310 | 0 | 0.6350 | 0 | 0.7010 | 0 | 0.7487 | 0.0017 | ||

| 0.7 | 0.6963 | 0 | 0.5963 | 0 | 0.5887 | 0 | 0.6267 | 0 | 0.7187 | 0.0030 | ||

| 0.5 | 0.3 | 0.9427 | 0 | 0.8863 | 0 | 0.8350 | 0 | 0.8013 | 0 | 0.6810 | 0.0053 | |

| 0.5 | 0.9397 | 0 | 0.8593 | 0 | 0.8223 | 0 | 0.8137 | 0 | 0.7363 | 0.0053 | ||

| 0.7 | 0.8967 | 0 | 0.7960 | 0 | 0.7743 | 0 | 0.7053 | 0 | 0.6927 | 0.0043 | ||

| 0.7 | 0.3 | 0.9693 | 0 | 0.9170 | 0 | 0.8490 | 0 | 0.8177 | 0 | 0.6667 | 0.0053 | |

| 0.5 | 0.9393 | 0 | 0.8720 | 0 | 0.8013 | 0 | 0.7557 | 0 | 0.6413 | 0.0060 | ||

| 0.7 | 0.8887 | 0 | 0.7880 | 0 | 0.7027 | 0 | 0.6490 | 0.0003 | 0.5513 | 0.0097 | ||

| −0.6 | 0.3 | 0.3 | 0.9993 | 0 | 0.9820 | 0 | 0.9190 | 0 | 0.8440 | 0 | 0.6530 | 0 |

| 0.5 | 0.9950 | 0 | 0.9597 | 0 | 0.8873 | 0 | 0.7367 | 0 | 0.4600 | 0.0020 | ||

| 0.7 | 0.9583 | 0 | 0.9067 | 0 | 0.7660 | 0 | 0.6250 | 0 | 0.3983 | 0.0037 | ||

| 0.5 | 0.3 | 1 | 0 | 0.9987 | 0 | 0.9793 | 0 | 0.9023 | 0 | 0.6710 | 0.0007 | |

| 0.5 | 1 | 0 | 0.9957 | 0 | 0.9397 | 0 | 0.8127 | 0 | 0.5087 | 0.0037 | ||

| 0.7 | 0.9953 | 0 | 0.9747 | 0 | 0.8743 | 0 | 0.7107 | 0 | 0.4563 | 0.0057 | ||

| 0.7 | 0.3 | 1 | 0 | 0.9987 | 0 | 0.9807 | 0 | 0.9143 | 0 | 0.6290 | 0.0017 | |

| 0.5 | 1 | 0 | 0.9953 | 0 | 0.9337 | 0 | 0.8033 | 0 | 0.5123 | 0.0037 | ||

| 0.7 | 0.9967 | 0 | 0.9720 | 0 | 0.8637 | 0 | 0.7013 | 0 | 0.4497 | 0.0050 | ||

| 0.3 | 0.3 | 0.3352 | 0.0869 | 0.3357 | 0.1005 | 0.3539 | 0.1363 | 0.3910 | 0.1909 | 0.4335 | 0.2344 |

| 0.5 | 0.3698 | 0.1386 | 0.3639 | 0.1390 | 0.3648 | 0.1501 | 0.3904 | 0.1869 | 0.4276 | 0.2272 | |

| 0.7 | 0.4097 | 0.1895 | 0.3996 | 0.1817 | 0.3849 | 0.1731 | 0.3697 | 0.1661 | 0.3608 | 0.1719 | |

| 0.5 | 0.3 | 0.5335 | 0.0841 | 0.5277 | 0.0891 | 0.5263 | 0.1087 | 0.5279 | 0.1350 | 0.5217 | 0.1578 |

| 0.5 | 0.5538 | 0.1093 | 0.5393 | 0.1094 | 0.5378 | 0.1206 | 0.5246 | 0.1377 | 0.5200 | 0.1589 | |

| 0.7 | 0.5708 | 0.1436 | 0.5564 | 0.1441 | 0.5359 | 0.1487 | 0.5115 | 0.1577 | 0.4737 | 0.1765 | |

| 0.7 | 0.3 | 0.7185 | 0.0557 | 0.7103 | 0.0618 | 0.6941 | 0.0973 | 0.6831 | 0.1194 | 0.6498 | 0.1749 |

| 0.5 | 0.7201 | 0.0732 | 0.7102 | 0.0867 | 0.6963 | 0.1071 | 0.6815 | 0.1317 | 0.6533 | 0.1748 | |

| 0.7 | 0.7188 | 0.1059 | 0.7062 | 0.1215 | 0.6937 | 0.1397 | 0.6642 | 0.1736 | 0.6294 | 0.2082 | |

| 0.3 | 0.3 | 0.3332 | 0.0794 | 0.3528 | 0.1086 | 0.3868 | 0.1539 | 0.4450 | 0.2166 | 0.5106 | 0.2814 |

| 0.5 | 0.3462 | 0.1042 | 0.3674 | 0.1345 | 0.3971 | 0.1700 | 0.4511 | 0.2273 | 0.5089 | 0.2844 | |

| 0.7 | 0.3702 | 0.1493 | 0.3882 | 0.1678 | 0.4101 | 0.1901 | 0.4525 | 0.2300 | 0.5051 | 0.2831 | |

| 0.5 | 0.3 | 0.5177 | 0.0898 | 0.5312 | 0.1153 | 0.5605 | 0.1430 | 0.5886 | 0.1805 | 0.6184 | 0.2152 |

| 0.5 | 0.5134 | 0.1134 | 0.5219 | 0.1297 | 0.5473 | 0.1540 | 0.5766 | 0.1843 | 0.5975 | 0.2131 | |

| 0.7 | 0.5055 | 0.1457 | 0.5193 | 0.1534 | 0.5366 | 0.1655 | 0.5643 | 0.1874 | 0.5747 | 0.2126 | |

| 0.7 | 0.3 | 0.7028 | 0.0894 | 0.7088 | 0.1068 | 0.7036 | 0.1358 | 0.7081 | 0.1548 | 0.6871 | 0.1900 |

| 0.5 | 0.6797 | 0.1273 | 0.6876 | 0.1365 | 0.6812 | 0.1595 | 0.6798 | 0.1774 | 0.6594 | 0.2073 | |

| 0.7 | 0.6415 | 0.1773 | 0.6408 | 0.1858 | 0.6407 | 0.1980 | 0.6392 | 0.2078 | 0.6276 | 0.2226 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, S.; Jin, H.; Su, M. Modified Block Bootstrap Testing for Persistence Change in Infinite Variance Observations. Mathematics 2024, 12, 258. https://doi.org/10.3390/math12020258

Zhang S, Jin H, Su M. Modified Block Bootstrap Testing for Persistence Change in Infinite Variance Observations. Mathematics. 2024; 12(2):258. https://doi.org/10.3390/math12020258

Chicago/Turabian StyleZhang, Si, Hao Jin, and Menglin Su. 2024. "Modified Block Bootstrap Testing for Persistence Change in Infinite Variance Observations" Mathematics 12, no. 2: 258. https://doi.org/10.3390/math12020258

APA StyleZhang, S., Jin, H., & Su, M. (2024). Modified Block Bootstrap Testing for Persistence Change in Infinite Variance Observations. Mathematics, 12(2), 258. https://doi.org/10.3390/math12020258