Causality between Terrorism and FDI in Tourism: Evidence from Panel Data

Abstract

:1. Introduction

2. Overview

3. Limitations, Data and Methodological Framework

3.1. Research Limitations

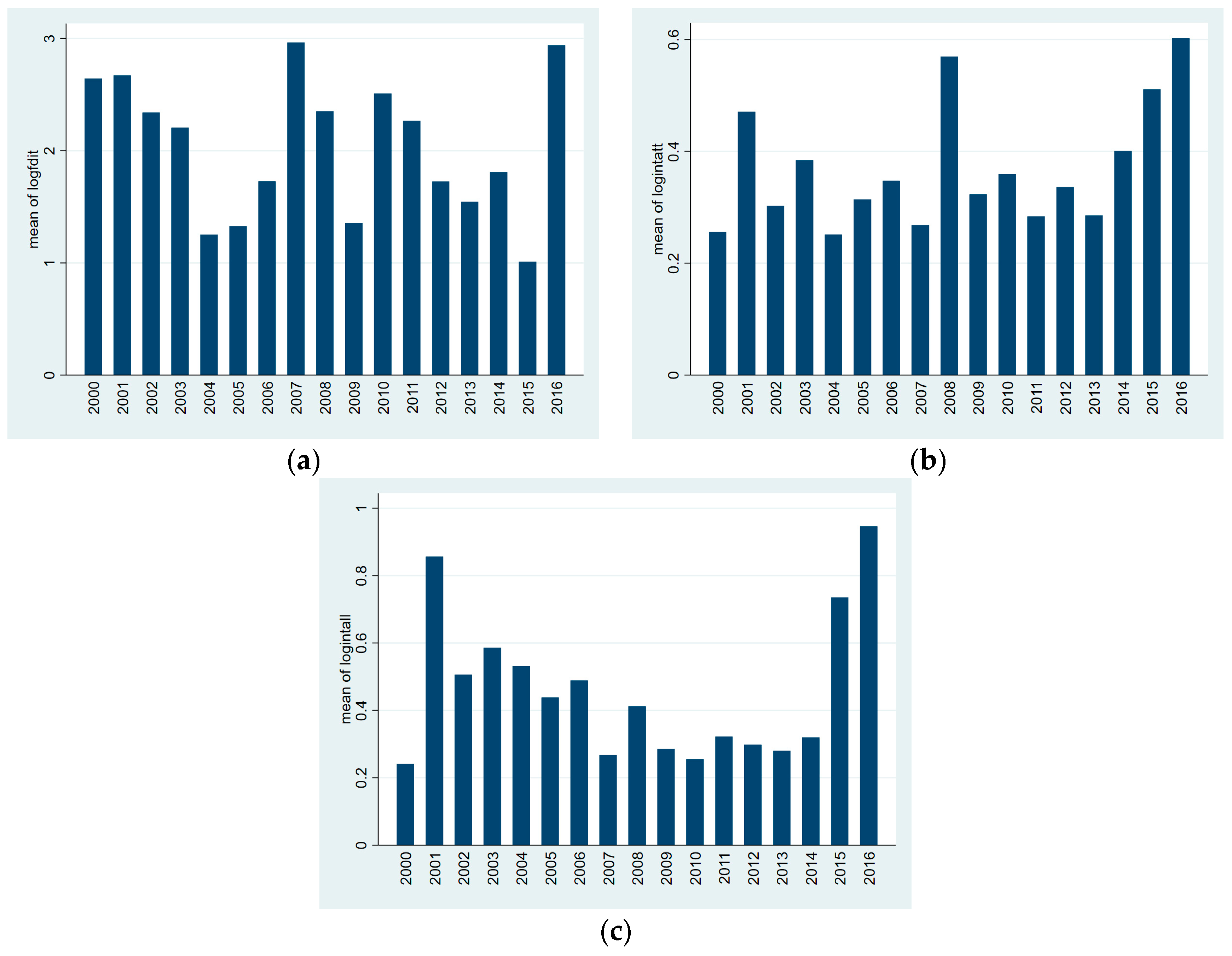

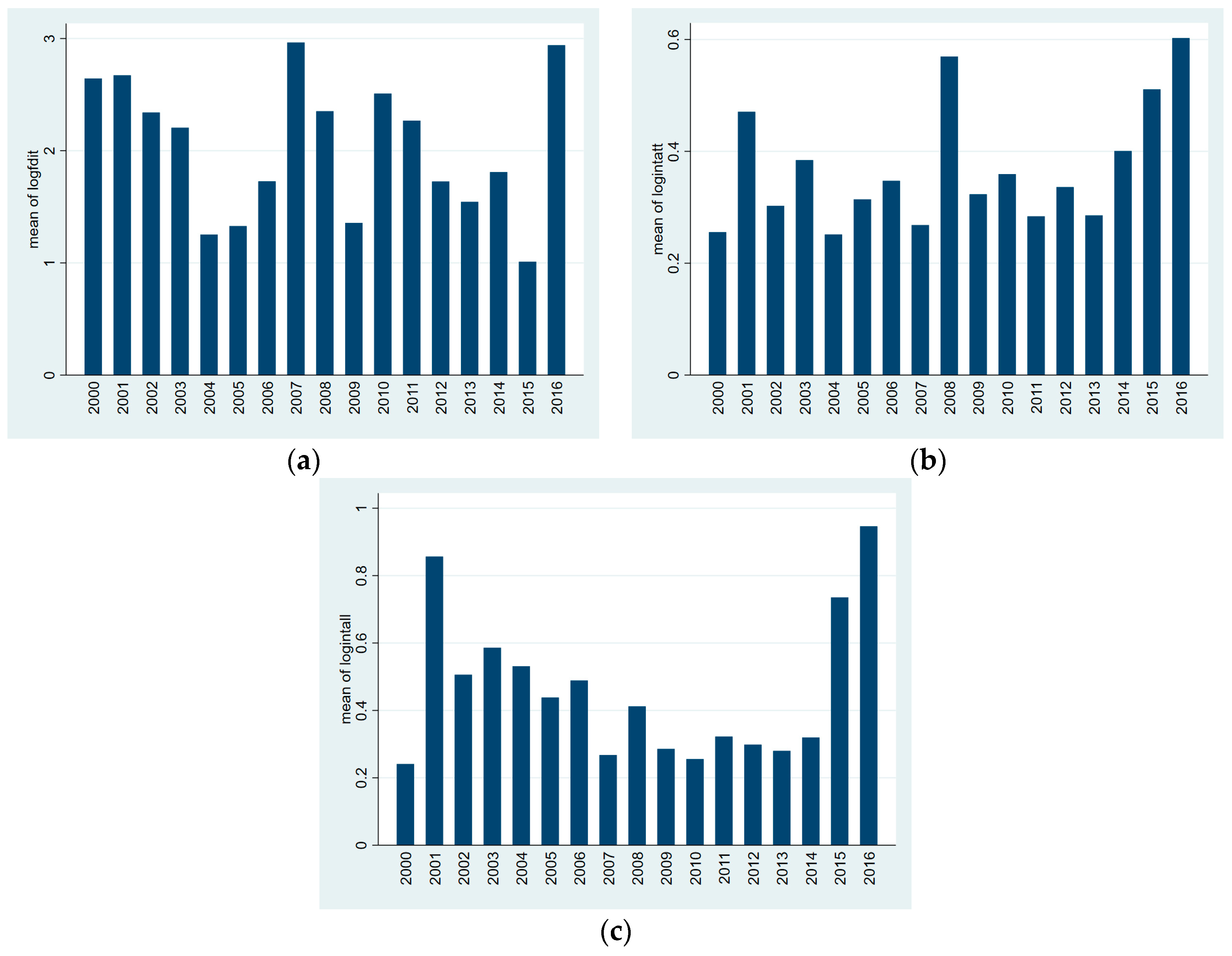

3.2. Data

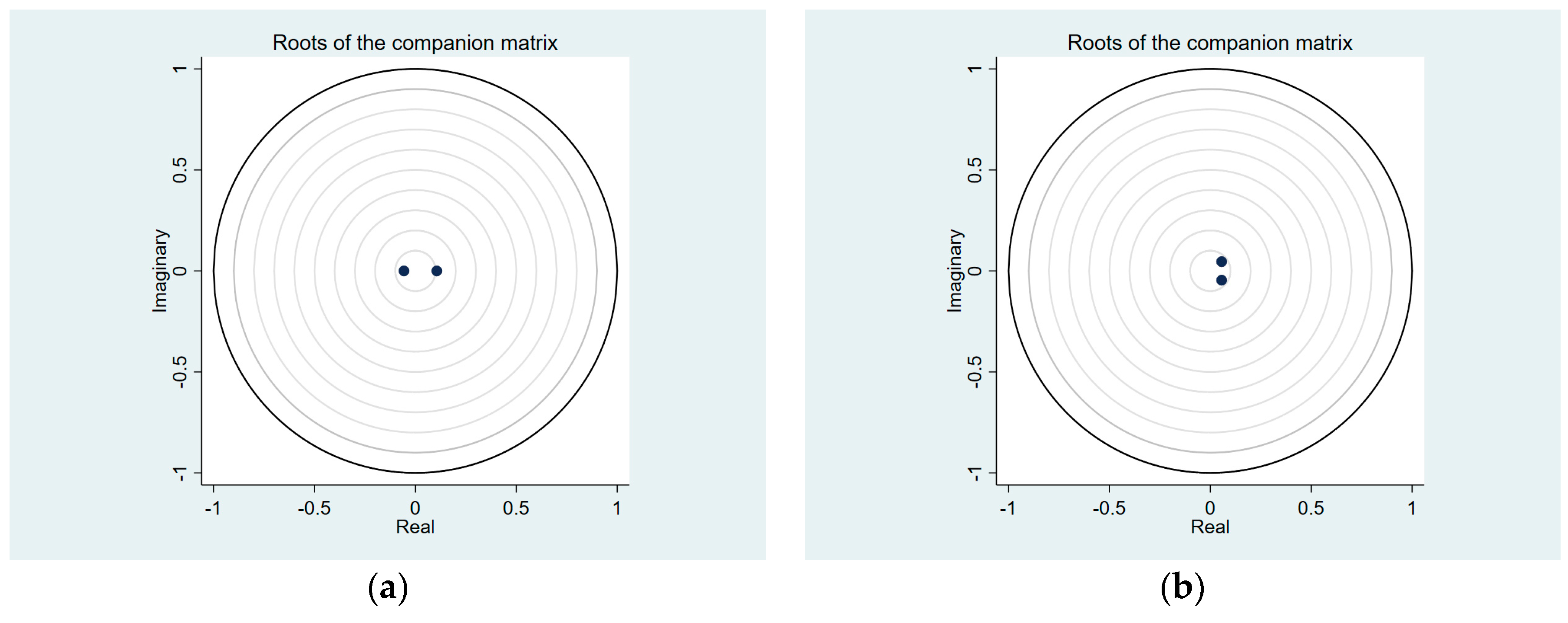

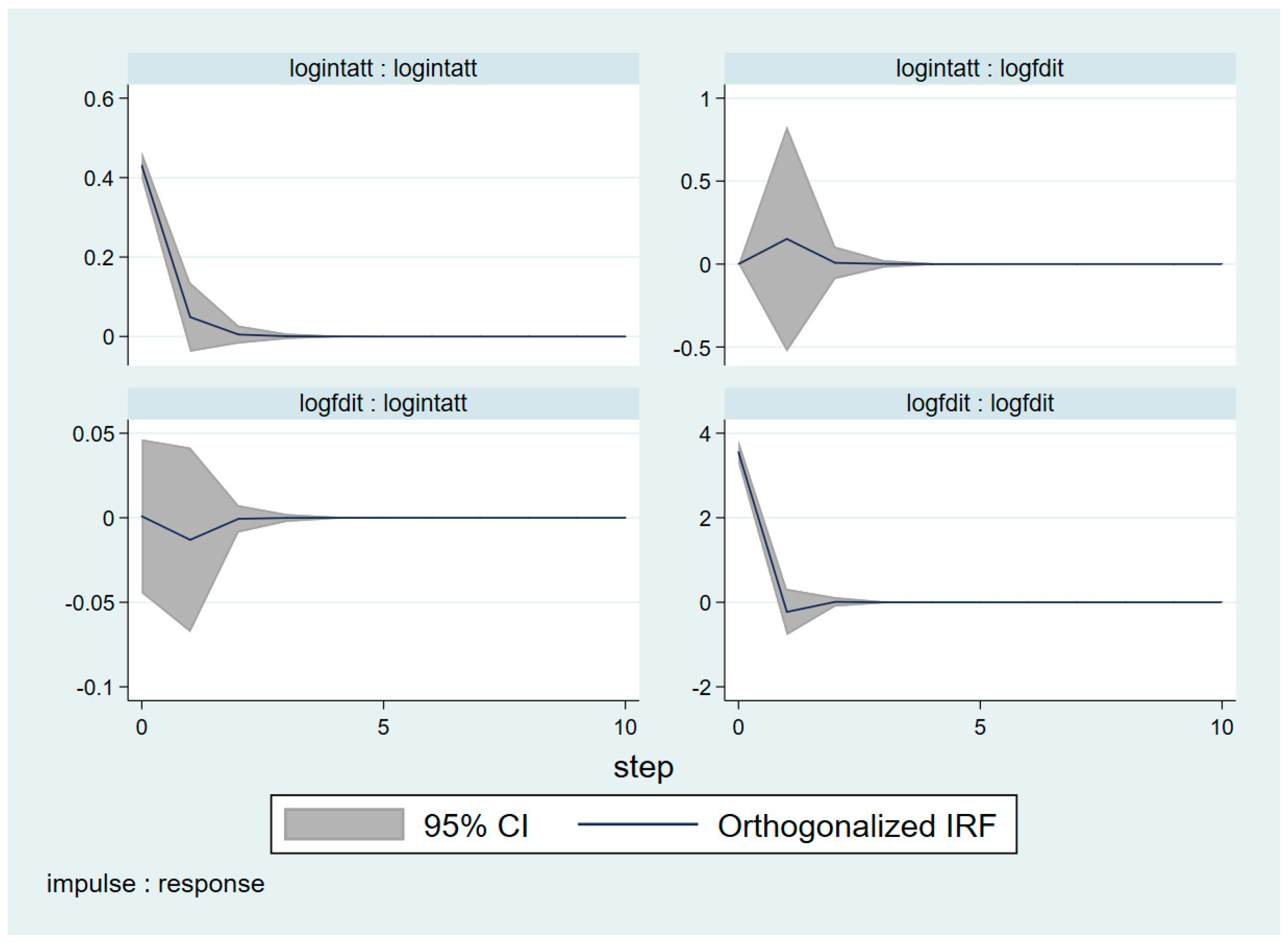

3.3. Econometric Methodology

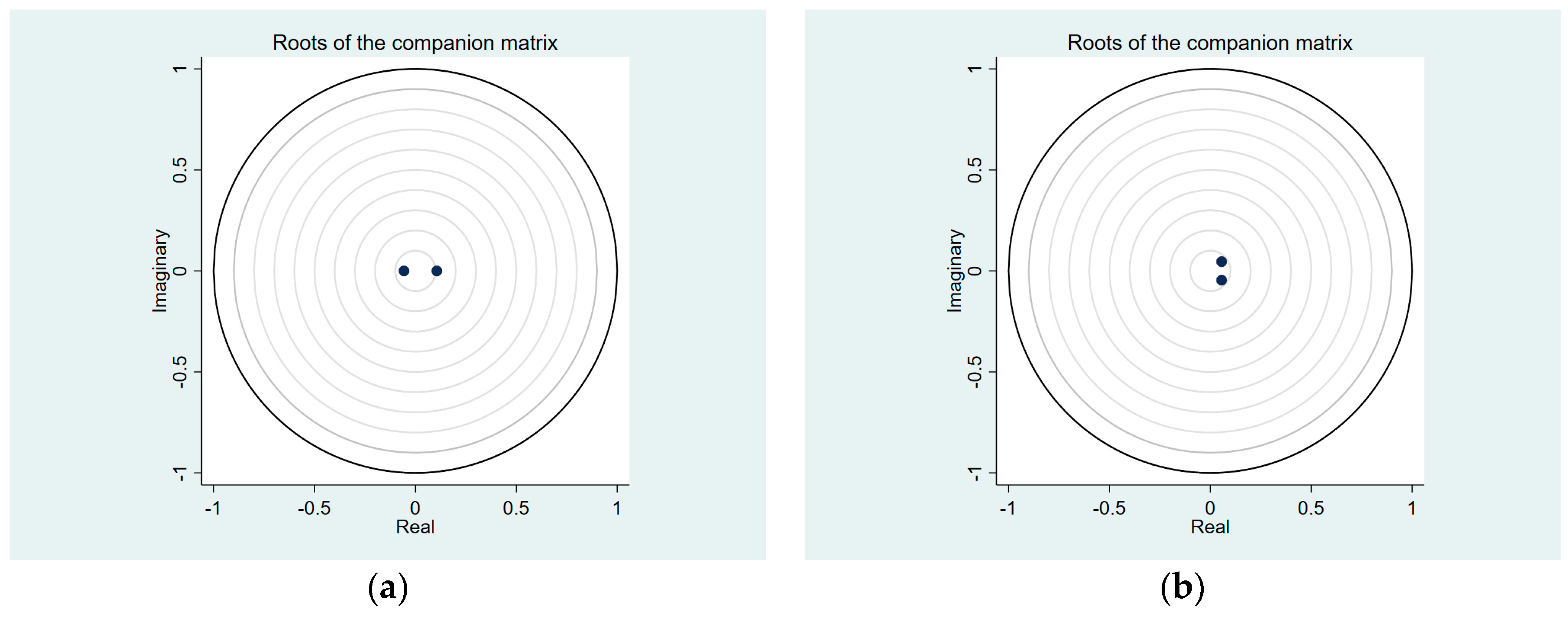

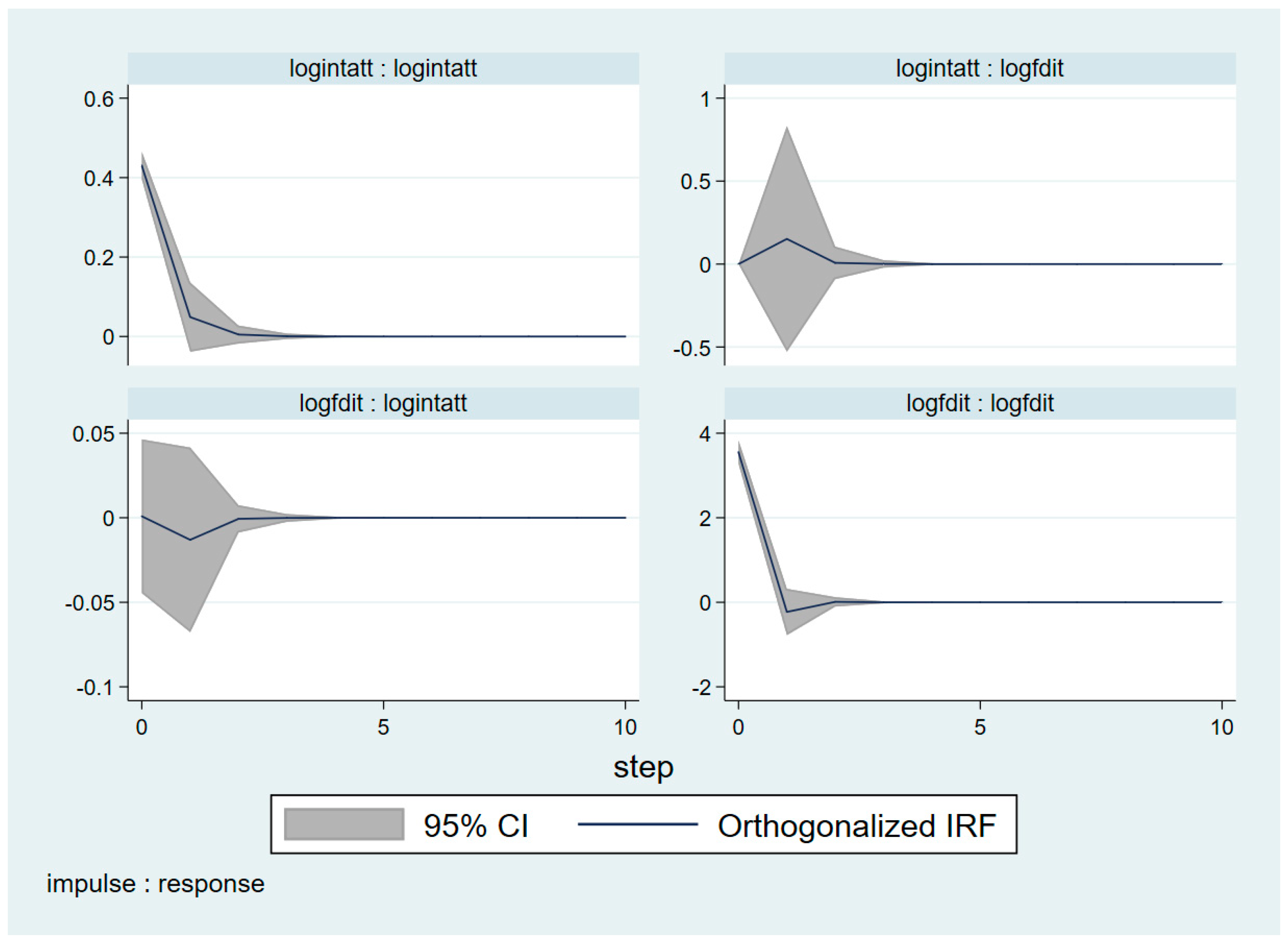

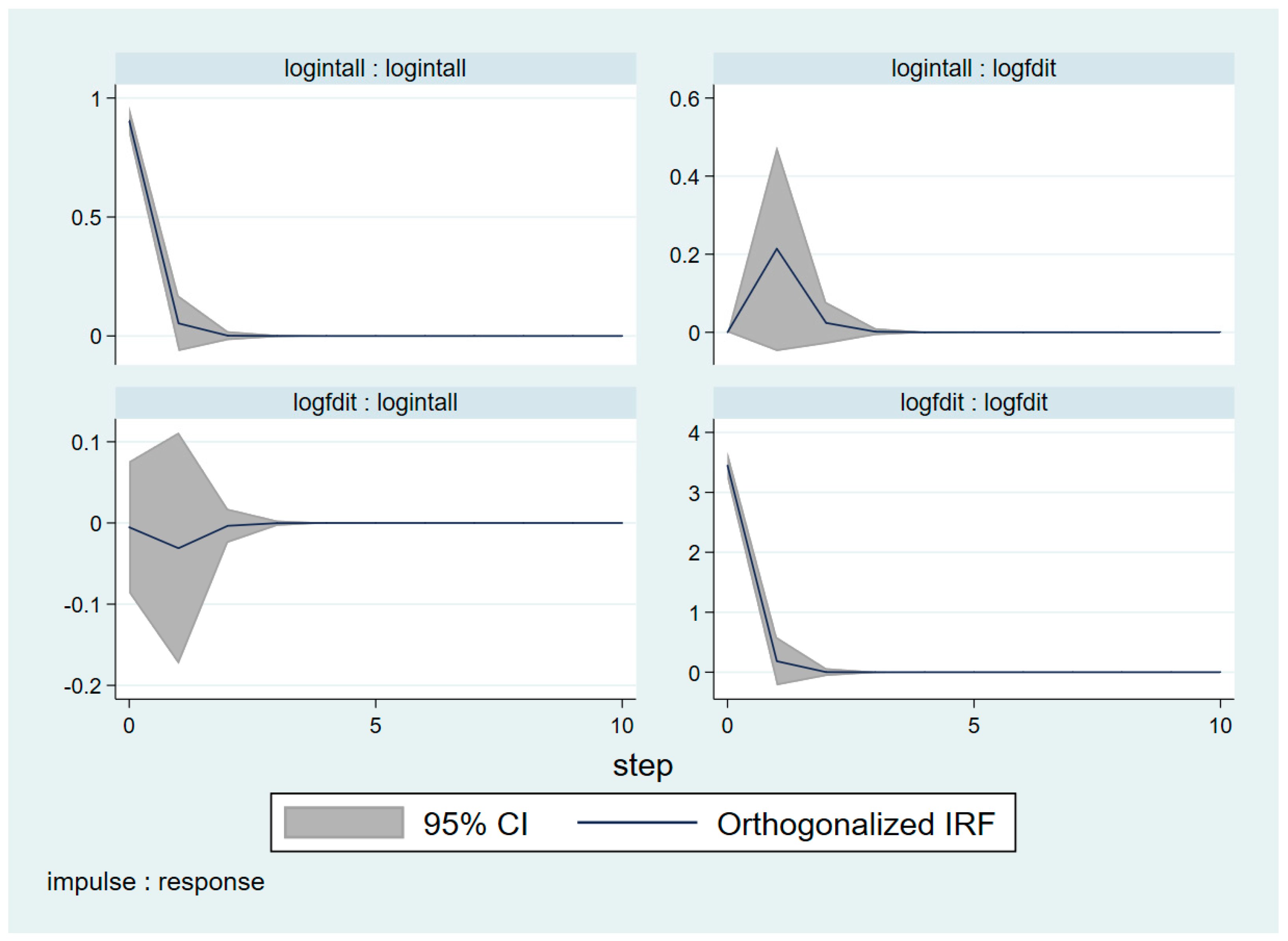

4. Research Results

5. Concluding Remarks

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| logfdit | 574 | 2.006643 | 3.790301 | −8.149729 | 8.835171 |

| logintatt | 850 | 0.3685579 | 0.7320667 | 0 | 4.204693 |

| logintall | 850 | 0.4570625 | 1.317708 | 0 | 9.789254 |

| logintarr_p | 850 | 0.4626352 | 0.3558233 | 0 | 1.847234 |

| logka_open | 745 | 0.5320018 | 0.2047938 | 0 | 0.6931472 |

| logkofgi | 784 | 4.293395 | 0.1655348 | 3.667282 | 4.507197 |

| loggdppc | 850 | 9.616736 | 1.223536 | 5.547282 | 11.62597 |

| Year | Missing Data Ratio | Country | Missing Data Ratio | Country | Missing Data Ratio | Country | Missing Data Ratio |

|---|---|---|---|---|---|---|---|

| 2000 | 0.60 | Australia | 0.12 | Iceland | 0.00 | Norway | 0.65 |

| 2001 | 0.52 | Austria | 0.24 | India | 0.29 | Poland | 0.00 |

| 2002 | 0.46 | Belgium | 0.65 | Ireland | 0.53 | Portugal | 0.35 |

| 2003 | 0.46 | Bosnia and Herzegovina | 0.65 | Israel | 0.59 | Russia | 0.59 |

| 2004 | 0.42 | Bulgaria | 0.82 | Italy | 0.00 | Serbia | 0.65 |

| 2005 | 0.34 | Chile | 0.35 | Kazakhstan | 0.59 | Slovak Republic | 0.12 |

| 2006 | 0.28 | China | 0.88 | Korea | 0.00 | Slovenia | 0.35 |

| 2007 | 0.32 | Croatia | 0.00 | Kosovo | 0.71 | Spain | 0.06 |

| 2008 | 0.30 | Czech Republic | 0.06 | Latvia | 0.00 | Sweden | 0.71 |

| 2009 | 0.28 | Denmark | 0.18 | Lithuania | 0.24 | Switzerland | 0.88 |

| 2010 | 0.20 | Estonia | 0.00 | Luxembourg | 0.29 | Thailand | 0.29 |

| 2011 | 0.22 | Finland | 0.41 | Macedonia | 0.53 | Tunisia | 0.12 |

| 2012 | 0.18 | France | 0.00 | Mauritius | 0.11 | Turkey | 0.18 |

| 2013 | 0.24 | Germany | 0.06 | Mexico | 0.24 | United Kingdom | 0.24 |

| 2014 | 0.20 | Greece | 0.06 | Morocco | 0.59 | United States | 0.00 |

| 2015 | 0.24 | Hong Kong | 0.24 | Mozambique | 0.71 | Vietnam | 0.88 |

| 2016 | 0.26 | Hungary | 0.06 | Netherland | 0.00 |

| Variance Period | Variance Decomposition of Logfdit | Variance Decomposition of Intatt | ||

| Logfdit | Logintatt | Logfdit | Logintatt | |

| 0 | 0 | 0 | 0 | 0 |

| 1 | 1 | 0 | 4.37 × 10−6 | 0.9999956 |

| 2 | 0.9981868 | 0.0018131 | 0.0009129 | 0.9990872 |

| 3 | 0.9981825 | 0.0018175 | 0.0009149 | 0.9990851 |

| 4 | 0.9981824 | 0.0018176 | 0.000915 | 0.9990851 |

| 5 | 0.9981824 | 0.0018176 | 0.000915 | 0.9990851 |

| 6 | 0.9981824 | 0.0018176 | 0.000915 | 0.9990851 |

| 7 | 0.9981824 | 0.0018176 | 0.000915 | 0.9990851 |

| 8 | 0.9981824 | 0.0018176 | 0.000915 | 0.9990851 |

| 9 | 0.9981824 | 0.0018176 | 0.000915 | 0.9990851 |

| 10 | 0.9981824 | 0.0018176 | 0.000915 | 0.9990851 |

| Variance Period | Variance Decomposition of Logfdit | Variance Decomposition of Intall | ||

| Logfdit | Logintall | Logfdit | Logintall | |

| 0 | 0 | 0 | 0 | 0 |

| 1 | 1 | 0 | 0.000034 | 0.999966 |

| 2 | 0.9961649 | 0.0038351 | 0.0012115 | 0.9987885 |

| 3 | 0.9961168 | 0.0038831 | 0.0012261 | 0.9987739 |

| 4 | 0.9961166 | 0.0038834 | 0.0012261 | 0.9987739 |

| 5 | 0.9961166 | 0.0038834 | 0.0012261 | 0.9987739 |

| 6 | 0.9961166 | 0.0038834 | 0.0012261 | 0.9987739 |

| 7 | 0.9961166 | 0.0038834 | 0.0012261 | 0.9987739 |

| 8 | 0.9961166 | 0.0038834 | 0.0012261 | 0.9987739 |

| 9 | 0.9961166 | 0.0038834 | 0.0012261 | 0.9987739 |

| 10 | 0.9961166 | 0.0038834 | 0.0012261 | 0.9987739 |

References

- Abadie, Alberto, and Javier Gardeazabal. 2008. Terrorism and the world economy. European Economic Review 52: 1–27. [Google Scholar] [CrossRef]

- Abrigo, Michael R. M., and Inessa Love. 2015. Estimation of Panel Vector Autoregression in Stata: A Package of Programs. Available online: http://paneldataconference2015.ceu.hu/Program/Michael-Abrigo.pdf (accessed on 21 June 2018).

- Asongu, Simplice, Uchenna Efobi, and Ibukun Beecroft. 2015. FDI, Aid, Terrorism: Conditional Threshold Evidence from Developing Countries. Yaoundé: African Governance and Development Institute, pp. 1–26. [Google Scholar] [CrossRef]

- Atherton, Mike. 2016. Facing New Threats: Challenges and Risk in Today’s Travel Industry. Available online: http://www.manticpoint.com/blog/facing-new-threats-challenges-and-risk-in-todays-travel-industry (accessed on 28 June 2018).

- ATKearney. 2015. The 2015 A.T. Kearney Foreign Direct Investment Confidence Index: Connected Risks—Investing in a Divergent World. Chicago: ATKearney. [Google Scholar]

- Bandyopadhyay, Subhayuand, Todd Sandler, and Javed Younas. 2014. Foreign direct investment, aid, and terrorism. Oxford Economic Papers 66: 25–50. [Google Scholar] [CrossRef]

- Barrowclough, Diana, Anne Miroux, and Hafiz Mirza, eds. 2007. FDI in Tourism: The Development Dimension. New York and Geneva: UNCTAD. [Google Scholar]

- Barry, Colin M., and Matthew DiGiuseppe. 2018. Transparency, Risk, and FDI. Political Research Quarterly 72: 132–46. [Google Scholar] [CrossRef]

- Bass, Bernard M., Donald W. McGregor, and James L. Walters. 1977. Selecting foreign plant sites: Economic, social and political considerations. The Academy of Management Journal 20: 535–51. [Google Scholar]

- Bassil, Charbel. 2014. The Effect of Terrorism on Tourism Demand in the Middle East. Peace Economics, Peace Science, and Public Policy 20: 669–84. [Google Scholar] [CrossRef]

- Berry, Charles. 2007. The Convergence of the Terrorism Insurance and Political Risk Insurance Markets for Emerging Market Risk: Why It Is Necessary and How It Will Come About. In International Political Risk Management: Needs of the Present, Challenges for the Future. Edited by Theodore H. Moran, Gerald T. West and Keith Martin. Washington, DC: The World Bank, pp. 13–35. [Google Scholar]

- Bezić, Heri, Maja Nikšić Radić, and Tomislav Kandžija. 2010. Foreign direct investments in the tourism sector of the Republic of Croatia. Valahian Journal of Economic Studies-An International Review of Theories and Applied Studies in Performance Management 1: 21–28. [Google Scholar]

- Bharwani, Sonia, and David Mathews. 2012. Risk identification and analysis in the hospitality industry: Practitioners’ perspectives from India. Worldwide Hospitality and Tourism Themes 4: 410–27. [Google Scholar] [CrossRef]

- Blanton, Robert G., and Shannon L. Blanton. 2012. Rights, institutions, and foreign direct investment: An empirical assessment. Foreign Policy Analysis 8: 431–51. [Google Scholar] [CrossRef]

- Blomberg, S. Brock, Gregory D. Hess, and Athanasios Orphanides. 2004. The macroeconomic consequences of terrorism. Journal of Monetary Economics 51: 1007–32. [Google Scholar] [CrossRef]

- Blonigen, Bruce A., and Jeremy Piger. 2014. Determinants of foreign direct investment. Canadian Journal of Economics/Revue Canadienne D’économique 47: 775–812. [Google Scholar] [CrossRef]

- Chermak, Janie M. 1992. Political risk analysis: Past and present. Resources Policy 18: 167–78. [Google Scholar] [CrossRef]

- Craigwell, Roland, and Winston Moore. 2008. Foreign direct investment and tourism in SIDS: Evidence from panel causality tests. Tourism Analysis 13: 427–32. [Google Scholar]

- Crenshaw, Martha. 1983. Terrorism, Legitimacy, and Power: The Consequences of Political Violence: Essays. Middletown: Wesleyan University Press. [Google Scholar]

- De Silva, Samantha. 2017. Role of Education in the Prevention of Violent. Working Paper World Bank Group. Available online: http://documents.worldbank.org/curated/en/448221510079762554/Role-of-education-in-the-prevention-of-violent-extremism (accessed on 28 June 2018).

- Doggrell, Katherine. 2017. This Is More Threatening to Hotel Revenue than Terror Attacks. Available online: https://www.hotelmanagement.net/own/more-threatening-to-hotel-revenue-than-terror-attacks (accessed on 22 April 2018).

- Dreher, Axel. 2006. Does globalization affect growth? Evidence from a new index of globalization. Applied Economics 38: 1091–110. [Google Scholar] [CrossRef]

- Dunning, J. H. 1981. International Production and the Multinational Enterprise. London: Allen & Unwin. [Google Scholar]

- Dwyer, Larry, Peter Forsyth, and Wayne Dwyer. 2010. Tourism Economics and Policy. Cheltenham: Channel View Publications. [Google Scholar]

- Eckstein, Zvi, and Daniel Tsiddon. 2004. Macroeconomic consequences of terror: Theory and the case of Israel. Journal of Monetary Economics 51: 971–1002. [Google Scholar] [CrossRef]

- EIU. 2008. Risk 2018: Planning for an Unpredictable Decade. New York: EIU. [Google Scholar]

- Enders, Walter, Todd Sandler, and Gerald F. Parise. 1992. An Econometric Analysis of the Impact of Terrorism on Tourism. Kyklos 45: 531–54. [Google Scholar] [CrossRef]

- Enders, Walter, Adolfo Sachsida, and Todd Sandler. 2006. The impact of transnational terrorism on US foreign direct investment. Political Research Quarterly 59: 517–31. [Google Scholar] [CrossRef]

- Enders, Walter, Todd Sandler, and Khusrav Gaibulloev. 2011. Domestic versus transnational terrorism: Data, decomposition, and dynamics. Journal of Peace Research 48: 319–37. [Google Scholar] [CrossRef]

- Endo, Kumi. 2006. Foreign direct investment in tourism—Flows and volumes. Tourism Management 27: 600–14. [Google Scholar] [CrossRef]

- Fatehi-Sedeh, Kamal, and M. Hossein Safizadeh. 1989. The association between political instability and flow of foreign direct investment. Management International Review 29: 4–13. Available online: https://www.jstor.org/stable/40227943 (accessed on 15 June 2018).

- Feinberg, Susan E., and Anil K. Gupta. 2009. MNC subsidiaries and country risk: Internalization as a safeguard against weak external institutions. Academy of Management Journal 52: 381–99. [Google Scholar] [CrossRef]

- Fereidouni, Hassan Gholipour, and Usama Al-mulali. 2014. The interaction between tourism and FDI in real estate in OECD countries. Current Issues in Tourism 17: 105–13. [Google Scholar] [CrossRef]

- Fingar, Courtney. 2017. Inside fDi: Why the Tourism Industry is Finally Going Places. Available online: https://www.fdiintelligence.com/Inside-fDi/Inside-fDi-Why-the-tourism-industry-is-finally-going-places (accessed on 29 May 2018).

- Formica, Sandro. 1996. Political risk analysis in relation to foreign direct investment: A view from the hospitality industry. The Tourist Review 51: 15–23. [Google Scholar] [CrossRef]

- Friedman, Thomas L. 1996. Foreign Affairs Big Mac I. Available online: https://www.nytimes.com/1996/12/08/opinion/foreign-affairs-big-mac-i.html (accessed on 6 June 2018).

- Globerman, Steven, and Daniel Shapiro. 2003. Governance infrastructure and US foreign direct investment. Journal of International Business Studies 34: 19–39. [Google Scholar] [CrossRef]

- Goldman, Ogen S., and Michal Neubauer-Shani. 2017. Does international tourism affect transnational terrorism? Journal of Travel Research 56: 451–67. [Google Scholar] [CrossRef]

- Granger, Clive WJ. 1969. Investigating causal relations by econometric models and cross-spectral methods. Econometrica 37: 424–38. [Google Scholar] [CrossRef]

- Green, Robert T. 1974. Political structures as a predictor of radical political change. Columbia Journal of World Business 9: 28–36. [Google Scholar]

- Gygli, Savina, Florian Haelg, and Jan-Egbert Sturm. 2018. The KOF Globalisation Index—Revisited. KOF Working Papers. Zurich: ETH Zurich. [Google Scholar] [CrossRef]

- Haddad, Stéphane. 2018. M&A in Hospitality: Stick or Twist? Available online: https://www.hotel-online.com/press_releases/release/ma-in-hospitality-stick-or-twist (accessed on 15 July 2018).

- Hallberg, Arvid. 2016. Expecting the Unexpected: The Marginal Effect of Unanticipated Terrorist Attacks on Foreign Direct Investment in Israel and Turkey. Dissertation. Available online: http://urn.kb.se/resolve?urn=urn:nbn:se:uu:diva-297402 (accessed on 10 May 2018).

- Harper, David. 2017. The Diminishing Impact of Terrorism. Available online: http://hotelspec.com/wp-content/uploads/2017/10/The-diminishing-impact-of-terrorism.pdf (accessed on 13 June 2018).

- Hitchcock, Michael, and I. Nyoman Darma Putra. 2005. The Bali bombings: Tourism crisis management and conflict avoidance. Current Issues in Tourism 8: 62–76. [Google Scholar] [CrossRef]

- Holden, Andrew. 2013. Tourism, Poverty and Development. London: Routledge. [Google Scholar]

- Holtz-Eakin, Douglas, Whitney Newey, and Harvey S. Rosen. 1988. Estimating vector autoregressions with panel data. Econometrica 56: 1371–95. [Google Scholar] [CrossRef]

- Hongkong and Shanghai Hotels. 2016. The Hongkong and Shanghai Hotels Annual Report 2015: Tradition meets Innovation. Hong Kong: The Hongkong and Shanghai Hotels. [Google Scholar]

- IEP. 2018. Global Peace Index 2018. New York: IEP, p. 58. [Google Scholar]

- Jarvis, Darryl S. L., and Martin Griffiths. 2007. Learning to fly: The evolution of political risk analysis. Global Society 21: 5–21. [Google Scholar] [CrossRef]

- Katircioglu, Salih. 2011. The Bounds Test to the Level Relationship and Causality between Foreign Direct Investment and International Tourism: The Case of Turkey. Ekonomie a Management 14: 6–13. Available online: http://www.ekonomie-management.cz/download/1346061130_0a07/2011_01_katircioglu.pdf (accessed on 25 May 2018).

- Kis-Katos, Krisztina, Helge Liebert, and Günther G. Schulze. 2011. On the origin of domestic and international terrorism. European Journal of Political Economy 27: S17–S36. [Google Scholar] [CrossRef]

- Kobrin, Stephen J. 1979. Political risk: A review and reconsideration. Journal of International Business Studies 10: 67–80. [Google Scholar] [CrossRef]

- Kobrin, Stephen J. 1980. Foreign enterprise and forced divestment in LDCs. International Organization 34: 65–88. [Google Scholar] [CrossRef]

- Kolstad, Ivar, and Espen Villanger. 2008. Determinants of foreign direct investment in services. European Journal of Political Economy 24: 518–33. [Google Scholar] [CrossRef]

- Krug, Barbara, and Patrick Reinmoeller. 2003. The Hidden Cost of Ubiquity: Globalisation and Terrorism. ERIM Report Series, No. ERS-2003-062-ORG. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=463810 (accessed on 28 May 2018).

- Kumar, Sanjay, and Jiangxia Liu. 2015. Contagion in International Stock Markets from Terrorist Attacks. Edited by Karin Glaser. Hague: Eleven International Publishing. [Google Scholar]

- Kundu, Sumit K., and Farok J. Contractor. 1999. Country location choices of service multinationals: An empirical study of the international hotel sector. Journal of International Management 5: 299–317. [Google Scholar] [CrossRef]

- Latif, Zahid, Zeng Jianqiu, Shafaq Salam, Zulfiqar Hussain Pathan, Nasir Jan, and Muhammad Zahid Tunio. 2017. FDI and ‘political’violence in Pakistan’s telecommunications. Human Systems Management 36: 341–52. [Google Scholar] [CrossRef]

- Lee, Chia-yi. 2017. Terrorism, Counterterrorism Aid, and Foreign Direct Investment. Foreign Policy Analysis 13: 168–87. [Google Scholar] [CrossRef]

- Levis, Mario. 1979. Does political instability in developing countries affect foreign investment flow? An empirical examination. Management International Review 19: 59–68. [Google Scholar]

- Li, Quan. 2006. Political Violence and Foreign Direct Investment. In Regional Economic Integration. Edited by Michele Fratianni. Bingley: Emerald Group Publishing Limited, pp. 225–49. [Google Scholar]

- Li, Quan. 2008. Foreign direct investment and interstate military conflict. Journal of International Affairs 62: 53–66. Available online: https://www.jstor.org/stable/24358144 (accessed on 25 May 2018).

- Li, Quan, and Adam Resnick. 2003. Reversal of Fortunes: Democratic Institutions and Foreign Direct Investment Inflows to Developing Countries. International Organization 57: 175–211. [Google Scholar] [CrossRef]

- Li, Quan, and Drew Schaub. 2004. Economic Globalization and Transnational Terrorism A Pooled Time-Series Analysis. Journal of Conflict Resolution 48: 230–58. [Google Scholar] [CrossRef]

- Liu, Wen-Hsien. 2005. Determinants of the semiconductor industry cycles. Journal of Policy Modeling 27: 853–66. [Google Scholar] [CrossRef]

- Loree, David W., and Stephen E. Guisinger. 1995. Policy and non-policy determinants of US equity foreign direct investment. Journal of International Business Studies 26: 281–99. [Google Scholar] [CrossRef]

- Lutkepohl, H. 2005. New Introduction to Multiple Time Series Analysis. New York: Springer. [Google Scholar]

- Lutz, James M., and Brenda J. Lutz. 2006. International Terrorism in Latin America: Efforts on Foreign Investment and Tourism. Journal of Social, Political, and Economic Studies 31: 321–38. Available online: http://www.jspes.org/fall2006_lutz.html (accessed on 14 June 2018).

- Lutz, Brenda J., and James M. Lutz. 2017. Globalization and the Economic Consequences of Terrorism. New York: Springer. [Google Scholar]

- Maslow, Abraham Harold. 1970. Motivation and Personality, 2nd ed. New York: Harper & Row. [Google Scholar]

- Mathews, Harry G. 1975. International tourism and political science research. Annals of Tourism Research 2: 195–203. [Google Scholar] [CrossRef]

- Matthee, Heinrich. 2011. Political Risk Analysis. In International Encyclopedia of Political Science. Edited by Bertrand Badie, Dirk Berg-Schlosser and Leonardo Morlino. Thousand Oaks: Sage, pp. 2010–13. [Google Scholar]

- Mazzarella, John J. 2005. Terrorism and Multinational Corporations: International Business Deals with the Costs of Geopolitical Conflict. Major Themes in Economics 7: 59–73. [Google Scholar]

- Metaxas, Theodore, and Polyxeni Kechagia. 2017. FDI and Terrorism in developing Asia: Approaches and Discussion. Munich Personal RePEc Archive. No. 78165. Munich: University Library of Munich, Available online: https://mpra.ub.uni-muenchen.de/78165/ (accessed on 14 June 2018).

- Mihalache, Andreea S. 2010. Who’s afraid of political violence? Evidence from industry level FDI flows. Paper Presented at the Annual Meeting of the Theory vs. Policy? Connecting Scholars and Practioners, New Orleans, LA, USA, February 17–20. [Google Scholar]

- Nigh, Douglas. 1985. The effect of political events on United States direct foreign investment: A pooled time-series cross-sectional analysis. Journal of International Business Studies 16: 1–17. [Google Scholar] [CrossRef]

- Nikšić Radić, Maja. 2018. Terrorism as a Determinant of Attracting FDI in Tourism: Panel Analysis. Sustainability 10: 4553. [Google Scholar] [CrossRef]

- Nikšić Radić, Maja, and Matea Barišić. 2018. Does Terrorism have a Limited Impact on International Investments in Tourism? Some Theoretical Considerations. Almatourism-Journal of Tourism, Culture and Territorial Development 9: 153–64. [Google Scholar]

- Nikšić Radić, Maja, Daniel Dragičević, and Marina Barkiđija Sotošek. 2018. The tourism-led terrorism hypothesis--evidence from Italy, Spain, UK, Germany and Turkey. Journal of International Studies 11: 236–49. [Google Scholar] [CrossRef]

- O’Connor, Noëlle, Mary Rose Stafford, and Gerry Gallagher. 2008. The impact of global terrorism on Ireland’s tourism industry: An industry perspective. Tourism and Hospitality Research 8: 351–63. [Google Scholar] [CrossRef]

- Oaten, Simon, Katharine Le Quesne, and Harry Segal. 2015. Adapting to Uncertainty—The Global Hotel Industry. Geneva. Available online: Deloitte LLPhttp://www3.weforum.org/docs/TT15/WEF_TTCR_Chapter1.2_2015.pdf (accessed on 14 June 2018).

- Olibe, Kingsley O., and C. Larry Crumbley. 1997. Determinants of US private foreign direct investments in OPEC nations: From public and non-public policy perspectives. Journal of Public Budgeting, Accounting & Financial Management 9: 331–55. [Google Scholar] [CrossRef]

- Othman, R., Norlida H. M. Salleh, and Tamat Sarmidi. 2012. Analysis of Causal Relationship between Tourism Development, Economic Growth and Foreign Direct Investment: An ARDL Approach. Journal of Applied Sciences 12: 1245–54. [Google Scholar] [CrossRef]

- Pearce, Philip L. 2005. Tourist Behaviour: Themes and Conceptual Schemes. Bristol: Channel View Publications. [Google Scholar]

- Perić, Jože, and Maja Nikšić Radić. 2016. FDI-led tourism growth hypothesis: Empirical evidence from Croatian tourism. European Journal of Tourism, Hospitality and Recreation 7: 168–75. [Google Scholar] [CrossRef]

- Pizam, Abraham, and Aliza Fleischer. 2002. Severity versus frequency of acts of terrorism: Which has a larger impact on tourism demand? Journal of Travel Research 40: 337–39. [Google Scholar] [CrossRef]

- Porcano, Thomas M. 1993. Factors affecting the foreign direct investment decision of firms from and into major industrialized countries. Multinational Business Review 1: 26. [Google Scholar]

- Powers, Matthew, and Seung-Whan Choi. 2012. Does transnational terrorism reduce foreign direct investment? Business-related versus non-business-related terrorism. Journal of Peace Research 49: 407–22. [Google Scholar] [CrossRef]

- Rivoli, Pietra, and Eugene Salorio. 1996. Foreign direct investment and investment under uncertainty. Journal of International Business Studies 27: 335–57. [Google Scholar] [CrossRef]

- Ryans, John K., Jr., and William L. Shanklin. 1980. How managers cope with terrorism. California Management Review 23: 66–72. [Google Scholar] [CrossRef]

- Salleh, Norlida Hanim Mohd, Redzuan Othman, and Tamat Sarmidi. 2011. An Analysis of The Relationships Between Tourism Development And Foreign Direct Investment: An Empirical Study In Elected Major Asian Countries. International Journal of Business and Social Science 2: 250–57. [Google Scholar]

- Samimi, Ahmad Jafari, Somaye Sadeghi, and Soraya Sadeghi. 2013. The Relationship between Foreign Direct Investment and Tourism Development: Evidence from Developing Countries. Institutions and Economies 5: 59–68. [Google Scholar]

- Sanford, Douglas M., Jr., and Huiping Dong. 2000. Investment in familiar territory: Tourism and new foreign direct investment. Tourism Economics 6: 205–19. [Google Scholar] [CrossRef]

- Schneider, Friedrich, and Bruno S. Frey. 1985. Economic and political determinants of foreign direct investment. World Development 13: 161–75. [Google Scholar] [CrossRef]

- Selvanathan, Saroja, E. Antony Selvanathan, and Brinda Viswanathan. 2012. Causality between foreign direct investment and tourism: Empirical evidence from India. Tourism Analysis 17: 91–98. [Google Scholar] [CrossRef]

- Sethi, Deepak, Stephen E. Guisinger, Steven E. Phelan, and David M. Berg. 2003. Trends in foreign direct investment flows: A theoretical and empirical analysis. Journal of International Business Studies 34: 315–26. [Google Scholar] [CrossRef]

- Shehadi, Sebastian. 2017. On a Journey: Tourism Takes a New Turn towards Sustainable Development. Available online: https://www.fdiintelligence.com/Sectors/Hotels-Tourism/On-a-journey-tourism-takes-a-new-turn-towards-sustainable-development (accessed on 14 June 2018).

- Sinclair, Thea A., and M. J. Stabler. 1991. The Tourism Industry: An International Analysis. Wallingford: CAB International. [Google Scholar]

- Sonmez, Sevil F., and Alan R. Graefe. 1998. Influence of terrorism risk on foreign tourism decisions. Annals of Tourism Research 25: 112–44. [Google Scholar] [CrossRef]

- Sottilotta, Cecilia Emma. 2017. Rethinking Political Risk: Concepts, Theories, Challenges. New York: Routledge. [Google Scholar]

- START. 2017. Global Terrorism Database Codebook: Inclusion Criteria and Variables. Available online: http://www.start.umd.edu/gtd/downloads/Codebook.pdf (accessed on 15 January 2018).

- START. 2018. Global Terrorism Database (Data File). College Park: National Consortium for the Study of Terrorism and Responses to Terrorism. [Google Scholar]

- Steiner, Christian. 2010. An overestimated relationship? Violent political unrest and tourism foreign direct investment in the Middle East. International Journal of Tourism Research 12: 726–38. [Google Scholar] [CrossRef]

- Stohl, Michael. 2003. The Mystery of the New Global Terrorism: Old Myths, New Realities? In The New Global Terrorism: Characteristics, Causes, Controls. Edited by Charles W. Kegley. Upper Saddle River: Pearson. [Google Scholar]

- Tang, Sumei, E. Antony Selvanathan, and Saroja Selvanathan. 2007. The relationship between foreign direct investment and tourism: Empirical evidence from China. Tourism Economics 13: 25–39. [Google Scholar] [CrossRef]

- Thunell, Lars H. 1977. Political Risks in International Business: Investment Behavior of Multinational Corporations. New York and London: Praeger Publishers. [Google Scholar]

- Tosun, M. Umur, M. Onur Yurdakul, and Pelin Varol Iyidogan. 2014. The relationship between corruption and foreign direct investment inflows in Turkey: An empirical examination. Transylvanian Review of Administrative Sciences 10: 247–57. [Google Scholar]

- UNCTAD. Forthcoming. Methods of Data Collection and National Policies in the Treatment of FDI. Available online: http://unctad.org/en/Pages/DIAE/Methods-of-Data-Collection-and-National-Policies-in-the-Treatment-of-FDI.aspx (accessed on 15 May 2018).

- UNESCO. 2017. Preventing Violent Extremism through Education: A Guide for Policy-Makers. Paris: UNESCO. [Google Scholar]

- UNWTO. 2017. UNWTO Tourism Highlights: 2017 Edition. Madrid: UNWTO. [Google Scholar]

- UNWTO. 2018. UNWTO World Tourism Barometer. Madrid: UNWTO. [Google Scholar]

- Vargas, Mauricio, and Florian Sommer. 2015. Political Risks and Their Impact on Government Bonds. Frankfurt am Main: Union Investment Institutional GmbH. [Google Scholar]

- Witte, Caroline T., Martijn J. Burger, Elena I. Ianchovichina, and Enrico Pennings. 2017. Dodging bullets: The heterogeneous effect of political violence on greenfield FDI. Journal of International Business Studies 48: 862–92. [Google Scholar] [CrossRef]

- WTTC. 2018. Travel & Tourism Global Economic Impact and Issues 2018. London: WTTC. [Google Scholar]

- Zhang, Jianhong, Haico Ebbers, and Chaohong Zhou. 2011. Flows of Tourists, Commodities and Investment: The Case of China. In Tourism Economics: Impact Analysis. Edited by Alvaro Matias, Peter Nijkamp and Manuela Sarmento. New York: Springer, pp. 43–63. [Google Scholar]

- Zillman, Claire. 2015. Terrorism’s Effect on Tourism Doesn’t Last Very Long. Available online: http://fortune.com/2015/11/30/terrorism-tourism-paris/ (accessed on 16 September 2017).

- Hamilton, James D. 1994. Time Series Analysis. Princeton: Princeton University Press. [Google Scholar]

| Authors | Sample and Period | Methodology | Results |

|---|---|---|---|

| Schneider and Frey (1985) | 54 developing countries, 1976–1980 | Multiple regression analysis | Political instability has a negative influence on FDI inflow |

| Nigh (1985) | 24 countries, 1954–1975 | The pooled time-series cross-section design | Conflict has a negative influence on FDI flows by US firms |

| Fatehi-Sedeh and Safizadeh (1989) | 15 countries, 1950–1982 | Multiple regression analysis | There is no evidence of statistical connotation among political stability and FDI inflow |

| Loree and Guisinger (1995) | 36 countries, 1977 and 1982 | Multiple regression analysis | Political stability promotes FDI in 1982 but not in 1977 |

| Olibe and Crumbley (1997) | OPEC countries, 1989–1994 | Multiple regression analysis | Without evidence that political risk influences U.S. FDI flows to 10 out of 13 countries |

| Li and Resnick (2003) | 53 countries, 1982–1995 | The pooled time-series cross-section design | Political instability does not have any statistically significant effect on FDI inflows (but regime durability encourages FDI inflows) |

| Sethi et al. (2003) | 28 countries, 1981–2000 | Multiple regression analysis, factor analysis | Political instability does not affect U.S. FDI flows |

| Globerman and Shapiro (2003) | 143 countries, 1994–1997 | Probit estimates, regression | Index of political stability and violence reduce the amount of FDI inflow a country receives |

| Li and Schaub (2004) | 112 countries, 1975–1997 | Negative binomial regression | FDI inflows have a stabilising indirect effect on transnational terrorist attacks by promoting economic development |

| Hitchcock and Darma Putra (2005) | Bali | Case study | Although the Bali bombings had a huge impact on international tourism, foreign-owned resorts with strong marketing helped restore confidence in Bali after the terrorist attack |

| Enders et al. (2006) | 69 countries, 1989–1999 | Time-series intervention analysis | Terrorism has a significant effect on US FDI in OECD countries, but the effect disappears in non-OECD countries |

| Li (2006) | 129 countries, 1976–1996 | The pooled time-series cross-section design | Transnational terrorism in a country does not affect its chances of being chosen as an investment destination or the amount it receives once being chosen |

| Lutz and Lutz (2006) | Theoretical discussion | Short-term investments are more sensitive to terrorist attacks since long-term investments have higher sunk costs | |

| Abadie and Gardeazabal (2008) | 186-country full sample and the 110 countries regression sample, 2003 | The pooled time-series cross-section design | Negative correlation between terrorism and FDI |

| Kolstad and Villanger (2008) | 57 countries, 1989–2000 | Panel fixed effects estimation vs random effects estimation | Institutional quality and democracy appear more important for FDI in services than general investment risk or political stability |

| Mihalache (2010) | 50 developing countries, 1980–2004 | The pooled time-series cross-section design | Positive impact of political violence on FDI in capital-intensive tertiary sector industries such as hotels and restaurants, transportation, communications, real estate, etc. |

| Steiner (2010) | Egypt | Case study | Impact of violent political turmoil on FDI in tourism cannot be confirmed by a clear link between the observed variables. |

| Powers and Choi (2012) | 123 developing countries, 1980–2008 | The pooled time-series cross-section design | Terrorism that targets TNC in developing countries negatively affects FDI inflow to those countries, but terrorist attacks that do not target businesses have no statistically significant effect on FDI |

| Blonigen and Piger (2014) | OECD countries | Bayesian statistical techniques—systematic investigation of the determinants of FDI | No robust evidence that policy variables have an effect on FDI |

| Bandyopadhyay et al. (2014) | 78 developing countries, 1984–2008 | Dynamic panel data framework | Wealthy, developed countries with a diversified economic structure are better off with the consequences of terrorist attacks than small, poor, more specialised countries |

| Tosun et al. (2014) | Turkey, 1992M01–2010M12 | Cointegration and error correction methods | Political risk may contribute to FDI inflow |

| Lutz and Lutz (2017) | More terrorism led to more FDI in some of the regions and for the developing world as a whole, which suggested perversely that terrorism encouraged FDI, especially in the 1990s. | ||

| Nikšić Radić (2018) | 50 countries, 2000–2016 | System generalized method of moments | Terrorism is not a significant determinant that affects FDI in tourism |

| Variable | ADF-Fischer Chi Square | Conclusion |

|---|---|---|

| logfdi_t | 349.4491 *** | I(0) |

| logintatt | 444.3383 *** | I(0) |

| logintall | 354.6990 *** | I(0) |

| logint_arr_pop | 145.2888 *** | I(0) |

| logkaopen | 277.6628 *** | I(0) |

| loggdppercapita | 143.7357 *** | I(0) |

| logKOFGI | 195.4971 *** | I(0) |

| Null Hypothesis | χ2 Test | p-Value | |

|---|---|---|---|

| No control variables | logintall does not Granger cause logfdit | 2.413 | 0.120 |

| logfdit does not Granger cause logintall | 0.195 | 0.658 | |

| Including control variables | logintall does not Granger cause logfdit | 0.097 | 0.755 |

| logfdit does not Granger cause logintall | 1.922 | 0.166 | |

| No control variables | logintatt does not Granger cause logfdit | 0.225 | 0.635 |

| logfdit does not Granger cause logintatt | 0.187 | 0.666 | |

| Including control variables | logintatt does not Granger cause logfdit | 0.661 | 0.416 |

| logfdit does not Granger cause logintatt | 0.720 | 0.396 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nikšić Radić, M.; Dragičević, D.; Barkiđija Sotošek, M. Causality between Terrorism and FDI in Tourism: Evidence from Panel Data. Economies 2019, 7, 38. https://doi.org/10.3390/economies7020038

Nikšić Radić M, Dragičević D, Barkiđija Sotošek M. Causality between Terrorism and FDI in Tourism: Evidence from Panel Data. Economies. 2019; 7(2):38. https://doi.org/10.3390/economies7020038

Chicago/Turabian StyleNikšić Radić, Maja, Daniel Dragičević, and Marina Barkiđija Sotošek. 2019. "Causality between Terrorism and FDI in Tourism: Evidence from Panel Data" Economies 7, no. 2: 38. https://doi.org/10.3390/economies7020038

APA StyleNikšić Radić, M., Dragičević, D., & Barkiđija Sotošek, M. (2019). Causality between Terrorism and FDI in Tourism: Evidence from Panel Data. Economies, 7(2), 38. https://doi.org/10.3390/economies7020038