Climate Change Exposure and Firm Performance: Does Managerial Ability Matter?

Abstract

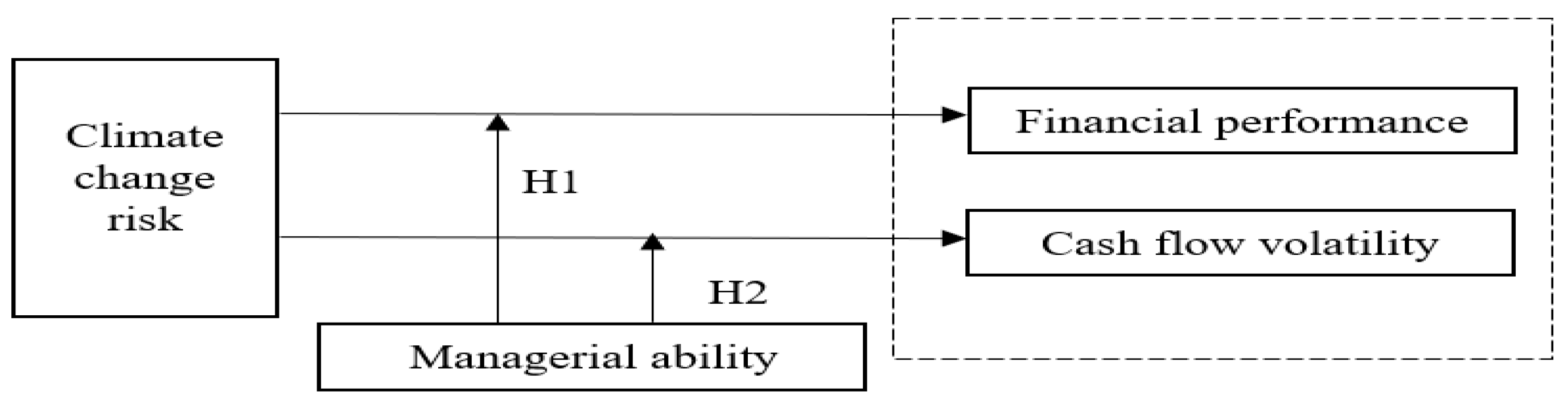

:1. Introduction

2. Literature Review and Hypotheses Development

3. Research Design

3.1. Data and Sample

3.2. Model Specification

4. Results and Discussion

5. Addressing the Endogeneity Issue and Robustness Checks

5.1. Addressing the Endogeneity Issue

5.2. Robustness Checks

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Dell, M.; Jones, B.F.; Olken, B.A. What do we learn from the weather? The new climate-economy literature. J. Econ. Lit. 2014, 52, 740–798. [Google Scholar] [CrossRef]

- Dell, M.; Jones, B.F.; Olken, B.A. Temperature and income: Reconciling new cross-sectional and panel estimates. Am. Econ. Rev. 2009, 99, 198–204. [Google Scholar] [CrossRef]

- Gallup, J.L.; Sachs, J.D.; Mellinger, A.D. Geography and economic development. Int. Reg. Sci. Rev. 1999, 22, 179–232. [Google Scholar] [CrossRef]

- Berkhout, F.; Hertin, J.; Gann, D.M. Learning to adapt: Organisational adaptation to climate change impacts. Clim. Chang. 2006, 78, 135–156. [Google Scholar] [CrossRef]

- Gasbarro, F.; Pinkse, J. Corporate adaptation behaviour to deal with climate change: The influence of firm-specific interpretations of physical climate impacts. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 179–192. [Google Scholar] [CrossRef]

- Linnenluecke, M.K.; Griffiths, A.; Winn, M.I. Firm and industry adaptation to climate change: A review of climate adaptation studies in the business and management field. Wiley Interdiscip. Rev. Clim. Chang. 2013, 4, 397–416. [Google Scholar] [CrossRef]

- Ozkan, A.; Temiz, H.; Yildiz, Y. Climate risk, corporate social responsibility, and firm performance. Br. J. Manag. 2022. [Google Scholar] [CrossRef]

- Henderson, P.R.M.; Reinert, S.A. Climate Change in 2018: Implications for Business; Harvard Business School Background Note; Havard University: Cambridge, MA, USA, 2015. [Google Scholar]

- Jia, J.; Li, Z. Does external uncertainty matter in corporate sustainability performance? J. Corp. Financ. 2020, 65, 101743. [Google Scholar] [CrossRef]

- Huang, H.H.; Kerstein, J.; Wang, C. The impact of climate risk on firm performance and financing choices: An international comparison. J. Int. Bus. Stud. 2018, 49, 633–656. [Google Scholar] [CrossRef]

- Klasa, S.; Ortiz-Molina, H.; Serfling, M.; Srinivasan, S. Protection of trade secrets and capital structure decisions. J. Financ. Econ. 2018, 128, 266–286. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper Echelon: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Hambrick, D.C. Upper echelons theory: An update. Acad. Manag. Rev. 2007, 32, 334–343. [Google Scholar] [CrossRef]

- Hmaittane, A.; Bouslah, K.; M’Zali, B.; Ibariouen, I. Corporate sustainability and cost of equity capital: Do managerial abilities matter? Sustainability 2022, 14, 1363. [Google Scholar] [CrossRef]

- Demerjian, P.; Lev, B.; Lewis, M.F.; McVay, S.E. Managerial ability and earnings quality. Account. Rev. 2013, 88, 463–498. [Google Scholar] [CrossRef]

- Andreou, P.C.; Karasamani, I.; Louca, C.; Ehrlich, D. The impact of managerial ability on crisis-period corporate investment. J. Bus. Res. 2017, 79, 107–122. [Google Scholar] [CrossRef]

- Krishnan, G.V.; Wang, C. The relation between managerial ability and audit fees and going concern opinions. Audit. J. Pract. Theory 2015, 34, 139–160. [Google Scholar] [CrossRef]

- Lee, K.Y.; Yoon, S.M. Managerial ability and tax planning: Trade-off between tax and nontax costs. Sustainability 2020, 12, 370. [Google Scholar] [CrossRef]

- Chang, Y.Y.; Dasgupta, S.; Hilary, G. CEO ability, pay, and firm performance. Manag. Sci. 2016, 56, 1633–1652. [Google Scholar] [CrossRef]

- Carmeli, A.; Tishler, A. The relationships between intangible organizational elements and organizational performance. Strateg. Manag. J. 2004, 25, 1257–1278. [Google Scholar] [CrossRef]

- Andreou, P.C.; Philip, D.; Robejsek, P. Bank liquidity creation and risk-taking: Does managerial ability matter? J. Bus. Financ. Account. 2016, 43, 226–259. [Google Scholar] [CrossRef]

- Cao, M.; Wei, J. Stock market returns: A note on temperature anomaly. J. Bank. Financ. 2005, 29, 1559–1573. [Google Scholar] [CrossRef]

- Novy-Marx, R. Predicting anomaly performance with politics, the weather, global warming, sunspots, and the stars. J. Financ. Econ. 2014, 112, 137–146. [Google Scholar] [CrossRef]

- Ahmad, M.F.; Aktas, N.; Croci, E. Climate risk and deployment of corporate resources to working capital. Econ. Lett. 2023, 224, 111002. [Google Scholar] [CrossRef]

- Bertrand, M.; Schoar, A. Managing with style: The effect of managers on firm policies. Q. J. Econ. 2003, 118, 1169–1208. [Google Scholar] [CrossRef]

- Beatty, A.; Liao, S. Do delays in expected loss recognition affect banks’ willingness to lend? J. Account. Econ. 2011, 52, 1–20. [Google Scholar] [CrossRef]

- Chen, Y.; Podolski, E.J.; Veeraraghavan, M. Does managerial ability facilitate corporate innovative success? J. Empir. Financ. 2015, 34, 313–326. [Google Scholar] [CrossRef]

- Leverty, J.T.; Grace, M.F. Dupes or incompetents? An examination of management’s impact on firm distress. J. Risk Insur. 2012, 79, 751–783. [Google Scholar] [CrossRef]

- Demerjian, P.; Lev, B.; McVay, S. Quantifying managerial ability: A new measure and validity tests. Manag. Sci. 2012, 58, 1229–1248. [Google Scholar] [CrossRef]

- Chen, S.S.; Lin, C.Y. Managerial ability and acquirer returns. Q. Rev. Econ. Financ. 2018, 68, 171–182. [Google Scholar] [CrossRef]

- Chemmanur, T.J.; Paeglis, I.; Simonyan, K. Financial and investment quality, management information policies, and asymmetric. J. Financ. Quant. Anal. 2009, 44, 1045–1079. [Google Scholar] [CrossRef]

- Chemmanur, T.J.; Paeglis, I. Management quality, certification, and initial public offerings. J. Financ. Econ. 2005, 76, 331–368. [Google Scholar] [CrossRef]

- Park, W.; Byun, C.G. Effect of sme’s managerial ability and executive compensation on firm value. Sustainability 2021, 13, 1828. [Google Scholar] [CrossRef]

- Sautner, Z.; Van Lent, L.; Vilkov, G.; Zhang, R. Firm-level climate change exposure. J. Financ. 2023, LXXVIII, 1449–1498. [Google Scholar] [CrossRef]

- Almustafa, H.; Nguyen, Q.K.; Liu, J.; Dang, V.C. The impact of COVID-19 on firm risk and performance in MENA countries: Does national governance quality matter? Gaeta GL, editor. PLoS ONE 2023, 18, e0281148. [Google Scholar] [CrossRef]

- Ibhagui, O.W.; Olokoyo, F.O. Leverage and firm performance: New evidence on the role of firm size. N. Am. J. Econ. Financ. 2018, 45, 57–82. [Google Scholar] [CrossRef]

- Sautner, Z.; van Lent, L.; Vilkov, G.; Zhang, R. Pricing climate change exposure. Manag. Sci. 2023; in press. [Google Scholar] [CrossRef]

- Gujarati, D. Basic Econometrics; McGraw-Hill: New York, NY, USA, 2003. [Google Scholar]

- Wooldridge, J.M. Introductory Econometrics: A Modern Approach, 6th ed.; Cengage Learning: Boston, MA, USA, 2016. [Google Scholar]

- Dougal, C.; Rettl, D.A. Firm listing status and the investment home bias. J. Corp. Financ. 2021, 71, 102095. [Google Scholar] [CrossRef]

- Asker, J.; Farre-Mensa, J.; Ljungqvist, A. Corporate investment and stock market listing: A puzzle? Rev. Financ. Stud. 2015, 28, 342–390. [Google Scholar] [CrossRef]

- Leuven, E.; Sianesi, B. PSMATCH2: Stata Module to Perform Full Mahalanobis and Propensity Score Matching, Common Support Graphing, and Covariate Imbalance Testing; Boston College Department of Economics: Boston, MA, USA, 2003. [Google Scholar]

- Almaghrabi, K.S. Borrowing during periods of policy uncertainty: The role of foreign lenders. Int. Rev. Financ. Anal. 2021, 77, 101860. [Google Scholar] [CrossRef]

- Almaghrabi, K.S. Non-operating risk and cash holdings: Evidence from pension risk. J. Bank. Financ. 2023, 152, 106878. [Google Scholar] [CrossRef]

- Almaghrabi, K.S. COVID-19 and the cost of bond debt: The role of corporate diversification. Financ. Res. Lett. 2022, 46, 102454. [Google Scholar] [CrossRef] [PubMed]

- DeFond, M.; Erkens, D.; Zhang, J. Do client characteristics really drive the big N audit quality effect? New evidence from propensity score matching. Manag. Sci. 2017, 63, 3628–3649. [Google Scholar] [CrossRef]

- Shipman, J.E.; Swanquist, Q.T.; Whited, R.L. Propensity score matching in accounting research. Account. Rev. 2017, 92, 213–244. [Google Scholar] [CrossRef]

- Engle, R.F.; Giglio, S.; Kelly, B.; Lee, H.; Stroebel, J. Hedging climate change news. Rev. Financ. Stud. 2020, 33, 1184–1216. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Definition | Source |

|---|---|---|

| ROA | Earnings before interest, taxes, and depreciation divided by total assets (date items: ebitda/at). | Compustat |

| NI | Net income divided by total assets (date items: ni/at). | Compustat |

| CF | Cash flow from operations divided by total assets (date items: (oibdp-xint-txt)/at). | Compustat |

| Climate Risk | Firm-level climate change exposure. | Sautner et al. [34]: https://climatechangelab.info/publications/firm-level-climate-change-exposure (accessed on 20 June 2023) |

| Mang. Ability | The efficiency of managers in transforming corporate resources into revenues and maximizing profitability relative to industry peers. | Demerjian et al. [29]: https://peterdemerjian.weebly.com/managerialability.html (accessed on 20 June 2023) |

| Size | The natural logarithm of total assets (date item: at). | Compustat |

| MB | A firm’s market-to-book ratio (date items: (prcc_f*csho)/ceq). | Compustat |

| Tangibility | Property, plants, and equipment by total assets (date items: ppent/ceq). | Compustat |

| Sales growth | Sales growth from year t − 1 to year t (date item sale). | Compustat |

| CF Volatility3 | Volatility of cash flows over the next three years (date items: (oibdp-xint-txt)/at). | Compustat |

| CF Volatility5 | Volatility of cash flows over the next five years (date items: (oibdp-xint-txt)/at). | Compustat |

| Count | sd. | Mean | p10 | p25 | p50 | p75 | p90 | |

|---|---|---|---|---|---|---|---|---|

| ROA | 43,620 | 0.087 | 0.112 | 0.00 | 0.045 | 0.107 | 0.160 | 0.223 |

| NI | 43,620 | 0.209 | 0.001 | −0.140 | −0.010 | 0.032 | 0.075 | 0.123 |

| CF | 43,620 | 0.181 | 0.072 | −0.11 | 0.045 | 0.107 | 0.160 | 0.223 |

| CF Volatility3 | 40,252 | 0.098 | 0.059 | 0.01 | 0.012 | 0.025 | 0.060 | 0.140 |

| CF Volatility5 | 40,252 | 0.132 | 0.078 | 0.01 | 0.017 | 0.033 | 0.078 | 0.179 |

| Climate Risk | 43,620 | 0.004 | 0.002 | 0.000 | 0.001 | 0.002 | 0.003 | 0.005 |

| Mang. Ability | 43,620 | 0.147 | −0.002 | −0.14 | −0.088 | −0.035 | 0.040 | 0.175 |

| Size | 43,620 | 1.940 | 6.610 | 4.12 | 5.307 | 6.585 | 7.868 | 9.109 |

| MB | 43,620 | 6.021 | 3.301 | 0.69 | 1.305 | 2.241 | 3.967 | 7.388 |

| Tangibility | 43,620 | 0.231 | 0.243 | 0.03 | 0.069 | 0.158 | 0.346 | 0.629 |

| Sales growth | 43,620 | 0.432 | 0.151 | −0.16 | −0.024 | 0.072 | 0.205 | 0.453 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | VIF | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) ROA | 1.00 | |||||||||||

| (2) NI | 0.59 *** | 1.00 | ||||||||||

| (3) CF | 0.76 *** | 0.85 *** | 1.00 | |||||||||

| (4) CF Volatility3 | −0.21 *** | −0.47 *** | −0.49 *** | 1.00 | ||||||||

| (5) CF Volatility5 | −0.21 *** | −0.46 *** | −0.49 *** | 0.83 *** | 1.00 | |||||||

| (6) Climate Risk | −0.08 *** | −0.05 *** | −0.08 *** | 0.02 *** | 0.02 *** | 1.00 | 1.58 | |||||

| (7) Mang. Ability | 0.19 *** | 0.12 *** | 0.12 *** | −0.06 *** | −0.08 *** | −0.08 *** | 1.00 | 1.46 | ||||

| (8) Size | 0.27 *** | 0.39 *** | 0.41 *** | −0.40 *** | −0.42 *** | −0.03 *** | 0.09 *** | 1.00 | 1.23 | |||

| (9) MB | 0.07 *** | 0.02 *** | −0.00 | 0.06 *** | 0.07 *** | −0.02 *** | 0.10 *** | −0.00 | 1.00 | 1.05 | ||

| (10) Tangibility | 0.17 *** | 0.09 *** | 0.18 *** | −0.10 *** | −0.12 *** | 0.04 *** | −0.12 *** | 0.23 *** | −0.09 *** | 1.00 | 2.37 | |

| (11) Sales growth | 0.02 * | 0.06 * | 0.01 * | 0.04 | 0.05 | 0.00 | 0.13 *** | −0.11 *** | 0.09 *** | −0.04 *** | 1.00 | 1.10 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| ROA | NI | CF | ROA | NI | CF | |

| Climate Risk | −1.14 *** (−4.71) | −3.19 *** (−4.36) | −4.48 *** (−5.78) | −1.27 *** (−5.36) | −2.39 *** (−3.57) | −3.77 *** (−6.45) |

| Mang. Ability | 0.14 *** (39.29) | 0.22 *** (26.56) | 0.25 *** (26.69) | 0.12 * (1.79) | 0.16 * (1.78) | 0.17 *** (24.15) |

| Climate Risk ∗ Mang. Ability | 5.85 *** (2.93) | 16.96 *** (2.82) | 15.58 *** (2.72) | 5.10 ** (2.45) | 12.91 ** (2.32) | 11.07 ** (2.35) |

| Size | 0.01 *** (48.72) | 0.04 *** (58.86) | 0.04 *** (61.60) | |||

| MB | 0.00 *** (12.86) | 0.00 *** (4.23) | 0.00 *** (2.59) | |||

| Tangibility | 0.07 *** (26.71) | 0.04 *** (7.10) | 0.12 *** (26.51) | |||

| Sales growth | −0.00 (−0.26) | −0.01 (−1.44) | −0.02 *** (−5.98) | |||

| Constant | 0.11 *** (288.16) | −0.02 *** (−24.81) | 0.07 *** (63.65) | 0.02 *** (14.06) | −0.31 *** (−56.30) | −0.20 *** (−42.85) |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 43,620 | 43,620 | 43,620 | 43,620 | 43,620 | 43,620 |

| Adjusted R2 | 0.147 | 0.094 | 0.101 | 0.217 | 0.225 | 0.229 |

| Test [Climate Risk + Climate Risk ∗ Mang. Ability] = 0 | 1.05 | 1.01 | 0.98 | 0.92 | 0.90 | 0.75 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| CF Volatility3 | CF Volatility5 | CF Volatility3 | CF Volatility5 | |

| Climate Risk | 1.94 *** (5.26) | 1.44 ** (2.39) | 0.55 * (1.68) | 1.68 *** (3.27) |

| Mang. Ability | −0.00 (−0.97) | 0.03 (1.57) | 0.02 (1.10) | 0.04 (1.55) |

| Climate Risk ∗ Mang. Ability | −8.74 *** (−2.99) | −7.97 *** (−2.74) | −9.12 *** (−3.72) | −8.37 ** (−2.03) |

| Size | −0.02 *** (−57.57) | −0.03 *** (−59.04) | ||

| MB | 0.00 *** (3.72) | 0.00 *** (2.63) | ||

| Tangibility | −0.05 *** (−13.46) | −0.07 *** (−15.85) | ||

| Sales growth | 0.03 *** (15.19) | 0.05 *** (16.67) | ||

| Constant | 0.06 *** (127.47) | 0.08 *** (121.34) | 0.20 *** (68.86) | 0.28 *** (69.92) |

| Year FE | Yes | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes | Yes |

| Observations | 40,252 | 40,252 | 40,252 | 40,252 |

| Adjusted R2 | 0.112 | 0.072 | 0.272 | 0.293 |

| Test [Climate Risk + Climate Risk ∗ Mang. Ability] = 0 | 1.22 | 1.22 | 1.07 | 1.07 |

| (1) | (2) | (3) | |

|---|---|---|---|

| ROA | NI | CF | |

| Panel A: PSM results | |||

| Climate Risk | −1.48 *** (−6.58) | −3.04 *** (−5.54) | −4.71 *** (−10.18) |

| Mang. Ability | 0.12 *** (44.36) | 0.17 *** (24.88) | 0.18 *** (32.85) |

| Climate Risk ∗ Mang. Ability | 4.21 ** (2.23) | 9.42 ** (2.14) | 9.79 ** (2.51) |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Panel B: Clustering the standard errors at the industry level | |||

| Climate Risk | −1.27 *** (−4.04) | −2.39 *** (−2.93) | −4.07 *** (−4.96) |

| Mang. Ability | 0.12 *** (23.70) | 0.16 *** (11.92) | 0.19 *** (11.49) |

| Climate Risk ∗ Mang. Ability | 5.10 * (1.69) | 12.91 * (1.74) | 10.91 * (1.76) |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Panel C: Controlling for time-series changes in public attention to climate change | |||

| Climate Risk | −0.85 *** (−3.13) | −1.40 * (−1.80) | −3.49 *** (−4.10) |

| Mang. Ability | 0.14 *** (33.14) | 0.19 *** (20.92) | 0.23 *** (21.39) |

| Climate Risk ∗ Mang. Ability | 13.31 *** (4.98) | 37.57 *** (4.85) | 35.21 *** (4.34) |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Panel D: Controlling for additional firm-level variables | |||

| Climate Risk | −1.86 *** (−8.15) | −5.09 *** (−8.50) | −6.98 *** (−11.33) |

| Mang. Ability | 0.15 *** (45.98) | 0.26 *** (36.94) | 0.32 *** (40.18) |

| Climate Risk ∗ Mang. Ability | 3.97 ** (2.02) | 6.15 * (1.77) | 4.59 ** (1.99) |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| Panel E: Excluding the financial crisis and COVID−19 periods | |||

| Climate Risk | −1.25 *** (−4.69) | −2.10 *** (−2.69) | −4.24 *** (−4.87) |

| Mang. Ability | 0.12 *** (31.85) | 0.16 *** (17.61) | 0.19 *** (19.02) |

| Climate Risk ∗ Mang. Ability | 6.92 *** (2.83) | 12.32 * (1.77) | 12.84 * (1.83) |

| Controls | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes |

| Industry FE | Yes | Yes | Yes |

| (1) | (2) | |

|---|---|---|

| CF Volatility3 | CF Volatility5 | |

| Panel A: PSM results | ||

| Climate Risk | 0.85 * (1.84) | 2.11 ** (2.21) |

| Mang. Ability | −0.03 *** (−5.43) | −0.04 *** (−5.22) |

| Climate Risk ∗ Mang. Ability | −10.33 *** (−3.21) | −16.81 ** (−2.10) |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

| Panel B: Clustering the standard errors at the industry level | ||

| Climate Risk | 0.02 ** (2.06) | 1.61 *** (2.86) |

| Mang. Ability | 0.03 (1.57) | 0.04 (1.21) |

| Climate Risk ∗ Mang. Ability | −9.97 *** (−3.80) | −8.72 ** (−2.16) |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

| Panel C: Controlling for time-series changes in public attention to climate change | ||

| Climate Risk | 0.18 * (1.66) | 1.36 ** (2.16) |

| Mang. Ability | 0.00 (0.77) | 0.02 (0.91) |

| Climate Risk ∗ Mang. Ability | −14.10 *** (−3.93) | −12.95 ** (−2.06) |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

| Panel D: Controlling for additional firm-level variables | ||

| Climate Risk | 0.49 ** (1.99) | 1.48 *** (2.98) |

| Mang. Ability | −0.01 * (−1.66) | −0.00 (−0.32) |

| Climate Risk ∗ Mang. Ability | −9.57 *** (−3.82) | −8.53 ** (−2.12) |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

| Panel E: Excluding the financial crisis and COVID-19 periods | ||

| Climate Risk | 0.16 * (1.75) | 1.34 ** (2.14) |

| Mang. Ability | 0.03 (0.98) | −0.04 * (−1.69) |

| Climate Risk ∗ Mang. Ability | −10.16 *** (−3.66) | −8.78 * (−1.90) |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Industry FE | Yes | Yes |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almaghrabi, K.S. Climate Change Exposure and Firm Performance: Does Managerial Ability Matter? Sustainability 2023, 15, 12878. https://doi.org/10.3390/su151712878

Almaghrabi KS. Climate Change Exposure and Firm Performance: Does Managerial Ability Matter? Sustainability. 2023; 15(17):12878. https://doi.org/10.3390/su151712878

Chicago/Turabian StyleAlmaghrabi, Khadija S. 2023. "Climate Change Exposure and Firm Performance: Does Managerial Ability Matter?" Sustainability 15, no. 17: 12878. https://doi.org/10.3390/su151712878

APA StyleAlmaghrabi, K. S. (2023). Climate Change Exposure and Firm Performance: Does Managerial Ability Matter? Sustainability, 15(17), 12878. https://doi.org/10.3390/su151712878