Designing an Accounting Course Module on Cost Allocation: Pedagogical and Didactical Considerations from a Norwegian Perspective

Abstract

1. Introduction

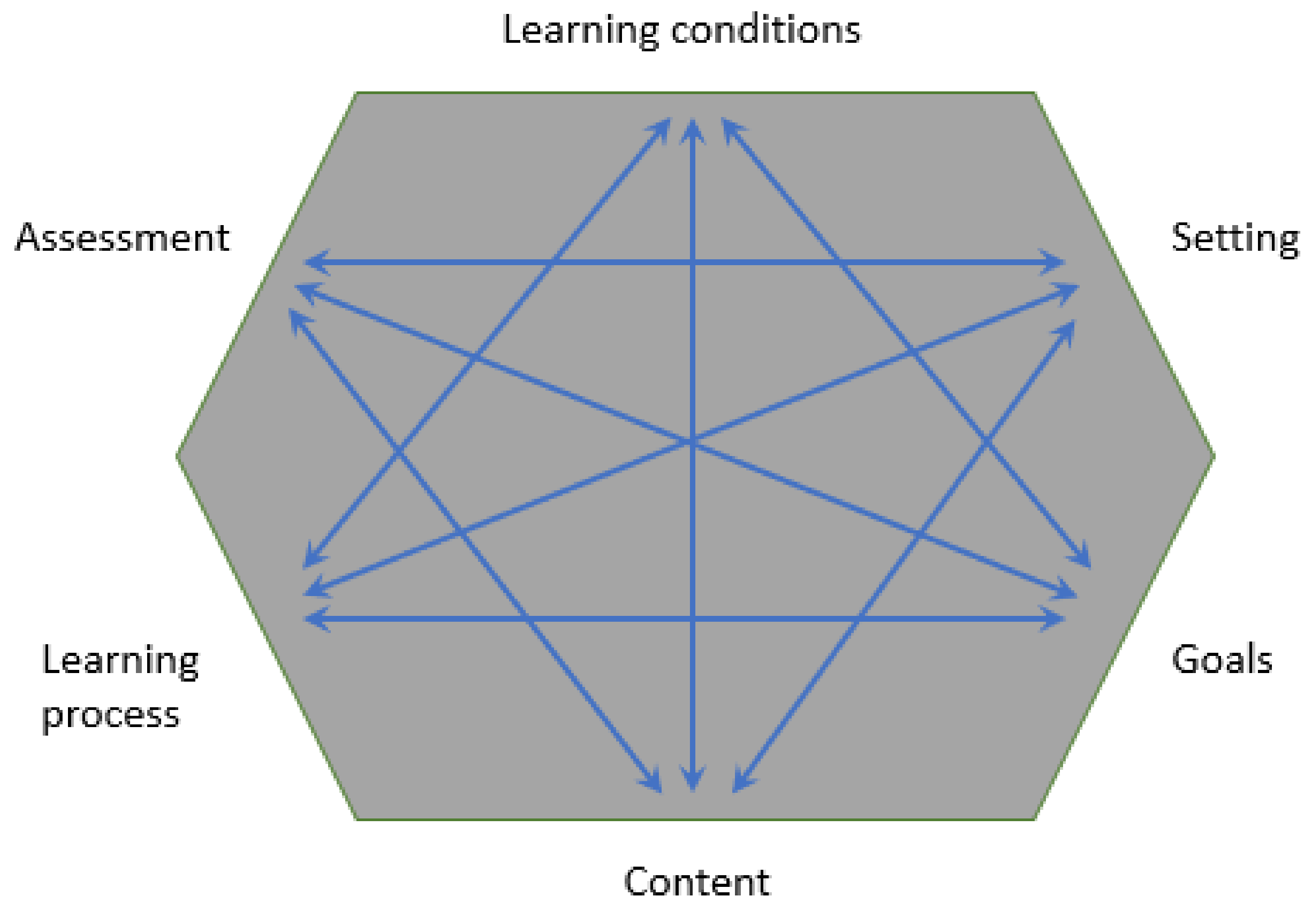

2. Theoretical Foundation—The Didactical Relationship Model

3. The Six Conditioning Factors Described: Reflections from a Norwegian Context

3.1. Learning Goals and Objectives

3.2. Module Content

3.3. The Learning Process

- The traditional lecture-based format with PowerPoint slides, black- and whiteboards, and short video presentations aimed at providing an outline of work to be covered (i.e., to introduce and describe the diverse approaches to cost allocation and their inherent features and drawbacks). It should be noted here that all face-to-face lecture materials, such as PowerPoint slides, are normally uploaded online on a weekly basis. Guest lectures with business representatives are also delivered whenever possible. Drawing upon real-life cases and experiences, guest lectures are thought to make classes more approachable and appealing to students.

- The group discussion format (team learning) with the case-study model geared towards giving opportunity for reflection on and the application of material covered in lectures, as well as discussing issues related to course (module) matter (i.e., to juxtapose the costing approaches, critically discuss them, and reflect on their applications).

3.4. Assessment

- A high-stakes individual written school exam that takes place at the end of the learning process and encompasses the integral parts of the course (including those taught under the rubric of cost allocation). The contribution of this end-of-semester summative assessment to the final grade is worth 100%. During the lockdown, the assessment changed into a 100% individual written home exam. Although falling short for the purpose of assessing knowledge at the higher levels of synthesis and evaluation, it deems appropriate for gauging knowledge and comprehension OB#1–2. Albeit to a lesser extent, it also aids in assessing applying skills OB#3. Since the module in question centers largely around teaching rather structured material, incorporating inter alia facts, management accounting concepts and tools, the degree of learning is best captured using behaviorist assessment methods.

- A group assignment that occurs in the middle of the learning process and deals exclusively with cost allocation issues. The pass/fail scale is applied as an independent scale with only two possible results. This type of assessment is primarily geared towards applying and analyzing OB#3–6 traditional and contemporary methods of cost allocation to particular situations and for diverse purposes. This kind of approach to assessment entails setting students a series of ‘problems’ to be tackled in groups. It is an informal atmosphere that permits students to curb the fear of failure and feel rather comfortable and relaxed. As pointed out earlier, such interaction and dialogue with peers offers a unique opportunity for ‘scaffolding’ and is viewed pivotal to further learning, thereby aiding students to develop higher-order thinking skills (i.e., deep learning). Thus far, the elements of socio-constructivist perspective on learning, including Bakhtin’s and Vygotsky’s thoughts on dialogues [28], are key to this type of assessment as students are encouraged to form study groups to solve the assignment and, more importantly, critically reflect on the results [27].

3.5. Settings

3.6. Learning Conditions

4. Summary and Looking Ahead

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Hiim, H.; Hippe, E. Læring Gjennom Opplevelse, Forståelse og Handling: En Studiebok i Didaktikk; Universitetsforlaget: Oslo, Norway, 1998. [Google Scholar]

- Skagen, T.; Torras, M.C.; Kavli, S.M.; Mikki, S.; Hafstad, S.; Hunskår, I. Pedagogical considerations in developing an online tutorial in information literacy. Commun. Inf. Lit. 2009, 2, 4. [Google Scholar] [CrossRef]

- Bjørndal, B.; Lieberg, S. Nye Veier i Didaktikken?: En Innføring i Didaktiske Emner og Begreper; Aschehoug: Oslo, Norway, 1978. [Google Scholar]

- Pettersen, R.C. Didaktiske modeller og verktøy. In Kvalitetslæring i Høgere Utdanning. Innføring i Problem-og Praksisbasert Didaktikk; Pettersen, R.C., Ed.; Universitetsforlaget: Oslo, Norway, 2005; pp. 3–50. [Google Scholar]

- Norwegian Ministry of Education. Nasjonalt Kvalifikasjonsrammeverk for Livslang Læring [NKR]; Norwegian Ministry of Education: Oslo, Norway, 2011. [Google Scholar]

- Bloom, B.; Englehart, M.; Furst, E.; Hill, W.; Krathwohl, D. Taxonomy of Educational Objectives, The Classication of Educational Goals, Handbook 1: Cognitive Domain; David McKay: New York, NY, USA, 1956. [Google Scholar]

- Bloom, B.S. Reflections on the Development and Use of the Taxonomy. In Bloom’s Taxonomy: A Forty-Year Retrospective; Anderson, L.W., Sosniak, L.A., Eds.; The National Society for the Study of Education: Chicago, IL, USA, 1994; pp. 1–8. [Google Scholar]

- Biggs, J.B.; Collis, K.F. Evaluating the Quality of Learning: The SOLO Taxonomy (Structure of the Observed Learning Outcome); Academic Press: Cambridge, MA, USA, 2014. [Google Scholar]

- Handy, S.; Basile, A. Improving accounting education using Bloom’s taxonomy of educational objectives. J. Appl. Res. Bus. Instr. 2005, 3, 1–6. [Google Scholar]

- Davidson, R.A.; Baldwin, B.A. Cognitive skills objectives in intermediate accounting textbooks: Evidence from end-of-chapter material. J. Account. Educ. 2005, 23, 79–95. [Google Scholar] [CrossRef]

- Lucas, U.; Mladenovic, R. The identification of variation in students’ understandings of disciplinary concepts: The application of the SOLO taxonomy within introductory accounting. High. Educ. 2009, 58, 257–283. [Google Scholar] [CrossRef]

- BIGGS, J. Multimodal learning and the quality of intelligent behavior. In Intelligence: Reconceptualization and Measurement; Rowe, H., Ed.; Laurence Erlbaum: Hillsdale, NJ, USA, 1991; pp. 57–76. [Google Scholar]

- Boulton-Lewis, G. Applying the SOLO taxonomy to learning in higher education. In Teaching and Learning in Higher Education; Dart, B., Boulton-Lewis, G., Eds.; Australian Council for Educational Research: Melbourne, Australia, 1998; pp. 201–221. [Google Scholar]

- Hattie, J.A.; Donoghue, G.M. Learning strategies: A synthesis and conceptual model. NPJ Sci. Learn. 2016, 1, 1–13. [Google Scholar] [CrossRef] [PubMed]

- Entwistle, N.; Smith, C. Personal understanding and target understanding: Mapping influences on the outcomes of learning. Br. J. Educ. Psychol. 2002, 72, 321–342. [Google Scholar] [CrossRef] [PubMed]

- Duff, A.; McKinstry, S. Students’ approaches to learning. Issues Account. Educ. 2007, 22, 183–214. [Google Scholar] [CrossRef]

- Birkett, B.; Mladenovic, R. The approaches to learning paradigm: Theoretical and empirical issues for accounting education research. In Proceedings of the AAANZ Conference, Perth, Australia, 7–9 July 2002. [Google Scholar]

- Lucas, U.; Meyer, J.H. Supporting student awareness: Understanding student preconceptions of their subject matter within introductory courses. Innov. Educ. Teach. Int. 2004, 41, 459–471. [Google Scholar] [CrossRef]

- Hall, M.; Ramsay, A.; Raven, J. Changing the learning environment to promote deep learning approaches in first-year accounting students. Account. Educ. 2004, 13, 489–505. [Google Scholar] [CrossRef]

- Fink, L.D. Creating Significant Learning Experiences: An Integrated Approach to Designing College Courses; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Opdecam, E.; Everaert, P. Seven disagreements about cooperative learning. Account. Educ. 2018, 27, 223–233. [Google Scholar] [CrossRef]

- Hwang, N.C.R.; Lui, G.; Tong, M.Y.J.W. An empirical test of cooperative learning in a passive learning environment. Issues Account. Educ. 2005, 20, 151–165. [Google Scholar] [CrossRef]

- Aldamen, H.; Al-Esmail, R.; Hollindale, J. Does lecture capturing impact student performance and attendance in an introductory accounting course? Account. Educ. 2015, 24, 291–317. [Google Scholar] [CrossRef]

- Opdecam, E.; Everaert, P. Choice-based learning: Lecture-based or team learning? Account. Educ. 2019, 28, 239–273. [Google Scholar] [CrossRef]

- Montano, J.L.A.; Donoso, J.A.; Hassall, T.; Joyce, J. Vocational skills in the accounting professional profile: The Chartered Institute of Management Accountants (CIMA) employers’ opinion. Account. Educ. 2001, 10, 299–313. [Google Scholar] [CrossRef]

- Vygotsky, L.S. Interaction between Learning and Development; W.H. Freeman and Company: New York, NY, USA, 1997. [Google Scholar]

- Dolin, J. Undervisning for livet. In Universitetspædagogik; Rienecker, L., Jørgensen, P.S., Dolin, J., Ingerslev, G.H., Eds.; Samfundslitteratur: Fredriksberg, Sweden, 2013. [Google Scholar]

- Kubli, F. Science teaching as a dialogue–Bakhtin, Vygotsky and some applications in the classroom. Sci. Educ. 2005, 14, 501–534. [Google Scholar] [CrossRef]

- Scaife, J.; Wellington, J. Varying perspectives and practices in formative and diagnostic assessment: A case study. J. Educ. Teach. 2010, 36, 137–151. [Google Scholar] [CrossRef]

- Black, P.; Wiliam, D. Assessment and classroom learning. Assess. Educ. Princ. Policy Pract. 1998, 5, 7–74. [Google Scholar] [CrossRef]

- Peimani, N.; Kamalipour, H. Online Education and the COVID-19 Outbreak: A Case Study of Online Teaching during Lockdown. Educ. Sci. 2021, 11, 72. [Google Scholar] [CrossRef]

- García-Alberti, M.; Suárez, F.; Chiyón, I.; Mosquera Feijoo, J.C. Challenges and Experiences of Online Evaluation in Courses of Civil Engineering during the Lockdown Learning Due to the COVID-19 Pandemic. Educ. Sci. 2021, 11, 59. [Google Scholar] [CrossRef]

- Amhag, L.; Hellström, L.; Stigmar, M. Teacher educators’ use of digital tools and needs for digital competence in higher education. J. Digit. Learn. Teach. Educ. 2019, 35, 203–220. [Google Scholar] [CrossRef]

- Ramachandran Rackliffe, U.; Ragland, L. Excel in the accounting curriculum: Perceptions from accounting professors. Account. Educ. 2016, 25, 139–166. [Google Scholar] [CrossRef]

- Willis, V.F. A model for teaching technology: Using Excel in an accounting information systems course. J. Account. Educ. 2016, 36, 87–99. [Google Scholar] [CrossRef]

- Wang, A.I.; Tahir, R. The effect of using Kahoot! for learning–A literature review. Comput. Educ. 2020, 149, 103818. [Google Scholar] [CrossRef]

- Rudolph, J. A brief review of Mentimeter—A student response system. J. Appl. Learn. Teach. 2018, 1, 35–37. [Google Scholar]

- Vallely, K.; Gibson, P. Engaging students on their devices with Mentimeter. Compass J. Learn. Teach. 2018, 11. [Google Scholar] [CrossRef]

- Ausubel, D.P.; Novak, J.D.; Hanesian, H. Educational Psychology: A Cognitive View; Holt, Rinehart & Winston: New York, USA, 1968. [Google Scholar]

- Lucas, U.; Meyer, J.H. ‘Towards a mapping of the student world’: The identification of variation in students’ conceptions of, and motivations to learn, introductory accounting. Br. Account. Rev. 2005, 37, 177–204. [Google Scholar] [CrossRef]

- Crawford, K.; Gordon, S.; Nicholas, J.; Prosser, M. University mathematics students’ conceptions of mathematics. Stud. Higher Educ. 1998, 23, 87–94. [Google Scholar] [CrossRef]

- Mladenovic, R. An investigation into ways of challenging introductory accounting students’ negative perceptions of accounting. Account. Educ. 2000, 9, 135–155. [Google Scholar] [CrossRef]

- Gonçalves, E.; Capucha, L. Student-Centered and ICT-Enabled Learning Models in Veterinarian Programs: What Changed with COVID-19? Educ. Sci. 2020, 10, 343. [Google Scholar] [CrossRef]

- Marinoni, G.; van’t Land, H. The impact of COVID-19 on global higher education. Int. High. Educ. 2020, 7–9. [Google Scholar] [CrossRef]

- Leask, B.; Ziguras, C. The Impact of COVID-19 on Australian Higher Education. Int. High. Educ. 2020, 36–37. [Google Scholar] [CrossRef]

- Mishra, L.; Gupta, T.; Shree, A. Online teaching-learning in higher education during lockdown period of COVID-19 pandemic. Int. J. Educ. Res. Open 2020, 1, 100012. [Google Scholar] [CrossRef]

- Krishnamurthy, S. The future of business education: A commentary in the shadow of the Covid-19 pandemic. J. Bus. Res. 2020, 117, 1–5. [Google Scholar] [CrossRef]

- Bao, W. COVID-19 and online teaching in higher education: A case study of Peking University. Hum. Behav. Emerg. Technol. 2020, 2, 113–115. [Google Scholar] [CrossRef]

- Pokhrel, S.; Chhetri, R. A literature review on impact of COVID-19 pandemic on teaching and learning. High. Educ. Future 2021, 8, 133–141. [Google Scholar] [CrossRef]

- Sangster, A.; Stoner, G.; Flood, B. Insights into accounting education in a COVID-19 world. Account. Educ. 2020, 29, 431–562. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Nord University | University of South-Eastern Norway | The Arctic University of Norway | |

|---|---|---|---|

| Number of students | 11,462 | 18,061 | 17,124 |

| Number of employees | 1342 | 1782 | 3725 |

| State grants, in thousand NOK | 1491,841 | 1976,838 | 3487,560 |

| Study locations (campuses) | Bodø Levanger Mo i Rana Namsos Nesna Steinkjer Stjørdal Tromsø Vesterålen | Bo Drammen Kongsberg Notodden Porsgrunn Rauland Ringerike Vestfold | Tromsø Alta Kirkenes Hammerfest Harstad Narvik Bardufoss Bodø Mo i Rana Svalbard |

| The NQF Level | Learning Outcomes (Objectives) | Description |

|---|---|---|

| Knowledge On completion of this module, the student will be able to: | OB#1 | Identify the purposes for allocating costs. |

| OB#2 | Explain traditional and contemporary approaches to cost allocation, primarily variable costing, absorption/full costing and activity-based costing. | |

| Skills By the end of the module, the student will be able to: | OB#3 | Determine the costs of producing a product [providing a service or serving a customer] using variable costing, absorption/full costing and activity-based costing. |

| OB#4 | Contrast variable costing, absorption/full costing and activity-based costing. | |

| OB#5 | Analyze the results of costing approaches appropriate to different activities and decisions. | |

| General competence After having completed the module, the student will be able to: | OB#6 | Reflect on the use of different costing approaches for varied purposes, both alone and together with others. |

| The NQF Level | Learning Outcomes (Objectives) | Key Action Verbs (Keywords) | The Level of Expertise According to | |

|---|---|---|---|---|

| Bloom’s Taxonomy | The SOLO Taxonomy | |||

| Knowledge | OB#1 | Identify | Remembering | Unistructural |

| OB#2 | Explain | Understanding | Multistructural | |

| Skills | OB#3 | Determine | Applying | Multistructural |

| OB#4 | Contrast | Analyzing | Relational | |

| OB#5 | Analyze | Analyzing | Relational | |

| General competence | OB#6 | Reflect | Evaluating | Extended abstract |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Timoshenko, K.; Hansen, O.B.; Madsen, D.Ø.; Stenheim, T. Designing an Accounting Course Module on Cost Allocation: Pedagogical and Didactical Considerations from a Norwegian Perspective. Educ. Sci. 2021, 11, 232. https://doi.org/10.3390/educsci11050232

Timoshenko K, Hansen OB, Madsen DØ, Stenheim T. Designing an Accounting Course Module on Cost Allocation: Pedagogical and Didactical Considerations from a Norwegian Perspective. Education Sciences. 2021; 11(5):232. https://doi.org/10.3390/educsci11050232

Chicago/Turabian StyleTimoshenko, Konstantin, Odd Birger Hansen, Dag Øivind Madsen, and Tonny Stenheim. 2021. "Designing an Accounting Course Module on Cost Allocation: Pedagogical and Didactical Considerations from a Norwegian Perspective" Education Sciences 11, no. 5: 232. https://doi.org/10.3390/educsci11050232

APA StyleTimoshenko, K., Hansen, O. B., Madsen, D. Ø., & Stenheim, T. (2021). Designing an Accounting Course Module on Cost Allocation: Pedagogical and Didactical Considerations from a Norwegian Perspective. Education Sciences, 11(5), 232. https://doi.org/10.3390/educsci11050232