Valuation of Commodity-Linked Bond with Stochastic Convenience Yield, Stochastic Volatility, and Credit Risk in an Intensity-Based Model

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Model

3. Pricing of Commodity-Linked Bond

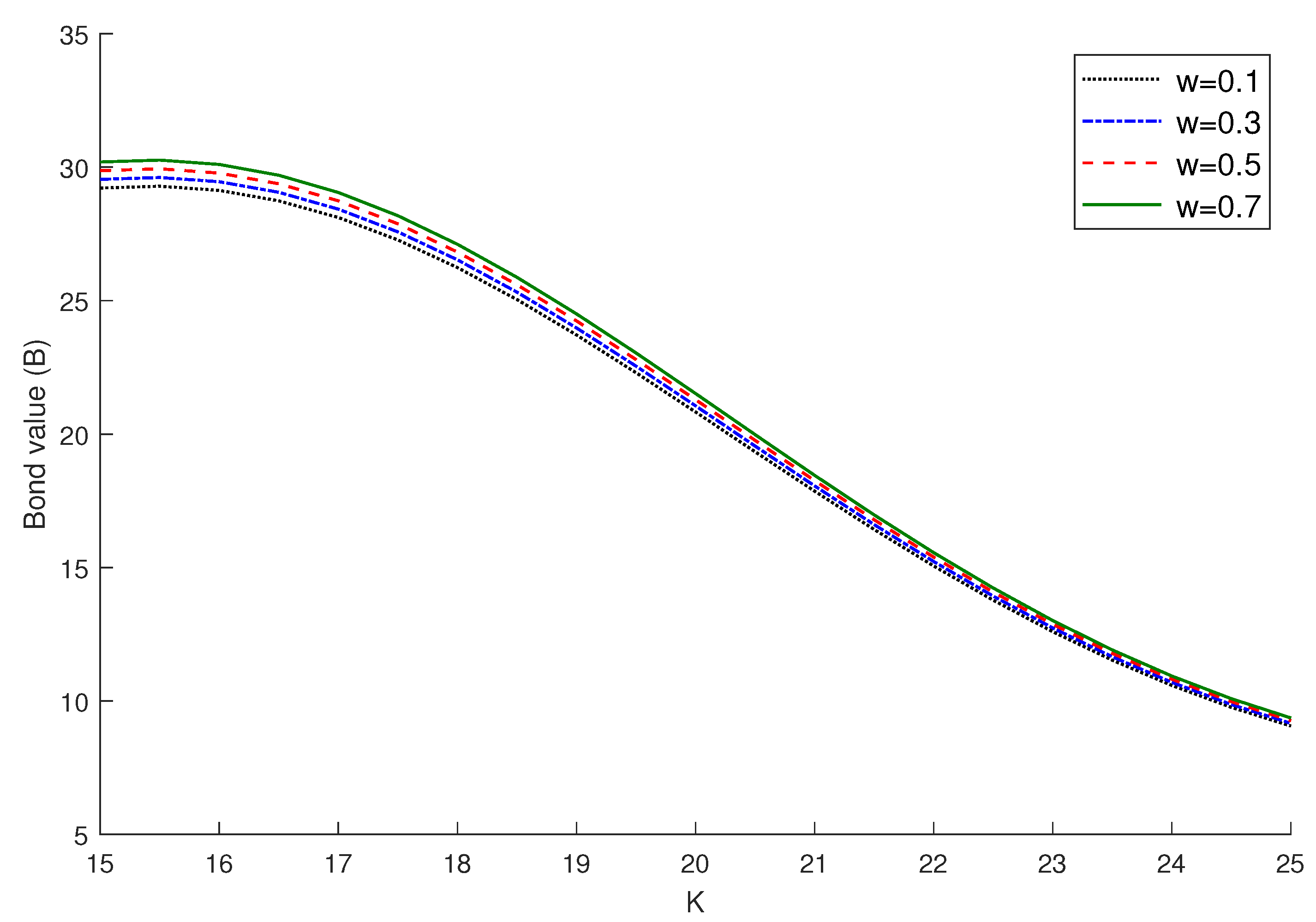

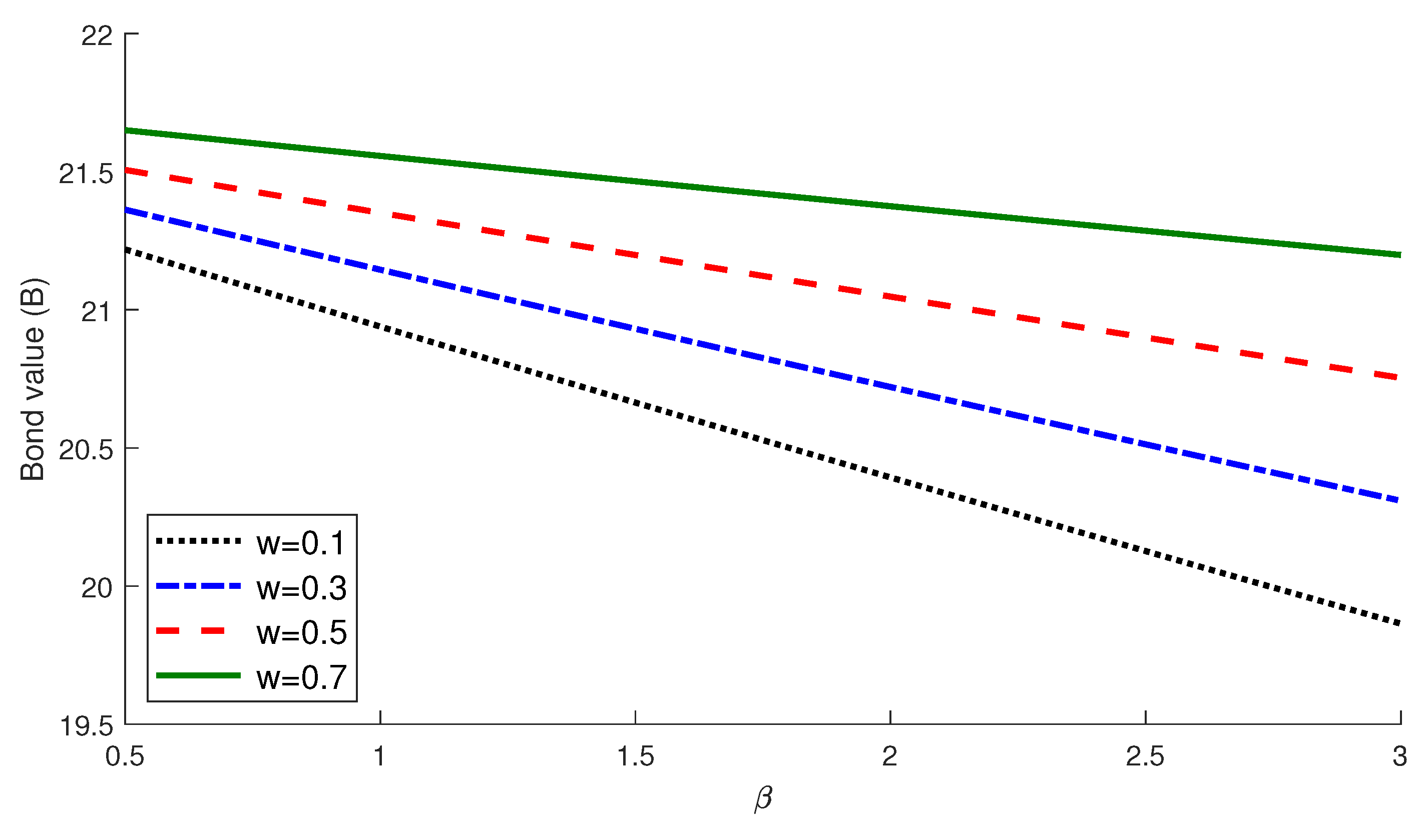

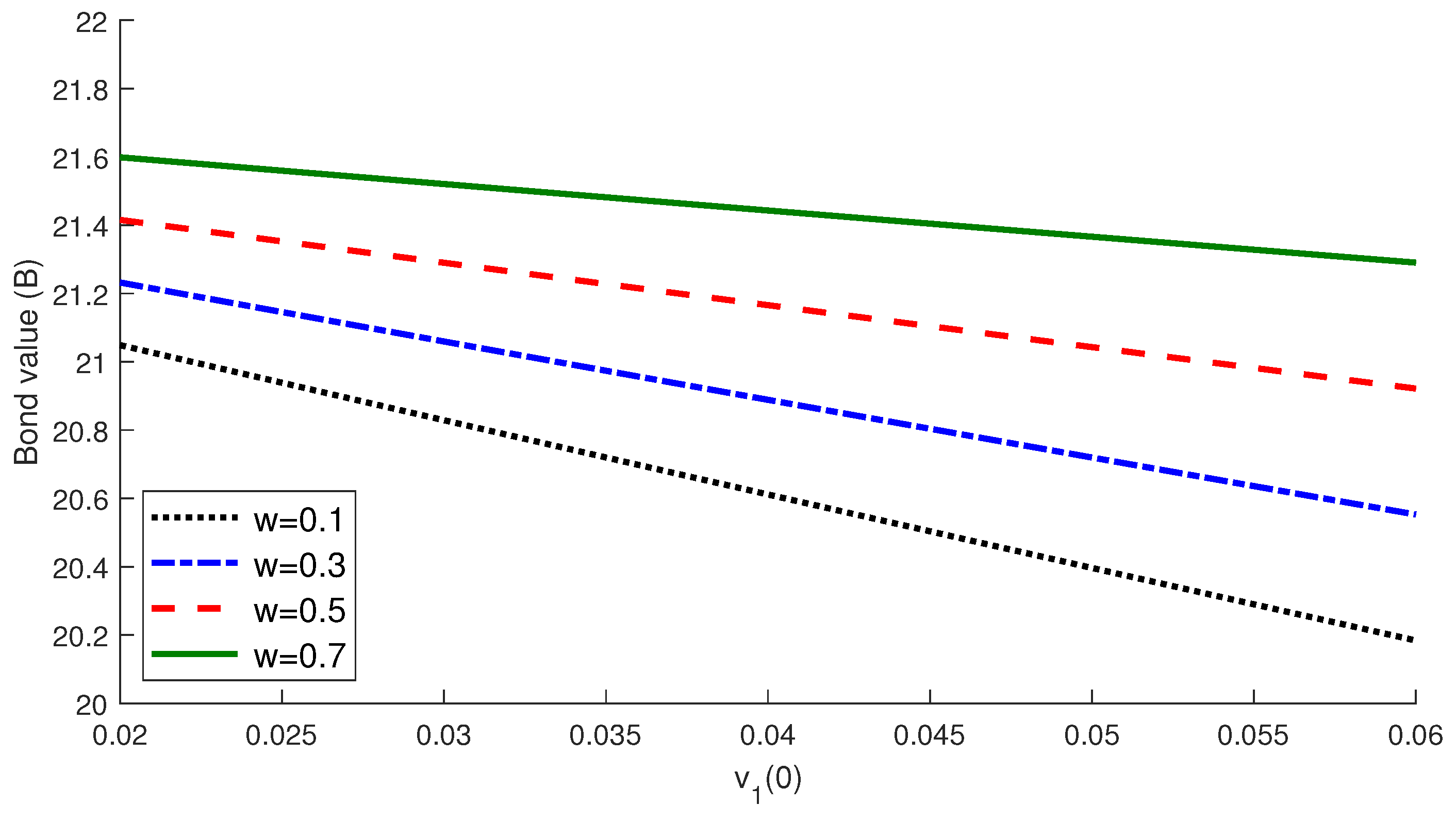

4. Numerical Example

5. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Johnson, H.; Stulz, R. The pricing of options with default risk. J. Financ. 1987, 42, 267–280. [Google Scholar] [CrossRef]

- Klein, P. Pricing Black-Scholes options with correlated credit risk. J. Bank. Financ. 1996, 20, 1211–1229. [Google Scholar] [CrossRef]

- Yang, S.J.; Lee, M.K.; Kim, J.H. Pricing vulnerable options under a stochastic volatility model. Appl. Math. Lett. 2014, 34, 7–12. [Google Scholar] [CrossRef]

- Wang, G.; Wang, X.; Zhou, K. Pricing vulnerable options with stochastic volatility. Phys. A Stat. Mech. Its Appl. 2017, 485, 91–103. [Google Scholar] [CrossRef]

- Ma, C.; Yue, S.; Wu, H.; Ma, Y. Pricing Vulnerable Options with Stochastic Volatility and Stochastic Interest Rate. Comput. Econ. 2020, 56, 391–429. [Google Scholar] [CrossRef]

- Jeon, J.; Kim, G.; Huh, J. An asymptotic expansion approach to the valuation of vulnerable options under a multiscale stochastic volatility model. Chaos Solitons Fractals 2021, 144, 110641. [Google Scholar] [CrossRef]

- Xu, W.; Xu, W.; Li, H.; Xiao, W. A jump-diffusion approach to modelling vulnerable option pricing. Financ. Res. Lett. 2012, 9, 48–56. [Google Scholar] [CrossRef]

- Tian, L.; Wang, G.; Wang, X.; Wang, Y. Pricing vulnerable options with correlated credit risk under jump-diffusion processes. J. Futur. Mark. 2014, 34, 957–979. [Google Scholar] [CrossRef]

- Han, X. Valuation of vulnerable options under the double exponential jump model with stochastic volatility. Probab. Eng. Inf. Sci. 2019, 33, 81–104. [Google Scholar] [CrossRef]

- Klein, P.; Inglis, M. Valuation of European options subject to financial distress and interest rate risk. J. Deriv. 1999, 6, 44–56. [Google Scholar] [CrossRef]

- Lv, G.; Xu, P.; Zhang, Y. Pricing of vulnerable options based on an uncertain CIR interest rate model. AIMS Math. 2023, 8, 11113–11130. [Google Scholar] [CrossRef]

- Liao, S.L.; Huang, H.H. Pricing Black–Scholes options with correlated interest rate risk and credit risk: An extension. Quant. Financ. 2005, 5, 443–457. [Google Scholar] [CrossRef]

- Wang, W.; Wang, W. Pricing vulnerable options under a Markov-modulated regime switching model. Commun. Stat. Methods 2010, 39, 3421–3433. [Google Scholar] [CrossRef]

- Niu, H.; Wang, D. Pricing vulnerable options with correlated jump-diffusion processes depending on various states of the economy. Quant. Financ. 2016, 16, 1129–1145. [Google Scholar] [CrossRef]

- Xie, Y.; Deng, G. Vulnerable European option pricing in a Markov regime-switching Heston model with stochastic interest rate. Chaos Solitons Fractals 2022, 156, 111896. [Google Scholar] [CrossRef]

- Yoon, J.H.; Kim, J.H. The pricing of vulnerable options with double Mellin transforms. J. Math. Anal. Appl. 2015, 422, 838–857. [Google Scholar] [CrossRef]

- Guardasoni, C.; Rodrigo, M.R.; Sanfelici, S. A Mellin transform approach to barrier option pricing. IMA J. Manag. Math. 2020, 31, 49–67. [Google Scholar] [CrossRef]

- Kim, G.; Koo, E. Closed-form pricing formula for exchange option with credit risk. Chaos Solitons Fractals 2016, 91, 221–227. [Google Scholar] [CrossRef]

- Kim, D.; Yoon, J.H.; Kim, G. Closed-form pricing formula for foreign equity option with credit risk. Adv. Differ. Equ. 2021, 2021, 1–17. [Google Scholar] [CrossRef]

- Fard, F.A. Analytical pricing of vulnerable options under a generalized jump–diffusion model. Insur. Math. Econ. 2015, 60, 19–28. [Google Scholar] [CrossRef]

- Koo, E.; Kim, G. Explicit formula for the valuation of catastrophe put option with exponential jump and default risk. Chaos Solitons Fractals 2017, 101, 1–7. [Google Scholar] [CrossRef]

- Wang, X. Analytical valuation of vulnerable options in a discrete-time framework. Probab. Eng. Inf. Sci. 2017, 31, 100–120. [Google Scholar] [CrossRef]

- Wang, X. Analytical valuation of vulnerable European and Asian options in intensity-based models. J. Comput. Appl. Math. 2021, 393, 113412. [Google Scholar] [CrossRef]

- Wang, X. Pricing vulnerable fader options under stochastic volatility models. J. Ind. Manag. Optim. 2023, 19, 5749–5766. [Google Scholar] [CrossRef]

- Schwartz, E.S. The pricing of commodity-linked bonds. J. Financ. 1982, 37, 525–539. [Google Scholar]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Cox, J.C.; Ross, S.A. The valuation of options for alternative stochastic processes. J. Financ. Econ. 1976, 3, 145–166. [Google Scholar] [CrossRef]

- Carr, P. A note on the pricing of commodity-linked bonds. J. Financ. 1987, 42, 1071–1076. [Google Scholar]

- Yan, X. Valuation of commodity derivatives in a new multi-factor model. Rev. Deriv. Res. 2002, 5, 251–271. [Google Scholar] [CrossRef]

- Ma, Z.; Ma, C.; Wu, Z. Pricing commodity-linked bonds with stochastic convenience yield, interest rate and counterparty credit risk: Application of Mellin transform methods. Rev. Deriv. Res. 2022, 25, 47–91. [Google Scholar] [CrossRef]

- Schwartz, E.S. The stochastic behavior of commodity prices: Implications for valuation and hedging. J. Financ. 1997, 52, 923–973. [Google Scholar] [CrossRef]

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef]

- Cox, J.C.; Ingersoll, J.E., Jr.; Ross, S.A. A theory of the term structure of interest rates. In Theory of Valuation; World Scientific: Singapore, 2005; pp. 129–164. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jeon, J.; Kim, G. Valuation of Commodity-Linked Bond with Stochastic Convenience Yield, Stochastic Volatility, and Credit Risk in an Intensity-Based Model. Mathematics 2023, 11, 4969. https://doi.org/10.3390/math11244969

Jeon J, Kim G. Valuation of Commodity-Linked Bond with Stochastic Convenience Yield, Stochastic Volatility, and Credit Risk in an Intensity-Based Model. Mathematics. 2023; 11(24):4969. https://doi.org/10.3390/math11244969

Chicago/Turabian StyleJeon, Junkee, and Geonwoo Kim. 2023. "Valuation of Commodity-Linked Bond with Stochastic Convenience Yield, Stochastic Volatility, and Credit Risk in an Intensity-Based Model" Mathematics 11, no. 24: 4969. https://doi.org/10.3390/math11244969

APA StyleJeon, J., & Kim, G. (2023). Valuation of Commodity-Linked Bond with Stochastic Convenience Yield, Stochastic Volatility, and Credit Risk in an Intensity-Based Model. Mathematics, 11(24), 4969. https://doi.org/10.3390/math11244969