Impact of Climate Risk on the Financial Performance and Financial Policies of Enterprises

Abstract

:1. Introduction

2. Literature Review

2.1. Analysis of the Existing Literature

2.1.1. Climate Risk

2.1.2. Measurement of Climate Risk

2.1.3. The Impact of Climate Risk on Financial Performance

2.1.4. The Impact of Climate Risk on Debt

2.1.5. Application of Modern Financial Theory

2.2. Innovation and Research Questions of This Study

2.3. Hypotheses

3. Research Methodology

3.1. Methodological Choice and Data Analysis Technique

3.2. Description of Data and Sources

4. Data Analysis and Research Findings

4.1. Data Analysis Process

4.1.1. Application of Statistical Analysis

4.1.2. Regression Analysis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Trexler, M.C.; Kosloff, L.H. Adapting to Climate Change: 2.0 Enterprise Risk Management, 1st ed.; Routledge: London, UK, 2013. [Google Scholar]

- Alola, A.A. Risk to investment and renewables production in the United States: An inference for environmental sustainability. J. Clean. Prod. 2022, 312, 127652. [Google Scholar] [CrossRef]

- Wang, T. An In-Depth Analysis of the Impact of ESG Investing on Returns Using Large-Scale News Data. Master’s Thesis, ETH Zurich, Zürich, Switzerland, 2019. [Google Scholar]

- Liu, F. The Development of Climate Finance in Asia: Drivers, Processes, Outcomes. Ph.D. Thesis, King’s College London, London, UK, 2021. [Google Scholar]

- Paseda, O.A.; Okanya, O. Climate Change in the Theory of Finance. J. Econ. Sustain. Dev. 2020, 11, 29–46. [Google Scholar]

- Zhu, B.; Hu, X.; Deng, Y.; Zhang, B.; Li, X. The differential effects of climate risks on non-fossil and fossil fuel stock markets: Evidence from China. Financ. Res. Lett. 2023, 55, 103962. [Google Scholar] [CrossRef]

- Choudhury, T.; Hasan, F.; Djajadikerta, H.; Hassan, M.K.; Kamran, M.; Boubaker, S.; Sarker, T. Renewable Energy Supply and Risk in Global Banking. 2023. Available online: https://www.orfonline.org/wp-content/uploads/2023/06/T20_PolicyBrief_TF4_408_RenewableEnergyAndGlobalBanking.pdf (accessed on 19 July 2023).

- IPCC. Fifth Assessment Report; The United Nations Intergovernmental Panel on Climate Change: Pairs, France, 2014.

- UNFCCC. Paris Agreement; The United Nations Framework Convention on Climate Change: Pairs, France, 2015.

- Sakhel, A. Corporate climate risk management: Are European companies prepared? J. Clean. Prod. 2017, 165, 103–118. [Google Scholar] [CrossRef]

- Fang, M.; Tan, K.S.; Wirjanto, T.S. Sustainable portfolio management under climate change. J. Sustain. Financ. Invest. 2019, 9, 45–67. [Google Scholar] [CrossRef]

- Eckstein, D.; Künzel, V.; Schäfer, L. Global Climate Risk Index 2021; Germanwatch: Bonn, Germany, 2021. [Google Scholar]

- Dell, M.; Jones, B.F.; Olken, B.A. What Do We Learn from the Weather? The New Climate-Economy Literature. J. Econ. Lit. 2014, 52, 740–798. [Google Scholar] [CrossRef]

- Sun, Y.; Yang, Y.; Huang, N.; Zou, X. The impacts of climate change risks on financial performance of mining industry: Evidence from listed companies in China. Resour. Policy 2020, 69, 101828. [Google Scholar] [CrossRef]

- Midttun, M.S.; Gjengedal, L.Ø. The Impact of Carbon Emissions on Investment Performance: An Empirical Analysis of How Carbon Footprint Affects Risk-Adjusted Return for Stocks Listed on the Oslo Stock Exchange. Master’s Thesis, Norwegian School of Economics, Bergen, Norway, 2019. [Google Scholar]

- Bos, J.W.; Li, R.; Sanders, M.W. Hazardous lending: The impact of natural disasters on bank asset portfolio. Econ. Model. 2022, 108, 105760. [Google Scholar] [CrossRef]

- Huang, H.H.; Kerstein, J.; Wang, C. The impact of climate risk on firm performance and financing choices: An international comparison. J. Int. Bus. Stud. 2018, 49, 633–656. [Google Scholar] [CrossRef]

- Tschakert, P.; Dietrich, K.A. Anticipatory Learning for Climate Change Adaptation and Resilience. Ecol. Soc. 2010, 15, 26268129. [Google Scholar] [CrossRef]

- Lemma, T.T.; Lulseged, A.; Tavakolifar, M. Corporate commitment to climate change action, carbon risk exposure, and a firm’s debt financing policy. Bus. Strategy Environ. 2021, 30, 3919–3936. [Google Scholar] [CrossRef]

- Freedman, M. The Social Responsibility of Business is to Increase Profits. The New York Times, 13 September 1970. [Google Scholar]

- Freeman, R.E.; Harrison, J.S.; Wicks, A.C.; Parmar, B.L.; De Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: New York, NY, USA, 2010. [Google Scholar]

- Sandberg, J. Towards a Theory of Sustainable Finance; UNEP Inquiry & The Centre for International Governance Innovation: Waterloo, ON, Canada, 2015. [Google Scholar]

- Masulis, R.; Mobbs, S. Independent director incentives: Where do talented directors spend their limited time and energy? J. Financ. Econ. 2014, 111, 406–429. [Google Scholar] [CrossRef]

- In, S.Y.; Weyant, J.P.; Manav, B. Pricing climate-related risks of energy investments. Renew. Sustain. Energy Rev. 2022, 154, 111881. [Google Scholar] [CrossRef]

- Wagner, M.; Schaltegger, S.; Wehrmeyer, W. The relationship between the environmental and economic performance of firms: What does theory propose and what does empirical evidence tell us? Greener Manag. Int. 2001, 34, 95–108. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| n | Minimum | Maximum | Mean | Std. Deviation | |

|---|---|---|---|---|---|

| Return on Assets | 431 | −38.3188 | 41.4595 | 5.425303 | 8.2453643 |

| Cash From Operations | 435 | −115,970.098 | 207,459 | 9651.847502 | 23,138.71624 |

| Short-Term Debt | 435 | 0 | 163,397.407 | 8711.012456 | 19,611.27849 |

| Long-Term Debt | 435 | 0 | 405,217.489 | 30,436.14316 | 65,019.98609 |

| Short- and Long-Term Debt | 435 | 1.516 | 940,682.427 | 49,382.74031 | 118,058.9699 |

| Total Assets | 435 | 31.426 | 1,899,340.511 | 159,275.9495 | 320,122.631 |

| Total Intangible Assets | 435 | 0 | 142,742.613 | 14,616.80705 | 26,018.15411 |

| Sales—5 Year Average Growth | 435 | −13.1864 | 111.6382 | 6.607081 | 10.9374627 |

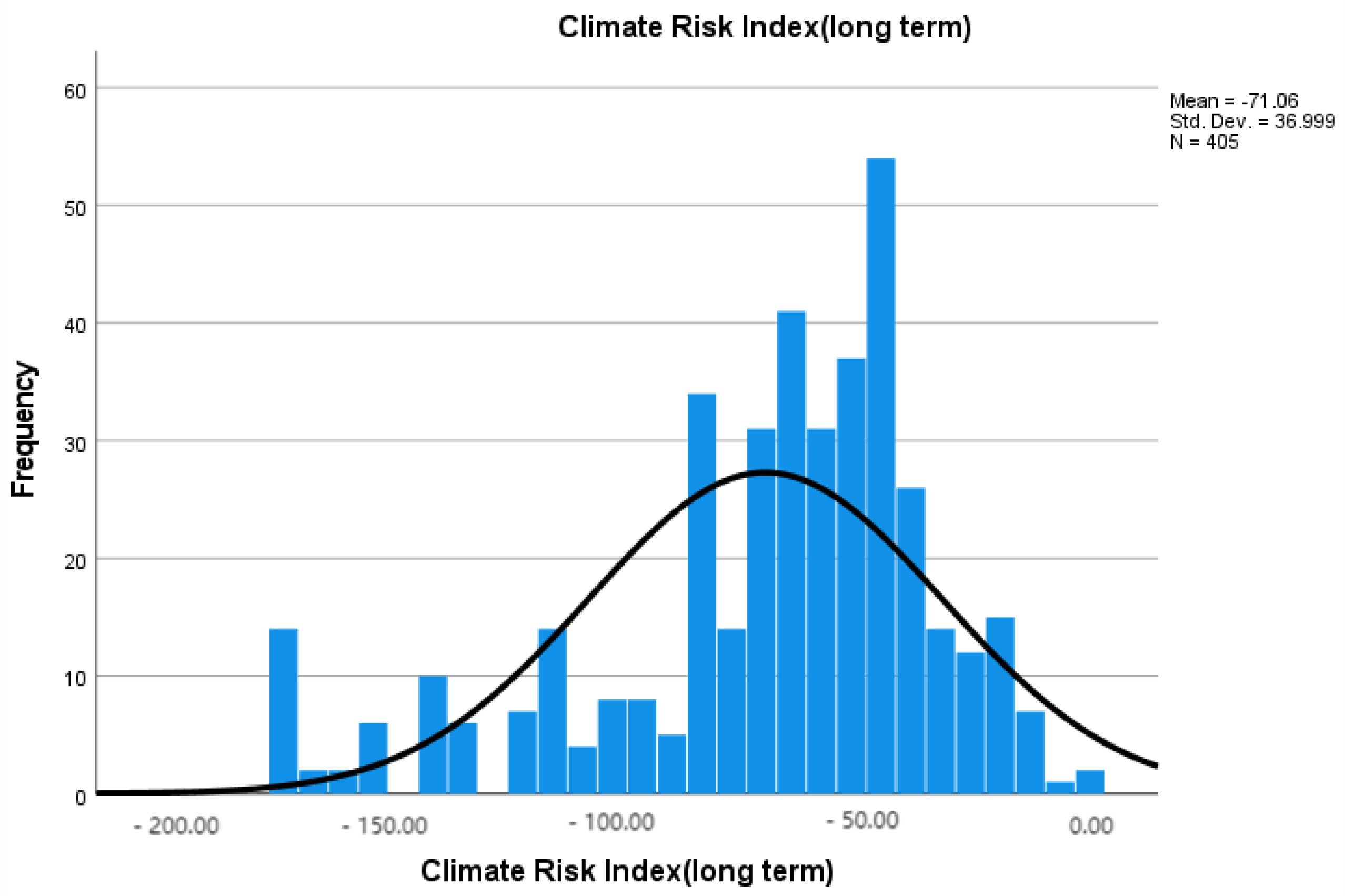

| climate risk index (annual) | 435 | −125 | −5.5 | −61.8998 | 28.90067 |

| CRI Annual | ROA | CFO | Short-Term Debt | Long-Term Debt | Short- and Long-Term Debt | Total Assets | Total Intangible Assets | Sales Growth | |

|---|---|---|---|---|---|---|---|---|---|

| CRI annual | 1 | ||||||||

| ROA | −0.049 | 1 | |||||||

| CFO | 0.034 | 0.069 | 1 | ||||||

| Short-Term Debt | −0.039 | −0.161 ** | 0.383 ** | 1 | |||||

| Long-Term Debt | 0.082 | −0.143 ** | 0.498 ** | 0.668 ** | 1 | ||||

| Short- and Long-Term Debt | 0.048 | −0.149 ** | 0.339 ** | 0.736 ** | 0.834 ** | 1 | |||

| Total Assets | 0.019 | −0.136 ** | 0.427 ** | 0.734 ** | 0.772 ** | 0.936 ** | 1 | ||

| Total Intangible Assets | 0.001 | −0.049 | 0.294 ** | 0.261 ** | 0.345 ** | 0.235 ** | 0.257 ** | 1 | |

| Sales Growth | 0.110 * | 0.088 | −0.02 | −0.104 * | −0.118 * | −0.093 | −0.074 | −0.122 * | 1 |

| Regression Coefficients (Significance in Parentheses) | ||

|---|---|---|

| ROA | CFO | |

| CRI annual | −0.017(0.263) | 18.411 (0.606) |

| Total Assets | −3.284 × 10−6 (0.013) | 0.027 (<0.001) |

| Total Intangible Assets | −2.060 × 10−6 (0.900) | 0.178 (<0.001) |

| Sales growth | 0.063 (0.098) | 63.442 (0.505) |

| Adjusted R² | 0.281 | 0.212 |

| F | 2.839 (0.024) | 28.186 (<0.001) |

| Durbin-Watson test | 1.176 | 1.591 |

| Variance Inflation Factor (VIF) Analysis | ||

|---|---|---|

| ROA | CFO | |

| CRI annual | 1.013 | 1.013 |

| Total Assets | 1.072 | 1.073 |

| Total Intangible Assets | 1.083 | 1.083 |

| Sales growth | 1.031 | 1.030 |

| Regression Coefficients (Significance in Parentheses) | |||

|---|---|---|---|

| Short-Term Debt | Long-Term Debt | Short- and Long-Term Debt | |

| CRI annual | −32.927 (0.153) | 166.129 (0.017) | 133.452 (0.064) |

| Total Assets | 0.044 (<0.001) | 0.148 (<0.001) | 0.345 (<0.001) |

| Total Intangible Assets | 0.055 (0.038) | 0.380 (<0.001) | −0.037 (0.651) |

| Sales growth | −65.817 (0.284) | −318.358 (0.086) | −306.365 (0.111) |

| Adjusted R² | 0.543 | 0.623 | 0.877 |

| F | 120.782 (<0.001) | 167.631 (<0.001) | 719.735 (<0.001) |

| Durbin-Watson test | 0.947 | 0.652 | 0.780 |

| Variance Inflation Factor (VIF) Analysis | |||

|---|---|---|---|

| Short-Term Debt | Long-Term Debt | Short- and Long-Term Debt | |

| CRI annual | 1.013 | 1.013 | 1.013 |

| Total Assets | 1.073 | 1.073 | 1.073 |

| Total Intangible Assets | 1.083 | 1.083 | 1.083 |

| Sales growth | 1.030 | 1.030 | 1.030 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, X.; Zhang, M.; Fang, Z. Impact of Climate Risk on the Financial Performance and Financial Policies of Enterprises. Sustainability 2023, 15, 14833. https://doi.org/10.3390/su152014833

Zhang X, Zhang M, Fang Z. Impact of Climate Risk on the Financial Performance and Financial Policies of Enterprises. Sustainability. 2023; 15(20):14833. https://doi.org/10.3390/su152014833

Chicago/Turabian StyleZhang, Xin, Mateng Zhang, and Zhong Fang. 2023. "Impact of Climate Risk on the Financial Performance and Financial Policies of Enterprises" Sustainability 15, no. 20: 14833. https://doi.org/10.3390/su152014833

APA StyleZhang, X., Zhang, M., & Fang, Z. (2023). Impact of Climate Risk on the Financial Performance and Financial Policies of Enterprises. Sustainability, 15(20), 14833. https://doi.org/10.3390/su152014833