Spillover Effects of Green Finance on Attaining Sustainable Development: Spatial Durbin Model

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

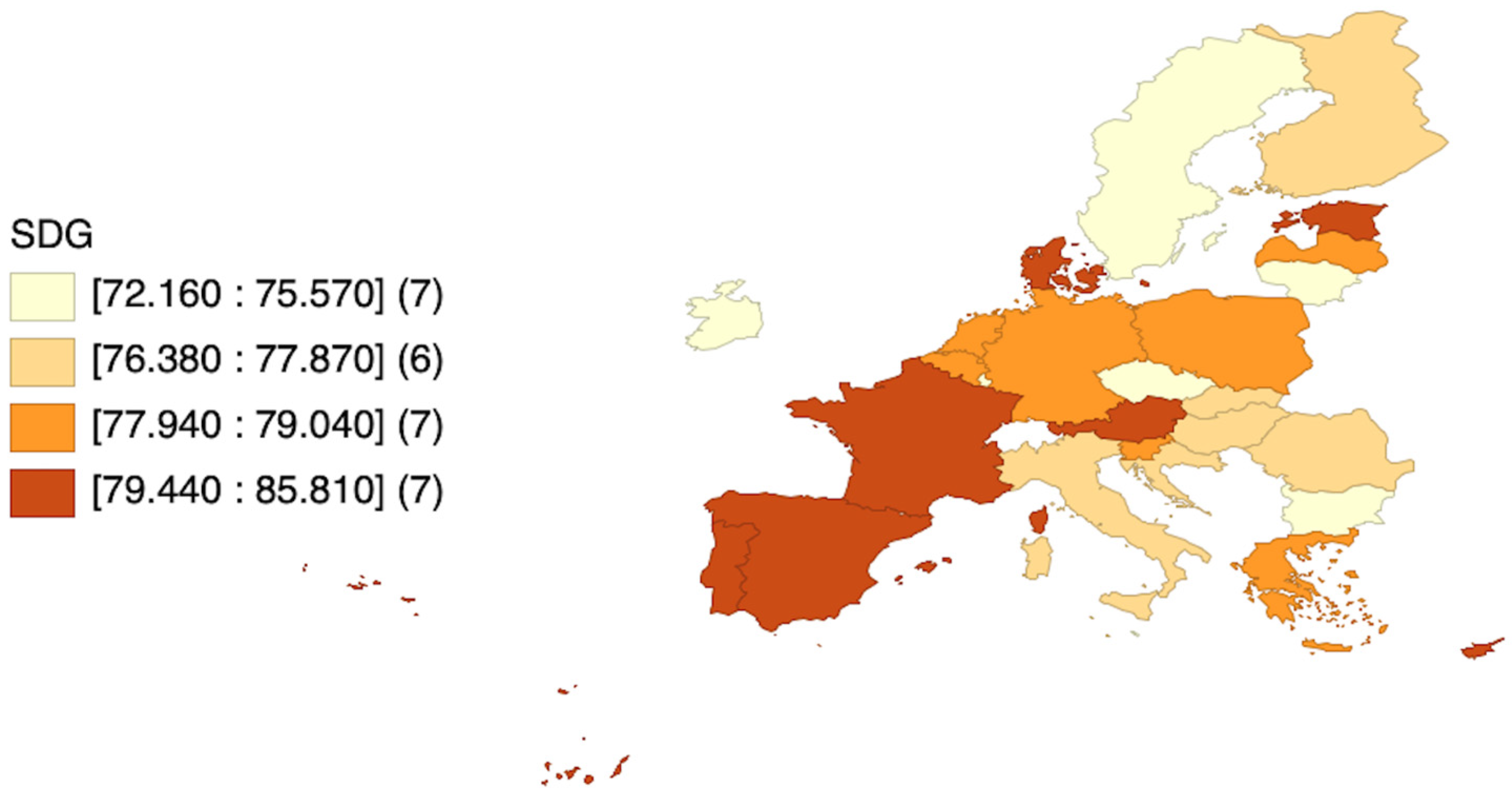

3.1. Explanation of the Variables

3.2. Econometric Methodology

4. Results

5. Discussion

6. Conclusions

- Recognize the regional heterogeneity in the impact of green finance and design targeted strategies that address the unique needs and challenges of each EU region. This entails conducting thorough assessments of the local context, identifying the specific sectors with the greatest potential for green finance integration, and understanding the regulatory landscapes unique to each region. Policymakers should develop targeted strategies that align with the existing strengths of the region while mitigating the barriers that may hinder the adoption of green finance initiatives. For instance, regions with a robust renewable energy sector benefit from incentivizing investments in clean energy technologies. Meanwhile, areas grappling with high population density could explore innovative urban planning solutions, and sustainable transport projects enabled by green finance. Similarly, regions facing specific environmental challenges, such as water scarcity or biodiversity loss, could direct green finance toward projects that directly address these concerns.

- Encourage cross-border collaboration among EU regions to share best practices and experiences related to green finance. By fostering knowledge exchange [74,75], regions learn from successful initiatives, adapt them to their contexts, and collectively drive progress toward SDGs. This cross-regional learning process enables each region to adapt and customize successful initiatives to suit their specific circumstances and needs. By building upon proven models and avoiding the pitfalls experienced by others, regions save valuable time and resources in implementing green finance measures. Collaboration fosters a sense of collective responsibility and solidarity among EU regions, creating a cohesive front in the pursuit of sustainable development.

- Establish robust monitoring and evaluation mechanisms to measure the effectiveness of green finance interventions in different regions [76,77,78]. A well-designed monitoring and evaluation framework allows for the collection of quantitative and qualitative data that reflect the progress made in different regions. This information sheds light on the extent to which green finance interventions are contributing to SDGs, whether they are reducing carbon emissions, promoting renewable energy adoption, or enhancing environmental quality.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Kaul, S.; Akbulut, B.; Demaria, F.; Gerber, J.F. Alternatives to sustainable development: What can we learn from the pluriverse in practice? Sustain. Sci. 2022, 17, 1149–1158. [Google Scholar] [CrossRef] [PubMed]

- Mhlanga, D. The role of artificial intelligence and machine learning amid the COVID-19 pandemic: What lessons are we learning on 4IR and the sustainable development goals. Int. J. Environ. Res. Public Health 2022, 19, 1879. [Google Scholar] [CrossRef] [PubMed]

- Akkuş, Y.; Çalıyurt, K. The role of sustainable entrepreneurship in un sustainable development goals: The case of ted talks. Sustainability 2022, 14, 8035. [Google Scholar] [CrossRef]

- Pell, O. The ESG Triangle: How Lithium Mining in Latin America Could Point the Way Toward Long-Term Environmental and Social Value Strategies. In Critical Minerals, the Climate Crisis and the Tech Imperium; Springer Nature: Cham, Switzerland, 2023; pp. 179–201. [Google Scholar]

- Versal, N.; Sholoiko, A. Green bonds of supranational financial institutions: On the road to sustainable development. Invest. Manag. Financ. Innov. 2022, 19, 91–105. [Google Scholar] [CrossRef] [PubMed]

- Li, C.; Umair, M. Does green finance development goals affects renewable energy in China. Renew. Energy 2023, 203, 898–905. [Google Scholar] [CrossRef]

- Li, G.; Zhang, R.; Feng, S.; Wang, Y. Digital finance and sustainable development: Evidence from environmental inequality in China. Bus. Strategy Environ. 2022, 31, 3574–3594. [Google Scholar] [CrossRef]

- Lu, Q.; Farooq, M.U.; Ma, X.; Iram, R. Assessing the combining role of public–private investment as a green finance and renewable energy in carbon neutrality target. Renew. Energy 2022, 196, 1357–1365. [Google Scholar] [CrossRef]

- Debrah, C.; Chan, A.P.C.; Darko, A. Green finance gap in green buildings: A scoping review and future research needs. Build. Environ. 2022, 207, 108443. [Google Scholar] [CrossRef]

- Kwilinski, A.; Slatvitskaya, I.; Dugar, T.; Khodakivska, L.; Derevyanko, B. Main Effects of Mergers and Acquisitions in International Enterprise Activities. Int. J. Entrep. 2020, 24, 1–8. [Google Scholar]

- Dementyev, V.; Dalevska, N.; Kwilinski, A. Innovation and Information Aspects of the Structural Organization of the World Political and Economic Space. Virtual Econ. 2021, 4, 54–76. [Google Scholar] [CrossRef]

- Trushkina, N.; Abazov, R.; Rynkevych, N.; Bakhautdinova, G. Digital Transformation of Organizational Culture under Conditions of the Information Economy. Virtual Econ. 2020, 3, 7–38. [Google Scholar] [CrossRef] [PubMed]

- Melnychenko, O. Application of artificial intelligence in control systems of economic activity. Virtual Econ. 2019, 2, 30–40. [Google Scholar] [CrossRef] [PubMed]

- Trzeciak, M.; Kopec, T.P.; Kwilinski, A. Constructs of Project Programme Management Supporting Open Innovation at the Strategic Level of the Organization. J. Open Innov. Technol. Mark. Complex. 2022, 8, 58. [Google Scholar] [CrossRef]

- Letunovska, N.; Offei, F.A.; Junior, P.A.; Lyulyov, O.; Pimonenko, T.; Kwilinski, A. Green Supply Chain Management: The Effect of Procurement Sustainability on Reverse Logistics. Logistics 2023, 7, 47. [Google Scholar] [CrossRef]

- Miśkiewicz, R.; Matan, K.; Karnowski, J. The Role of Crypto Trading in the Economy, Renewable Energy Consumption and Ecological Degradation. Energies 2022, 15, 3805. [Google Scholar] [CrossRef]

- Trushkina, N. Development of the information economy under the conditions of global economic transformations: Features, factors and prospects. Virtual Econ. 2019, 2, 7–25. [Google Scholar] [CrossRef] [PubMed]

- Pudryk, D.; Kwilinski, A.; Lyulyov, O.; Pimonenko, T. Toward Achieving Sustainable Development: Interactions between Migration and Education. Forum Sci. Oeconomia 2023, 11, 113–132. [Google Scholar] [CrossRef]

- Chen, Y.; Lyulyov, O.; Pimonenko, T.; Kwilinski, A. Green development of the country: Role of macroeconomic stability. Energy Environ. 2023, 1–23. [Google Scholar] [CrossRef]

- Zhanibek, A.; Abazov, R.; Khazbulatov, A. Digital Transformation of a Country’s Image: The Case of the Astana International Finance Centre in Kazakhstan. Virtual Econ. 2022, 5, 71–94. [Google Scholar] [CrossRef]

- Chen, Y.; Kwilinski, A.; Chygryn, O.; Lyulyov, O.; Pimonenko, T. The Green Competitiveness of Enterprises: Justifying the Quality Criteria of Digital Marketing Communication Channels. Sustainability 2021, 13, 13679. [Google Scholar] [CrossRef]

- Stępień, S.; Smędzik-Ambroży, K.; Polcyn, J.; Kwiliński, A.; Maican, I. Are small farms sustainable and technologically smart? Evidence from Poland, Romania, and Lithuania. Cent. Eur. Econ. J. 2023, 10, 116–132. [Google Scholar] [CrossRef]

- Us, Y.; Pimonenko, T.; Lyulyov, O.; Chen, Y.; Tambovceva, T. Promoting Green Brand of University in Social Media: Text Mining and Sentiment Analysis. Virtual Econ. 2022, 5, 24–42. [Google Scholar] [CrossRef] [PubMed]

- Prokopenko, O.; Miśkiewicz, R. Perception of “green shipping” in the contemporary conditions. Entrep. Sustain. Issues 2020, 8, 269–284. [Google Scholar] [CrossRef] [PubMed]

- Letunovska, N.; Abazov, R.; Chen, Y. Framing a Regional Spatial Development Perspective: The Relation between Health and Regional Performance. Virtual Econ. 2022, 5, 87–99. [Google Scholar] [CrossRef] [PubMed]

- Arefieva, O.; Polous, O.; Arefiev, S.; Tytykalo, V.; Kwilinski, A. Managing sustainable development by human capital reproduction in the system of company`s organizational behavior. IOP Conf. Ser. Earth Environ. Sci. 2021, 628, 012039. [Google Scholar] [CrossRef]

- Dźwigoł, H. The Uncertainty Factor in the Market Economic System: The Microeconomic Aspect of Sustainable Development. Virtual Econ. 2021, 4, 98–117. [Google Scholar] [CrossRef]

- Sachs, J.D.; Lafortune, G.; Fuller, G.; Drumm, E. Implementing the SDG Stimulus. Sustainable Development Report 2023; SDSN: Paris, France; Dublin University Press: Dublin, Ireland, 2023. [Google Scholar] [CrossRef]

- Lafortune, G.; Fuller, G.; Bermont-Diaz, L.; Kloke-Lesch, A.; Koundouri, P.; Riccaboni, A. Achieving the SDGs: Europe’s Compass in a Multipolar World. Europe Sustainable Development Report 2022; SDSN and SDSN Europe: Paris, France, 2022. [Google Scholar]

- Rasoulinezhad, E.; Taghizadeh-Hesary, F. Role of green finance in improving energy efficiency and renewable energy development. Energy Effic. 2022, 15, 14. [Google Scholar] [CrossRef]

- Ahmed, N.; Areche, F.O.; Sheikh, A.A.; Lahiani, A. Green Finance and Green Energy Nexus in ASEAN Countries: A Bootstrap Panel Causality Test. Energies 2022, 15, 5068. [Google Scholar] [CrossRef]

- Ronaldo, R.; Suryanto, T. Green finance and sustainability development goals in Indonesian Fund Village. Resour. Policy 2022, 78, 102839. [Google Scholar] [CrossRef]

- Huang, H.; Mbanyele, W.; Wang, F.; Song, M.; Wang, Y. Climbing the quality ladder of green innovation: Does green finance matter? Technol. Forecast. Soc. Chang. 2022, 184, 122007. [Google Scholar] [CrossRef]

- Zhang, L.; Saydaliev, H.B.; Ma, X. Does green finance investment and technological innovation improve renewable energy efficiency and sustainable development goals. Renew. Energy 2022, 193, 991–1000. [Google Scholar] [CrossRef]

- Mohanty, S.; Nanda, S.S.; Soubhari, T.; Vishnu, N.S.; Biswal, S.; Patnaik, S. Emerging Research Trends in Green Finance: A Bibliometric Overview. J. Risk Financ. Manag. 2023, 16, 108. [Google Scholar] [CrossRef]

- Du, M.; Ruirui, Z.; Shanglei, C.; Qiang, L.; Ruixuan, S.; Wenjun, C. Can Green Finance Policies Stimulate Technological Innovation and Financial Performance? Evidence from Chinese Listed Green Enterprises. Sustainability 2022, 14, 9287. [Google Scholar] [CrossRef]

- Bei, J.; Wang, C. Renewable energy resources and sustainable development goals: Evidence based on green finance, clean energy and environmentally friendly investment. Resour. Policy 2023, 80, 103194. [Google Scholar] [CrossRef]

- Jian, X.; Afshan, S. Dynamic effect of green financing and green technology innovation on carbon neutrality in G10 countries: Fresh insights from CS-ARDL approach. Econ. Res.-Ekon. Istraživanja 2023, 36, 2130389. [Google Scholar] [CrossRef]

- Hasan, M.M.; Du, F. Nexus between green financial development, green technological innovation and environmental regulation in China. Renew. Energy 2023, 204, 218–228. [Google Scholar] [CrossRef]

- Li, J.; Dong, X.; Dong, K. How much does financial inclusion contribute to renewable energy growth? Ways to realize green finance in China. Renew. Energy 2022, 198, 760–771. [Google Scholar] [CrossRef]

- Zhang, H.; Geng, C.; Wei, J. Coordinated development between green finance and environmental performance in China: The spatial-temporal difference and driving factors. J. Clean. Prod. 2022, 346, 131150. [Google Scholar] [CrossRef]

- Lu, Y.; Gao, Y.; Zhang, Y.; Wang, J. Can the green finance policy force the green transformation of high-polluting enterprises? A quasinatural experiment based on “Green Credit Guidelines”. Energy Econ. 2022, 114, 106265. [Google Scholar] [CrossRef]

- Saleem, H.; Khan, M.B.; Mahdavian, S.M. The role of green growth, green financing, and eco-friendly technology in achieving environmental quality: Evidence from selected Asian economies. Environ. Sci. Pollut. Res. 2020, 29, 57720–57739. [Google Scholar] [CrossRef]

- Jiakui, C.; Abbas, J.; Najam, H.; Liu, J.; Abbas, J. Green technological innovation, green finance, and financial development and their role in green total factor productivity: Empirical insights from China. J. Clean. Prod. 2023, 382, 135131. [Google Scholar] [CrossRef]

- Sun, Y.; Gao, P.; Razzaq, A. How does fiscal decentralization lead to renewable energy transition and a sustainable environment? Evidence from highly decentralized economies. Renew. Energy 2023, 206, 1064–1074. [Google Scholar] [CrossRef]

- Alamgir, M.; Cheng, M.-C. Do Green Bonds Play a Role in Achieving Sustainability? Sustainability 2023, 15, 10177. [Google Scholar] [CrossRef]

- Sancak, I.E. Change management in sustainability transformation: A model for business organizations. J. Environ. Manag. 2023, 330, 117165. [Google Scholar] [CrossRef] [PubMed]

- Islam, S.; Hosseini, S.H.; McPhillips, K. The Transformative Capacities of the Sustainable Development Goals: A Comparison Between the Global Critical Literature and Key Development Actors’ Perceptions in Bangladesh. In The Palgrave Handbook of Global Social Change; Springer International Publishing: Cham, Switzerland, 2022; pp. 1–22. [Google Scholar]

- Hughes, S.S.; Velednitsky, S.; Green, A.A. Greenwashing in Palestine/Israel: Settler colonialism and environmental injustice in the age of climate catastrophe. Environ. Plan. E Nat. Space 2023, 6, 495–513. [Google Scholar] [CrossRef]

- Wang, X.; Elahi, E.; Khalid, Z. Do Green Finance Policies Foster Environmental, Social, and Governance Performance of Corporate? Int. J. Environ. Res. Public Health 2022, 19, 14920. [Google Scholar] [CrossRef] [PubMed]

- Huang, Y.; Chen, C.; Lei, L.; Zhang, Y. Impacts of green finance on green innovation: A spatial and nonlinear perspective. J. Clean. Prod. 2022, 365, 132548. [Google Scholar] [CrossRef]

- Kwilinski, A.; Lyulyov, O.; Pimonenko, T. Environmental Sustainability within Attaining Sustainable Development Goals: The Role of Digitalization and the Transport Sector. Sustainability 2023, 15, 11282. [Google Scholar] [CrossRef]

- Babajide, A.; Lawal, A.; Asaleye, A.; Okafor, T.; Osuma, G. Financial stability and entrepreneurship development in sub-Sahara Africa: Implications for sustainable development goals. Cogent Soc. Sci. 2020, 6, 1798330. [Google Scholar] [CrossRef]

- Fagbemi, F. COVID-19 and sustainable development goals (SDGs): An appraisal of the emanating effects in Nigeria. Res. Glob. 2021, 3, 100047. [Google Scholar] [CrossRef]

- Wang, R.; Wang, F. Exploring the Role of Green Finance and Energy Development toward High-Quality Economic Development: Application of Spatial Durbin Model and Intermediary Effect Model. Int. J. Environ. Res. Public Health 2022, 19, 8875. [Google Scholar] [CrossRef]

- Cheng, P.; Wang, X.; Choi, B.; Huan, X. Green Finance, International Technology Spillover and Green Technology Innovation: A New Perspective of Regional Innovation Capability. Sustainability 2023, 15, 1112. [Google Scholar] [CrossRef]

- Guo, C.Q.; Wang, X.; Cao, D.D.; Hou, Y.G. The impact of green finance on carbon emission--analysis based on mediation effect and spatial effect. Front. Environ. Sci. 2022, 10, 844988. [Google Scholar] [CrossRef]

- Huo, D.; Zhang, X.; Meng, S.; Wu, G.; Li, J.; Di, R. Green finance and energy efficiency: Dynamic study of the spatial externality of institutional support in a digital economy by using hidden Markov chain. Energy Econ. 2022, 116, 106431. [Google Scholar] [CrossRef]

- Chen, X.; Chen, Z. Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces. Sustainability 2021, 13, 12137. [Google Scholar] [CrossRef]

- Mitchell, I.; Ritchie, E.; Tahmasebi, A. Is climate finance toward $100 billion “new and additional”. GCD Policy Pap. 2021, 205, 1–14. [Google Scholar]

- Mahat, T.J.; Bláha, L.; Uprety, B.; Bittner, M. Climate finance and green growth: Reconsidering climate-related institutions, investments, and priorities in Nepal. Environ. Sci. Eur. 2019, 31, 1–13. [Google Scholar] [CrossRef]

- Hussain, H.I.; Haseeb, M.; Kamarudin, F.; Dacko-Pikiewicz, Z.; Szczepańska-Woszczyna, K. The role of globalization, economic growth and natural resources on the ecological footprint in Thailand: Evidence from nonlinear causal estimations. Processes 2021, 9, 1103. [Google Scholar] [CrossRef]

- Szczepańska-Woszczyna, K.; Gedvilaitė, D.; Nazarko, J.; Stasiukynas, A.; Rubina, A. Assessment of Economic Convergence among Countries in the European Union. Technol. Econ. Dev. Econ. 2022, 28, 1572–1588. [Google Scholar] [CrossRef]

- Kharazishvili, Y.; Kwilinski, A. Methodology for Determining the Limit Values of National Security Indicators Using Artificial Intelligence Methods. Virtual Econ. 2022, 5, 7–26. [Google Scholar] [CrossRef]

- Moskalenko, B.; Lyulyov, O.; Pimonenko, T. The investment attractiveness of countries: Coupling between core dimensions. Forum Sci. Oeconomia 2022, 10, 153–172. [Google Scholar] [CrossRef]

- Karnowski, J.; Rzońca, A. Should Poland join the euro area? The challenge of the boom-bust cycle. Argum. Oeconomica 2023, 1, 227–262. [Google Scholar] [CrossRef]

- Savvidou, G.; Atteridge, A.; Omari-Motsumi, K.; Trisos, C.H. Quantifying international public finance for climate change adaptation in Africa. Clim. Policy 2021, 21, 1020–1036. [Google Scholar] [CrossRef]

- UNCTAD. World Investment Report. 2022. Available online: https://worldinvestmentreport.unctad.org (accessed on 10 December 2022).

- World Bank. Available online: https://data.worldbank.org (accessed on 14 April 2023).

- Mondal, S.; Kundu, D. Exact likelihood ratio and Wald tests for the balanced joint progressive censoring scheme. Appl. Stoch. Models Bus. Ind. 2022, 38, 1113–1126. [Google Scholar] [CrossRef]

- Ost, D.E. Interpretation and application of the likelihood ratio to clinical practice in thoracic oncology. J. Bronchol. Interv. Pulmonol. 2022, 29, 62–70. [Google Scholar] [CrossRef]

- Wang, B.X.; Hughes, V.; Foulkes, P. The effect of sampling variability on systems and individual speakers in likelihood ratio-based forensic voice comparison. Speech Commun. 2022, 138, 38–49. [Google Scholar] [CrossRef]

- LeSage, J.P.; Pace, R.K. The Biggest Myth in Spatial Econometrics. Econometrics 2014, 2, 217–249. [Google Scholar] [CrossRef]

- Dzwigol, H. Research Methodology in Management Science: Triangulation. Virtual Econ. 2022, 5, 78–93. [Google Scholar] [CrossRef]

- Szczepańska-Woszczyna, K.; Gatnar, S. Key Competences of Research and Development Project Managers in High Technology Sector. Forum Sci. Oeconomia 2022, 10, 107–130. [Google Scholar] [CrossRef]

- Dacko-Pikiewicz, Z. Building a family business brand in the context of the concept of stakeholder-oriented value. Forum Sci. Oeconomia 2019, 7, 37–51. [Google Scholar] [CrossRef]

- Miśkiewicz, R. Challenges facing management practice in the light of Industry 4.0: The example of Poland. Virtual Econ. 2019, 2, 37–47. [Google Scholar] [CrossRef] [PubMed]

- Karnowski, J.; Miśkiewicz, R. Climate Challenges and Financial Institutions: An Overview of the Polish Banking Sector’s Practices. Eur. Res. Stud. J. 2021, 24, 120–139. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

| Variable | Measurement | Source | Mean | SD | Min | Max |

|---|---|---|---|---|---|---|

| SDG | score | Sachs et al. [28] | 77.9 | 3.6 | 69.8 | 86.5 |

| GF | Millions of USD | UNTCAD [68] | 9141 | 15,712 | 3 | 84,826 |

| GDP | GDP per capita (current US$) | World Bank [69] | 34,086 | 23,150 | 6862 | 133,590 |

| PD | people per sq. km of land area | World Bank [69] | 176 | 265 | 17 | 1646 |

| WGI | unit | World Bank [69] | 1.03 | 0.49 | 0.09 | 1.87 |

| Test | Coef. | Prob. |

|---|---|---|

| Wald test spatial lag | 35.572 | 0.000 |

| Wald test spatial error | 41.175 | 0.000 |

| LR test spatial lag | 75.34 | 0.000 |

| LR test spatial error | 80.61 | 0.000 |

| Depend Variable: SDG | OLS | SDM | SAR | |||

|---|---|---|---|---|---|---|

| Coef. | Prob. | Coef. | Prob. | Coef. | Prob. | |

| GF | 0.005 | 0.000 | 0.004 | 0.000 | 0.006 | 0.000 |

| GDP | 0.007 | 0.074 | 0.008 | 0.089 | −0.001 | 0.805 |

| PD | −0.020 | 0.000 | −0.020 | 0.000 | −0.022 | 0.000 |

| WGI | 0.028 | 0.000 | 0.035 | 0.000 | 0.032 | 0.000 |

| W × GF | – | – | 0.009 | 0.000 | – | – |

| W × GDP | – | – | 0.009 | 0.348 | – | – |

| W × PD | – | – | -0.002 | 0.517 | – | – |

| W × WGI | – | – | 0.030 | 0.001 | – | – |

| R squared | 0.459 | 0.489 | 0.460 | |||

| Log-likelihood | – | 818.2348 | 800.9794 | |||

| AIC | – | −1616.471 | −1589.959 | |||

| BIC | – | −1577.121 | −1566.351 | |||

| Depend Variable: SDG | Direct | Indirect | Total | |||

|---|---|---|---|---|---|---|

| Coef. | Prob. | Coef. | Prob. | Coef. | Prob. | |

| GF | 0.005 | 0.000 | 0.009 | 0.000 | 0.004 | 0.041 |

| GDP | 0.007 | 0.141 | 0.005 | 0.509 | 0.013 | 0.122 |

| PD | −0.020 | 0.000 | 0.004 | 0.240 | −0.016 | 0.000 |

| WGI | 0.033 | 0.000 | 0.015 | 0.028 | 0.049 | 0.000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kwilinski, A.; Lyulyov, O.; Pimonenko, T. Spillover Effects of Green Finance on Attaining Sustainable Development: Spatial Durbin Model. Computation 2023, 11, 199. https://doi.org/10.3390/computation11100199

Kwilinski A, Lyulyov O, Pimonenko T. Spillover Effects of Green Finance on Attaining Sustainable Development: Spatial Durbin Model. Computation. 2023; 11(10):199. https://doi.org/10.3390/computation11100199

Chicago/Turabian StyleKwilinski, Aleksy, Oleksii Lyulyov, and Tetyana Pimonenko. 2023. "Spillover Effects of Green Finance on Attaining Sustainable Development: Spatial Durbin Model" Computation 11, no. 10: 199. https://doi.org/10.3390/computation11100199

APA StyleKwilinski, A., Lyulyov, O., & Pimonenko, T. (2023). Spillover Effects of Green Finance on Attaining Sustainable Development: Spatial Durbin Model. Computation, 11(10), 199. https://doi.org/10.3390/computation11100199