Abstract

This paper aims to elucidate some didactical and pedagogical issues related to the design of a course module on cost allocation, a pivotal topic in management accounting education at the undergraduate level around the globe. The module in question is specifically tailored to third-year undergraduates in business pursuing a major in accounting-related topics. As a theoretical backdrop, the paper draws on the didactical relationship model developed by Norwegian education researchers Hiim and Hippe. While it has proved to be of considerable value in planning education and teaching in Norwegian primary and upper secondary schools, this model, to the best of the authors’ knowledge, has not previously been applied in the context of accounting education at the university level. Without seeking to wholly generalize our thoughts and views to all higher educational institutions, we refer, in this paper, primarily to our own personal experiences of teaching management accounting gained at the three Norwegian universities, namely, Nord University, University of South-Eastern Norway, and The Arctic University of Norway. It is argued in this paper that the didactical relationship model may be of great help to accounting educators by providing an illustrative account of key conditioning factors (didactic elements) to consider while planning the learning process. Additionally, the paper strives to delve deeper into the use of technology in light of the current COVID-19 situation that we are all locked in.

1. Introduction

This paper aims to elaborate pedagogical and didactical considerations that should be taken into account while designing a course module on cost allocation in a face-to-face setting (hereafter, module). As such, it draws upon our reactions, feelings, and analyses of what we have personally experienced as teachers of management accounting in Norwegian higher education over time. Without seeking to wholly generalize our thoughts and views to all institutes of higher education, we refer in this research primarily to our own teaching experiences gained at the three Norwegian public universities, namely, Nord University, University of South-Eastern Norway, and The University of Tromsø—The Arctic University of Norway (hereafter, The Arctic University of Norway). These universities are relatively comparable in terms of size, budget appropriations, numbers of students and employees, multi-campus structure, and academic program offerings (see Table 1). Each university also has a business school, with which the authors of this paper either have been or are currently affiliated.

Table 1.

The three universities presented: key figures for 2020.

By critically analyzing what worked well and what did not in the classroom, this paper offers us the opportunity to reflect upon our choices concerning the design of the module. A module to be considered in this paper is an integral and indispensable part of the curriculum for third-year undergraduates in business pursuing a major in accounting-related topics. The other course modules include, but are not restricted to, topics such as performance measurement, compensation and reward systems, productivity and benchmarking, balanced scorecard, and beyond budgeting. While the module in question used to be largely delivered face-to-face with some limited streaming until 2020, it has been promptly tailored for the online and remote mode of delivery only in the aftermath of the COVID-19 outbreak. However, it should be noted that although we touch somehow upon our experience of using technology during the COVID-19 lockdown in Norway in this paper, we proceed from the fact that the module in question mostly adopts the face-to-face mode of delivery.

Drawing primarily upon the didactical relationship model developed by Hiim and Hippe [1], this paper demonstrates how a general didactic model can help improve the design of the module. So far, experience has shown that the model has proved effective for planning face-to-face user education on campus, as well as for developing the online tutorials. When it comes to the latter, it has, in particular, been very useful for the purpose of designing an online information literacy tutorial Søk & Skriv (“Search and Write”) developed by the University of Bergen Library, the Bergen University College Library, and the library at the Norwegian School of Economics and Business Administration [2]. However, to the best of our knowledge, no assiduous endeavor has been made to apply this didactical model in the context of accounting education until now. By sharing our own experiences with a wider audience, it is our hope that the paper will affect the readers’ ideas and possible practice of teaching management accounting in the future.

The rest of the paper is structured in the following way. Serving as the theoretical foundation, Section 2 provides a concise overview of the didactical relationship model. Section 3 gives an account of six conditioning factors that shape the design of the module in question. As it gradually proceeds, the paper refers to and critically reflects on a plethora of pedagogical and didactical concepts and views, as evidenced in the accounting education literature. The paper ends in Section 4 with a brief summary and enticing avenues for further research.

2. Theoretical Foundation—The Didactical Relationship Model

Initially designed by Bjørndal and Lieberg [3], the didactical relationship model has proved to be very useful for planning education and teaching in the Norwegian context, especially in primary and upper secondary schools. Deeply rooted in the German academic tradition, it is calibrated to serve as a viable tool geared towards helping educators (teachers, instructors, mentors, and trainers) to use reflection in planning, conducting, evaluating, and developing teaching and guidance. A distinguishing feature of the model is that it encapsulates a myriad of inextricably linked conditioning factors (categories and elements), which make up or determine a teaching (learning) situation.

In the aftermath of this development, a series of endeavors have been made to hammer out modified models for didactic analysis that are well-suited for planning education (see, e.g., those categorizations discussed in Pettersen [4]). Although lacking broad consensus on the chosen factors, the description and content of the elements and the semantics in general, they (models) all find the concept of depicting interrelated factors quite worth using. One of the most notable categorizations in this regard is that of Hiim and Hippe [1], which has gained widespread use.

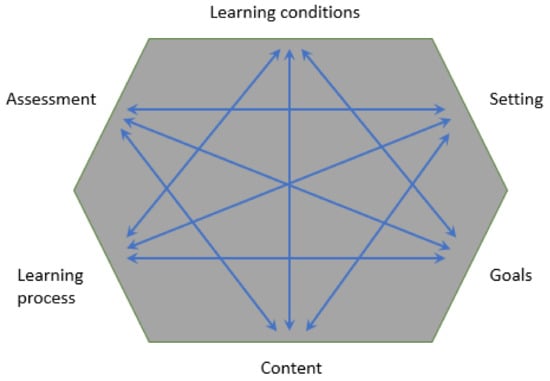

Building on Bjørndal and Lieberg [3], Hiim and Hippe [1] designed the model for didactic analysis to discern crucial relations between six categories of didactic elements: (1) learning goals and objectives, (2) content, (3) learning process, (4) assessment, (5) settings, and (6) learning conditions (see Figure 1). The aforementioned conditioning factors are said to be closely intertwined, meaning that the choice within one category does have far-reaching repercussions on the choice within other factors in varied ways and to varying degrees [4]. All factors in the model (may) serve as a starting point for planning learning and education. Notwithstanding the fact that there are calls for rectifying the model by amending the current factors and including new ones, it is beyond the scope of this paper to question the structure and assumptions of the model.

Figure 1.

The didactical relationship model by Hiim and Hippe [1] (p. 103). Reprinted

with permission from ref. [1]. Copyright 1998 Universitetsforlaget.

In what follows, the six didactic categories are critically discussed one after another regarding the course module succinctly outlined above. It should again be noted that the views expressed below are our own, which have to a large extent been shaped by our thoughts and reflections on teaching management accounting and have also been impacted by lessons learned from our own previous teaching experience.

3. The Six Conditioning Factors Described: Reflections from a Norwegian Context

3.1. Learning Goals and Objectives

It has become increasingly taken-for-granted among educators to start the design of new curricula by writing intended learning outcomes (objectives and goals). The latter are often defined as general statements of what the educator intends his/her students will be able to accomplish in the aftermath of their learning [1,2]. Generally speaking, the module in question aims at exposing the students to costing approaches that management accountants are expected to use to generate information relevant for decision-making. Drawing upon the Norwegian qualifications framework for lifelong learning (NQF) [5], the following learning outcomes for the module above are formulated in terms of knowledge, skills, and general competence (see Table 2).

Table 2.

Learning outcomes in terms of knowledge, skills and general competence.

It should be noted here that each learning outcome above targets one particular aspect of student performance, is expressed with a single key action verb, and aligns with a specific level of the two most known and commonly used learning taxonomies, (1) Bloom’s taxonomy of educational objectives [6,7], and (2) structure of the observed learning outcome (SOLO) taxonomy [8]. The former, arguably the most often used taxonomy for educational goals and objectives, represents a hierarchy of six levels that educators set for their students in order to boost communication. The latter, in turn, classifies understanding into four levels, rising in complexity and competence.

Although not immune to criticism, both taxonomies have been extensively applied in higher education generally and accounting particularly. For instance, Handy and Basile [9] have used Bloom’s taxonomy in accounting classes designed to develop higher-order critical thinking skills through cases, projects using the Wall Street Journal, flowcharting projects, developing business plans, debates, guest speakers, and company tours, to name just some. An examination of intermediate accounting textbooks by Davidson and Baldwin [10] has produced intriguing results—about 48% of end-of-chapter exercises were elaborated at the knowledge, comprehension, and application levels, whereas 43% at the analysis level and 9% at the synthesis and evaluation levels. As to the SOLO taxonomy, it has, e.g., served as a sensitizing lens to investigate students’ understanding of two fundamental concepts within introductory accounting, namely, the relationship between cash and profit and the concept of depreciation [11].

Table 3 accentuates the module’s desired learning goals viewed through the lens of both models. Using Bloom’s taxonomy of objectives, the module’s curriculum emphasizes the first five (out of six) levels of learning, commencing with the lower-order Bloom’s knowledge (i.e., remembering and comprehending level objectives) and ending with higher-order skills and competence (i.e., applying, analyzing and even evaluating level goals). Pointing to the SOLO model, the module design encapsulates all the four hierarchical levels of understanding, ranging from the unistructural to the extended abstract. This is in conformity with a general belief in higher education that students should develop knowledge that is organized structurally at the relational or extended abstract level [11,12,13].

Table 3.

Student learning outcomes in the light of the Bloom taxonomy and the SOLO model.

3.2. Module Content

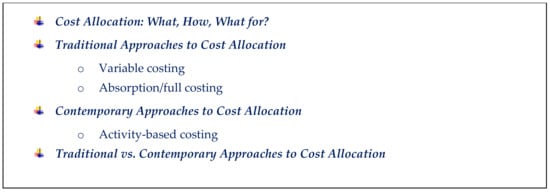

While designing the module, we are driven by a keen desire to assist our students in mastering its content. In doing so, it is pivotal to decide as to what the learning is comprised of, and how one selects to approach it. The main themes that the students are anticipated to go through in this module are traditional and contemporary approaches to cost allocation. Rather than focusing on all approaches to cost allocation (which are many), our choice deliberately fell on a few selected ones, namely variable costing, absorption costing, and activity-based costing. Based on our previous experience, a reasonable scope for the module in question is preferred, a scope that incorporates essential content, but which also provides ample opportunities for students to practice applying and analyzing the skills and knowledge they gain.

In so doing, we strive to focus more on developing analytical and conceptual thinking rather than merely training students to pass summative exams, thereby favoring deep (transformative, global) approaches to learning to take place [14]. However, this does not necessarily mean that surface (shallow, superficial) strategies, such as memorization, are completely non-existent. As a growing body of research on students’ approaches to learning indicates [15,16,17,18,19], rote learning and paraphrasing are often deemed necessary before students eventually become capable of applying knowledge and successfully reflecting on the appropriateness of utilizing management accounting techniques. As pinpointed by Entwistle and Smith [15] (p. 326), memorization can be used “… to master unfamiliar terminology by initial rote learning, as a first step towards developing understanding…”.

Based on the mentioned above, a reasonable set of essential topics to be covered under the rubric of cost allocation is as follows, in order of their presentation (Figure 2):

Figure 2.

Essential topics to be covered under the rubric of cost allocation.

Noteworthily, the module is designed in such a way as to move sequentially towards greater complexity. More precisely, it commences with rather separate (fragmented) pieces (i.e., various costing approaches) and works towards their synthesis and integration. This design fits impeccably well with Fink [20] (p. 128): “The goal is to sequence the topics so that they build on one another in a way that allows students to integrate each new idea, topic, or theme with the preceding ones as the course proceeds”. Additionally, the application component of the module in question arises as a result of theoretical underpinnings.

3.3. The Learning Process

The learning process is intended to encompass both the educator’s and learner’s approach to the content [1]. The former’s comprehension of learning creates a solid foundation for selecting teaching and learning strategies. Since the intended learning outcomes above are for students to be able to explain traditional and contemporary approaches to cost allocation, contrast them, analyze them, and apply them to particular situations and for varied purposes, then an effective teaching strategy is likely to amalgamate the following primary means:

- The traditional lecture-based format with PowerPoint slides, black- and whiteboards, and short video presentations aimed at providing an outline of work to be covered (i.e., to introduce and describe the diverse approaches to cost allocation and their inherent features and drawbacks). It should be noted here that all face-to-face lecture materials, such as PowerPoint slides, are normally uploaded online on a weekly basis. Guest lectures with business representatives are also delivered whenever possible. Drawing upon real-life cases and experiences, guest lectures are thought to make classes more approachable and appealing to students.

- The group discussion format (team learning) with the case-study model geared towards giving opportunity for reflection on and the application of material covered in lectures, as well as discussing issues related to course (module) matter (i.e., to juxtapose the costing approaches, critically discuss them, and reflect on their applications).

The appropriateness of using one or another form of learning has been a matter of discussion in the academic community. On the one hand, lecturing remains the dominant pedagogy in higher education generally and accounting particularly, and its impacts on student learning have been addressed in a plethora of studies see, e.g., [21,22,23]. On the other hand, the effects of team working on student learning outcomes have so far shown mixed results, as evidenced in the accounting education literature, see, e.g., [21,22,24].

Thus far, the learning process in the module is designed in a way that combines the inherent features of both the lecture-based and team learning interventions. Of paramount importance here is the role of team working in the learning process. Without having the intention to diminish the importance of lecture-based learning, tutorials, and problem-solving are considered indispensable components of learning in this module in that they foster peer interaction. This is because the communication and teamwork skills developed in these sessions by actively participating in discussions are reckoned to be most important in Norwegian higher education and are sought after by employers. This is especially the case for the accounting profession, in which the ability of employees to work in teams has been widely recognized as ‘a must’ for successful carrier development [24,25].

Another reason stems from our long-lasting pedagogical experience. Having had the opportunity to teach different audiences (both traditional and non-traditional, undergraduate and graduate) on a variety of courses for 15+ years, we found that students who were reluctant (or shy) to ask questions during traditional lectures felt free, during these group sessions, to discuss questions with their peers.

This provided an excellent opportunity for collaborative learning [26]; students who comprehended the material well (the so-called more knowledgeable others, to use the words of Lev Vygotsky) could aid weaker classmates. This experience convinced us that the more students interact with faculty staff and fellow students alike, the more they absorb and grasp. Thus far, interaction and dialogue with the more knowledgeable others is regarded as essential to accomplish (foster) learning, thereby helping students to develop higher-order thinking skills (i.e., deep learning). In such a context, the role of the educator is that of a discussion (dialogue) partner and a facilitator (rather than a “sage on the stage”), whose ‘voice’ is only one in the plural discourse that the learner is exposed to [2]. This fits well with “Vygotsky scaffolding” and the related concept of the zone of proximal development [11], that is, teaching methods that help students learn more and more quickly by working with a teacher or a more advanced classmate than they would with traditional instruction.

Taking all of the above-mentioned into account, learning in this module is not circumscribed by individual processes only; it occurs in a context and through close interaction and dialogue with others, thereby increasing the feeling of belonging to a community. Our teaching evaluations have demonstrated that students greatly appreciate our constant willingness and readiness for dialogue. All this suggests that the module in question adopts the elements of both behaviorist and socio-constructivist perspectives on learning [27].

3.4. Assessment

While designing the module, there is a dire need to assess the learner’s skills and performance. That said, there is a broad consensus within the academic community concerning the need to evaluate as to whether and eventually to what extent the learning objectives have been accomplished. Hence, for learning to blossom and thrive, its desired objectives should be fine-tuned with evaluation methods. The converse is also true in that the assessment criteria should address the outcomes so that the educator can test to observe whether and how well the students have mastered what the outcomes state they should be learning.

The course assessment is portfolio-based, encapsulating the following two major elements:

- A high-stakes individual written school exam that takes place at the end of the learning process and encompasses the integral parts of the course (including those taught under the rubric of cost allocation). The contribution of this end-of-semester summative assessment to the final grade is worth 100%. During the lockdown, the assessment changed into a 100% individual written home exam. Although falling short for the purpose of assessing knowledge at the higher levels of synthesis and evaluation, it deems appropriate for gauging knowledge and comprehension OB#1–2. Albeit to a lesser extent, it also aids in assessing applying skills OB#3. Since the module in question centers largely around teaching rather structured material, incorporating inter alia facts, management accounting concepts and tools, the degree of learning is best captured using behaviorist assessment methods.

- A group assignment that occurs in the middle of the learning process and deals exclusively with cost allocation issues. The pass/fail scale is applied as an independent scale with only two possible results. This type of assessment is primarily geared towards applying and analyzing OB#3–6 traditional and contemporary methods of cost allocation to particular situations and for diverse purposes. This kind of approach to assessment entails setting students a series of ‘problems’ to be tackled in groups. It is an informal atmosphere that permits students to curb the fear of failure and feel rather comfortable and relaxed. As pointed out earlier, such interaction and dialogue with peers offers a unique opportunity for ‘scaffolding’ and is viewed pivotal to further learning, thereby aiding students to develop higher-order thinking skills (i.e., deep learning). Thus far, the elements of socio-constructivist perspective on learning, including Bakhtin’s and Vygotsky’s thoughts on dialogues [28], are key to this type of assessment as students are encouraged to form study groups to solve the assignment and, more importantly, critically reflect on the results [27].

Besides the two forms above, mock exams have proven their worth in accomplishing desired learning outcomes. Although non-mandatory and with zero impact on the grade, they are often highly valued or even regarded as indispensable by students. Noteworthily, the choice of questions to be included in such exams requires careful calibration in order to develop key knowledge, while not replicating too closely the summative exam. Summing up the discussion, we are of the firm opinion that students perceive any type of formative assessment to be of great value as long as they view it as contributing towards summative assessment tasks, “like practice without anxiety, analogous to hitting golf balls round a field or practicing tennis shorts against a wall. It (formative assessment) occurs in a no-failure/no lose context” [29] (p. 149). This corresponds well with Black and Wiliam [30] who came to a conclusion in their study of classroom-based formative assessment that the achievement gains associated with this type of assessment were among the largest ever documented for the purpose of promoting the engagement and involvement of students.

3.5. Settings

Learning is likely to be conditioned by external factors that may affect it in many ways. Some factors may foster meaningful teaching and learning, while others, on the contrary, may have very corrosive and debilitating effects. Furthermore, some of these factors are within our easy grasp, while others are predominantly beyond our control. Yet, the importance of external factors may vary over time. It is pertinent to note here that a list of factors below is not all-inclusive but, rather, illustrative.

The geographical scope of the class participants. A distinctive feature of Norwegian higher education today is that each university has several geographically distant campuses, owing to numerous mergers that have occurred during the last decade. As shown in Table 1, students at University of South-Eastern Norway may get education at one of its eight campuses, whereas their peers at Nord University and The Arctic University of Norway may select between nine and 10 study locations, respectively. Since teaching takes place on various geographically distant campuses and not least due to the emergence and unprecedented spread of the COVID-19 as a global pandemic, distance learning techniques have been applied in the learning process at an accelerated rate. Included is the use of document cameras, also known as visual presenters, visualizers, or docucams, allowing us to write on a sheet of paper while students at diverse campuses watch. However, visualizers are not without drawbacks, e.g., their usage does not permit distant education students to raise questions online while we teach.

An educator’s work burden. The number of students with respect to the assigned faculty staff is also considered a decisive factor [2]. Needless to say, the greater that ratio gets, the less accessible and approachable the educator becomes.

Time. In stark contrast to surface learning, deep understanding takes a much longer time to emerge. That accentuated, determining core content with regard to the allocated time is of paramount importance for the module design. As previously underlined, a reasonable coverage for the module in question is emphasized, thereby enabling learners to practice applying and analyzing the skills and knowledge they get. Consequently, rather than going through all approaches to cost allocation (which are many) in one module, it seemed preferable to focus on a few selected ones–variable costing, absorption costing, and activity-based costing.

The use of information and communication technology. Because of the diversity of their uses, digitalized tools have grown to become lifelong friends of education and nowadays play a crucial role in teaching and learning. Amid the coronavirus outbreak and subsequent lockdowns that we all are still witnessing, universities and other institutes of higher learning, both within Norway and internationally, have been subjected to an unprecedented pressure to shift away from traditional face-to-face learning on campus to nearly exclusively online and remote modes of teaching and assessment. Rather than being either meticulously pre-planned or optional, this hasty transition was considered an urgent need in the face of this global health emergency, forcing many educators to “jump in at the deep end”. This has led to the use of digital technologies on an even grander scale [15].

Besides all the bad news brought about by the COVID-19 pandemic, this crisis might become a tremendous opportunity for dramatic reshaping and implementing novel digital strategies in higher education. As stated by Peimani and Kamalipour [31] (p. 10), the spread of COVID-19 might be “an opportunity for universities to learn from the rapid changes and adaptations during this unprecedented time, and as such rethink the extent to which many courses rely on face-to-face teaching on campus”. Likewise, in their assessment of the quick changes from face-to-face to online teaching during the COVID-19 lockdown, García-Alberti, et al. [32] (p. 4) have claimed that “there is no doubt that these changes have led to a step forward in both the digital transformation of universities and the teaching of the future”.

Speaking of online modes of teaching, the current pool of digitalized tools in the educational domain is wide [33]. Choices are many (e.g., PowerPoint, Word, YouTube, Canvas, Zoom, Padlet, Skype, Microsoft Teams, etc.), thereby enabling teachers to incorporate appropriate digital solutions into lectures and tutorials, given a number of subject-related factors and learning conditions. It is pertinent to note here that the range of applications below does not provide all the opportunities for the use of digitalized tools in the module in question but, rather, those that are the most illustrative.

To begin with, it would be difficult to overstate the use of Microsoft’s Excel or any other similar application in the teaching of accounting in general [34,35] and cost allocation in particular as it (Microsoft’s Excel) does not only enable students to achieve lower-level comprehension knowledge but can also assist in developing higher-order applying, analyzing and evaluating skills. Among other things, using Excel may considerably enhance comprehension of content with a graphic presentation of the management accounting information; it provides a visual representation of cost data that makes it easier to contrast, analyze, interpret, and reflect on; it helps generate charts and graphs in seconds that makes it much easier to quickly demonstrate relationships between numbers.

Next, the use of Kahoot, a game-based learning platform that has been shown to improve learning [36], is highly recommended as it provides an exciting and accessible way to assess students’ prior knowledge early in the semester. For example, the results obtained through administering multiple-choice quizzes via Kahoot may give a glimpse of how well students currently comprehend and assist the educator in making the curriculum more engaging. Last but not least, using Mentimeter or similar student response systems may make learning more interactive, captivating, and entertaining by letting the students actively participate in lectures and tutorial sessions in real-time [37,38]. In our experience, this software platform may be especially suited for those students who otherwise are too shy to participate.

3.6. Learning Conditions

There is a broad consensus in the pedagogical community that learning of new knowledge heavily relies upon what is already known, thus highlighting the significance of previous knowledge (see, e.g., [18]). Using the words of Ausubel, et al. [39] (p. vi), “If we had to reduce all of educational psychology to just one principle, we would say this: The most important single factor influencing learning is what the learner already knows. Ascertain this and teach him accordingly”. Given that the overwhelming majority of students pursuing the module are third-year undergraduate students in business, it would seem reasonable to assume that they constitute a rather homogenous group, and they have certain kinds of background knowledge, skills, and experience (that is, prerequisites) needed to accomplish learning. Regarding the module in question, it is, therefore, expected that students are, although in varying ways and degrees, equipped with a host of the basic management accounting concepts, including cost objects, expenses, expenditures, direct and indirect (overhead) costs, fixed and variables costs.

Furthermore, since the course is a sequence of other business- and accounting-related courses, it is a stunning idea to unveil what themes have been covered in the courses preceding the one in question. This can be done either by talking to colleagues who have taught the preceding courses or asking for a copy of their course materials. First-hand information can also be obtained by interviewing students at the beginning of the semester. Providing an ever-increasing focus on strengthening students’ digital literacy, one effective way to gauge students’ prior knowledge early in the semester is to administer multiple-choice quizzes via Kahoot. As mentioned above, the results so obtained can seemingly provide a vivid indication of how well students currently grasp and help the educator make material in the course module more engaging.

Noteworthily, even though third-year undergraduates specializing in accounting are assumed to constitute a rather homogenous group, significant variations in conceptions about the course in general and the module in particular are likely to exist among students [18]. As quoted by Lucas and Meyer [40] (p. 178), Crawford, et al. [41] (pp. 81–82) effectively summarized these variations in the context of math students as follows, “… within the same class, there substantial variation in the way students perceive the quality of teaching, clarity and meaning of goals, the amount of work required, the nature of assessments, etc. … These perceptions are systematically related to the approaches to learning adopted by the students”. This seems to be the case of accounting students as well. As, e.g., evidenced by Lucas and Meyer [18] and Mladenovic [42], the former enter their studies with quite varying perceptions of the subject (i.e., accounting). Alongside positive preconceptions of accounting, this wide array of views also encapsulates those such as dull, boring, and lacking in interest [42], thus indicating the need for carefully calibrated teaching interventions and responses.

4. Summary and Looking Ahead

This paper has sought to discuss the pedagogical and didactic framework within which the design of a face-to-face module on cost allocation is developed. The module in question has been specifically tailored to third-year bachelor students in business pursuing a major in accounting-related topics. The evidence for this paper has been primarily drawn from our own personal experiences of teaching management accounting at the three Norwegian universities—Nord University, University of South-Eastern Norway, and The Arctic University of Norway. As the paper has demonstrated, the didactical relationship model by Norwegian education researchers Hiim and Hippe [1] has proved to be of significant value for accounting educators in fostering the learning process as it lays down a solid foundation for reflecting on key conditioning factors and their close interplay while designing the module.

The learning goals and objectives of the module in question, which are derived from the Bloom’s and SOLO taxonomies, are reflected in its content. Rather than focusing on all approaches to cost allocation (which are many), our choice deliberately fell on a few selected ones, thereby providing ample opportunities for students to practice applying and analyzing the skills and knowledge they gain. In assiduous endeavors to aid students in developing higher-order thinking skills (i.e., deep learning), the learning process is to a large extent geared towards fostering collaborative (cooperative) learning, that is, interaction and dialogue with the more knowledgeable others (faculty staff and fellow students). The module assessment contains the considerable elements of the socio-constructivist perspective on learning as students are encouraged to form study groups to solve the assignment and, more importantly, critically reflect on the results.

Due to the very nature of the module, the issue of using technology in the course design has been highlighted in this paper. This issue is likely to have been even more aggravated in light of the COVID-19 outbreak that confronts us today. Not surprisingly, therefore, there is an evolving body of knowledge geared toward gauging the impacts of the COVID-19 on higher education worldwide [31,32,43,44,45,46,47,48,49]. As shown in this paper, information and communication technology can offer a host of viable solutions to numerous problems and challenges. For instance, preliminary experiences indicate that technology has indeed been useful in coming up with lasting solutions to ensure cogent academic standards and high-quality student experience in the aftermath of the COVID-19 pandemic. As Sangster, et al. [50] have noted, accounting educators have been compelled to make considerable adaptations to the learning process in the face of altering realities triggered by the prevalence of the COVID-19 in the past year.

The question arises, however, as to whether online provision and the enforced digitalization of pedagogical approaches engendered by the advent of the recent global health emergency will be retained and integrated into traditional classroom in a future COVID-free world. That emphasized, the extent to which technologically infused distance learning tools will supersede or complement traditional well-calibrated, face-to-face modes of delivery remains unclear. Perhaps, the path to a better future is through amalgamating traditional and online forms of teaching and learning, rather than putting either of the two on a pedestal, thereby paving the way for developing blended or hybrid forms and designs of learning. Although not without skepticism, this approach is deemed tempting in the long run. For instance, García-Alberti, Suárez, Chiyón and Mosquera Feijoo [32] (p. 15) have argued that a blend of face-to-face and online learning can lead to “a better learning experience, since online resources provide tools and promote dynamics that are not possible in the classroom, but this combination can also lead to a less motivated group of students”.

In any case, it is our opinion that technology can act to (drastically) enhance traditional teaching and learning on campus by offering captivating insights and opportunities for the increased student engagement and motivation. Thus far, case studies may explore the challenges and opportunities in relation to all the six conditioning factors above (particularly, learning process and assessment) that the headlong transition from face-to-face mode of delivery to online teaching has encroached upon individual higher educational institutions.

Author Contributions

Conceptualization, K.T.; methodology, K.T.; software, K.T.; O.B.H.; D.Ø.M.; T.S.; validation, K.T.; O.B.H.; D.Ø.M.; T.S.; formal analysis, K.T.; O.B.H.; D.Ø.M.; T.S.; investigation, K.T.; resources, K.T.; O.B.H.; D.Ø.M.; data curation, K.T.; O.B.H.; D.Ø.M.; T.S.; writing—original draft preparation, K.T.; O.B.H.; D.Ø.M.; T.S.; writing—review and editing, K.T.; O.B.H.; D.Ø.M.; T.S; visualization, D.Ø.M.; supervision, K.T. and D.Ø.M.; project administration, K.T. and D.Ø.M.; funding acquisition, K.T.; D.Ø.M.; T.S. All authors have read and agreed to the published version of the manuscript.

Funding

The APC was funded by the University of South-Eastern Norway.

Acknowledgments

The authors would like to thank two anonymous referees for their constructive and inspiring comments and suggestions on earlier versions of this paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Hiim, H.; Hippe, E. Læring Gjennom Opplevelse, Forståelse og Handling: En Studiebok i Didaktikk; Universitetsforlaget: Oslo, Norway, 1998. [Google Scholar]

- Skagen, T.; Torras, M.C.; Kavli, S.M.; Mikki, S.; Hafstad, S.; Hunskår, I. Pedagogical considerations in developing an online tutorial in information literacy. Commun. Inf. Lit. 2009, 2, 4. [Google Scholar] [CrossRef]

- Bjørndal, B.; Lieberg, S. Nye Veier i Didaktikken?: En Innføring i Didaktiske Emner og Begreper; Aschehoug: Oslo, Norway, 1978. [Google Scholar]

- Pettersen, R.C. Didaktiske modeller og verktøy. In Kvalitetslæring i Høgere Utdanning. Innføring i Problem-og Praksisbasert Didaktikk; Pettersen, R.C., Ed.; Universitetsforlaget: Oslo, Norway, 2005; pp. 3–50. [Google Scholar]

- Norwegian Ministry of Education. Nasjonalt Kvalifikasjonsrammeverk for Livslang Læring [NKR]; Norwegian Ministry of Education: Oslo, Norway, 2011. [Google Scholar]

- Bloom, B.; Englehart, M.; Furst, E.; Hill, W.; Krathwohl, D. Taxonomy of Educational Objectives, The Classication of Educational Goals, Handbook 1: Cognitive Domain; David McKay: New York, NY, USA, 1956. [Google Scholar]

- Bloom, B.S. Reflections on the Development and Use of the Taxonomy. In Bloom’s Taxonomy: A Forty-Year Retrospective; Anderson, L.W., Sosniak, L.A., Eds.; The National Society for the Study of Education: Chicago, IL, USA, 1994; pp. 1–8. [Google Scholar]

- Biggs, J.B.; Collis, K.F. Evaluating the Quality of Learning: The SOLO Taxonomy (Structure of the Observed Learning Outcome); Academic Press: Cambridge, MA, USA, 2014. [Google Scholar]

- Handy, S.; Basile, A. Improving accounting education using Bloom’s taxonomy of educational objectives. J. Appl. Res. Bus. Instr. 2005, 3, 1–6. [Google Scholar]

- Davidson, R.A.; Baldwin, B.A. Cognitive skills objectives in intermediate accounting textbooks: Evidence from end-of-chapter material. J. Account. Educ. 2005, 23, 79–95. [Google Scholar] [CrossRef]

- Lucas, U.; Mladenovic, R. The identification of variation in students’ understandings of disciplinary concepts: The application of the SOLO taxonomy within introductory accounting. High. Educ. 2009, 58, 257–283. [Google Scholar] [CrossRef]

- BIGGS, J. Multimodal learning and the quality of intelligent behavior. In Intelligence: Reconceptualization and Measurement; Rowe, H., Ed.; Laurence Erlbaum: Hillsdale, NJ, USA, 1991; pp. 57–76. [Google Scholar]

- Boulton-Lewis, G. Applying the SOLO taxonomy to learning in higher education. In Teaching and Learning in Higher Education; Dart, B., Boulton-Lewis, G., Eds.; Australian Council for Educational Research: Melbourne, Australia, 1998; pp. 201–221. [Google Scholar]

- Hattie, J.A.; Donoghue, G.M. Learning strategies: A synthesis and conceptual model. NPJ Sci. Learn. 2016, 1, 1–13. [Google Scholar] [CrossRef] [PubMed]

- Entwistle, N.; Smith, C. Personal understanding and target understanding: Mapping influences on the outcomes of learning. Br. J. Educ. Psychol. 2002, 72, 321–342. [Google Scholar] [CrossRef] [PubMed]

- Duff, A.; McKinstry, S. Students’ approaches to learning. Issues Account. Educ. 2007, 22, 183–214. [Google Scholar] [CrossRef]

- Birkett, B.; Mladenovic, R. The approaches to learning paradigm: Theoretical and empirical issues for accounting education research. In Proceedings of the AAANZ Conference, Perth, Australia, 7–9 July 2002. [Google Scholar]

- Lucas, U.; Meyer, J.H. Supporting student awareness: Understanding student preconceptions of their subject matter within introductory courses. Innov. Educ. Teach. Int. 2004, 41, 459–471. [Google Scholar] [CrossRef]

- Hall, M.; Ramsay, A.; Raven, J. Changing the learning environment to promote deep learning approaches in first-year accounting students. Account. Educ. 2004, 13, 489–505. [Google Scholar] [CrossRef]

- Fink, L.D. Creating Significant Learning Experiences: An Integrated Approach to Designing College Courses; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Opdecam, E.; Everaert, P. Seven disagreements about cooperative learning. Account. Educ. 2018, 27, 223–233. [Google Scholar] [CrossRef]

- Hwang, N.C.R.; Lui, G.; Tong, M.Y.J.W. An empirical test of cooperative learning in a passive learning environment. Issues Account. Educ. 2005, 20, 151–165. [Google Scholar] [CrossRef]

- Aldamen, H.; Al-Esmail, R.; Hollindale, J. Does lecture capturing impact student performance and attendance in an introductory accounting course? Account. Educ. 2015, 24, 291–317. [Google Scholar] [CrossRef]

- Opdecam, E.; Everaert, P. Choice-based learning: Lecture-based or team learning? Account. Educ. 2019, 28, 239–273. [Google Scholar] [CrossRef]

- Montano, J.L.A.; Donoso, J.A.; Hassall, T.; Joyce, J. Vocational skills in the accounting professional profile: The Chartered Institute of Management Accountants (CIMA) employers’ opinion. Account. Educ. 2001, 10, 299–313. [Google Scholar] [CrossRef]

- Vygotsky, L.S. Interaction between Learning and Development; W.H. Freeman and Company: New York, NY, USA, 1997. [Google Scholar]

- Dolin, J. Undervisning for livet. In Universitetspædagogik; Rienecker, L., Jørgensen, P.S., Dolin, J., Ingerslev, G.H., Eds.; Samfundslitteratur: Fredriksberg, Sweden, 2013. [Google Scholar]

- Kubli, F. Science teaching as a dialogue–Bakhtin, Vygotsky and some applications in the classroom. Sci. Educ. 2005, 14, 501–534. [Google Scholar] [CrossRef]

- Scaife, J.; Wellington, J. Varying perspectives and practices in formative and diagnostic assessment: A case study. J. Educ. Teach. 2010, 36, 137–151. [Google Scholar] [CrossRef]

- Black, P.; Wiliam, D. Assessment and classroom learning. Assess. Educ. Princ. Policy Pract. 1998, 5, 7–74. [Google Scholar] [CrossRef]

- Peimani, N.; Kamalipour, H. Online Education and the COVID-19 Outbreak: A Case Study of Online Teaching during Lockdown. Educ. Sci. 2021, 11, 72. [Google Scholar] [CrossRef]

- García-Alberti, M.; Suárez, F.; Chiyón, I.; Mosquera Feijoo, J.C. Challenges and Experiences of Online Evaluation in Courses of Civil Engineering during the Lockdown Learning Due to the COVID-19 Pandemic. Educ. Sci. 2021, 11, 59. [Google Scholar] [CrossRef]

- Amhag, L.; Hellström, L.; Stigmar, M. Teacher educators’ use of digital tools and needs for digital competence in higher education. J. Digit. Learn. Teach. Educ. 2019, 35, 203–220. [Google Scholar] [CrossRef]

- Ramachandran Rackliffe, U.; Ragland, L. Excel in the accounting curriculum: Perceptions from accounting professors. Account. Educ. 2016, 25, 139–166. [Google Scholar] [CrossRef]

- Willis, V.F. A model for teaching technology: Using Excel in an accounting information systems course. J. Account. Educ. 2016, 36, 87–99. [Google Scholar] [CrossRef]

- Wang, A.I.; Tahir, R. The effect of using Kahoot! for learning–A literature review. Comput. Educ. 2020, 149, 103818. [Google Scholar] [CrossRef]

- Rudolph, J. A brief review of Mentimeter—A student response system. J. Appl. Learn. Teach. 2018, 1, 35–37. [Google Scholar]

- Vallely, K.; Gibson, P. Engaging students on their devices with Mentimeter. Compass J. Learn. Teach. 2018, 11. [Google Scholar] [CrossRef]

- Ausubel, D.P.; Novak, J.D.; Hanesian, H. Educational Psychology: A Cognitive View; Holt, Rinehart & Winston: New York, USA, 1968. [Google Scholar]

- Lucas, U.; Meyer, J.H. ‘Towards a mapping of the student world’: The identification of variation in students’ conceptions of, and motivations to learn, introductory accounting. Br. Account. Rev. 2005, 37, 177–204. [Google Scholar] [CrossRef]

- Crawford, K.; Gordon, S.; Nicholas, J.; Prosser, M. University mathematics students’ conceptions of mathematics. Stud. Higher Educ. 1998, 23, 87–94. [Google Scholar] [CrossRef]

- Mladenovic, R. An investigation into ways of challenging introductory accounting students’ negative perceptions of accounting. Account. Educ. 2000, 9, 135–155. [Google Scholar] [CrossRef]

- Gonçalves, E.; Capucha, L. Student-Centered and ICT-Enabled Learning Models in Veterinarian Programs: What Changed with COVID-19? Educ. Sci. 2020, 10, 343. [Google Scholar] [CrossRef]

- Marinoni, G.; van’t Land, H. The impact of COVID-19 on global higher education. Int. High. Educ. 2020, 7–9. [Google Scholar] [CrossRef]

- Leask, B.; Ziguras, C. The Impact of COVID-19 on Australian Higher Education. Int. High. Educ. 2020, 36–37. [Google Scholar] [CrossRef]

- Mishra, L.; Gupta, T.; Shree, A. Online teaching-learning in higher education during lockdown period of COVID-19 pandemic. Int. J. Educ. Res. Open 2020, 1, 100012. [Google Scholar] [CrossRef]

- Krishnamurthy, S. The future of business education: A commentary in the shadow of the Covid-19 pandemic. J. Bus. Res. 2020, 117, 1–5. [Google Scholar] [CrossRef]

- Bao, W. COVID-19 and online teaching in higher education: A case study of Peking University. Hum. Behav. Emerg. Technol. 2020, 2, 113–115. [Google Scholar] [CrossRef]

- Pokhrel, S.; Chhetri, R. A literature review on impact of COVID-19 pandemic on teaching and learning. High. Educ. Future 2021, 8, 133–141. [Google Scholar] [CrossRef]

- Sangster, A.; Stoner, G.; Flood, B. Insights into accounting education in a COVID-19 world. Account. Educ. 2020, 29, 431–562. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).