Abstract

The goal of this study is to use the Markov Regime Model (MSM) to evaluate the impact of three important FCIs and the political economy on Pakistan’s economic growth. The current research used quarterly data from 2000 to 2020. The empirical results demonstrate that dictatorship contributes favorably to the high and low growth regime of the economy, while election time contributes positively to the expansion period and adversely in recession times of the economy. Results confirmed that external debt has a strong negative influence on economic growth in both the high and low-growth regimes. Remittances, FDI, and growth, on the other hand, have a positive and substantial link with economic growth. This research suggested that effective fiscal and monetary policies, as well as a suitable political environment, should be provided so that foreign investors would be enticed to invest in Pakistan.

Keywords:

foreign capital inflows; political economy; election time; Markov Switching Model; Pakistan JEL Codes:

B22; E44; F21; F41; P16

1. Introduction

Since the time of independence, Pakistan has been making tireless efforts to boost its economic performance. Policymakers set ambitious growth targets for every fiscal year. However, despite these efforts, the country has not achieved much success due to political and social instability, terrorism, increasing population, lack of law enforcement, severe deficiencies in basic services, such as electricity generation and railway transportation, and widespread corruption (Ali and Saif 2017). According to the economic survey of Pakistan, the country’s average GDP growth rate has been volatile, with a record low of −1.80% in 1952 and an all-time high of 10.22% in 1954. During the 1960s, the average growth rate was 6.8%, followed by 4.8% in the 1970s, 6.5% in the 1980s, and 3.95% in the 1990s. The GDP growth rate in the early 2000s (2000–2005) averaged around 3–4%. From 2005 to 2007, Pakistan experienced a relatively higher GDP growth rate of around 6–7%. The global financial crisis of 2008 had an impact on Pakistan’s economy, leading to a lower GDP growth rate of around 2–3% in the late 2000s. In the early 2010s, GDP growth rate averaged around 3–4%. From 2013 onwards, Pakistan’s economy began to show signs of improvement, with the GDP growth rate picking up to around 4–5%. Towards the end of the decade, the GDP growth rate reached around 5–6%. Policymakers and analysts are concerned about Pakistan’s declining economic development tendency, which has been attributed to rising inflation, a growing budget deficit, and debt payments (Khan et al. 2017). In this regard, foreign capital inflows can serve as a viable solution to bridge the savings gap by providing the necessary funds to finance investment projects. Developing countries like Pakistan can leverage foreign capital inflows to promote economic growth, create job opportunities, and enhance competitiveness in the global market. Foreign direct investment (FDI), foreign remittances, and external debt are some of the ways foreign capital inflows can take shape. By channeling these inflows towards productive sectors, such as infrastructure and human capital development, Pakistan can mitigate the effects of its economic challenges and move towards sustainable economic development.

The factors that contribute to Pakistan’s economic growth have long been debated in Pakistan’s economic literature. According to empirical research conducted under the neoclassical growth paradigm, FCIs have a beneficial influence on economic growth. The majority of this research gave their perspective on the additional function of foreign capital, implying that inflows of foreign capital benefit the receiving economy by providing fresh resources for capital accumulation. “On the other hand, endogenous growth theory highlights the role of foreign capital inflows (FCIs) in facilitating the transmission and dissemination of knowledge. The endogenous growth model, for instance, argues that capital flows can help bridge the knowledge gap between wealthy and poor nations by providing access to resources, such as technology and expertise. By facilitating the transfer of these resources, foreign capital inflows can play a crucial role in boosting economic growth and development (Tahir et al. 2020). Two types of hypotheses were employed to explain the direction of FCIs: Push-factor and pull-factor ideas (Calvo et al. 1996; Chuhan et al. 1998). The push-factor hypothesis investigates the role of FCIs in terms of dropping international interest rates and changes in industrial nations’ economic cycles (Calvo et al. 1996; Reinhart and Calvo 2000). The pull-factor hypothesis, on the other hand, describes how capital inflows affect domestic factors such as autonomous growth in the domestic money demand function and increases in domestic capital productivity (Haq and Luqman 2014), as well as increasing domestic capital market integration with global capital markets (Agenor and Montiel 1999).

Numerous studies have consistently emphasized the substantial impact of foreign capital inflows. According to many researchers (Mohey-ud-Din 2007; Yasmin 2005; Jawaid and Saleem 2017), Foreign capital inflows like remittances, external debt, and Foreign Direct Investment are very important macroeconomic factors that influence Pakistan’s economic growth. FDI is vital for the host country’s well-being as it not only helps to mitigate capital shortfall but also serves as a channel for transferring new technology, management approaches, other innovations, and skills, as well as improving worker qualifications, resulting in economic growth, job opportunities, and an increase in the host country’s state budget (Haddad and Harrison 1993; Markusen and Venables 1999).

Remittances are another major FCI that contributes towards economic growth. Inflows of remittances primarily assist poor households in reducing the negative consequences of income shocks (Yang and Choi 2007). Transfer of direct income also improves the living standard of the recipient family by increasing their marginal propensity to save (Javid et al. 2012). Furthermore, the impact of remittance inflows extends beyond economic growth to encompass the accumulation of physical and human capital, total factor productivity growth, and labor force participation (Barajas et al. 2009).

Remittance inflows help in building the infrastructure and accumulation of human capital (Taylor 1999) and increase access to better healthcare services and education (Orozco 2002). Economic theories advise that a low amount of debt can assist both emerging and developed countries by boosting their economic growth. However, some theories also contend that rising debt levels stifle economic growth because of an increase in government borrowing. This surge in borrowing raises interest rates, which, in turn, raises the cost of renting for both investment and consumption, a phenomenon known as the crowding effect (Kharusi and Ada 2018).

Economic stability and growth are fundamental pillars for the development of any nation. It is widely recognized that political instability can create ambiguity and uncertainty, leading to a decline in investment and a reduction in economic growth. Furthermore, political uncertainty can alter the pattern of expenditure and influence the nature of investment, which can have a direct impact on economic growth (Asteriou and Price 2001). Given the critical link between political stability and economic growth, it is crucial to evaluate the impact of foreign capital inflows on the Pakistani economy within the context of its political economy. Previous research has indicated that an unstable political situation in Pakistan creates uncertainty in policies and decision-making, making it essential to explore strategies to promote economic stability and growth (MengYun et al. 2018; Irshad 2017). Investors often view political instability and frequent changes in government as potential risks to their investments. As a result, investors invest in countries with more stable political environments and less political uncertainty. Due to the decline in investment productivity, consumption, and savings were also affected. The decline in investment productivity reduces the overall output and returns generated by investments, leading to lower income levels. This, in turn, impacts consumption and savings as individuals have less disposable income available for spending and saving. Political unrest disrupts economic activities, undermines investor confidence, and leads to decreased business investment, growth, job losses, and higher unemployment rates. Additionally, it results in higher production costs and price inflation. These consequences of rising inflation and unemployment generate social unrest, anxiety among people, and can lead to widespread strikes and violence against government policies. For a better understanding of economic growth, it is pertinent to analyze both foreign capital inflows and political economy on economic growth. Our review of the existing literature revealed a scarcity of research examining the impact of foreign capital inflows and political economy on different growth regimes in Pakistan. To the best of our knowledge, no empirical studies have addressed Pakistan, specifically in terms of economic growth regime shifts. Numerous studies on this type of relationship have typically assumed that the period under research is homogeneous with regard to economic growth, but in the case of Pakistan, such continuous relationships may not be useful because the country has undergone multiple different periods, which may have affected its economic progress. The structure of these different periods may also have affected FCIs in Pakistan. Kuan (2002) argues that macroeconomic variables are likely to behave differently in various periods and situations.

In a time of globalization, when countries are interdependent, and the decisions of one country may affect the economic growth and development of other countries, it is pertinent to analyze the combined effect of economic and political factors on development. It will help to formulate better policies that will affect economic growth. This study analyzes how foreign capital inflows and political economy variables affect the economic growth of Pakistan in different growth regimes, taking into account other variables such as inflation rate and government expenditure. The association among foreign capital inflows, political economy, and economic growth in Pakistan is mostly examined by making use of conventional econometric approaches such as ECM, NARDL, VECM, ARDL, and SVAR. The impact of foreign capital inflows and political economy variables on economic growth is expected to vary depending on regimes. Specifically, it has raised two main questions: (i) To what extent do FCIs affect growth under different regimes? (ii) What is the relationship between political economy and growth under different regimes? To address these research questions, our study investigates the correlation between foreign capital inflows, political economy, and economic growth by employing Markov Regime-Switching Models (MSMs), taking the quarterly data from 2000 to 2020 in Pakistan.

Economic Performance of Pakistan under Different Political Regimes

Although Pakistan is a democratic country, its political structure has been marked by periods of instability due to prolonged military dictatorships. These military dictators held control over Pakistan’s political system during the periods of 1958–1969, 1978–1988, and 2000–2008. Conversely, Pakistan has also experienced democratic eras, which can be categorized into three phases: 1970–1977, 1988–2000, and 2008 onwards, continuing until the present study.

The growth rate of GDP is important for understanding how well an economy is doing. It helps us assess the overall progress of a country’s economy. Pakistan has experienced fluctuations in growth rate since 1971, when a contraction in economic growth was observed because of political uncertainty due to shocks of war. As a consequence of the war, Pakistan lost a massive share of money as well as human resources. After that, Pakistan had a steady growth rate until the year 1988, of worthy and consistent economic strategies. After 1988, the economy again noticed a drop due to mainly a politically unstable environment, and unreliable political and economic policies. During the period from 1988 to 1998, despite many government changes, there was a basic continuity of policies. Due to the seizure of overseas accounts and implementation of sanctions resulting from nuclear testing, foreign inflows suffered a setback in 1998–1999 and 1999–2000 (Asghar and Ashfaq 2004). After 2000, notable enhancement in economic management combined with structural reforms has been observed from until 2008 (Hussain 2009). Inflation has also accelerated in this period after the SBP had raised the discount rate thrice. During 2008–2013, overall performance of Pakistan was not good. The macroeconomic statistics reveal that during 2008–2013 there was a dismally low performance of Pakistan’s economy, and, in this period, annual GDP declined to 2.9 percent (Tanoli 2016). Macroeconomic statistics indicate that Pakistan’s economy performed poorly during the period of 2008–2013, with an annual GDP decline of 2.9% (Tanoli 2016). During this, a strict monetary policy was implemented, and many other steps were made to reduce Pakistan’s budget deficits.

The era of 2008–2013 is seen as one of the poorest in terms of economic growth, and Pakistan witnessed recessionary patterns throughout these years. Poor governance, corruption, and thus, less potential to collect revenues, ignoring structural reforms, are the main reason behind the recessionary trends in these years. After 2013, when the government changed, and after tremendous days of struggle, Pakistan’s economic situation changed, and macroeconomic indicators reflect rising tendencies in this period. After a change in government in 2013, Pakistan’s economic situation improved, and macroeconomic indicators began to show positive trends, indicating a trend of growth. The status of Pakistan is set to change, and the economy of Pakistan is growing day by day in this era. The deterioration in the political system has encouraged scholars to figure out the relationship between political instability and economic progress. Several research studies have been conducted to explore the relationship between democracy and economic growth in Pakistan. However, there is a lack of empirical examination of Pakistan’s economic performance under two distinct regimes, despite experiencing three successful and three unsuccessful military coup attempts. This study aims to shed light on the impact of dictatorship/democracy on Pakistan’s economic performance from 2000 to 2020.

2. Some Snippets from Past Literature

This section provides a review of empirical investigations of the dynamics of FCIs, political economy, and economic growth in Pakistan. The important question raised by the present study, that is, “how FCIs and political economy is important for the economic growth of Pakistan?” has been discussed in the light of accessible literature.

FCIs are a major factor of national revenue in developing nations and contribute to the country’s economic growth. “FCIs affect the growth process by closing the savings-investment gap, enhancing productivity, and transmitting contemporary technologies” (Khan and Ahmed 2007). Tahir et al. (2020) used time series data from 1976 to 2018 to investigate the association between important external and Pakistani economic development. The results indicate that all types of inflows, such as Foreign Direct Investment (FDI), debt, official development assistance, and remittances, have had a significant and positive influence on economic growth in the long run.

According to previous studies, external debts are an important source of foreign capital inflow. The study carried out by Ahmad et al. (2014) explores the comparative study of the average inflow of external debts in Pakistan across democratic and non-democratic governments. He used the T-test to compare both rules to find which government took less average annual external debt. According to his study results, military governments acquired fewer external debts as compared to democratic governments. Oshota and Badejo (2015) also studied the relationship between foreign remittances and economic growth in Nigeria. They found that remittances positively impact economic growth in the long and short run, while remittances show a negative relationship with economic development in the case of Nigeria. The research on this aspect is further extended by Jawaid and Saleem (2017). They investigated the effect of remittances on the quality of democracy by using panel data from 40 years from 113 developing countries. Using SGMM dynamic panel estimator, they found that remittances promote the quality of democratic institutions in the home country. Hayat (2019) investigated the existence of distinct regimes in the influence of FDI on economic growth in Pakistan using the Markov Switching Model (MSM). They discovered that Pakistan’s economy went through two phases. While the economy in the first state did not experience any FDI-induced economic development, the economy in the second state had significant FDI-induced economic growth.

Akinlo (2020) discovered that there is a significant influence of external debt on economic growth. By using Markov Regime-Switching method, they also found that both public and private foreign debt have a considerable negative impact on economic growth throughout the contractionary and recessionary periods. These findings indicate that public external debt is inefficiently utilized in the country. Bird and Choi (2020) described the relationship between remittance inflow, foreign investment, and external aid on the growth rate of 51 developing countries by covering the period 1976–2015. The results showed that foreign investment had a significant positive influence on economic growth, whereas remittance had both positive and negative impact on economic growth. The study suggested that to achieve sustainable development, the government needs to utilize all three sources and exploit the areas in which they have a comparative advantage. The recent study has been done by Fiaz et al. (2021) on the exchange rate misalignment in Pakistan. They estimated the key determinants of the exchange rate (RER) by using the MSM technique, and the results revealed that misalignment of the RER is affected by terms of trade, net foreign assets, interest differential, government investment, and consumption decisions.

Rahman et al. (2020) used the Markov Regime-Switching vector auto-regression (MS-VAR) model with time-varying transition probabilities to determine Pakistan’s high and low growth regimes. The findings reveal that in high-growth regimes, output responds positively to positive spending shocks, but in low-growth regimes, production responds negatively. In another study was carried out by Akinlo (2020). They also used the Markov Regime-Switching method to analyze the link between foreign debt and economic growth in Nigeria from 1970 to 2016 time period. According to the findings, the connection between foreign debt and economic growth is nonlinear. They also found that both public and private foreign debt have a considerable negative impact on economic growth throughout the contractionary and recessionary periods. Malik and Nishat (2017) utilized the Markov Switching Model to evaluate the volatility of short-term real interest rates in Pakistan. The study reveals that since 1973, real interest rates in Pakistan have exhibited high volatility due to factors, such as high budget deficits and other sources of instability in the economy. Using the Markov Regime-Switching Model, Bilgili et al. (2020) empirically examined the impact of globalization on environmental quality. The results from all regime-switching models consistently indicate that the growth of economic globalization and social globalization leads to an increase in ecological footprint growth in Turkey.

In summary, these empirical studies concur on the undeniable advantages of FCIs for the host country. They largely support the hypothesis derived from the reviewed growth theory, indicating that capital inflows contribute to enhanced economic growth. However, it is noteworthy that none of the reviewed empirical studies focused exclusively on FCIs and economic growth under an MSM approach in Pakistan. Consequently, the existing research has not sufficiently distinguished between different growth regimes/states that an economy may undergo concurrently. Understanding the growth effect of FCIs within specific growth states is crucial, particularly for informing policy implications.

According to previous studies, economic growth is impossible to achieve in the face of political unrest. Political instability arises from a misalignment of economic development with political institutions. In both intellectual and political arguments, opponents of democracy argue that democracy is an ineffective system for emerging countries. According to this viewpoint, developing-country economic success necessitates a “developmental dictatorship” in which people are forced to work hard and make sacrifices (Kurzman et al. 2002). The study presented by Hayat (2019) analyzed the performance of the economy under Democracy and Dictatorship era in Pakistan from 1951 to 2014. They concluded that the economic performance of Pakistan was much better in a dictatorship than democracy regime. Another study was carried out by Qadeer and Jehan (2021), and they also investigated the type of political system that increases the growth rate of Pakistan. They conclude dictatorship governments are better for Pakistan’s economy. Their finding furthermore indicates that growth, inflation, and debts are better in military governments.

Anwar et al. (2020) explored the impact of macroeconomic factors on the economic growth of Pakistan during the democratic and dictatorship periods. They argued that major macroeconomic factors like remittances, exchange rates, and export positively affected growth in the long term. The study also reported that the nondemocratic era’s performance was not better than the democratic government in the case of Pakistan.

3. Materials and Methods

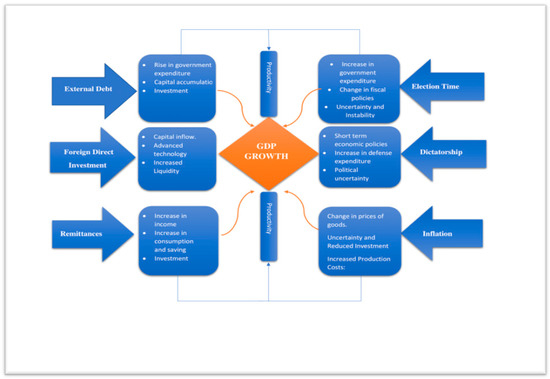

3.1. Conceptual Framework

A conceptual framework for current research is presented below (Chart 1).

Chart 1.

Transmission Mechanism of Study Variables (Source: Authors’ creation).

3.2. Data and Variables

The study and data covered the period from 2000 to 2020. The dependent variables in the study were economic growth, while the independent variables were external debt, remittances, foreign direct investment, government expenditures, inflation, dictatorship/democracy, and election time. The details regarding variables are presented in Table 1 below.

Table 1.

Description of Variables.

3.3. Preliminary Integration

3.3.1. Test of Nonlinearity

Nonlinearity exists due to changes in mean or is due to changes in variance. In both cases, the linear model is not given appropriate results. Teräsvirta (1995) suggested specifying the linear model first before moving on to the nonlinear model to ensure that the linear model is adequate for the data. As a result, he recommended using the linearity test when selecting a nonlinear model. The linearity test determines the Lagrange Multiplier (LM) statistics value and p-values of the delay parameter to check for the null hypothesis of linearity. The one with the highest statistics, which were higher than the Chi-squared distributions, and the lowest p-values, had nonlinearity attributes.

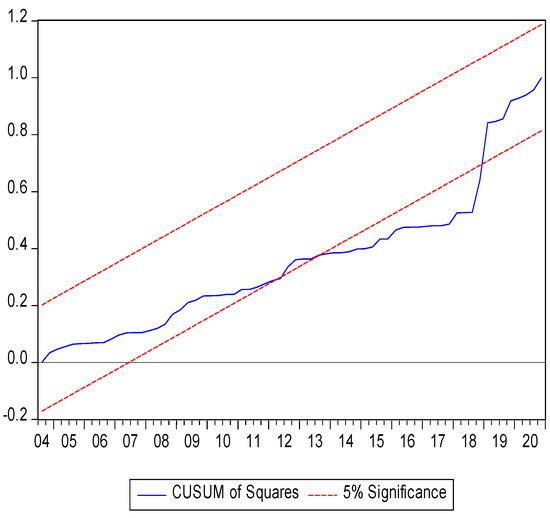

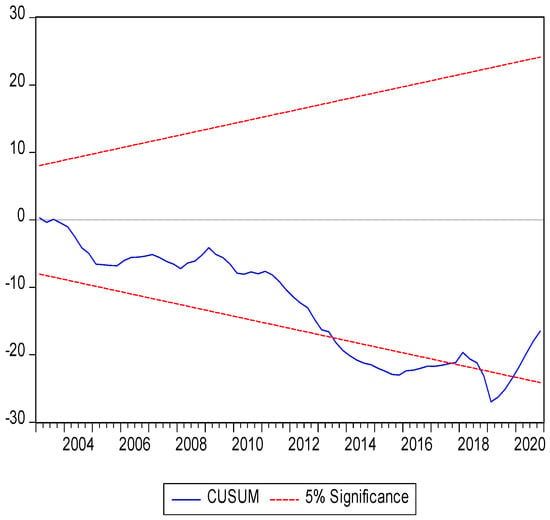

3.3.2. Structural Stability Tests

We used the cumulative sum of recursive residuals and the cumulative sum of squares of recursive residuals square stability methods to assess the MS model’s stability. Figure 1 and Figure 2 depict the Cusum Square and Cusum graphs, respectively. Because both plots remain over the crucial lines at the 5% level of significance, we conclude that the model is not stable. As a result, we must assume that the parameters are not stable since the blue line exists outside the red line, which is why we must employ the nonlinear model in our research.

Figure 1.

CUSUM of Squares.

Figure 2.

CUSUM graphs.

The Brock et al. (1995) (BDS) test was used to confirm the presence of non-linearity in an FCI and growth connection. Because the BDS test is powerful enough against switching models, it may be used as a diagnostic tool to evaluate the validity of regime-switching models for discovering nonlinear series.

The BDS test results confirmed the existence of nonlinearity between FCIs and growth. The results presented in Table 2 indicate that all variables are significant at the 1% level, so we may conclude that the MS technique is appropriate for investigating the link between FCIs and growth. Because the MS approach requires that all variables in the model be stationary, we applied the Augmented Dickey–Fuller (ADF) to determine the non-stationarity of the variables. The findings are summarized in Table 3.

Table 2.

BDS Test Result.

Table 3.

Unit Root (ADF) Test Results.

3.4. Markov Regime-Switching Technique

This current study also employs the Markov Regime-Switching Model to identify the high and low growth regimes and to examine the influence of major foreign capital inflows, such as external debt and remittances on economic growth, as well as other control variables. The use of the MSM technique was motivated by shifts in political regimes in Pakistan. Pakistan’s economy experienced many ups and downs during the last two decades. These structural changes cannot be detected via linear econometric models. The behavior of economic growth is typically dependent on economic trends, such as high- or low-growth regimes, this approach makes it easier to understand empirical data.

In this analysis, we use GDP as dependent variables while external debt and remittances FDI, government expenditure, and political economy dummies are our independent variables. The specified form of the Markov model can be written as

where is the GDP, R is the regime, denotes state-dependent switching variable, t is a trend, where is the regime-variant variables such as external debt, remittances, FDI, government expenditure, and inflation. is the residual time (error) and t is the time:

where

where Regime 1 is the high growth and Regime 2 is the low growth period and and are the probabilities remaining in Regime 1 and Regime 2, respectively, while p12 and p21 indicate the movement of probability from one regime to another. Thus,

In the Markov model, the mean and variance are expected to behave as

where = 2 refers to a high average growth regime and = 2 refers to a low average growth regime.

For a two-state Markov chain, the four transition probabilities are given as

where = 1 or 2 represents the unobserved state of the equation (Hamilton 1989). The transition probability takes the range of 1 < 1, and the transition probabilities are summed up to one.

4. Results and Discussion

4.1. Markov Switching Model Results

The Markov Switching Approach was used to analyze the influence of FCI and Political Economy on economic growth. We limit our study to two regimes due to the limited sample size and a better understanding of the relation between FCI, Political Economy, and economic growth. We have developed three models for analysis to have a better understanding. In Model 1, the influence of FCI on economic development was examined without regard to election timing. In Model 1 of our analysis, we investigated the relationship between foreign capital inflows and economic development in Pakistan without taking into account the influence of election timing. FCI Impact was examined in Model 2 in the absence of the influence of Democracy/Dictatorship. In Model 3, we ignored the effect of political economy, focusing solely on the FCI’s impact on economic growth. The findings of three different Markov Switching Models, identified by Model 1, Model 2, and Model 3, are presented in Table 4 below.

Table 4.

Markov Regime-Switching Results.

As we observed in the first model, Regime 1 is considered a high-growth period. For instance, Regime 1 has the highest value of the mean (µ = 7.656) with the lowest value of volatility (σ = 0.79), and Regime 2 corresponds to a period of low growth where the estimated value of the intercept coefficient is 6.0293 with high variance of 0.593. Furthermore, in models 1 and 2, Regime 1 has the highest intercept coefficient (µ = 7.310 and µ = 7.02) with the lowest volatility (σ = −1.039 and σ = −0.79), and Regime 2 has the coefficient value coefficient, i.e., µ = 4.29 and µ = 6.02 in the case of models 2 and 3. We also observed that despite having a low mean value, Regime 2 has a relatively high value of variance, i.e., σ = 1.122 and σ = 1.05, respectively. Thus, the result indicates that all three models’ second periods correspond to low growth with high volatility, and period 1 corresponds to high growth with low volatility. Therefore, it can be assumed that the low-growth regime is more volatile than the high-growth regime in our sample period.

In Model 1, we examine the impact of FCI along with dictatorship on economic growth. Dictatorship appears to have a positive substantial effect on economic development in both regimes of Model 1. Our findings are consistent with the conclusions of Qadir et al. (2016), who indicated that non-democratic regimes have been better for Pakistan’s economic development, with significantly noteworthy results in terms of main macroeconomic metrics such as GDP growth, CPI inflation, and FDI. Hayat (2019) agree with our findings, arguing that economic performance under military dictatorships is superior to democratic republic regimes because democratic governments are extremely dependent on the IMF and World Bank, and non-payment of loans hurts economic stability. Furthermore, election seasons have a positive impact on economic development during expansionary periods. During a contractionary growth period, the coefficient election time hurts economic growth. The favorable findings support the concept that electoral pressures encourage high levels of government spending to allure voters and increase the likelihood of winning the next elections (James and Oneal 1991).

In Model 2, when we incorporate the second political economy dummy variable, namely election periods, the impacts of this variable on economic growth are different in both regimes of Model 2, where election time has a significant beneficial influence on economic growth in the expansion periods, while in the contraction era of growth, the coefficient election time reveals a negative influence on economic growth. The positive results support the argument that electoral pressures promote high levels of government expenditure to entice voters and enhance the chance of winning upcoming elections (Payne 1991). On the other hand, the observations of the adverse effects of elections in the downturn period are consistent with the findings of (Alesina and Perotti 1996), who argued that political instability creates problems for government policies, which can frustrate existing as well as new potential investors to increase their investment in the economy. They would prefer to invest their capital after this period has passed. In consequence, election time hampers economic growth. Several additional studies have similarly demonstrated the adverse impact of political instability on economic development (Tabassam et al. 2016).

On the other hand, when there is no political uncertainty in the economy and the economy is stable, then FDI positively affects economic growth, as demonstrated in the findings of Model 3. Two implications may be taken from this finding: First, when there is political uncertainty in the economy then FDI seems to have a negative influence on growth, a conclusion like that of Asaad and Mustafa (2020). Second, when the economy is stable and there is no political uncertainty in the economy, then FDI tends to have a favorable influence on growth in Regime 1 and Regime 2. This observation is in accordance with the findings of (Almfraji and Almsafir 2014; Koojaroenprasit 2012). However, the fact that FDI has varying impacts on development under various regimes in Pakistan suggests that the status of economic growth has a major influence on the inflows.

Remittances influence positively in all three models except the low growth period of Model 2. This indicates that there is a negative influence of remittances on in contraction phase of economic growth when there is an election period. In all three models, foreign debt was found to have a negative and considerable impact on both the recession and expansion phases of economic growth. This illustrates that external debt is a significant obstacle to economic progress since it discourages private investment, a source of economic activity producing growth in the economy. Our result is similar to the results of Sajjad and Khan (2018) and Hassan and Meyer (2021).

Fiscal and monetary policies evaluated in this research by government spending and inflation also have a major influence on growth in Pakistan. Fiscal policy, assessed by government consumption expenditure, is positively significant in all three models. Although a strong fiscal policy is vital to a country’s progress, economic theories imply that larger government spending might impede growth, particularly in emerging countries (Fry 1997). The positive coefficient of government spending in all regimes shows that no matter whether the economy is in a sustainable or depressed growth regime, government intervention via fiscal policy might have a positive influence on growth. In the literature, precisely opposite outcomes might also be observed. Davar (2013) conclude in their research that government spending influences growth negatively, while Musa and Asare (2013) and Muhammad et al. (2015) believe that there is a positive association between government spending and growth. On the other hand, there is a negative effect of inflation in a politically stable time of high growth regime, as revealed in Model 3, which confirms the findings of Hussain and Malik (2011), who conclude that high growth may also increase inflation. Economic literature believes that monetary policy instruments of inflation are a measure of the overall macroeconomic stability of a nation (Mishkin 2000). Higher inflation rates, for instance, might indicate hurdles to growth in a nation.

4.2. Transition Probabilities

The transitional probabilities of shifting from State 1 to State 2 of all three models are determined and reported in Table 5 below.

Table 5.

Transitional Probabilities.

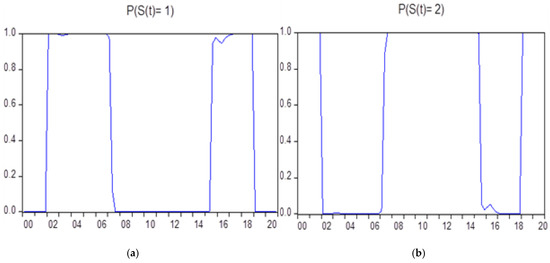

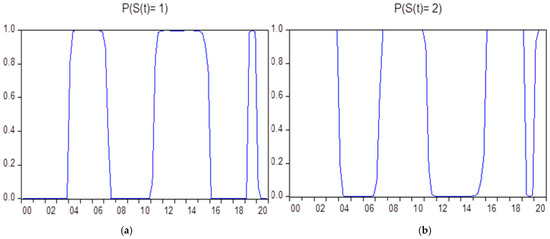

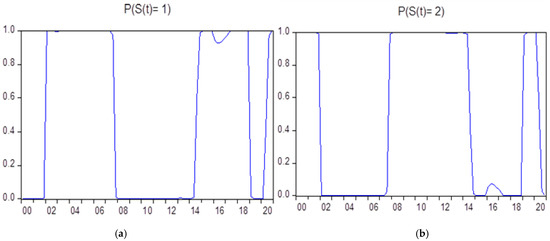

It may also be required to examine overtime (between regimes) and smoothed probabilities throughout the transition phase. Figure 3, Figure 4 and Figure 5 indicate the smoothed probability of Regime 1 and Regime 2 for the three different models. The behavior of smoothed probabilities also confirms that smoothed probabilities are persistent in both regimes.

Figure 3.

(a,b) Smoothed probabilities of Model 1.

Figure 4.

(a,b) Smoothed probabilities of Model 2.

Figure 5.

(a,b) Smoothed probabilities of Model 3.

4.3. Markov Switching Smooth Regime Probabilities

It may also be required to examine overtime (between regimes), smoothed probabilities throughout the transition phase. Figure 3a,b, Figure 4a,b and Figure 5a,b indicate the smoothed probability of Regime 1 and Regime 2 for the three different models. The figures below illustrate the smoothed probability of Regime 1 and Regime 2 of the three different models. In Figure 3a, Regime 1 points are 2001q4–2007q1 and 2014q2–2018q1. Regime 2 points in Figure 3b cover the periods of 2002–2006q2 and 2015–2018. In Figure 3a,b, the Regime 1 points for Model 2 include the years 2004–2006, 2010q1–2015q1 and 2018q1–2019q2. The Regime 1 points for Model 2 include the period 2004–2006, 2011q1–2014q4 and 2018q2–2019q1 (Figure 4a,b). In Figure 3a,b, Regime 1 point covers the years 2002–2007, 2014–2018 and 2019q1–2020q1. However, Regime 2 points correspond to 2001q1–2006q4, 2014–2018 and 2019q2–2020q1.

5. Conclusions and Policy Recommendations

The study aimed to examine various issues concerning FCIs, political economy, and economic growth in Pakistan. It used a quarterly time series dataset to forecast economic development in Pakistan from 2000 to 2020. The two-stage Markov Regime-Switching Model was used in this study. The analysis indicated the presence of two distinct growth regimes. However, the transitions between these regimes were characterized as sudden and sporadic, particularly during the period from 2000 to 2020.

After understanding and analyzing the nature of the economy, the next step was to examine the behavior of FCIs, political economy and other macroeconomic variables under the various growth regimes. For this objective, we measured political instability by means of two proxies: Government type (democracy/dictatorship) and election year. Our data shows that the dictatorship era led to a significant increase in GDP under both regimes. This can be attributed to the tremendous improvements that took place under military regimes, leading to historical growth rates in the economy. Additionally, dictatorship eras are often characterized by the absence of issues, such as candidate horse trading, bribery, unlawful obligations, and other forms of corruption typically associated with democracy. Furthermore, throughout the country’s dictatorship era, a negative relationship was discovered between foreign debt and economic growth in both regimes. This illustrates that external debt is a significant obstacle to economic progress since it discourages private investment, a source of economic activity producing growth in the economy. This finding also suggests that external debt is inefficiently utilized in both the democracy and dictatorship periods in Pakistan. Election periods, on the other hand, have different effects on GDP growth under the two regimes. Elections time impact growth positively in the high-growth regime, while in low growth regime, election time hurt growth in the low-growth regime. Following the identification and assessment of the characteristics of the economy when the country is politically unstable, the next stage was to analyze the behavior of foreign capital inflows and other macroeconomic indicators under different growth regimes. External debt is inversely proportionate to growth in both states when political stability exists, yet remittances contribute positively to growth in both regimes. However, when there is uncertainty in the economy due to election periods, FDI has a negative impact on the growth period. On the other hand, in stable economic conditions with no political uncertainty, FDI has a positive effect on economic growth, as indicated by the findings of Model 1 and 3. This highlights the significant influence of local conditions on the relationship between FDI and economic performance. In Models 2 and 3, government expenditure positively contributes to economic growth, while inflation has a negative influence on economic growth. According to the conclusions based on regime smoothing likelihood and regime categorization, a high-growth regime was generally untenable in Pakistan from 2000 to 2020.

Research findings confirm the substantial debt load in Pakistan, which affect growth badly, authorities should make sure that the debt burden is monitored by an efficient debt management strategy in Pakistan. The government should prioritize the effective utilization of external loans in development projects and infrastructure that offer promising returns on investment while also taking steps to eliminate unproductive and redundant projects. It is essential for the government to develop clear criteria for the selection of projects that align with development priorities and promote sustainability. To hasten infrastructural expansion, the government should first endeavor to achieve economic growth.

To enact our future growth, it is important and relevant to boost the remittances and FDI to boost growth and rely less on external debts, legislators should encourage and facilitate to the extent possible the undisrupted flow of FDI and remittances, as they contribute to stable financial and economic development in Pakistan. In order to enhance economic growth through foreign capital inflows, policymakers should focus on substituting external debt with foreign direct investment and remittances in sectors where external debt has a positive impact. By strategically reallocating these inflows, the country can reduce its debt burden and ultimately benefit its economy. From a policy standpoint, the government should provide a favorable climate, enough security, and effective fiscal and monetary policy to entice investors to invest in Pakistan.

Author Contributions

Conceptualization: N.K. and H.S.; Methodology: N.K. and A.F.; software: M.I.T., B.H., N.K., A.F., B.H. and M.I.T.; Validation: M.I.T. and F.M.; Formal analysis: N.K.; Resources: N.K. and M.I.T.; Data Curation: H.S. and A.F.; Writing—original draft preparation: N.K. and H.S.; Review and Editing: M.I.T., B.H. and F.M.; Project Administration: N.K. and A.F.; Supervision: N.K. and B.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data will be provided on request.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Agenor, Pierre, and Peter Montiel. 1999. Macroeconomics Development. Princeton: Princeton University Press. [Google Scholar]

- Ahmad, Nawaz, Rizwan Ahmed, Imamuddin Khoso, Rana Palwishah, and Unaib Raza. 2014. Impact of exchange rate on balance of payment: An investigation from Pakistan. Research Journal of Finance and Accounting 5: 32–42. [Google Scholar]

- Akinlo, Anthony Enisan. 2020. Impact of External Debt on Economic Growth: A Markov Regime–Switching Approach. Journal of Applied Financial Econometrics 1: 123–43. [Google Scholar]

- Alesina, Alberto, and Roberto Perotti. 1996. Income distribution, political instability, and investment. European Economic Review 40: 1203–28. [Google Scholar] [CrossRef]

- Ali, Afshan, and Sabeen Saif. 2017. Determinants of economic growth in Pakistan: A time series analysis. European Online Journal of Natural and Social Sciences 6: 686. [Google Scholar]

- Almfraji, Mohammad Amin, and Mahmoud Khalid Almsafir. 2014. Foreign direct investment and economic growth literature review from 1994 to 2012. Procedia-Social and Behavioral Sciences 129: 206–13. [Google Scholar] [CrossRef]

- Anwar, M. Masood, Aftab Anwar, and Ghulam Yahya Khan. 2020. Inclusive Growth Measurement Under Different Political Regimes of Pakistan. Global Social Sciences Review 5: 42–49. [Google Scholar] [CrossRef]

- Asaad, Zeravan, and Hazheen Mustafa. 2020. The impact of FDI Inflows on GDP Growth in Iraq for the period (2004–2017): An applied study. Tanmiyat Al-Rafidain 39: 56–86. [Google Scholar] [CrossRef]

- Asghar, Ashfaq, and A. Ashfaq. 2004. Remittances not very productively employed. Daily Dawn, September 13. [Google Scholar]

- Asteriou, Dimitrios, and Simon Price. 2001. Political instability and economic growth: UK time series evidence. Scottish Journal of Political Economy 48: 383–99. [Google Scholar] [CrossRef]

- Barajas, Adolfo, Ralph Chami, Connel Fullenkamp, Michael Gapen, and Peter J. Montiel. 2009. Do Workers’ Remittances Promote Economic Growth? Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1442255 (accessed on 20 February 2022).

- Bilgili, Faik, Recep Ulucak, Emrah Koçak, and Salih Çağrı İlkay. 2020. Does globalization matter for environmental sustainability? Empirical investigation for Turkey by Markov regime switching models. Environmental Science and Pollution Research 27: 1087–100. [Google Scholar] [CrossRef]

- Bird, Graham, and Yongseok Choi. 2020. The effects of remittances, foreign direct investment, and foreign aid on economic growth: An empirical analysis. Review of Development Economics 24: 1–30. [Google Scholar] [CrossRef]

- Brock, William, Blake Lebaron, and Jose Scheinkman. 1995. A Test for Independence Based on the Correlation Dimension. Working Paper. Madison: University of Wisconsin at Madison, Department of Economics. [Google Scholar]

- Calvo, Guillermo A., Leonardo Leiderman, and Carmen M. Reinhart. 1996. Inflows of Capital to Developing Countries in the 1990s. Journal of Economic Perspectives 10: 123–39. [Google Scholar] [CrossRef]

- Chuhan, Punam, Stijn Claessens, and Nlandu Mamingi. 1998. Equity and bond flows to Latin America and Asia: The role of global and country factors. Journal of Development Economics 55: 439–63. [Google Scholar] [CrossRef]

- Davar, Ezra. 2013. Government Spending and Economic Growth. The Finance and Business 2: 4–19. [Google Scholar]

- Fiaz, Asma, Nabila Khurshid, Ahsan Satti, and Muhammad Shuaib Malik. 2021. Real exchange rate misalignment in Pakistan: An application of regime switching model. The Journal of Asian Finance, Economics and Business 8: 63–73. [Google Scholar]

- Fry, Maxwell J. 1997. In favour of financial liberalisation. The Economic Journal 107: 754–70. [Google Scholar] [CrossRef]

- Haddad, Mona, and Ann Harrison. 1993. Are there positive spillovers from direct foreign investment?: Evidence from panel data for Morocco. Journal of Development Economics 42: 51–74. [Google Scholar] [CrossRef]

- Hamilton, James D. 1989. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica: Journal of the Econometric Society 57: 357–84. [Google Scholar] [CrossRef]

- Haq, Mirajul, and Muhammad Luqman. 2014. The contribution of international trade to economic growth through human capital accumulation: Evidence from nine Asian countries. Cogent Economics & Finance 2: 947000. [Google Scholar]

- Hassan, Adewale, and Daniel Meyer. 2021. Exploring the channels of transmission between external debt and economic growth: Evidence from Sub-Saharan African countries. Economies 9: 50. [Google Scholar] [CrossRef]

- Hayat, Arshad. 2019. Foreign direct investments, institutional quality, and economic growth. The Journal of International Trade & Economic Development 28: 561–79. [Google Scholar]

- Hussain, Karrar. 2019. Monetary Policy Channels of Pakistan and Their Impact on Real GDP and Inflation. CID Research Fellow and Graduate Student Working Paper Series; Cambridge, MA: Center for International Development at Harvard University. [Google Scholar]

- Hussain, Shahzad, and Shahnawaz Malik. 2011. Inflation and economic growth: Evidence from Pakistan. International Journal of Economics and Finance 3: 262–76. [Google Scholar] [CrossRef]

- Irshad, Hira. 2017. Relationship among political instability, stock market returns and stock market volatility. Studies in Business and Economics 12: 70–99. [Google Scholar] [CrossRef]

- James, Patrick, and John R. Oneal. 1991. The influence of domestic and international politics on the president’s use of force. Journal of Conflict Resolution 35: 307–32. [Google Scholar] [CrossRef]

- Javid, Muhammad, Umaima Arif, and Abdul Qayyum. 2012. Impact of remittances on economic growth and poverty. Academic Research International 2: 433. [Google Scholar]

- Jawaid, Syed Tehseen, and Shaikh Muhammad Saleem. 2017. Foreign capital inflows and economic growth of Pakistan. Journal of Transnational Management 22: 121–49. [Google Scholar] [CrossRef]

- Khan, Muhammad Arshad, and Ayaz Ahmed. 2007. Foreign aid—Blessing or curse: Evidence from Pakistan. The Pakistan Development Review 46: 215–40. [Google Scholar] [CrossRef]

- Khan, Muhammad Arshad, Atif Ali Jaffri, Faisal Abbas, and Azad Haider. 2017. Does Trade Liberalization Improve Trade Balance in Pakistan? South Asia Economic Journal 18: 158–83. [Google Scholar] [CrossRef]

- Kharusi, Sami Al, and Mbah Stella Ada. 2018. External debt and economic growth: The case of emerging economy. Journal of Economic Integration 33: 1141–57. [Google Scholar] [CrossRef]

- Koojaroenprasit, Sauwaluck. 2012. The impact of foreign direct investment on economic growth: A case study of South Korea. International Journal of Business and Social Science 3: 8–19. [Google Scholar]

- Kuan, Chung-Ming. 2002. Lecture on the Markov switching model. Institute of Economics Academia Sinica 8: 1–30. [Google Scholar]

- Kurzman, Charles, Regina Werum, and Ross E. Burkhart. 2002. Democracy’s effect on economic growth: A pooled time-series analysis 1951–80. Studies in Comparative International Development 37: 3–33. [Google Scholar] [CrossRef]

- Malik, Fahad Javed, and Mohammed Nishat. 2017. Real interest rate volatility in the Pakistani economy: A regime switching approach. IBA Business Review 12: 22–32. [Google Scholar] [CrossRef]

- Markusen, James, and Anthony Venable. 1999. Foreign direct investment as a catalyst for industrial development. European Economic Review 43: 335–56. [Google Scholar] [CrossRef]

- MengYun, Wu, Muhammad Imran, Muhammad Zakaria, Zhang Linrong, Muhammad Umer Farooq, and Shah Khalid Muhammad. 2018. Impact of terrorism and political instability on equity premium: Evidence from Pakistan. Physica A: Statistical Mechanics and its Applications 492: 1753–62. [Google Scholar] [CrossRef]

- Mishkin, Frederic S. 2000. Inflation targeting in emerging-market countries. American Economic Review 90: 105–9. [Google Scholar] [CrossRef]

- Mohey-ud-Din, Ghulam. 2007. Impact of Foreign Capital Inflows (FCI) on Economic Growth in Pakistan [1975–2004]. Journal of Independent Studies and Research (JISR) 5: 24–29. [Google Scholar]

- Muhammad, Faqeer, Tongsheng Xu, and Rehmat Karim. 2015. Impact of expenditure on economic growth in Pakistan. International Journal of Academic Research in Business and Social Sciences 5: 231–36. [Google Scholar] [CrossRef]

- Musa, Yakubu, and B. K. Asare. 2013. Long and short run relationship analysis of monetary and fiscal policy on economic growth in Nigeria: A VEC model approach. Research Journal of Applied Sciences, Engineering and Technology 5: 3044–51. [Google Scholar] [CrossRef]

- Orozco, Manuel. 2002. Globalization and migration: The impact of family remittances in Latin America. Latin American Politics and Society 44: 41–66. [Google Scholar] [CrossRef]

- Oshota, Sebil O., and Abdulazeez A. Badejo. 2015. Impact of remittances on economic growth in Nigeria: Further evidence. Economics Bulletin 35: 247–58. [Google Scholar]

- Payne, James L. 1991. Elections and government spending. Public Choice 70: 71–82. [Google Scholar] [CrossRef]

- Qadeer, Samia, and Zainab Jehan. 2021. Democracy and Human Development in Developing Countries: Role of Globalization. FJWU (Economics) Working Paper Series 1: 49. [Google Scholar]

- Qadir, Shakeel, Muhammad Tariq, and Muhammad Waqas. 2016. Democracy or military dictatorship: A choice of governance for the economic growth of Pakistan. IBT Journal of Business Studies (JBS) 12: 39–51. [Google Scholar] [CrossRef]

- Rahman, Abdul, Muhammad Arshad Khan, and Lanouar Charfeddine. 2020. Financial development–economic growth nexus in Pakistan: New evidence from the Markov switching model. Cogent Economics & Finance 8: 1716446. [Google Scholar]

- Reinhart, Carmen, and Guillermo Calvo. 2000. When capital inflows come to a sudden stop: Consequences and policy options. In Reforming the International Monetary and Financial System. Washington: International Monetary Fund, pp. 175–201. [Google Scholar]

- Sajjad, Irum, and Muhammad Azam Khan. 2018. Investigating the impact of external debt on economic growth: A case study of Pakistan. Journal of Business & Tourism 4: 41–51. [Google Scholar]

- Tabassam, Aftab Hussain, Shujahat Haider Hashmi, and Faiz Ur Rehman. 2016. Nexus between political instability and economic growth in Pakistan. Procedia-Social and Behavioral Sciences 230: 325–34. [Google Scholar] [CrossRef]

- Tahir, Muhammad, Ahmad Ali Jan, Syed Quaid Ali Shah, Md Badrul Alam, Muhammad Asim Afridi, Yasir Bin Tariq, and Malik Fahim Bashir. 2020. Foreign inflows and economic growth in Pakistan: Some new insights. Journal of Chinese Economic and Foreign Trade Studies 13: 97–113. [Google Scholar] [CrossRef]

- Tanoli, Junaid Roshan. 2016. Comparative Analysis of Gwadar and Chabahar: The Two Rival Ports. Islamabad: Center for Strategic and Contemporary Research. [Google Scholar]

- Taylor, Edward J. 1999. The new economics of labour migration and the role of remittances in the migration process. International Migration 37: 63–88. [Google Scholar] [CrossRef]

- Teräsvirta, Timo. 1995. Modelling nonlinearity in US gross national product 1889–987. Empirical Economics 20: 577–97. [Google Scholar] [CrossRef]

- Yang, Dean, and HwaJung Choi. 2007. Are remittances insurance? Evidence from rainfall shocks in the Philippines. The World Bank Economic Review 21: 219–48. [Google Scholar] [CrossRef]

- Yasmin, Bushra. 2005. Foreign capital inflows and growth in Pakistan: A simultaneous equation model. South Asia Economic Journal 6: 207–19. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).