Abstract

This work uses the collocation approximation method to solve a specific type of backward stochastic Volterra integral equations (BSVIEs). Using Newton’s method, BSVIEs can be solved using block pulse functions and the corresponding stochastic operational matrix of integration. We present examples to illustrate the estimate analysis and to demonstrate the convergence of the two approximating sequences separately. To measure their accuracy, we compare the solutions with values of exact and approximative solutions at a few selected locations using a specified absolute error. We also propose an efficient method for solving a triangular linear algebraic problem using a single integral equation. To confirm the effectiveness of our method, we conduct numerical experiments with issues from real-world applications.

Keywords:

backward stochastic volterra integral equations; block-pulse functions; collocation approximation; operational matrix MSC:

60H20; 65C30; 60H07

1. Introduction

Backward stochastic differential equations (BSDEs) represent stochastic differential equations with terminal conditions. The existence and uniqueness of solutions for BSDEs have been proven by Pardoux and Peng, who also developed a general nonlinear BSDE [1,2]. Backward stochastic differential equations have numerous applications in finance, stochastic games, and optimal control. The concept of backward stochastic differential equations has been extended to include backward stochastic Volterra integral equations (BSVIEs), which depend on two specific time moments for their drift and diffusion coefficients. Nonlinearities are present in the general of BSDEs as follows.

We will introduce a primary space corresponding to a total probability space with a filtration, where meets the usual criteria (i.e., it is right continuous and contains all P-null sets). In constrast, defines the Wiener process. The terminal condition is an -measurable random variable, and the driver g is a progressively measurable function. The adapted solution of the BSDE (1) is the pair of the adapted processes that satisfy (1). The adapted solution’s second component, , is known as the martingale integrand.

Our investigation is inspired by the method for estimating the BSDEs’ adapted solutions [3]. We recommend researching backward stochastic Volterra integral equations (BSVIEs) in light of the most recent research of [4,5,6]. Pardoux and Peng began this research over a decade ago [7]. According to Lin [8], the modified solutions were studied as existence and uniqueness problems under global Lipschitz conditions. The global Lipschitz condition on drift has been eased by Aman and N’zi [9]. For a comprehensive explanation of the theory and applications of BSDE (1), including stochastic controls and mathematical finance, the reader might consult El Karoui, Peng, and Quenez’s overview paper [10]. The emergence of BSVIEs of the form has significantly developed BSDEs. As a natural progression from BSDEs, BSVIEs can be represented as follows.

In the literature, (2) is referred to as a Type-II BSVIE. Unlike a Type-I BSVIE, solving a Type-II BSVIE requires an extra constraint on the term , where for the equation to demonstrated well-posedness. Researchers have developed the adapted M solution, which was inspired by the duality principle in stochastic control problems of stochastic Volterra integral equations, to solve the Type-II BSVIE. This equation is essential for studying stochastic control and mathematical finance problems. Researchers have used BSVIEs to calculate dynamic risk estimates for position operations and to examine dynamic capital allocations. BSVIE solutions can describe time-inconsistent recursive utility processes of general discounting, and they are strongly linked to time-inconsistent stochastic control problems. Several researchers have proposed differentiability results, investigated stochastic control problems for SVIE and BSVIE systems, and proven numerous comparison theorems for adapted solutions and adapted M solutions to BSVIEs in multidimensional Euclidean spaces. Notably, BSVIE theory is path-dependent, and numerical elements have also been considered (see, e.g., [5,11,12,13,14,15,16,17,18,19,20] and the references therein).

Approximations for adapted M solutions of Type-II backward stochastic Volterra integral equations were studied, where backward stochastic differential equations converge to the adapted M solution of the original equation [21]. In addition, the convolution method has been extended to solve the conditional expectation to solve BSDEs numerically, and a generalized scheme has been applied to discretize the backward component [22].

The numerical approximations problem for Type-II BSVIEs has been completely open. There needs to be more quantitative interest in BSVIEs. Hence, with the aid of block pulse functions and their stochastic operational matrix of integration, backward stochastic Volterra integral equations can be effectively solved. These equations can then be reduced to a linear lower triangular system, which can then be solved by forward substitution (See, e.g., [23,24,25,26,27,28,29,30,31,32,33] and the references therein).

The primary characteristic of BSVIEs (2) is that they include memories, which are more accurate to reality. We seek the unknown pair , where and are adapted for each . In the above, the free term , also known as the terminal condition, is allowed to be only a -measurable stochastic process (not necessarily -adapted). Here, represents the Borel field of . The generator or the driver of the BSVIE is a given map , which can be deterministic or random. The coefficient is dependent on both t and s, and it depends not only on , but also on . The drift generally depends on and . In the case where the driver g is independent of the term , the BSVIE becomes the following:

For convenience, we have rewritten the following BSVIE:

The structure of this work is as follows. Section 2 covers the basic characteristics of block-pulse functions and an integration operational matrix approximation. In Section 3, the stochastic integration operational matrix is presented. Section 4 solves stochastic Volterra integral equations using the stochastic integration operational matrix via collocation approximation. Section 5 presents an analysis of the solution’s general error estimated regularity properties of the solution. In Section 6, we offer numerical results and use numerical examples to demonstrate the accuracy of the suggested approach.

2. Block-Pulse Functions BPFs

The block-pulse function (BPF) over the unit interval is defined as follows: for , and ,

with , and .

The block-pulse functions have the following properties:

- (1)

- Disjointness: The BPFs are disjointed with each other in the interval .

- (2)

- Orthogonality: The BPFs are disjointed with each other in the interval .

- (3)

- The third property is completeness: For every , when , Parseval’s identity holds, that is:

Therefore, we can write the relationship between BPFs and their integrals in the following matrix form.

The above representation and disjointness property follows

and

where usually denotes a diagonal matrix whose diagonal entries are related to a constant vector .

2.1. Function Approximations

A real bounded function , where , can be expanded into a block-pulse series as

where is the block-pulse coefficient with respect to the th BPF .

Let . It can be similarly expanded with respect to BPFs such as

where and are and dimensional BPF vectors, respectively, and is the block-pulse coefficient matrix with

where and . For convenience, we put .

2.2. Integration Operational Matrix

Computing follows to yield

From [34], we have:

where the operational matrix of integration is given by

Therefore, each function can be expressed as

3. Stochastic Integration Operational Matrix

The It integral of each single BPF can be computed as follows:

Now by expressing in terms of the BPFs, we have

Therefore,

In this case, the stochastic operational matrix of integration can be expressed as follows:

where and ; and .

Therefore, the It integral of every function can be manipulated as follows:

By approximating the functions via BPFs by relations, we have

.

4. Implementation in Stochastic Integral Equation

Using the block-pulse operational matrices, we first find the collocation approximation to the functions and for drift and diffusion, respectively, which are defined by

We can approximate and , and we can assume that is a function of two variables via the block-pulse series as follows:

such that m vectors and matrix G are the block-pulse coefficients of and and , respectively. By substituting (24) in (22), we obtain

In addition, the Its integral of (22) can be written as

where diag , and diag. By substituting (25) and (26) into (23), as well as by replacing ≃ with =, we obtain

5. General Error Estimate

In this section, we will provide the general estimate used to determine the convergence. We shall first rely the following presumptions:

- (I)

- If , there exists a constant L such that

- (II)

- If , there exists a constant L such that

- (III)

- There exists a constant and L such that, for continuous process , there is an -adapted value.

The regularity of (Theorem 3.7 and 4.1 in [5]) provide the following result of well-posedness of the BSVIE.

Theorem 1.

A unique solution to the BSIVE is admissible under assumptions (I)–(III). In addition, the following estimate holds:

Furthermore, the following BSVIE has an adapted solution :

Additionally, for each .

The convergence speed is calculated using the following result:

Lemma 1.

For each , it holds under assumptions (I)–(III) that

where C is a constant.

Proof.

Assume that . Under the assumptions (Corollary 3.6 in [5]) and (I)–(III), we have

In order to apply the assumptions (Corollary 3.6 in [5]) to , one must first apply the following:

Grownwall’s inequality leads to the conclusion that . Thus,

6. Numerical Results

In this section, we will provide two numerical examples to illustrate the results obtained in Section 3 and Section 4. All computations were carried out in MATLAB R2018a, with a precision of . To compare the values of the approximate and exact solutions at selected points, we used the definition of the absolute error, which is as follows:

where represents the exact solution, and represents the approximate solution.

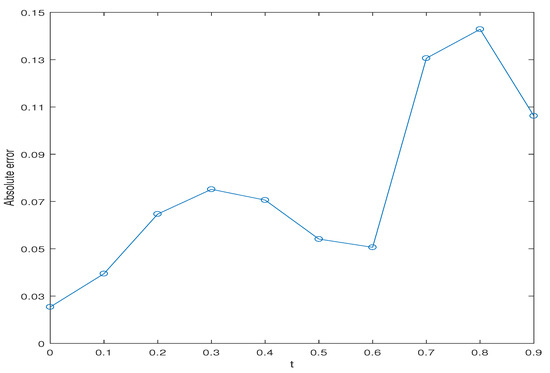

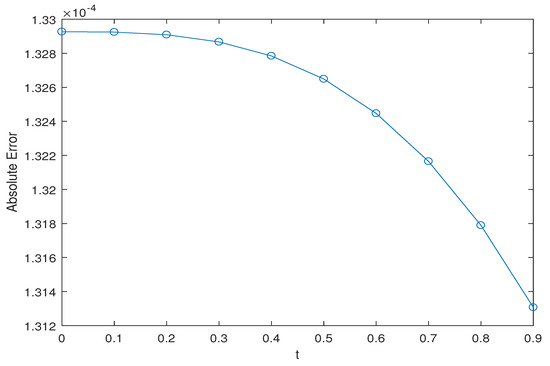

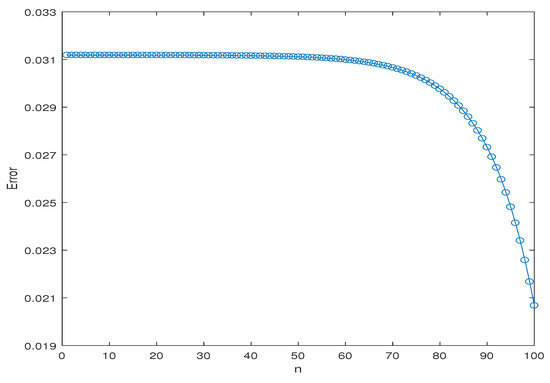

Example 1

([24]). The Hull–White Model: Hull and White investigated Vasicek model extensions that perfectly fit the basic term structure in 1990. A single-factor interest rate model is the Hull–White model. The short interest rate is assumed to have a normal distribution in this model, and there is no arbitrage assumption. The short interest rate, therefore, satisfies the stochastic differential equation.

is a Brownian motion, and . The exact solution of Equation (37) for is provided by

The results obtained for and in this example are given in Table 1. The approximate and exact solutions’ graphs and the absolute error for ; , , , and are plotted in Figure 1, Figure 2 and Figure 3, respectively. The accuracy of the generalized absolute error in Table 1 depends on the parameters . The error decreases as time steps increase.

Table 1.

Mean, standard deviation, and mean confidence interval for error.

Figure 1.

The graph of absolute error function for Example 1.

Figure 2.

The trajectory of the approximate solution and exact solution of Example 1.

Figure 3.

Variation trend of absolute error of Example 1.

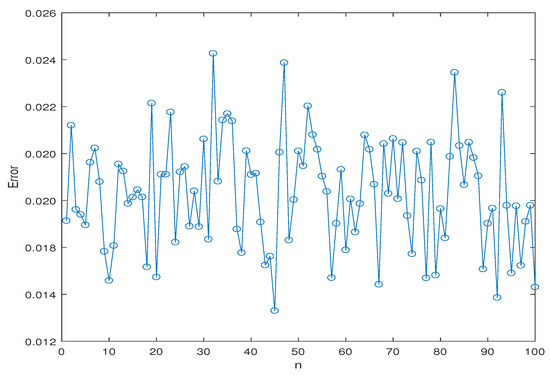

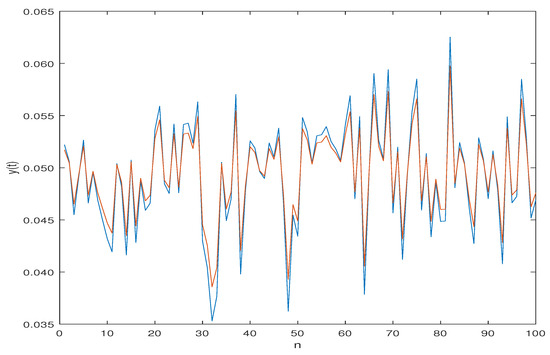

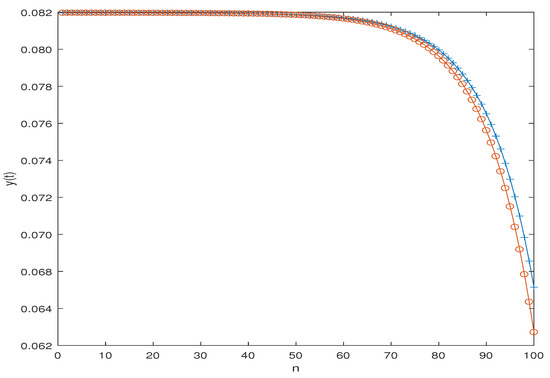

Example 2

([24]). Consider the following nonlinear stochastic Volterra integral equation

with the exact solution

Assume that , and . Table 2 displays the numerical results for various values of m, including the absolute error for the figures—both exact and approximate—for the parameters , and . Figure 4, Figure 5 and Figure 6 show the exact and approximate solutions, as well as the variation trend.

Table 2.

Mean, standard deviation, and mean confidence interval for error.

Figure 4.

The graph of absolute error function for Example 2.

Figure 5.

Variation trend of absolute error of Example 2.

Figure 6.

The trajectory of the approximate solution and exact solution of Example 2.

7. Conclusions

The current study focuses on the so-called Type-II BSVIEs, where the coefficient is dependent on both t and s, and depends not only on , but also on . This paper proposed a collocation approximation method to predict an unknown function. By implementing Newton’s method, we solve the BSVIEs using block-pulse functions and the corresponding stochastic operational matrix of integration. In addition, we have included examples that demonstrate estimate analysis while highlighting the separate convergence of the two approximating sequences. We also measured the solutions against the values of the exact and approximate solutions at a few selected locations using a specified absolute error. According to the collocation approximation solutions, the issues raised in the work might be applied to Type-I BSVIEs. However, this strategy requires an entirely new methodology, and it is left to future studies to determine the error by computing conditional expectations. It might be the focus of some future research.

Author Contributions

Conceptualization, K.E.Y.; methodology, M.S. and K.E.Y.; software, M.S.; validation, M.S.; formal analysis and investigation, X.Z.; resources, M.S. and X.Z.; writing—original draft preparation, K.E.Y. and M.S.; supervision, X.Z. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by the Zhejiang Normal University Postdoctoral Research Fund (Grant No. ZC304022938), the Natural Science Foundation of China (Project No. 61976196) and the Zhejiang Provincial Natural Science Foundation of China under Grant No. LZ22F030003.

Data Availability Statement

Not applicable.

Acknowledgments

We would like to express our thanks to the editors and reviewers.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Pardoux, E.; Peng, S.G. Adapted solution of a backward stochastic differential equation. Syst. Control Lett. 1990, 14, 55–61. [Google Scholar] [CrossRef]

- Pardoux, E.; Peng, S.G. Backward stochastic differential equations and quasilinear parabolic partial differential equations. In Stochastic Partial Differential Equations and Their Applications; Springer: Berlin/Heidelberg, Germany, 1992; Volume 176, pp. 200–217. [Google Scholar]

- Shi, Y.; Wang, T. Solvability of general backward stochastic volterra integral equations. J. Korean Math. Soc. 2012, 49, 1301–1321. [Google Scholar] [CrossRef]

- Yong, J. Backward stochastic Volterra integral equations and some related problems. Stoch. Process. Their Appl. 2006, 116, 779–795. [Google Scholar] [CrossRef]

- Yong, J. Well-posedness and regularity of backward stochastic Volterra integral equations. Probab. Theory Relat. Fields 2008, 142, 21–77. [Google Scholar] [CrossRef]

- Wang, H. Extended backward stochastic Volterra integral equations, quasilinear parabolic equations, and Feynman-Kac formula. Stoch. Dyn. 2021, 21, 2150004. [Google Scholar] [CrossRef]

- Pardoux, E.; Peng, S.G. Backward doubly stochastic differential equation and systems of quasilinear SPDEs. Probab. Theory Relat. Fields 1994, 98, 209–227. [Google Scholar] [CrossRef]

- Lin, J. Adapted solution of a backward stochastic nonlinear Volterra integral equation. Stoch. Anal. Appl. 2002, 20, 165–183. [Google Scholar] [CrossRef]

- Aman, A.; N’zi, M. Backward stochastic nonlinear Volterra integral equations with local Lipschitz drift. Prob. Math. Stat. 2005, 25, 105–127. [Google Scholar]

- Karoui, N.E.; Peng, S.; Quenez, M. Backward stochastic differential equations in finance. Math. Financ. 1997, 7, 1–71. [Google Scholar] [CrossRef]

- Yong, J. Continuous-time dynamick risk measures by backward stochastic Volterra integral equations. Appl. Anal. 2007, 86, 1429–1442. [Google Scholar] [CrossRef]

- Wang, H.; Sun, J.; Yong, J. Recursive utility processes, dynamick risk measures and quadratic backward stochastic Volterra integral equations. Appl. Math. Optim. 2021, 84, 145–190. [Google Scholar] [CrossRef]

- Kromer, E.; Overbeck, L. Differentiability of BSIVEs and dynamic capital allocations. Int. J. Theory Appl. Financ. 2017, 20, 1–26. [Google Scholar] [CrossRef]

- Bender, C.; Denk, R. A forward scheme for backward SDEs. Stoch. Process. Their Appl. 2007, 117, 1793–1812. [Google Scholar] [CrossRef]

- Bender, C.; Pokalyuk, S. Discretization of backward stochastic Volterra integral equations, Recent Developments in Computational Finance. Interdiscip. Math. Sci. 2013, 14, 245–278. [Google Scholar]

- Zhang, J. A Numerical scheme for BSDEs. Ann. Appl. Probab. 2004, 14, 459–488. [Google Scholar] [CrossRef]

- Zhang, J. Backward Stochastic Differential Equations: From Linear to Fully Nonlinear Theory; Springer: Berlin/Heidelberg, Germany, 2017. [Google Scholar]

- Popier, A. Backward stochastic Volterra integral equations with jumps in a general filtration. ESAIM Prob. Stats. 2021, 25, 133–203. [Google Scholar] [CrossRef]

- Hu, Y.; Oksendal, B. Linear Volterra backward stochastic integral equations. Stoch. Process. Their Appl. 2019, 129, 626–633. [Google Scholar] [CrossRef]

- Agram, N. Dynamick risk measure for BSVIE with jumps and semimartingale issues. Stoch. Anal. Appl. 2019, 37, 361–376. [Google Scholar] [CrossRef]

- Hamaguchi, Y.; Taguchi, D. Approximations for adapted M-solution of type-II backward stochastic Volterra integral equations. ESAIM Probab. Stat. 2023, 27, 19–79. [Google Scholar] [CrossRef]

- Fu, K.; Zeng, X.; Li, X.; Du, J. A Convolution Method for Numerical Solution of Backward Stochastic Differential Equations Based on the Fractional FFT. Fractal Fract. 2023, 7, 44. [Google Scholar] [CrossRef]

- Maleknejad, K.; Khodabin, M.; Rostami, M. Numerical solution of stochastic Volterra integral equations by a stochastic operational matrix based on block pulse functions. Math. Comput. Model. 2012, 55, 791–800. [Google Scholar] [CrossRef]

- Saffarzadeh, M.; Loghmani, G.B.; Heydari, M. An iterative technique for the numerical solution of nonlinear stochastic Itô-Volterra integral equations. J. Comput. Appl. Math. 2018, 333, 74–86. [Google Scholar] [CrossRef]

- Khan, S.U.; Ali, M.; Ali, I. A spectral collocation method for stochastic Volterra integro-differential equations and its error analysis. Adv. Differ. Equ. 2019, 2019, 161. [Google Scholar] [CrossRef]

- Xie, J.; Huang, Q.; Zhao, F. Numerical solution of nonlinear Volterra-Fredholm-Hammerstein integral equations in two-dimensional spaces based on block pulse functions. J. Comp. Appl. Math. 2017, 317, 565–572. [Google Scholar] [CrossRef]

- Khodabina, M.; Maleknejad, K.; Rostami, M.; Nouri, M. Numerical approach for solving stochastic Volterra-Fredholm integral equations by stochastic operational matrix. Comput. Math. Appl. 2012, 64, 1903–1913. [Google Scholar] [CrossRef][Green Version]

- Maleknejad, K.; Khodabin, M.; Rostami, M. A numerical method for solving m-dimensional stochastic Ito-Volterra integral equations by stochastic operational matrix. Comput. Math. Appl. 2012, 63, 133–143. [Google Scholar] [CrossRef][Green Version]

- Geng, F.Z. Piecewise reproducing kernel-based symmetric collocation approach for linear stationary singularly perturbed problems. AIMS Math. 2020, 5, 6020–6029. [Google Scholar] [CrossRef]

- Ali, I.; Khan, S.U. A Dynamic Competition Analysis of Stochastic Fractional Differential Equation Arising in Finance via Pseudospectral Method. Mathematics 2023, 11, 1328. [Google Scholar] [CrossRef]

- Momendzade, N.; Vahidi, A.R.; Babolian, E. A computational method for solving stochastic Ito-Volterra integral equation with multi-stochastic terms. Math. Sci. 2018, 12, 295–303. [Google Scholar] [CrossRef]

- Maleknejad, K.; Hashemizadeh, E.; Ezzati, R. A new approach to the numerical solution of Volterra integral equations by using Bernstein’s approximation. Commun. Nonlinear Sci. Numer. Simulat. 2011, 16, 647–655. [Google Scholar] [CrossRef]

- He, J.-H.; Taha, M.H.; Ramadan, M.A.; Moatimid, G.M. Improved Block-Pulse Functions for Numerical Solution of Mixed Volterra-Fredholm Integral Equations. Axioms 2021, 10, 200. [Google Scholar] [CrossRef]

- Jiang, Z.H.; Schaufelberger, W. Block Pulse Functions and Their Applications in Control Systems; Springer: Berlin/Heidelberg, Germany, 1992. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).