The Impact of Non-Economic Factors on Voluntary Tax Compliance Behavior: A Case Study of Small and Medium Enterprises in Vietnam

Abstract

:1. Introduction

2. Literature Review

3. Research Hypothesis and Model

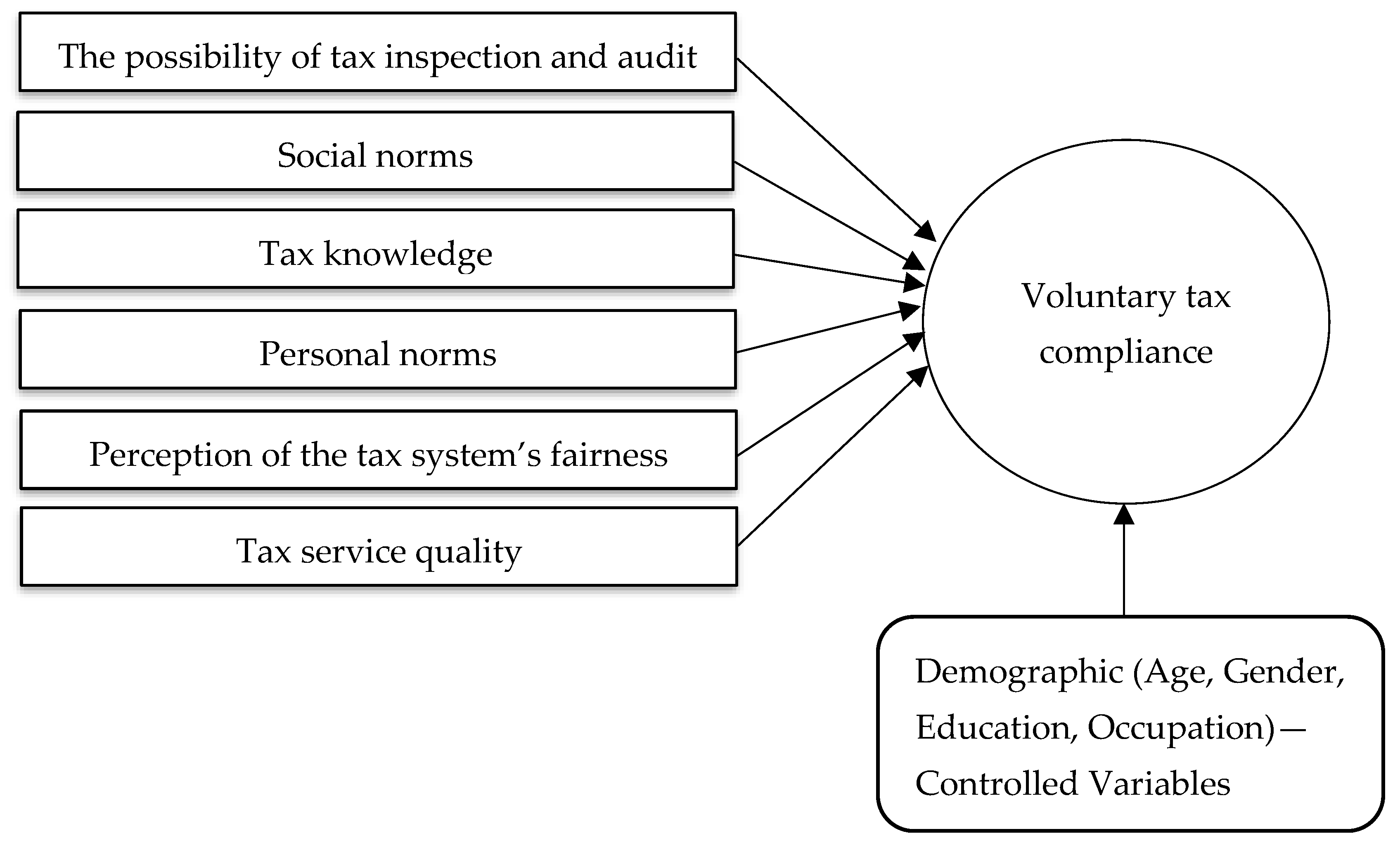

3.1. The Possibility of Tax Inspection and Audit

3.2. Social Norms

3.3. Tax Knowledge

3.4. Personal Norms

3.5. Perception of the Tax System’s Fairness

3.6. Tax Service Quality

3.7. Demographic

3.8. Research Models

- α: Constant term

- βi: Coefficients of the independent variables

- εi: Residual

4. Research Methodology

4.1. Sampling Method

4.2. Data Collection Methods

4.3. Data Analysis Methods

5. Research Results

5.1. Cronbach’s Alpha Test

5.2. Exploratory Factor Analysis (EFA)

5.3. Linear Regression Analysis

5.3.1. Pearson’s Correlation Test

5.3.2. Test the Research Hypotheses

6. Discussion

6.1. The Possibility of Tax Inspection and Audit

6.2. Tax Knowledge

6.3. Social Norms

6.4. Perception of the Tax System’s Fairness

6.5. Personal Norms

6.6. Tax Service Quality

7. Conclusions and Recommendations

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Alabede, James O., Zaimah Zainol Ariffin, and Kamil Md Idris. 2011. Individual taxpayers’ attitude and compliance behaviour in Nigeria: The moderating role of financial condition and risk preference. Journal of Accounting and Taxation 3: 91–104. [Google Scholar]

- Allingham, Michael G., and Agnar Sandmo. 1972. Income tax evasion: A theoretical analysis. Journal of Public Economics 1: 323–38. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Benno Torgler. 2006. Culture differences and tax morale in the United States and in Europe. Journal of Economic Psychology 27: 224–46. [Google Scholar] [CrossRef] [Green Version]

- Alm, James, and Michael McKee. 1998. Extending the lessons of laboratory experiments on tax compliance to managerial and decision economics. Managerial and Decision Economics 19: 259–75. [Google Scholar] [CrossRef]

- Alm, James, Roy Bahl, and Matthew N. Murray. 1991. Tax base erosion in developing countries. Economic Development and Cultural Change 39: 849–72. [Google Scholar] [CrossRef]

- Amina, Ahmed, and Kedir Saniya. 2015. Tax compliance and its determinants: The case of Jimma zone, Ethiopia. International Journal of Research in Social Sciences 6: 7–21. [Google Scholar]

- Anderson, James C., and David W. Gerbing. 1988. Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin 103: 411–23. [Google Scholar] [CrossRef]

- Andreoni, James, Brian Erard, and Jonathan Feinstein. 1998. Tax compliance. Journal of Economic Literature 36: 818–60. [Google Scholar]

- Battiston, Pietro, and Simona Gamba. 2013. Is tax compliance a social norm? A field experiment. SSRN Electronic Journal 249: 1–28. [Google Scholar] [CrossRef] [Green Version]

- Battiston, Pietro, and Simona Gamba. 2016. The impact of social pressure on tax compliance: A field experiment. International Review of Law and Economics 46: 78–85. [Google Scholar] [CrossRef]

- Becker, Gary S. 1968. Crime and punishment: An economic approach. Journal of Political Economy 76: 169–217. [Google Scholar] [CrossRef] [Green Version]

- Benk, Serkan, Ahmet Ferda Cakmak, and Tamer Budak. 2011. An investigation of tax compliance intention: A Theory of planned behavior approach. European Journal of Economics, Finance and Administrative Sciences 28: 180–88. [Google Scholar]

- Bobek, Donna D., Richard C. Hatfield, and Kristin Wentzel. 2007. An investigation of why taxpayers prefer refunds: A Theory of planned behavior approach. The Journal of the American Taxation Association 29: 93–111. [Google Scholar] [CrossRef]

- Chan, Chris W., Coleen S. Troutman, and David O’Bryan. 2000. An expanded model of taxpayer compliance: Empirical evidence from the United States and Hong Kong. Journal of International Accounting, Auditing and Taxation 9: 83–103. [Google Scholar] [CrossRef]

- Chung, Janne, and Vaswanath Umashanker Trivedi. 2003. The effect of friendly persuasion and gender on tax compliance behavior. Journal of Business Ethics 47: 133–45. [Google Scholar] [CrossRef]

- Cummings, Ronald G., Jorge Martinez-Vazquez, Michael McKee, and Benno Torgler. 2009. Tax morale affects tax compliance: Evidence from surveys and an art factual field experiment. Journal of Economic Behavior & Organization 70: 447–57. [Google Scholar] [CrossRef] [Green Version]

- Doerrenberg, Philipp, and Andreas Peichl. 2018. Tax Morale and the Role of Social Norms and Reciprocity: Evidence from a Randomized Survey Experiment. CESifo Working Paper Series No. 7149; Munich: Munich Society for the Promotion of Economic Research—CESifo GmbH, 40p. [Google Scholar]

- Eriksen, Knut, and Lars Fallan. 1996. Tax knowledge and attitudes towards taxation; A report on a quasi-experiment. Journal of Economic Psychology 17: 387–402. [Google Scholar] [CrossRef]

- Fischer, Carol M., Martha Wartick, and Melvin M. Mark. 1992. Detection probability and taxpayer compliance: A review of the literature. Journal of Accounting Literature 11: 1–46. [Google Scholar]

- Frey, Bruno S. 1997. Not Just for the Money. Cheltenham and Brookfield: Edward Elgar Publishing. [Google Scholar]

- Gangl, Katharina, Stephan Muehlbacher, Manon de Groot, Sjoerd Goslinga, Eva Hofmann, Christoph Kogler, Gerrit Antonides, and Erich Kirchler. 2013. “How can I help you?” Perceived service orientation of tax authorities and tax compliance. FinanzArchiv: Public Finance Analysis 69: 487–510. [Google Scholar] [CrossRef]

- Government. 2021. Decree No. 80/2021/ND-CP Dated 26 August 2021 on Elaboration of Some Articles of the Law on Provision of Assistance for Small and Medium Enterprises. Available online: https://vanbanphapluat.co/decree-80-2021-nd-cp-elaboration-law-on-provision-of-assistance-for-small-and-medium-enterprises (accessed on 30 November 2021).

- Hair, Joseph F., Rolph E. Anderson, Ronald L. Tatham, and William C. Black. 1998. Multivariate Data Analysis, 5th ed. Englewood Cliffs: Prentice-Hall International, Inc. [Google Scholar]

- Hamm, Jeffrey Lloyd. 1995. Income Level and Tax Rate as Determinants of Taxpayer Compliance: An Experiment Examination. Unpublished Doctoral dissertation, Texas Tech University, Lubbock, TX, USA. [Google Scholar]

- Hasseldine, John, and Peggy A. Hite. 2003. Framing, gender and tax compliance. Journal of Economic Psychology 24: 517–33. [Google Scholar] [CrossRef]

- Hidayat, N. Rusdi, Darminto Suhadak, Ragil Handayani Siti, and Widjanarko Otok Bambang. 2014. Measurement model of service quality, regional tax regulations, taxpayer satisfaction level, behavior and compliance using confirmatory factor analysis. World Applied Sciences Journal 29: 56–61. [Google Scholar]

- Hoang, Trong, and Chu Nguyen Mong Ngoc. 2008. Analyzing Researched Data with SPSS, 2nd ed. Ho Chi Minh City: Hong Duc Publishing House. [Google Scholar]

- Inasius, Fany. 2015. Tax compliance of small and medium enterprises: Evidence from Indonesia. Accounting & Taxation 7: 67–73. [Google Scholar]

- Inasius, Fany. 2018. Factors influencing SME tax compliance: Evidence from Indonesia. International Journal of Public Administration 42: 367–79. [Google Scholar] [CrossRef]

- Jackson, Betty R., and Pauline R. Jaouen. 1989. Influencing taxpayer compliance through sanction threat or appeals to conscience. Advances in Taxation 2: 131–47. [Google Scholar]

- Jackson, Betty R., and Valerie C. Milliron. 1986. Tax compliance research: Findings, problems, and prospects. Journal of Accounting Literature 5: 125–65. [Google Scholar]

- James, Simon, and Clinton Alley. 1999. Tax compliance, self-assessment, and tax administration in New Zealand: Is the carrot or the stick more appropriate to encourage compliance? New Zealand Journal of Taxation Law and Policy 5: 3–14. [Google Scholar]

- Kastlunger, Barbara, Edoardo Lozza, Erich Kirchler, and Alfred Schabmann. 2013. Powerful authorities and trusting citizens: The slippery slope framework and tax compliance in Italy. Journal of Economic Psychology 34: 36–45. [Google Scholar] [CrossRef]

- Kim, Ho-Sung, and Hyun-Ah Lee. 2020. Associations among procedural fairness, tax compliance, and tax re-audits. Journal of Asian Finance, Economics and Business 7: 187–98. [Google Scholar] [CrossRef]

- Kirchler, Erich. 2007. The Economic Psychology of Tax Behaviour. Cambridge: Cambridge University Press. [Google Scholar] [CrossRef]

- Kirchler, Erich, and Ingrid Wahl. 2010. Tax compliance inventory TAX-I: Designing an inventory for surveys of tax compliance. Journal of Economic Psychology 31: 331–46. [Google Scholar] [CrossRef] [Green Version]

- Kirchler, Erich, Erik Hoelzl, and Ingrid Wahl. 2008. Enforced versus voluntary tax compliance: The “slippery slope” framework. Journal of Economic Psychology 29: 210–25. [Google Scholar] [CrossRef]

- Lewis, Alan. 1982. The Psychology of Taxation. Oxford: Martin Robertson. [Google Scholar]

- Liu, Xin. 2014. Use Tax Compliance: The Role of Norms, Audit Probability, and Sanction Severity. Academy of Accounting and Financial Studies Journal 18: 65–80. [Google Scholar]

- Luttmer, Erzo F. P., and Monica Singhal. 2014. Tax morale. Journal of Economic Perspectives 28: 149–68. [Google Scholar] [CrossRef] [Green Version]

- Lymer, Andrew, and Lynne Oats. 2009. Taxation: Policy and Practice 16th Edition 2009/10. Birmingham: Fiscal Publications. [Google Scholar]

- Muehlbacher, Stephan, and Erich Kirchler. 2010. Tax Compliance by Trust and Power of Authorities. International Economic Journal 24: 607–10. [Google Scholar] [CrossRef]

- Nguyen, Dinh Tho. 2011. Methods of Scientific Research in Business. Hanoi: Labor and Social Publishing House. [Google Scholar]

- Obid, Siti Normala Bt. Sheikh, and Mustapha Bojuwon. 2014. Reengineering Tax Service Quality Using a Second Order Confirmatory Factor Analysis for SelfEmployed Taxpayers. International Journal of Trade, Economics and Finance 5: 429–34. [Google Scholar] [CrossRef] [Green Version]

- Rawlings, Gregory. 2003. Cultural narratives of taxation and citizenship: Fairness, groups and globalisation. Australian Journal of Social Issues 38: 269–306. [Google Scholar] [CrossRef]

- Richardson, Grant. 2006. Determinants of tax evasion: A cross-country investigation. Journal of International Accounting, Auditing and Taxation 15: 150–69. [Google Scholar] [CrossRef]

- Sam, Hoang. 2021. Small and Medium Enterprise Conference with EVFTA Agreement. Available online: https://varisme.org.vn/hoi-nghi-doanh-nghiep-nho-va-vua-voi-hiep-dinh-evfta-n221.html (accessed on 15 January 2022).

- Singh, Veerinderjeet, and Renuka Bhupalan. 2001. The malaysian self assessment system of taxation: Issues and challenges. Tax National 3: 12–17. [Google Scholar]

- Song, dahl Song, and Tinsley E. Yarbrough. 1978. Tax ethics and taxpayer attitudes: A survey. Public Administration Review 38: 442–52. [Google Scholar] [CrossRef]

- Tabachnick, Barbara G., and Linda S. Fidell. 2007. Using Multivariate Statistics, 5th ed. Boston: Allyn and Bacon. [Google Scholar]

- Taing, Heang Boong, and Yongjin Chang. 2020. Determinants of tax compliance intention: Focus on the theory of planned behavior. International Journal of Public Administration 44: 62–73. [Google Scholar] [CrossRef]

- Taylor, Natalie. 2003. Understanding taxpayer attitudes through understanding taxpayer identities. In Taxing Democracy: Understanding Tax Avoidance and Tax Evasion. Edited by Valerie Braithwaite. Aldershot: Ashgate, pp. 71–92. [Google Scholar]

- The Prime Minister. 2022. Decision No. 368/QD-TTg Dated 21 March 2022 on Approving the Financial Strategy until 2030. Available online: https://luatvietnam.vn/tai-chinh/quyet-dinh-368-qd-ttg-218471-d1.html (accessed on 29 April 2022).

- Torgler, Benno. 2007. Tax Compliance and Taxmorale: A Theoretical and Empirical Analysis. Cheltenham: Edward Elgar. [Google Scholar]

- Torgler, Benno, and Kristina Murphy. 2004. Tax morale in Australia: What shapes it and has it changed over time. Journal of Australian Taxation 7: 298–335. [Google Scholar]

- Traxler, Christian. 2010. Social norms and conditional cooperative taxpayers. European Journal of Political Economy 26: 89–103. [Google Scholar] [CrossRef] [Green Version]

- Vogel, Joachim. 1974. Taxation and public opinion in Sweden: An interpretation of recent survey data. National Tax Journal 27: 499–513. [Google Scholar] [CrossRef]

- Wenzel, Michael. 2004. The social side of sanctions: Personal and social norms as moderators of deterrence. Law and Human Behavior 28: 547–67. [Google Scholar] [CrossRef] [Green Version]

- Zikmund, William G. 2003. Business Research Methodology, 7th ed. Mason: Thomson South Western. [Google Scholar]

{kind=link}

| Characteristics | Classification | Frequency | Percentage (%) | Code |

|---|---|---|---|---|

| Occupation | Director | 44 | 13 | 1 |

| Deputy Director | 59 | 17 | 2 | |

| Chief accountant | 98 | 29 | 3 | |

| Tax accountant | 138 | 41 | 4 | |

| Working time | Less than 5 years | 36 | 11 | - |

| From 5 to less than 10 years | 58 | 17 | - | |

| From 10 to less than 20 years | 144 | 42 | - | |

| Over 20 years | 101 | 30 | - | |

| Education | Postgraduate level | 45 | 13 | 1 |

| University degree | 246 | 73 | 2 | |

| College degree | 48 | 14 | 3 | |

| Age | From 18 to 25 years old | 34 | 10 | 1 |

| From 25 to 35 years old | 108 | 32 | 2 | |

| From 35 to 50 years old | 110 | 32 | 3 | |

| Over 50 years old | 87 | 26 | 4 | |

| Gender | Male | 201 | 59 | 1 |

| Female | 138 | 41 | 0 |

| Component | N of Items | Cronbach’s Alpha | |

|---|---|---|---|

| 1 | The possibility of tax inspection and audit (AT) | 3 | 0.826 |

| 2 | Social norms (SN) | 3 | 0.834 |

| 3 | Tax knowledge (KT) | 5 | 0.815 |

| 4 | Personal norms (PN) | 3 | 0.834 |

| 5 | Perception of the tax system’s fairness (FT) | 6 | 0.882 |

| 6 | Tax service quality (ST) | 4 | 0.808 |

| 7 | Voluntary tax compliance (VTC) | 6 | 0.850 |

| Component | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | |

| FT5 | 0.886 | |||||

| FT4 | 0.844 | |||||

| FT2 | 0.790 | |||||

| FT6 | 0.748 | |||||

| FT1 | 0.719 | |||||

| FT3 | 0.714 | |||||

| KT4 | 0.876 | |||||

| KT2 | 0.759 | |||||

| KT3 | 0.717 | |||||

| KT5 | 0.691 | |||||

| KT1 | 0.680 | |||||

| ST1 | 0.826 | |||||

| ST4 | 0.786 | |||||

| ST2 | 0.785 | |||||

| ST3 | 0.780 | |||||

| SN2 | 0.904 | |||||

| SN1 | 0.868 | |||||

| SN3 | 0.833 | |||||

| PN2 | 0.878 | |||||

| PN3 | 0.865 | |||||

| PN1 | 0.837 | |||||

| AT2 | 0.938 | |||||

| AT3 | 0.857 | |||||

| AT1 | 0.780 | |||||

| Kaiser–Meyer–Olkin Measure of Sampling Adequacy. | KMO | 0.744 | ||||

| Bartlett’s Test of Sphericity | Sig. | 0.000 | ||||

| Extraction Sums of Squared Loadings | Total | 1.936 | ||||

| Cumulative % | 67.224 | |||||

| Component | ||

|---|---|---|

| 1 | ||

| VTC6 | 0.843 | |

| VTC5 | 0.808 | |

| VTC3 | 0.797 | |

| VTC1 | 0.748 | |

| VTC4 | 0.683 | |

| VTC2 | 0.666 | |

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | KMO | 0.852 |

| Bartlett’s Test of Sphericity | Sig. | 0.000 |

| Extraction Sums of Squared Loadings | Total | 3.468 |

| Cumulative % | 57.802 | |

| Variables | PN | AT | SN | KT | FT | ST | VTC |

|---|---|---|---|---|---|---|---|

| PN | 1 | ||||||

| AT | 0.020 | 1 | |||||

| SN | 0.111 * | −0.001 | 1 | ||||

| KT | 0.122 * | 0.030 | −0.048 | 1 | |||

| FT | 0.090 | 0.011 | −0.025 | 0.310 ** | 1 | ||

| ST | 0.074 | −0.112 * | 0.059 | 0.079 | 0.061 | 1 | |

| VTC | 0.279 ** | 0.449 ** | 0.213 ** | 0.452 ** | 0.326 ** | 0.150 ** | 1 |

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collinearity Statistics | |||

|---|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | Tolerance | VIF | ||||

| 1 | (Constant) | −0.386 | 0.306 | −1.264 | 0.207 | |||

| PN | 0.124 | 0.030 | 0.161 | 4.117 | 0.000 | 0.905 | 1.105 | |

| AT | 0.248 | 0.021 | 0.444 | 11.745 | 0.000 | 0.968 | 1.033 | |

| SN | 0.151 | 0.027 | 0.209 | 5.511 | 0.000 | 0.959 | 1.042 | |

| FT | 0.189 | 0.039 | 0.193 | 4.908 | 0.000 | 0.897 | 1.114 | |

| KT | 0.362 | 0.041 | 0.348 | 8.749 | 0.000 | 0.873 | 1.146 | |

| ST | 0.130 | 0.039 | 0.128 | 3.383 | 0.001 | 0.960 | 1.041 | |

| Age | −0.056 | 0.039 | −0.056 | −1.421 | 0.156 | 0.902 | 1.108 | |

| Gender | −0.031 | 0.020 | −0.060 | −1.579 | 0.115 | 0.958 | 1.044 | |

| Education | −0.010 | 0.035 | −0.011 | −0.294 | 0.769 | 0.992 | 1.008 | |

| Occupation | −0.020 | 0.018 | −0.043 | −1.139 | 0.255 | 0.982 | 1.018 | |

| Adjusted R Square | 0.533 | |||||||

| Durbin-Watson | 1.873 | |||||||

| Sig value of the ANOVA test | 0.000 | |||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nguyen, T.H. The Impact of Non-Economic Factors on Voluntary Tax Compliance Behavior: A Case Study of Small and Medium Enterprises in Vietnam. Economies 2022, 10, 179. https://doi.org/10.3390/economies10080179

Nguyen TH. The Impact of Non-Economic Factors on Voluntary Tax Compliance Behavior: A Case Study of Small and Medium Enterprises in Vietnam. Economies. 2022; 10(8):179. https://doi.org/10.3390/economies10080179

Chicago/Turabian StyleNguyen, Thu Hien. 2022. "The Impact of Non-Economic Factors on Voluntary Tax Compliance Behavior: A Case Study of Small and Medium Enterprises in Vietnam" Economies 10, no. 8: 179. https://doi.org/10.3390/economies10080179

APA StyleNguyen, T. H. (2022). The Impact of Non-Economic Factors on Voluntary Tax Compliance Behavior: A Case Study of Small and Medium Enterprises in Vietnam. Economies, 10(8), 179. https://doi.org/10.3390/economies10080179