Decision-Making under Uncertainty: How Easterners and Westerners Think Differently

Abstract

:1. Introduction

2. Materials and Methods

2.1. Participants

2.2. Main Task

2.3. Payment and Estimation

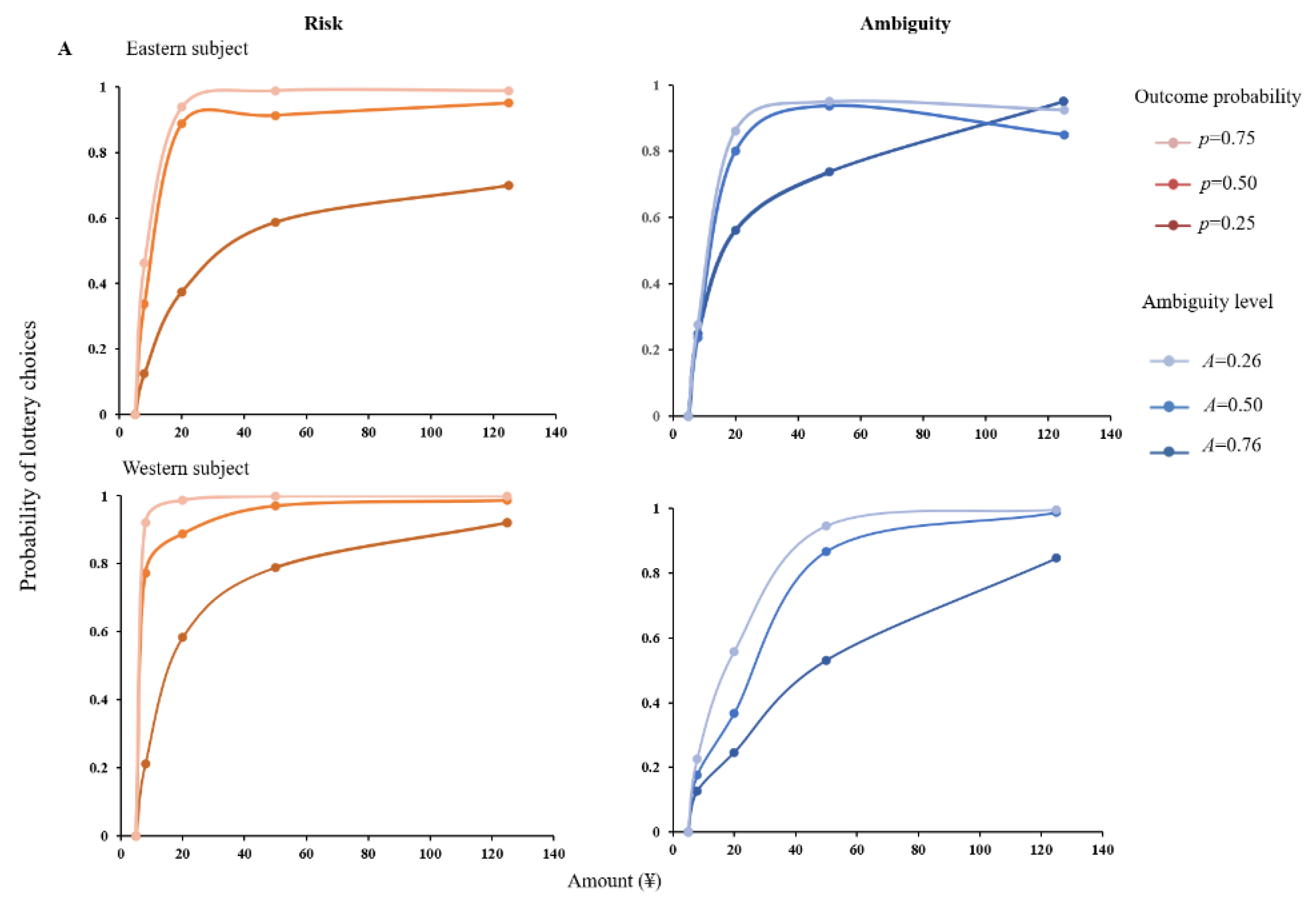

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ellsberg, D. Risk, ambiguity, and the savage axioms. Q. J. Econ. 1961, 75, 643–669. [Google Scholar] [CrossRef] [Green Version]

- Kahneman, D.; Tversky, A. Prospect theory: An analysis of decision under risk. Econometrica 1979, 47, 263–291. [Google Scholar] [CrossRef] [Green Version]

- Opper, S.; Nee, V.; Holm, H.J. Risk aversion and guanxi activities: A behavioral analysis of ceos in China. Acad. Manag. J. 2017, 60, 1504–1530. [Google Scholar] [CrossRef] [Green Version]

- Hou, S.-I.; Basen-Engquist, K. Human immunodeficiency virus risk behavior among white and Asian/Pacific Islander high school students in the united states: Does culture make a difference? J. Adolesc. Health 1997, 20, 68–74. [Google Scholar] [CrossRef]

- Boufous, S.; Ivers, R.; Senserrick, T.; Norton, R.; Stevenson, M.; Chen, H.-Y.; Lam, L.T. Risky driving behavior and road traffic crashes among young Asian Australian drivers: Findings from the DRIVE study. Traffic Inj. Prev. 2010, 11, 222–227. [Google Scholar] [CrossRef]

- Hu, L. Changing travel behavior of Asian immigrants in the U.S. Transp. Res. Part A Policy Pract. 2017, 106, 248–260. [Google Scholar] [CrossRef]

- Hanna, S.D.; Lee, J.; Lindamood, S. Financial behavior and attitudes of Asians compared to other racial/ethnic groups in the United States. J. Fam. Econ. Issues 2015, 36, 309–318. [Google Scholar] [CrossRef]

- Chandavarkar, A. Saving behaviour in the Asian-Pacific region. Asian-Pac. Econ. Lit. 2005, 7, 9–27. [Google Scholar] [CrossRef]

- Acharya, A. Can Asia lead? Power ambitions and global governance in the twenty-first century. Int. Aff. 2011, 87, 851–869. [Google Scholar] [CrossRef]

- Bavel, J.J.V.; Baicker, K.; Boggio, P.S.; Capraro, V.; Cichocka, A.; Cikara, M.; Crockett, M.J.; Crum, A.J.; Douglas, K.M.; Druckman, J.N.; et al. Using social and behavioural science to support COVID-19 pandemic response. Nat. Hum. Behav. 2020, 4, 460–471. [Google Scholar] [CrossRef]

- Paige, L.E.; Amado, S.; Gutchess, A.H. Influence of encoding instructions and response bias on cross-cultural differences in specific recognition. Cult. Brain 2017, 5, 153–168. [Google Scholar] [CrossRef] [PubMed]

- Kokkoris, M.D.; Kühnen, U. Choice and dissonance in a European cultural context: The case of Western and Eastern Europeans. Int. J. Psychol. 2013, 48, 1260–1266. [Google Scholar] [CrossRef] [PubMed]

- Hamamura, T.; Meijer, Z.; Heine, S.J.; Kamaya, K.; Hori, I. Approach--avoidance motivation and information processing: A cross-cultural analysis. Personal. Soc. Psychol. Bull. 2009, 35, 454–462. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Gelfand, M.J.; Raver, J.L.; Nishii, L.; Leslie, L.M.; Lun, J.; Lim, B.C.; Duan, L.; Almaliach, A.; Ang, S.; Arnadottir, J. Differences between tight and loose cultures: A 33-nation study. Science 2011, 332, 1100–1104. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Prentice, L.; Klackl, J.; Agroskin, D.; Grossmann, I.; Alexandrov, Y.; Apanovich, V.; Bezdenezhnykh, B.; Jonas, E. Reaction to norm transgressions and Islamization threat in culturally tight and loose contexts: A cross-cultural comparison of Germany versus Russia. Cult. Brain 2020, 8, 46–69. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Realo, A.; Linnamägi, K.; Gelfand, M.J. The cultural dimension of tightness-looseness: An analysis of situational constraint in Estonia and Greece. Int. J. Psychol. 2015, 50, 193–204. [Google Scholar] [CrossRef]

- Power, D.; Schoenherr, T.; Samson, D. The cultural characteristic of individualism/collectivism: A comparative study of implications for investment in operations between emerging Asian and industrialized Western countries. J. Oper. Manag. 2010, 28, 206–222. [Google Scholar] [CrossRef]

- Markus, H.R.; Kitayama, S. Culture and the self: Implications for cognition, emotion, and motivation. Psychol. Rev. 1991, 98, 224–253. [Google Scholar] [CrossRef]

- Hofstede, G. Culture′s Consequences: Comparing Values, Behaviors, Institutions and Organizations across Nations; Sage Publications: Thousand Oaks, CA, USA, 2001. [Google Scholar]

- Frijns, B.; Hubrs, F.; Kim, D.; Roh, T.-Y.; Xu, Y. National culture and corporate risk-taking around the world. Glob. Financ. J. 2022, 52, 100710. [Google Scholar] [CrossRef]

- Hofstede, G. Dimensionalizing cultures: The Hofstede model in context. Online Read. Psychol. Cult. 2011, 2, 2307-0919. [Google Scholar] [CrossRef]

- Frijns, B.; Garel, A. The effect of cultural distance between an analyst and a CEO on analysts’ earnings forecast performance. Econ. Lett. 2021, 205, 109957. [Google Scholar] [CrossRef]

- Hoang, H.V.; Nguyen, C.; Nguyen, D.K. Corporate immunity, national culture and stock returns: Startups amid the COVID-19 pandemic. Int. Rev. Financ. Anal. 2022, 79, 101975. [Google Scholar] [CrossRef]

- Karolyi, G.A. The gravity of culture for finance. J. Corp. Financ. 2016, 41, 610–625. [Google Scholar] [CrossRef]

- Levy, I.; Snell, J.; Nelson, A.J.; Rustichini, A.; Glimcher, P.W. Neural representation of subjective value under risk and ambiguity. J. Neurophysiol. 2010, 103, 1036–1047. [Google Scholar] [CrossRef] [Green Version]

- Tymula, A.; Belmaker, L.A.R.; Ruderman, L.; Glimcher, P.W.; Levy, I. Like cognitive function, decision making across the life span shows profound age-related changes. Proc. Natl. Acad. Sci. USA 2013, 110, 17143–17148. [Google Scholar] [CrossRef] [Green Version]

- Tymula, A.; Rosenberg Belmaker, L.A.; Roy, A.K.; Ruderman, L.; Manson, K.; Glimcher, P.W.; Levy, I. Adolescents’ risk-taking behavior is driven by tolerance to ambiguity. Proc. Natl. Acad. Sci. USA 2012, 109, 17135–17140. [Google Scholar] [CrossRef] [Green Version]

- Grubb, M.A.; Tymula, A.; Gilaie-Dotan, S.; Glimcher, P.W.; Levy, I. Neuroanatomy accounts for age-related changes in risk preferences. Nat. Commun. 2016, 7, 13822. [Google Scholar] [CrossRef] [Green Version]

- Herman, A.M.; Esposito, G.; Tsakiris, M. Body in the face of uncertainty: The role of autonomic arousal and interoception in decision-making under risk and ambiguity. Psychophysiology 2021, 58, e13840. [Google Scholar] [CrossRef]

- Cox James, C.; Harrison Glenn, W. Risk aversion in experiments: An introduction. In Risk Aversion in Experiments; James, C.C., Glenn, W.H., Eds.; Emerald Group Publishing Limited: Bingley, UK, 2008; Volume 12, pp. 1–7. [Google Scholar]

- Kelsey, D.; le Roux, S. Strategic ambiguity and decision-making: An experimental study. Theory Decis. 2018, 84, 387–404. [Google Scholar] [CrossRef]

- Carver, C.S.; White, T.L. Behavioral inhibition, behavioral activation, and affective responses to impending reward and punishment: The BIS/BAS scales. J. Personal. Soc. Psychol. 1994, 67, 319–333. [Google Scholar] [CrossRef]

- Patton, J.H.; Stanford, M.S.; Barratt, E.S. Factor structure of the Barratt impulsiveness scale. J. Clin. Psychol. 1995, 51, 768–774. [Google Scholar] [CrossRef]

- Blais, A.-R.; Weber, E.U. A domain-specific risk-taking (DOSPERT) scale for adult populations. Judgm. Decis. Mak. 2006, 1, 33–47. [Google Scholar]

- Pushkarskaya, H.; Tolin, D.; Ruderman, L.; Henick, D.; Kelly, J.M.; Pittenger, C.; Levy, I. Value-based decision making under uncertainty in hoarding and obsessive-compulsive disorders. Psychiatry Res. 2017, 258, 305–315. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Gilboa, I.; Schmeidler, D. Maxmin expected utility with non-unique prior. J. Math. Econ. 1989, 18, 141–153. [Google Scholar] [CrossRef] [Green Version]

- Holt, C.A.; Laury, S.K. Risk aversion and incentive effects. Am. Econ. Rev. 2002, 92, 1644–1655. [Google Scholar] [CrossRef] [Green Version]

- Wong, K.F.E.; Kwong, J.Y.Y. Resolving the judgment and decision-making paradox between adaptive learning and escalation of commitment. Manag. Sci. 2018, 64, 1911–1925. [Google Scholar] [CrossRef]

- Gelfand, M.J.; Nishii, L.H.; Raver, J.L. On the nature and importance of cultural tightness-looseness. J. Appl. Psychol. 2006, 91, 1225–1244. [Google Scholar] [CrossRef] [Green Version]

- Srivisal, N.; Sanoran, K.L.; Bukkavesa, K. National culture and saving: How collectivism, uncertainty avoidance, and future orientation play roles. Glob. Financ. J. 2021, 50, 100670. [Google Scholar] [CrossRef]

- Harrington, J.R.; Gelfand, M.J. Tightness–looseness across the 50 united states. Proc. Natl. Acad. Sci. USA 2014, 111, 7990–7995. [Google Scholar] [CrossRef] [Green Version]

- Levy, I.; Schiller, D. Neural computations of threat. Trends Cogn. Sci. 2021, 25, 151–171. [Google Scholar] [CrossRef]

- Dimmock, S.G.; Kouwenberg, R.; Mitchell, O.S.; Peijnenburg, K. Estimating ambiguity preferences and perceptions in multiple prior models: Evidence from the field. J. Risk Uncertain. 2015, 51, 219–244. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Peysakhovich, A.; Karmarkar, U.R. Asymmetric effects of favorable and unfavorable information on decision making under ambiguity. Manag. Sci. 2016, 62, 2163–2178. [Google Scholar] [CrossRef] [Green Version]

- Baillon, A.; Bleichrodt, H. Testing ambiguity models through the measurement of probabilities for gains and losses. Am. Econ. J. Microecon. 2015, 7, 77–100. [Google Scholar] [CrossRef] [Green Version]

- Ruggeri, K.; Ali, S.; Berge, M.L.; Bertoldo, G.; Bjorndal, L.D.; Cortijos-Bernabeu, A.; Davison, C.; Demic, E.; Esteban-Serna, C.; Friedemann, M.; et al. Replicating patterns of prospect theory for decision under risk. Nat. Hum. Behav. 2020, 4, 622–633. [Google Scholar] [CrossRef]

- Curley, S.P.; Yates, J.F.; Abrams, R.A. Psychological sources of ambiguity avoidance. Organ. Behav. Hum. Decis. Processes 1986, 38, 230–256. [Google Scholar] [CrossRef] [Green Version]

- Cohen, M.; Tallon, J.-M.; Vergnaud, J.-C. An experimental investigation of imprecision attitude and its relation with risk attitude and impatience. Theory Decis. 2010, 71, 81–109. [Google Scholar] [CrossRef] [Green Version]

- Di Mauro, C.; Maffioletti, A. Attitudes to risk and attitudes to uncertainty: Experimental evidence. Appl. Econ. 2004, 36, 357–372. [Google Scholar] [CrossRef]

- Dean, M.; Ortoleva, P. The empirical relationship between nonstandard economic behaviors. Proc. Natl. Acad. Sci. USA 2019, 116, 16262–16267. [Google Scholar] [CrossRef] [Green Version]

- Calford, E.M. Uncertainty aversion in game theory: Experimental evidence. J. Econ. Behav. Organ. 2020, 176, 720–734. [Google Scholar] [CrossRef]

- Bossaerts, P.; Ghirardato, P.; Guarnaschelli, S.; Zame, W.R. Ambiguity in asset markets: Theory and experiment. Rev. Financ. Stud. 2010, 23, 1325–1359. [Google Scholar] [CrossRef] [Green Version]

- Abdellaoui, M.; Baillon, A.; Placido, L.; Wakker, P.P. The rich domain of uncertainty: Source functions and their experimental implementation. Am. Econ. Rev. 2011, 101, 695–723. [Google Scholar] [CrossRef] [Green Version]

- Lauriola, M.; Levin, I.P. Relating individual differences in attitude toward ambiguity to risky choices. J. Behav. Decis. Mak. 2001, 14, 107–122. [Google Scholar] [CrossRef]

- Chakravarty, S.; Roy, J. Recursive expected utility and the separation of attitudes towards risk and ambiguity: An experimental study. Theory Decis. 2008, 66, 199–228. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| α | β | |

|---|---|---|

| Easterners | −0.154 * | −0.463 ** |

| (−1.97) | (−4.22) | |

| BAS drive | −0.012 | −0.042 |

| (−0.41) | (−1.16) | |

| BAS fun | −0.003 | 0.007 |

| (−0.18) | (0.25) | |

| BAS reward | −0.057 * | 0.154 |

| (−1.33) | (2.21) | |

| BIS | 0.021 | −0.024 |

| (0.87) | (−0.63) | |

| Constant | 0.826 | 0.544 |

| (3.12) | (0.87) |

| α | β | |

|---|---|---|

| Easterners | −0.298 ** | −0.322 ** |

| (−3.36) | (−2.23) | |

| First-order B11 factors | ||

| Attention | 0.022 | −0.075 |

| (0.83) | (−1.13) | |

| Motor | −0.014 | 0.043 |

| (−0.38) | (0.64) | |

| Self-control | 0.036 | 0.088 |

| (0.92) | (0.79) | |

| Cognitive complexity | −0.058 | 0.052 |

| (−1.65) | (1.13) | |

| Perseverance | −0.006 | −0.032 |

| (−0.17) | (−0.32) | |

| Cognitive instability | 0.014 | −0.018 |

| (0.42) | (−0.37) | |

| Second-order B11 factors | ||

| Attentional | 0.035 * | −0.017 |

| (1.43) | (−0.16) | |

| Motor | −0.118 * | 0.015 |

| (−2.18) | (0.12) | |

| Nonplanning | 0.018 | −0.065 |

| (1.14) | (−1.45) | |

| Constant | 1.056 * | 0.794 |

| (3.42) | (1.18) | |

| α | β | |

|---|---|---|

| Easterners | −0.149 * | −0.432 ** |

| (−1.76) | (−3.32) | |

| Male | 0.073 | 0.086 |

| (0.71) | (0.63) | |

| Household wealth | 0.000 | 0.000 |

| (0.12) | (−0.18) | |

| Personal financial situation | −0.017 | −0.002 |

| (−0.56) | (−0.03) | |

| Constant | 0.487 | 0.243 |

| (1.41) | (0.42) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guo, W.; Chen, X.-R.; Liu, H.-C. Decision-Making under Uncertainty: How Easterners and Westerners Think Differently. Behav. Sci. 2022, 12, 92. https://doi.org/10.3390/bs12040092

Guo W, Chen X-R, Liu H-C. Decision-Making under Uncertainty: How Easterners and Westerners Think Differently. Behavioral Sciences. 2022; 12(4):92. https://doi.org/10.3390/bs12040092

Chicago/Turabian StyleGuo, Wei, Xin-Rong Chen, and Hu-Chen Liu. 2022. "Decision-Making under Uncertainty: How Easterners and Westerners Think Differently" Behavioral Sciences 12, no. 4: 92. https://doi.org/10.3390/bs12040092

APA StyleGuo, W., Chen, X.-R., & Liu, H.-C. (2022). Decision-Making under Uncertainty: How Easterners and Westerners Think Differently. Behavioral Sciences, 12(4), 92. https://doi.org/10.3390/bs12040092