Abstract

The literature on the influence of political and policy-related uncertainties on financial aspects has gained an impetus in the last two decades. This study adds to the existing literature by reviewing the impact of political uncertainty on initial public offerings (IPOs). We aim to provide a holistic overview of the past research in this domain, identify the potential research gaps, and explore them further. We performed a bibliometric analysis using VOSviewer to identify the major keywords used, the most cited papers, the authors, and the major countries where research in this domain has taken place. Our perspective on the current state of the literature has been threefold. First, considering the importance of market timing in the firm’s decision to go public, it was seen that firms had shown an unwillingness to come up with an IPO during periods of high political uncertainty. Second, political uncertainty has shown its influence in all the phases of the IPO process; however, political connections and donations mitigate this effect. Third, the research in this domain is still at a very nascent stage and is mainly restricted to China and the US. Thus, we believe that there are several areas that are yet to be explored.

Keywords:

systematic literature review; political uncertainty; political connection; IPO; underpricing JEL Classification:

D72; G32; G38

1. Introduction

With the rise in democracy around the world, there has been a spur in the number of political parties formed. Political parties are representatives of individuals with similar ideologies, such as liberalism, communism, socialism, conservatism, or feminism. They emerge mainly because of differences in the caste system or in religion. Different countries have different party systems; China has a one-party system where only a single party can form the government. Countries like the US and the UK follow a two-party system. A multi-party system is where several parties or coalitions can have control over the government, such as in India, Sweden, and Ireland. Depending on their views and objectives, these parties frame their sets of policies; for example, a right-wing party might frame policies in favor of the growth of businesses, such as reducing tax rates, while a left-wing party might focus more on income equality and raising tax rates for the rich. These differences lead to policy-related uncertainties and policy reversals at the time of elections and political turnover. Along with this, uncertain events, such as financial shocks and crises (the dot-com bubble of the 2000s, the financial crisis of 2008), the pandemic, and the Russia-Ukraine war, have forced the government to bring about frequent amendments in the regulations and policies. Thus, ambiguities regarding who shall frame the government, what new policies shall be implemented, and how these policies shall affect the economy are referred to as political or policy uncertainties.

Political uncertainties crop up as policy changes, geopolitical reforms, political regime changes, the rise of opposition parties, elections, terrorism, and corruption (Bahmani-Oskooee and Nayeri 2020). The unpredictability of what changes (in a government’s future policies relating to fiscal, monetary, and regulatory aspects) will come up is referred to as economic policy uncertainty (EPU) (Al-Thaqeb and Algharabali 2019). EPU can arise from government changes, changes in the macro-economic environment, or situations of uncertainty such as pandemics, financial crises, or war.

Politics, elections, and government policies comprise a major component of the macroe-conomic environment in which the firms operate. Any changes brought in can impact a firm’s value and investment behavior, which delays economic recovery (Baker et al. 2016; Al-Thaqeb et al. 2022). A rise in these uncertainties leads to increased market volatility (Baker et al. 2019; Liu and Zhang 2015), poor firm performance (Feng et al. 2021; Iqbal et al. 2020; Trakarnsirinont et al. 2023), reduced mergers and acquisitions (Sha et al. 2020; Bonaime et al. 2018; Lee 2018; Paudyal et al. 2021), reduced flow of foreign direct investments (Avom et al. 2020; Choi et al. 2021; Hsieh et al. 2019; Zhou et al. 2021), increased cash holdings by firms (Goodell et al. 2021; Hankins et al. 2020; Javadi et al. 2021; Zhao and Niu 2022), reduced firm innovation activities (Lou et al. 2022; Cong and Howell 2018). Researchers in the past have focused on political uncertainty and its impact on investment decisions (Elmassri et al. 2016; Kong et al. 2022; Liu et al. 2020; Amore and Minsichilli 2018; Wadhwa and Syamala 2023). Political uncertainty has shown its impact in each stage of the IPO process (Colak et al. 2017), right from the decision of the firm to raise funds (Colak et al. 2017) to setting the offer price, listing the stock, first-day initial returns, and its long-run performance (Gupta et al. 2021; Meluzin et al. 2018).

There has been a plethora of research highlighting the influence of political uncertainty on firm performance, investment, and financing decisions. However, a systematic literature review focusing specifically on the impact of political uncertainty on the IPO event of a firm is still lacking. The past literature reviews conducted on economic policy uncertainty by Al-Thaqeb and Algharabali (2019) and Dai and Zhang (2019) gave a broad overview of the relationship between EPUs with major financial areas, such as stock market returns, capital investment and spending, corporate finance, and risk management, rather than focusing on one particular segment. By keeping in mind the importance of the firm’s decision to go public and its market timings, this paper aims to provide a systematic literature review and bibliometric analysis using the VOSviewer technique to organize the existing research on the topic and to explore further areas of research.

This study analyzes the role of political uncertainty, elections, political regime changes, policy changes, and political contributions in the financial and investment decisions of a firm, focusing specifically on IPOs. With no restriction on the number of years of publications, we scrutinized the literature for political uncertainties and IPOs. The research question that we aim to address are:

Research Question 1: How researchers in the past have blended the concepts of political uncertainty with the IPO decision of the firm?

Research Question 2: What are the potential research gaps and areas yet to be focused on?

In order to address the first research question and to evaluate the evolution of research in political uncertainty, we took out academic papers from the Web of Science, Scopus, and EBSCO. We screened through the title, abstract, and keywords and studied 42 papers. We used VOSviewer to conduct a bibliometric analysis to further investigate the literature and identify the most cited papers, the main keywords used, the countries where most research has been conducted, and the suitable journals in this area. In order to answer the second question, we reviewed the shortlisted papers to find out unexplored research areas and the future scope of the work.

Our analysis indicates that political uncertainty has gained immense attention from researchers from diverse fields because of its contagious effect on the economy, finance, investor sentiments, etc. The present study aims to contribute to the existing literature in three ways. First, it provides a holistic overview of the effect of political uncertainty on the firm’s decision to go public. The main keywords found in the political uncertainty and IPO literature were uncertainty, underpricing, political connections, corruption, donations, and information asymmetry. The countries significantly contributing to this domain were the USA and China. The main journals on political uncertainty and IPOs were the Journal of Corporate Finance, The Journal of Financial Economics, and The Journal of International Financial Markets, institutions, and Money. Second, this paper provides a visual network of co-occurrences, co-citations, bibliographic coupling on political uncertainty, and finance-related concepts, focusing especially on IPOs. Third, we analyze what areas have already been worked on and what areas are yet to be explored.

The rest of the paper is structured as follows. Section 2 provides a background on political uncertainty and IPOs, respectively. Section 3 discusses the methodology used for the research, followed by the findings and analysis in Section 4. Section 5 presents the discussion and future scope of the study. We conclude the paper in Section 6.

2. Brief Background of the Study

We have classified this section into two parts. First, we discuss the political and electoral uncertainty and its impact on the financial environment. Then, we elaborate on the IPO process and provide hints about how political uncertainty affects each stage of the process.

2.1. Political Uncertainty

It was after the publication of John Kenneth Galbraith’s book and television series titled “The Age of Uncertainty”, that the term uncertainty came into the limelight and attracted the attention of researchers all around the world. Authors have given their different definitions of uncertainty. Rowe (1994) stated that uncertainty occurs due to a lack of available information. Jurado et al. (2015) described uncertainty as a situation of “conditional volatility” that could not be predicted by economic agents. The most common proxy used for measuring uncertainty in the empirical literature was stock market volatility (Arnold and Vrugt 2008). Jurado et al. (2015) and Bekaert et al. (2013) considered statistical forecasts and economic indicators to predict uncertainty rather than the responses of market participants. Baker et al. (2016) developed the most useful proxy for policy-related uncertainty. They created an index using policy keywords related to uncertainty appearing in the newspapers of 11 countries. EPU is considered a more robust technique for predicting exchange rate volatility when compared to other macro-economic variables (Ruan et al. 2023). Adeosun et al. (2023) used Baker’s EPU index to find out the impact of uncertainty and oil prices. In this paper, we mainly focus on political- and policy-related uncertainty; hence, we shall consider the measure for economic policy uncertainty of Baker et al. (2016).

Political uncertainty refers to the risk or uncertainty about changes in the future government, amendments to government policies, or the risk of frequent policy reversals. Political uncertainty can arise due to (a) a lack of clarity regarding which party will set up the government, (b) which policies shall be revoked and what new policies might be implemented, and (c) how would the new policy impact firms (Pastor and Veronesi 2012). Political uncertainties increase prior to elections. The uncertainty becomes even higher when the parties involved in the election have equal chances of winning (Jens 2017) or when the probability of the incumbent party getting re-elected reduces. It has been theoretically proved by Goodell et al. (2020) that any form of financial uncertainty during the election phase has a positive association with the probability of the incumbent party getting re-elected.

Stock markets have shown increased volatility during high electoral uncertainty (Bowes 2018; Yu et al. 2018). Household participation in the stock market also shows a dip during such volatile times. Investors tend to reallocate their funds to safer assets (Agarwal et al. 2022). Firms become more skeptical regarding their investment decisions during macro-economic uncertainty rather than firm-level uncertainty (Rashid and Saeed 2017). Bernanke (1983) came up with a theoretical model proving that firms delay or postpone their investment decisions during high political or electoral uncertainties. Heightened EPU is also associated with a reduction in the quality and quantity of information provided by the firms and the intermediaries (Le et al. 2023)

Firms’ financing activities also dampen as their cost of financing increases (Kim 2019). Debt financing is more influenced compared to equity financing (Lee et al. 2021). Firms usually delay their decision to go public, and a significant decrease in the number of IPOs is seen during elections. The effect of elections is more profuse in firms that have less geographically diversified businesses, firms in close contact with the government, and firms that are harder to value (Colak et al. 2017).

2.2. Initial Public Offerings

Firms constantly need funds to bear their expenses and fulfill their investment needs. These firms can raise capital by issuing equities through retained earnings or initial public offerings, allocating and transferring capital within the business units, which is also referred to as the internal capital market, getting loans from banks, or issuing debentures. Despite the varied sources for raising funds, IPOs remain one of the best ways for entrepreneurs (Ritter and Welch 2002). It is considered one of the most crucial steps in the life cycle of a firm as it comes under the scrutiny of the regulatory bodies and the public for the first time (Helbing 2019).

The literature on IPOs has classified the process into three phases. Carbone et al. (2022) described the three phases as the input, process, and output of the firm’s journey of going public (Carbone et al. 2022). The first phase (pre-IPO) majorly involves the choice of whether the firm should go for an IPO or consider other methods of raising capital. The initial cost of capital, liquidity (Röell 1996), information considerations (Subrahmanyam and Titman 1999), and the willingness of the managers to diversify ownership (Pagano and Roell 1998) majorly influence this decision. The benefits of listing (higher visibility and recognition, higher liquidity, better access to other sources of financing) should be more than the costs involved (Carbone et al. 2022). The other factors that may affect the decision are periods of hot or cold markets (Altı 2005) and investor sentiments and their behavior (Szyszka 2014). Government policy changes and political uncertainty also influence IPO decisions. Periods of high uncertainties are not considered favorable in terms of timing for IPOs. A rise in asset prices, risk premiums, and the cost of capital leads to the undervaluation of the firm, hence making them reluctant to go for an IPO. Luo et al. (2017) proved the number of IPOs decreases during the time of political elections.

The second phase begins once the firm goes public. This phase is further subdivided into three steps. The first step involves the hunt for external advisors, such as investment banks, underwriters, book runner lead managers, and auditors. Choosing reputable advisors has a positive impact on the underpricing and long-run performance of IPOs (Carter and Manaster 1990; Carter et al. 1998; Beatty and Ritter 1986). The second step involves the determination of the offer price. There are two principal methods of deciding the offer price—the fixed price method and the book-building method. In the fixed-price method, the firm fixes the rate at which shares will be offered. In the book-building process, the underwriter sets the offer price based on the bids received by investors (Khurshed et al. 2014). The third step measures the short-run performance of the IPO from the first day of trading until price stabilization. Researchers in the past have given several explanations for first-day initial returns (underpricing). Information asymmetry between the issuing firm and the underwriter (Baron 1982) and between the types of investors (Rock 1986) were considered a cause for underpricing. Grinblatt and Hwang (1989) and Allen and Faulhaber (1989) considered underpricing as a signaling tool for firm quality. Apart from these seminal works, researchers have now started finding out other reasons that may affect underpricing, such as ownership structures (Venkatesh and Neupane 2005), principal-agent conflicts (Arthurs et al. 2008), and corporate governance characteristics (Teti and Montefusco 2022). Macro-economic factors, like economic policy uncertainty, also impact the first-day initial returns. Boulton (2022) showed that IPOs issued during times of high EPU are more likely to be underpriced because of the greater information disparity. Their positive relationship substantially improves during elections. Colak et al. (2021) proved that the political risk arising due to excessive political intervention at a local level has a positive impact on IPO underpricing. Similar results were found by Marcato and Zheng (2021) and Song and Kutsuna (2022).

The third phase (post-IPO) usually begins one month after the IPO is issued. It measures the long-run performance of the IPO. IPOs underperform in the long run. The divergence of investors hypothesis proposed by Miller (1977), the overreaction or fads hypothesis proposed by De Bondt and Thaler (1985, 1987), and the windows of opportunity hypothesis by Teoh et al. (1998) showed the reasons for long-run underperformance. The IPOs of firms (having politically connected CEOs) have shown relatively poor long-run performance compared to firms with no political connection because of the presence of bureaucracy (Fan et al. 2007).

3. Methodology

We conducted the literature review based on the guidelines of Snyder (2019). He classified the entire literature review process into four phases: designing the review, conducting the review, analysis, and writing the review.

Phase 1: Designing the Review: We used the Web of Science, Scopus, and EBSCO databases to extract academic papers. The keywords used for the search were divided into two groups. The first set of keywords focused on political uncertainty, economic policy uncertainty, elections, and political connections. The second set of keywords focused on papers on political uncertainty with finance-related concepts. Hence, the keywords were political uncertainty, economic policy uncertainty, stock market volatility, firm investment decision, and IPO. We conducted the search using Boolean (And/Or) operators and confined it to the article title, abstract, and keywords. There were no restrictions on the years of publication. We limited our focus only to academic journals and excluded news articles, books, magazines, and conference papers.

In order to delve further into the topic, we also conducted a bibliometric analysis. Bibliometric analysis helps in providing a graphical summation of topics, authors, keywords, and citations from databases such as the Web of Science, Scopus, EBSCO (Merediz-Solà and Bariviera 2019). VOSviewer is one of the most frequently used scientometric mapping tools and was developed by Nees Jan van Eck and Ludo Waltman in 2010 (Perannagari and Chakrabarti 2020). It helps in providing network visualization, overlay visualization, and density visualization (Orastean and Marginean 2023).

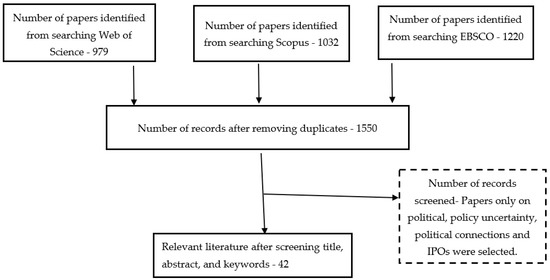

Phase 2: Conducting the Review: As suggested by Snyder (2019), we first conducted a pilot search by testing the keywords and inclusion and exclusion criteria on the Web of Science database. Once satisfied with the results, we further expanded our search on Scopus and EBSCO. The search based on the above keywords showed 979 papers in the Web of Science, 1032 papers in Scopus, and 1220 papers in EBSCO. With the help of Zotero, we removed any duplicates from the databases (1550 remaining). By further scrutinizing these papers by reviewing the article title, abstract, and keywords, we considered only those papers which highlighted the influence of political uncertainty on IPOs. Only 42 articles satisfied our search objective. The following PRISMA flow diagram (Figure 1) briefly describes the screening process for a systematic literature review (Moher et al. 2009; Sharma and Chillakuri 2022).

Figure 1.

PRISMA flow chart. Sources: Moher et al. (2009) and Sharma and Chillakuri (2022).

Phase 3: Analysis: The analysis of the literature review is described in Section 4 of this paper.

Phase 4: Writing the review.

4. Findings and Analysis

This segment focuses on the findings from and analysis of the literature review and bibliometric analysis performed. We aim to provide a holistic overview of the selected literature, including the keywords used by researchers, the most cited documents, the major countries where research has been performed, and the chief authors contributing to this field.

4.1. Number of Publications

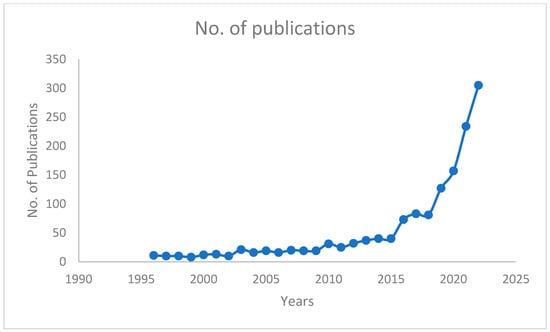

Figure 2 shows an overview of the number of publications on economic policy uncertainty and finance-related concepts. The yearly EPU data were taken from the EPU index created by Baker et al. (2016). The rising trend of this graph shows that the increased attention on political and policy-related uncertainty has gained over the years. However, one striking feature we observe is that some years have suddenly shown a spur compared to other years. It is worth noting that research significantly increased during or after any uncertain or abnormal event. The rise in publications in 2003 (from 10 to 21) was after the dot-com bubble of the 2000s; in 2010 (from 19 to 31), this came after the global financial crisis of 2008, and in 2016 (from 40 to 73), it was because of the US presidential elections. Since 2019, there has been a linear growth in the number of publications, mainly because of a series of events like the pandemic and the war.

Figure 2.

Graph of the number of publications on political uncertainty and finance-related concepts.

4.2. Overview of Collected Data

After reviewing the article title, abstract, and keywords, we found 42 papers relevant to our study. This indicates that research on the influence of political uncertainty and IPOs is at a very nascent stage, and there are several areas that are yet to be explored. The following Table 1 summarizes and provides a brief overview of the papers selected.

Table 1.

Overview of the Data.

4.3. Keyword Analysis

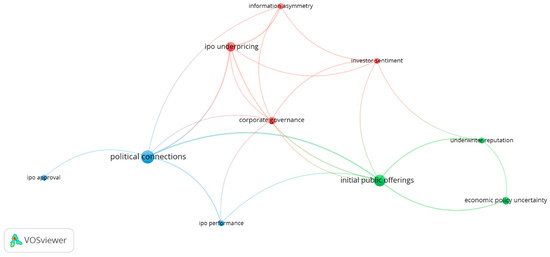

By using VOSviewer, we identified the main keywords plus those which were used by the researchers. The following Figure 3 shows the co-occurrence analysis of these keywords. We considered only those keywords which occurred over five times. Out of 169 keywords found, only 11 satisfied the criteria. Political connections, initial public offerings, and underpricing were the three main keywords.

Figure 3.

Keyword analysis using VOSviewer.

4.4. Analysis of Journals

Table 2 shows the list of journals that published work on political uncertainty and IPOs. The table includes the number of articles in each journal, their publisher’s name, citation score, and impact factor. For the list, we have considered only those journals which fall under the ABDC (Australian Business Deans Council) ranking. The Journal of Corporate Finance has the maximum number of publications, followed by the Journal of Financial Economics.

Table 2.

List of Journals.

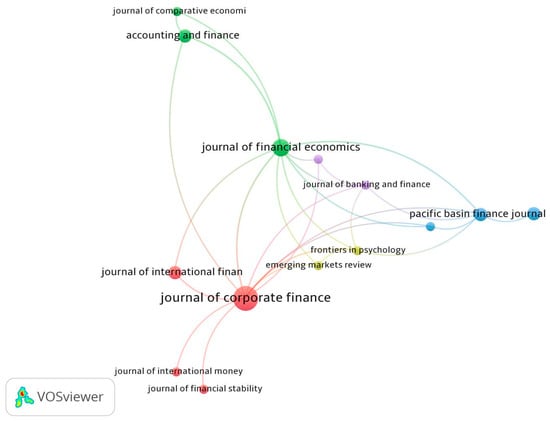

Figure 4 shows a citation analysis using publication sources conducted through VOSviewer. Citation analysis gives us the relatedness of the journals on the basis of the number of times they cite each other (Raan 2003; Perannagari and Chakrabarti 2020). Out of the 25 publication sources, only 14 were interconnected and classified into five clusters containing two to five items. The first cluster containing the Journal of Corporate Finance, the Journal of Financial Stability, the Journal of International Financial Markets, Institutions and Money, and the Journal of International Money and Finance, had a maximum link strength of 15.

Figure 4.

Citation analysis using publication sources.

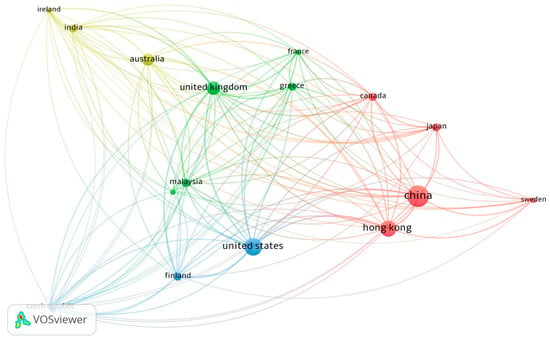

4.5. Country Analysis

The United States and China were the countries that produced the most productive research in the field of political uncertainty and IPOs. Until now, only 18 countries have worked in this domain. Only the US and China performed single-country publications, while India, Finland, Malaysia, Ireland, and France were involved in cross-country publications. Figure 5 shows bibliographic coupling using countries as the unit of analysis. Bibliographic coupling gives us an overlap between the countries. The link between the two countries in the figure shows that a common third country has been cited in the paper, which has those countries (Van Eck and Waltman 2014). The greater the link strength, the stronger will be the bibliographic coupling. The United States and China have shown maximum link strengths of 1669 and 1533, respectively. We have found only 17 of the 18 countries to be interconnected with each other. A total of four clusters were formed, containing three to five items in each.

Figure 5.

Bibliographic coupling using countries as the unit of analysis.

4.6. Citation Analysis

Table 3 presents the number of citations received by the articles, along with the field-weighted citation impact (FWCI). Citation count gives us the number of research works that have shown their views for or against the work cited (Raan 2003). We eliminated those articles which were cited less than 10 times. The field-weighted citation impact enables us to compare how well a document is cited in contrast to similar documents. The greater the FWCI, the better it is. The maximum citation received was 1435, and the highest FWCI was 11.71 (Fan et al. 2007).

Table 3.

Citation analysis of the articles.

4.7. Author Analysis

The authors whose works have made a significant contribution to the domain of political uncertainty and IPOs were J. Fan, T.J. Fong, T. Zhang, J.D. Pitroski, G. Colak, Y. Li, D. Gounopoulos, J. Liu, and Tang J.

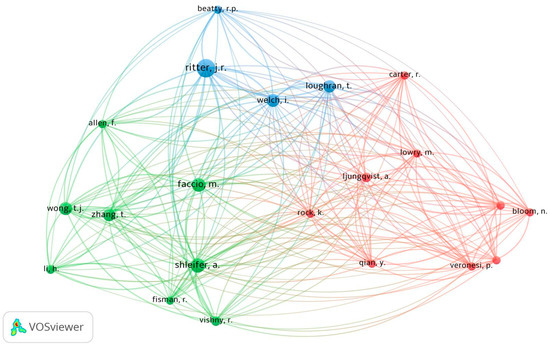

We also conducted a co-citation analysis to link the authors who have been cited together. A co-citation analysis gives us the relatedness of the authors based on the number of times they have been cited together. Figure 6 (below) shows a co-citation analysis of the cited authors. We restricted the maximum number of citations of an author to 15. A total of 22 authors satisfied this criterion. A total of three clusters were formed with, five to nine items in each. The authors with the maximum co-citations were J.R. Ritter, A. Shleifer, T. Loughran, and T.J. Wong.

Figure 6.

Co-citation analysis of authors.

4.8. Content Analysis

Based on the bibliometric analysis conducted, two major themes of research have emerged. The first theme includes the impact of political, electoral, or economic policy uncertainty on firms’ decision to go for an IPO, as well as underpricing and long-run performance. The second theme highlights the impact of political connections, donations, and contributions on IPO decisions, initial returns, and post-issue performance. We reviewed the literature on both of these themes.

4.8.1. Political, Electoral, and Policy Uncertainty and IPOs

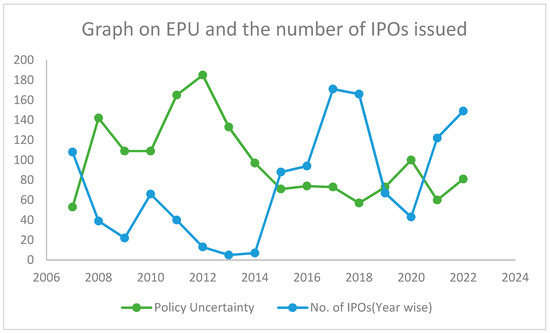

Political and election uncertainty affects policy and financial uncertainty (Goodell et al. 2020). Uncertainties crop up regarding who shall form the government, which new policies will come up, and how these policies will impact the firms. Political uncertainty adversely affects asset prices and risk premiums (Pastor and Veronesi 2012; 2013). Based on this argument, firms will be valued at a lower rate, and their cost of capital shall increase (Liu and Wang 2022). This shall have a detrimental effect on firms going for IPOs. The effect will be more prominent for younger firms as investors already have a lack of clarity on their financials and valuations (Sehgal and Singh 2008). Political uncertainty can elevate this problem of information asymmetry, and hence, firms will be unwilling to come up with an IPO during such times when their shares would be valued at a lower rate, and the cost of raising capital would be higher (Colak et al. 2017). Another reason for firms’ reluctance to go public during elections is due to being unsure about the policy changes that might come up if the government changes. Periods of higher economic policy uncertainty have shown a negative association with the number of firms going for IPOs. The graph shown in Figure 7 highlights the adverse relationship between policy uncertainty and the number of IPOs in India. The policy uncertainty data have been taken from the EPU index constructed by Baker et al. (2016).

Figure 7.

Graph on economic policy uncertainty and the number of IPOs issued.

Contrary to their findings, Luo et al. (2017) found out that, in China, the number of firms going for IPOs increases during elections. The reason stated by them was that government officials’ political promotions depend on the growth of the economy, hikes in GDP, capital market development, or other welfare programs. Hence, with an incentive to get promoted before elections, government officials might amplify the IPO process, thereby increasing the number of IPOs during the time of elections (Piotroski and Zhang 2014).

One of the major reasons for underpricing cited in the literature was information asymmetry (Baron 1982; Rock 1986). Political uncertainty prevailing in the market distorts the quality of information available regarding the firm (Lei and Luo 2023). Firms may either improve corporate disclosure to limit information asymmetry or may take advantage of this uncertainty by reducing the level of information available or manipulating the financial accounts through window dressing (Chen et al. 2017). Regarding the firms going for an IPO, increased information asymmetry leads to higher underpricing. The positive relation is, however, reduced in the presence of reputed venture capitalists, underwriters, and auditors (Boulton 2022). Firms take advantage of political information uncertainty to inflate their offer prices. Higher information asymmetry creates a divergence of opinion in the minds of the investors. As per the divergence of opinion theory proposed by De Bondt and Thaler (1985, 1987), the divergence of opinion creates an initial overoptimism, thereby improving the short-run performance of the IPOs. However, as the shares trade in the stock markets, more information becomes clearly available to the investors, and their overoptimism subsides, leading to poor long-run performance (Liu and Wang 2022).

4.8.2. Political Connections

One of the most common ways firms use to reduce the impact of political uncertainties is through setting political connections. Firms can set up political connections by having a board of directors, a venture capitalist, or underwriters who are associated with a political party.

The probability of firms getting their IPO approval from the regulatory body increases if the firm has a strong political connection (Chen et al. 2017). The fees required for getting themselves listed in the stock market are also considerably less compared to those firms that are not politically connected. By using a sample of Chinese firms, it was seen that politically connected firms set high offer prices and are less underpriced (Francis et al. 2009). Contrary to this, Liu et al. (2020) stated that state-owned firms controlled by the government offer underpricing compared to non-state-owned firms. Rudy and Cavich (2020) proved that firms engaging in corporate political activity prior to their decision to go public reduce information asymmetry regarding the value of the firm, thereby reducing underpricing. Similarly, political donations also act as a non-market strategy used by the issuers to fight ex-ante uncertainty and gain the confidence of investors about the firm’s financial soundness (Gounopoulos et al. 2021).

5. Discussions and Future Scope of Study

After reviewing and analyzing the literature on political uncertainty and IPOs, certain critical areas have not yet received attention. This section highlights these research gaps and the future scope of this research.

5.1. Study on Multi-party System

The majority of the research carried out in this domain was conducted through a single-country analysis restricted to the US and China. The US follows a dual-party system, and China has a single-party system. Boulton (2022) worked on a cross-country analysis of 22 countries, which included a single, dual, and multi-party system. However, it is clear from the studies that a multi-party system is prone to higher and more frequent political uncertainties because of the number of oppositions involved and coalitions formed. It would be essential to advance the discussions on the influence of political uncertainties on IPOs in countries like India that follow a multi-party system having national and regional parties. India’s well-established capital market has some salient features which provide transparency to the investors, such as real-time data on IPOs, relating to listings and subscription rates, grey market information, where shares are traded prior to listing, and the grading system, where the top rating agencies grade the firm, as highlighted by Neupane and Poshakwale (2012). Hence, it would be interesting to see that despite the several measures used by regulatory authorities to reduce information asymmetry, will political uncertainty amplify the information asymmetry regarding the value of the firm? If yes, then how shall firms respond or fight back the uncertainty?

5.2. Political Uncertainty and IPO Withdrawal

Researchers have found the influence of political uncertainty on IPO listings, pricings, and their long-run performance. An under-researched yet important segment of the IPO literature—IPO withdrawal because of political uncertainties—remains unexplored. One reason for withdrawing from an IPO can be the event of upcoming elections or political unrest in the country. However, the direct relationship between the two is yet to be empirically tested.

5.3. Board Diversity and Political Connections

Prior research has highlighted the importance of board composition, such as board independence, gender diversity, family-controlled ownership on firm performance, and corporate social responsibility. It would be interesting to find out whether board composition and, more specifically, gender diversity will impact a firm’s political connections and its decision to go public during periods of high political uncertainty.

6. Conclusions and Limitations of the Study

The primary purpose of this study is to provide a holistic overview of the research carried out in the field of the influence of political uncertainty on IPO firms. We thoroughly reviewed the relevant academic studies in this domain. We used VOSviewer to identify the main keywords, journals, most cited papers, authors, and countries where the research was conducted.

Our review showed that political uncertainty had gained immense attention from researchers of diverse fields because of its contagious effect on the economy, finance, and investor sentiment. By focusing only on the IPO market, it was seen that political uncertainties influence all the three phases of the IPO process. Firms delay their decision to go public during such uncertain times (Luo et al. 2017). The reason for this was heightened information asymmetry and a rise in the cost of capital (Liu and Wang 2022). However, the political connections of the firm and donations to political parties mitigate the impact of these uncertainties (Gounopoulos et al. 2021). Boulton (2022) found that firms issuing IPOs during the election period are more underpriced compared to off-election years. On the other hand, it was empirically proved by Rudy and Cavich (2020) that firms that get involved in political activities prior to listing their shares have shown reduced underpricing. It was also seen that stocks of firms having political connections exhibit poor long-run performance (Liu et al. 2012).

Thus, the main findings from this study were that political uncertainties impact the IPO process. However, the influence of political connections and donations limits this effect. Research in this domain is still at a very nascent stage, with most papers restricted to the US and China. We propose research areas for further exploration.

This study has a few limitations. First, we used only three databases—the Web of Science, Scopus, and EBSCO—to search for research papers on political uncertainty and IPOs. Therefore, there might be a chance that some useful papers included in other databases were skipped. Second, we restricted our focus to only academic journals and did not consider book chapters, conferences, journal proceedings, unpublished works, etc. Third, we considered only articles published in the English language. Thus, papers published in other languages were not considered.

Author Contributions

Conceptualization, P.J. and J.K.S.; methodology, P.J. and J.K.S.; software, P.J.; validation, J.K.S.; formal analysis, P.J.; investigation, P.J. and J.K.S.; resources, P.J. and J.K.S.; data curation, P.J.; writing—original draft preparation, P.J.; writing—review and editing, J.K.S.; visualization, P.J.; supervision, J.K.S.; project administration, J.K.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

No new data were created in this study. Data sharing is not applicable to this article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Adeosun, Opeoluwa Adeniyi, Richard O. Olayeni, Mosab I. Tabash, and Suhaib Anagreh. 2023. The dynamics of oil prices, uncertainty measures and unemployment: A time and frequency approach. China Finance Review International, ahead-of-print. [Google Scholar] [CrossRef]

- Agarwal, Vikas, Hadiye Aslan, Lixin Huang, and Honglin Ren. 2022. Political Uncertainty and Household Stock Market Participation. Journal of Financial and Quantitative Analysis 57: 2899–928. [Google Scholar] [CrossRef]

- Allen, Franklin, and Gerald R. Faulhaber. 1989. Signalling by Underpricing in the IPO Market. Journal of Financial Economics 23: 303–23. [Google Scholar] [CrossRef]

- Al-Thaqeb, Saud Asaad, and Barrak Ghanim Algharabali. 2019. Economic Policy Uncertainty: A Literature Review. The Journal of Economic Asymmetries 20: e00133. [Google Scholar] [CrossRef]

- Al-Thaqeb, Saud Asaad, Barrak Ghanim Algharabali, and Khaled Tareq Alabdulghafour. 2022. The Pandemic and Economic Policy Uncertainty. International Journal of Finance & Economics 27: 2784–94. [Google Scholar] [CrossRef]

- Altı, Aydoğan. 2005. IPO Market Timing. Review of Financial Studies 18: 1105–38. [Google Scholar] [CrossRef]

- Amore, Mario Daniele, and Alessandro Minsichilli. 2018. Local Political Uncertainty, Family Control, and Investment Behavior. The Journal of Financial and Quantitative Analysis 53: 1781–804. [Google Scholar] [CrossRef]

- Arnold, Ivo J. M., and Evert B. Vrugt. 2008. Fundamental Uncertainty and Stock Market Volatility. Applied Financial Economics 18: 1425–40. [Google Scholar] [CrossRef]

- Arthurs, Jonathan D., Robert E. Hoskisson, Lowell W. Busenitz, and Richard A. Johnson. 2008. Managerial Agents Watching Other Agents: Multiple Agency Conflicts Regarding Underpricing in IPO Firms. The Academy of Management Journal 51: 277–94. [Google Scholar] [CrossRef]

- Avom, Désiré, Henri Njangang, and Larissa Nawo. 2020. World Economic Policy Uncertainty and Foreign Direct Investment. Economics Bulletin 40: 1457–64. [Google Scholar]

- Bahmani-Oskooee, Mohsen, and Majid Maki Nayeri. 2020. Policy Uncertainty and the Demand for Money in Japan. Review of Economic Analysis 12: 73–87. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85078991888&partnerID=40&md5=e9d4c6ccc2d5d305553b85ccb9ab6256 (accessed on 30 May 2023). [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring Economic Policy Uncertainty. Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, and Kyle J. Kost. 2019. Policy News and Stock Market Volatility. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Baron, David P. 1982. A Model of the Demand for Investment Banking Advising and Distribution Services for New Issues. The Journal of Finance 37: 955–76. [Google Scholar] [CrossRef]

- Beatty, Randolph P., and Jay R. Ritter. 1986. Investment Banking, Reputation, and the Underpricing of Initial Public Offerings. Journal of Financial Economics 15: 213–32. [Google Scholar] [CrossRef]

- Bekaert, Geert, Marie Hoerova, and Marco Lo Duca. 2013. Risk, Uncertainty and Monetary Policy. Journal of Monetary Economics 60: 771–88. [Google Scholar] [CrossRef]

- Bernanke, Ben S. 1983. Irreversibility, Uncertainty, and Cyclical Investment. The Quarterly Journal of Economics 98: 85–106. [Google Scholar] [CrossRef]

- Bonaime, Alice, Huseyin Gulen, and Mihai Ion. 2018. Does Policy Uncertainty Affect Mergers and Acquisitions? Journal of Financial Economics 129: 531–58. [Google Scholar] [CrossRef]

- Boulton, Thomas J. 2022. Economic Policy Uncertainty and International IPO Underpricing. Journal of International Financial Markets, Institutions and Money 81: 101689. [Google Scholar] [CrossRef]

- Bowes, David R. 2018. Stock Market Volatility and Presidential Election Uncertainty: Evidence from Political Futures Markets. Journal of Applied Business Research 34: 143–50. [Google Scholar] [CrossRef]

- Carbone, Emmadonata, Alessandro Cirillo, Sara Saggese, and Fabrizia Sarto. 2022. IPO in Family Business: A Systematic Review and Directions for Future Research. Journal of Family Business Strategy 13: 100433. [Google Scholar] [CrossRef]

- Carter, Richard B., Frederick H. Dark, and Ajai K. Singh. 1998. Underwriter Reputation, Initial Returns, and the Long-Run Performance of IPO Stocks. The Journal of Finance 53: 285–311. [Google Scholar] [CrossRef]

- Carter, Richard, and Steven Manaster. 1990. Initial Public Offerings and Underwriter Reputation. The Journal of Finance 45: 1045–67. [Google Scholar] [CrossRef]

- Chen, Donghua, Yuyan Guan, Tianyu Zhang, and Gang Zhao. 2017. Political Connection of Financial Intermediaries: Evidence from China’s IPO Market. Journal of Banking & Finance 76: 15–31. [Google Scholar] [CrossRef]

- Choi, Sangyup, Davide Furceri, and Chansik Yoon. 2021. Policy Uncertainty and Foreign Direct Investment. Review of International Economics 29: 195–227. [Google Scholar] [CrossRef]

- Colak, Gonul, Art Durnev, and Yiming Qian. 2017. Political Uncertainty and IPO Activity: Evidence from US Gubernatorial Elections. Journal of Financial and Quantitative Analysis 52: 2523–64. [Google Scholar] [CrossRef]

- Colak, Gonul, Dimitrios Gounopoulos, Panagiotis Loukopoulos, and Georgios Loukopoulos. 2021. Political Power, Local Policy Uncertainty and IPO Pricing. Journal of Corporate Finance 67: 101907. [Google Scholar] [CrossRef]

- Cong, Lin William, and Sabrina T. Howell. 2018. Policy Uncertainty and Innovation: Evidence from IPO Interventions in China. Working Paper. Working Paper Series. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Dai, Lili, and Bohui Zhang. 2019. Political Uncertainty and Finance: A Survey. Asia-Pacific Journal of Financial Studies 48: 307–33. [Google Scholar] [CrossRef]

- De Bondt, Werner F. M., and Richard H. Thaler. 1987. Further Evidence on Investor Overreaction and Stock Market Seasonality. The Journal of Finance 42: 557–81. [Google Scholar] [CrossRef]

- De Bondt, Werner F. M., and Richard Thaler. 1985. Does the Stock Market Overreact? The Journal of Finance 40: 793–805. [Google Scholar] [CrossRef]

- Elmassri, Moataz Moamen, Eliaine Pamela Harris, and David Bernard Carter. 2016. Accounting for Strategic Investment Decision-Making under Extreme Uncertainty. British Accounting Review 48: 151–68. [Google Scholar] [CrossRef]

- Fan, Joseph P. H., T. J. Wong, and Tianyu Zhang. 2007. Politically Connected CEOs, Corporate Governance, and Post-IPO Performance of China’s Newly Partially Privatized Firms. Journal of Financial Economics 84: 330–57. [Google Scholar] [CrossRef]

- Feng, Xinge, Weijie Luo, and Yong Wang. 2021. Economic Policy Uncertainty and Firm Performance: Evidence from China. Journal of the Asia Pacific Economy. [Google Scholar] [CrossRef]

- Francis, Bill B., Iftekhar Hasan, and Xian Sun. 2009. Political Connections and the Process of Going Public: Evidence from China. Journal of International Money and Finance, Emerging Market Finance 28: 696–719. [Google Scholar] [CrossRef]

- Goodell, John W., Abhinav Goyal, and Andrew Urquhart. 2021. Uncertainty of Uncertainty and Firm Cash Holdings. Journal of Financial Stability 56: 100922. [Google Scholar] [CrossRef]

- Goodell, John W., Richard McGee, and Frank McGroarty. 2020. Election Uncertainty, Economic Policy Uncertainty and Financial Market Uncertainty: A Prediction Market Analysis. Journal of Banking & Finance 110: 105684. [Google Scholar] [CrossRef]

- Gounopoulos, Dimitrios, Khelifa Mazouz, and Geoffrey Wood. 2021. The Consequences of Political Donations for IPO Premium and Performance. Journal of Corporate Finance 67: 101888. [Google Scholar] [CrossRef]

- Grinblatt, Mark, and Chuan Yang Hwang. 1989. Signalling and the Pricing of New Issues. The Journal of Finance 44: 393–420. [Google Scholar] [CrossRef]

- Gupta, Vikas, Shveta Singh, and Surendra S. Yadav. 2021. Disaggregated IPO Returns, Economic Uncertainty and the Long-Run Performance of SME IPOs. International Journal of Emerging Markets. [Google Scholar] [CrossRef]

- Hankins, William B., Anna Leigh Stone, Chak Hung Jack Cheng, and Ching Wai Chiu. 2020. Corporate Decision Making in the Presence of Political Uncertainty: The Case of Corporate Cash Holdings. Financial Review 55: 307–37. [Google Scholar] [CrossRef]

- Helbing, Pia. 2019. A Review on IPO Withdrawal. International Review of Financial Analysis 62: 200–8. [Google Scholar] [CrossRef]

- Hsieh, Hui Ching, Sofia Boarelli, and Thi Huyen Chi Vu. 2019. The Effects of Economic Policy Uncertainty on Outward Foreign Direct Investment. International Review of Economics & Finance 64: 377–92. [Google Scholar] [CrossRef]

- Iqbal, Umer, Christopher Gan, and Muhammad Nadeem. 2020. Economic Policy Uncertainty and Firm Performance. Applied Economics Letters 27: 765–70. [Google Scholar] [CrossRef]

- Javadi, Siamak, Mohsen Mollagholamali, Ali Nejadmalayeri, and Saud Al-Thaqeb. 2021. Corporate Cash Holdings, Agency Problems, and Economic Policy Uncertainty. International Review of Financial Analysis 77: 101859. [Google Scholar] [CrossRef]

- Jens, Candace E. 2017. Political Uncertainty and Investment: Causal Evidence from US Gubernatorial Elections. Journal of Financial Economics 124: 563–79. [Google Scholar] [CrossRef]

- Jurado, Kyle, Sydney C. Ludvigson, and Serena Ng. 2015. Measuring Uncertainty. American Economic Review 105: 1177–216. [Google Scholar] [CrossRef]

- Khurshed, Arif, Stefano Paleari, Alok Pande, and Silvio Vismara. 2014. Transparent Bookbuilding, Certification and Initial Public Offerings. Journal of Financial Markets 19: 154–69. [Google Scholar] [CrossRef]

- Kim, Olivia. 2019. Does Political Uncertainty Increase External Financing Costs? Measuring the Electoral Premium in Syndicated Lending. Journal of Financial and Quantitative Analysis 54: 2141–78. [Google Scholar] [CrossRef]

- Kong, Qunxi, Rongrong Li, Ziqi Wang, and Dan Peng. 2022. Economic Policy Uncertainty and Firm Investment Decisions: Dilemma or Opportunity? International Review of Financial Analysis 83: 102301. [Google Scholar] [CrossRef]

- Le, Cao Hoang Anh, Yaowen Shan, and Stephen L. Taylor. 2023. International Economic Policy Uncertainty and Properties of Analysts’ Earnings Forecasts. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Lee, Chi-Chuan, Chien-Chiang Lee, and Shunyi Xiao. 2021. Policy-Related Risk and Corporate Financing Behavior: Evidence from China’s Listed Companies. Economic Modelling 94: 539–47. [Google Scholar] [CrossRef]

- Lee, Kyeong Hun. 2018. Cross-Border Mergers and Acquisitions amid Political Uncertainty: A Bargaining Perspective. Strategic Management Journal 39: 2992–3005. [Google Scholar] [CrossRef]

- Lei, Lijun (Gillian), and Yan Luo. 2023. Political/Policy Uncertainty, Corporate Disclosure, and Information Asymmetry. Accounting Perspectives 22: 87–110. [Google Scholar] [CrossRef]

- Liu, Jianlei, Konari Uchida, and Ruidong Gao. 2012. Political Connections and Long Term Stock Performance of Chinese IPOs. Journal of International Financial Markets, Institutions and Money 22: 814–33. [Google Scholar] [CrossRef]

- Liu, Jianlei, Konari Uchida, and Yuan Li. 2020. Provincial Economic Performance and Underpricing of IPOs: Evidence from Political Interventions in China. Economic Modelling 86: 274–85. [Google Scholar] [CrossRef]

- Liu, Jinjing J., and Hong Wang. 2022. Economic Policy Uncertainty and the Cost of Capital. International Review of Financial Analysis 81: 102070. [Google Scholar] [CrossRef]

- Liu, Li, and Tao Zhang. 2015. Economic Policy Uncertainty and Stock Market Volatility. Finance Research Letters 15: 99–105. [Google Scholar] [CrossRef]

- Lou, Zhukun, Siyu Chen, Wenwei Yin, Chuan Zhang, and Xiaoyu Yu. 2022. Economic Policy Uncertainty and Firm Innovation: Evidence from a Risk-Taking Perspective. International Review of Economics & Finance 77: 78–96. [Google Scholar] [CrossRef]

- Luo, Danglun, Naqiong Tong, and Guoman She. 2017. City-Level Political Uncertainty and City-Level IPO Activities. Accounting and Finance 57: 1447–80. [Google Scholar] [CrossRef]

- Marcato, G., and C. Zheng. 2021. Political Uncertainty and Cross Country IPO Underpricing. Working Paper. Available online: https://www.efmaefm.org/0EFMAMEETINGS/EFMA%20ANNUAL%20MEETINGS/2021-Leeds/papers/EFMA%202021_stage-2049_question-Full%20Paper_id-276.pdf (accessed on 30 May 2023).

- Meluzin, T., Adam P. Balcerzak, Michał B. Pietrzak, Marek Zinecker, and Karel Doubravsky. 2018. The Impact of Rumours Related to Political and Macroeconomic Uncertainty on IPO Success: Evidence from a Qualitative Model. Transformations in Business & Economics 17: 148–69. [Google Scholar]

- Merediz-Solà, Ignasi, and Aurelio F. Bariviera. 2019. A Bibliometric Analysis of Bitcoin Scientific Production. Research in International Business and Finance 50: 294–305. [Google Scholar] [CrossRef]

- Miller, Edward M. 1977. Risk, Uncertainty, and Divergence of Opinion. The Journal of Finance 32: 1151–68. [Google Scholar] [CrossRef]

- Moher, David, Alessandro Liberati, Jennifer Tetzlaff, Douglas G. Altman, and PRISMA Group. 2009. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. Open Medicine: A Peer-Reviewed, Independent, Open-Access Journal 3: e123–e130. [Google Scholar]

- Neupane, Suman, and Sunil S. Poshakwale. 2012. Transparency in IPO Mechanism: Retail Investors’ Participation, IPO Pricing and Returns. Journal of Banking & Finance 36: 2064–76. [Google Scholar] [CrossRef]

- Orăștean, Ramona, and Silvia Cristina Mărginean. 2023. Renminbi Internationalization Process: A Quantitative Literature Review. International Journal of Financial Studies 11: 15. [Google Scholar] [CrossRef]

- Pagano, Marco, and Ailsa Roell. 1998. The Choice of Stock Ownership Structure: Agency Costs, Monitoring, and the Decision to Go Public. The Quarterly Journal of Economics 113: 187–225. [Google Scholar] [CrossRef]

- Pastor, Lubos, and Pietro Veronesi. 2012. Uncertainty about Government Policy and Stock Prices. Journal of Finance 67: 1219–64. [Google Scholar] [CrossRef]

- Pastor, Lubos, and Pietro Veronesi. 2013. Political Uncertainty and Risk Premia. Journal of Financial Economics 110: 520–45. [Google Scholar] [CrossRef]

- Paudyal, Krishna, Chandra Thapa, Santosh Koirala, and Sulaiman Aldhawyan. 2021. Economic Policy Uncertainty and Cross-Border Mergers and Acquisitions. Journal of Financial Stability 56: 100926. [Google Scholar] [CrossRef]

- Perannagari, Krishna Teja, and Somnath Chakrabarti. 2020. Analysis of the Literature on Political Marketing Using a Bibliometric Approach. Journal of Public Affairs 20: e2019. [Google Scholar] [CrossRef]

- Piotroski, Joseph D., and Tianyu Zhang. 2014. Politicians and IPO Decision: The Impact of Impending Political Promotions on IPO Activity in China. Journal of Financial Economics 111: 111–36. [Google Scholar] [CrossRef]

- Raan, Ton. 2003. The Use of Bibliometric Analy-Sis in Research Performance Assessment and Monitoring of Interdisciplinary Scientific de-Velopments. Jg 12. [Google Scholar] [CrossRef]

- Rashid, Abdul, and Muhammad Saeed. 2017. Firms’ Investment Decisions—Explaining the Role of Uncertainty. Journal of Economic Studies 44: 833–60. [Google Scholar] [CrossRef]

- Ritter, Jay R., and Ivo Welch. 2002. A Review of IPO Activity, Pricing, and Allocations. The Journal of Finance 57: 1795–828. [Google Scholar] [CrossRef]

- Rock, Kevin. 1986. Why New Issues Are Underpriced. Journal of Financial Economics 15: 187–212. [Google Scholar] [CrossRef]

- Röell, Ailsa. 1996. The Decision to Go Public: An Overview. European Economic Review, Papers and Proceedings of the Tenth Annual Congress of the European Economic Association 40: 1071–81. [Google Scholar] [CrossRef]

- Rowe, William D. 1994. Understanding Uncertainty. Risk Analysis 14: 743–50. [Google Scholar] [CrossRef]

- Ruan, Qingsong, Jiarui Zhang, and Dayong Lv. 2023. Forecasting Exchange Rate Volatility: Is Economic Policy Uncertainty Better? Applied Economics, 1–19. [Google Scholar] [CrossRef]

- Rudy, Bruce C., and Jason Cavich. 2020. Nonmarket Signals: Investment in Corporate Political Activity and the Performance of Initial Public Offerings. Business & Society 59: 419–38. [Google Scholar] [CrossRef]

- Sehgal, Shikha, and Balwinder Singh. 2008. Determinants of Initial and Long-Run Performance of IPOs in Indian Stock Market. Asia Pacific Business Review 4: 24–37. [Google Scholar] [CrossRef]

- Sha, Yezhou, Chenlei Kang, and Zilong Wang. 2020. Economic Policy Uncertainty and Mergers and Acquisitions: Evidence from China. Economic Modelling 89: 590–600. [Google Scholar] [CrossRef]

- Sharma, Naman, and Bharat Kumar Chillakuri. 2022. Positive Deviance at Work: A Systematic Review and Directions for Future Research. Personnel Review, ahead-of-print. [Google Scholar] [CrossRef]

- Snyder, Hannah. 2019. Literature Review as a Research Methodology: An Overview and Guidelines. Journal of Business Research 104: 333–39. [Google Scholar] [CrossRef]

- Song, Tianyi, and Kenji Kutsuna. 2022. Venture capital investment and institutional factors: Evidence from China. Research in International Business and Finance 65: 101960. [Google Scholar] [CrossRef]

- Subrahmanyam, Avanidhar, and Sheridan Titman. 1999. The Going-Public Decision and the Development of Financial Markets. The Journal of Finance 54: 1045–82. [Google Scholar] [CrossRef]

- Szyszka, Adam. 2014. Factors Influencing IPO Decisions. Do Corporate Managers Use Market and Corporate Timing? A Survey. International Journal of Management and Economics 42: 30–39. [Google Scholar] [CrossRef]

- Teoh, Siew Hong, Ivo Welch, and T. J. Wong. 1998. Earnings Management and the Long-Run Market Performance of Initial Public Offerings. The Journal of Finance 53: 1935–74. [Google Scholar] [CrossRef]

- Teti, Emanuele, and Ilaria Montefusco. 2022. Corporate Governance and IPO Underpricing: Evidence from the Italian Market. Journal of Management and Governance 26: 851–89. [Google Scholar] [CrossRef]

- Trakarnsirinont, Worraphan, Wisuttorn Jitaree, and Wonlop Writthym Buachoom. 2023. Political Uncertainty and Financial Firm Performance: Evidence from the Thai Economy as an Emerging Market in Asia. Economies 11: 18. [Google Scholar] [CrossRef]

- Van Eck, Nees Jan, and Ludo Waltman. 2014. Visualizing Bibliometric Networks. In Measuring Scholarly Impact: Methods and Practice. Edited by Ying Ding, Ronald Rousseau and Dietmar Wolfram. Cham: Springer International Publishing, pp. 285–320. [Google Scholar] [CrossRef]

- Venkatesh, Sundar, and Suman Neupane. 2005. Does Ownership Structure Effect IPO Underpricing: Evidence from Thai IPOs. Corporate Ownership and Control 3: 106–15. [Google Scholar] [CrossRef][Green Version]

- Wadhwa, Kavita, and Sudhakara Reddy Syamala. 2023. Are Business Groups Different from Other Family Firms? Evidence from Corporate Investments during Political Uncertainty. Emerging Markets Review 54: 100947. [Google Scholar] [CrossRef]

- Yu, Honghai, Libing Fang, Sunqi Zhang, and Donglei Du. 2018. The Role of the Political Cycle in the Relationship between Economic Policy Uncertainty and the Long-Run Volatility of Industry-Level Stock Returns in the United States. Applied Economics 50: 2932–37. [Google Scholar] [CrossRef]

- Zhao, Xi, and Teng Niu. 2022. Economic Policy Uncertainty and Corporate Cash Holdings: The Mechanism of Capital Expenditures. Asia-Pacific Journal of Accounting & Economics. [Google Scholar] [CrossRef]

- Zhou, Kexuan, Sanjay Kumar, Linhui Yu, and Xinlin Jiang. 2021. The Economic Policy Uncertainty and the Choice of Entry Mode of Outward Foreign Direct Investment: Cross-Border M&A or Greenfield Investment. Journal of Asian Economics 74: 101306. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).