Formal vs. Informal Institutional Distances and the Competitive Advantage of Foreign Subsidiaries in Latin America

Abstract

:1. Introduction

2. Literature Review and Hypotheses

2.1. Directional Cultural Distance (DCD) Hypothesis

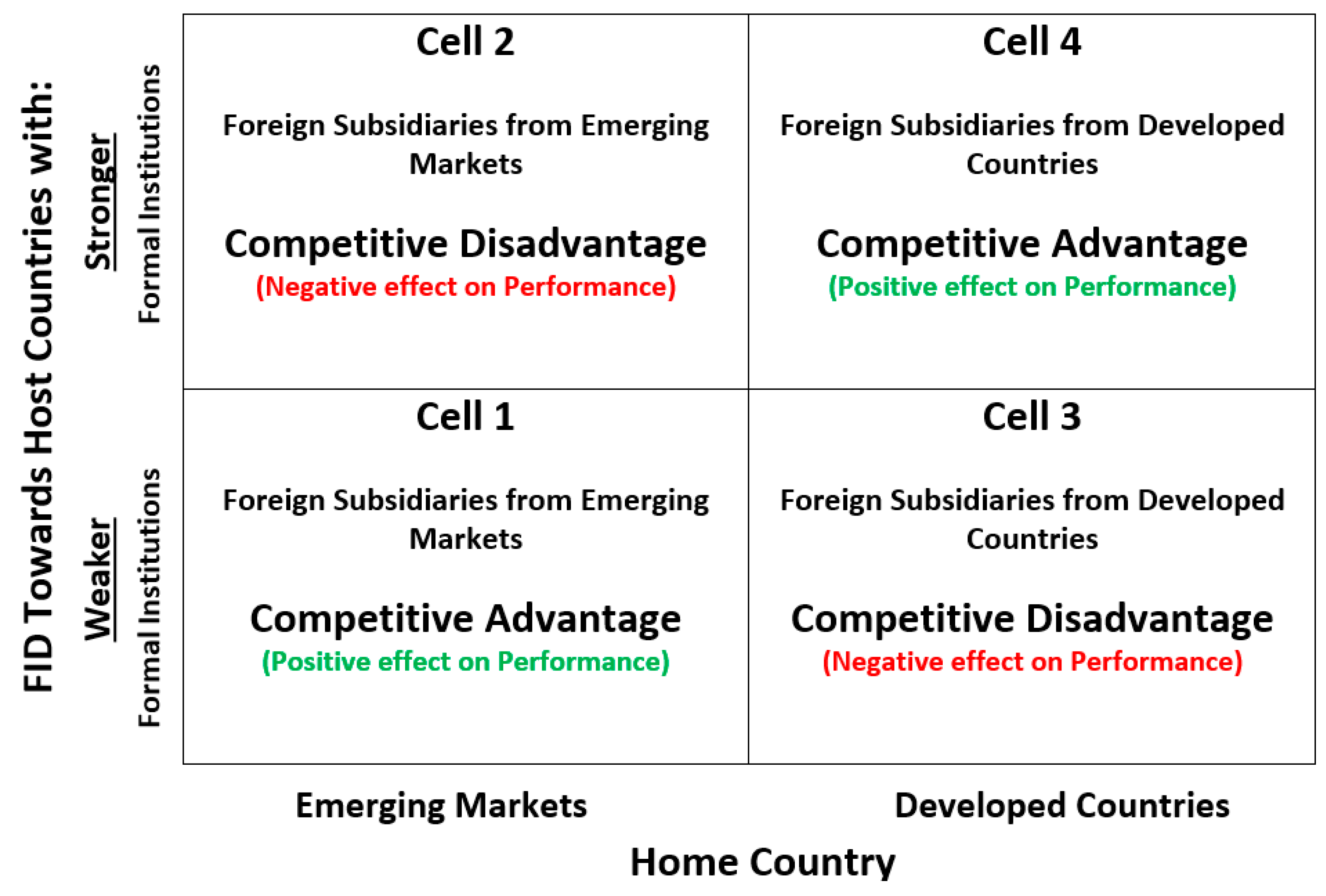

2.2. Formal Institutional Distance (FID) Hypothesis

3. Data and Methodology

3.1. Panel Data Method

3.2. Computing the Directional FID and CD

- Distance in LH Direction

- Distance in HL Direction

3.3. Dependent Variable

3.4. Independent Variables

3.5. Control Variables

3.6. Descriptive Statistics and Correlation Matrices

4. Main Results and Discussion

4.1. Preliminary Tests

4.2. Main Results—Directional Cultural Distance (DCD)

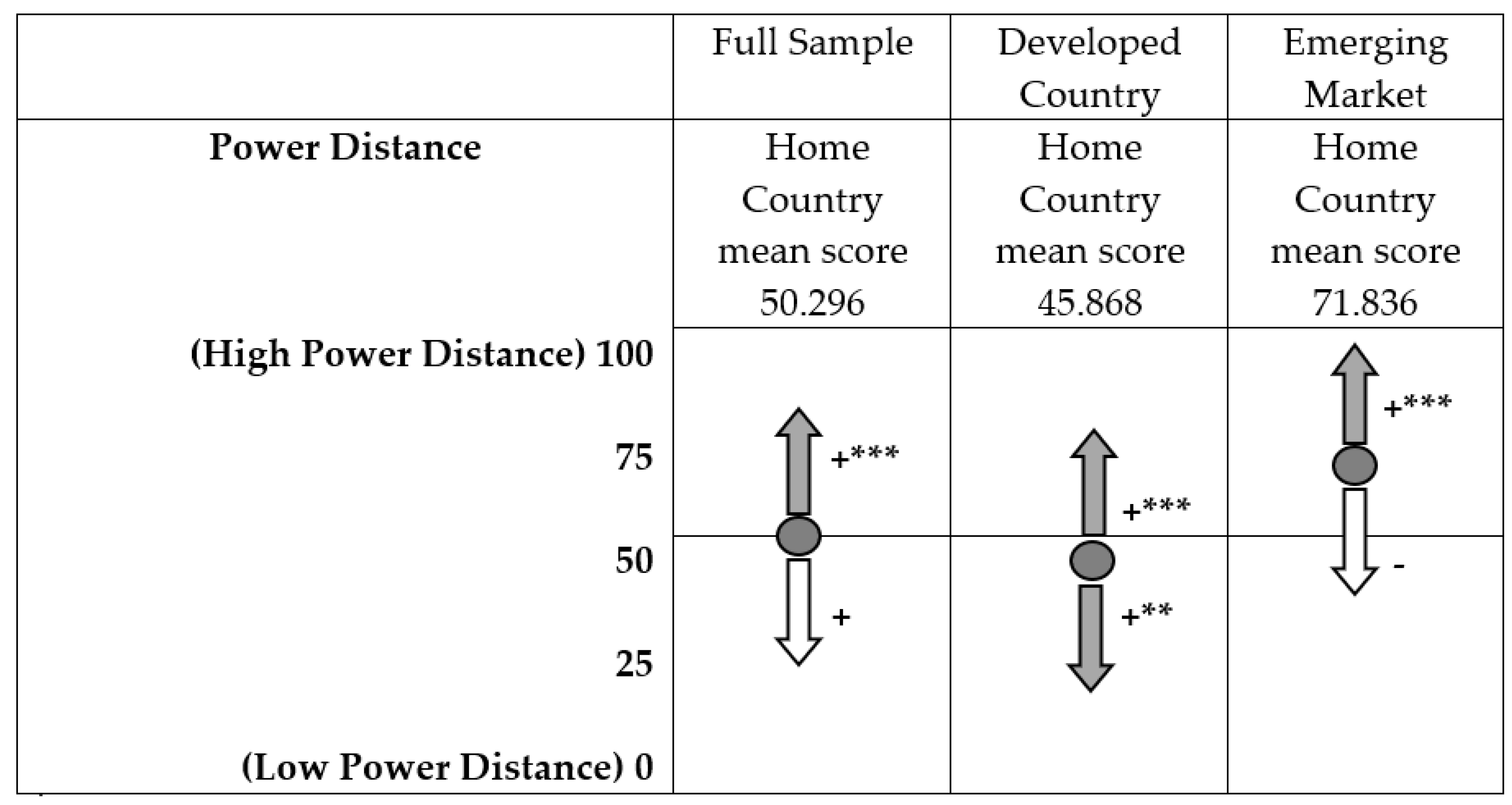

4.2.1. DCD—Power Distance Index

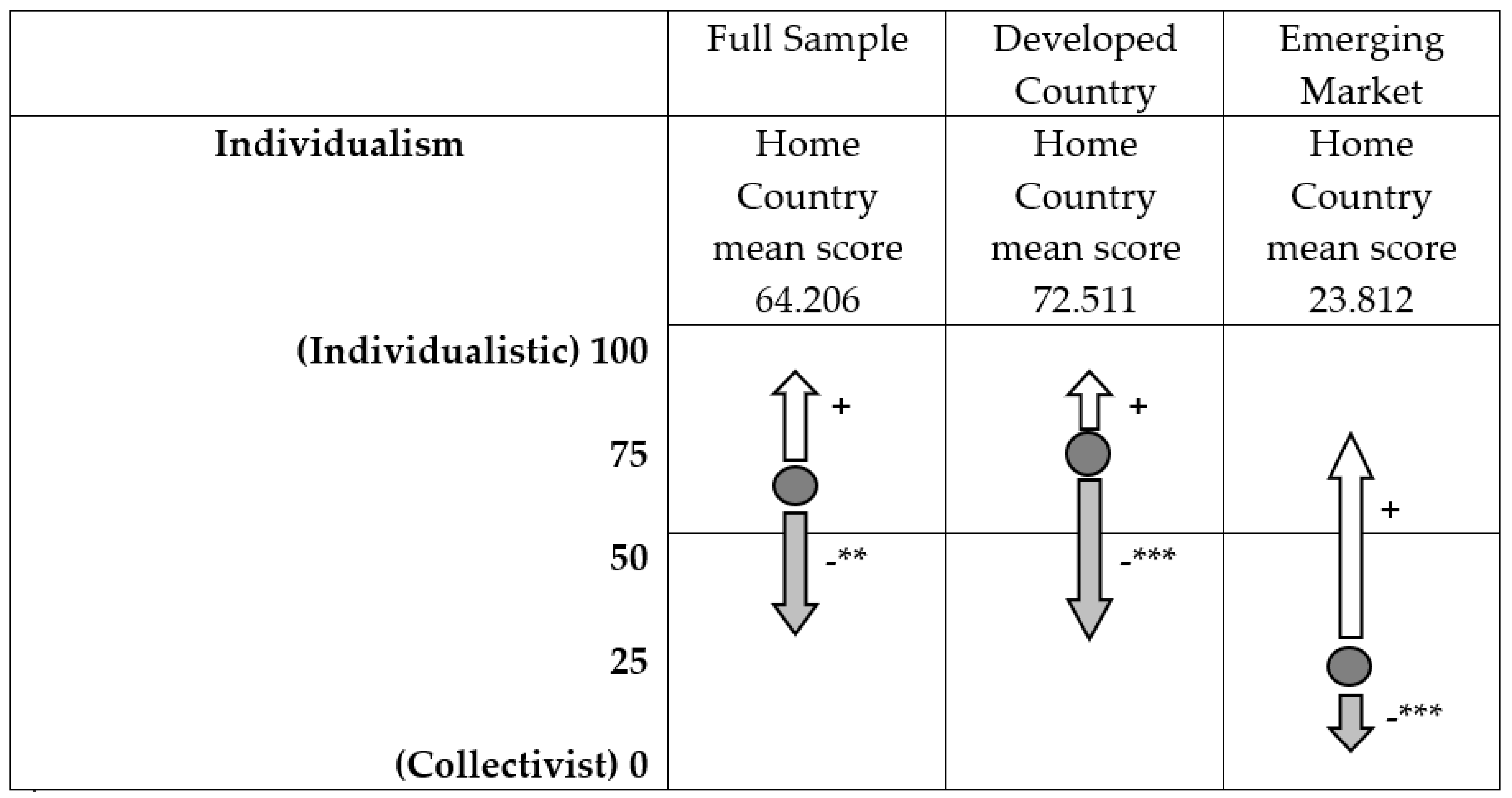

4.2.2. DCD—Individualism vs. Collectivism

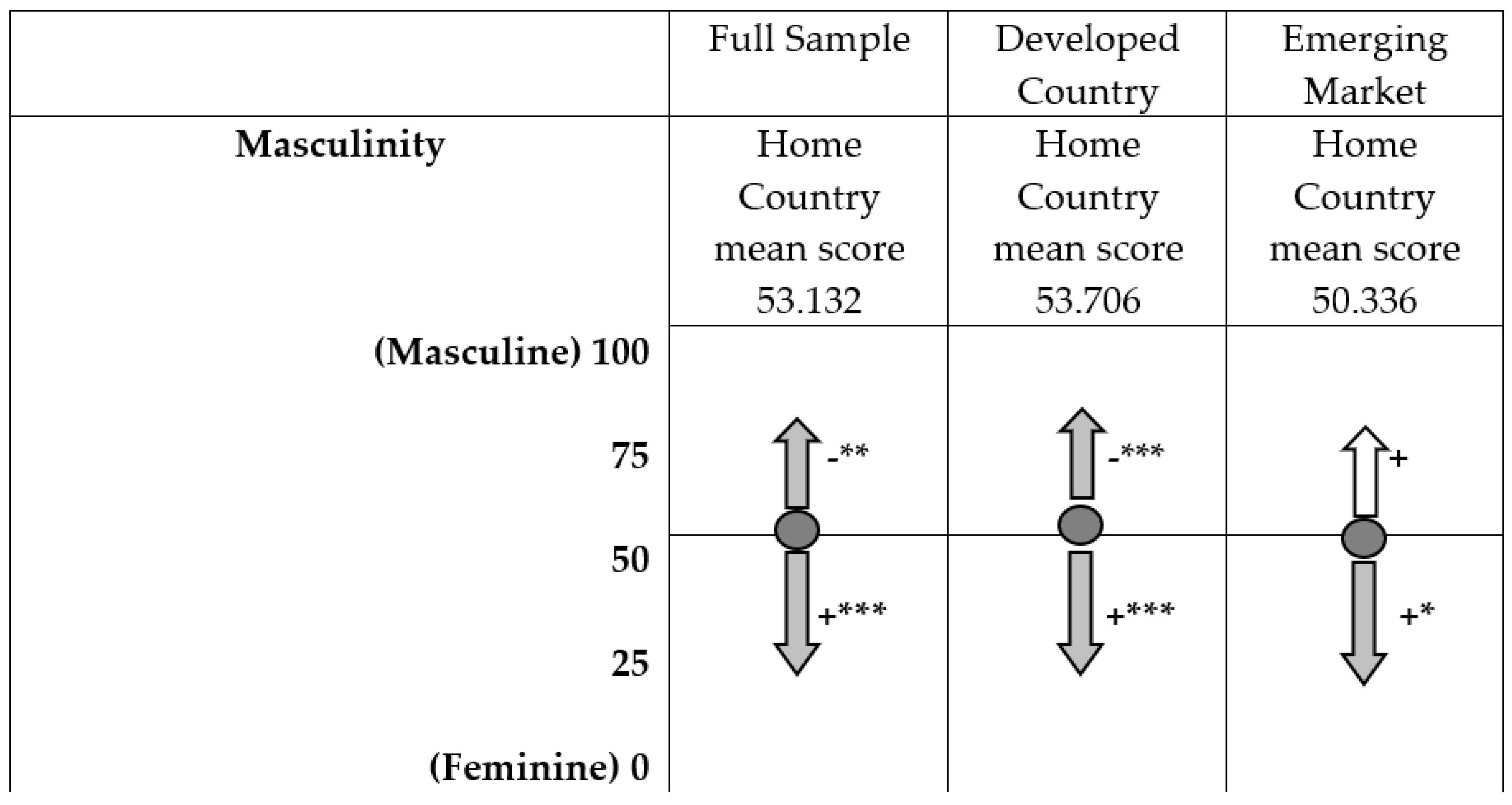

4.2.3. DCD—Masculinity vs. Femininity Dimension

4.2.4. DCD—Uncertainty Avoidance Dimension

4.3. Main Results—Formal Institutional Distance (FID)

4.3.1. FID and the Financial Performance of Foreign Subsidiaries from Developed Countries

4.3.2. FID and the Financial Performance of Foreign Subsidiaries from Emerging Markets

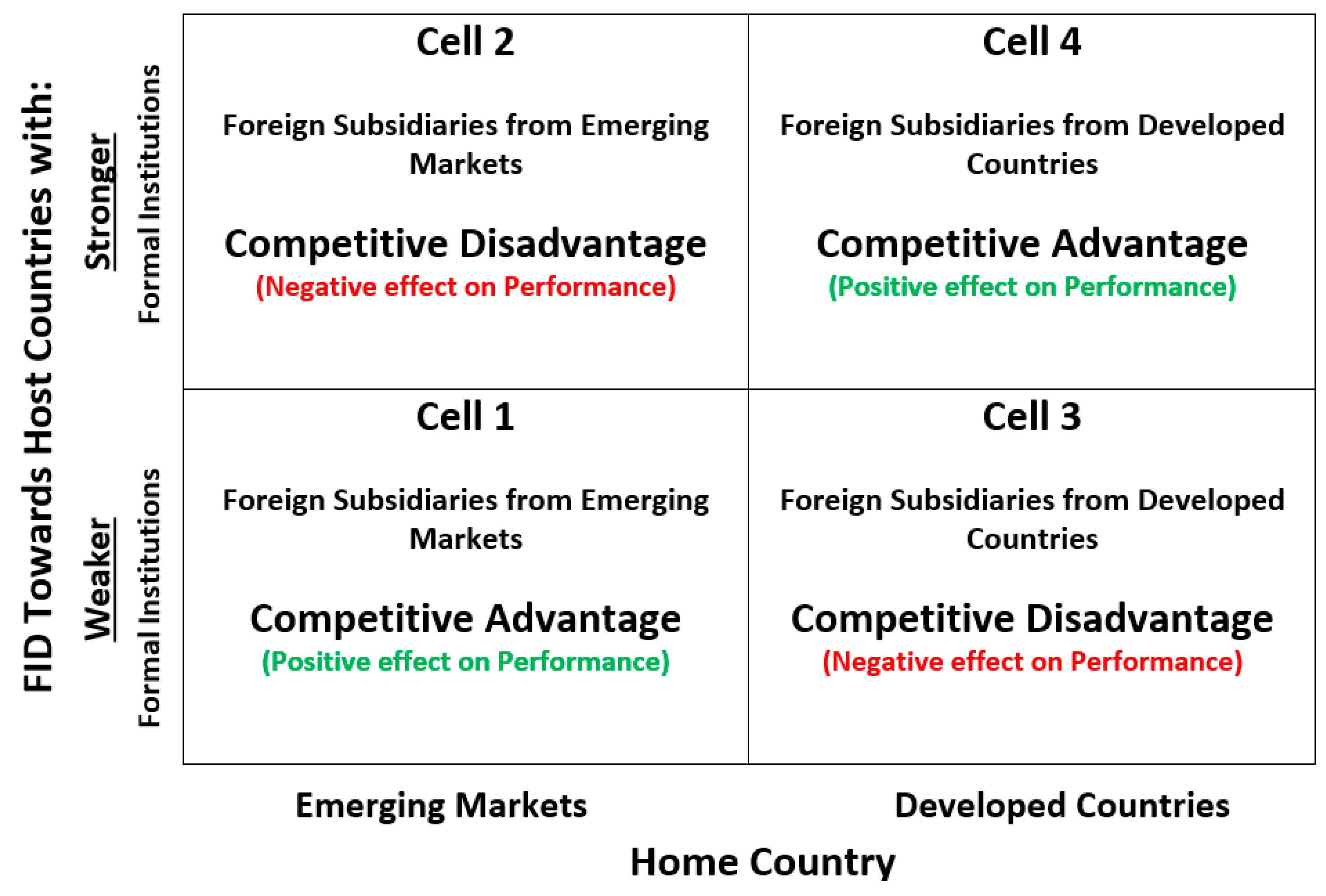

4.3.3. FID as a Competitive Advantage (or Disadvantage)

4.4. Theoretical Contributions

4.5. Practical Implications

4.6. Limitations and Directions for Future Research

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Aguilera, Ruth V., Luciano Ciravegna, Alvaro Cuervo-Cazurra, and Maria Alejandra Gonzalez-Perez. 2017. Multilatinas and the internationalization of Latin American firms. Journal of World Business 52: 447–60. [Google Scholar] [CrossRef] [Green Version]

- Aguinis, Herman, Isabel Villamor, Sergio G. Lazzarini, Roberto S. Vassolo, José Ernesto Amorós, and David G. Allen. 2020. Conducting management research in Latin America: Why and what’s in it for you? Journal of Management 46: 615–36. [Google Scholar] [CrossRef] [Green Version]

- Ambos, Björn, and Lars Håkanson. 2014. The concept of distance in international management research. Journal of International Management 20: 1–7. [Google Scholar] [CrossRef]

- Baltagi, Badi H., and Baldev Raj. 1992. A survey of recent theoretical developments in the econometrics of panel data. Empirical Economics 17: 85–109. [Google Scholar] [CrossRef]

- Beckerman, Wilfred. 1956. Distance and the pattern of intra-European trade. The Review of Economics and Statistics 38: 31–40. [Google Scholar] [CrossRef]

- Beugelsdijk, Sjoerd, Tatiana Kostova, Vincent E. Kunst, Ettore Spadafora, and Marc Van Essen. 2018. Cultural Distance and Firm Internationalization: A Meta-Analytical Review and Theoretical Implications. Journal of Management 44: 89–130. [Google Scholar] [CrossRef] [Green Version]

- Chikhouni, Abdulrahman, Gwyneth Edwards, and Mehdi Farashahi. 2017. Psychic distance and ownership in acquisitions: Direction matters. Journal of International Management 23: 32–42. [Google Scholar] [CrossRef]

- Chopra, Rohit, and Juan Mier. 2017. Profitability Trends in Emerging Markets Setting the Stage for Active Management. New York: Lazard Asset Management LLC. [Google Scholar]

- Contractor, Farok J., Sumit K. Kundu, and Chin-Chun Hsu. 2003. A three-stage theory of international expansion: The link between multinationality and performance in the service sector. Journal of International Business Studies 34: 5–18. [Google Scholar] [CrossRef]

- Contractor, Farok, Yong Yang, and Ajai S. Gaur. 2016. Firm-specific intangible assets and subsidiary profitability: The moderating role of distance, ownership strategy and subsidiary experience. Journal of World Business 51: 950–64. [Google Scholar] [CrossRef]

- Correa da Cunha, Henrique. 2019. Asymmetry and the moderating effects of for-mal institutional distance on the relationship between cultural distance and performance: The case of multinational foreign subsidiaries in Latin America. In The Direction of Cultural Distance and the Performance of Foreign Subsidiaries in Latin America Disser-Tations No. 61. Halmstad: Halmstad University Press. [Google Scholar]

- Correa da Cunha, Henrique, Carlyle Farrell, Svante Andersson, Mohamed Amal, and Dinora Eliete Floriani. 2020. The Direction of Cultural Distance and the Performance of Foreign Subsidiaries in Latin America. In Academy of Management Proceedings. Briarcliff Manor: Academy of Management, vol. 2020, p. 22159. [Google Scholar]

- Correa da Cunha, Henrique, Carlyle Farrell, Svante Andersson, Mohamed Amal, and Dinora Eliete Floriani. 2022a. Toward a more in-depth measurement of cultural distance: A re-evaluation of the underlying assumptions. International Journal of Cross Cultural Management 22: 157–88. [Google Scholar] [CrossRef]

- Correa da Cunha, Henrique, Vik Singh, and Shengkun Xie. 2022b. The Determinants of Outward Foreign Direct Investment from Latin America and the Caribbean: An Integrated Entropy-Based TOPSIS Multiple Regression Analysis Framework. Journal of Risk and Financial Management 15: 130. [Google Scholar] [CrossRef]

- Cuervo-Cazurra, Alvaro, and Mehmet Erdem Genc. 2011. Obligating, pressuring, and supporting dimensions of the environment and the non-market advantages of developing-country multinational companies. Journal of Management Studies 48: 441–55. [Google Scholar] [CrossRef]

- Dow, Douglas. 2017. Are we at a Turning Point for Distance Research in International Business Studies? In Distance in International Business: Concept, Cost and Value. Bingley: Emerald Publishing Limited, pp. 47–68. [Google Scholar]

- Ficici, Aysun, Lingling Wang, C. Bulent Aybar, and Bo Fan. 2014. The Correlation between the Internationalization Processes and Performance of Firms: The Case of Emerging Market Firms of the BRIC Countries. Journal of Economics and Political Economy 1: 4–25. [Google Scholar]

- Gani, Azmat. 2007. Governance and foreign direct investment links: Evidence from panel data estimations. Applied Economics Letters 14: 753–56. [Google Scholar] [CrossRef]

- Geringer, J. Michael, and Louis Hebert. 1989. Control and performance of international joint ventures. Journal of International Business Studies 20: 235–54. [Google Scholar] [CrossRef] [Green Version]

- Globerman, Steven, and Daniel Shapiro. 2003. Governance Infrastructure and US Foreign Direct Investment. Journal of International Business Studies 34: 19–39. [Google Scholar] [CrossRef]

- Gorodnichenko, Yuriy, and Gerard Roland. 2011. Which dimensions of culture matter for long-run growth? American Economic Review 101: 492–98. [Google Scholar] [CrossRef] [Green Version]

- Gupta, Vipin, Paul J. Hanges, and Peter Dorfman. 2002. Cultural clusters: Methodology and findings. Journal of World Business 37: 11–15. [Google Scholar] [CrossRef]

- Hannan, Michael T., and John Freeman. 1984. Structural inertia and organizational change. American Sociological Review 49: 149–64. [Google Scholar] [CrossRef]

- Hay, Donald A., Derek Morris, and Derek J. Morris. 1991. Industrial Economics and Organization: Theory and Evidence. Oxford: Oxford University Press. [Google Scholar]

- Hernández, Virginia, and María Jesús Nieto. 2015. The effect of the magnitude and direction of institutional distance on the choice of international entry modes. Journal of World Business 50: 122–32. [Google Scholar] [CrossRef]

- Hernández, Virginia, María Jesús Nieto, and Andrea Boellis. 2018. The asymmetric effect of institutional distance on international location: Family versus nonfamily firms. Global Strategy Journal 8: 22–45. [Google Scholar] [CrossRef]

- Hofstede, Geert. 1980. Culture and organizations. International Studies of Management & Organization 10: 15–41. [Google Scholar]

- Hofstede, Geert, Gert Jan Hofstede, and Michael Minkov. 2005. Cultures and Organizations: Software of the Mind. New York: Mcgraw-Hill, vol. 2. [Google Scholar]

- Inglehart, Ronald, and Marita Carballo. 1997. Does Latin America Exist? (And is There a Confucian Culture?): A Global Analysis of Cross-Cultural Differences1. PS: Political Science & Politics 30: 34–47. [Google Scholar]

- Johanson, Jan, and Finn Wiedersheim-Paul. 1975. The internationalization of the firm—Four Swedish cases 1. Journal of Management Studies 12: 305–23. [Google Scholar] [CrossRef]

- Kaufmann, Daniel, and Aart Kraay. 2008. Governance Indicators: Where Are We. Where Should We Be Going? The World Bank Research Observer 23: 1–30. [Google Scholar] [CrossRef] [Green Version]

- Klasing, Mariko. J. 2013. Cultural dimensions, collective values and their importance for institutions. Journal of Comparative Economics 41: 447–67. [Google Scholar] [CrossRef]

- Kogut, Bruce, and Harbir Singh. 1988. The effect of national culture on the choice of entry mode. Journal of International Business Studies 19: 411–32. [Google Scholar] [CrossRef]

- Konara, Palitha, and Vikrant Shirodkar. 2018. Regulatory institutional distance and MNCs’ subsidiary performance: Climbing up vs. climbing down the institutional ladder. Journal of International Management 24: 333–47. [Google Scholar] [CrossRef]

- Kostova, Tatiana. 1996. Success of the Transnational Transfer of Organizational Practices Within Multinational Companies. Minneapolis: University of Minnesota. [Google Scholar]

- Kraus, Sascha, Tina C. Ambos, Felix Eggers, and Beate Cesinger. 2015. Distance and perceptions of risk in internationalization decisions. Journal of Business Research 68: 1501–5. [Google Scholar] [CrossRef]

- Linnemann, Hans. 1966. An Econometric Study of International Trade Flows (No. 42). Amsterdam: North-Holland. [Google Scholar]

- Magnani, Giovanna, Antonella Zucchella, and Dinorá Eliete Floriani. 2018. The logic behind foreign market selection: Objective distance dimensions vs. strategic objectives and psychic distance. International Business Review 27: 1–20. [Google Scholar] [CrossRef] [Green Version]

- Maseland, Robbert. 2013. Parasitical cultures? The cultural origins of institutions and development. Journal of Economic Growth 18: 109–36. [Google Scholar] [CrossRef]

- Mengistu, Alemu Aye, and Bishnu Kumar Adhikary. 2011. Does good governance matter for FDI inflows? Evidence from Asian economies. Asia Pacific Business Review 17: 281–99. [Google Scholar] [CrossRef]

- Meyer, Klaus E., Saul Estrin, Sumon Kumar Bhaumik, and Mike W. Peng. 2009. Institutions, resources, and entry strategies in emerging economies. Strategic Management Journal 30: 61–80. [Google Scholar] [CrossRef] [Green Version]

- Mukerji, Chandra. 2014. The cultural power of tacit knowledge: Inarticulacy and Bourdieu’s habitus. American Journal of Cultural Sociology 2: 348–75. [Google Scholar] [CrossRef]

- Neter, John, William Wasserman, and Michael H. Kutner. 1990. Applied Statistical Models. Burr Ridge: Richard D. Irwin, Inc. [Google Scholar]

- North, Douglass C. 1990. Institutions, Institutional Change and Economic Performance. Cambridge: Cambridge University Press. [Google Scholar]

- O’grady, Shawna, and Henry W. Lane. 1996. The psychic distance paradox. Journal of International Business Studies 27: 309–33. [Google Scholar] [CrossRef]

- Palepu, Krishna G., and Tarun Khanna. 1998. Institutional voids and policy challenges in emerging markets. The Brown Journal of World Affairs 5: 71. [Google Scholar]

- Peng, Mike W., Sunny Li Sun, Brian Pinkham, and Hao Chen. 2009. The institution-based view as a third leg for a strategy tripod. Academy of Management Perspectives 23: 63–81. [Google Scholar] [CrossRef] [Green Version]

- Polanyi, Michael. 1967. The Tacit Dimension. Anchor: Garden City. [Google Scholar]

- Ramamurti, Ravi, and Jitendra V. Singh. 2009. Emerging Multinationals in Emerging Markets. Cambridge: Cambridge University Press. [Google Scholar]

- Scott, William Richard. 1995. Institutions and Organizations. Thousand Oaks: Sage, vol. 2. [Google Scholar]

- Selmer, Jan, Randy K. Chiu, and Oded Shenkar. 2007. Cultural distance asymmetry in expatriate adjustment. Cross Cultural Management: An International Journal 4: 150–60. [Google Scholar] [CrossRef]

- Shenkar, Oded. 2001. CD revisited: Towards a more rigorous conceptualization and measurement of cultural differences. Journal of International Business Studies 32: 519–35. [Google Scholar] [CrossRef]

- Shenkar, Oded, Yadong Luo, and Orly Yeheskel. 2008. From “distance” to “friction”: Substituting metaphors and redirecting intercultural research. Academy of Management Review 33: 905–23. [Google Scholar] [CrossRef]

- Shenkar, Oded, Stephen B. Tallman, Hao Wang, and Jie Wu. 2020. National culture and international business: A path forward. Journal of International Business Studies 53: 516–33. [Google Scholar] [CrossRef]

- Stahl, Günter K., and Rosalie L. Tung. 2015. Towards a more balanced treatment of culture in international business studies: The need for positive cross-cultural scholarship. Journal of International Business Studies 46: 391–414. [Google Scholar] [CrossRef]

- Stein, Ernesto, and Christian Daude. 2001. Institutions, integration and the location of foreign direct investment. In Global Forum on International Investment: New Horizons for Foreign Direct Investment. Paris: OECD Publications Services, pp. 101–30. [Google Scholar]

- Stor, Marzena. 2021. The configurations of HRM bundles in MNCs by their contributions to subsidiaries’ performance and cultural dimensions. International Journal of Cross Cultural Management 21: 123–66. [Google Scholar] [CrossRef]

- Trąpczyński, Piotr, and Elitsa R. Banalieva. 2016. Institutional difference, organizational experience, and foreign affiliate performance: Evidence from Polish firms. Journal of World Business 51: 826–42. [Google Scholar] [CrossRef]

- Vaccarini, Katiuscia, Francesca Spigarelli, Ernesto Tavoletti, and Christoph Lattemann. 2017. Cultural Distance in International Ventures: Exploring Perceptions of European and Chinese Managers. Berlin/Heidelberg: Springer. [Google Scholar]

- Vahlne, Jan-Erik, and Jan Johanson. 2017. From internationalization to evolution: The Uppsala model at 40 years. Journal of International Business Studies 48: 1087–102. [Google Scholar] [CrossRef]

- Verbeke, Alain, Rob van Tulder, and Jonas Puck. 2017. Distance in International Business Studies: Concept, Cost and Value. In Distance in International Business: Concept, Cost and Value. Bingley: Emerald Publishing Limited, pp. 17–43. [Google Scholar]

- Wernick, David A., Jerry Haar, and Shane Singh. 2009. Do governing institutions affect foreign direct investment inflows? New evidence from emerging economies. International Journal of Economics and Business Research 1: 317–32. [Google Scholar] [CrossRef]

- Williamson, Oliver E. 1975. Markets and Hierarchies: Analysis and Antitrust Implications: A Study in the Economics of Internal Organization. New York: Free Press. [Google Scholar]

- World Bank. 2021. World Bank Open Data. Free and Open Access to Global Development Data. Washington, DC: The World Bank Group, Available online: https://data.worldbank.org/ (accessed on 1 December 2021).

- Zaheer, Srilata. 1995. Overcoming the liability of foreignness. Academy of Management Journal 38: 341–63. [Google Scholar]

- Zaheer, Srilata, Margaret Spring Schomaker, and Lilach Nachum. 2012. Distance without direction: Restoring credibility to a much-loved construct. Journal of International Business Studies 43: 18–27. [Google Scholar] [CrossRef]

DCD significant effects (gray arrow).

DCD significant effects (gray arrow).

DCD non-significant effects (white arrow).

DCD non-significant effects (white arrow).  Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01. DCD significant effects (gray arrow). DCD non-significant effects (white arrow ). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

DCD significant effects (gray arrow). DCD non-significant effects (white arrow ). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

DCD significant effects (gray arrow). DCD non-significant effects (white arrow ). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

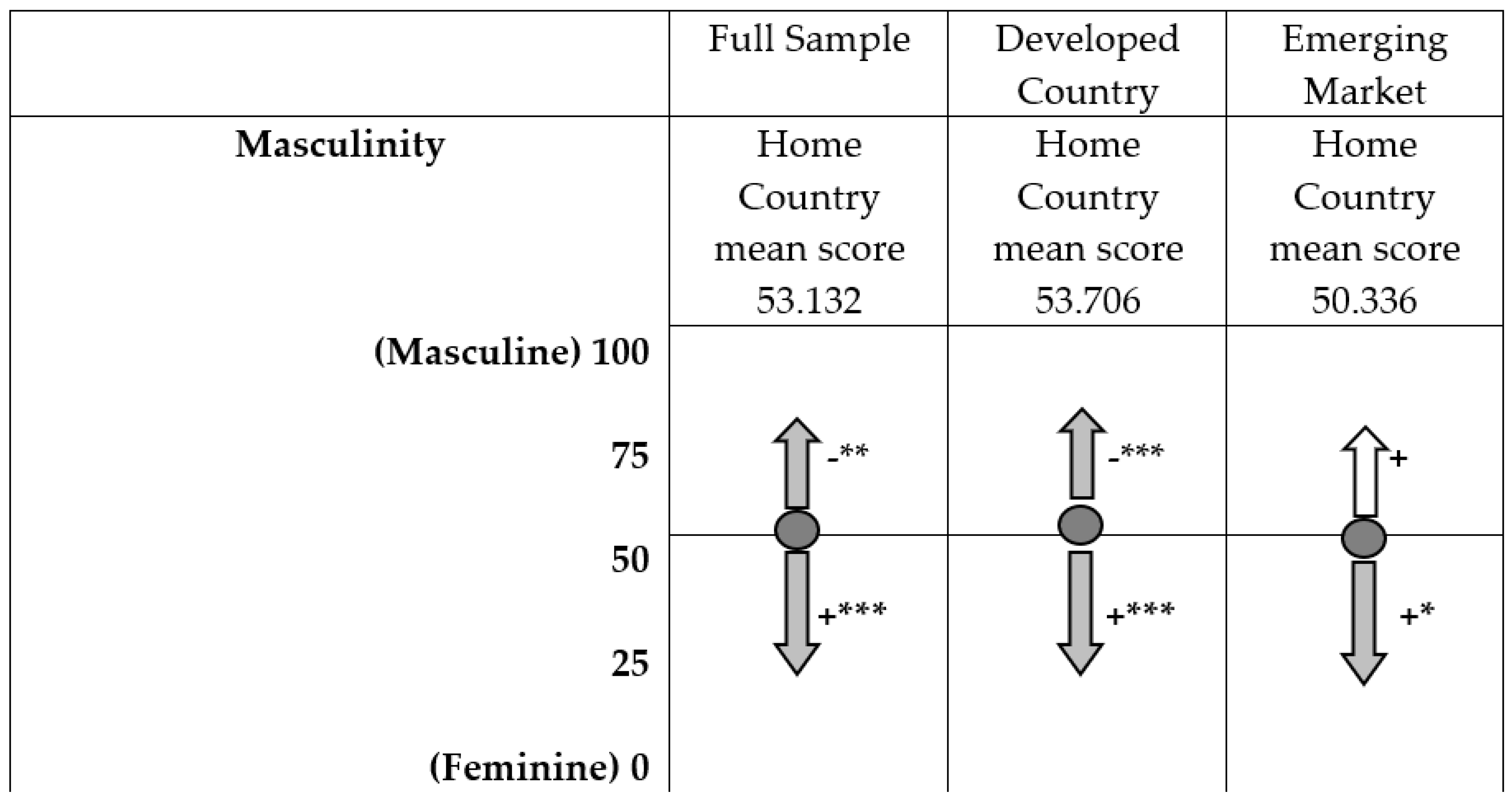

DCD significant effects (gray arrow). DCD non-significant effects (white arrow ). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01. DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01.

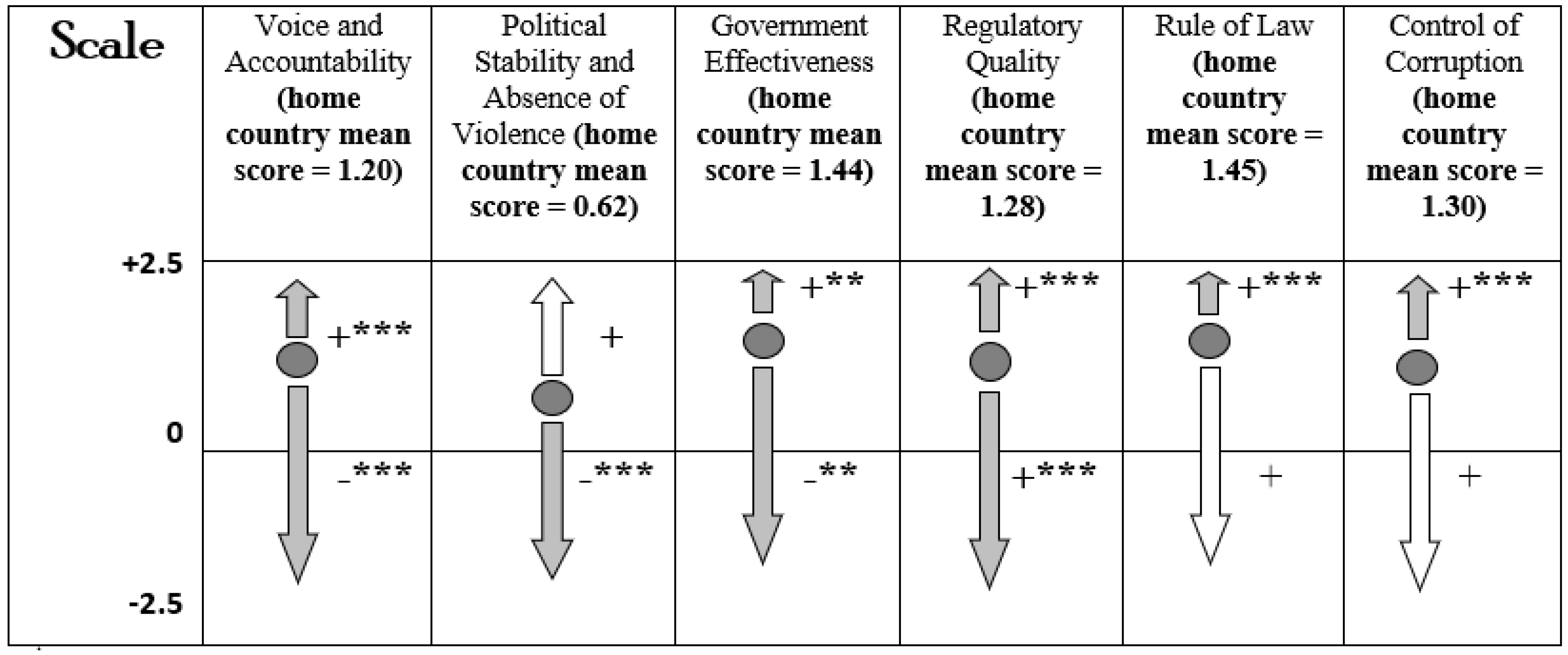

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01.

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01.

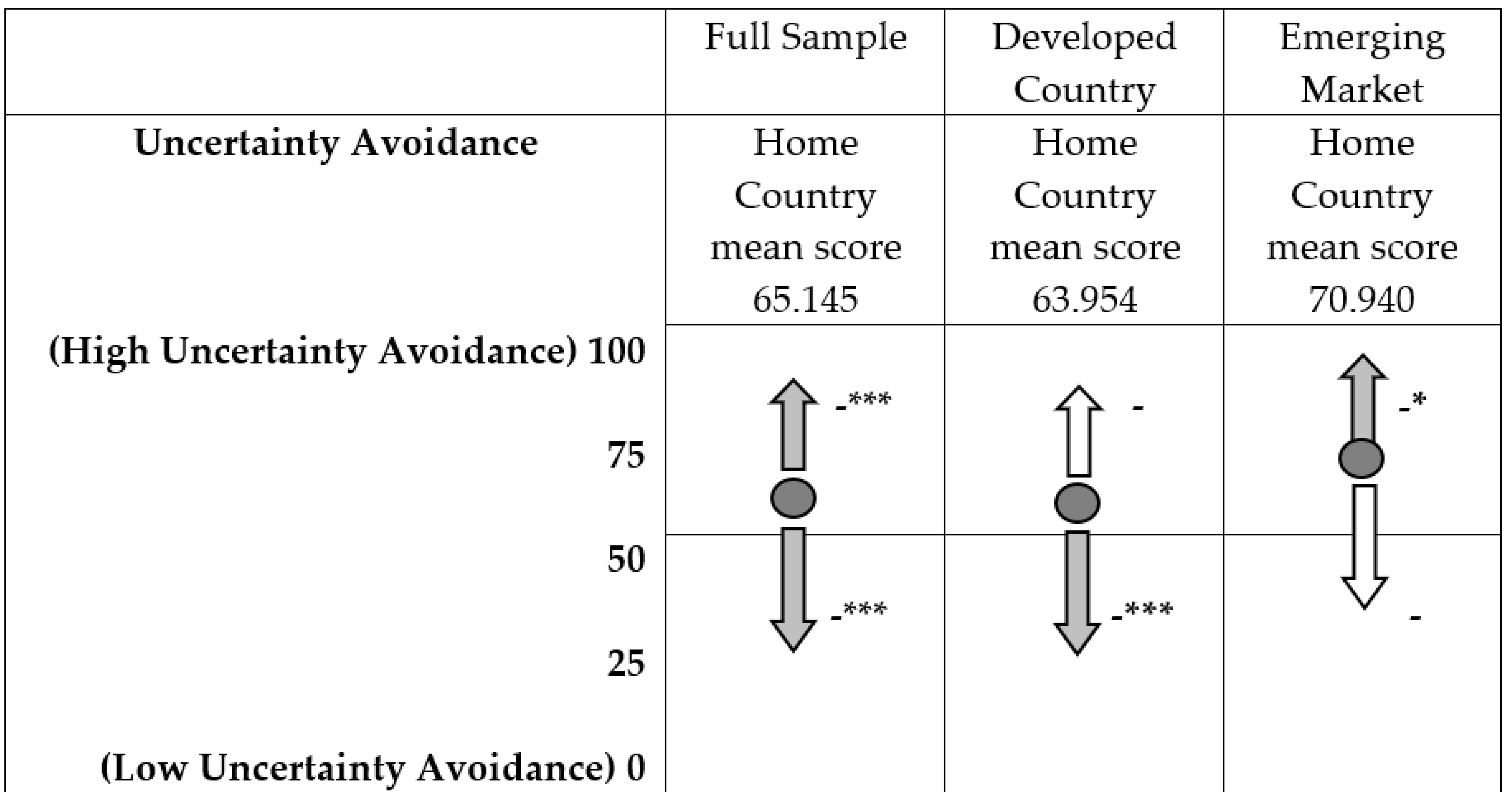

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01. DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; *** p < 0.01.

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; *** p < 0.01.

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; *** p < 0.01.

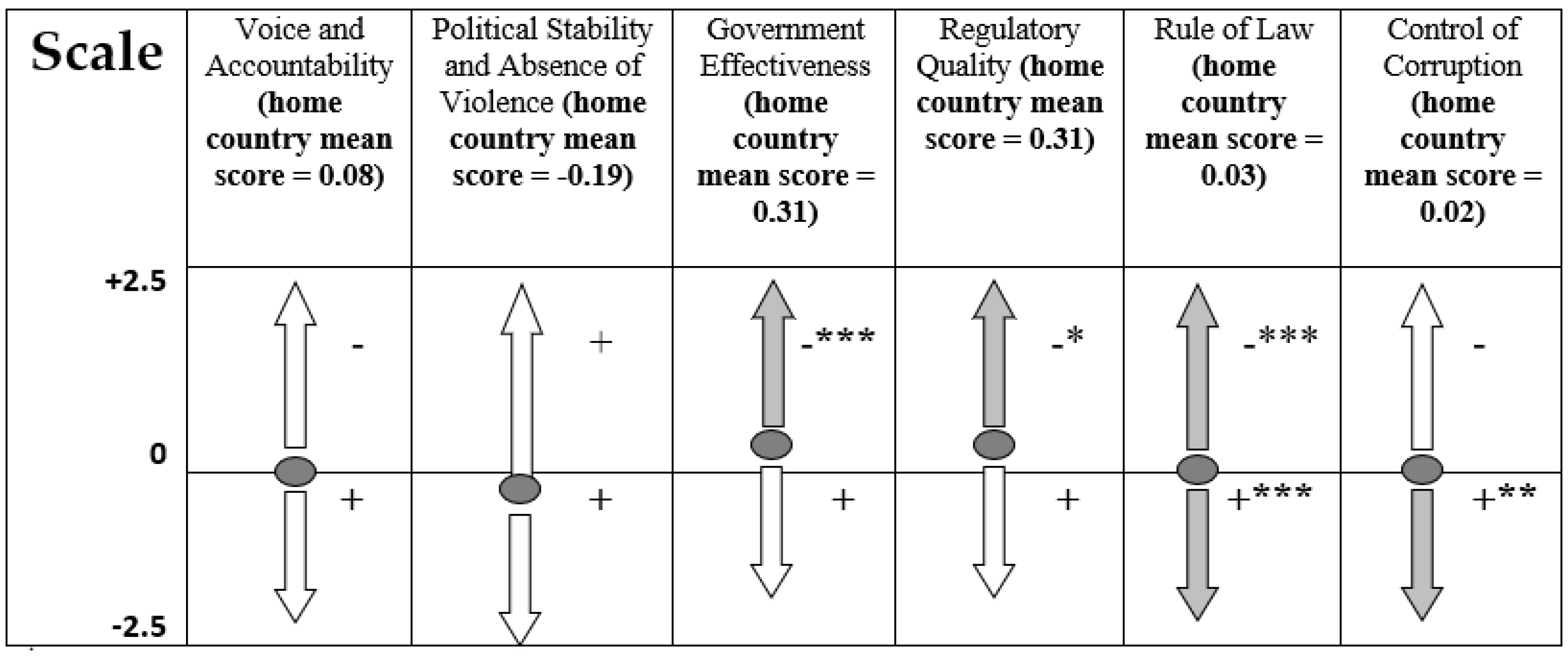

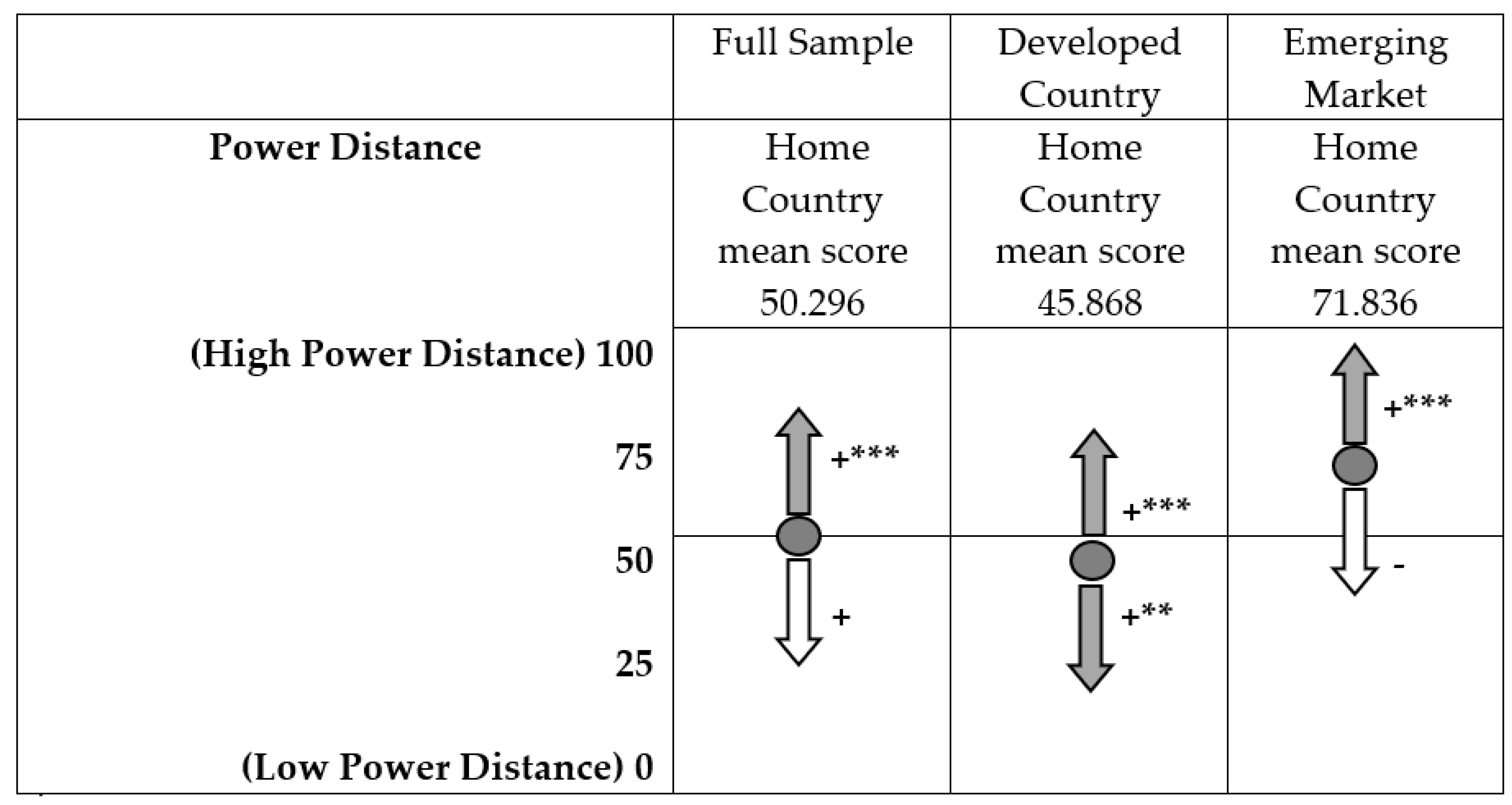

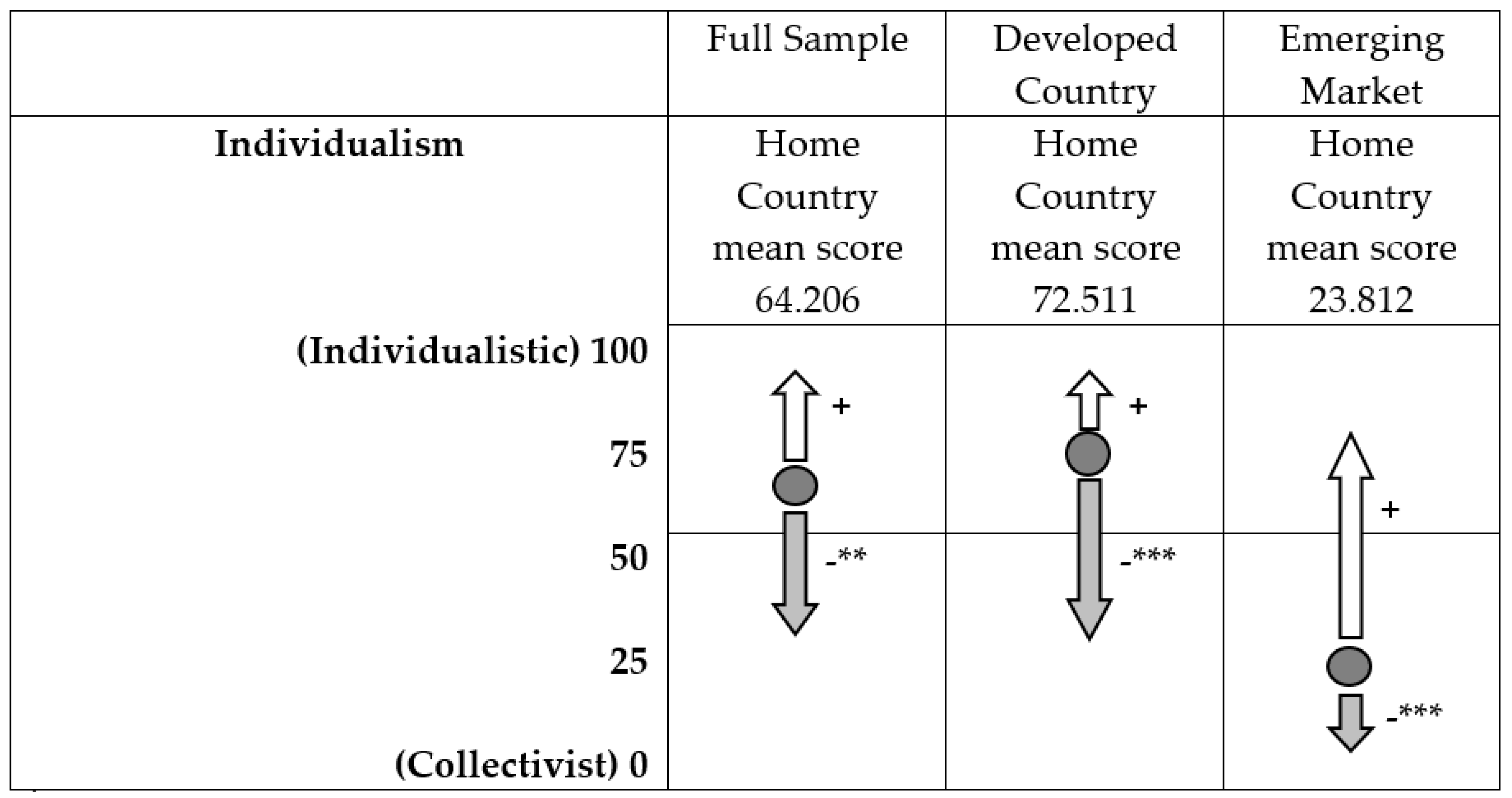

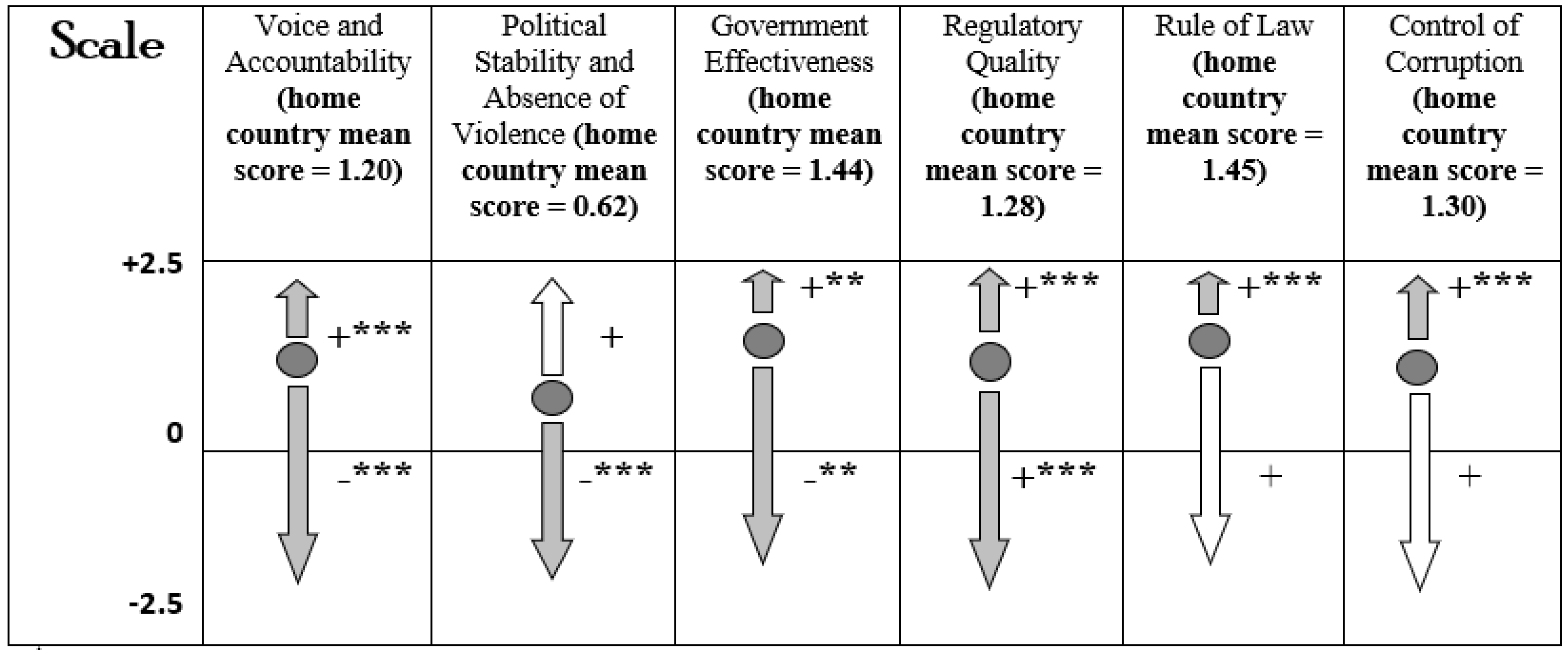

DCD significant effects (gray arrow). DCD non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; *** p < 0.01. FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01.

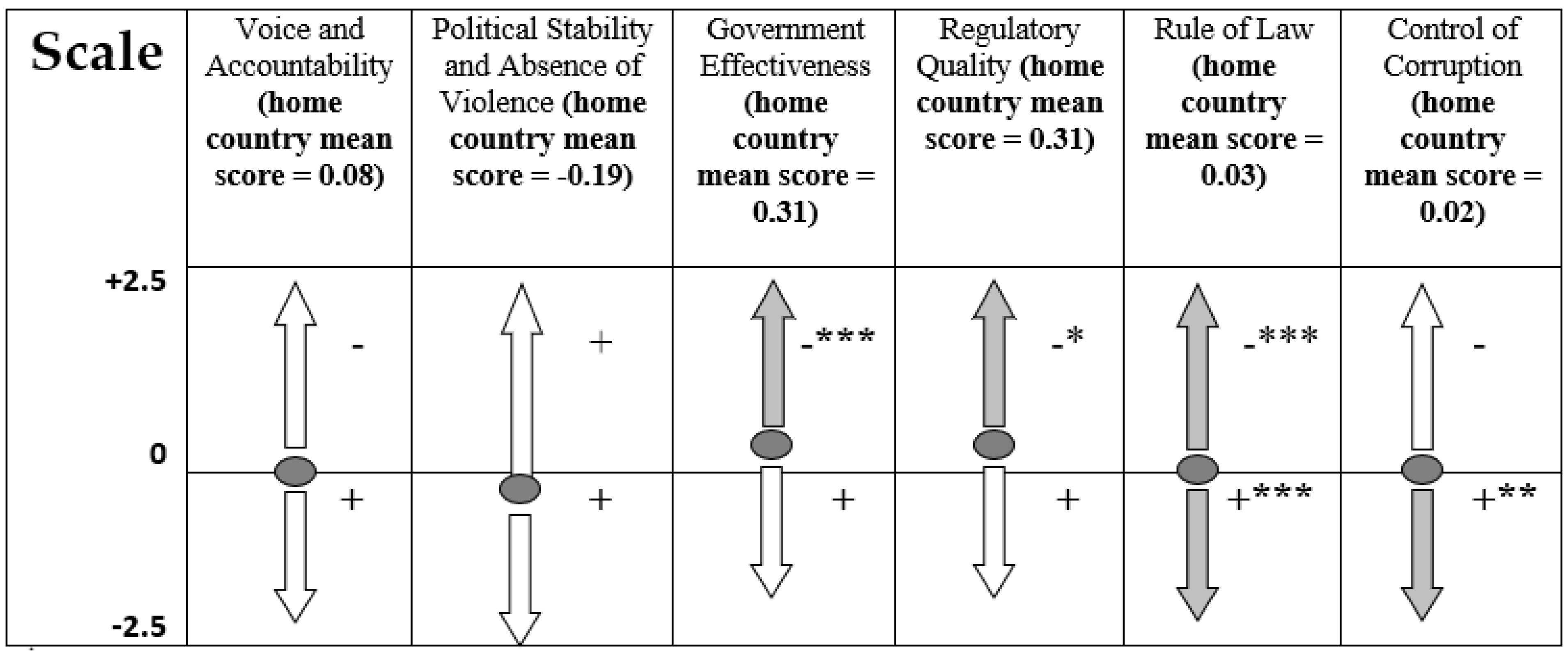

FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). ** p < 0.05; *** p < 0.01. FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01.

FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01.

FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01.

FID significant effects (gray arrow). FID non-significant effects (white arrow). Mean score for the home countries in the sample (position in the scale). * p < 0.10; ** p < 0.05; *** p < 0.01.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Mean | Median | S.D. | Min | Max |

|---|---|---|---|---|---|

| Latin American Home Country (dummy) | 0.121 | 0 | 0.326 | 0 | 1 |

| Developed Home Country (dummy) | 0.829 | 1 | 0.376 | 0 | 1 |

| Subsidiary Size (Total Assets) | 1,280,000 | 18,600 | 8,330,000 | 12 | 196,000,000 |

| Industry or Service (dummy) | 0.293 | 0 | 0.455 | 0 | 1 |

| DCD_PDI_L_H | 2.24 | 2.19 | 2.45 | 0 | 27.9 |

| DCD_PDI_H_L | 0.117 | 0 | 0.507 | 0 | 5.68 |

| DCD_IDV_L_H | 0.0125 | 0 | 0.0979 | 0 | 2 |

| DCD_IDV_H_L | 4.91 | 4.87 | 3.79 | 0 | 11.9 |

| DCD_MAS_L_H | 1.01 | 0.0144 | 2.1 | 0 | 12.5 |

| DCD_MAS_H_L | 0.333 | 0 | 0.987 | 0 | 7.61 |

| DCD_UAI_L_H | 1.61 | 0.539 | 2.06 | 0 | 12.4 |

| DCD_UAI_H_L | 0.0679 | 0 | 0.229 | 0 | 3.28 |

| FID—Government Effectiveness LH | 0.0712 | 0 | 0.525 | 0 | 9.05 |

| FID—Government Effectiveness HL | 5.53 | 6.05 | 3.59 | 0 | 27.1 |

| FID—Political Stability and Absence of Violence LH | 0.175 | 0 | 1.14 | 0 | 22.8 |

| FID—Political Stability and Absence of Violence HL | 8.7 | 7.73 | 6.49 | 0 | 28.6 |

| FID—Voice and Accountability LH | 0.277 | 0 | 1.49 | 0 | 21.6 |

| FID—Voice and Accountability HL | 3.73 | 3.86 | 2.51 | 0 | 14.9 |

| FID—Regulatory Quality LH | 0.213 | 0 | 1.19 | 0 | 18.3 |

| FID—Regulatory Quality HL | 2.73 | 1.95 | 3.44 | 0 | 31.8 |

| FID—Control of Corruption LH | 0.115 | 0 | 0.695 | 0 | 11.7 |

| FID—Control of Corruption HL | 4.06 | 4.37 | 3.29 | 0 | 15.1 |

| FID—Rule of Law LH | 0.0906 | 0 | 0.652 | 0 | 12.8 |

| FID—Rule of Law HL | 5.18 | 5.95 | 3.46 | 0 | 22.2 |

| Profit Margin | 9.77 | 7.52 | 23 | −100 | 100 |

| Industry Annual Growth | 0.0176 | 0.0169 | 0.0233 | −0.104 | 0.191 |

| Variables | Mean | Median | S.D. | Min | Max |

|---|---|---|---|---|---|

| Latin American Home Country (dummy) | 0 | 0 | 0 | 0 | 0 |

| Developed Home Country (dummy) | 1 | 1 | 0 | 1 | 1 |

| Subsidiary Size (Total Assets) | 1,240,000 | 15,500 | 8,720,000 | 12 | 196,000,000 |

| Industry or Service (dummy) | 0.291 | 0 | 0.454 | 0 | 1 |

| DCD_PDI_L_H | 2.56 | 3.02 | 2.26 | 0 | 17 |

| DCD_PDI_H_L | 0.00859 | 0 | 0.0895 | 0 | 1.5 |

| DCD_IDV_L_H | 0.00069 | 0 | 0.012 | 0 | 0.21 |

| DCD_IDV_H_L | 5.85 | 5.24 | 3.47 | 0 | 11.9 |

| DCD_MAS_L_H | 1 | 0.0144 | 2.18 | 0 | 12.5 |

| DCD_MAS_H_L | 0.335 | 0 | 1.02 | 0 | 7.61 |

| DCD_UAI_L_H | 1.63 | 0.734 | 1.89 | 0 | 12.1 |

| DCD_UAI_H_L | 0.0551 | 0 | 0.187 | 0 | 3.28 |

| FID—Government Effectiveness LH | 0.00792 | 0 | 0.113 | 0 | 1.86 |

| FID—Government Effectiveness HL | 6.35 | 6.38 | 3.16 | 0 | 27.1 |

| FID—Political Stability and Absence of Violence LH | 0.0389 | 0 | 0.25 | 0 | 2.31 |

| FID—Political Stability and Absence of Violence HL | 9.87 | 9.98 | 6.25 | 0 | 28.6 |

| FID—Voice and Accountability LH | 0.000787 | 0 | 0.00566 | 0 | 0.0749 |

| FID—Voice and Accountability HL | 4.29 | 3.98 | 2.29 | 0 | 14.9 |

| FID—Regulatory Quality LH | 0.0245 | 0 | 0.168 | 0 | 1.94 |

| FID—Regulatory Quality HL | 2.96 | 1.97 | 3.46 | 0 | 25.3 |

| FID—Control of Corruption LH | 0.0416 | 0 | 0.292 | 0 | 3.95 |

| FID—Control of Corruption HL | 4.62 | 4.61 | 3.16 | 0 | 15.1 |

| FID—Rule of Law LH | 0.0143 | 0 | 0.145 | 0 | 2.11 |

| FID—Rule of Law HL | 5.93 | 6.6 | 3.12 | 0 | 22.2 |

| Profit Margin | 10.1 | 7.93 | 23.1 | −100 | 100 |

| Industry Annual Growth | 0.0147 | 0.0144 | 0.0187 | −0.0592 | 0.164 |

| Variables | Mean | Median | S.D. | Min | Max |

|---|---|---|---|---|---|

| Latin American Home Country (dummy) | 0.708 | 1 | 0.455 | 0 | 1 |

| Developed Home Country (dummy) | 0 | 0 | 0 | 0 | 0 |

| Subsidiary Size (Total Assets) | 1,490,000 | 38,700 | 6,030,000 | 77.7 | 54,900,000 |

| Industry or Service (dummy) | 0.3 | 0 | 0.459 | 0 | 1 |

| DCD_PDI_L_H | 0.687 | 0 | 2.72 | 0 | 27.9 |

| DCD_PDI_H_L | 0.646 | 0.0663 | 1.06 | 0 | 5.68 |

| DCD_IDV_L_H | 0.0697 | 0 | 0.227 | 0 | 2 |

| DCD_IDV_H_L | 0.319 | 0.0849 | 0.581 | 0 | 3.2 |

| DCD_MAS_L_H | 1.04 | 0.176 | 1.64 | 0 | 7.28 |

| DCD_MAS_H_L | 0.324 | 0 | 0.81 | 0 | 4.66 |

| DCD_UAI_L_H | 1.47 | 0.00239 | 2.71 | 0 | 12.4 |

| DCD_UAI_H_L | 0.13 | 0 | 0.364 | 0 | 2.61 |

| FID—Government Effectiveness LH | 0.379 | 0 | 1.2 | 0 | 9.05 |

| FID—Government Effectiveness HL | 1.56 | 0.258 | 2.77 | 0 | 21.1 |

| FID—Political Stability and Absence of Violence LH | 0.836 | 0 | 2.61 | 0 | 22.8 |

| FID—Political Stability and Absence of Violence HL | 3.03 | 1.18 | 4.23 | 0 | 26.3 |

| FID—Voice and Accountability LH | 1.62 | 0 | 3.29 | 0 | 21.6 |

| FID—Voice and Accountability HL | 0.987 | 0.116 | 1.52 | 0 | 7.81 |

| FID—Regulatory Quality LH | 1.13 | 0.00725 | 2.67 | 0 | 18.3 |

| FID—Regulatory Quality HL | 1.59 | 0 | 3.14 | 0 | 31.8 |

| FID—Control of Corruption LH | 0.47 | 0 | 1.51 | 0 | 11.7 |

| FID—Control of Corruption HL | 1.33 | 0.00641 | 2.45 | 0 | 13.5 |

| FID—Rule of Law LH | 0.462 | 0 | 1.49 | 0 | 12.8 |

| FID—Rule of Law HL | 1.55 | 0.0842 | 2.59 | 0 | 15.7 |

| Profit Margin | 8.36 | 6 | 22.7 | −98.9 | 99.9 |

| Industry Annual Growth | 0.0327 | 0.0287 | 0.0353 | −0.104 | 0.191 |

| Variables | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Latin American Home Country (dummy) | −0.817 | −0.011 | 0.042 | −0.250 | 0.368 | 0.091 | −0.450 | 0.060 | −0.020 | −0.269 | 0.175 | 0.009 | 0.084 |

| Developed Home Country (dummy) | 1 | −0.011 | −0.007 | 0.288 | −0.474 | −0.265 | 0.549 | −0.006 | 0.004 | 0.030 | −0.124 | 0.027 | −0.287 |

| Subsidiary Size (Total Assets) | 1 | −0.043 | 0.029 | −0.022 | 0.021 | −0.112 | −0.002 | 0.018 | −0.023 | −0.004 | 0.081 | −0.001 | |

| Industry or Service (dummy) | 1 | −0.034 | 0.032 | 0.050 | −0.018 | −0.007 | 0.095 | −0.074 | 0.036 | −0.027 | −0.153 | ||

| DCD_PDI_L_H | 1 | −0.212 | −0.115 | 0.442 | 0.045 | −0.059 | 0.298 | −0.180 | 0.058 | 0.024 | |||

| DCD_PDI_H_L | 1 | 0.292 | −0.287 | −0.043 | −0.012 | −0.022 | 0.031 | −0.016 | 0.198 | ||||

| DCD_IDV_L_H | 1 | −0.165 | −0.053 | 0.105 | 0.072 | 0.024 | −0.027 | 0.151 | |||||

| DCD_IDV_H_L | 1 | −0.122 | −0.155 | 0.393 | −0.245 | −0.033 | −0.059 | ||||||

| DCD_MAS_L_H | 1 | −0.163 | 0.005 | 0.096 | −0.037 | −0.027 | |||||||

| DCD_MAS_H_L | 1 | 0.064 | 0.048 | 0.063 | −0.034 | ||||||||

| DCD_UAI_L_H | 1 | −0.232 | −0.017 | 0.266 | |||||||||

| DCD_UAI_H_L | 1 | −0.054 | −0.010 | ||||||||||

| Profit Margin | 1 | 0.001 | |||||||||||

| Industry Annual Growth | 1 |

| Variables | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Subsidiary Size (Total Assets) | −0.038 | 0.021 | −0.005 | 0.005 | −0.132 | 0.009 | 0.016 | −0.054 | 0.014 | 0.083 | 0.001 |

| Industry or Service (dummy) | 1 | −0.019 | −0.016 | 0.058 | −0.015 | 0.013 | 0.086 | −0.062 | 0.008 | −0.027 | −0.117 |

| DCD_PDI_L_H | 1 | −0.109 | −0.061 | 0.390 | 0.034 | −0.065 | 0.455 | −0.275 | 0.044 | 0.181 | |

| DCD_PDI_H_L | 1 | −0.006 | −0.124 | −0.022 | −0.020 | −0.080 | −0.027 | 0.089 | −0.034 | ||

| DCD_IDV_L_H | 1 | −0.097 | 0.004 | −0.019 | −0.050 | 0.560 | −0.044 | −0.052 | |||

| DCD_IDV_H_L | 1 | −0.149 | −0.197 | 0.546 | −0.297 | −0.059 | 0.167 | ||||

| DCD_MAS_L_H | 1 | −0.151 | 0.073 | 0.053 | −0.054 | −0.029 | |||||

| DCD_MAS_H_L | 1 | 0.054 | 0.114 | 0.068 | −0.057 | ||||||

| DCD_UAI_L_H | −0.254 | 0.003 | 0.220 | ||||||||

| DCD_UAI_H_L | 1 | −0.069 | −0.094 | ||||||||

| Profit Margin | 1 | 0.017 | |||||||||

| Industry Annual Growth | 1 |

| Variables | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Latin American Home Country (dummy) | −0.118 | 0.152 | −0.054 | −0.038 | −0.227 | −0.036 | 0.297 | −0.086 | −0.778 | 0.194 | 0.135 | −0.468 |

| Subsidiary Size (Total Assets) | 1 | −0.085 | 0.117 | −0.103 | 0.063 | −0.031 | −0.106 | 0.034 | 0.122 | −0.077 | 0.074 | −0.028 |

| Industry or Service (dummy) | 1 | −0.095 | 0.087 | 0.107 | −0.078 | −0.134 | 0.152 | −0.119 | 0.111 | −0.023 | −0.303 | |

| DCD_PDI_L_H | 1 | −0.154 | −0.075 | 0.379 | 0.135 | −0.055 | −0.124 | 0.091 | 0.087 | 0.012 | ||

| DCD_PDI_H_L | 1 | 0.201 | −0.198 | −0.152 | −0.025 | 0.007 | −0.043 | −0.048 | 0.124 | |||

| DCD_IDV_L_H | 1 | −0.169 | −0.177 | 0.333 | 0.162 | −0.088 | −0.040 | 0.132 | ||||

| DCD_IDV_H_L | 1 | −0.047 | −0.161 | −0.144 | 0.158 | −0.120 | −0.169 | |||||

| DCD_MAS_L_H | 1 | −0.254 | −0.299 | 0.274 | 0.078 | −0.050 | ||||||

| DCD_MAS_H_L | 1 | 0.116 | −0.143 | 0.028 | 0.041 | |||||||

| DCD_UAI_L_H | 1 | −0.194 | −0.090 | 0.414 | ||||||||

| DCD_UAI_H_L | 1 | −0.012 | 0.010 | |||||||||

| Profit Margin | 1 | −0.021 | ||||||||||

| Industry Annual Growth | 1 |

| Variables | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Subsidiary Size (Total Assets) | −0.038 | 0.047 | −0.042 | −0.01 | −0.113 | 0.033 | −0.072 | 0.067 | 0.019 | 0.058 | −0.028 | 0.057 | −0.041 | 0.083 | 0.001 |

| Industry or Service (dummy) | 1 | 0.084 | −0.043 | 0.004 | −0.08 | 0.066 | −0.061 | 0.138 | 0.038 | 0.113 | −0.038 | 0.105 | −0.055 | −0.027 | −0.117 |

| FID—Government Effectiveness LH | 1 | −0.141 | −0.008 | −0.111 | 0.386 | −0.132 | 0.62 | −0.06 | 0.846 | −0.103 | 0.932 | −0.134 | 0.093 | −0.095 | |

| FID—Government Effectiveness HL | 1 | −0.227 | 0.486 | −0.249 | 0.687 | −0.292 | 0.666 | −0.273 | 0.838 | −0.198 | 0.873 | −0.026 | 0.219 | ||

| FID—Political Stability and Absence of Violence LH | 1 | −0.246 | 0.573 | −0.29 | 0.05 | −0.096 | 0.268 | −0.227 | 0.008 | −0.264 | 0.05 | −0.065 | |||

| FID—Political Stability and Absence of Violence HL | 1 | −0.219 | 0.806 | −0.23 | 0.031 | −0.225 | 0.684 | −0.156 | 0.577 | −0.114 | 0.151 | ||||

| FID—Voice and Accountability LH | 1 | −0.26 | 0.447 | −0.111 | 0.624 | −0.203 | 0.35 | −0.257 | 0.1 | −0.184 | |||||

| FID—Voice and Accountability HL | 1 | −0.273 | 0.388 | −0.267 | 0.818 | −0.185 | 0.782 | −0.089 | 0.158 | ||||||

| FID—Regulatory Quality LH | 1 | −0.125 | 0.855 | −0.214 | 0.788 | −0.277 | 0.113 | −0.109 | |||||||

| FID—Regulatory Quality HL | 1 | −0.12 | 0.588 | −0.085 | 0.694 | 0.067 | 0.102 | ||||||||

| FID—Control of Corruption LH | 1 | −0.209 | 0.909 | −0.269 | 0.122 | −0.102 | |||||||||

| FID—Control of Corruption HL | 1 | −0.145 | 0.915 | 0.007 | 0.195 | ||||||||||

| FID—Rule of Law LH | 1 | −0.187 | 0.1 | −0.084 | |||||||||||

| FID—Rule of Law HL | 1 | −0.001 | 0.203 | ||||||||||||

| Profit Margin | 1 | 0.017 | |||||||||||||

| Industry Annual Growth | 1 |

| Variables | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Latin American Home Country (dummy) | −0.118 | 0.152 | −0.059 | −0.185 | −0.065 | 0.020 | −0.641 | 0.312 | −0.178 | −0.020 | 0.052 | 0.016 | −0.036 | −0.006 | 0.135 | −0.468 |

| Subsidiary Size (Total Assets) | 1 | −0.085 | 0.029 | 0.199 | 0.019 | 0.049 | −0.014 | −0.041 | −0.039 | 0.209 | 0.004 | 0.155 | −0.003 | 0.177 | 0.074 | −0.028 |

| Industry or Service (dummy) | 1 | 0.074 | −0.118 | 0.056 | −0.160 | −0.019 | −0.116 | −0.039 | −0.028 | 0.121 | −0.118 | 0.091 | −0.131 | −0.023 | −0.303 | |

| FID—Government Effectiveness LH | 1 | −0.178 | 0.435 | −0.208 | 0.216 | −0.203 | 0.734 | −0.160 | 0.786 | −0.172 | 0.950 | −0.188 | −0.002 | −0.108 | ||

| FID—Government Effectiveness HL | 1 | −0.149 | 0.660 | −0.206 | 0.412 | −0.229 | 0.768 | −0.175 | 0.854 | −0.174 | 0.917 | 0.020 | −0.028 | |||

| FID—Political Stability and Absence of Violence LH | 1 | −0.230 | 0.199 | −0.206 | 0.154 | −0.106 | 0.561 | −0.164 | 0.456 | −0.170 | 0.051 | −0.052 | ||||

| FID—Political Stability and Absence of Violence HL | 1 | −0.287 | 0.497 | −0.187 | 0.333 | −0.220 | 0.726 | −0.206 | 0.693 | −0.007 | −0.064 | |||||

| FID—Voice and Accountability LH | 1 | −0.321 | 0.217 | −0.238 | 0.251 | −0.265 | 0.252 | −0.289 | −0.062 | 0.479 | ||||||

| FID—Voice and Accountability HL | 1 | −0.252 | 0.441 | −0.203 | 0.650 | −0.200 | 0.661 | 0.096 | −0.023 | |||||||

| FID—Regulatory Quality LH | 1 | −0.215 | 0.493 | −0.230 | 0.742 | −0.252 | −0.137 | −0.049 | ||||||||

| FID—Regulatory Quality HL | 1 | −0.158 | 0.635 | −0.157 | 0.738 | 0.079 | −0.015 | |||||||||

| FID—Control of Corruption LH | 1 | −0.170 | 0.870 | −0.186 | 0.013 | −0.159 | ||||||||||

| FID—Control of Corruption HL | 1 | −0.168 | 0.957 | 0.034 | −0.052 | |||||||||||

| FID—Rule of Law LH | 1 | −0.185 | 0.002 | −0.103 | ||||||||||||

| FID—Rule of Law HL | 1 | 0.061 | −0.062 | |||||||||||||

| Profit Margin | 1 | −0.021 | ||||||||||||||

| Industry Annual Growth | 1 |

| Full Sample CD (KS Index) | Full Sample DCD (LH-HL Directions) | Developed Country Sample CD (KS Index) | Developed Country Sample DCD (LH-HL Directions) | Emerging Market Sample CD (KS Index) | Emerging Market Sample DCD (LH-HL Directions) | |

|---|---|---|---|---|---|---|

| Const | 7.94 *** | 8.33 *** | 10.6 *** | 10.3 *** | 8.50 *** | 7.71 *** |

| (1.00) | (1.08) | (1.00) | (1.13) | (3.63) | (3.33) | |

| [0.000] | [0.000] | [0.000] | [0.000] | [0.019] | [0.021] | |

| Industry Annual Growth | 4.51 | 8.78 | 3.45 | 13.5 | −7.68 | −0.932 |

| (15.4) | (13.7) | (22.8) | (22.3) | (20.1) | (17.3) | |

| [0.770] | [0.521] | [0.880] | [0.544] | [0.703] | [0.957] | |

| Subsidiary Size (Total Assets) | 2.39 × 10−7 *** | 2.31 × 10−7 *** | 2.53 × 10−7 *** | 2.51 × 10−7 *** | 3.18 × 10−7 | 3.67 × 10−7 *** |

| (5.39 × 10−8) | (4.26 × 10−8) | (5.01 × 10−8) | (4.21 × 10−8) | (2.04 × 10−7) | (1.33 × 10−7) | |

| [0.000] | [0.000] | [0.000] | [0.000] | [0.119] | [0.006] | |

| Industry or Service (dummy) | −0.566 | −1.09 | −0.323 | −0.612 | −0.476 | −0.837 |

| (0.729) | (0.687) | (0.791) | (0.769) | (1.65) | (1.37) | |

| [0.437] | [0.114] | [0.683] | [0.426] | [0.773] | [0.543] | |

| Developed Home Country (dummy) | 2.54 ** | 1.20 | ||||

| (1.20) | (1.25) | |||||

| [0.035] | [0.336] | |||||

| Latin American Home Country (dummy) | 0.199 | 1.63 | ||||

| (3.25) | (2.65) | |||||

| [0.951] | [0.539] | |||||

| CD_PDI_KS | 0.873 *** | 0.812 *** | 0.841 | |||

| (0.209) | (0.216) | (0.563) | ||||

| [0.000] | [0.000] | [0.136] | ||||

| DCD_PDI_LH | 1.17 *** | 0.801 *** | 1.82 *** | |||

| (0.201) | (0.212) | (0.297) | ||||

| [0.000] | [0.000] | [0.000] | ||||

| DCD_PDI_HL | 0.440 | 29.5 ** | −0.638 | |||

| (0.735) | (14.1) | (0.785) | ||||

| [0.549] | [0.036] | [0.416] | ||||

| CD_IDV_KS | −0.382 *** | −0.419 *** | −4.38 *** | |||

| (0.136) | (0.134) | (1.20) | ||||

| [0.005] | [0.002] | [0.000] | ||||

| DCD_IDV_LH | 2.01 | 54.9 | 2.35 | |||

| (7.77) | (95.6) | (7.36) | ||||

| [0.796] | [0.565] | [0.749] | ||||

| DCD_IDV_HL | −0.295 ** | −0.431 *** | −4.25 *** | |||

| (0.133) | (0.142) | (1.22) | ||||

| [0.027] | [0.002] | [0.001] | ||||

| CD_MAS_KS | −0.133 | −0.310 ** | 0.885 | |||

| (0.156) | (0.151) | (0.698) | ||||

| [0.394] | [0.040] | [0.205] | ||||

| DCD_MAS_LH | −0.332 ** | −0.481 *** | 0.576 | |||

| (0.134) | (0.137) | (0.642) | ||||

| [0.014] | [0.000] | [0.369] | ||||

| DCD_MAS_HL | 2.05 *** | 1.87 *** | 2.63 * | |||

| (0.434) | (0.461) | (1.37) | ||||

| [0.000] | [0.000] | [0.055] | ||||

| CD_UAI_KS | −0.353 ** | −0.205 | −0.650 | |||

| (0.174) | (0.210) | (0.474) | ||||

| [0.043] | [0.327] | [0.171] | ||||

| DCD_UAI_LH | −0.734 *** | −0.124 | −0.693 * | |||

| (0.141) | (0.236) | (0.388) | ||||

| [0.000] | [0.600] | [0.075] | ||||

| DCD_UAI_HL | −4.65 *** | −12.5 *** | −1.38 | |||

| (1.45) | (3.31) | (1.31) | ||||

| [0.001] | [0.000] | [0.293] | ||||

| N | 4226 | 4226 | 3545 | 3545 | 681 | 681 |

| Adj. R2 | 0.010 | 0.030 | 0.013 | 0.032 | 0.029 | 0.118 |

| p-value (F) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Variables | Voice and Accountability | Political Stability and Absence of Violence | Government Effectiveness | Regulatory Quality | Rule of Law | Control of Corruption |

|---|---|---|---|---|---|---|

| Const | 11.6 *** | 11.8 *** | 11.3 *** | 8.23 *** | 9.58 *** | 8.82 *** |

| (0.959) | (0.900) | (0.897) | (0.657) | (0.892) | (0.782) | |

| [0.000] | [0.000] | [0.000] | [0.000] | [0.000] | [0.000] | |

| Industry Annual Growth | 37.1 * | 43.9 ** | 28.4 | 20.6 | 16.9 | 15.3 |

| (22.0) | (21.1) | (22.4) | (21.6) | (22.0) | (21.8) | |

| [0.092] | [0.037] | [0.206] | [0.340] | [0.443] | [0.483] | |

| Subsidiary Size (Total Assets) | 2.79 × 10−7 *** | 2.44 × 10−7 *** | 2.60 × 10−7 *** | 2.40 × 10−7 *** | 2.46 × 10−7 *** | 2.30 × 10−7 *** |

| (4.92 × 10−8) | (4.55 × 10−8) | (5.11 × 10−8) | (4.20 × 10−8) | (4.97 × 10−8) | (4.03 × 10−8) | |

| [0.000] | [0.000] | [0.000] | [0.000] | [0.000] | [0.000] | |

| Industry or Service (dummy) | −1.36 * | −1.06 | −1.56 ** | −1.80 ** | −1.84 ** | −1.74 ** |

| (0.774) | (0.776) | (0.792) | (0.810) | (0.793) | (0.789) | |

| [0.078] | [0.174] | [0.049] | [0.026] | [0.021] | [0.027] | |

| FID—Voice and Accountability LH | 345 *** | |||||

| −114 | ||||||

| [0.002] | ||||||

| FID—Voice and Accountability HL | −0.547 *** | |||||

| (0.156) | ||||||

| [0.000] | ||||||

| FID—Political Stability and Absence of Violence LH | 3.11 | |||||

| (2.68) | ||||||

| [0.246] | ||||||

| FID—Political Stability and Absence of Violence HL | −0.263 *** | |||||

| (0.0560) | ||||||

| [0.000] | ||||||

| FID—Government Effectiveness LH | 19.9 ** | |||||

| (10.0) | ||||||

| [0.048] | ||||||

| FID—Government Effectiveness HL | −0.265 ** | |||||

| (0.109) | ||||||

| [0.015] | ||||||

| FID—Regulatory Quality LH | 18.8 *** | |||||

| (4.19) | ||||||

| [0.000] | ||||||

| FID—Regulatory Quality HL | 0.453 *** | |||||

| (0.144) | ||||||

| [0.002] | ||||||

| FID—Rule of Law LH | 24.4 *** | |||||

| (6.10) | ||||||

| [0.000] | ||||||

| FID—Rule of Law HL | 0.0379 | |||||

| (0.116) | ||||||

| [0.745] | ||||||

| FID—Control of Corruption LH | 11.8 *** | |||||

| (3.04) | ||||||

| [0.000] | ||||||

| FID—Control of Corruption HL | 0.175 | |||||

| (0.121) | ||||||

| [0.148] | ||||||

| N | 3545 | 3545 | 3545 | 3545 | 3545 | 3545 |

| Adj. R2 | 0.017 | 0.018 | 0.011 | 0.018 | 0.012 | 0.014 |

| p-value (F) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Variables | Voice and Accountability | Political Stability and Absence of Violence | Government Effectiveness | Regulatory Quality | Rule of Law | Control of Corruption |

|---|---|---|---|---|---|---|

| Const | 4.33 *** | 3.29 *** | 2.73 *** | 4.41 *** | 3.26 *** | 3.47 *** |

| (1.10) | (1.08) | (0.897) | (1.08) | (1.01) | (1.03) | |

| [0.000] | [0.002] | [0.002] | [0.000] | [0.001] | [0.001] | |

| Industry Annual Growth | 23.4 ** | 25.5 ** | 33.3 *** | 18.3 | 21.2 * | 21.7 * |

| (11.6) | (11.0) | (10.0) | (11.2) | (11.1) | (11.2) | |

| [0.043] | [0.020] | [0.001] | [0.105] | [0.057] | [0.054] | |

| Subsidiary Size (Total Assets) | −5.57 × 10−8 | −5.27 × 10−8 | −2.95 × 10−8 | −5.31 × 10−8 | −5.74 × 10−8 | −6.11 × 10−8 * |

| (3.66 × 10−8) | (3.47 × 10−8) | (2.80 × 10−8) | (3.98 × 10−8) | (3.52 × 10−8) | (3.57 × 10−8) | |

| [0.128] | [0.130] | [0.292] | [0.183] | [0.104] | [0.088] | |

| Industry or Service (dummy) | −0.130 | −0.0766 | 0.0416 | −0.211 | 0.165 | −0.198 |

| (0.758) | (0.770) | (0.631) | (0.771) | (0.742) | (0.761) | |

| [0.864] | [0.921] | [0.947] | [0.784] | [0.825] | [0.795] | |

| Latin America Home Country (dummy) | 2.12 ** | 2.67 *** | 3.59 *** | 2.36 *** | 3.01 *** | 2.82 *** |

| (1.04) | (0.875) | (0.763) | (0.881) | (0.829) | (0.847) | |

| [0.042] | [0.002] | [0.000] | [0.008] | [0.000] | [0.001] | |

| FID—Voice and Accountability LH | −0.103 | |||||

| (0.0697) | ||||||

| [0.140] | ||||||

| FID—Voice and Accountability HL | 0.00485 | |||||

| (0.221) | ||||||

| [0.982] | ||||||

| FID—Political Stability and Absence of Violence LH | 0.00427 | |||||

| (0.0631) | ||||||

| [0.946] | ||||||

| FID—Political Stability and Absence of Violence HL | 0.122 | |||||

| (0.0825) | ||||||

| [0.139] | ||||||

| FID—Government Effectiveness LH | −0.423 *** | |||||

| (0.0881) | ||||||

| [0.000] | ||||||

| FID—Government Effectiveness HL | 0.0405 | |||||

| (0.105) | ||||||

| [0.701] | ||||||

| FID—Regulatory Quality LH | −0.257* | |||||

| (0.139) | ||||||

| [0.066] | ||||||

| FID—Regulatory Quality HL | 0.0751 | |||||

| (0.0745) | ||||||

| [0.313] | ||||||

| FID—Rule of Law LH | −0.327 *** | |||||

| (0.0974) | ||||||

| [0.001] | ||||||

| FID—Rule of Law HL | 0.214 *** | |||||

| (0.0674) | ||||||

| [0.002] | ||||||

| FID—Control of Corruption LH | −0.207 | |||||

| (0.317) | ||||||

| [0.515] | ||||||

| FID—Control of Corruption HL | 0.180 ** | |||||

| (0.0789) | ||||||

| [0.023] | ||||||

| N | 533 | 533 | 533 | 533 | 533 | 533 |

| Adj. R2 | 0.038 | 0.037 | 0.394 | 0.037 | 0.130 | 0.034 |

| p-value (F) | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Correa da Cunha, H.; Amal, M.; Viminitz, J.M. Formal vs. Informal Institutional Distances and the Competitive Advantage of Foreign Subsidiaries in Latin America. Economies 2022, 10, 114. https://doi.org/10.3390/economies10050114

Correa da Cunha H, Amal M, Viminitz JM. Formal vs. Informal Institutional Distances and the Competitive Advantage of Foreign Subsidiaries in Latin America. Economies. 2022; 10(5):114. https://doi.org/10.3390/economies10050114

Chicago/Turabian StyleCorrea da Cunha, Henrique, Mohamed Amal, and James Mark Viminitz. 2022. "Formal vs. Informal Institutional Distances and the Competitive Advantage of Foreign Subsidiaries in Latin America" Economies 10, no. 5: 114. https://doi.org/10.3390/economies10050114

APA StyleCorrea da Cunha, H., Amal, M., & Viminitz, J. M. (2022). Formal vs. Informal Institutional Distances and the Competitive Advantage of Foreign Subsidiaries in Latin America. Economies, 10(5), 114. https://doi.org/10.3390/economies10050114