Abstract

Central bank communication has changed over the years, following the trend of digitalization. It has been used as a tool for the implementation of monetary policies since the 1990s, when central banks started publishing their inflation reports, outlooks, and meeting minutes on the road towards greater transparency, and to help meet their price stability mandate. This mandate cannot be achieved through traditional financial instruments alone, so digital communication and marketing has become an economic policy tool. The effectiveness of the European Central Bank’s online communication tools will be tested via a GAP model, by applying an adapted version of the servuction scale to the Bank and disseminating it to 500 citizens, with the purpose of measuring citizen satisfaction with its website and communications. The servuction model focuses on high quality services that are perceived as such by private sector customers, having a strong marketing component. The originality of the research consists in adapting it to the public sector, more specifically to central banks, and by treating citizens as customers throughout the study. The model was successfully applied to the European Central Bank, demonstrating that citizens’ expectations are highest regarding both the reliability and assurance dimensions, meaning that they want to feel confident in ECB actions, and to the understandability dimension of its online content. The largest gaps between citizens’ expectations and perceptions were identified within the efficiency, understandability, and empathy dimensions. In future, the study can be replicated and adapted to both national central banks and private banks within the European Union, assessing how citizens perceive their websites, communication, and marketing strategies, with the purpose of improving the latter two, and increasing civic engagement. The model can also be adapted to narrower topics relating to sustainable digital development, such as the expectations and perceptions of citizens with regards to central bank digital currencies.

1. Introduction

How is central bank information conveyed and what can be done to improve central bank marketing communication in the contemporary digital society? By being transparent, open, and releasing timely information regarding their financial outlook and monetary policies, central banks create a link between the latter and future inflation (Jung and Kühl 2021). Central banks, such as the US Federal Reserve, the European Central Bank (ECB), the Bank of England (BoE), Bank of Japan, and Banque de France focus primarily on acting and communicating about money supply and interest rates, with the goal of stabilizing the currency they are responsible for, stimulating the economy, and controlling inflation. They have a certain amount of power over the cost of money, which in exchange, can influence the amount of money spent by citizens, and private and public organizations (MonetaryPolicy 2022).

More than a decade ago, central bank studies confirmed that banks should be more careful in how they communicate with their audience (Blinder 2009). Currently, even though central bank communication has improved to a great extent, it is not ideal (Haldane and McMahon 2018); there is a need to improve transparency and communication dimensions and make central bank content easier to understand for citizens. In contemporary society, marked by the Fourth Industrial Revolution and an ever-evolving digital landscape, digital marketing communication strategies can be used to increase agility, competitivity, and transparency, both in the private and public sectors. Big data stemming from social media can be adopted as a communication tool and analysed to generate new strategies and even promote the smooth implementation of digital currencies, such as electronic money or central bank digital currencies, that are partly supported by artificial intelligence. This digital transformation is brought about by contemporary digital technologies, combined with the increasing digital activities of citizens, which, in turn, generates Big Data and expands the digital capacities of companies both in the private and public sector (Nyagadza 2022; Fragkos et al. 2020). Online communication with citizens is crucial in this context because the better central banks explain the reasoning behind their monetary policy decisions and actions, the more effective they will be. By disclosing comprehensive information about their strategies, mandates, decisions, and analyses, they can push the markets in the desired direction (Issing 2006).

To measure the quality of services, the literature (Parasuraman et al. 1988) proposed a novel scale, namely SERVQUAL. This scale has been frequently reduced and extended with the purpose of adapting it to certain service sectors (Buttle 1996). Most modifications have been made to the private service sectors rather than the public sectors. Avkiran (1994) applied it to Australian retail banks, Vasiliadis (2008) to Greek Cypriot banks, Newman and Cowling (1996) to British banks, Koushiki (2013) to the Indian banking sector, Ozretic-Dosen and Zizak (2015) to Croatian banks, and Khan and Imami (2020) to Bangladeshi banks. So far, no studies have applied the SERVQUAL scale or a modified version of it to central banks. The authors applied the SERVQUAL scale to the European Central Bank, having adapted it based on the above-mentioned applications of the scale on private banks, with the purpose of measuring citizen satisfaction, using a GAP model and asking questions regarding citizens’ expectations and perceptions concerning the European Central Bank’s communication via its website.

Given the public institution digitalization trend and following the fully digitalized trend in the private sector, with private companies having 100% digital services (Nyagadza 2022), as viable alternatives to traditional banking facilities, the aim of this paper is to investigate to what extent European citizens are satisfied with the quality of central bank services and communications strategy. In other words, the authors aim to explore the perceptions and expectations of citizens about the quality of central bank e-services, as presented on their website. In this regard, the authors have relied on a modified SERVQUAL approach, with the goal of pinpointing how an adapted version of this model can be applied to test citizen satisfaction towards central banks communication. The research scope is implemented by means of a case study developed for the European Central Bank, aimed at testing citizen satisfaction, given that in the public sphere, citizens are the equivalent of customers. The tested ECB e-service quality scale includes six dimensions adapted from the SERVQUAL (4 dimensions), E-SERVQUAL (1 dimension) and Webqual (1 dimension) scales and tested against 500 people via a questionnaire, using the convenience sampling method. Of these, 406 questionnaires were completed successfully. Each question had an expectation and perception aspect, the gap between these being measured to assess service quality.

The originality of the endeavour is based on the adaptation of private sector measurement tools to public organizations, such as central banks, and the intention to uncover the degree of citizen satisfaction with central banks. By implementing digitalization in their daily activities, central banks can improve citizens’ experiences, thus contributing to their general satisfaction. The paper aims to identify improvement areas in the following categories: reliability, responsiveness, assurance, empathy, efficiency, understandability when it comes to European Central Bank communication, and the categories with the highest importance in the eyes of the citizens, as well as those with the highest expectation/performance gaps.

The paper is structured as follows: Section 1 and Section 2 present the past and present state of public service quality evolution, with an emphasis on central banks and their marketing communication in the context of service quality, followed by a short review of the SERVQUAL and E-SERVQUAL scales, both of which are used for measuring service quality. Section 3 presents the results and discussions, while Section 4 contains the research methodology that revolves around the following research question: What are the perceptions and expectations regarding the quality of online communications of central banks? The conclusions are presented within Section 5.

2. The Quality of Public Sector Services Now and Then

The components of service typology in relation to the marketing and business-oriented service perspective were recorded more than 20 years ago (Cook et al. 1999). Marketing must be considered when designing future services and service processes, together with the information gained through service process analysis (Naik et al. 2010). The service quality dimension includes marketing variables such as intangibility, commitment, differentiation, customer type, and variables such as customer contact and involvement, customization degree, labour intensity, and employee direction (Fitzsimmons and Fitzsimmons 2006). With all these components in mind, service quality must be measured to be properly evaluated and improved, given that sector efficiency, quality, and performance are primary focus issues (Hsiao and Jie 2008).

Contemporary society demands that the public sector be more efficient and effective (Fountain 2002) as part of an alignment with the New Public Management (NPM) principles focusing on trust, transparency, and democratic dialogue (Fountain 2002; Serrat 2017; Andronie et al. 2021). These characteristics are based on meeting user and citizen needs. Therefore, measures have been implemented to incorporate NPM principles and improve the quality of public sector delivery, with states stepping in to assume responsibilities (Ling 2002; Indahsari and Raharja 2020).

NPM characteristics include cost cutting, decentralization, commitment of staff to performance targets and indicators, greater availability in public service employment, increased citizen focus, and service quality (Indahsari and Raharja 2020), in a context in which citizens prefer to solve their official obligations without having physical contact with the administration (Steinbach et al. 2019). Recent technological advancements, especially by means of digitalization, have eased the concentration of different public services, citizens now have the possibility of interacting online with administrations (Tagscherer and Carbon 2023; Windasari et al. 2022). However, measuring the impact of these modern alternatives represents a challenge (Steinbach et al. 2019) given that the conflicting interests of different stakeholders, such as citizens, civil servants, and politicians must be considered (Carvalho et al. 2010), and because of their rapid development.

From a methodological perspective, the procedures for measuring service quality can be applied to both private and public organizations; however, there are some limitations in the public sector, as it can be difficult to properly assess certain specific characteristics, such as intangibility and inseparability (Célérier et al. 2022). Moreover, there is no general agreement on a universal measurement scale. According to the expectation-disconfirmation paradigm, service quality follows from comparing performance and expectations (Oliver 1980; Siu et al. 2016; Pinquart et al. 2021). Several scales with different constructs and items have been developed over the years, which, to a certain extent, is the challenge. For instance, SERVQUAL (created by Parasuraman et al. 1988) measures service quality by analysing the gap between customer expectations and perceptions, while another scale, SERVPERF (by Cronin and Taylor 1992), measures only the actual performance of a service. SERVQUAL and SERVPERF, together with their extensions, remain the most widely used and studied service quality measurement scales (Carrillat et al. 2007; Bui Thi Thu et al. 2022).

2.1. Development of Central Bank Communication

How is central bank information transmitted? By being transparent and releasing timely information regarding their financial outlook, central banks create a link between monetary policy and future inflation (Jung and Kühl 2021). While, over a decade ago, central banks had to be careful about how they communicated with customers (Blinder 2009), despite the fact that communication has improved to a great extent, it is still not ideal (Haldane and McMahon 2018). Central banks need to improve transparency and communication techniques, by making their content easier for people to understand. Communication is crucial, because the better central banks explain the reasoning behind their monetary policy decisions, the more successful these decisions will be. Therefore, they need to disclose comprehensive information about their strategies, mandates, decisions, and analyses (Issing 2006; Ferrara and Angino 2022). Things have evolved over time, which has impacted central banking practice. Now that banks are much more transparent than previously, it is well-known that effective communication needs to be open, timely, and clear. In other words, central banks should provide as much information as possible, in a timely manner so that the public can make use of it immediately, leaving no room for various interpretations hindering transparency (Bulir and Smidkova 2008; Ferrara and Angino 2022).

As a result of expanding monetary policy frameworks and increased independence, communication and marketing communication now play a pivotal role as policy instruments: central banks are now careful about what and how they communicate about their current, future, and expanding mandates, so that the market actors know what a central bank can and cannot perform (Marcus 2014; Ferrara and Angino 2022). In the past 20 to 25 years, many central banks, including those of New Zealand, Norway, Sweden, and the European Central Bank, have led the way in becoming more transparent, emphasizing their communications strategies, and making it a global phenomenon (Weidmann 2018; Cross and Greene 2020). When the Federal Open Market Committee (FOMC) first made its choices about federal fund rate targets public in 1994, even the Fed followed this practice. Later, in 1999, they also started publishing information regarding their opinions on future monetary policy changes and more comprehensive statements. In 2002, they started announcing FOMC votes after their meetings, by 2005, they released FOMC meeting minutes just before meetings, and at the end of 2007, they started publishing more comprehensive forecasts on member growth, inflation, interest rates, and unemployment four times per year (Weidmann 2018; Cross and Greene 2020).

Central banks need to supply high quality information to citizens to be credible and successful in implementing their policies (Bicchal 2022). Communication at the central bank level has expanded, and transparency increased, in line with the belief that independent central banks need to be held accountable, describing their actions, and justifying the thinking behind them (Blinder et al. 2008; Bholat et al. 2019).

This increase in the degree of accountability came following government decisions to grant them independence. Given that central banks are not elected, yet carry a great deal of responsibility over money, it is in their best interests to make their policies known to the public, if they want to realize those policies and to be credible in the eyes of financial market participants (Belke 2017). Communication policy saw a shift from being a burden to becoming a key instrument when it became clear that the management of expectations can be used successfully in achieving monetary policy objectives by creating genuine news (and shifting short-term rates in the desired direction) and reducing market uncertainty by lowering the amount of noise (Blinder et al. 2008). Central bank communication is an important tool to increase transparency, enhance credibility, and better manage private sector expectations (Pescatori 2018; Bholat et al. 2019).

Central banks know that if markets understand their policy actions, they will be more effective. They need to do everything in their power to be transparent and achieve their mandate, given that they only control one interest rate. They need to potentially influence several interest rates and asset prices, which can be achieved through effective and transparent communication and credible policy actions (Belke 2017; Bennani 2020). The increase in transparency, when it comes to monetary policy, goes hand in hand with an improvement in central banks’ accountability before market participants, while the increasing degree of accountability is a result of them being granted independence from government and pushing the move towards more transparency and communication (Belke 2017; Bholat et al. 2019). This shift has been happening since the end of the 1990s, as communication and transparency became pillars of the monetary policy mandate, being part of the best practices toolkit of central bankers. The shift is ongoing, but great progress has already been made, as banks are no longer secretive, but tend to publish meeting minutes and communicate verbally in their transition toward more openness (Belke 2017; Haldane et al. 2020). In summary, the two main reasons for transparency are the fact that independence needs to be controlled by accountability, and that economic stability is fostered more easily if economic agents correctly and clearly understand the goals of central banks (Ekkehard and Merola 2018).

One key channel for central bank communication is traditional media, such as television, radio, and print news. This allows central banks to reach a wide audience and ensure that their messages are widely disseminated. For example, the FED regularly holds press conferences and issues statements that are widely covered by traditional media outlets (Federal Reserve 2022). Similarly, the Bank of England (BoE) uses traditional media to communicate with the public, including issuing press releases and holding press conferences (Bank of England 2022).

Digital transformations and technologies are now changing strategies within the private and public sector, both internally (by enhancing productivity and shifting ways of working) and externally (by creating added value for customers and digitalizing and adapting existing business models). They are broad, affecting organizations in their entirety. The leadership dimension within the digitalization context refers to having a vision regarding the transformation, accepting that change is the new constant, being digitally fluent as a leader, and willing to experiment and partner, while at the same time being customer- and employee-centric and promoting cultural diversity (Tagscherer and Carbon 2023). In this context, social media has become an important channel for central bank communication and digital strategy implementation. Several central banks, including the Federal Reserve and the ECB have active social media accounts on platforms such as Twitter, Facebook, and Instagram. Social media allows the banks to interact directly with the public and share information and analysis in a more informal and interactive way. For example, the ECB uses its Twitter account to share updates on monetary policy decisions, economic research, and educational resources (European Central Bank 2022; Federal Reserve 2022).

The ECB uses its website to publish its speeches, with the aim of ensuring greater monetary policy transparency. Speeches that are afterwards published on the website offer a unique and timely channel via which it can affect public opinion and behaviour due to the significant news coverage and potential to adapt topics to specific audiences. Over the ECB history, speeches have become more frequent and have all been posted on its website and translated in various languages of the European Union, depending on their importance. Between 1999 and 2020, the average number of delivered and published speeches per month nearly doubled. In terms of clarity, the typical length of a speech has significantly decreased over time. A gradual improvement in readability has coincided with the growth in conciseness. The typical number of education years needed to comprehend a speech has decreased by about two years. The ECB now offers a growing amount of information that is presented on its website in a more condensed and understandable manner. Nevertheless, the opaqueness of speeches has remained high in recent years, requiring nearly 14 years of education for comprehension. Early in 2020, readability declined, undoing the achievements made in Lagarde’s first several months in office (Glas and Müller 2021; Lazarevic et al. 2022). Several euro area studies (Calvo et al. 2013; Haldane and McMahon 2018; Prodan and Dabija 2022) highlight the fact that regular citizens who do not have higher education degrees have difficulties in comprehending essential publications such as the inflation reports outlining the Bank’s monetary policy directions. Haldane and McMahon (2018) performed a study in which the BoE inflation report was rewritten and made easily understandable to all citizens. The same experiment was conducted on the ECB inflation report in 2022 (Prodan and Dabija 2022), with the purpose of finding out whether better readability brought about an increased level of trust in the Bank’s actions. According to the results of both studies, inflation reports that are easily understood by citizens are viewed positively and enhance their trust in the messages contained therein.

2.2. Public Service Marketing Communication within Central Banks

How do users assess the quality of public services provided by central banks? In today’s competitive environment, service organizations, including central banks, must provide high-quality services to be credible and successful in implementing their policies (Bicchal 2022). During the 2007–2008 financial crisis, the confidence of citizens in central banks was shattered (Scalera and Dixon 2016). Despite this, research showing how loyalty and trust can be improved remains limited (Dabija et al. 2013). However, citizens are increasingly recognised as cornerstones in the provision of public services (Lamsal and Gupta 2022). Once a burden for central banks, marketing communication is now a key instrument, being used successfully to achieve monetary policy by creating genuine news (and shifting short-term rates in the desired direction) and reducing noise (thereby reducing market uncertainty) (Belke 2017).

The central bank marketing communication strategy represents an important tool for increasing organizational transparency, enhancing credibility and visibility among citizens (Lăzăroiu et al. 2020), and fostering their expectations. As a result, markets can respond more quickly and smoothly to policy decisions without going into financial distress due to strong movements in asset prices (Pescatori 2018).

One major goal of central banks is to target inflation, ensuring transparency and accountability, and linking it to their monetary policy (Belke and Polleit 2011; Stojanovikj 2022). Of course, this implies releasing timely information regarding their view on the inflation outlook (Belke and Polleit 2011), in a context in which monetary policymakers often deal with market uncertainty, economic shocks, and changes in economic patterns, further complicating monetary policy decisions and predictions. The economy never moves exactly according to projections (Mester 2018), making forecasting almost impossible.

Central banks in contemporary society must explain their monetary policy decisions to the public to increase confidence in their ability to manage monetary policy decisions. The central bank’s mandate on price stability is the equivalent of the service they offer to private and public institutions, and to citizens. Communication influences monetary policy, with regard to citizens’ expectations of the evolution of currency exchange courses, currency stability, inflation evolution, currency transformations, etc. For example, within the contemporary digital environment and emerging smart cities, electronic money and central bank digital currencies are becoming increasingly popular and controversial; likewise, communications around their positive and negative aspects are widely debated on social media platforms, such as Twitter. The main arguments in favour of them relate to ease of use and enforcement of anti-money laundering measures, while the main concerns revolve around privacy aspects, despite the fact that artificial intelligence can be used to improve the privacy and performance features. At the same time, members of Generations Y and Z strongly prefer digital-only banks and services and cashless payments, seeking ease of use, among other things (Weidmann 2018; Fragkos et al. 2020; Windasari et al. 2022; Prodan and Dabija 2023). Therefore, marketing communication with citizens is crucial (Krizanova et al. 2019) because the better central banks explain their reasoning behind the provided public services, such as monetary policy decisions, the more successful these decisions will be. Therefore, central banks must disclose comprehensive information about their strategies, mandates, decisions, and analyses (Weber 2020). The marketing communication strategy must be clear, comprehensive, and exhaustive. Because people have limited information processing skills, they weigh information based on how accessible it is. Moreover, they simplify and categorize it before grouping it and considering it. Central banks must transmit information clearly, accentuating and emphasizing it appropriately (Musa et al. 2021), without forgetting to convey the complexity and uncertainty related to economic conditions. They must rise to the challenge of communicating simply, while at the same time conveying the complexity of economic conditions (Hüning 2016). Feasibility should also be considered: central banks must ensure that the efforts and resources they invest for the purpose of reaching a wider audience are not wasted. This is a difficult task but can be achieved, for example, by using content that is easy to read and understand, to help improve the institution and alignment of general citizens’ beliefs with the forecasts of central banks (Haldane et al. 2020). Central banking and the provision of public services are perceived as an interactive process (Gajanova et al. 2020) in which banks and financial markets play crucial roles. Therefore, the success of monetary policy depends on responding to banks’ sensitivity to the changing context and their interactions with agents. The language and communication of banks’ decision-making have been shown to be a more effective way to guide market expectations (Kliestik et al. 2020), compared with promises to base decision-making on fixed numerical rules.

As interactions are based on common understanding, and do not come from the sender, everyday language should be preferred in communication by central banks. The idea that a coded language simulates certainty is misleading and will backfire because communication is not a linear practice, as has already been seen in the context of an economic crisis. The efficacy of a central bank is based on its capacity to act, and the acknowledgement of its actions by citizens. Drawing on research on the connection between central bank communication and language, financial texts should be made more accessible to citizens. This is important, since the quality of central bank services depends on adequate citizen participation (Ozretic-Dosen and Zizak 2015; Ramanathan et al. 2018). How can service quality be measured?

2.2.1. The SERVQUAL Scale

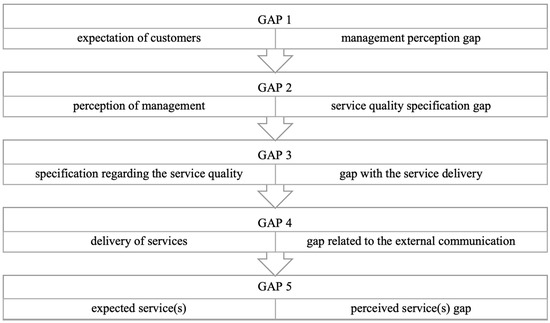

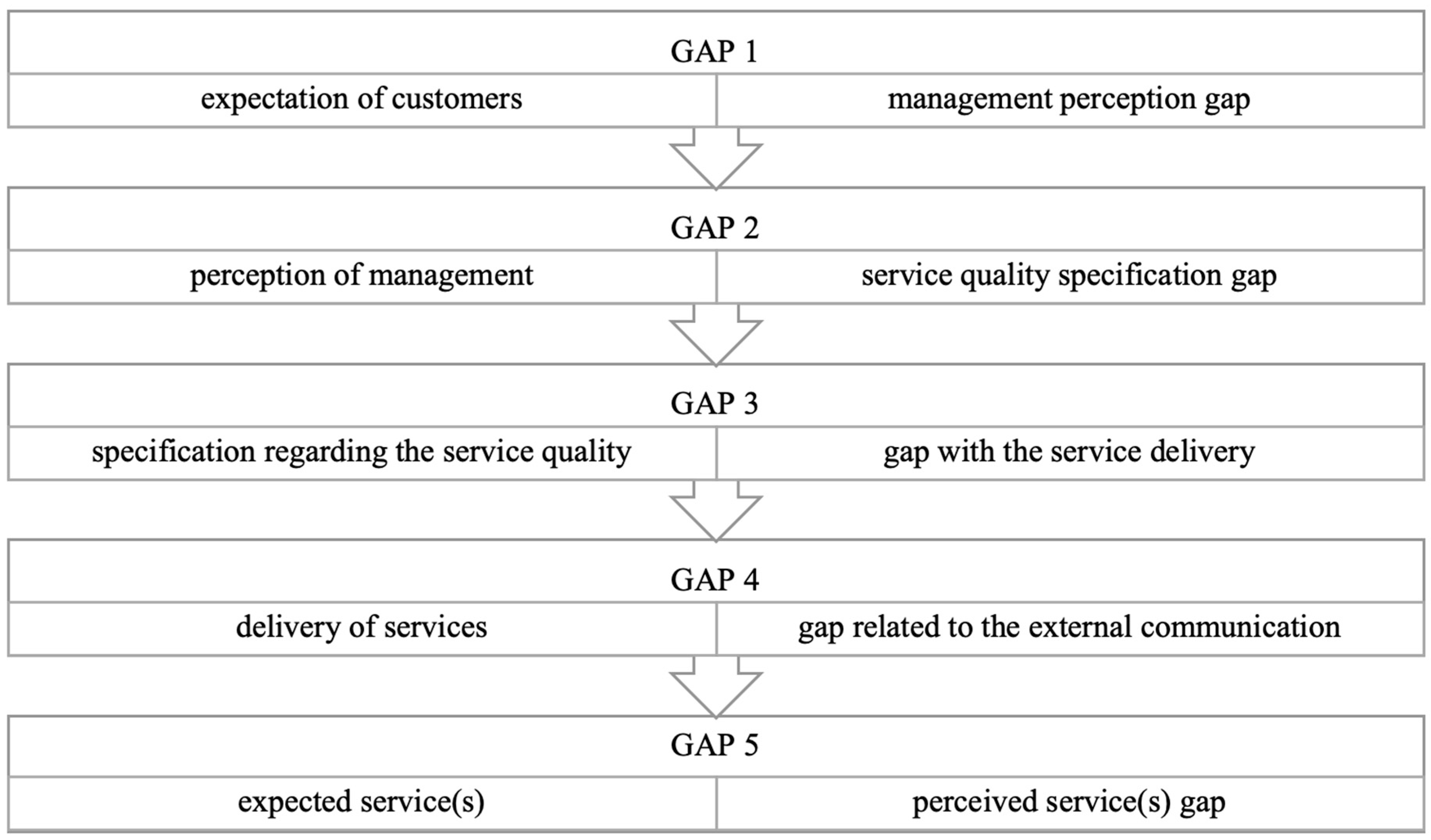

In 1984, Grönroos created a model for measuring grasped or perceived service quality, by measuring practical, functional, and reputation-related components of companies from a quality perspective. Only four years later, Parasuraman et al. (1988) designed the SERVQUAL scale, aimed at determining service quality by analysing the gap between expected performance in relation to actual performance from a customer perspective, via a GAP model, highlighted in Figure 1.

Figure 1.

Representation of the GAP model (Parasuraman et al. 1988).

SERVQUAL is extensively used to evaluate customer expectations and perceptions regarding service quality (Angur et al. 1999; Gajdosikova et al. 2023). The five most important dimensions impacting service quality are tangibility, responsiveness, assurance, reliability, and empathy (Parasuraman et al. 1988). Tangibility attributes incorporate facilities, equipment used, physical appearance of staff and the visual quality of printed documents, while responsiveness focuses on measuring whether the provided services are prompt and the concrete willingness to help the customer. Reliability attributes measure how accurately and professionally the service is performed (Rowland et al. 2021), while assurance covers attributes such as the level of confidence and trust inspired by the service provider to the customer. The last dimension, empathy, focuses on whether the customer feels appreciated and receives high-quality, individual attention. The attributes around the five above-mentioned dimensions have been centralized by Parasuraman within 22 items measured separately within the traditional scale, SERVQUAL, from an expectation and perception perspective (Parasuraman et al. 1988).

2.2.2. E-SERVQUAL

The early service quality models (Grönroos 1984; Parasuraman et al. 1985) evolved with the emergence of the Internet. At first, they addressed face-to-face interactions between providers and customers. Over the years, they have been adapted (Parasuraman et al. 2005) with the purpose of determining the service quality provided by websites, called E-SERVQUAL or E-S-QUAL and consisting of 22 items. Subsequent models, such as E-RecS-QUAL (Parasuraman et al. 2005), TailQ (Wolfinbarger and Gilly 2002), Webqual, and others have also been developed to measure website performance, given that e-service quality is directly proportional to customer loyalty and satisfaction (Oliveira et al. 2002). Table 1 illustrates the quality scales developed over the years, consisting of modified versions of the SERVQUAL scale.

Table 1.

Service quality dimensions (own enriched representation of e-service quality dimensions following the review by Li and Suomi 2009).

The main limitation of these models lies in the fact that they have not been adapted to different markets and have a unitary, industry-wide approach, regardless of sector specificities. Moreover, they mostly measure dimensions revolving around website features and customer service, and less about the level of service.

3. Results and Discussion

Given that the authors combined dimensions from three scales to measure citizen satisfaction, the reliability of the data was tested by applying the Cronbach’s alpha formula, a method used to measure the consistency of internal data and reliability of the scale. According to this method, the score must be greater than 0.7 for the data to be reliable and for internal consistency to be acceptable (Hair et al. 2010; Henseler and Sarstedt 2013). The authors measured the alpha coefficient of the questions that determined citizen expectations and perceptions. The expectations questions had an alpha coefficient of 0.77, while the questions measuring perceptions had one of 0.72. The fact that the score is higher than 0.7 shows that the data were reliable and the questions consistent.

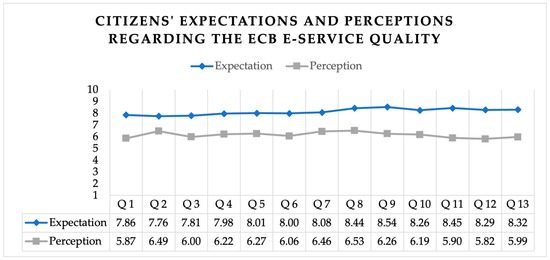

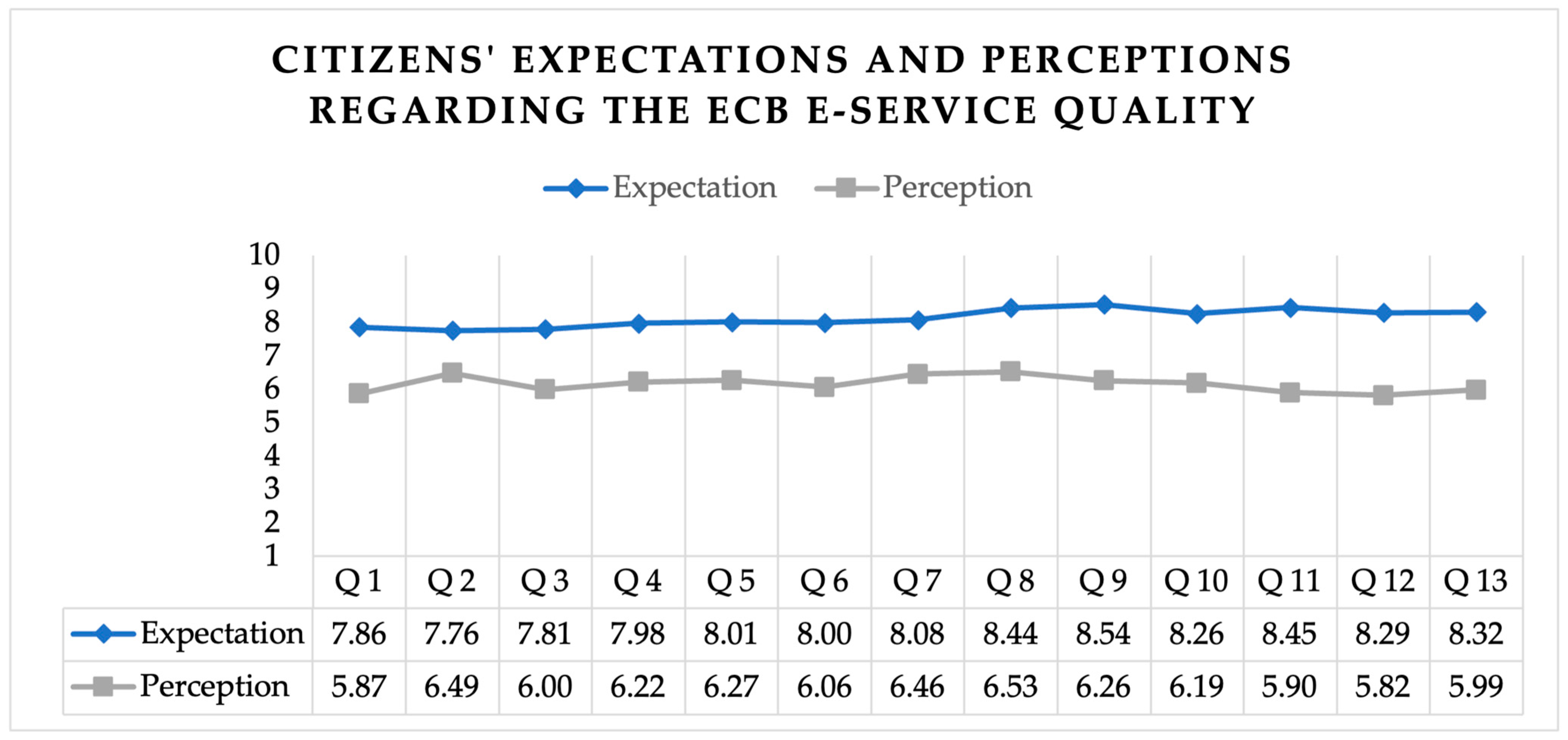

Figure 2 shows the descriptive statistical results of expectations versus perceptions of citizens. The highest gap was found within Question 11 (a gap of 2.55), which measured efficiency and asked participants if the ECB had information that was easy to find, while the lowest gap was measured within Question 2 (a gap of 1.27), where citizens were asked if the ECB took action on time. Therefore, it can be concluded that the ECB website search engine could be improved, since according to participants, information was not easy to find there. However, the general perception was that the ECB took action on time and was thus reliable, meaning that its communication with citizens, and its shift in communication strategies were starting to show results. Lately, the bank has started publishing explainers and layering its publications, making them accessible to a wider audience with no financial background, to increase trust and transparency, two of its core principles.

Figure 2.

Comparison of citizen expectations and perceptions regarding the ECB e-service quality.

Table 2 shows the average unweighted GAP scores per dimension and per question. The dimension with the lowest GAP score is the reliability one, used from the SERVQUAL scale, while the one with the highest GAP score is the efficiency one, applied from E-SERVQUAL and measuring website features.

Table 2.

GAP score for the constructs and items.

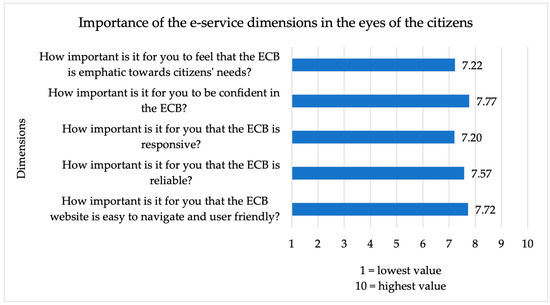

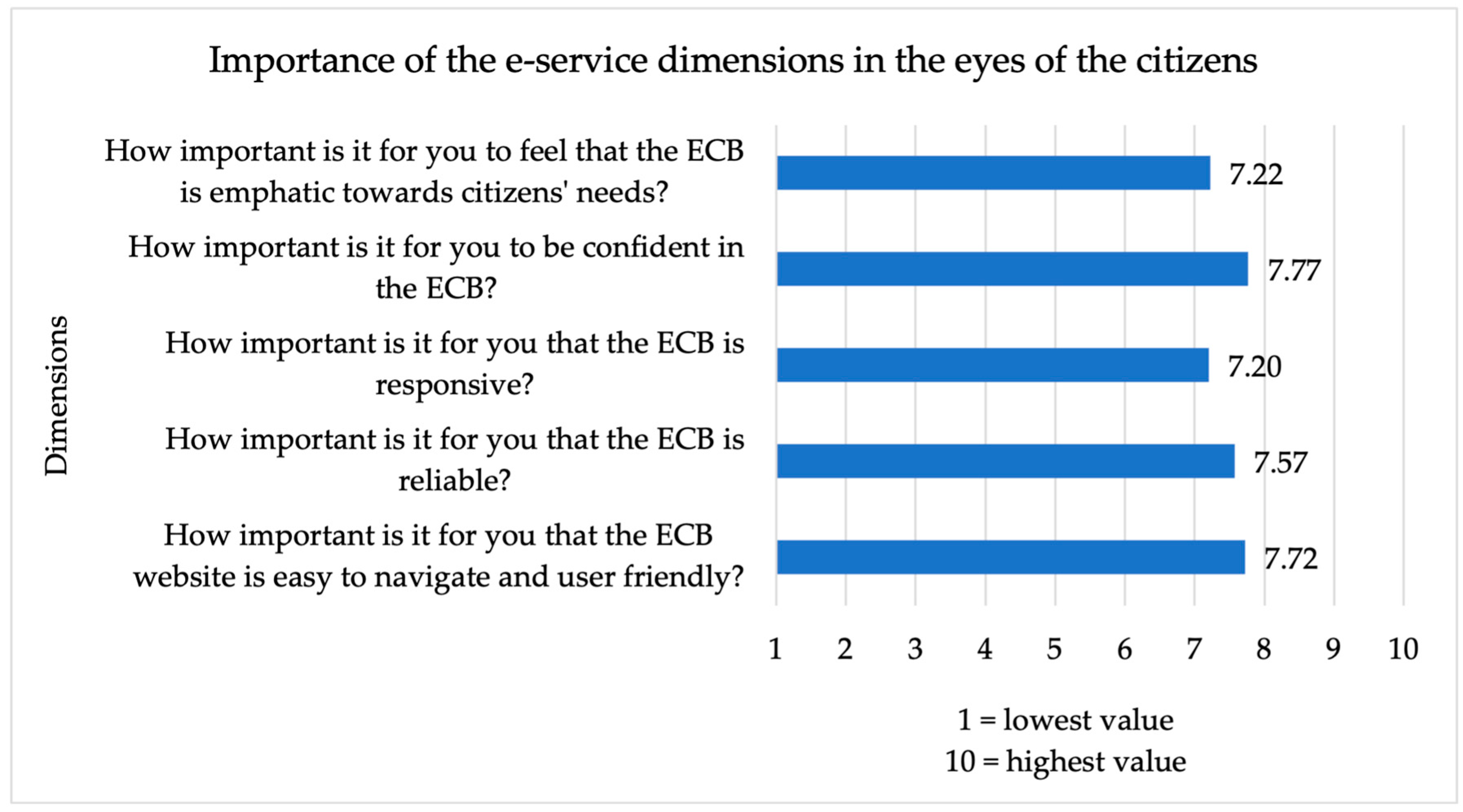

Citizens were also asked to rate the importance of the measured dimensions on a scale from 1 to 10, to measure if the dimensions carried similar significance and weight in the minds of participants. The goal was for the authors to see if there were dimensions that were deemed more important than others in the eyes of the citizens. The results are visible in Figure 3.

Figure 3.

Importance of dimensions in the eyes of the citizens.

It is clear that the chosen dimensions seemed to carry very similar weight in the perceptions of participants. Perhaps this is due to the dimension of the sample (406 respondents) (Table 3), while a higher sample would have yielded different results. The most important dimension, scoring 7.77 out of 10, was the confidence dimension, suggesting that citizens deemed it very important to be able to trust the actions of the ECB. This is normal, given that we are talking about a European institution that influences markets and is in charge of financial stability for the European Union and beyond. User friendliness and website navigation ranked second. This is very interesting, given that these were the dimensions for which the authors measured the highest expectation-perception gap. Thus, it can be concluded that the ECB should focus on improving these features of the website and facilitating citizen access and navigability, making it easier for citizens to access information.

Table 3.

Socio-demographic profile of respondents (n = 406) (authors’ own reproduction).

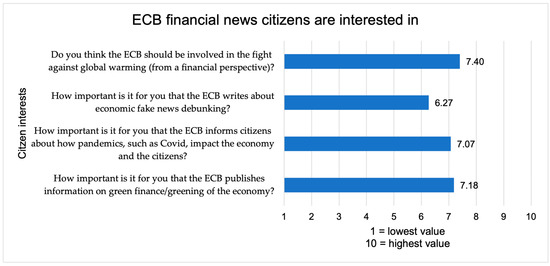

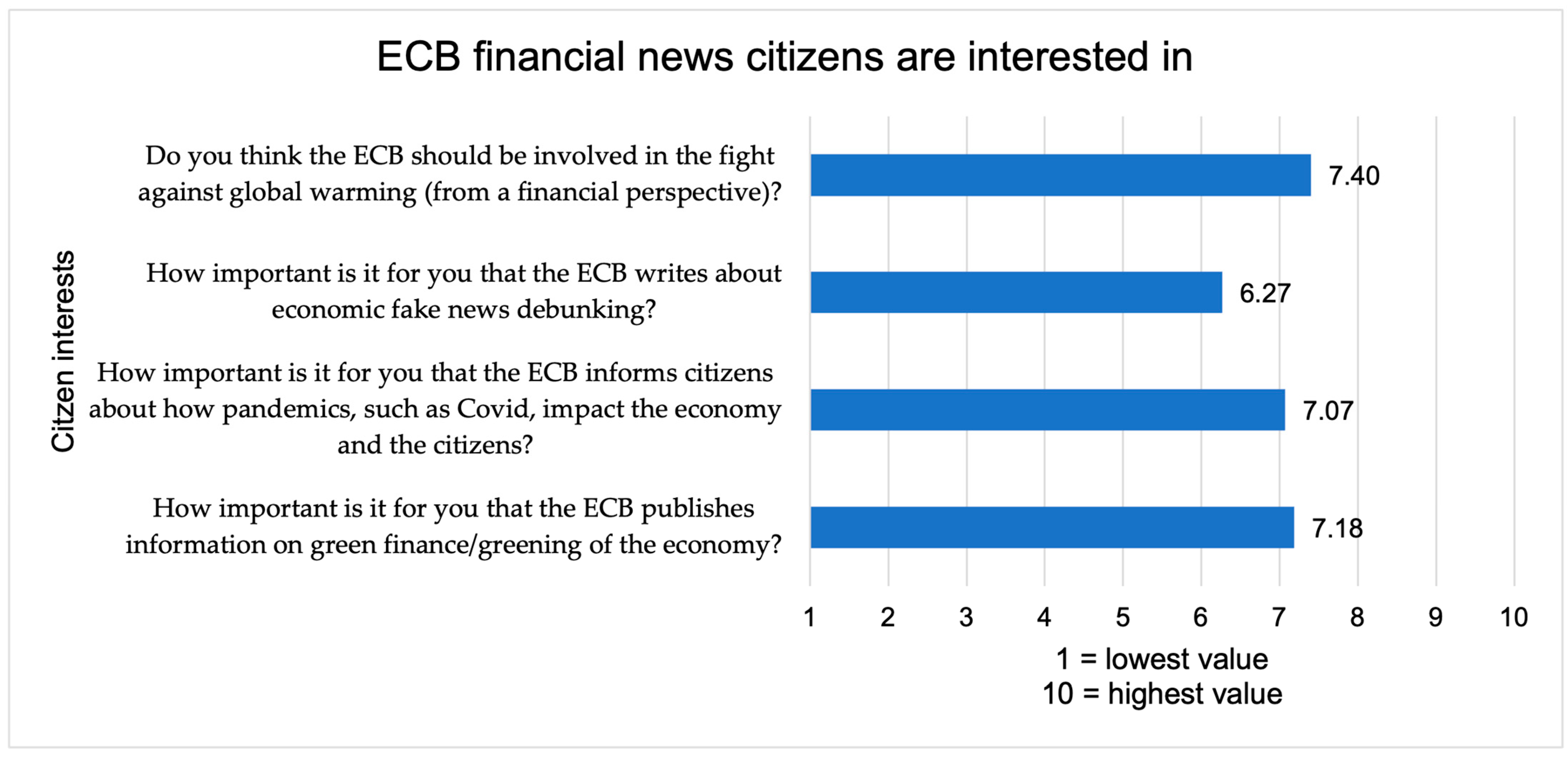

In the third part of the questionnaire, the authors asked the respondents if they thought the ECB should write about recent topics, such as green finance, the impact of COVID-19, economic fake news, or global warming and its financial implications (see Figure 4). The highest interest was expressed in global warming news from a financial perspective and in green finance. The ECB already publishes information on these topics, especially through social networks, such as LinkedIn, and even conducted a 2022 climate risk stress test.

Figure 4.

Financial news that citizens are interested in.

Citizens would like financial public institutions, like the European Central Bank, to publish information about current events, such as global warming, green finance, COVID-19, and their impact on financial markets. According to the literature (Bernardelli et al. 2021) the banking sector absorbed the economic costs of COVID-19 and thus had a direct effect on the general life quality of citizens. The fact that participants were interested in the above-mentioned topics was unsurprising, given the fact that they were impacted by such events. Moreover, the above-mentioned topics mostly align with the objective of the European Union to achieve climate neutrality by 2050, in line with the goals of the Paris Agreement. European institutions, including central banks, need to align to this mandate, which will impact, amongst others, price stability, financial markets, and thus citizens, especially through inflation, as is the case in the European Union, where inflation increased to a level of 10.9% in September 2022, according to Statista. It was thus interesting to note participants’ main interests with respect to news published by the ECB.

According to previous research (Khan and Imami 2020; Ramanathan et al. 2018), the questionnaire was applied using the convenience sampling method, already used in the past for SERVQUAL analysis, which implies that the number of responses should be 5–10 times the number of variables used (according to Hatcher and O’Rourke 2013). The empathy dimension (stemming from SERVQUAL), followed by efficiency (E-SERVQUAL) and understandability (Webqual), were rated highest in terms of customer expectations, having the strongest impact on citizen satisfaction. The high empathy score is in line with research by Lassar et al. (2000) and Ramanathan et al. (2018).

The fact that the dimensions deemed to be most important by participants came from three different scales implies that the levels of expectation have evolved and adapted in line with technological advances. This is an encouraging finding and can constitute the basis for further adaptations of private sector scales into public sector ones. In a further step, it would be interesting to disseminate the questionnaire to a larger and less homogeneous sample, increasing the robustness of the results and offering more statistical power, by verifying whether people with different backgrounds (education, profession, age, and geography) have different expectations and perceptions when it comes to ECB e-service quality. Studies have already shown that people with a lower educational level are more likely to trust more readable information and visually attractive texts (Prodan and Dabija 2022), and that layering central bank website reports increases citizen trust and satisfaction (Hayo and Neuenkirch 2015; Bholat et al. 2017).

Interesting to note is the fact that our results do not coincide with those of Kakouris and Panagiotis (2016), who applied SERVQUAL to top Serbian banks within the private sector and found the largest gaps in the reliability and responsiveness dimensions. A similar study testing service quality within an urban cooperative bank in India also identified the highest gap within the reliability dimension (Sharma 2016). When it comes to the European Central Bank, the highest gaps were identified within the efficiency (E-SERVQUAL) and understandability (Webqual) dimensions, followed by empathy and responsiveness (SERVQUAL). The fact that the highest gaps were identified in the two dimensions added by the authors from E-SERVQUAL and Webqual reinforces the belief that service quality perception scales need to be adapted to the current digitalised world, not only when it comes to the private sector, but also within the public sector, as all citizens are reliant on it. The literature (Herington and Weaven 2009) found that the efficiency component was the only one that was not predictive in terms of overall levels of satisfaction when it came to Australian consumers. This can change with the emergence of e-money and central bank digital currencies, that can become a fundamental tool within the economy, and whose efficiency and security are key arguments favouring their introduction, according to research (Chuen et al. 2021). Citizen satisfaction with such currencies should be measured in the future and broken down by age groups, given that the usage of traditional electronic payment methods is low among the elderly and vulnerable groups (Barontini and Holden 2019). Several CBDC studies focus on the risks associated with such currencies. It was found that risk aversion is lower within young generations, whose degree of digital literacy is higher and who have access to more information, especially via social media platforms, such as Twitter, and which are now being used for communication strategy implementation by central banks (Ozili 2022). The authors have found no studies measuring citizen satisfaction correlated with risk aversion when it comes to electronic money and emerging digital technologies, but only 2023 research (Tan) that focuses on the necessity of a two-sided adoption strategy, meaning that citizens need to adopt CBDCs, while at the same time retailers need to accept payments by using them. Both parties can be incentivised to adopt CBDCs (through their low cost and attractive savings options for citizens, and the implementation of subsidies or tax exemptions on the retailer side).

Young adults sometimes use fully digital banks in the private sector, basing their decision on the banking services’ economic value, bank reputation, ease of use and features, and also the banks’ social influence, promotions, rewards, and curiosity components (Windasari et al. 2022). These are both objective and subjective components and could also be tested, following their adaptation, to central banks (especially the social influence, curiosity, and reputation components). The authors believe that the digital banking components identified by Windasari et al. (2022) should equally be considered when measuring citizen satisfaction. Reputation is similar to reliability, and focuses on taking correct action on time, and showing a genuine interest in solving problems, being deeply connected to the Environmental, Social and Governance (ESG) objectives. The literature (Samaniego-Medina and Giráldez-Puig 2022) found that ESG polemics negatively impact European banks’ reputation and credit ratings, meaning that analysing and improving the reputation dimension through policy adaptations could increase banks’ sustainable growth.

Mwiya et al. (2022) also noted the lack of service quality studies in the digital banking sector and applied an E-SERVQUAL questionnaire to bank customers in Zambia, arguing that customer satisfaction is directly proportional to loyalty, and finding that reliability influences customer satisfaction the most. This is not in line with the findings of George and Kumar (2014), who found that privacy was the most important E-Servqual dimension, but is close to our findings, where reliability and responsiveness ranked highest.

4. Materials and Methods

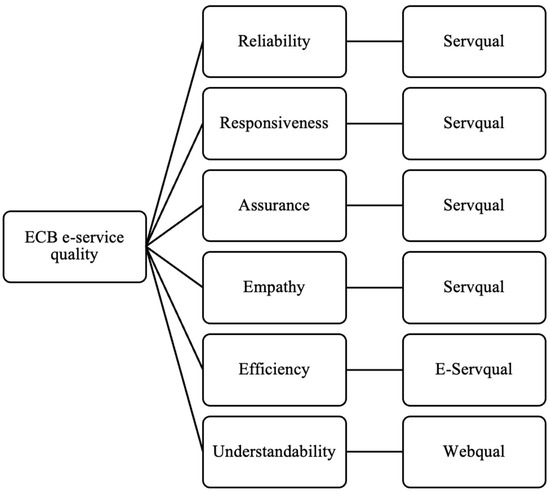

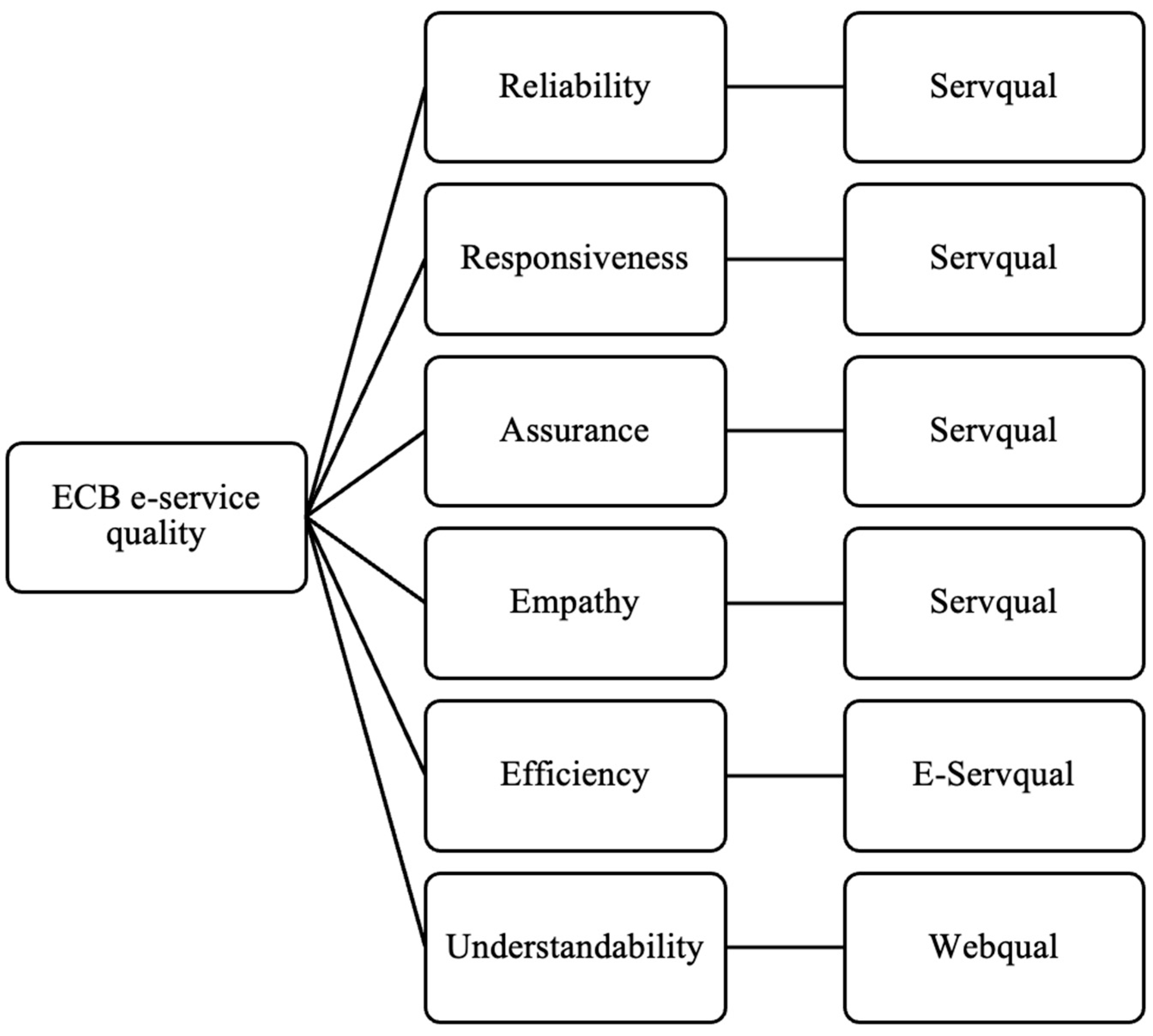

The aim of this paper is to contribute to an improved understanding of the perceptions and expectations of citizens with respect to central banks, by developing a valid measure of citizen satisfaction with respect to the usage of central bank websites. Relevant questions from the traditional SERVQUAL measurement scale used within the servuction model, of the E-SERVQUAL scale, and Webqual scale have been adapted to the marketing communication strategy of central banks, based on a previously performed literature review. Upon analysis of the SERVQUAL scale, the authors chose not to adapt all its five dimensions to central banks and specifically to the European Central Bank, given that the tangibility aspect cannot be tested against it, as it measures the physical components of buildings, personnel appearance, and visual assessment of used equipment. Four SERVQUAL dimensions were deemed applicable: reliability, responsiveness, assurance, and empathy). Given the fact that most citizens interact with central banks via digital means and the strong digitalization shift of today’s society, the authors searched for additional dimensions that could complement the first four and at the same time have a digital component. Out of the E-SERVQUAL dimensions (efficiency, system availability, privacy, and query fulfilment), the first one was chosen and the latter three were not adapted, as they did not constitute the primary focus for citizens interacting with central banks, or were not applicable. Following the literature review, the authors equally retained a Webqual dimension (understandability), given that it was linked to the efficiency of the banks’ communication strategy. Webqual measures website quality from the consumer’s point of view. Six dimensions resulted, that were applied to the European Central Bank and can also be applied to other national central banks within the European Union, as long as they have a website.

The relevant dimensions (such as reliability, responsiveness, assurance, empathy, efficiency, and understandability) were combined, measured, and tested with regard to the expectations and perceptions of citizens, and the questions were applied to the European Central Bank and disseminated to 500 participants, via email, social media, and in paper format. A total of 406 participants successfully answered all the questions, making possible the use of the convenience sampling method by the authors, with the goal of standardisation at the central bank level or even the European institution level (more studies are necessary), as the questions could be relevant to several types of public institution at national and international levels.

Measurement of e-service quality is relevant in a world in which digitalization provides a voice to citizens, making their opinions count progressively, with their weight as central bank stakeholders expanding (Prodan and Dabija 2022).

As shown in Figure 5, the authors adapted the questions from the SERVQUAL, E-SERVQUAL and Webqual measurement scales and made them relevant to the mostly digital interactions between institutions and citizens today, with the goal of verifying if it was relevant to standardize and apply them to institutions that had minimal physical interaction with citizens, such as European institutions, but where citizen satisfaction was important.

Figure 5.

Proposed framework for measuring e-service quality applied to the European Central Bank (authors’ own reproduction).

Reliability encompasses the capacity to execute a service accurately, correctly, and on time, whereas responsiveness refers to the readiness to assist and capability to perform prompt and accurate actions. Assurance implies that confidence and trust are instilled through the behaviour and economic impact, while empathy implies performing actions with the best interests in mind, together with customer (or in this case, citizen) needs, whereas efficiency means that the website consists of easy to find and well-organised information, and understandability entails website information that is easy to read. The result consists of an e-service measurement scale that has been updated for interactions that are mostly or 100% digital, and that focus both on dimensions around website features and consider the actual service.

The questionnaire was built around several constructs, divided into three sections. The first part consisted of 13 expectations and perception questions relating to the dimensions mentioned in Figure 5 and associated with the quality dimensions. Participants were asked to rate their expectations and perceptions of ECB e-services (including the content of the ECB website) on a scale from 1 to 10 (1 = the lowest, 10 = the highest rating). Respondents were also asked to assess the importance or weight of each dimension on a scale from 1 to 10, as the authors wanted to measure how important each dimension was in the eyes of respondents.

The second part of the questionnaire contained questions relating to current topics, rated from 1 to 10, with 10 being the highest grade. Respondents were asked to assess the significance of the ECB publishing economic and financial information relating to the COVID-19 pandemic, economic false news, global warming, and the green economy. The goal was to check whether citizens expected European institutions to disclose their views on current events to the public.

The third and last part contained questions on sociodemographic profiles and financial background. All questions in the survey were closed questions in order to facilitate the evaluation of results (Saunders et al. 2015). Participants were also asked whether they had a financial background and read financial news, as the authors wanted to test if the perceptions and expectations of citizens with a specific background were higher, lower, or the same.

The goal was to verify if this model could be standardised and replicated in other institutions of public interest at national or European level, such as financial administration, central banks, and institutions of the European Union.

5. Conclusions, Limitations, and Research Perspectives

From a theoretical perspective, this paper adds value to the literature by extending and applying the SERVQUAL model to the under-studied context of central banks. To the authors’ best knowledge, this model has not yet been applied to central banks, but only to private banks. Central banks are increasingly using their websites, as well as social media (such as LinkedIn, Twitter, and Facebook) to communicate with both the financial markets and citizens and in this context. Measuring citizen satisfaction with the provided information was deemed to be relevant by the authors. A GAP model was applied and the authors measured citizens’ expectations, compared with their perceptions regarding six dimensions relevant to central banks: reliability, responsiveness, assurance, empathy, as well as efficiency and understandability of the information presented on the website, as if the citizens were customers of a private sector entity. The authors also verified whether the chosen and adapted questions were relevant according to Cronbach alphas once the answers were centralized and the resulting coefficient ranked higher than 0.70, which means that the questions were pertinent. Given that, according to Cronbach alphas, the chosen questions were relevant, it can be concluded that the created GAP model, consisting of aggregated SERVQUAL, E-SERVQUAL, and Webqual constructs, can be applied to citizens and the public sector, even though in the past, these have been applied separately to the private sector. Such tools are valuable and can be adapted to the public sector and central banks in an ever-changing age of digitalisation and technological developments. The employed tools and set of questions could be further adapted, depending on the type of public institution they are tested against, given the high specificity and different characteristics of such institutions. It would be interesting to apply the same questions to a different central bank than the ECB and to then compare the findings. Moreover, given that the ECB supervises the European Union national central banks and several private banks (either directly or indirectly), the research could be extended and the questionnaire applied to such banks within the European Union as well, with the purpose of comparing the findings and analysing the discrepancies between different countries and banks, both within the public and private sector.

From a managerial perspective, it is also noteworthy that citizens are interested in reading about current major events, such as global warming and green finance, on the ECB-website. If citizens create a behaviour of regularly verifying such topics on the websites of European institutions, this will further increase their interaction, and possibly lead to a change in e-service quality expectations and perceptions. The same goes for the sustainability aspects of central bank actions, in the field of sustainable digital developments and financial strategies. Central Banks must adapt their communication strategies accordingly and focus more on civic engagement, ensuring high service quality, measured through adapted private sector metrics, such as SERVQUAL.

Among the limitations of the research, one can pinpoint the fact that the questionnaire was applied using the convenience sampling technique, more research being necessary. Another limitation lies in the fact that the investigated population was narrowed to only one research context, further research needing to consider its application to a larger and more heterogeneous citizen group. The current research has also not considered the influence of the socio-demographic profile of respondents in dealing with central bank information. From this perspective, possible further research should emphasize to what degree citizens with an economic and/or financial background, and those with a proper economic education or interest have the same expectations and perceptions as those whose primary focus is not related to economic and financial developments. Another emerging topic in the context of digitalisation and the Internet of Things are central bank digital currencies whose methods of implementation are currently being studied by several central banks around the world, including the ECB, and which will greatly impact citizens, if (when) implemented. Testing citizen satisfaction regarding central banks’ communication and, eventually, implementation of such currencies will become paramount in future years, as well as measuring citizens’ opinions regarding the sustainability aspects of such currencies, and using big data and artificial intelligence to predict citizen behaviour.

Another further research perspective relates to studying the website readability according to Flesch–Kincaid, that can lead to differences in service quality among different age groups, citizens with different education levels, or among citizens living in EU countries that have already adopted the euro versus those coming from countries with their own currency?

One thing is sure: we live in a digital world, and service science will need to adapt accordingly, by keeping pace with the latest technological developments and citizen behaviours, and by adapting private sector best practices to the public sector, especially concerning central banks.

Author Contributions

The authors participated in the research topic and share joint responsibility for this work. Conceptualization, S.P. and D.-C.D.; methodology, S.P.; software, S.P.; validation, S.P. and D.-C.D.; formal analysis, S.P. and D.-C.D.; investigation, S.P. and D.-C.D.; resources, S.P.; data curation, S.P.; writing—original draft preparation, S.P.; writing—review and editing, S.P. and D.-C.D.; visualization, S.P. and D.-C.D.; supervision, D.-C.D.; project administration, S.P.; funding acquisition, D.-C.D. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by a grant of the Babes-Bolyai University Cluj-Napoca: GS-UBB-FSEGADabijaDanCristian and a grant of the Romanian Ministry of Education and Research, CNCS—UEFISCDI, project number PN-III-P1-1.1-TE-2021-0795, with-in PNCDI III.

Institutional Review Board Statement

The study was approved by the SEGA Doctoral appropriate ethics committee and informed consent was obtained from all 500 participants prior to their participation in the survey, which was conducted using Jotform.com and did not collect any personal information such as addresses or email addresses.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study. The authors did not collect any personal data, such as email addresses, addresses or phone numbers.

Data Availability Statement

The data presented in the study are available on request from the corresponding author.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Andronie, Mihai, George Lăzăroiu, Roxana Ștefănescu, Luminița Ionescu, and Mădălina Cocoșatu. 2021. Neuromanagement decision-making and cognitive algorithmic processes in the technological adoption of mobile commerce apps. Oeconomia Copernicana 12: 1033–62. [Google Scholar] [CrossRef]

- Angur, Madhukar G., Rajan Nataraajan, and John S. Jahera Jr. 1999. Service quality in the banking industry: An assessment in a developing economy. International Journal of Bank Marketing 17: 116–25. [Google Scholar] [CrossRef]

- Avkiran, Necmi Kemal. 1994. Developing an Instrument to Measure Customer Service Quality in Branch Banking. International Journal of Bank Marketing 12: 10–18. [Google Scholar] [CrossRef]

- Bank of England. 2022. Available online: https://www.bankofengland.co.uk/ (accessed on 18 August 2023).

- Barontini, Christian, and Henry Holden. 2019. Proceeding with Caution—A Survey on Central Bank Digital Currencies. BIS Papers 101. Available online: https://www.bis.org/publ/bppdf/bispap101.pdf (accessed on 19 August 2023).

- Belke, Ansgar. 2017. Central Bank Communication: Managing Expectations through the Monetary Dialogue. ROME Working Papers 201704. Available online: https://ideas.repec.org/p/rmn/wpaper/201704.html (accessed on 14 November 2022).

- Belke, Ansgar, and Thorsten Polleit. 2011. How much fiscal backing must the ECB have? The euro area is not (yet) the Philippines. Économie Internationale 124: 5–30. [Google Scholar] [CrossRef]

- Bennani, Hamza. 2020. Central bank communication in the media and investor sentiment. Journal of Economic Behavior and Organization 176: 431–44. [Google Scholar] [CrossRef]

- Bernardelli, Michal, Zbigniew Korzeb, and Pawel Niedziółka. 2021. The banking sector as the absorber of the COVID-19 crisis’ economic consequences: Perception of WSE investors. Oeconomia Copernicana 12: 335–74. [Google Scholar] [CrossRef]

- Bholat, David, James Brookes, Chris Cai, Katy Grundy, and Jakob Lund. 2017. Sending Firm Messages: Text Mining Letters from PRA Supervisors to Banks and Building Societies They Regulate. Bank of England Working Papers. Available online: https://ideas.repec.org/p/boe/boeewp/0688.html (accessed on 14 November 2022).

- Bholat, David, Nida Broughton, Alice Parker, Janna Ter Meer, and Eryk Walczak. 2019. Enhancing Central Bank Communications Using Simple and Relatable Information. Journal of Monetary Economics 108: 1–15. [Google Scholar] [CrossRef]

- Bicchal, Motilal. 2022. Central bank credibility and its effect on stabilization. Economic Analysis and Policy 76: 73–94. [Google Scholar] [CrossRef]

- Blinder, Alan S. 2009. Talking about monetary policy: The virtues (and vice?) of central bank communication. SSRN Electronic Journal, 2–25. [Google Scholar] [CrossRef]

- Blinder, Alan S., Michael Ehrmann, Marcel Fratzscher, Jakob De Haan, and David-Jan Jansen. 2008. Central Bank Communication and Monetary Policy: A Survey of Theory and Evidence. Journal of Economic Literature, American Economic Association 46: 910–45. [Google Scholar] [CrossRef]

- Blut, Markus, Nivriti Chowdhry, Vikas Mittal, and Christian Brock. 2015. E-service quality: A meta-analytic review. Journal of Retailing 91: 679–700. [Google Scholar] [CrossRef]

- Bui Thi Thu, Ha, Quyen Bui Tu, Thanh Nguyen Thi Phuong, Quang Cao Huu, Thuy Phung Van, and Ha Nguyen Thanh. 2022. Does the SERVPERF instrument have reliability and validity in an academic setting: The results from Vietnam. Journal of Health and Development Studies 6: 27–37. [Google Scholar] [CrossRef]

- Bulir, Ales, and Katerina Smidkova. 2008. Striving to Be ‘Clearly Open’ and ‘Crystal Clear’: Monetary Policy Communication of the CNB. IMF Working Papers 084. [Google Scholar] [CrossRef]

- Buttle, Francis A. 1996. SERVQUAL: Review, critique, research agenda. European Journal of Marketing 30: 8–32. [Google Scholar] [CrossRef]

- Calvo, Marcos, Fernando García, Lluis-F. Hurtado, Santiago Jiménez, and Emilio Sanchis. 2013. Exploiting multiple hypotheses for Multilingual Spoken Language Understanding. In Proceedings of the Seventeenth Conference on Computational Natural Language Learning. Sofia: Association for Computational Linguistics, pp. 193–201. [Google Scholar]

- Carrillat, François A., Fernando Jaramillo, and Jay P. Mulki. 2007. The validity of the SERVQUAL and SERVPERF scales: A meta-analytic view of 17 years of research across five continents. International Journal of Service Industry Management 18: 472–90. [Google Scholar] [CrossRef]

- Carvalho, Cláudia, Carlos Brito, and José Sarsfield Cabral. 2010. Towards a conceptual model for assessing the quality of public services. International Review on Public and Nonprofit Marketing 7: 69–86. [Google Scholar] [CrossRef]

- Célérier, Laure, Eve Chiapello, and Anne Jeny. 2022. The Intangible Assetization of the State. The Case of a French Reform (2007–2020). SSRN Electronic Journal, 2–38. [Google Scholar] [CrossRef]

- Chuen, David, Li Yan, and Yu Wang. 2021. A global perspective on central bank digital currency. China Economic Journal 14: 1–16. [Google Scholar] [CrossRef]

- Cook, David P., Chon Huat Goh, and Chen H. Chung. 1999. Service typologies: A state-of-the-art survey. Production and Operations Management 8: 318–38. [Google Scholar] [CrossRef]

- Cristobal, Eduard, Carlos Flavian, and Guinaliu Miguel. 2007. Perceived e-service quality: Measurement validity and effects on consumer satisfaction and web site loyalty. Managing Service Quality 17: 317–40. [Google Scholar] [CrossRef]

- Cronin, Joseph J., Jr., and Steven A. Taylor. 1992. Measuring Service Quality—A Reexamination and Extension. The Journal of Marketing 56: 55–68. [Google Scholar] [CrossRef]

- Cross, James P., and Derek Greene. 2020. Talk Is Not Cheap: Policy Agendas, Information Processing, and the Unusually Proportional Nature of European Central Bank Communications Policy Responses. Governance 33: 425–44. [Google Scholar] [CrossRef]

- Dabholkar, Pratibha A. 1996. Consumer evaluations of new technology-based self-service options: An investigation of alternative modes of service quality. International Journal of Research in Marketing 13: 29–51. [Google Scholar] [CrossRef]

- Dabija, Dan-Cristian, Raluca Băbuţ, and Ciprian-Marcel Pop. 2013. A Customer-Oriented Approach to Satisfaction with Public Service Providers. Empirical Findings from a Market Undergoing Liberalization. Transylvanian Review of Administrative Sciences 9: 26–49. [Google Scholar]

- Ekkehard, Ernst, and Rossana Merola. 2018. Central Bank Communication: A Quantitative Assessment. International Labour Office, 33. Research Department Working Paper n°33: Central Bank Communication: A Quantitative Assessment. Available online: https://ideas.repec.org/p/ilo/ilowps/995008793102676.html (accessed on 18 August 2023).

- European Central Bank. 2022. Available online: https://www.ecb.europa.eu/home/html/index.en.html (accessed on 18 August 2023).

- Fassnacht, Martin, and Ibrahim Koese. 2006. Quality of electronic services: Conceptualizing and testing a hierarchical model. Journal of Service Research 9: 19–31. [Google Scholar] [CrossRef]

- Federal Reserve. 2022. Federal Reserve Board—About the Fed. Available online: https://www.federalreserve.gov/aboutthefed.htm (accessed on 18 August 2023).

- Ferrara, Federico Maria, and Siria Angino. 2022. Does Clarity Make Central Banks More Engaging? Lessons from ECB Communications. European Journal of Political Economy 74: 102146. [Google Scholar] [CrossRef]

- Field, Joy M., Gregory R. Heim, and Kingshuk K. Sinha. 2004. Managing quality in the e-service system: Development an application of a process model. Production and Operations Management 13: 291–306. [Google Scholar] [CrossRef]

- Fitzsimmons, James A., and Mona J. Fitzsimmons. 2006. Service Management: Operations, Strategy, and Information Technology. New York: Irwin McGraw-Hill. [Google Scholar]

- Fountain, Jane E. 2002. Paradoxes of Public Sector Customer Service. Jane E. Fountain 14: 55–73. [Google Scholar] [CrossRef]

- Fragkos, Georgios, Cyrus Minwalla, Jim Plusquellic, and Eirini Eleni Tsiropoulou. 2020. Artificially Intelligent Electronic Money. IEEE Consumer Electronics Magazine 10: 81–89. [Google Scholar] [CrossRef]

- Gajanova, Lubica, Margareta Nadanyiova, and George Lazaroiu. 2020. Specifics in brand value sources of customers in the banking industry from the psychographic point of view. Central European Business Review 9: 1–18. [Google Scholar] [CrossRef]

- Gajdosikova, Dominika, George Lăzăroiu, and Katarina Valaskova. 2023. How Particular Firm-Specific Features Influence Corporate Debt Level: A Case Study of Slovak Enterprises. Axioms 12: 183. [Google Scholar] [CrossRef]

- George, Ajimon, and Gireesh G. S. Kumar. 2014. Impact of service quality dimensions in internet banking on customer satisfaction. DECISION 41: 73–85. [Google Scholar] [CrossRef]

- Glas, Alexander, and Lena Sophia Müller. 2021. Talking in a language that everyone can understand? Transparency of speeches by the ECB Executive Board. SSRN Electronic Journal, 2–30. [Google Scholar] [CrossRef]

- Grönroos, Christian. 1984. A Service Quality Model and its Marketing Implications. European Journal of Marketing 18: 36–44. [Google Scholar] [CrossRef]

- Hair, Joseph F., William C. Black, Babyn Barry J, and E. Anderson Rolph. 2010. Multivariate Data Analysis: A Global Perspective. London: Pearson Education. [Google Scholar]

- Haldane, Andrew, Alistair Macaulay, and Michael McMahon. 2020. The 3 E’s of Central Bank Communication with the Public. CEPR Discussion Paper No. DP14265. Available online: https://ssrn.com/abstract=3518605 (accessed on 14 November 2022).

- Haldane, Andrew, and Michael McMahon. 2018. Central Bank Communications and the General Public. AEA Papers and Proceedings 108: 578–83. [Google Scholar] [CrossRef]

- Hatcher, Larry, and Norm O’Rourke. 2013. A Step-by-Step Approach to Using SAS for Factor Analysis and Structural Equation Modelling. Cary: SAS Institute. [Google Scholar]

- Hayo, Bernd, and Matthias Neuenkirch. 2015. Central bank communication in the financial crisis: Evidence from a survey of financial market participants. Journal of International Money and Finance 59: 166–81. [Google Scholar] [CrossRef]

- Henseler, Jörg, and Marko Sarstedt. 2013. Goodness-of-fit indices for partial least squares path modeling. Computer Statistics 28: 565–80. [Google Scholar] [CrossRef]

- Herington, Carmel, and Scott Weaven. 2009. E-retailing by banks: E-service quality and its importance to customer satisfaction. European Journal of Marketing 43: 1220–31. [Google Scholar] [CrossRef]

- Hsiao, Chih-Tung, and Shin Lin Jie. 2008. A Study of Service Quality in Public Sector. International Journal of Electronic Business Management 6: 29–37. [Google Scholar]

- Hüning, Hendrik. 2016. Asset market response to monetary policy news from SNB press releases. Hamburg Institue of International Economics Research Paper 177: 1–24. [Google Scholar] [CrossRef]

- Ighomereho, Ogheneochuko Salome, Afolabi Ayotunde Ojo, Olufemi Samuel Omoyele, and Oluwayinka Samuel Olabode. 2022. From Service Quality to E-Service Quality: Measurement, Dimensions and Model. Journal of Management Information and Decision Sciences 25: 1–15. [Google Scholar]

- Indahsari, Charity Latanza, and Sam’un Jaja S. Raharja. 2020. New Public Management (NPM) as an Effort in Governance. Jurnal Manajemen Pelayanan Publik 3: 73–129. [Google Scholar] [CrossRef]

- Issing, Otmar. 2006. Kommunikation, Transparenz, Rechenschaft—Geldpolitik im 21. Jahrhundert. Perspektiven der Wirtschaftspolitik 6: 521–40. [Google Scholar] [CrossRef]

- Jung, Alexander, and Patrick Kühl. 2021. Can Central Bank Communication Help to Stabilise Inflation Expectations? ECB Working Paper Series No. 2547. Hoboken: Wiley, pp. 1–31. [Google Scholar] [CrossRef]

- Kakouris, Andreas P, and Finos K. Panagiotis. 2016. Applying Servqual to The Banking Industry. East-West Journal of Economics and Business 19: 57–71. [Google Scholar]

- Khan, Rahat, and Soliman K. Imami. 2020. Applying the Service Quality (SERVQUAL) Model to Evaluate the Satisfaction of the Customers: A Study on Private Commercial Banks in Bangladesh. AIBA Savar Journal 1: 93–111. [Google Scholar]

- Kliestik, Tomas, Katarina Valaskova, George Lazaroiu, Maria Kovacova, and Jaromir Vrbka. 2020. Remaining Financially Healthy and Competitive: The Role of Financial Predictors. Journal of Competitiveness 12: 74–92. [Google Scholar] [CrossRef]

- Koushiki, Choudhury. 2013. Service quality and customers’ purchase intentions: An empirical study of the Indian banking sector. International Journal of Bank Marketing 31: 529–43. [Google Scholar] [CrossRef]

- Krizanova, Anna, George Lăzăroiu, Lubica Gajanova, Jana Kliestikova, Margareta Nadanyiova, and Dominika Moravcikova. 2019. The Effectiveness of Marketing Communication and Importance of Its Evaluation in an Online Environment. Sustainability 11: 7016. [Google Scholar] [CrossRef]

- Lamsal, Bishnu Prasad, and Anil Kumar Gupta. 2022. Citizen Satisfaction with Public Service: What Factors Drive? Policy & Governance Review 6: 78–89. [Google Scholar] [CrossRef]

- Lassar, Walfried M., Chris Manolis, and Robert D. Winsor. 2000. Service quality perspectives and satisfaction in private banking. Journal of Services Marketing 14: 244–71. [Google Scholar] [CrossRef]

- Lazarevic, Jelisaveta, Tanja Kuzman, and Milan Nedeljkovic. 2022. Credit cycles and macroprudential policies in emerging market economies. Oeconomia Copernicana 13: 633–66. [Google Scholar] [CrossRef]

- Lăzăroiu, George, Luminița Ionescu, Mihai Andronie, and Irina Dijmărescu. 2020. Sustainability Management and Performance in the Urban Corporate Economy: A Systematic Literature Review. Sustainability 12: 7705. [Google Scholar] [CrossRef]

- Li, Hongxiu, and Reima Suomi. 2009. A Proposed Scale for Measuring E-service Quality. International Journal of U- and E-Service, Science and Technology 2: 1–10. [Google Scholar]

- Ling, Tom. 2002. Delivering joined-up government in the UK: Dimensions, issues and problems. Public Administration 80: 615–42. [Google Scholar] [CrossRef]

- Loiacono, Eleanor T., Richard T. Watson, and Dale L. Goodhue. 2007. WebQual: An Instrument for Consumer Evaluation of Web Sites. International Journal of Electronic Commerce 11: 51–87. [Google Scholar] [CrossRef]

- Madu, Christian N., and Assumpta A. Madu. 2002. Dimensions of e-quality. International Journal of Quality & Reliability Management 19: 246–59. [Google Scholar] [CrossRef]

- Marcus, Gill. 2014. The importance of central bank communication, Address to the Central Banks Communicators. Paper presented at Conference Dinner South African Reserve Bank, Pretoria, South Africa, March 13; Available online: https://www.bis.org/review/r140314d.htm (accessed on 18 August 2023).

- Mester, Loretta J. 2018. The Federal Reserve and Monetary Policy Communications: The Tangri Lecture. New Brunswick: Rutgers University. Available online: https://econpapers.repec.org/paper/fipfedcsp/91.htm (accessed on 17 August 2023).

- MonetaryPolicy. 2022. What is Monetary Policy? Definition and Meaning. Available online: https://marketbusinessnews.com/financial-glossary/monetary-policy-definition-meaning (accessed on 14 November 2022).

- Musa, Hussam, Viacheslav Natorin Zdenka Musova, George Lazaroiu, and Martin Boda. 2021. Comparison of factors influencing liquidity of European Islamic and conventional banks. Oeconomia Copernicana 12: 375–98. [Google Scholar] [CrossRef]

- Mwiya, Bruce, Mathew Katai, Justice Bwalya, Maidah Kayekesi, Sekela Kaonga, Edwin Kasanda, Christopher Munyonzwe, Bernadette Kaulungombe, Eledy Sakala, Alexinah Muyenga, and et al. 2022. Examining the Effects of Electronic Service Quality on Online Banking Customer Satisfaction: Evidence from Zambia. Cogent Business & Management 9: 2143017. [Google Scholar] [CrossRef]

- Naik, Krishna C. N., Swapna Bhargavi Gantasala, and Gantasala V. Prabhakar. 2010. Service Quality (SERVQUAL) and its Effect on Customer Satisfaction in Retailing Introduction—Measures of Service Quality. European Journal of Social Sciences 16: 239–51. [Google Scholar]

- Newman, Karin, and Alan Cowling. 1996. Service quality in retail banking: The experience of two British clearing banks. International Journal of Bank Marketing 14: 3–11. [Google Scholar] [CrossRef]

- Nyagadza, Brighton. 2022. Sustainable digital transformation for ambidextrous digital firms: A systematic literature review and future research directions. Sustainable Technology and Entrepreneurship 1: 100020. [Google Scholar] [CrossRef]

- Oliveira, Pedro, Aleda V. Roth, and Wendell Gilland. 2002. Achieving competitive capabilities in e-services. Technological Forecasting & Social Change 69: 721–39. [Google Scholar] [CrossRef]

- Oliver, Richard L. 1980. A Cognitive Model of Antecedents and Consequences of Satisfaction Decisions. Journal of Marketing Research 17: 460–69. [Google Scholar] [CrossRef]

- Ozili, Peterson. 2022. Central bank digital currency research around the World: A review of literature. Journal of Money Laundering Control. Advance online publication. [Google Scholar] [CrossRef]

- Ozretic-Dosen, Durdana, and Ines Zizak. 2015. Measuring the quality of banking services targeting student population. EuroMed Journal of Business 10: 98–117. [Google Scholar] [CrossRef]

- Parasuraman, Ananthanarayanan, Valarie A. Zeithaml, and Arvind Malhotra. 2005. E-S-QUAL: A Multiple-Item Scale for Assessing Electronic Service Quality. Journal of Service Research 7: 213–33. [Google Scholar] [CrossRef]

- Parasuraman, Ananthanarayanan, Valarie A. Zeithaml, and Leonard L. Berry. 1985. A Conceptual Model of Service Quality and its Implication for Future Research (SERVQUAL). The Journal of Marketing 49: 41–50. [Google Scholar] [CrossRef]

- Parasuraman, Ananthanarayanan, Valarie A. Zeithaml, and Leonard L. Berry. 1988. SERVQUAL: A Multiple-Item Scale for Measuring Consumer Perceptions of service quality. Journal of Retailing 64: 12–40. [Google Scholar]

- Pescatori, Andrea. 2018. Central Bank Communication and Monetary Policy Surprises in Chile. IMF Working Paper No. 18/156. pp. 2–33. Available online: https://ssrn.com/abstract=3221266 (accessed on 14 November 2022).

- Pinquart, Martin, Dominik Endres, Sarah Teige-Mocigemba, Christian Panitz, and Schütz Alexander C. 2021. Why expectations do or do not change after expectation violation: A comparison of seven models. Consciousness and Cognition 89: 103086. [Google Scholar] [CrossRef]

- Prodan, Silvana, and Dan Cristian Dabija. 2022. Enhancing the Attractiveness and Readability of Central Bank Reports: An Experiment. Paper presented at the 8th BASIQ International Conference on New Trends in Sustainable Business and Consumption, Graz, Austria, May 25–27; Edited by Rodica Pamfilie, Vasile Dinu, Cristinel Vasiliu, Doru Pleșea and Laurentiu Tăchiciu. Bucharest: ASE, pp. 163–70. [Google Scholar] [CrossRef]

- Prodan, Silvana, and Dan Cristian Dabija. 2023. Exploring Consumer Sentiment on Central Bank Digital Currencies: A Twitter analysis from 2021 to 2023. Proceedings of the International Conference on Business Excellence 17: 1085–102. [Google Scholar] [CrossRef]

- Ramanathan, Usha, Sandar Win, and Andreas Wien. 2018. A SERVQUAL approach to identifying the influences of service quality on leasing market segment in the German financial sector. Benchmarking: An International Journal 25: 1935–55. [Google Scholar] [CrossRef]

- Rowland, Zuzana, George Lazaroiu, and Ivana Podhorská. 2021. Use of Neural Networks to Accommodate Seasonal Fluctuations When Equalizing Time Series for the CZK/RMB Exchange Rate. Risks 9: 1. [Google Scholar] [CrossRef]

- Samaniego-Medina, Reyes, and Pilar Giráldez-Puig. 2022. Do Sustainability Risks Affect Credit Ratings? Evidence from European Banks. Amfiteatru Economic 24: 720–38. [Google Scholar] [CrossRef]

- Santos, Jessica. 2003. E-service quality—A model of virtual service dimensions. Managing Service Quality 13: 233–47. [Google Scholar] [CrossRef]

- Saunders, Mark, Philip Lewis, and Adrian Thornhill. 2015. Research Methods for Business Students. London: Pearson Education Limited. [Google Scholar]

- Scalera, Jamie, and Melissa Crosby Dixon. 2016. Crisis of confidence: The 2008 global financial crisis and public trust in the European Central Bank. European Politics and Society 17: 1–14. [Google Scholar] [CrossRef]

- Serrat, Olivier. 2017. Marketing in the public sector. In Knowledge Solutions. Singapore: Springer. [Google Scholar]

- Sharma, Seema. 2016. Using SERVQUAL to Assess the Customer Satisfaction Level: A Study of an Urban Cooperative Bank. Journal of Economics and Public Finance 2: 57–85. [Google Scholar] [CrossRef]

- Siu, Noel Yee-Man, Ho-Yan Kwan, Huen Wong, and Tracy Jun-Feng Zhang. 2016. Enhancing Positive Disconfirmation and Personal Identity Through Customer Engagement in Cultural Consumption. In Marketing at the Confluence between Entertainment and Analytics: Proceedings of the 2016 Academy of Marketing Science World Marketing Conference, Paris, France, July 19–23. Cham: Springer International Publishing, pp. 525–36. [Google Scholar]

- Sohn, Changsoo, and Suresh K. Tadisina. 2008. Development of e-service quality measure for the internet-based financial institutions. Total Quality Management & Business Excellence 19: 903–18. [Google Scholar] [CrossRef]

- Steinbach, Malte, Jost Sieweke, and Stefan Süß. 2019. The diffusion of e-participation in public administrations: A systematic literature review. Journal of Organizational Computing and Electronic Commerce 29: 61–95. [Google Scholar] [CrossRef]

- Stojanovikj, Martin. 2022. Can inflation targeting reduce price information asymmetry and alleviate corruptive behavior? Evidence from developing countries. Economic Systems 46: 100986. [Google Scholar] [CrossRef]

- Surjadaja, Heston, Sid Ghosh, and Jiju Antony. 2003. Determinants and assessing the determinants of e-service operation. Managing Service Quality 13: 39–44. [Google Scholar] [CrossRef]

- Tagscherer, Florian, and Claus-Christian Carbon. 2023. Leadership for successful digitalization: A literature review on companies’ internal and external aspects of digitalization. Sustainable Technology and Entrepreneurship 2: 100039. [Google Scholar] [CrossRef]

- Vasiliadis, Labros. 2008. Greek banks in international markets: A study of entry modes and approaches. Journal for International Business and Entrepreneurship Development 3: 254–69. [Google Scholar] [CrossRef]

- Weber, Christoph S. 2020. The unemployment effect of central bank transparency. Empirical Economics 59: 2947–75. [Google Scholar] [CrossRef]

- Weidmann, Jens. 2018. Central Bank Communication as an Instrument of Monetary Policy. Central Bank Speech. Available online: https://www.bis.org/review/r180511a.htm (accessed on 14 November 2022).

- Windasari, Nila Armelia, Nurrani Kusumawati, Niken Larasati, and Revira Puspasuci Amelia. 2022. Digital-only banking experience: Insights from gen Y and gen Z. Journal of Innovation & Knowledge 7: 100170. [Google Scholar] [CrossRef]

- Wolfinbarger, Mary, and Mary C. Gilly. 2002. ETailQ: Dimensionalization, Measuring and Predicting Etail quality. Journal of Retailing 79: 183–98. [Google Scholar] [CrossRef]