Past, Present, and Future Research Trajectories on Retail Investor Behaviour: A Composite Bibliometric Analysis and Literature Review

Abstract

1. Introduction

2. The Evolution of the Retail Investor Terminology

3. Methodology

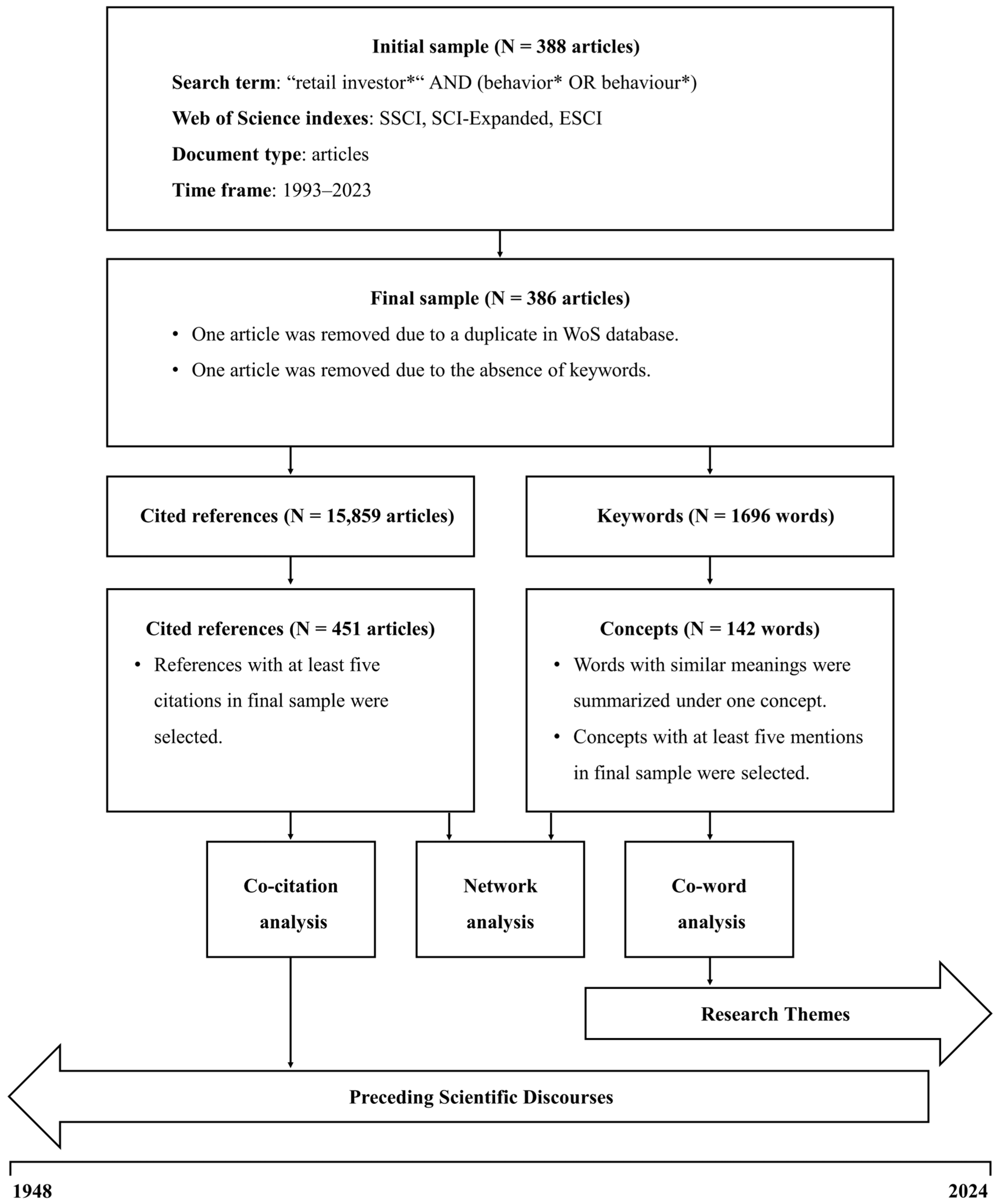

3.1. Sample Selection Process

3.2. Data Pre-Processing

3.3. Analysis Methods

3.3.1. Co-Word Analysis

3.3.2. Co-Citation Analysis

3.3.3. Network Analysis

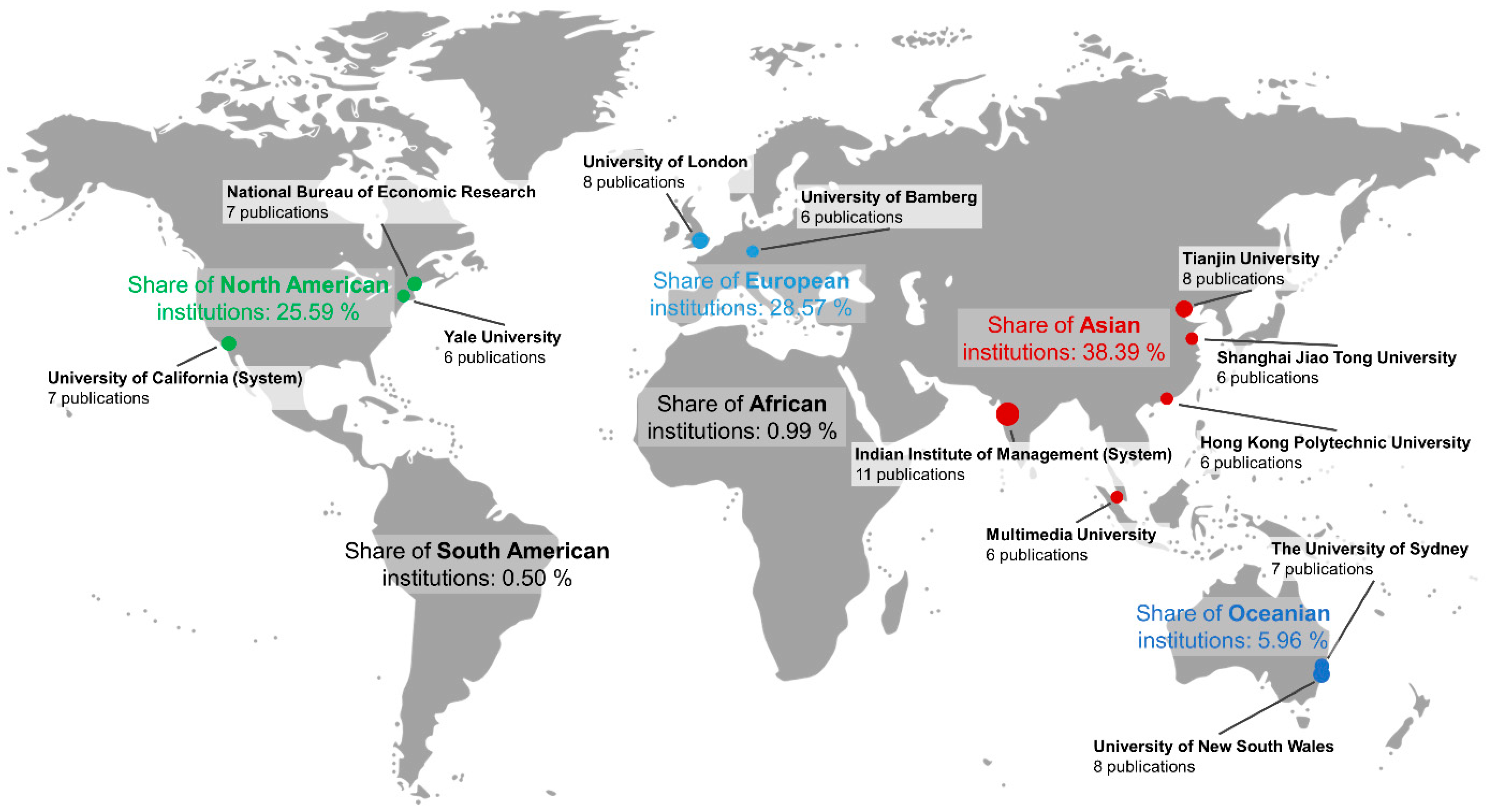

4. Descriptive Summary of Literature on Retail Investor Behaviour

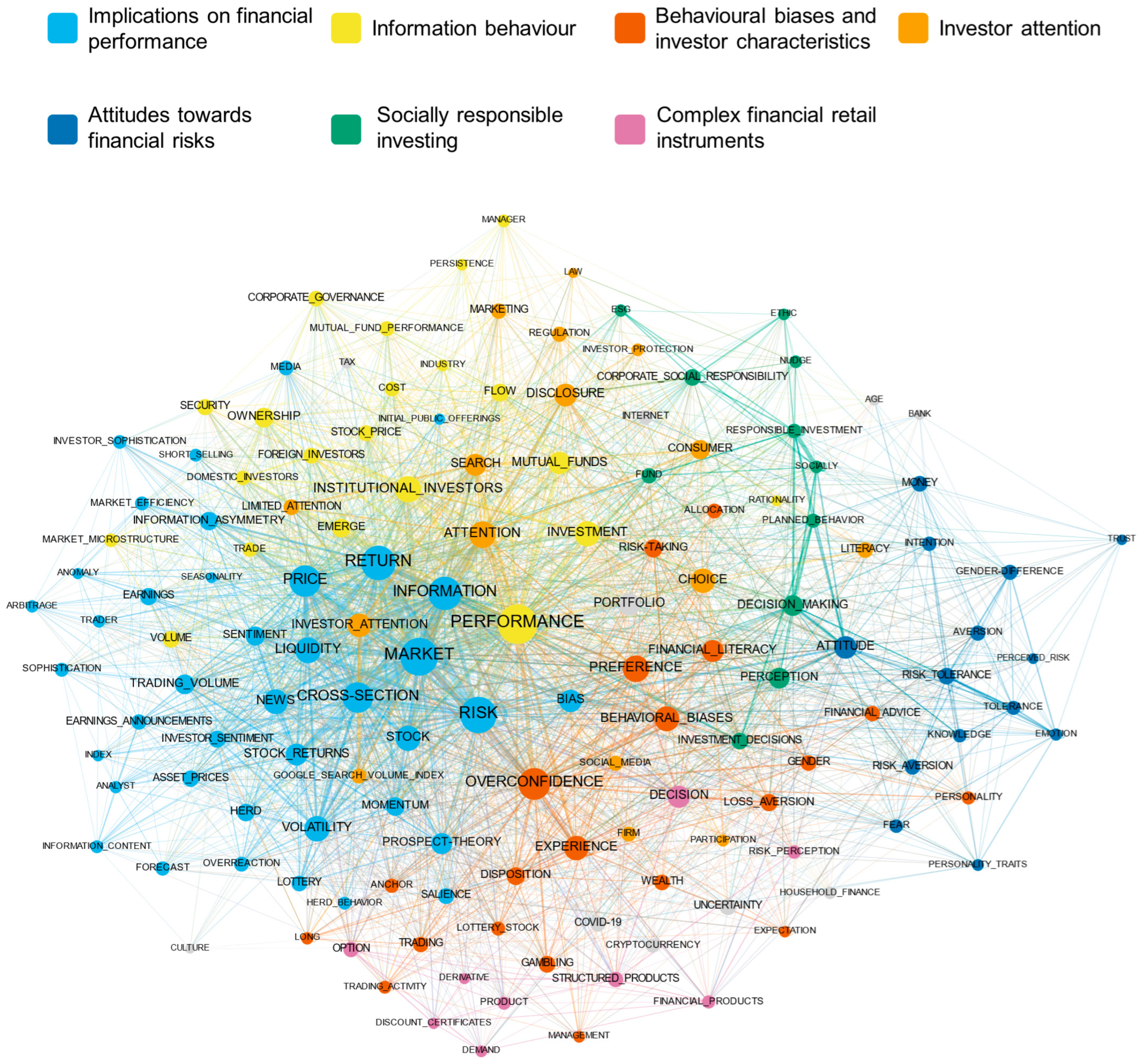

5. Past and Present Trajectories of Research on Retail Investor Behaviour

5.1. Implications on Financial Performance

5.1.1. Preceding Scientific Discourses on Implications for Financial Performance

5.1.2. Research Theme 1: Implications on Financial Performance

5.2. Information Behaviour

5.2.1. Preceding Scientific Discourse on Information Behaviour

5.2.2. Research Theme 2: Information Behaviour

5.3. Behavioural Biases and Investor Characteristics

5.3.1. Preceding Scientific Discourses on Behavioural Biases and Investor Characteristics

5.3.2. Research Theme 3: Behavioural Biases and Investor Characteristics

5.4. Investor Attention

5.4.1. Preceding Scientific Discourse on Investor Attention

5.4.2. Research Theme 4: Investor Attention

5.5. Attitudes Towards Financial Risks

5.5.1. Preceding Scientific Discourse on Attitudes Towards Financial Risks

5.5.2. Research Theme 5: Attitudes Towards Financial Risks

5.6. Socially Responsible Investing

5.6.1. Preceding Scientific Discourse on Socially Responsible Investing

5.6.2. Research Theme 6: Socially Responsible Investing

5.7. Complex Financial Retail Instruments

5.7.1. Preceding Scientific Discourse on Complex Financial Retail Instruments

5.7.2. Research Theme 7: Complex Financial Retail Instruments

6. Network Analysis of the Co-Citation and Concept Co-Occurrence Networks

7. Avenues for Future Research

7.1. Future Research on “Implications on Financial Performance”

7.2. Future Research on “Information Behavior”

7.3. Future Research on “Behavioral Biases and Investor Characteristics”

7.4. Future Research on “Investor Attention”

7.5. Future Research on “Attitudes Towards Financial Risks”

7.6. Future Research on “Socially Responsible Investing”

7.7. Future Research on “Complex Financial Retail Instruments”

8. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| #Cited in References | Author(s) (Year) | Title | Journal | #Cited in WoS |

|---|---|---|---|---|

| 98 | Barber and Odean (2008) | All that glitters: The effect of attention andnews on the buying behavior of individualand institutional investors | Review of Financial Studies | 2140 |

| 57 | Barber and Odean (2000) | Trading is hazardous to your wealth: The common stock investment performance of individual investors | Journal of Finance | 1537 |

| 50 | Barber and Odean (2001) | Boys will be boys: Gender, overconfidence, and common stock investment | Quarterly Journal of Economics | 2313 |

| 48 | Da et al. (2011) | In search of attention | Journal of Finance | 1622 |

| 47 | Fama and French (1993) | Common risk factors in the returns on stocks and bonds | Journal of Financial Economics | 11,684 |

| 45 | Kahnemann and Tversky (1979) | Prospect Theory—Analysis of decision under risk | Econometrica | 30,894 |

| 43 | Odean (1999) | Do investors trade too much? | American Economic Review | 883 |

| 41 | Carhart (1997) | On persistence in mutual fund performance | Journal of Finance | 7508 |

| 41 | Odean (1998) | Are investors reluctant to realize their losses? | Journal of Finance | 1499 |

| 40 | Kumar (2009) | Who gambles in the stock market? | Journal of Finance | 803 |

| 34 | Shefrin and Statman (1985) | The disposition to sell winners too early and ride losers too long: Theory and evidence | Journal of Finance | 1364 |

| 33 | Barber et al. (2009) | Do Retail Trades Move Markets? | Review of Financial Studies | 411 |

| 33 | Grinblatt and Keloharju (2000) | The investment behavior and performance of various investor types: a study of Finland’s unique data set | Journal of Financial Economics | 759 |

| 32 | A. Kumar and Lee (2006) | Retail investor sentiment and return comovements | Journal of Finance | 715 |

| 31 | Barber et al. (2009) | Just how much do individual investors lose by trading? | Review of Financial Studies | 493 |

| 30 | de Long et al. (1990) | Noise trader risk in financial markets | Journal of Political Economy | 2722 |

| 28 | Baker and Wurgler (2006) | Investor sentiment and the cross-section of stock returns | Journal of Finance | 3042 |

| 28 | Daniel et al. (1998) | Investor psychology and security market under- and overreactions | Journal of Finance | 2430 |

| 27 | Tversky and Kahnemann (1974) | Judgement under uncertainty—heuristics and biases | Science | 19,410 |

| 26 | Kaniel et al. (2008) | Individual investor trading and stock returns | Journal of Finance | 460 |

| 25 | Barber and Odean (2013) | The behavior of individual investors | Handbook of the Economics in Finance | n.n. 1 |

| 24 | Fama and Macbeth (1973) | Risk, return, and equilibrium: Empirical tests | Journal of Political Economy | 6194 |

| 24 | Grinblatt and Keloharju (2001) | What makes investors trade? | Journal of Finance | 532 |

| 23 | Jegadeesh and Titman (1993) | Returns to buying winners and selling losers: Implications for stock market efficiency | Journal of Finance | 4656 |

| 23 | Nofsinger and Sias (1999) | Herding and feedback trading by institutional and individual investors | Journal of Finance | 754 |

| 21 | Amihud (2002) | Illiquidity and stock returns: cross-section and time-series effects | Journal of Financial Markets | 4731 |

| 21 | Newey and Powell (1987) | Asymmetric least squares estimation and testing | Econometrica | 638 |

| 20 | Gervais and Odean (2001) | Learning to be overconfident | Review of Financial Studies | 713 |

| 20 | Kyle (1985) | Continuous auctions and insider trading | Econometrica | 4122 |

| 20 | Merton (1987) | A simple model of capital market equilibrium with incomplete information | Journal of Finance | 2602 |

| 18 | Black (1986) | Noise | Journal of Finance | 1411 |

| 18 | Lakonishok et al. (1992) | The impact of institutional trading on stock prices | Journal of Financial Economics | 907 |

| 18 | Griffin et al. (2003) | The dynamics of institutional and individual trading | Journal of Finance | 253 |

| 18 | Grullon et al. (2004) | Advertising, breadth of ownership, and liquidity | Review of Financial Studies | 437 |

| 17 | Bali et al. (2011) | Maxing out: Stocks as lotteries and the cross-section of expected returns | Journal of Financial Economics | 774 |

| 17 | Barberis et al. (1998) | A model of investor sentiment | Journal of Financial Economics | 2193 |

| 17 | Foucault et al. (2011) | Individual investors and volatility | Journal of Finance | 184 |

| 17 | Grinblatt and Keloharju (2009) | Sensation seeking, overconfidence, and trading activity | Journal of Finance | 380 |

| 17 | Schleifer and Vishny (1997) | The limits of arbitrage | Journal of Finance | 2065 |

| 17 | Seasholes and Wu (2007) | Predictable behavior, profits, and attention | Journal of Empirical Finance | n.n. 1 |

| 16 | Barber et al. (2009) | Systematic noise | Journal of Financial Markets | 206 |

| 16 | Barberis and Huang (2008) | Stocks as lotteries: The implications of probability weighting for security prices | American Economic Review | 705 |

| 16 | Hvidkjaer (2008) | Small trades and the cross-section of stock returns | Review of Financial Studies | 178 |

| 16 | Tversky and Kahneman (1992) | Advances in prospect theory: Cumulative representation of uncertainty | Journal of Risk and Uncertainty | 8535 |

| 15 | Grinblatt et al. (1995) | Momentum investment strategies, portfolio performance, and herding: A study of mutual fund behavior | Journal of Finance | 849 |

| 15 | Peng and Xiong (2006) | Investor attention, overconfidence and category learning | Journal of Financial Economics | 689 |

| 15 | Seru et al. (2010) | Learning by trading | Review of Financial Studies | 234 |

| 14 | Fama and French (2015) | A five-factor asset pricing model | Journal of Financial Economics | 3298 |

| 14 | Gervais et al. (2001) | The high-volume return premium | Journal of Finance | 418 |

| 14 | Han and Kumar (2013) | Speculative retail trading and asset prices | Journal of Financial and Quantitative Analysis | 218 |

| 14 | Wermers (1999) | Mutual fund herding and the impact on stock prices | Journal of Finance | 777 |

| 11 | Ang et al. (2006) | The cross-section of volatility and expected returns | Journal of Financial Markets | 2061 |

| 11 | Hong and Stein (1999) | A unified theory of underreaction, momentum trading, and overreaction in asset markets | Journal of Finance | 1768 |

| 11 | Pástor and Stambaugh (2003) | Liquidity risk and expected stock returns | Journal of Political Economy | 2323 |

| 10 | Grinblatt and Han (2005) | Prospect theory, mental accounting, and momentum | Journal of Financial Economics | 440 |

References

- Abreu, M. (2019). How biased is the behavior of the individual investor in warrants? Research in International Business and Finance, 47, 139–149. [Google Scholar] [CrossRef]

- Abreu, M., & Mendes, V. (2012). Information, overconfidence and trading: Do the sources of information matter? Journal of Economic Psychology, 33(4), 868–881. [Google Scholar] [CrossRef]

- Abreu, M., & Mendes, V. (2018). The investor in structured retail products: Advice driven or gambling oriented? Journal of Behavioral and Experimental Finance, 17, 1–9. [Google Scholar] [CrossRef]

- Ahn, Y. (2022). The anatomy of the disposition effect: Which factors are most important? Finance Research Letters, 44, 102040. [Google Scholar] [CrossRef]

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. [Google Scholar] [CrossRef]

- Ajzen, I. (2002). Constructing a TPB questionnaire: Conceptual and methodological considerations. University of Massachusetts. Available online: https://people.umass.edu/aizen/pdf/tpb.measurement.pdf (accessed on 4 March 2025).

- Alexander, G. J., Jones, J. D., & Nigro, P. J. (1998). Mutual fund shareholders: Characteristics, investor knowledge, and sources of information. Financial Services Review, 7(4), 301–316. [Google Scholar] [CrossRef]

- Alqudah, M., Ferruz, L., Martín, E., Qudah, H., & Hamdan, F. (2023). The sustainability of investing in cryptocurrencies: A bibliometric analysis of research trends. International Journal of Financial Studies, 11(3), 93. [Google Scholar] [CrossRef]

- Al-Somali, S. A., Gholami, R., & Clegg, B. (2009). An investigation into the acceptance of online banking in Saudi Arabia. Technovation, 29(2), 130–141. [Google Scholar] [CrossRef]

- Andriosopoulos, D., Steliaros, M., & Thomas, D. C. (2015). The short-term impact of director trading in UK closed-end funds. The European Journal of Finance, 21(8), 672–690. [Google Scholar] [CrossRef]

- Ansari, Y., Albarrak, M. S., Sherfudeen, N., & Aman, A. (2022). A study of financial literacy of investors—A bibliometric analysis. International Journal of Financial Studies, 10(2), 36. [Google Scholar] [CrossRef]

- Aouadi, A., Arouri, M., & Teulon, F. (2013). Investor attention and stock market activity: Evidence from France. Economic Modelling, 35, 674–681. [Google Scholar] [CrossRef]

- Armitage, C. J., & Conner, M. (2001). Efficacy of the theory of planned behaviour: A meta-analytic review. British Journal of Social Psychology, 40(4), 471–499. [Google Scholar] [CrossRef] [PubMed]

- Arnold, M., Pelster, M., & Subrahmanyam, M. G. (2022). Attention triggers and investors’ risk-taking. Journal of Financial Economics, 143(2), 846–875. [Google Scholar] [CrossRef]

- Arora, N., & Mishra, B. K. (2023). Influence of bull and bear market phase on financial risk tolerance of urban individual investors in an emerging economy. Review of Behavioral Finance, 15(4), 570–591. [Google Scholar] [CrossRef]

- Arribas, I., Espinós-Vañó, M. D., García García, F., & Oliver-Muncharaz, J. (2019). Defining socially responsible companies according to retail investors’ preferences. Entrepreneurship and Sustainability Issues, 7(2), 1641–1653. [Google Scholar] [CrossRef]

- Atilgan, Y., Bali, T. G., Demirtas, K. O., & Gunaydin, A. D. (2020). Left-tail momentum: Underreaction to bad news, costly arbitrage, and equity returns. Journal of Financial Economics, 135(3), 725–753. [Google Scholar] [CrossRef]

- Baars, M., & Mohrschladt, H. (2021). An alternative behavioral explanation for the MAX effect. Journal of Economic Behavior & Organization, 191, 868–886. [Google Scholar] [CrossRef]

- Badrinath, S. G., & Wahal, S. (2002). Momentum trading by institutions. The Journal of Finance, 57(6), 2449–2478. [Google Scholar] [CrossRef]

- Bae, K. H., & Dixon, P. (2018). Do investors use options and futures to trade on different types of information? Evidence from an aggregate stock index. Journal of Futures Markets, 38(2), 175–198. [Google Scholar] [CrossRef]

- Baker, H. K., Kumar, S., Goyal, N., & Gaur, V. (2019). How financial literacy and demographic variables relate to behavioral biases. Managerial Finance, 45(1), 124–146. [Google Scholar] [CrossRef]

- Bakos, Y., Lucas, H. C., Jr., Oh, W., Simon, G., Viswanathan, S., & Weber, B. W. (2005). The impact of e-commerce on competition in the retail brokerage industry. Information Systems Research, 16(4), 352–371. [Google Scholar] [CrossRef]

- Baldwin, N. S., & Rice, R. E. (1997). Information-seeking behavior of securities analysts: Individual and institutional influences, information sources and channels, and outcomes. Journal of the American Society for Information Science, 48(8), 674–693. [Google Scholar] [CrossRef]

- Bali, T. G., Brown, S. J., Murray, S., & Tang, Y. (2017). A lottery-demand-based explanation of the beta anomaly. Journal of Financial and Quantitative Analysis, 52(6), 2369–2397. [Google Scholar] [CrossRef]

- Barber, B. M., Huang, X., Odean, T., & Schwarz, C. (2022). Attention-induced trading and returns: Evidence from Robinhood users. The Journal of Finance, 77(6), 3141–3190. [Google Scholar] [CrossRef]

- Barber, B. M., & Odean, T. (2000). Trading is hazardous to your wealth: The common stock investment performance of individual investors. The Journal of Finance, 55(2), 773–806. [Google Scholar] [CrossRef]

- Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261–292. [Google Scholar] [CrossRef]

- Barber, B. M., & Odean, T. (2008). All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. The Review of Financial Studies, 21(2), 785–818. [Google Scholar] [CrossRef]

- Barber, B. M., Odean, T., & Zheng, L. (2005). Out of sight, out of mind: The effects of expenses on mutual fund flows. The Journal of Business, 78(6), 2095–2120. [Google Scholar] [CrossRef]

- Barber, B. M., Odean, T., & Zhu, N. (2009). Systematic noise. Journal of Financial Markets, 12(4), 547–569. [Google Scholar] [CrossRef]

- Barberis, N., & Huang, M. (2008). Stocks as lotteries: The implications of probability weighting for security prices. American Economic Review, 98(5), 2066–2100. [Google Scholar] [CrossRef]

- Barberis, N., Huang, M., & Santos, T. (2001). Prospect theory and asset prices. The Quarterly Journal of Economics, 116(1), 1–53. [Google Scholar] [CrossRef]

- Barreda-Tarrazona, I., Matallín-Sáez, J. C., & Balaguer-Franch, M. R. (2011). Measuring investors’ socially responsible preferences in mutual funds. Journal of Business Ethics, 103, 305–330. [Google Scholar] [CrossRef]

- Bastian, M., Heymann, S., & Jacomy, M. (2009). Gephi: An open source software for exploring and manipulating networks. Proceedings of the International AAAI Conference on Web and Social Media, 3(1), 361–362. [Google Scholar] [CrossRef]

- Basu, A. K., & Dulleck, U. (2020). Why do (some) consumers purchase complex financial products? An experimental study on investment in hybrid securities. Economic Analysis and Policy, 67, 203–220. [Google Scholar] [CrossRef]

- Bazrafshan, E. (2023). The role of ESG ranking in retail and institutional investors’ attention and trading behavior. Finance Research Letters, 58, 104462. [Google Scholar] [CrossRef]

- Beal, D., Goyen, M., & Phillips, P. J. (2005). Why do we invest ethically? The Journal of Investing, 14(3), 66–77. [Google Scholar] [CrossRef]

- Behrendt, S., Peter, F. J., & Zimmermann, D. J. (2020). An encyclopedia for stock markets? Wikipedia searches and stock returns. International Review of Financial Analysis, 72, 101563. [Google Scholar] [CrossRef]

- Benveniste, L. M., & Wilhelm, W. J. (1990). A comparative analysis of IPO proceeds under alternative regulatory environments. Journal of Financial Economics, 28(1–2), 173–207. [Google Scholar] [CrossRef]

- Berk, J. B., & Green, R. C. (2004). Mutual fund flows and performance in rational markets. Journal of Political Economy, 112(6), 1269–1295. [Google Scholar] [CrossRef]

- Berkman, H., Koch, P., & Westerholm, P. J. (2023). The other insiders: Personal trading by brokers, analysts, and fund managers. The Review of Asset Pricing Studies, 13(3), 481–522. [Google Scholar] [CrossRef]

- Berkman, H., Koch, P. D., Tuttle, L., & Zhang, Y. J. (2012). Paying attention: Overnight returns and the hidden cost of buying at the open. Journal of Financial and Quantitative Analysis, 47(4), 715–741. [Google Scholar] [CrossRef]

- Bhatia, A., Chandani, A., Atiq, R., Mehta, M., & Divekar, R. (2021). Artificial intelligence in financial services: A qualitative research to discover robo-advisory services. Qualitative Research in Financial Markets, 13(5), 632–654. [Google Scholar] [CrossRef]

- Bihari, A., Dash, M., Muduli, K., Kumar, A., Mulat-Weldemeskel, E., & Luthra, S. (2023). Does cognitive biased knowledge influence investor decisions? An empirical investigation using machine learning and artificial neural network. VINE Journal of Information and Knowledge Management Systems, 1–15, ahead of print. [Google Scholar] [CrossRef]

- Black, F. (1986). Noise. The Journal of Finance, 41(3), 528–543. [Google Scholar] [CrossRef]

- Block, J. H., & Fisch, C. (2020). Eight tips and questions for your bibliographic study in business and management research. Management Review Quarterly, 70, 307–312. [Google Scholar] [CrossRef]

- Borgatti, S. P., & Everett, M. G. (2000). Models of core/periphery structures. Social Networks, 21(4), 375–395. [Google Scholar] [CrossRef]

- Borgatti, S. P., Everett, M. G., & Freeman, L. C. (2002). Ucinet for Windows: Software for social network analysis. Harvard, MA: Analytic Technologies, 6, 12–15. [Google Scholar]

- Brandt, M. W., Brav, A., Graham, J. R., & Kumar, A. (2010). The idiosyncratic volatility puzzle: Time trend or speculative episodes? The Review of Financial Studies, 23(2), 863–899. [Google Scholar] [CrossRef]

- Brennan, M. J. (1993). Aspects of insurance, intermediation and finance. The Geneva Papers on Risk and Insurance Theory, 18, 7–30. [Google Scholar] [CrossRef]

- Brenncke, M. (2018). The legal framework for financial advertising: Curbing behavioural exploitation. European Business Organization Law Review, 19(4), 853–882. [Google Scholar] [CrossRef]

- Broadus, R. N. (1987). Toward a definition of “bibliometrics”. Scientometrics, 12(5–6), 373–379. [Google Scholar] [CrossRef]

- Brooks, C., Sangiorgi, I., Hillenbrand, C., & Money, K. (2018). Why are older investors less willing to take financial risks? International Review of Financial Analysis, 56, 52–72. [Google Scholar] [CrossRef]

- Brooks, C., Sangiorgi, I., Hillenbrand, C., & Money, K. (2019). Experience wears the trousers: Exploring gender and attitude to financial risk. Journal of Economic Behavior & Organization, 163, 483–515. [Google Scholar] [CrossRef]

- Brooks, C., Sangiorgi, I., Saraeva, A., Hillenbrand, C., & Money, K. (2023). The importance of staying positive: The impact of emotions on attitude to risk. International Journal of Finance & Economics, 28(3), 3232–3261. [Google Scholar] [CrossRef]

- Brooks, C., & Williams, L. (2021). The impact of personality traits on attitude to financial risk. Research in International Business and Finance, 58, 101501. [Google Scholar] [CrossRef]

- Brooks, C., & Williams, L. (2022). When it comes to the crunch: Retail investor decision-making during periods of market volatility. International Review of Financial Analysis, 80, 102038. [Google Scholar] [CrossRef]

- Brown, K. C., Harlow, W. V., & Starks, L. T. (1996). Of tournaments and temptations: An analysis of managerial incentives in the mutual fund industry. The Journal of Finance, 51(1), 85–110. [Google Scholar] [CrossRef]

- Brunen, A. C., & Laubach, O. (2022). Do sustainable consumers prefer socially responsible investments? A study among the users of robo advisors. Journal of Banking & Finance, 136, 106314. [Google Scholar] [CrossRef]

- Bui, D. G., Hasan, I., Lin, C. Y., & Zhai, R. X. (2022). Income, trading, and performance: Evidence from retail investors. Journal of Empirical Finance, 66, 176–195. [Google Scholar] [CrossRef]

- Carlsson Hauff, J., & Nilsson, J. (2023). Is ESG mutual fund quality in the eye of the beholder? An experimental study of investor responses to ESG fund strategies. Business Strategy and the Environment, 32(4), 1189–1202. [Google Scholar] [CrossRef]

- Castellano, R., & Cerqueti, R. (2013). Roots and effects of financial misperception in a stochastic dominance framework. Quality & Quantity, 47, 3371–3389. [Google Scholar] [CrossRef]

- Castellano, R., & Cerqueti, R. (2018). A theory of misperception in a stochastic dominance framework and its application to structured financial products. IMA Journal of Management Mathematics, 29(1), 23–37. [Google Scholar] [CrossRef]

- Castillo-Vergara, M., Alvarez-Marin, A., & Placencio-Hidalgo, D. (2018). A bibliometric analysis of creativity in the field of business economics. Journal of Business Research, 85, 1–9. [Google Scholar] [CrossRef]

- Chan, K., & Kwok, J. K. (2005). Market segmentation and share price premium: Evidence from Chinese stock markets. Journal of Emerging Market Finance, 4(1), 43–61. [Google Scholar] [CrossRef]

- Chan, K. H., Chong, L. L., Ng, T. H., & Ong, W. L. (2022). A model of green investment decision making for societal well-being. Heliyon, 8(8), e10024. [Google Scholar] [CrossRef] [PubMed]

- Chan, Y. C. (2014). How does retail sentiment affect IPO returns? Evidence from the internet bubble period. International Review of Economics & Finance, 29, 235–248. [Google Scholar] [CrossRef]

- Chandra, A., Sanningammanavara, K., & Nandini, A. S. (2017). Does individual heterogeneity shape retail investor behaviour? International Journal of Social Economics, 44(5), 578–593. [Google Scholar] [CrossRef]

- Chen, H. L., Chow, E. H., & Shiu, C. Y. (2015). The informational role of individual investors in stock pricing: Evidence from large individual and small retail investors. Pacific-Basin Finance Journal, 31, 36–56. [Google Scholar] [CrossRef]

- Chen, X., Diao, X., & Wu, C. (2022). Heterogeneous investor attention and post earnings announcement drift: Evidence from China. Economic Modelling, 110, 105796. [Google Scholar] [CrossRef]

- Chevalier, J., & Ellison, G. (1997). Risk taking by mutual funds as a response to incentives. Journal of Political Economy, 105(6), 1167–1200. [Google Scholar] [CrossRef]

- Chhimwal, B., & Bapat, V. (2021). Comparative study of momentum and contrarian behavior of different investors: Evidence from the Indian Market. Asia-Pacific Financial Markets, 28(1), 19–53. [Google Scholar] [CrossRef]

- Chhimwal, B., Bapat, V., & Gaurav, S. (2021). Investors’ preferences and the factors affecting investment in the Indian stock market: An industry view. Managerial Finance, 47(5), 723–744. [Google Scholar] [CrossRef]

- Chiu, S. B., Hsu, J., Lai, H. K., & Wool, P. (2021). Market timing skill and trading activity in Taiwan’s retail-dominated futures market. The Journal of Portfolio Management, 47(7), 185–199. [Google Scholar] [CrossRef]

- Chui, A. C., Subrahmanyam, A., & Titman, S. (2022). Momentum, reversals, and investor clientele. Review of Finance, 26(2), 217–255. [Google Scholar] [CrossRef]

- Conlin, A., Kyröläinen, P., Kaakinen, M., Järvelin, M. R., Perttunen, J., & Svento, R. (2015). Personality traits and stock market participation. Journal of Empirical Finance, 33, 34–50. [Google Scholar] [CrossRef]

- Cornelli, F., Goldreich, D., & Ljungqvist, A. (2006). Investor sentiment and pre-IPO markets. The Journal of Finance, 61(3), 1187–1216. [Google Scholar] [CrossRef]

- Coronel-Pangol, K., Heras-Tigre, D., Jiménez Yumbla, J., Aguirre Quezada, J., & Mora, P. (2023). Microfinance, an Alternative for Financing Entrepreneurship: Implications and Trends-Bibliometric Analysis. International Journal of Financial Studies, 11(3), 83. [Google Scholar] [CrossRef]

- Da, Z., Engelberg, J., & Gao, P. (2011). In search of attention. The Journal of Finance, 66(5), 1461–1499. [Google Scholar] [CrossRef]

- de Long, J. B., Shleifer, A., Summers, L. H., & Waldmann, R. J. (1990). Positive feedback investment strategies and destabilizing rational speculation. The Journal of Finance, 45(2), 379–395. [Google Scholar] [CrossRef]

- Dilla, W., Janvrin, D., Perkins, J., & Raschke, R. (2016). Investor views, investment screen use, and socially responsible investment behavior. Sustainability Accounting, Management and Policy Journal, 7(2), 246–267. [Google Scholar] [CrossRef]

- Dimpfl, T., & Jank, S. (2016). Can internet search queries help to predict stock market volatility? European Financial Management, 22(2), 171–192. [Google Scholar] [CrossRef]

- Diouf, D., Hebb, T., & Touré, E. H. (2016). Exploring factors that influence social retail investors’ decisions: Evidence from Desjardins fund. Journal of Business Ethics, 134, 45–67. [Google Scholar] [CrossRef]

- Domina, M. (2023). Shall we play? Use of gamification techniques in investment services. European Company Law, 20(2), 49–52. [Google Scholar] [CrossRef]

- Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., & Lim, W. M. (2021). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133, 285–296. [Google Scholar] [CrossRef]

- Dorn, D., Huberman, G., & Sengmueller, P. (2008). Correlated trading and returns. The Journal of Finance, 63(2), 885–920. [Google Scholar] [CrossRef]

- Drake, M. S., Roulstone, D. T., & Thornock, J. R. (2012). Investor information demand: Evidence from Google searches around earnings announcements. Journal of Accounting Research, 50(4), 1001–1040. [Google Scholar] [CrossRef]

- Durand, R. B., Newby, R., & Sanghani, J. (2008). An intimate portrait of the individual investor. The Journal of Behavioral Finance, 9(4), 193–208. [Google Scholar] [CrossRef]

- Dwyer, P. D., Gilkeson, J. H., & List, J. A. (2002). Gender differences in revealed risk taking: Evidence from mutual fund investors. Economics Letters, 76(2), 151–158. [Google Scholar] [CrossRef]

- Ebers, A., & Thomsen, S. L. (2021). How do warnings affect retail demand for Bitcoin? Evidence from an international survey experiment. Journal of Behavioral and Experimental Finance, 32, 100567. [Google Scholar] [CrossRef]

- Entrop, O., Fischer, G., McKenzie, M., Wilkens, M., & Winkler, C. (2016a). How does pricing affect investors’ product choice? Evidence from the market for discount certificates. Journal of Banking & Finance, 68, 195–215. [Google Scholar] [CrossRef]

- Entrop, O., McKenzie, M., Wilkens, M., & Winkler, C. (2016b). The performance of individual investors in structured financial products. Review of Quantitative Finance and Accounting, 46, 569–604. [Google Scholar] [CrossRef]

- Evans, A. D. (2009). A requiem for the retail investor. Virginia Law Review, 95(4), 1105–1129. [Google Scholar]

- Evans, A. D. (2010). Do individual investors affect share price accuracy? Some preliminary evidence (Working Paper Series No. 75). The John M. Olin Center for Law and Economics at University of Michigan Law School. [Google Scholar] [CrossRef]

- Faff, R. W., Parwada, J. T., & Poh, H. L. (2007). The information content of Australian managed fund ratings. Journal of Business Finance & Accounting, 34(9–10), 1528–1547. [Google Scholar] [CrossRef]

- Fama, E. F., & MacBeth, J. D. (1973). Risk, return, and equilibrium: Empirical tests. Journal of Political Economy, 81(3), 607–636. [Google Scholar] [CrossRef]

- Fang, L., & Peress, J. (2009). Media coverage and the cross-section of stock returns. The Journal of Finance, 64(5), 2023–2052. [Google Scholar] [CrossRef]

- Faul, F., Erdfelder, E., Buchner, A., & Lang, A. G. (2009). Statistical power analyses using G* Power 3.1: Tests for correlation and regression analyses. Behavior Research Methods, 41(4), 1149–1160. [Google Scholar] [CrossRef] [PubMed]

- Figlewski, S. (1989). Options arbitrage in imperfect markets. The Journal of Finance, 44(5), 1289–1311. [Google Scholar] [CrossRef]

- FISMA. (2023). Retail investment strategy. Directorate-General for Financial Stability, Financial Services and Capital Markets Union. Available online: https://finance.ec.europa.eu/publications/retail-investment-strategy_en (accessed on 4 March 2025).

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. [Google Scholar] [CrossRef]

- Foucault, T., Sraer, D., & Thesmar, D. J. (2011). Individual investors and volatility. The Journal of Finance, 66(4), 1369–1406. [Google Scholar] [CrossRef]

- Frazzini, A., & Lamont, O. A. (2008). Dumb money: Mutual fund flows and the cross-section of stock returns. Journal of Financial Economics, 88(2), 299–322. [Google Scholar] [CrossRef]

- Froot, K. A., O’Connell, P. G., & Seasholes, M. S. (2001). The portfolio flows of international investors. Journal of Financial Economics, 59(2), 151–193. [Google Scholar] [CrossRef]

- Frydman, C., Hartzmark, S. M., & Solomon, D. H. (2018). Rolling mental accounts. The Review of Financial Studies, 31(1), 362–397. [Google Scholar] [CrossRef]

- Fushiya, H., Kitamura, T., & Nakasato, M. (2021). Structured product investment behavior in low-interest rate environments. The Journal of Risk Finance, 22(2), 113–129. [Google Scholar] [CrossRef]

- Gajewski, J. F., Heimann, M., & Meunier, L. (2022). Nudges in SRI: The power of the default option. Journal of Business Ethics, 177, 547–566. [Google Scholar] [CrossRef]

- Gamel, J., Menrad, K., & Decker, T. (2017). Which factors influence retail investors’ attitudes towards investments in renewable energies? Sustainable Production and Consumption, 12, 90–103. [Google Scholar] [CrossRef]

- Gao, Y., Xiong, X., & Feng, X. (2020). Responsible investment in the Chinese stock market. Research in International Business and Finance, 52, 101173. [Google Scholar] [CrossRef]

- Garfield, E., & Sher, I. H. (1993). Key words plus [TM]-algorithmic derivative indexing. Journal of the American Society for Information Science, 44, 298. [Google Scholar] [CrossRef]

- Garg, A., Goel, P., Sharma, A., & Rana, N. P. (2022). As you sow, so shall you reap: Assessing drivers of socially responsible investment attitude and intention. Technological Forecasting and Social Change, 184, 122030. [Google Scholar] [CrossRef]

- George, T. J., & Hwang, C. Y. (2004). The 52-week high and momentum investing. The Journal of Finance, 59(5), 2145–2176. [Google Scholar] [CrossRef]

- Gervais, S., & Odean, T. (2001). Learning to be overconfident. The Review of Financial Studies, 14(1), 1–27. [Google Scholar] [CrossRef]

- Ginsberg, J., Mohebbi, M. H., Patel, R. S., Brammer, L., Smolinski, M. S., & Brilliant, L. (2009). Detecting influenza epidemics using search engine query data. Nature, 457(7232), 1012–1014. [Google Scholar] [CrossRef] [PubMed]

- Glaser, M., & Weber, M. (2007). Overconfidence and trading volume. The Geneva Risk and Insurance Review, 32, 1–36. [Google Scholar] [CrossRef]

- Gong, P., & Dai, J. (2017). Monetary policy, exchange rate fluctuation, and herding behavior in the stock market. Journal of Business Research, 76, 34–43. [Google Scholar] [CrossRef]

- Goodell, J. W., Kumar, S., Li, X., Pattnaik, D., & Sharma, A. (2022). Foundations and research clusters in investor attention: Evidence from bibliometric and topic modelling analysis. International Review of Economics & Finance, 82, 511–529. [Google Scholar] [CrossRef]

- Gopi, M., & Ramayah, T. (2007). Applicability of theory of planned behavior in predicting intention to trade online: Some evidence from a developing country. International Journal of Emerging Markets, 2(4), 348–360. [Google Scholar] [CrossRef]

- Goyal, K., & Kumar, S. (2021). Financial literacy: A systematic review and bibliometric analysis. International Journal of Consumer Studies, 45(1), 80–105. [Google Scholar] [CrossRef]

- Grable, J. E. (2000). Financial risk tolerance and additional factors that affect risk taking in everyday money matters. Journal of Business and Psychology, 14, 625–630. [Google Scholar] [CrossRef]

- Graham, J. R., & Kumar, A. (2006). Do dividend clienteles exist? Evidence on dividend preferences of retail investors. The Journal of Finance, 61(3), 1305–1336. [Google Scholar] [CrossRef]

- Griffin, J. M., Harris, J. H., & Topaloglu, S. (2003). The dynamics of institutional and individual trading. The Journal of Finance, 58(6), 2285–2320. [Google Scholar] [CrossRef]

- Grinblatt, M., & Keloharju, M. (2009). Sensation seeking, overconfidence, and trading activity. The Journal of Finance, 64(2), 549–578. [Google Scholar] [CrossRef]

- Grinblatt, M., Titman, S., & Wermers, R. (1995). Momentum investment strategies, portfolio performance, and herding: A study of mutual fund behavior. American Economic Review, 85(5), 1088–1105. [Google Scholar]

- Grullon, G., Kanatas, G., & Weston, J. P. (2004). Advertising, breadth of ownership, and liquidity. The Review of Financial Studies, 17(2), 439–461. [Google Scholar] [CrossRef]

- Gupta, S., & Dey, D. K. (2024). Risk perception and adoption of digital innovation in mobile stock trading. Journal of Consumer Behaviour, 23(2), 639–654. [Google Scholar] [CrossRef]

- Gupta, S., & Shrivastava, M. (2022). Herding and loss aversion in stock markets: Mediating role of fear of missing out (FOMO) in retail investors. International Journal of Emerging Markets, 17(7), 1720–1737. [Google Scholar] [CrossRef]

- Hackethal, A., Hanspal, T., Lammer, D. M., & Rink, K. (2022). The characteristics and portfolio behavior of bitcoin investors: Evidence from indirect cryptocurrency investments. Review of Finance, 26(4), 855–898. [Google Scholar] [CrossRef]

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. [Google Scholar] [CrossRef]

- Hallahan, T. A., Faff, R. W., & McKenzie, M. D. (2004). An empirical investigation of personal financial risk tolerance. Financial Services Review, 13(1), 57–78. [Google Scholar]

- Han, B., & Kumar, A. (2013). Speculative retail trading and asset prices. Journal of Financial and Quantitative Analysis, 48(2), 377–404. [Google Scholar] [CrossRef]

- Hanneman, R. A., & Riddle, M. (2005). Introduction to social network methods. University of California, Riverside, CA. [Google Scholar]

- Haritha, P. H., & Rishad, A. (2020). An empirical examination of investor sentiment and stock market volatility: Evidence from India. Financial Innovation, 6(1), 34. [Google Scholar] [CrossRef]

- Harvey, C. R., & Siddique, A. (2000). Conditional skewness in asset pricing tests. The Journal of Finance, 55(3), 1263–1295. [Google Scholar] [CrossRef]

- Hass, J. J. (1998). Small issue public offerings conducted over the internet: Are they suitable for the retail investor. Southern California Law Review, 72, 67–144. [Google Scholar]

- Hasso, T., Müller, D., Pelster, M., & Warkulat, S. (2022). Who participated in the GameStop frenzy? Evidence from brokerage accounts. Finance Research Letters, 45, 102140. [Google Scholar] [CrossRef]

- Hasso, T., Pelster, M., & Breitmayer, B. (2019). Who trades cryptocurrencies, how do they trade it, and how do they perform? Evidence from brokerage accounts. Journal of Behavioral and Experimental Finance, 23, 64–74. [Google Scholar] [CrossRef]

- Heimer, R. Z. (2016). Peer pressure: Social interaction and the disposition effect. The Review of Financial Studies, 29(11), 3177–3209. [Google Scholar] [CrossRef]

- Henderson, B. J., & Pearson, N. D. (2011). The dark side of financial innovation: A case study of the pricing of a retail financial product. Journal of Financial Economics, 100(2), 227–247. [Google Scholar] [CrossRef]

- Henker, J., & Henker, T. (2010). Are retail investors the culprits? Evidence from Australian individual stock price bubbles. The European Journal of Finance, 16(4), 281–304. [Google Scholar] [CrossRef]

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43, 115–135. [Google Scholar] [CrossRef]

- Hofmann, E., Hoelzl, E., & Kirchler, E. (2008). A comparison of models describing the impact of moral decision making on investment decisions. Journal of Business Ethics, 82, 171–187. [Google Scholar] [CrossRef]

- Hong, H., & Wang, J. (2000). Trading and returns under periodic market closures. The Journal of Finance, 55(1), 297–354. [Google Scholar] [CrossRef]

- Hortaçsu, A., & Syverson, C. (2004). Product differentiation, search costs, and competition in the mutual fund industry: A case study of S&P 500 index funds. The Quarterly Journal of Economics, 119(2), 403–456. [Google Scholar] [CrossRef]

- Hsieh, S. F., Chan, C. Y., & Wang, M. C. (2020). Retail investor attention and herding behavior. Journal of Empirical Finance, 59, 109–132. [Google Scholar] [CrossRef]

- Hu, C., & Wang, Y. (2013). Noise trading and stock returns: Evidence from China. China Finance Review International, 3(3), 301–315. [Google Scholar] [CrossRef]

- Huang, J., Wei, K. D., & Yan, H. (2007). Participation costs and the sensitivity of fund flows to past performance. The Journal of Finance, 62(3), 1273–1311. [Google Scholar] [CrossRef]

- Hvidkjaer, S. (2008). Small trades and the cross-section of stock returns. The Review of Financial Studies, 21(3), 1123–1151. [Google Scholar] [CrossRef]

- Islam Khan, M. T., Tan, S. H., & Chong, L. L. (2016). The effects of stated preferences for firm characteristics, optimism and overconfidence on trading activities. International Journal of Bank Marketing, 34(7), 1114–1130. [Google Scholar] [CrossRef]

- Ivković, Z., & Weisbenner, S. (2005). Local does as local is: Information content of the geography of individual investors’ common stock investments. The Journal of Finance, 60(1), 267–306. [Google Scholar] [CrossRef]

- Ivković, Z., & Weisbenner, S. (2009). Individual investor mutual fund flows. Journal of Financial Economics, 92(2), 223–237. [Google Scholar] [CrossRef]

- Iwatsubo, K., & Watkins, C. (2020). Who influences the fundamental value of commodity futures in Japan? International Review of Financial Analysis, 67, 101404. [Google Scholar] [CrossRef]

- Jacomy, M., Venturini, T., Heymann, S., & Bastian, M. (2014). ForceAtlas2, a continuous graph layout algorithm for handy network visualization designed for the Gephi software. PLoS ONE, 9(6), e98679. [Google Scholar] [CrossRef]

- Jain, P. C., & Wu, J. S. (2000). Truth in mutual fund advertising: Evidence on future performance and fund flows. The Journal of Finance, 55(2), 937–958. [Google Scholar] [CrossRef]

- Jianakoplos, N. A., & Bernasek, A. (1998). Are women more risk averse? Economic Inquiry, 36(4), 620–630. [Google Scholar] [CrossRef]

- Johnson, W., Jory, S. R., Likitapiwat, T., & Ngo, T. (2024). The liquidity impact of commission-free trading on stocks with lottery features. The Journal of Investing, 33(1), 51–68. [Google Scholar] [CrossRef]

- Jonwall, R., Gupta, S., & Pahuja, S. (2022). A comparison of investment behavior, attitudes, and demographics of socially responsible and conventional investors in India. Social Responsibility Journal, 19(6), 1123–1141. [Google Scholar] [CrossRef]

- Kaniel, R., Liu, S., Saar, G., & Titman, S. (2012). Individual investor trading and return patterns around earnings announcements. The Journal of Finance, 67(2), 639–680. [Google Scholar] [CrossRef]

- Kannadhasan, M. (2015). Retail investors’ financial risk tolerance and their risk-taking behaviour: The role of demographics as differentiating and classifying factors. IIMB Management Review, 27(3), 175–184. [Google Scholar] [CrossRef]

- Kaustia, M., & Knüpfer, S. (2008). Do investors overweight personal experience? Evidence from IPO subscriptions. The Journal of Finance, 63(6), 2679–2702. [Google Scholar] [CrossRef]

- Kelley, E. K., & Tetlock, P. C. (2013). How wise are crowds? Insights from retail orders and stock returns. The Journal of Finance, 68(3), 1229–1265. [Google Scholar] [CrossRef]

- Khan, M. T. I., Tan, S. H., & Chong, L. L. (2017). How past perceived portfolio returns affect financial behaviors—The underlying psychological mechanism. Research in International Business and Finance, 42, 1478–1488. [Google Scholar] [CrossRef]

- Khan, S. U., Liu, X., Khan, I. U., Liu, C., & Rasheed, M. I. (2020). Assessing the investors’ acceptance of electronic stock trading in a developing country: The mediating of perceived risk dimensions. Information Resources Management Journal, 33(1), 59–82. [Google Scholar] [CrossRef]

- Khatib, S. F., Abdullah, D. F., Hendrawaty, E., & Elamer, A. A. (2022). A bibliometric analysis of cash holdings literature: Current status, development, and agenda for future research. Management Review Quarterly, 72(3), 707–744. [Google Scholar] [CrossRef]

- Kim, J. S., Kim, D. H., & Seo, S. W. (2017). Individual mean-variance relation and stock-level investor sentiment. Journal of Business Economics and Management, 18(1), 20–34. [Google Scholar] [CrossRef]

- Koesrindartoto, D. P., Aaron, A., Yusgiantoro, I., Dharma, W. A., & Arroisi, A. (2020). Who moves the stock market in an emerging country–Institutional or retail investors? Research in International Business and Finance, 51, 101061. [Google Scholar] [CrossRef]

- Konana, P., Menon, N. M., & Balasubramanian, S. (2000). The implications of online investing. Communications of the ACM, 43(1), 34–41. [Google Scholar] [CrossRef]

- Kumar, A., & Lee, C. M. (2006). Retail investor sentiment and return comovements. The Journal of Finance, 61(5), 2451–2486. [Google Scholar] [CrossRef]

- Kumar, A., Page, J. K., & Spalt, O. G. (2016). Gambling and comovement. Journal of Financial and Quantitative Analysis, 51(1), 85–111. [Google Scholar] [CrossRef]

- Kumar, S., & Goyal, N. (2015). Behavioural biases in investment decision making—A systematic literature review. Qualitative Research in Financial Markets, 7(1), 88–108. [Google Scholar] [CrossRef]

- Kuntner, T., & Teichert, T. (2016). The scope of price promotion research: An informetric study. Journal of Business Research, 69(8), 2687–2696. [Google Scholar] [CrossRef]

- Kunz, A. H., Messner, C., & Wallmeier, M. (2017). Investors’ risk perceptions of structured financial products with worst-of payout characteristics. Journal of Behavioral and Experimental Finance, 15, 66–73. [Google Scholar] [CrossRef]

- Kuo, W. H., Chung, S. L., & Chang, C. Y. (2015). The impacts of individual and institutional trading on futures returns and volatility: Evidence from emerging index futures markets. Journal of Futures Markets, 35(3), 222–244. [Google Scholar] [CrossRef]

- Kupfer, A., & Schmidt, M. G. (2021). In search of retail investors: The effect of retail investor attention on odd lot trades. Journal of Empirical Finance, 62, 315–326. [Google Scholar] [CrossRef]

- Lai, H. H., Chang, T. P., Hu, C. H., & Chou, P. C. (2022). Can Google Search Volume Index predict the returns and trading volumes of stocks in a retail investor dominant market. Cogent Economics & Finance, 10(1), 2014640. [Google Scholar] [CrossRef]

- Lai, S., & Teo, M. (2008). Home-biased analysts in emerging markets. Journal of Financial and Quantitative Analysis, 43(3), 685–716. [Google Scholar] [CrossRef]

- Larkin, Y., Leary, M. T., & Michaely, R. (2017). Do investors value dividend-smoothing stocks differently? Management Science, 63(12), 4114–4136. [Google Scholar] [CrossRef]

- Laudenbach, C., Loos, B., Pirschel, J., & Wohlfart, J. (2021). The trading response of individual investors to local bankruptcies. Journal of Financial Economics, 142(2), 928–953. [Google Scholar] [CrossRef]

- Lepone, G., Westerholm, J., & Wright, D. (2023). Speculative trading preferences of retail investor birth cohorts. Accounting & Finance, 63(1), 555–574. [Google Scholar] [CrossRef]

- Lepone, G., & Yang, Z. (2020). Do early birds behave differently from night owls in the stock market? Pacific-Basin Finance Journal, 61, 101333. [Google Scholar] [CrossRef]

- Leydesdorff, L., & Bornmann, L. (2016). The operationalization of “fields” as WoS subject categories (WCs) in evaluative bibliometrics: The cases of “library and information science” and “science & technology studies”. Journal of the Association for Information Science and Technology, 67(3), 707–714. [Google Scholar] [CrossRef]

- Li, T., Chen, H., Liu, W., Yu, G., & Yu, Y. (2023). Understanding the role of social media sentiment in identifying irrational herding behavior in the stock market. International Review of Economics & Finance, 87, 163–179. [Google Scholar] [CrossRef]

- Li, W., & Wang, S. S. (2010). Daily institutional trades and stock price volatility in a retail investor dominated emerging market. Journal of Financial Markets, 13(4), 448–474. [Google Scholar] [CrossRef]

- Li, Y., Zhao, C., & Zhong, Z. K. (2021). Trading behavior of retail investors in derivatives markets: Evidence from Mini options. Journal of Banking & Finance, 133, 106250. [Google Scholar] [CrossRef]

- Lippi, A., Lozza, E., Poli, F., & Castiglioni, C. (2021). How does the emotional meaning associated with money and financial advisor’s characteristics impact investors’ risk-taking? Journal of Neuroscience, Psychology, and Economics, 14(4), 207–221. [Google Scholar] [CrossRef]

- Liu, C., Liu, H., Nassar, R., & Li, L. (2021). Institutional information manipulation and individual investors’ disadvantages: A new explanation for momentum reversal on the Chinese Stock Market. Emerging Markets Finance and Trade, 57(2), 525–540. [Google Scholar] [CrossRef]

- Liu, H., Zhang, W., Zhang, X., & Li, D. (2023). Abnormal temperature and retail investors’ trading behavior. Finance Research Letters, 55, 103944. [Google Scholar] [CrossRef]

- Liu, X., & Wan, D. (2023). Retail investor trading and ESG pricing in China. Research in International Business and Finance, 65, 101911. [Google Scholar] [CrossRef]

- Liu, Z., Yin, Y., Liu, W., & Dunford, M. (2015). Visualizing the intellectual structure and evolution of innovation systems research: A bibliometric analysis. Scientometrics, 103, 135–158. [Google Scholar] [CrossRef]

- Lizárraga, J. (2023). Expanding investor protection. U.S. Securities and Exchange Commission. Available online: https://www.sec.gov/newsroom/speeches-statements/lizarraga-statement-predictive-data-analytics-072623 (accessed on 4 March 2025).

- Lo, A. W., Remorov, A., & Chaouch, Z. B. (2019). Measuring risk preferences and asset-allocation decisions: A global survey analysis. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Locke, P. R., & Mann, S. C. (2005). Professional trader discipline and trade disposition. Journal of Financial Economics, 76(2), 401–444. [Google Scholar] [CrossRef]

- Lou, D. (2014). Attracting investor attention through advertising. The Review of Financial Studies, 27(6), 1797–1829. [Google Scholar] [CrossRef]

- Lu, W., Liu, Z., Huang, Y., Bu, Y., Li, X., & Cheng, Q. (2020). How do authors select keywords? A preliminary study of author keyword selection behavior. Journal of Informetrics, 14(4), 101066. [Google Scholar] [CrossRef]

- Lucchini, L., Aiello, L. M., Alessandretti, L., De Francisci Morales, G., Starnini, M., & Baronchelli, A. (2022). From Reddit to Wall Street: The role of committed minorities in financial collective action. Royal Society Open Science, 9(4), 211488. [Google Scholar] [CrossRef]

- Madsen, J., & Niessner, M. (2019). Is investor attention for sale? The role of advertising in financial markets. Journal of Accounting Research, 57(3), 763–795. [Google Scholar] [CrossRef]

- Malmendier, U., & Nagel, S. (2011). Depression babies: Do macroeconomic experiences affect risk taking? The Quarterly Journal of Economics, 126(1), 373–416. [Google Scholar] [CrossRef]

- Marr, M. W., & Spivey, M. F. (1989). Par values on public utility preferred stock. Journal of Managerial Issues, 1(2), 159–171. [Google Scholar]

- Mavlutova, I., Fomins, A., Spilbergs, A., Atstaja, D., & Brizga, J. (2021). Opportunities to increase financial well-being by investing in environmental, social and governance with respect to improving financial literacy under COVID-19: The case of Latvia. Sustainability, 14(1), 339. [Google Scholar] [CrossRef]

- Mazzoli, C., & Palmucci, F. (2023). Reconciling self-assessed with psychometric risk tolerance: A new framework for profiling risk among investors. Journal of Behavioral Finance. advance online publication. [Google Scholar] [CrossRef]

- McCain, K. W. (1990). Mapping authors in intellectual space: A technical overview. Journal of the American Society for Information Science, 41, 433–443. [Google Scholar] [CrossRef]

- McDaniel, W. R. (1984). Sinking fund preferred stock. Financial Management, 13(1), 45–52. [Google Scholar] [CrossRef]

- Mehta, P., Singh, M., Mittal, M., & Singla, H. (2021). Is knowledge alone enough for socially responsible investing? A moderation of religiosity and serial mediation analysis. Qualitative Research in Financial Markets, 14(3), 413–432. [Google Scholar] [CrossRef]

- Meling, T. G. (2021). Anonymous trading in equities. The Journal of Finance, 76(2), 707–754. [Google Scholar] [CrossRef]

- Montazemi, A. R., & Qahri-Saremi, H. (2015). Factors affecting adoption of online banking: A meta-analytic structural equation modeling study. Information & Management, 52(2), 210–226. [Google Scholar] [CrossRef]

- Naqvi, M. H. A., Jiang, Y., Miao, M., & Naqvi, M. H. (2020). Linking biopsychosocial indicators with financial risk tolerance and satisfaction through macroeconomic literacy: A structural equation modeling approach. Cogent Economics & Finance, 8(1), 1730079. [Google Scholar] [CrossRef]

- Navone, M. (2012). Investors’ distraction and strategic repricing decisions. Journal of Banking & Finance, 36(5), 1291–1303. [Google Scholar] [CrossRef]

- Nilsson, J. (2008). Investment with a conscience: Examining the impact of pro-social attitudes and perceived financial performance on socially responsible investment behavior. Journal of Business Ethics, 83, 307–325. [Google Scholar] [CrossRef]

- Nilsson, J. (2009). Segmenting socially responsible mutual fund investors: The influence of financial return and social responsibility. International Journal of Bank Marketing, 27(1), 5–31. [Google Scholar] [CrossRef]

- Nofsinger, J. R., & Sias, R. W. (1999). Herding and feedback trading by institutional and individual investors. The Journal of Finance, 54(6), 2263–2295. [Google Scholar] [CrossRef]

- Nourallah, M. (2023). One size does not fit all: Young retail investors’ initial trust in financial robo-advisors. Journal of Business Research, 156, 113470. [Google Scholar] [CrossRef]

- Odean, T. (1998). Are investors reluctant to realize their losses? The Journal of Finance, 53(5), 1775–1798. [Google Scholar] [CrossRef]

- Oehler, A., Horn, M., & Wendt, S. (2016). Benefits from social trading? Empirical evidence for certificates on wikifolios. International Review of Financial Analysis, 46, 202–210. [Google Scholar] [CrossRef]

- Oertzen, A. S., & Odekerken-Schröder, G. (2019). Achieving continued usage in online banking: A post-adoption study. International Journal of Bank Marketing, 37(6), 1394–1418. [Google Scholar] [CrossRef]

- Ozik, G., Sadka, R., & Shen, S. (2021). Flattening the illiquidity curve: Retail trading during the COVID-19 lockdown. Journal of Financial and Quantitative Analysis, 56(7), 2356–2388. [Google Scholar] [CrossRef]

- Parveen, S., Satti, Z. W., Subhan, Q. A., & Jamil, S. (2020). Exploring market overreaction, investors’ sentiments and investment decisions in an emerging stock market. Borsa Istanbul Review, 20(3), 224–235. [Google Scholar] [CrossRef]

- Paule-Vianez, J., Gómez-Martínez, R., & Prado-Román, C. (2020). A bibliometric analysis of behavioural finance with mapping analysis tools. European Research on Management and Business Economics, 26(2), 71–77. [Google Scholar] [CrossRef]

- Pilaj, H. (2017). The choice architecture of sustainable and responsible investment: Nudging investors toward ethical decision-making. Journal of Business Ethics, 140, 743–753. [Google Scholar] [CrossRef]

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879. [Google Scholar] [CrossRef] [PubMed]

- Pritchard, A. (1969). Statistical bibliography or bibliometrics? Journal of Documentation, 25(4), 348–349. [Google Scholar]

- Prosad, J. M., Kapoor, S., & Sengupta, J. (2015). Behavioral biases of Indian investors: A survey of Delhi-NCR region. Qualitative Research in Financial Markets, 7(3), 230–263. [Google Scholar] [CrossRef]

- Qadan, M., & Nama, H. (2018). Investor sentiment and the price of oil. Energy Economics, 69, 42–58. [Google Scholar] [CrossRef]

- Rakowski, D., Shirley, S. E., & Stark, J. R. (2021). Twitter activity, investor attention, and the diffusion of information. Financial Management, 50(1), 3–46. [Google Scholar] [CrossRef]

- Renneboog, L., Ter Horst, J., & Zhang, C. (2008a). Socially responsible investments: Institutional aspects, performance, and investor behavior. Journal of Banking & Finance, 32(9), 1723–1742. [Google Scholar] [CrossRef]

- Renneboog, L., Ter Horst, J., & Zhang, C. (2008b). The price of ethics and stakeholder governance: The performance of socially responsible mutual funds. Journal of Corporate Finance, 14(3), 302–322. [Google Scholar] [CrossRef]

- Richards, A. (2005). Big fish in small ponds: The trading behavior and price impact of foreign investors in Asian emerging equity markets. Journal of Financial and Quantitative Analysis, 40(1), 1–27. [Google Scholar] [CrossRef]

- Rickett, L. K. (2016). Do financial blogs serve an infomediary role in capital markets? American Journal of Business, 31(1), 17–40. [Google Scholar] [CrossRef]

- Rickett, L. K., & Datta, P. (2018). Beauty-contests in the age of financialization: Information activism and retail investor behavior. Journal of Information Technology, 33(1), 31–49. [Google Scholar] [CrossRef]

- Riedl, A., & Smeets, P. (2017). Why do investors hold socially responsible mutual funds? The Journal of Finance, 72(6), 2505–2550. [Google Scholar] [CrossRef]

- Riley, W. B., Jr., & Chow, K. V. (1992). Asset allocation and individual risk aversion. Financial Analysts Journal, 48(6), 32–37. [Google Scholar] [CrossRef]

- Rost, K., Teichert, T., & Pilkington, A. (2017). Social network analytics for advanced bibliometrics: Referring to actor roles of management journals instead of journal rankings. Scientometrics, 112(3), 1631–1657. [Google Scholar] [CrossRef]

- Rubinstein, M., & Leland, H. E. (1981). Replicating options with positions in stock and cash. Financial Analysts Journal, 37(4), 63–72. [Google Scholar] [CrossRef]

- Rzeszutek, M. (2015). Personality traits and susceptibility to behavioral biases among a sample of Polish stock market investors. International Journal of Management and Economics, 47(1), 71–81. [Google Scholar] [CrossRef]

- Sahi, S. K., Arora, A. P., & Dhameja, N. (2013). An exploratory inquiry into the psychological biases in financial investment behavior. Journal of Behavioral Finance, 14(2), 94–103. [Google Scholar] [CrossRef]

- Saunders, A., & Smirlock, M. (1987). Intra-and interindustry effects of bank securities market activities: The case of discount brokerage. Journal of Financial and Quantitative Analysis, 22(4), 467–482. [Google Scholar] [CrossRef]

- Schall, D. L. (2020). More than money? An empirical investigation of socio-psychological drivers of financial citizen participation in the German energy transition. Cogent Economics & Finance, 8(1), 1777813. [Google Scholar] [CrossRef]

- Scheld, D., & Stolper, O. (2023). Leveling the playing field? The effect of disclosing fund manager activeness to individual investors. Journal of Banking & Finance, 154, 106915. [Google Scholar] [CrossRef]

- Schertler, A. (2016). Pricing effects when competitors arrive: The case of discount certificates in Germany. Journal of Banking & Finance, 68, 84–99. [Google Scholar] [CrossRef]

- Schmeling, M. (2009). Investor sentiment and stock returns: Some international evidence. Journal of Empirical Finance, 16(3), 394–408. [Google Scholar] [CrossRef]

- Schooley, D. K., & Worden, D. D. (1996). Risk aversion measures: Comparing attitudes and asset allocation. Financial Services Review, 5(2), 87–99. [Google Scholar] [CrossRef]

- Seru, A., Shumway, T., & Stoffman, N. (2010). Learning by trading. The Review of Financial Studies, 23(2), 705–739. [Google Scholar] [CrossRef]

- Shao, R., & Wang, N. (2021). Trust and local bias of individual investors. Journal of Banking & Finance, 133, 106273. [Google Scholar] [CrossRef]

- Sias, R. W. (2004). Institutional herding. The Review of Financial Studies, 17(1), 165–206. [Google Scholar] [CrossRef]

- Sirri, E. R., & Tufano, P. (1998). Costly search and mutual fund flows. The Journal of Finance, 53(5), 1589–1622. [Google Scholar] [CrossRef]

- Small, H. G. (1973). Co-citation in the scientific literature: A new measure of the relationship between two documents. Journal of the American Society for Information Science, 24(4), 265–269. [Google Scholar] [CrossRef]

- Small, H. G. (1977). A co-citation model of a scientific specialty: A longitudinal study of collagen research. Social Studies of Science, 7(2), 139–166. [Google Scholar] [CrossRef]

- Song, J. H., Adams, C. R., & Rhee, Y. (2007). Developing an effective deep support network for individual investors. Journal of Financial Services Marketing, 12, 208–218. [Google Scholar] [CrossRef]

- Sourirajan, S., & Perumandla, S. (2022). Do emotions, desires and habits influence mutual fund investing? A study using the model of goal-directed behavior. International Journal of Bank Marketing, 40(7), 1452–1476. [Google Scholar] [CrossRef]

- Sparkes, R., & Cowton, C. J. (2004). The maturing of socially responsible investment: A review of the developing link with corporate social responsibility. Journal of Business Ethics, 52, 45–57. [Google Scholar] [CrossRef]

- Subramaniam, S., & Chakraborty, M. (2020). Investor attention and cryptocurrency returns: Evidence from quantile causality approach. Journal of Behavioral Finance, 21(1), 103–115. [Google Scholar] [CrossRef]

- Sun, H., & Teichert, T. (2024). Scarcity in today’s consumer markets: Scoping the research landscape by author keywords. Management Review Quarterly, 74(1), 93–120. [Google Scholar] [CrossRef]

- Sun, Z., Sun, X., Wang, W., & Wang, W. (2023). Digital transformation and greenwashing in environmental, social, and governance disclosure: Does investor attention matter? Business Ethics, the Environment & Responsibility. Advance online publication. [Google Scholar] [CrossRef]

- Sunden, A. E., & Surette, B. J. (1998). Gender differences in the allocation of assets in retirement savings plans. The American Economic Review, 88(2), 207–211. [Google Scholar]

- Sung, J., & Hanna, S. D. (1996). Factors related to risk tolerance. Financial Counseling and Planning, 7, 11–19. [Google Scholar] [CrossRef]

- Switzer, L. N., Wang, J., & Lee, S. (2017). Extreme risk and small investor behavior in developed markets. Journal of Asset Management, 18, 457–475. [Google Scholar] [CrossRef]

- Takeda, F., & Wakao, T. (2014). Google search intensity and its relationship with returns and trading volume of Japanese stocks. Pacific-Basin Finance Journal, 27, 1–18. [Google Scholar] [CrossRef]

- Talwar, S., Talwar, M., Tarjanne, V., & Dhir, A. (2021). Why retail investors traded equity during the pandemic? An application of artificial neural networks to examine behavioral biases. Psychology & Marketing, 38(11), 2142–2163. [Google Scholar] [CrossRef]

- Tarim, E. (2016). Situated cognition and narrative heuristic: Evidence from retail investors and their brokers. The European Journal of Finance, 22(8–9), 688–711. [Google Scholar] [CrossRef]

- Tauni, M. Z., Fang, H. X., & Iqbal, A. (2017). The role of financial advice and word-of-mouth communication on the association between investor personality and stock trading behavior: Evidence from Chinese stock market. Personality and Individual Differences, 108, 55–65. [Google Scholar] [CrossRef]

- Tauni, M. Z., Fang, H. X., & Yousaf, S. (2015). The influence of investor personality traits on information acquisition and trading behavior: Evidence from Chinese futures exchange. Personality and Individual Differences, 87, 248–255. [Google Scholar] [CrossRef]

- Tauni, M. Z., Majeed, M. A., Mirza, S. S., Yousaf, S., & Jebran, K. (2018). Moderating influence of advisor personality on the association between financial advice and investor stock trading behavior. International Journal of Bank Marketing, 36(5), 947–968. [Google Scholar] [CrossRef]

- Tversky, A., & Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5, 297–323. [Google Scholar] [CrossRef]

- Umar, Z., Yousaf, I., & Zaremba, A. (2021). Comovements between heavily shorted stocks during a market squeeze: Lessons from the GameStop trading frenzy. Research in International Business and Finance, 58, 101453. [Google Scholar] [CrossRef]

- Ülkü, N., Ali, F., Saydumarov, S., & İkizlerli, D. (2023). COVID caused a negative bubble. Who profited? Who lost? How stock markets changed? Pacific-Basin Finance Journal, 79, 102044. [Google Scholar] [CrossRef]

- van Banning, R. C. (1978). Brokerage commissions charged by Toronto Stock Exchange members: An economic analysis of the arguments for and against fixed commissions. University of Western Ontario Law Review, 17, 77–110. [Google Scholar]

- van Eck, N. J., & Waltman, L. (2014). Visualizing bibliometric networks. In Y. Ding, R. Rousseau, & D. Wolfram (Eds.), Measuring scholarly impact (pp. 285–320). Springer. [Google Scholar]

- Vozlyublennaia, N. (2014). Investor attention, index performance, and return predictability. Journal of Banking & Finance, 41, 17–35. [Google Scholar] [CrossRef]

- Wang, W., & Duxbury, D. (2021). Institutional investor sentiment and the mean-variance relationship: Global evidence. Journal of Economic Behavior & Organization, 191, 415–441. [Google Scholar] [CrossRef]

- Wang, Z. M., & Lien, D. (2023). Limited attention, salient anchor, and the modified MAX effect: Evidence from Taiwan’s stock market. The North American Journal of Economics and Finance, 67, 101904. [Google Scholar] [CrossRef]

- Wanidwaranan, P., & Padungsaksawasdi, C. (2022). Unintentional herd behavior via the Google search volume index in international equity markets. Journal of International Financial Markets, Institutions and Money, 77, 101503. [Google Scholar] [CrossRef]

- Wen, F., Xu, L., Ouyang, G., & Kou, G. (2019). Retail investor attention and stock price crash risk: Evidence from China. International Review of Financial Analysis, 65, 101376. [Google Scholar] [CrossRef]

- White, H. D., & Griffith, B. C. (1981). Author cocitation: A literature measure of intellectual structure. Journal of the American Society for Information Science, 32(3), 163–171. [Google Scholar] [CrossRef]

- Williams, G. (2007). Some determinants of the socially responsible investment decision: A cross-country study. Journal of Behavioral Finance, 8(1), 43–57. [Google Scholar] [CrossRef]

- Wörfel, P. (2021). Unravelling the intellectual discourse of implicit consumer cognition: A bibliometric review. Journal of Retailing and Consumer Services, 61, 101960. [Google Scholar] [CrossRef]

- Yang, D., Ma, T., Wang, Y., & Wang, G. (2021). Does investor attention affect stock trading and returns? Evidence from publicly listed firms in China. Journal of Behavioral Finance, 22(4), 368–381. [Google Scholar] [CrossRef]

- Yao, R., Sharpe, D. L., & Wang, F. (2011). Decomposing the age effect on risk tolerance. The Journal of Socio-Economics, 40(6), 879–887. [Google Scholar] [CrossRef]

- Yao, S., & Zhang, J. (2022). The informativeness of the top holdings of Chinese equity mutual funds. International Journal of Emerging Markets. Advance online publication. [Google Scholar] [CrossRef]

- Ying, Q., Kong, D., & Luo, D. (2015). Investor attention, institutional ownership, and stock return: Empirical evidence from China. Emerging Markets Finance and Trade, 51(3), 672–685. [Google Scholar] [CrossRef]

- You, Y., Yu, Z., Zhang, W., & Lu, L. (2023). FinTech platforms and mutual fund markets. Journal of International Financial Markets, Institutions and Money, 84, 101652. [Google Scholar] [CrossRef]

- Yuan, Y. (2015). Market-wide attention, trading, and stock returns. Journal of Financial Economics, 116(3), 548–564. [Google Scholar] [CrossRef]

- Zahera, S. A., & Bansal, R. (2018). Do investors exhibit behavioral biases in investment decision making? A systematic review. Qualitative Research in Financial Markets, 10(2), 210–251. [Google Scholar] [CrossRef]

- Zhang, D., Zhang, Z., & Managi, S. (2019). A bibliometric analysis on green finance: Current status, development, and future directions. Finance Research Letters, 29, 425–430. [Google Scholar] [CrossRef]

- Zhang, J., Yu, Q., Zheng, F., Long, C., Lu, Z., & Duan, Z. (2016). Comparing keywords plus of WoS and author keywords: A case study of patient adherence research. Journal of the Association for Information Science and Technology, 67(4), 967–972. [Google Scholar] [CrossRef]

- Zhang, X., Wang, Z., Hao, J., & Liu, J. (2022). Stock market entry timing and retail investors’ disposition effect. International Review of Financial Analysis, 82, 102205. [Google Scholar] [CrossRef]

- Zhu, J., & Liu, W. (2020). A tale of two databases: The use of Web of Science and Scopus in academic papers. Scientometrics, 123(1), 321–335. [Google Scholar] [CrossRef]

- Zupic, I., & Čater, T. (2015). Bibliometric methods in management and organization. Organizational Research Methods, 18(3), 429–472. [Google Scholar] [CrossRef]

- Zuschke, N. (2020). An analysis of process-tracing research on consumer decision-making. Journal of Business Research, 111, 305–320. [Google Scholar] [CrossRef]

| Rank | Author(s) (Year) | Title | Journal | #Cited in WoS |

|---|---|---|---|---|

| 1 | Frazzini and Lamont (2008) | Dumb money: Mutual fund flows and the cross-section of stock returns | Journal of Financial Economics | 418 |

| 2 | Wen et al. (2019) | Retail investor attention and stock price crash risk: evidence from China | International Review of Financial Analysis | 279 |

| 3 | Brandt et al. (2010) | The Idiosyncratic Volatility Puzzle: Time Trend or Speculative Episodes? | The Review of Financial Studies | 229 |

| 4 | Dimpfl and Jank (2016) | Can internet search queries help to predict stock market volatility? | European Financial Management | 215 |

| 5 | Cornelli et al. (2006) | Investor sentiment and pre-IPO markets | Journal of Finance | 210 |

| 6 | Kelley and Tetlock (2013) | How wise are crowds? Insights from retail orders and stock returns | Journal of Finance | 206 |

| 7 | Graham and Kumar (2006) | Do dividend clienteles exist? Evidence on dividend preferences of retail investors | Journal of Finance | 202 |

| 8 | Hvidkjaer (2008) | Small trades and the cross-section of stock returns | Review of Financial Studies | 178 |

| 9 | Gopi and Ramayah (2007) | Applicability of theory of planned behaviour in predicting intention to trade online: Some evidence from a developing country | International Journal of Emerging Markets | 171 |

| 10 | Locke and Mann (2005) | Professional trader discipline and trade disposition | Journal of Financial Economics | 166 |

| Preceding Scientific Discourse | Institutional Investments, Momentum Trading, and Herd Behaviour | Effects of Risk-Related Actions or Market Environments on Stock Returns | Information Behaviour | Investor Attention | Background and Experiences of Investors | Quantitative Analysis Methods of Behavioural Biases | Personality of Investors | Attitudes Towards Financial Risks | Socially Responsible Investing |

|---|---|---|---|---|---|---|---|---|---|

| Institutional investments, momentum trading, and herd behaviour | 55.10% | ||||||||

| Effects of risk-related actions or market environments on stock returns | 30.50% | 78.60% | |||||||

| Information behaviour | 14.00% | 20.00% | 63.60% | ||||||

| Investor attention | 29.50% | 36.30% | 9.20% | 64.30% | |||||

| Background and experiences of investors | 19.70% | 29.30% | 17.70% | 22.90% | 58.30% | ||||

| Quantitative analysis methods of behavioural biases | 5.00% | 8.80% | 7.40% | 5.40% | 23.00% | 51.30% | |||

| Personality of investors | 20.80% | 19.40% | 6.90% | 24.60% | 23.50% | 14.50% | 51.50% | ||

| Attitudes towards financial risks | 1.40% | 4.30% | 5.40% | 3.40% | 24.40% | 24.80% | 13.30% | 75.00% | |

| Socially responsible investing | 1.40% | 2.70% | 8.00% | 2.80% | 8.00% | 21.20% | 3.70% | 10.70% | 83.30% |

| Research Theme | Implications on Financial Performance | Information Behaviour | Behavioural Biases and Investor Characteristics | Investor Attention | Attitudes Towards Financial Risks | Socially Responsible Investing | Complex Financial Retail Instruments |

|---|---|---|---|---|---|---|---|

| Implications on financial performance | 54.50% | ||||||

| Information behaviour | 33.70% | 57.60% | |||||

| Behavioural biases and investor characteristics | 29.00% | 21.10% | 53.30% | ||||

| Investor attention | 32.00% | 25.90% | 22.30% | 60.00% | |||

| Attitudes towards financial risks | 7.70% | 10.50% | 27.20% | 14.70% | 68.10% | ||

| Socially responsible investing | 16.40% | 19.00% | 19.00% | 25.00% | 26.10% | 61.80% | |

| Complex financial retail instruments | 18.30% | 11.10% | 17.50% | 16.70% | 11.10% | 15.20% | 83.30% |

| Research Theme | Research Question |

|---|---|

| Implications on financial performance |

|

| |

| |

| Information behaviour |

|

| |

| |

| Behavioural biases and investor characteristics |

|

| |

| Investor attention |

|

| |

| Attitudes towards financial risks |

|

| |

| Socially responsible investing |

|

| |

| |

| Complex financial retail instruments |

|

| |

|

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Simonn, F.C. Past, Present, and Future Research Trajectories on Retail Investor Behaviour: A Composite Bibliometric Analysis and Literature Review. Int. J. Financial Stud. 2025, 13, 105. https://doi.org/10.3390/ijfs13020105

Simonn FC. Past, Present, and Future Research Trajectories on Retail Investor Behaviour: A Composite Bibliometric Analysis and Literature Review. International Journal of Financial Studies. 2025; 13(2):105. https://doi.org/10.3390/ijfs13020105

Chicago/Turabian StyleSimonn, Finn Christian. 2025. "Past, Present, and Future Research Trajectories on Retail Investor Behaviour: A Composite Bibliometric Analysis and Literature Review" International Journal of Financial Studies 13, no. 2: 105. https://doi.org/10.3390/ijfs13020105

APA StyleSimonn, F. C. (2025). Past, Present, and Future Research Trajectories on Retail Investor Behaviour: A Composite Bibliometric Analysis and Literature Review. International Journal of Financial Studies, 13(2), 105. https://doi.org/10.3390/ijfs13020105