Abstract

The current economic trend worldwide is for an industrial economy based on tangible assets to convert into a non-tangible economy based on intellectual capital. Lately, a multidimensional view of intellectual capital and its implications on innovation performance have generated renewed research interests. Based on these facts, the relationship amongst different antecedent factors such as culture and trust on intellectual capital components was analysed. In addition, a correlation among intellectual capital components (as non-tangible assets) and innovation performance for the banking sector was established. The positivism philosophy, deductive approach and quantitative methods were used as the research methodology to accomplish the research objectives. In this process, a questionnaire survey and purposive sampling technique were used to collect the responses from 364 employees of the Iraqi commercial banks. The obtained data were analysed statistically using the SPSS v25 and AMOS v24 software. The results revealed a significant impact of culture and trust (antecedent factors) on various intellectual capital components. Furthermore, a strong connection between these antecedent factors and intellectual capital components was evidenced, confirming the study hypotheses. Interestingly, intellectual capital components were found to enhance significantly the innovation performance of the banks, leading to better competitive advantages. In addition, it provided evidence on the impacts of inter-relationships amongst human, structural and relational capitals. Consequently, the study provides academicians and practitioners valuable insights into and guidance on how developing intellectual capital enhances competitive performance, especially in the context of Iraqi commercial banks.

1. Introduction

Previous studies have reported intellectual capital as mental property based on facts, figures and institutional experiences [1]. It was argued that, in addition to improving employees’ knowledge, skills, perception and other non-sensorial and intangible characteristics, intellectual capital could be exploited to acquire wealth by expanding business assets [2]. The definitions of intellectual capital vary according to its scale. The intellectual capital of an organisation can be used to generate extra benefits or items that may be easily understood by its employees, thereby achieving the financial target. In this context, [3] described the probability of formalising, controlling and enabling intellectual contents to generate valuable assets wherein intellectual capital acts as the gap between the ledger interest of an enterprise and the value expected to be paid for it.

According to [4], intellectual capital is the static aspect of knowledge; it is passive, measurable, classified and potentially value-generating. A number of researchers have reported that intellectual capital is composed of four correlated elements: human, structural, relational and social capitals [5,6,7]. In addition, three facets of intellectual capital taxonomy were established as an emergent standard. In fact, human capital, an essential ingredient of intellectual capital, determines the organisation’s capital growth and overall performance enhancement [8]. Despite dedicated effort, no consensus has been reached regarding the actual essence of human capital and its impact on improvements in organisational performance.

Furthermore, human capital comprises over 50% of intellectual capital values, making it the foremost constituent of intellectual capital [7,9]. In terms of relational capital, the reliance on diverse modes, such as horizontal or vertical as well as downstream or upstream, reflects the different types of cooperation or collaboration mechanisms in a variety of settings. Social capital refers to the embedded interactional knowledge of an organisation, signifying the nature and level of interaction amongst its members. The main function of structural capital is to assemble and disseminate knowledge across the organisation, enabling interaction of the organisation with other communities and institutions [10].

Intensive review of previous literature has revealed that a dynamic and turbulent economic environment requires innovative strategies for survival, wherein modernisation acts as a key element in the organisation’s performance [11,12,13]. Synergy between intellectual capital and success in innovation performance has emerged as a recurring theme in economic growth studies, especially in the banking sector [14,15]. Few studies have investigated the role of intellectual capital in the correlation between the financial innovation performance of the banking sector and its growth [16,17]. In fact, sustained successful innovation performance is decided by efficient and reliable actions based on the capacity of a bank to learn and adjust dynamically [18].

The current research focused on the idea that innovation performance is vital for achieving competitive advantages, such as quality service or/and management, efficient strategy formulation and creativity, in the banking sector [15,19,20]. The majority of the studies related to innovation performance have focused mainly on the services and manufacturing sectors [21,22]. Intellectual capital comprises intangible assets that improve the competitive advantage in terms of organisational skills, knowledge, experiences, technologies and relationships [14]. Previous study demonstrated a close connection between the organisation’s intellectual capital and innovation performance, which was further validated in different contexts, regions and industries [23]. Earlier study examined the role of intellectual capital in encouraging radical and incremental innovations [24]. Despite all these efforts, insight into intellectual capital and its impact as a value creator is lacking.

Thus, the aim of the current research was to investigate the influence of two intellectual capital antecedent factors, culture and trust, on the main components of intellectual capital and the relationship between intellectual capital components and innovation performance. Hence, the following research questions were developed to help in the current investigation:

- What is the effect of the antecedent factors of culture and trust on intellectual capital?

- What are the impacts of human capital on structural and relational capitals?

- What are the influences of intellectual capital on innovation performance?

2. Theoretical Underpinnings and Hypotheses

2.1. Implications of Culture for Intellectual Capital

An overview of previous literature reveals that culture supports the infrastructure of human capital, which is composed of organisational culture, management philosophies, processes, systems and informational resources [25,26,27,28]. Management of intellectual capital involves the development of organisational culture that can help develop and store earlier and newly acquired knowledge. Consequently, it enhances the innovation performance inside an organisation [29]. Various definitions and content descriptions of organisational culture exist in the literature, revealing various implications of the management of intellectual capital and knowledge creation, because culture offers a basis for organisational management [30,31]. Another study focused on social media use by employees in the financial sector [32]. From this perspective, contingency theory can be viewed as the appropriate methodology to determine the implications of organisational culture for the process of knowledge asset creation [33,34,35,36].

Furthermore, organisational culture binds the intelligence of individuals and their respective core values to instigate the culture of excellence [37]. However, organisational culture can go off-centre if the core organisational values are based on punishment or fear or whenever a massive disagreement occurs between the interests of any organisation and respect for individual values. Therefore, it becomes the moral duty for the managers to continuously establish a strong cultural value within their organisation [30]. In conclusion, culture acts as the glue that connects the growth of intellectual capital to innovation performance [38]. The implications of culture for every single component in the structure of intellectual capital are discussed in the following sections.

2.1.1. Culture and Human Capital

Earlier investigations have confirmed that culture contributes to the development of human capital, a notion that has generated renewed interest [39]. In this framework, [38] referred to culture as the means of promoting the learning, staff commitment, knowledge sharing and participation of the organisational members in decision-making [40,41,42]. Due to the rapidly changing work environment in recent years, organisations are becoming increasingly aware of the necessity to make changes in the values, norms and motivations of their employees [43]. In this context, [44] disclosed that the implications of culture and human capital are indisputable as a two-way relationship wherein both factors depend on their properties. Additionally, as per contingency theory, culture is significantly influenced by the norms, values and constituted beliefs of the employees in an organisation, whereas human capital is considered as a more important asset possessed by any organisation [45]. Based on these disclosures, the following hypotheses can be made:

Hypothesis 1a (H1a).

The higher the influence of culture, the higher the level of human capital.

2.1.2. Culture and Structural Capital

Structural capital refers to the supportive infrastructure, having vital implications for human resource development [46]. It includes management policies, organisational processes, systems and other informational resources [24]. Each organisation displays a specific culture, consolidated and viewed at various levels. The culture factor is observed at any place where people come together to form a community. In this respect, contingency theory indicates that organisational culture can be learned, transmitted, multi-faceted, adaptable and partially conscious and exceeds any individual intent [47]. It also views organisational managers as visionaries who realise the importance of corporate culture in creating appropriate structure capital in an organisation. Thus, the following hypothesis was proposed:

Hypothesis 1b (H1b).

The higher the influence of culture, the higher the level of structural capital.

2.1.3. Culture and Relational Capital

The importance of the cultural factor for relational capital is shown in the relationship between employees themselves and with customers associated with the respective business performance. According to, [48] described organisational culture as the social environment that is established in the business, enabling the physical distribution of all members and determining their behaviours towards the beneficiary members. Recently, [49] developed a model for measuring the cultural implications of developing relational capital in an organisation. This model was also used to measure the desirable values and ideologies considered by the organisation while offering services. It was shown that most businesses aim to enhance their organisational culture (positively influencing customer satisfaction) [50] by improving the working system of the employees and their inter-relationships. Hence, the contingency approach considers culture as the neuralgic centre that justifies the organisational structure, personal relationships and surroundings [38]. Based on this fact, the following hypothesis was set:

Hypothesis 1c (H1c).

The higher the influence of culture, the higher the level of relational capital.

2.1.4. Culture and Social Capital

The development of social capital in an organisation is influenced by culture, which moderately affects customer satisfaction. Previous literature has shown that culture could strongly influence the relative factors of administration, means of communication and so forth [51,52]. Conferring to, [30] showed that the cultural factor represents the norms, values and established behavioural rules in the organisation, helping to define its correlation with the social environment. Cognition-based culture describes the beliefs regarding the reliability and competence of others, and affect-based culture relies on the social bonds that exist amongst the group members, reflecting the beliefs respecting the reciprocated concerns and care [53]. These forms of culture are significant for developing social relationships in the business environment, allowing the organisation to improve its performance [37]. In brief, to describe these implications, the following hypothesis was proposed:

Hypothesis 1d (H1d).

The higher the influence of culture, the higher the level of social capital.

2.2. Implications of Trust for Intellectual Capital

Earlier investigations [54] have stated that trust is an important factor for any research on intellectual capital since it is essential for stakeholders to share tacit knowledge with the organisation. Generally, capital stakeholders are divided into owners of the organisation, represented by managers, and employees, who hold the intellectual property. The relationship between them is based on specific conditions [55]. This poses an extra challenge for businesses to manage different interests of owner groups, where trust is required to develop intellectual capital in the business [56]. Earlier research [57] studied the importance of trust at both inter- and intra-levels in the organisation. It was demonstrated that employees do not share their private knowledge with others in a distrustful environment, making it difficult for the organisation to exploit any information [41]. The management of intellectual capital is clearly based on trust-based knowledge sharing inside the organisation [36].

Various researchers [55,58,59] have indicated that the element of trust is essential between personnel, employers and employees to encourage implicit knowledge sharing. Contingency theory implies that the establishment and development of intellectual capital are dependent on the levels of trust amongst the employees and final users in the organisation [38]. In contrast, the lack of trust between a client and a supplier can be a source of extra challenge in monitoring contracts between the participants in the organisation, thereby increasing the transaction costs [55]. Recently, [60] mentioned that the success of the business is at high risk when little attention is paid to the trust factor. The implication of this factor for each component in the structure of intellectual capital is discussed in the following sections.

2.2.1. Trust and Human Capital

The researchers of [61] showed that organisations usually hire workers with a higher human capital level for carrying out complex tasks. This is because when employees experience a higher level of trust, the monitoring costs are decreased in the organisation [48,62,63]. These workers tend to show higher cooperation during their work and share all vital information effectively with each other, further encouraging managers to hire workers with a higher human capital level to achieve better innovation performance [7]. This can be achieved by implementing the contingency approach to facilitate the correlation between the present research antecedent variables and intellectual capital. However, the presence of higher trust, the probability of extensive contracts and outcomes ending in expensive litigation are preferred because the deals can be easily sealed with a simple handshake [64]. Based on these arguments, the following hypothesis emerged:

Hypothesis 2a (H2a).

The higher the influence of trust, the higher the level of human capital.

2.2.2. Trust and Structural Capital

Structural capital includes infrastructure strategies, systems or processions that collectively allow an organisation to develop and deliver products to customers [65]. It also defines the capacity of the organisation to respond to a changing surrounding environment [66]. Newly, [15] acknowledged that structural capital defines the philosophy of trust in the management amongst the employees and other managerial stages to run a successful business. Previous literature on structural capital studies, especially those dealing with the development of intellectual capital, reveals high impacts of trust factor on the enhancement of structural capital [31,64,67], attributed to the significance of trust between the managerial levels to fund the process of developing intellectual structural property, affecting the success or development of the organisation plus enabling efficient fulfilment for all its objectives [68]. Based on these disclosures, the following hypothesis was made:

Hypothesis 2b (H2b).

The higher the influence of trust, the higher the level of structural capital.

2.2.3. Trust and Relational Capital

Relational capital is defined as the level of commitment, mutual trust, respect and friendship distinguished during interaction between the partners in an organisation [69]. Lately, [70] opined that mutual trust and close interaction are related to factors such as social interaction, trust and desire to fulfil similar goals and objectives [55]. In this regard, relational capital refers to the sum of resources related to respect, friendship, trust and mutual understanding that exist at the organisational level [71]. The organisation establishes that all the partners must reflect the values included in the business relationships [7]. Customarily, employees may no longer be loyal if they have no trust in the organisation, especially in the financial sector [15,72], and they become less motivated and less productive for the organisation. This status is immediately reflected in the customers’ intention to associate with the organisation without strong trust [66]. Based on these facts, the following hypothesis was made:

Hypothesis 2c (H2c).

The higher the influence of trust, the higher the level of relational capital.

2.2.4. Trust and Social Capital

Social capital requires a certain level of trust [73]. The authors of [38] emphasised that the trust of employees is the major mediating factor directly related to their inclination to share vital and tacit knowledge. Of late, [15] indicated that trust is the main variable for customer satisfaction when outsourcing training and developmental tasks due to the presence of tacit knowledge. Lately, [15] and [74] indicated that social capital could be presented in the levels of shared norms, trust, obligation and mutual identification that tie all the factors of intellectual capital together. In this study, the interpersonal levels of trust between the team members were analysed as the psychological state characterised by vulnerability based on the expectations of behaviours from and intentions towards other team members in the organisation [56]. Accordingly, the following hypothesis was made:

Hypothesis 2d (H2d).

The higher the influence of trust, the higher the level of social capital.

2.3. Relationship between Human, Structural and Relational Capitals

Human capital is considered as the main factor concerned with the skills, knowledge, satisfaction and motivation levels of the employees in the organisation [75]. Thus, it is viewed as a vital asset for any organisation. Yet, [76] stated that human capital includes the competence of the employees as well. However, structural capital is regarded as the tangible assets that support the human capital in performing the business. This is because the knowledge belonging to the organisation remains intact after the employee has left the job at the end of the shift [74]. Therefore, structural capital helps in building the infrastructure required by human capital to create value retained by the organisation even after the exit of the employee [77]. Meanwhile, relational capital tackles the relationships amongst the associates in the organisation and highlights their loyalty to the company and their link with other groups [78]. Nevertheless, [79] focused on the knowledge problem of economics by discussing its current status in light of digitalisation. In this essence, this study assumed a certain correlation between these variables by investigating their impacts on the development of intellectual capital, as discussed in the following sections.

2.3.1. Human Capital and Structural Capital

Human capital is regarded as a major asset that contributes to increasing an organisation’s performance. In the interim, [80] indicated that the creativity and skills of employees can be improved when the organisation invests in their training programs. Consequently, the organisation shows a higher efficiency by increasing the effectiveness of the value added by the employees [81]. However, structural capital involves all aspects of the organisational assembly that increase the employees’ capability to improve the economic condition of the organisation and stakeholders [82]. This process needs to be effective as it involves many internal processes that enable knowledge integration and sharing of different abilities, creating wealth for any organisation. Furthermore, the knowledge management procedures can encourage new customers to seek the services of the organisation that may require a substantial increase in the structural assets of the organisation [7]. Based on this revelation, a connection between human capital and structural capital was established through the following hypothesis:

Hypothesis 3 (H3).

The higher the influence of human capital, the higher the level of structural capital.

2.3.2. Human Capital and Relational Capital

The authors of [83] described human capital in terms of the economic value of human resources that are associated with the knowledge, ability, ideas, commitment and energy within an organisation. It combines the skill, innovativeness and ability of the employees to perform their duties so that it creates value, allowing the organisation to fulfil its objectives [41]. Relational capital helps managers to derive the knowledge from their environment that enables them to offer better services and products to their customers and understand their needs [84]. Hence, relational capital interacts with human capital to determine the impacts of the surrounding environment on the organisation, addressing all required issues for a successful business [48]. Overall, the relationship between human capital and relational capital was identified by examining the following hypothesis:

Hypothesis 4 (H4).

The higher the influence of human capital, the higher the level of relational capital.

2.4. Implications of Intellectual Capital for Innovation Performance

Intellectual capital is considered as a non-tangible asset that differs from tangible resources, such as raw materials, land and financial capital, in that the tangible resources are easily obtainable [85]. Thus, intellectual capital is regarded as the strategic resource and knowledge system that operates the processes of VRIN characteristics and helps the organisation to derive a sustainable advantage [86]. The resource-based approach views intellectual capital as the sum of knowledge used by the organisation, whereas innovation refers to the process of implementing and using this knowledge for producing novel products and resolving various problems [87]. Meanwhile, [88] stated that organisations with high intellectual capital are more competent in innovating and enhancing their performance. Numerous researchers have pointed out that new product expansion can be maintained by developing intellectual capital in an organisation [22,89,90].

The intimate relationship between innovation and intellectual capital has blurred the line between their narrow boundaries over time in the developmental process of an organisation performance [48]. Due to this reason, the innovation performance has generated immense research interests [91,92]. Proper management is considered an important prerequisite for managing intellectual capital. In the past decades, several researchers have highlighted the necessity for an organisation to develop a modern perspective to achieve innovation performance [12,20,93,94]. Driven by this idea, many frameworks have been developed depending on the research backgrounds and subjects without using any consistent design strategy [27,86].

The researchers of [95] studied the role of intellectual capital in the innovative performance of an organisation. It was argued that innovation increases the growth curves of organisations and opens up markets. Thus, innovation is regarded as an important element responsible for increasing the wealth, growth and success of an organisation [96]. In fact, innovative organisations use their managerial interventions to improve intellectual capital and develop approaches for innovation enhancement [97]. Innovation activities need powerful stimuli, which generate many results wherein the right people are placed in the right intellectual culture. Research and development managers have to understand the driving factors that affect innovation and create an environment for promoting innovation with the modern technological perception [6].

Most earlier studies have investigated intellectual capital following the framework developed by [98]. This framework considers structural capital, human capital and relational capital as the major components of intellectual capital [18,99]. In this framework, human capital includes the skills, capabilities, knowledge and attitudes of all employees in the organisation; structural capital encloses the organisational structure and culture related to it, and relational capital deals with the correlation between the organisation’s employees and other players, such as its suppliers and customers. In short, the contemporary measurement models in the past considered intellectual capital as an important factor for developing an organisation’s innovation performance [42,100].

2.4.1. Human Capital and Innovation Performance

Human capital is vital for innovation performance as the experience, knowledge and skills of the employees are necessary for the existing fast-paced and changing business environment [97]. For the meantime, [25] mentioned that human capital comprises human skills, expertise and motivation in the context of work. The authors of [101] stated that talented and educated employees with sophisticated skills tend to show better cognitive skills to improve the productivity, efficiency and innovative performance of the organisation. These employees help the organisation to achieve better entrepreneurial judgment, which enables the organisation to run all operations smoothly, improving innovation performance [102]. Meanwhile, some empirical studies have shown that human capital improves the innovation performance of organisations in emerging economies, such as China [103]. Furthermore, the impacts of intellectual capital are based on human capital, which facilitates the effects of other capitals on innovation performance [7]. Based on this argument, the present study hypothesised the following aspect:

Hypothesis 5a (H5a).

The higher the level of human capital, the higher the level of innovation performance.

2.4.2. Structural Capital and Innovation Performance

Structural capital refers to the information systems and infrastructures used in an organisation to achieve targeted innovation performance [104]. The processes inside the organisation enable it to coordinate its structures, strategies, routines and culture to improve operational efficiency [105]. Advanced systems help in collecting a wealth of information that assists in the decision-making process, increasing the organisation’s performance profitability and efficiency [106]. Previous works have suggested that the development of a unique process or routine to perform the activities and tasks can considerably increase the innovation performance [15,107,108]. Firms without adequate systems or processes cannot reach their full potential. However, organisations with effective and strong structural capital can carry out many value-creation tasks [15,109]. From this standpoint, structural capital that contains the structural features of production can encompass its processes, systems, solutions, databases, patents and innovation performance. These structure-driven innovations can contribute to building the required infrastructure for innovation and knowledge creation [7]. Based on this argument, the present research made the following hypothesis:

Hypothesis 5b (H5b).

The higher the level of structural capital, the higher the level of innovation performance.

2.4.3. Relational Capital and Innovation Performance

Relational capital presents the interpersonal relationship based on commitment, trust and respect between suppliers, government employees, customers and stakeholders [47]. Firms innovate or increase their performance after implementing solutions used by other organisations or after combining their existing knowledge with external and accessible resources [73]. Previous studies have illustrated that inter-organisational relationships offer numerous opportunities for an organisation to seek external knowledge resources and combine them with the existing knowledge resources [110]. Accordingly, after fulfilling their promises, organisations create a network of external relationships, indicating a cooperative innovation-based behaviour. This network of relationships can assist the organisation in acquiring valuable knowledge from external resources to improve its innovativeness in the future [7]. Based on this factor, this study made the following hypothesis:

Hypothesis 5c (H5c).

The higher the level of relational capital, the higher the level of innovation performance.

2.4.4. Social Capital and Innovation Performance

Social capital is another component of intellectual assets and incorporates modernisation to determine various implications for innovation performance [111]. The study [56] found strong ties amongst the employees of an organisation to be more suitable for generating new information due to the employees’ willingness to obtain useful knowledge. Meanwhile, Isanzu and Lirios [14,112] believed that weak ties might be a source of new knowledge because strong ties may occur with others who possess the same knowledge. It was acknowledged that organisations paying more attention to social capital often tend to achieve a higher level of innovation [110]. According to resource-based view theory, innovation performance results from the extraction and sharing of embedded knowledge with customers. This helps achieve operational excellence with suppliers, which leads to a better operational and economic performance [68,78,113]. Based on this argument, this research made the following hypothesis:

Hypothesis 5d (H5d).

The higher the level of social capital, the higher the level of innovation performance.

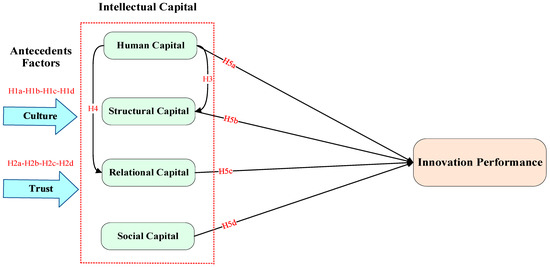

In the conceptual framework of the current study, there are two antecedent factors, culture and trust, one independent variable, namely, intellectual capital, and one dependent variable, namely, innovation performance, as shown in Figure 1.

Figure 1.

Conceptual framework of the present research.

3. Research Methodology

3.1. Participants and Research Design

The present research population encompassed 24 Iraqi commercial banks in the year 2020. The main reason for selecting these commercial banks from the financial population was mainly their flexibility and accessibility for research. In fact, these banks regard this flexibility as their visibility to external auditors. Additionally, the complex procedures for obtaining approval to access other types of Iraqi banks and collect data from them was one of the reasons for the researcher to focus on the commercial banks of Iraq as the dominant population for the study.

The ever-growing demand for research makes an effective technique necessary for defining the required sample size in a given population. Meanwhile, [114] declared that no additional calculations are required to identify the sample size in quantitative research. The authors developed a standard table for calculating the sizes of samples required for studies. The current study aimed to investigate a population of 7000 employees from 24 commercial banks. Thus, a sample size of 364 participants was required to investigate the current phenomena. In all, 470 questionnaires were distributed amongst the bank employees considering the fact that the larger the study sample, the more the results can be generalised to the target population. The selected sampling method enables gathering accurate information from the population concerning intellectual capital and innovation performance.

Furthermore, purposive sampling of the estimated population was considered to be more suitable than normal sampling. Purposive sampling is the process of selecting respondents who are best placed to deliver the required data for the study [115]. Bank accountants, being the most experienced and well informed in the preparation of financial statements, are thus claimed to possess and reflect expert knowledge capable of delivering data relevant to the research inquiries. The present research context required participants from the banking field who met specific criteria, such as being persons responsible for preparing financial reports and managing financial data in Iraqi commercial banks. This population of interest indeed comprised respondents who possessed the required facts and could provide the desired information. Briefly, the respondents of this study were bank accountants involved in rigorous banking business regardless of their rank or position.

In this work, the primary data were collected through a set of quantitative questions that served to measure the opinions, perceptions and attitudes of the respondents towards the main construct in the present investigation [115]. Considering the recent turbulent situation in Iraq, most of the respondents in the Iraqi commercial banks preferred to answer the questionnaire manually (using a hard copy). As a result, data cleaning was important to filter for usable responses and avoid any errors during the data analysis procedures. All the banks and their employees were informed before the researcher arrived to distribute the questionnaires and begin data collection. Thereafter, the researcher distributed 470 questionnaires across 24 Iraqi commercial banks and informed the respondents that they have to answer all the questions. The main data collection process was conducted from 20 August 2020 to 20 November 2020 (roughly over a period of 3 months). After the data were collected, the data cleaning process was started, ensuring the consistency of the responses for further data analysis with the required number of participants.

3.2. Measures

To quantify the antecedent factor (culture) to the independent variables, this study adopted seven items referred to by [34]. To measure another antecedent factor (trust), seven items as recommended by [69] were adapted. For selecting 12 items, the protocols of [116] were used, which helped measure the independent variables and the three primary components of intellectual capital (human, structural and relational capitals). Additionally, the fourth critical component of intellectual capital (social capital) was measured by adapting four items from the work of [117]. In this study, the dependent variables (six items) were used to measure the respondents’ innovation performance following [88] (see Appendix A). Responses were made on a 5-point scale ranging from 1 (strongly disagree) to 5 (strongly agree).

4. Data Analysis and Results

There were two main stages to the data analysis. The first stage was conducted using SPSS.v25 to provide information about the data distribution, the response rate, multicollinearity and coding. This was followed by the screening of the data to ensure there were no missing data or outliers. The second stage of the data analysis in the current study was conducted in two phases using AMOS.v24. The first phase was a confirmatory factor analysis (CFA) to assess the overall measurement model, while the second phase involved structural equation modelling (SEM), which included testing the hypothesis of the study.

4.1. Response Rate

To achieve the appropriate response rate, a total of 470 questionnaires were distributed to employees in 24 commercial banks in Iraq. Out of the 420 questionnaires that were returned to the researcher by the respondents, a total of 384 questionnaires showed a response rate of 89.4%, from which 20 questionnaires were excluded due to incomplete answers of the respondents. Thus, a total of 364 questionnaires was considered for the analysis, yielding a response rate of 77.4%. Table 1 shows the distribution of the questionnaires and the response rate.

Table 1.

Response rate obtained from the data collected through survey questionnaires.

4.2. Normality

The normality of the dataset was assessed in terms of the skewness and the kurtosis. Skewness signifies the degree to which the distribution of a variable is symmetrical. Conversely, kurtosis measures the peakedness or peak intensity of the distribution [118]. According to the rule of thumb, if the skewness and kurtosis values lie within the range of ± 2.58, the data distribution is considered normal [118]. The results showed that the skewness ranged from −0.283 to −0.037 and the kurtosis ranged from −0.614 to 0.420. Thus, the data distribution in the present study can be considered normal. In contrast, the mean and the standard deviation were in the range of 3.112 and 3.692 and 0.640 and 0.919, respectively. Table 2 presents the computed skewness, the kurtosis, the mean and the standard deviation of each variable.

Table 2.

Obtained values of multivariate skewness and kurtosis.

4.3. Measurement Model Assessment

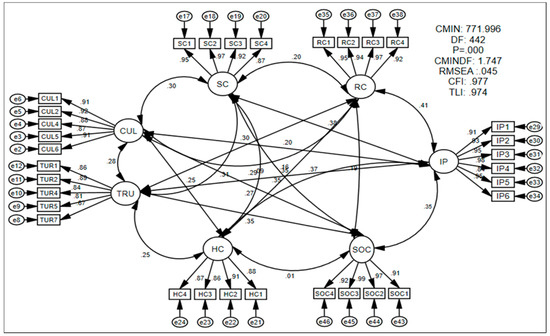

The proposed measurement model in this study comprised seven latent variables with 34 observed variables. Once the model was successfully built using AMOS software, the assessment process started with the measurement of the model. The results revealed that the reliability of the outer loadings was higher than 0.70, indicating the acceptable level of the items with good reliability. The factor loading estimates for all the items (ranging from 0.84 to 0.96) were above the minimum cut-off point. By modifying the model, the factor loadings for the items CUL3 and CUL7 corresponding to the culture variable were found to be 0.36 and 0.36, whereas those for the items TRU3 and TRU6 from the variable trust were found to be 0.33 and 0.29. These values were also lower than the minimum cut-off point. Consequently, the decision was taken to eliminate these items from the model and re-estimate the model to achieve a better model fit. Confirmatory factor analysis (see Figure 2) showed a CMIN value of 771.996 with 442 degrees of freedom, and the ratio of CMIN value to the degrees of freedom was 1.747. The normed CMIN value was smaller than 5, indicating an acceptable fit for the CFA model. The p-value was 0.000, and the value for the root mean square error of approximation (RMSEA) was 0.045 without exceeding 0.08. In addition, the value of the comparative fit index (CFI) was 0.977, suggesting its acceptable model fit. The calculated value of the Tucker–Lewis index (TLI) was 0.974. Overall, the results showed satisfactory indicators of the measurement model. Figure 2 displays the measurement model’s structure.

Figure 2.

Assessment of measurement modelling. Note: CUL = culture; TRU = trust; HC = human capital; SC = structural capital; RC = relational capital; SOC = social capital; IP = innovation performance.

Convergent validity is a type of variable validity. It is the extent to which scale items are presumed to be representative of a variable based on a range of facts about the same variables. Table 3 provides the results for the acceptable indicators of reliability and convergent validity. It is worth mentioning that the convergent validity calculation was adopted to measure the validity of the variables and, thereby, the extent to which the scale items could present a variable based on a range of facts about the same variables. Conversely, the values of Cronbach’s alpha (α) for all the variables were above 0.70 and ranged from 0.85 to 0.97. Furthermore, the values of composite reliability (CR) of all the variables were greater than 0.70 and ranged from 0.93 to 0.98. The values of average variance extracted (AVE) for all the variables were greater than 0.50 and between 0.73 and 0.90. Based on these results, it can be asserted that the present research acquired the recommended levels of convergent validity.

Table 3.

Overall convergent validity of the proposed measurement model.

Table 4 demonstrates the overall construct correlation of the measurement model wherein the square root of the AVE exceeded the off-diagonal values in rows and columns, indicating fulfilment of the discriminant validity criterion. Alternatively, the discriminant validity determines the extent to which the scores on a measure are uncorrelated with the measures of the conceptually distinct variables. Overall, the reliability and validity criterion assessment showed that the measurement model was satisfactory and fulfilled the requirement of validity to proceed with the estimation of the parameter that characterises the structural equation model.

Table 4.

Overall construct correlation of the measurement model.

4.4. Structural Equation Modelling Assessment

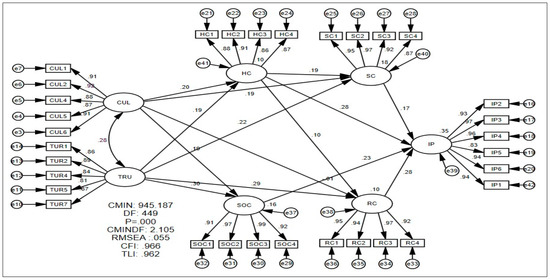

Figure 3 shows the proposed structural equation modelling enclosing all the study variables. In this study, the structural model was generated and estimated using SPSS.v25 and AMOS.v24. Previous literature considered structural equation modelling (SEM) as a reliable method for examining the inter-dependent correlation amongst the research variables [119]. In fact, SEM was designed to assess the proposed conceptual model that could fit the data collected to ascertain the structural relationships amongst these variables [120]. Table 5 reveals that the direction of the relationship between the variables had antecedent factors that are directly related to the independent variables. Another direct relationship was observed amongst the independent and dependent variables. The results of the structural equation modelling (see Figure 2) displayed a CMIN value of 945.187 with 449 degrees of freedom, and the ratio of CMIN value to the degrees of freedom was 2.105. The normed CMIN value was less than 5, indicating an acceptable fit for the SEM model. The p-value was 0.000, and the value of the root mean square error of approximation (RMSEA) was 0.055 without exceeding 0.08. In addition, the value of the comparative fit index (CFI) was 0.966, suggesting its acceptable model fit. The calculated value of the Tucker–Lewis index (TLI) was 0.962. Overall, the results showed satisfactory indicators of the final structural equation modelling.

Figure 3.

Assessment of the structural equation modelling. Note: CUL = culture; TRU = trust; HC = human capital; SC = structural capital; RC = relational capital; SOC = social capital; IP = innovation performance.

Table 5.

Relationship between culture and intellectual capital.

4.5. Hypothesis Testing

As mentioned earlier, the statistical method used in this study was structural equation modelling, which uses the fitness of the structural equation model to test a research hypothesis. To investigate a hypothesis, the path coefficients are calculated first. Then, the significance of these coefficients is determined by the t-value statistics. If the absolute t-value of the test statistic is greater than 1.96 (the critical value at the level of 0.05), then at a 95% confidence level, the path and the path coefficient of the target are significant; otherwise, the path coefficient is not significant.

Analysis of the direct relationship between culture and the four components of intellectual capital (human capital, relational capital, social capital and structural capital) indicates a positive or negative and significant relationship between them. The result of hypothesis H1a strongly supports a positive and significant relationship between culture and human capital (β = 0.195; t = 3.496; p < 0.000). The result of hypothesis H1b strongly supports a positive and significant relationship between culture and structural capital (β = 0.189; t = 3.548; p < 0.000). The results of hypothesis H1c supports a negative and insignificant relationship between culture and relational capital (β = −0.014; t = −0.245; p < 0.807). The results of hypothesis H1d support a positive and significant relationship between culture and social capital (β = 0.192; t = 3.669; p < 0.000). The results of the relationship between culture and intellectual capital are displayed in Table 5.

Analysis of the direct relationship between trust and the four components of intellectual capital (human capital, relational capital, social capital and structural capital) indicates a positive and significant relationship between them. The results of hypothesis H2a support a significant positive relationship between the variables of trust and human capital (β = 0.193; t = 3.412; p < 0.000). The results of hypothesis H2b strongly support a positive and significant relationship between trust and structural capital (β = 0.220; t = 4.077; p < 0.000). The results of hypothesis H2c support a positive and significant relationship between trust and relational capital (β = 0.286; t = 5.023; p < 0.000). The results of hypothesis H2d support a significant positive relationship between the variables of trust and social capital (β = 0.304; t = 5.645; p < 0.000). The results of the relationship between trust and intellectual capital exhibition are provided in Table 6.

Table 6.

Relationship between trust and intellectual capital.

The results of hypothesis H3 support a positive and significant relationship between human capital and structural capital (β = 0.194; t = 3.627; p < 0.000). The results of hypothesis H4 display a negative and insignificant relationship between human capital and relational capital (β = 0.097; t = 0.1745; p < 0.081). The relationship between human, relational and structural capitals is shown in Table 7.

Table 7.

Relationship between human, relational and structural capitals.

Analysis of the direct relationship between the components of intellectual capital and innovation performance displays a positive and significant relationship between them. The results of hypothesis H5a support a positive and significant relationship between human capital and innovation performance (β = 0.284; t = 5.863; p < 0.000). The results of hypothesis H5b support a positive and significant relationship between structural capital and innovation performance (β = 0.171; t = 3.671; p < 0.000). The results of hypothesis H5c support a positive and significant relationship between relational capital and innovation performance (β = 0.284; t = 6.263; p < 0.000). The results of hypothesis H5d support a positive and significant relationship between social capital and innovation performance (β = 0.231; t = 5.157; p < 0.000). The results of the relationship between intellectual capital and innovation performance are illustrated in Table 8.

Table 8.

Relationship between intellectual capital and innovation performance.

5. Discussion and Conclusions

A robust correlation was established between the antecedent factor of culture and the main components of intellectual capital. The findings of cultural impacts on intellectual capital support hypotheses H1a, H1b and H1d (t = 3.496, 3.548 and 3.669, respectively). It was demonstrated that Iraqi banks predominantly reflect some flexibility regarding culture to gain higher levels of human and structural capital. Conversely, the results do not support hypothesis H1c since no statistical significance was found between the antecedent factor of culture and the relational capital component of intellectual capital (t = −0.245). This result differs from those of the previous studies [38]. This inconsistency may be due to the different culture measurement scales, such as the competing-values approach [121,122]. This discrepancy may also emanate from an obvious cultural difference in terms of the attributes of relational capital in the Iraqi context and research conducted within the Western settings [27]. These findings also lend empirical support to the theoretical observations consistent with previous studies [33,36,48,123,124].

This study hypothesised that the antecedent factor of trust could positively affect all four components of intellectual capital. The legitimacy of this hypothesis was tested. The results reveal that there is a strong link between trust and the four components of intellectual capital (human, structural, relational and social capitals), supporting hypotheses H2a, H2b, H2c and H2d (t = 3.412, 4.077, 5.023 and 5.645, respectively). This implies that commercial banks in Iraq reflect a greater extent of trust to acquire higher levels of intellectual capital. The research outcomes strongly indicate the essential role of trust in the development of intellectual components within Iraqi commercial banks. In other words, trust is determinative in promoting the process of intellectual capital development in the context of Iraqi commercial banks. The present findings agree well with those of other studies [6,36,53,60,69].

Moreover, this research hypothesised significant impacts of human capital on structural and relational capital. The results support the influences of human capital on structural capital, represented through hypothesis H3 (t = 3.627). It was inferred that the banks reflect a flexible impact of human capital to achieve a higher level of structural capital. In contrast, the present outcomes do not support hypothesis H4 since no statistical significance was found between human and relational capitals (t = 1.745), which are in disagreement with earlier reports [37,78,125]. This inconsistency may be due to the different relational measurements [71,126] and obvious cultural difference in terms of relational capital features between Iraq and Western nations.

Furthermore, these hypotheses were made to examine whether the components of intellectual capital are positively correlated to the bank’s innovation performance. In this respect, the present outcomes support the positive impact of intellectual capital components on the Iraqi commercial banks’ innovation performance, validating hypotheses H5a (t = 5.863), H5b (t = 3.671), H5c (t = 6.263) and H5d (t = 5.157). Furthermore, it was reaffirmed that investment in human capital and structural capital rather than other intellectual capital can potentially bring higher levels of innovation performance improvement in Iraqi commercial banks. These findings are consistent with the existing literature that demonstrates the positive role played by human capital in enhancing commercial banks’ performance [85,86] when compared with the intellectual capital development. The outcomes of this research support the existing data in the literature concerning the correlation between relational capital and banks’ innovation performance [52,85,86,88,90,109,116,127,128,129,130].

Finally, the present conceptualisation of innovation predicted some positive impacts on an organisation’s productivity in the competitive markets. It was shown that the improved innovation performance of banks can be maintained as an empirical intellectual property. Two shortcomings of the previous studies were identified, and a new framework was formulated to resolve these issues. This work evaluated the role of innovation performance in a bank’s growth through intellectual capital, a concept in transition economies seldom addressed by earlier researchers. Following a resource-based view approach, the literature on developing countries showed that organisations’ internal capacity for innovation is limited, making the introduction of innovation less likely and restricting organisations from attaining required innovations. Based on these facts, it was argued that more specialised knowledge and resources might be found for suggesting a shift towards an integrated innovation approach.

The present findings reveal the emphasis on the enhancement of intellectual capital, which defines the levels of innovation performance in commercial banks. The findings are in good agreement with the idea that knowledge-intensive banks should be capable of planning and formulating knowledge-based strategies, communicating and showing the value relevance of such strategies. The integration of financial and non-financial techniques must lead to the development of suitable innovation performance, thereby ensuring that these strategies are realised in the performed financial tasks. To sum up, the results of this study are in harmony with the views in most other reports in the literature on the complexity of measuring intellectual capital, which influences the innovation performance in commercial banks.

5.1. Theoretical Implications

The contribution of this work to the existing state-of-the-art knowledge database was systematically analysed to understand the relationship between intellectual capital and innovation performance for the first time. This allowed Iraqi commercial banks to enhance intellectual property, acting as an indicator for sustaining a high level of innovation performance. It is strongly believed that the generated knowledge can help academicians and scholars to recognise the appropriate indicators of intellectual property that can act as better predictors for an organisation’s success in competitive markets in addition to furthering assessment and development. In addition, this study detected high impacts of the antecedent factors of culture and trust on the level of intellectual property in the commercial banks of Iraq to attain the highest innovation performance.

The current findings extend our understanding of the necessary reforms and mechanisms for enhancing intellectual capital in the context of Iraqi commercial banks. Most previous studies are on organisations in developed nations, which may not be fully applicable to emerging economies [81]. In contrast, this research focused on the common features of emerging economies, such as underdeveloped, market-supporting institutions, weak laws and rapid changes in the context of developing countries at varied settings [131,132,133,134].

5.2. Practical Implications

Intellectual capital can contribute to healthy innovation performance in the banking sector. This study presented a useful strategy for practitioners, scholars and policy makers to follow by examining the logical factors of intellectual property that can indicate reasons for non-perfect relationships between intellectual capital and innovation performance amongst banking institutions that highly impact the national economic policy. In brief, the study showed that intellectual capital requires more focus on strategic planning in the commercial banking sector. It showed some important managerial implications of the integration between intellectual capital and innovation performance, representing a causal connection between the two concepts.

In addition, this study provided some broad evidence for academics, local business leaders and government officials to play a more active role in encouraging the development of intellectual property or capital in their respective organisations. The proposed conceptual framework would enable them to acquire valid and practical measurements to identify the intellectual property in multidimensional relationships. This concept was incorporated with the findings of [135], which stated that financial institutions can acquire specific standards for identifying and developing their strategic resources and capabilities.

Together, the present disclosure affirms that intellectual-capital-based success is the essential component of and a prerequisite for the annual reports of every organisation. This may be one way of raising the profile of the intellectual capital usage in the banking sector as well as creating a uniform platform for investors to exploit the potential of intellectual capital property better. This concept can enable bank management to make successful and practical plans in the competitive markets, thus providing further elucidations to academicians about the dynamic relationship between intellectual capital property and innovation performance.

5.3. Limitations and Future Research

Despite the several notable contributions made by this study, it has some limitations. These limitations have been explained in this section, indicating the trustworthiness of the present research findings. The first limitation is related to the conceptual design that maintains a balance between the diagnostic and interactive use in Iraqi commercial banks. Such a design for different banking sectors, involving factors such as strategic and structural changes, overcoming the contemporary environmental opportunities or threats that intensify the competition and new regulation in the organisation, may not be completely applicable. Thus, the examination of these factors can offer a more comprehensive understanding of the mechanisms and conditions of the model fit in various banking sectors.

The next limitation is that this study depended mainly on a single research instrument represented by a survey questionnaire developed under controlled conditions and relying on the perception and opinions of the participants as key informants. Though the research instrument was tested for reliability and validity, previous scholars have indicated the existence of some bias when participants assess their own intellectual capital and innovation performance, which reflects in the bank’s performance. From this standpoint, one may analyse the annual reports of banks to compare and verify the information provided by the respondents in the questionnaire for better legitimacy of the developed research framework. The present conceptual model is examined with a cross-sectional technique rather than a longitudinal one, which may be unable to reflect the real causal relationship between long-term effects for future direction. Thus, the model may miss the effect of time, a limitation of the present study.

Instead, the present conclusive evidence was in line with the theoretical arguments and various outcomes reported in the literature. Future research might embark on a longitudinal survey to determine the causality and interrelationships amongst the present research constructs that are pivotal to the intellectual capital and innovation performance of the financial sector. In addition, the main area for future research is represented in developing an intellectual capital model that will be in multidimensional agreement with the International Accounting Standard Board 215 (IASB) in various research contexts. Moreover, the intellectual capital model must be observed by both internal management and external stakeholders for better innovation performance. The limitations of the present research indicate a way for the development of future lines of research. This study focused on using a single source of information, the consultation at the bank employees’ level, without considering other representative variables to measure innovation capacity. In future longitudinal studies, the opinions of various employees and multiple sources of information from management and other managerial levels should be included to confirm their impact on the development of intellectual capital and innovation performance.

Author Contributions

Conceptualization, M.A.A., N.H., H.H., R.A.-A. and I.A.A.; methodology, M.A.A. and N.H.; formal analysis M.A.A., N.H., H.H., R.A.-A. and I.A.A.; investigation, M.A.A. and N.H.; resources, M.A.A. and N.H.; writing original draft preparation, M.A.A.; writing review and editing, M.A.A. and N.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all participants involved in the study.

Data Availability Statement

The data presented in this study are available on request from the authors.

Acknowledgments

The authors also are grateful to the editor and the anonymous reviewers for providing very constructive and useful comments that enabled us to make additional efforts to improve the clarity and quality of our research.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Measurement Items

| Culture |

|

|

|

|

|

|

|

| Trust |

|

|

|

|

|

|

|

| Human Capital |

|

|

|

|

| Structural Capital |

|

|

|

|

| Relational Capital |

|

|

|

|

| Social Capital |

|

|

|

|

| Innovation Performance |

|

|

|

|

|

|

References

- Tastan, S.; Davoudi, S.M.M. A research on the relevance of intellectual capital and employee job performance as measured with distinct constructs of in-role and extra-role behaviors. Indian J. Sci. Technol. 2015, 8, 724–734. [Google Scholar] [CrossRef]

- Rindermann, H.; Kodila-Tedika, O.; Christainsen, G. Cognitive capital, good governance, and the wealth of nations. Intelligence 2015, 51, 98–108. [Google Scholar] [CrossRef]

- Deltorn, J.-M. Deep creations: Intellectual property and the automata. Front. Digit. Humanit. 2017, 4, 3. [Google Scholar] [CrossRef]

- Zambon, S.; Dumay, J. A critical reflection on the future of intellectual capital: From reporting to disclosure. J. Intellect. Cap. 2016, 17, 168–184. [Google Scholar]

- Al-Musali, M.A.; Ku Ismail, K.N.I. Cross-country comparison of intellectual capital performance and its impact on financial performance of commercial banks in GCC countries. Int. J. Islam. Middle East. Financ. Manag. 2016, 9, 512–531. [Google Scholar] [CrossRef]

- Allameh, S.M. Antecedents and consequences of intellectual capital: The role of social capital, knowledge sharing and innovation. J. Intellect. Cap. 2018, 19, 858–874. [Google Scholar] [CrossRef]

- Cabrilo, S.; Kianto, A.; Milic, B. The effect of IC components on innovation performance in Serbian companies. VINE J. Inf. Knowl. Manag. Syst. 2018, 48, 448–466. [Google Scholar] [CrossRef]

- Jardon, C.M.; Martos, M.S. Intellectual capital as competitive advantage in emerging clusters in Latin America. J. Intellect. Cap. 2012, 13, 462–481. [Google Scholar] [CrossRef]

- Bogers, M.; Chesbrough, H.; Heaton, S.; Teece, D.J. Strategic Management of Open Innovation: A Dynamic Capabilities Perspective. Calif. Manag. Rev. 2019, 62, 77–94. [Google Scholar] [CrossRef]

- Nevado, B.; Contreras-Ortiz, N.; Hughes, C.; Filatov, D.A. Pleistocene glacial cycles drive isolation, gene flow and speciation in the high-elevation Andes. New Phytol. 2018, 219, 779–793. [Google Scholar] [CrossRef]

- Ali, M.A.; Hussin, N.; Abed, I.A.; Othman, R.; Mohammed, M.A. Analysis and Measurement of Human Capital Based on Multi-Criteria Decision- Making (MCDM) Technique. Technol. Rep. Kansai Univ. 2020, 62, 4799–4825. [Google Scholar]

- Alford, P.; Duan, Y. Understanding collaborative innovation from a dynamic capabilities perspective. Int. J. Contemp. Hosp. Manag. 2018, 30, 2396–2416. [Google Scholar] [CrossRef]

- Ali, M.A.; Hussin, N.; Abed, I.A.; Nikkeh, N.S.; Mohammed, M.A. Dynamic Capabilities and Innovation Performance: Systematic Literature Review. Technol. Rep. Kansai Univ. 2020, 62, 5989–6000. [Google Scholar]

- Isanzu, J.N. The Relationship Between Intellectual Capital and Financial Performance of Banks in Tanzania. J. Innov. Sustain. 2017, 7, 28. [Google Scholar] [CrossRef][Green Version]

- Xu, J.; Shang, Y.; Yu, W.; Liu, F.; Han, Y.; Li, D.; Singh, B.; Rao, M.K.; Xin, J.; Ansari, R.; et al. Intellectual Capital, Knowledge Sharing, and Innovation Performance: Evidence from the Chinese Construction Industry. Res. J. Bus. Manag. 2019, 20, 603–630. [Google Scholar] [CrossRef]

- Nazari, J.A.; Herremans, I.M. Extended VAIC model: Measuring intellectual capital components. J. Intellect. Cap. 2007, 8, 595–609. [Google Scholar] [CrossRef]

- Ali, M.A.; Hussin, N.; Abed, I.A.; Othman, R.; Qahatan, N. Systematic Review of Intellectual Capital and Firm Performance. Technol. Rep. Kansai Univ. 2020, 62, 4199–4216. [Google Scholar]

- Hsu, L.C.; Wang, C.H. Clarifying the Effect of Intellectual Capital on Performance: The Mediating Role of Dynamic Capability. Br. J. Manag. 2012, 23, 179–205. [Google Scholar] [CrossRef]

- Ferreira, A.; Franco, M. The mediating effect of intellectual capital in the relationship between strategic alliances and organizational performance in Portuguese technology-based SMEs. Eur. Manag. Rev. 2017, 14, 303–318. [Google Scholar] [CrossRef]

- Wendra, W.; Sule, E.T.; Joeliaty, J.; Azis, Y. Exploring dynamic capabilities, intellectual capital and innovation performance relationship: Evidence from the garment manufacturing. Bus. Theory Pract. 2019, 20, 123–136. [Google Scholar] [CrossRef]

- Aluchna, M.; Roszkowska-Menkes, M. Non-Financial Reporting. Conceptual Framework, Regulation and Practice; Stehr, C., Przytuła, S., Długopolska, A., Eds.; CSR in Poland; Springer: Berlin/Heidelberg, Germany, 2018; forthcoming. [Google Scholar] [CrossRef]

- Peñalba-Aguirrezabalaga, C.; Sáenz, J.; Ritala, P. Marketing-specific intellectual capital: Conceptualization, scale development and empirical illustration. J. Intellect. Cap. 2020, 21, 947–984. [Google Scholar] [CrossRef]

- Abhayawansa, S.; Guthrie, J.; Bernardi, C. Intellectual capital accounting in the age of integrated reporting: A commentary. J. Intellect. Cap. 2019. [Google Scholar] [CrossRef]

- Arfah, A. Does Intellectual Capital have a Positive Effect on the e-Service Innovation of Public Employees? Available SSRN. 2019. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3487358 (accessed on 29 September 2021).

- Ali, M.A.; Hussin, N.; Abed, I.A.; Khalaf, B.K.; Nader, A. Systematic Literature Review of Intellectual Capital Components (Multi-View). Test Eng. Manag. 2020, 83, 4682–4700. [Google Scholar]

- Dabić, M.; Lažnjak, J.; Smallbone, D.; Švarc, J. Intellectual capital, organisational climate, innovation culture, and SME performance: Evidence from Croatia. J. Small Bus. Enterp. Dev. 2019, 26, 522–544. [Google Scholar] [CrossRef]

- Ghiasi, S.; Mehralizadeh, Y.; Husseinpoor, M.; Nasiri, M. Designing a Model for Culture-Oriented Intellectual Capital in Iranian Universities. Sci. J. Islam. Manag. 2020, 28, 193–219. [Google Scholar]

- Attar, M. Organisational Culture, Knowledge Sharing and Intellectual Capital: Directions for Future Research. Int. Bus. Inf. Manag. Assoc. 2020, 9, 11–20. [Google Scholar]

- Andreeva, T.; Garanina, T. Do all elements of intellectual capital matter for organizational performance? Evidence from Russian context. J. Intellect. Cap. 2016, 17, 397–412. [Google Scholar] [CrossRef]

- Haris, M.; Yao, H.; Tariq, G.; Malik, A.; Javaid, H. Intellectual Capital Performance and Profitability of Banks: Evidence from Pakistan. J. Risk Financ. Manag. 2019, 12, 56. [Google Scholar] [CrossRef]

- Abdal, M.; Alzuod, K.; Faizal, M.; Isa, M.; Zubaidah, S.; Othman, B. International Review of Management and Marketing Intellectual Capital, Innovative Performance and the Moderating Effect of Entrepreneurial Orientation among Small and Medium-sized Enterprises in Jordan. Int. Rev. Manag. Mark. 2017, 7, 308–314. [Google Scholar]

- Kaya, T.; Erkut, B. Tacit knowledge for strategic advantage: Social media use of employees in the financial sector. Proc. Eur. Conf. Knowl. Manag. ECKM 2017, 1, 516–523. [Google Scholar]

- Boneh, D.; Gentry, C.; Lynn, B.; Shacham, H. Aggregate and verifiably encrypted signatures from bilinear maps. In Proceedings of the International Conference on the Theory and Applications of Cryptographic Techniques, Warsaw, Poland, 4–8 May 2003; Springer: Berlin/Heidelberg, Germany, 2003; pp. 416–432. [Google Scholar]

- Reino, A.; Rõigas, K.; Müürsepp, M. Connections between organisational culture and financial performance in Estonian service and production companies. Balt. J. Manag. 2020, 15, 375–393. [Google Scholar] [CrossRef]

- Osinski, M.; Selig, P.M.; Matos, F.; Roman, D.J. Methods of evaluation of intangible assets and intellectual capital. J. Intellect. Cap. 2017, 18, 470–485. [Google Scholar] [CrossRef]

- Asiaei, K.; Jusoh, R. A multidimensional view of intellectual capital: The impact on organizational performance. Manag. Decis. 2015, 53, 668–697. [Google Scholar] [CrossRef]

- Massaro, M.; Mas, F.D.; Bontis, N.; Gerrard, B. Intellectual capital and performance in temporary teams. Manag. Decis. 2019, 58, 410–427. [Google Scholar] [CrossRef]

- Khosravipour, N.; Hamidian, M.; Asaadi, A. The role of management accounting systems in the development of intellectual (Human) capital. Int. J. Econ. Perspect. 2017, 11, 232–242. [Google Scholar] [CrossRef]

- Manes Rossi, F.; Citro, F.; Bisogno, M. Intellectual capital in action: Evidence from Italian local governments. J. Intellect. Cap. 2016, 17, 696–713. [Google Scholar] [CrossRef]

- Rangkuti, M.M.; Bukit, R.; Daulay, M. The Effect of Intellectual Capital and Financial Performance on Firm Value with Return on Investment as a Modeling Variable in the Mining Industry Listed on Indonesia Stock Exchange. Int. J. Public Budg. Account. Financ. 2020, 2, 1–11. [Google Scholar]

- Budiarso, N.S. Intellectual Capital in Public Sector. Accountability 2019, 8, 42. [Google Scholar] [CrossRef]

- Shafer, W.E.; Poon, M.C.C.; Tjosvold, D. Ethical climate, goal interdependence, and commitment among Asian auditors. Manag. Audit. J. 2013, 28, 217–244. [Google Scholar] [CrossRef]

- Berezinets, I.; Garanina, T.; Ilina, Y. Intellectual capital of a board of directors and its elements: Introduction to the concepts. J. Intellect. Cap. 2016, 17, 632–653. [Google Scholar] [CrossRef]

- Passaro, R.; Quinto, I.; Thomas, A. The impact of higher education on entrepreneurial intention and human capital. J. Intellect. Cap. 2018, 19, 135–156. [Google Scholar] [CrossRef]

- Pedro, E.; Leitão, J.; Alves, H. Intellectual capital and performance: Taxonomy of components and multi-dimensional analysis axes. J. Intellect. Cap. 2018, 19, 407–452. [Google Scholar] [CrossRef]

- Massaro, M.; Dumay, J.; Bagnoli, C. Where there is a will there is a way: IC, strategic intent, diversification and firm performance. J. Intellect. Cap. 2015, 16, 490–517. [Google Scholar] [CrossRef]

- Kim, T.; Chang, J. Organizational culture and performance: A macro-level longitudinal study. Leadersh. Organ. Dev. J. 2019, 40, 65–84. [Google Scholar] [CrossRef]

- Aureli, S.; Giampaoli, D.; Ciambotti, M.; Bontis, N. Key factors that improve knowledge-intensive business processes which lead to competitive advantage. Bus. Process Manag. J. 2019, 25, 126–143. [Google Scholar] [CrossRef]

- Kweh, Q.L.; Lu, W.M.; Wang, W.K. Dynamic efficiency: Intellectual capital in the chinese non-life insurance firms. J. Knowl. Manag. 2014, 18, 937–951. [Google Scholar] [CrossRef]

- Makhaiel, N.K.B.; Sherer, M.L.J. The effect of political-economic reform on the quality of financial reporting in Egypt. J. Financ. Rep. Account. 2018, 16, 245–270. [Google Scholar] [CrossRef]

- Chang, W.F.; Amran, A.; Iranmanesh, M.; Foroughi, B. Drivers of sustainability reporting quality: Financial institution perspective. Int. J. Ethics Syst. 2019, 35, 632–650. [Google Scholar] [CrossRef]

- Khalique, M.; Bontis, N.; Bin Shaari, J.A.N.; Yaacob, M.R.; Ngah, R. Intellectual capital and organisational performance in Malaysian knowledge-intensive SMEs. Int. J. Learn. Intellect. Cap. 2018, 15, 20–36. [Google Scholar] [CrossRef]

- Sadq, Z.M.; Ahmad, B.S.; Saeed, V.S.; Othman, B.; Mohammed, H.O. The relationship between intellectual capital and organizational trust and its impact on achieving the requirements of entrepreneurship strategy (The case of Korek Telecom Company, Iraq). Int. J. Adv. Sci. Technol. 2020, 29, 2639–2653. [Google Scholar]

- Secundo, G.; Massaro, M.; Dumay, J.; Bagnoli, C. Intellectual capital management in the fourth stage of IC research: A critical case study in university settings. J. Intellect. Cap. 2018, 19, 157–177. [Google Scholar] [CrossRef]

- Dumay, J.; La Torre, M.; Farneti, F. Developing trust through stewardship. J. Intellect. Cap. 2019, 20, 11–39. [Google Scholar] [CrossRef]

- Bontis, N. Assessing knowledge assets: A review of the models used to measure intellectual capital. Int. J. Manag. Rev. 2001, 3, 41–60. [Google Scholar] [CrossRef]

- Ali, M.A.; Hussin, N.; Jabbar, H.K.; Abed, I.A.; Othman, R.; Mohammed, A. Intellectual Capital and Firm Performance Classification and Motivation: Systematic Literature Review. Test Eng. Manag. 2020, 3, 28691–28703. [Google Scholar]

- Jiang, C.; Rashid, R.M.; Wang, J. Investigating the role of social presence dimensions and information support on consumers’ trust and shopping intentions. J. Retail. Consum. Serv. 2019, 51, 263–270. [Google Scholar] [CrossRef]

- Riahi-Belkaoui, A. Antecedents and Consequences of Earnings Opacity: An International Contingency Theory. SSRN Electron. J. 2009. [Google Scholar] [CrossRef]

- Savolainen, T. Trust and knowledge sharing in service business management. In Proceedings of the 2nd International Conference on Tourism Research, Porto, Portugal, 14–15 March 2019. [Google Scholar]

- Asiaei, K.; Jusoh, R. Using a robust performance measurement system to illuminate intellectual capital. Int. J. Account. Inf. Syst. 2017, 26, 1–19. [Google Scholar] [CrossRef]

- Palazzi, F.; Sgrò, F.; Ciambotti, M.; Bontis, N. Technological intensity as a moderating variable for the intellectual capital–performance relationship. Knowl. Process Manag. 2020, 27, 3–14. [Google Scholar] [CrossRef]

- Joshi, M.; Kansal, M.; Sharma, S. Awareness of intellectual capital among bank executives in India: A survey. Int. J. Account. Inf. Manag. 2018, 26, 291–310. [Google Scholar] [CrossRef]

- Sarjana, S.; Khayati, N.; Warini, L.; Praswiyati, P. Strengthening of Intellectual Capital Dimension. J. Din. Manaj. 2017, 8, 216–232. [Google Scholar] [CrossRef][Green Version]

- Jain, P.; Vyas, V.; Roy, A. Exploring the mediating role of intellectual capital and competitive advantage on the relation between CSR and financial performance in SMEs. Soc. Responsib. J. 2017, 13, 1–23. [Google Scholar] [CrossRef]

- Asiaei, K.; Barani, O.; Bontis, N.; Arabahmadi, M. Unpacking the black box: How intrapreneurship intervenes in the intellectual capital-performance relationship? J. Intellect. Cap. 2020, 21, 809–834. [Google Scholar] [CrossRef]

- Asiaei, K.; Jusoh, R.; Bontis, N. Intellectual capital and performance measurement systems in Iran. J. Intellect. Cap. 2018, 19, 294–320. [Google Scholar] [CrossRef]

- Al-Jinini, D.K.; Dahiyat, S.E.; Bontis, N. Intellectual capital, entrepreneurial orientation, and technical innovation in small and medium-sized enterprises. Knowl. Process Manag. 2019, 26, 69–85. [Google Scholar] [CrossRef]

- Paliszkiewicz, J.; Koohang, A. Organizational trust as a foundation for knowledge sharing and its influence on organizational performance. Online J. Appl. Knowl. Manag. 2013, 1, 116–127. [Google Scholar]

- Hammad Ahmad Khan, H.; Yaacob, M.A.; Abdullah, H.; Abu Bakar Ah, S.H. Factors affecting performance of co-operatives in Malaysia. Int. J. Product. Perform. Manag. 2016, 65, 641–671. [Google Scholar] [CrossRef]

- Ansari, R.; Barati, A.; Sharabiani, A.A.A. The role of dynamic capability in intellectual capital and innovative performance. Int. J. Innov. Learn. 2016, 20, 47–67. [Google Scholar] [CrossRef]

- Bogdan, V.; Sabău Popa, C.D.; Beleneşi, M.; Burja, V.; Popa, D.N. Empirical analysis of intellectual capital disclosure and financial performance—Romanian evidence. Econ. Comput. Econ. Cybern. Stud. Res. 2017, 51, 125–143. [Google Scholar]

- Hamad, A.A.; Tuzlukaya, Ş.; Kırkbeşoğlu, E. The Effect of Social Capital on Operational Performance: Research in Banking Sector in Erbil. Copernic. J. Financ. Account. 2019, 8, 101. [Google Scholar] [CrossRef]

- Haji, A.A. Trend of hidden values and use of intellectual capital information: Evidence from Malaysia. Account. Res. J. 2016, 29, 81–105. [Google Scholar] [CrossRef]

- Heaton, S.; Siegel, D.S.; Teece, D.J. Universities and innovation ecosystems: A dynamic capabilities perspective. Ind. Corp. Chang. 2019, 28, 921–939. [Google Scholar] [CrossRef]

- Ahmed, S.S.; Guozhu, J.; Mubarik, S.; Khan, M.; Khan, E. Intellectual capital and business performance: The role of dimensions of absorptive capacity. J. Intellect. Cap. 2019, 21, 23–39. [Google Scholar] [CrossRef]

- Poh, L.T.; Kilicman, A.; Ibrahim, S.N.I. On intellectual capital and financial performances of banks in Malaysia. Cogent Econ. Financ. 2018, 6, 1453574. [Google Scholar] [CrossRef]

- Pedro, E.; Leitão, J.; Alves, H. Back to the future of intellectual capital research: A systematic literature review. Manag. Decis. 2018, 56, 2502–2583. [Google Scholar] [CrossRef]

- Erkut, B. From digital government to digital governance: Are we there yet? Sustainability 2020, 12, 860. [Google Scholar] [CrossRef]

- Guerrero-Baena, M.D.; Gómez-Limón, J.A.; Fruet, J.V. A multicriteria method for environmental management system selection: An intellectual capital approach. J. Clean. Prod. 2015, 105, 428–437. [Google Scholar] [CrossRef]

- Chowdhury, L.A.M.; Rana, T.; Akter, M.; Hoque, M. Impact of intellectual capital on financial performance: Evidence from the Bangladeshi textile sector. J. Account. Organ. Chang. 2018, 14, 429–454. [Google Scholar] [CrossRef]

- Wang, Z.; Wang, N.; Cao, J.; Ye, X. The impact of intellectual capital—Knowledge management strategy fit on firm performance. Manag. Decis. 2016, 54, 1861–1885. [Google Scholar] [CrossRef]