How Smart City Construction Affects Digital Inclusive Finance in China: From the Perspective of the Relationship between Government and Large Private Capital

Abstract

1. Introduction

2. Literature Review and Empirical Strategy

2.1. Literature Review

2.2. Empirical Strategy

3. Model Setting and Data Sources

3.1. Econometric Model

3.2. Data Sources

- (1)

- Coverage: Digital finance coverage relies on electronic accounts, surpassing traditional indicators such as outlets/personnel. Internet-enabled, it transcends geographical boundaries. Regulations in China mandate linking third-party payments, e.g., Alipay, to bank cards for broader reach. More linked cards indicate improved service coverage, serving as a sub-indicator for digital finance coverage.

- (2)

- Usage depth: In terms of the depth of digital financial usage, it primarily measures the actual utilization of various digital financial services. These services encompass payment service, monetary fund business, credit business, insurance business, investment business, and credit service. From a usage standpoint, it includes both aggregate usage indicators (i.e., the number of people who use these services per 10,000 Alipay users) and individual activity indicators (per capita transaction number and per capita transaction amount).

- (3)

- Degree of digitization: Inclusive financial digitalization relies on convenience, low cost, and credit for user adoption. This showcases the benefits of these services, making digitalization crucial to the financial inclusion index system. Services with greater convenience (e.g., a higher proportion of mobile payment amounts), lower costs (e.g., lower average personal loan interest rates), and higher credit levels (e.g., a higher proportion of Sesame Credit’s deposit-free transactions) indicate effective digital financial inclusion.

4. Results

4.1. Benchmark Regression

4.2. Robustness Tests

4.2.1. Assessing Preconditions on the Effects of SCP on DIF

- (1)

- Before the approval of the first batch of SCP pilot lists in January 2013, the Digital Financial Inclusion Index of the treatment group and the control group exhibited a consistent trend, with differences remaining essentially constant. This initial observation suggests that the development trend of DIF between the prefecture-level cities included in the SCP and those not included is quite similar. Consequently, we do not reject the parallel trends assumption in the pre-period. However, Figure 1 does not indicate whether the process of each sample entering the treatment group or the control group is random, so it is necessary to further test whether the SCP is influenced by confounders (the results are presented in Section 4.2.2).

- (2)

- After the approval of the second and third batches of SCP pilot lists, the DIF development trend of the treatment group and the control group continued to converge. This observation merits consideration. First, it is recommended to conduct a dynamic heterogeneity test to determine whether the effect of SCP on the development of DIF indeed manifests over time (results are presented in Section 4.2.3). If the relationship between SCP and DIF is confirmed, it should be questioned why the difference in the Digital Financial Inclusion Index between the treatment group and the control group keeps decreasing after implementing SCP. The adjustment for prior trends and systematic bias, as well as the placebo test, are conducted to address this issue (results are shown in Section 4.2.4, Section 4.2.5 and Section 4.2.6, respectively).

- (3)

- Figure 1 preliminarily indicates that when the SCP policy is not affected, the DIF trend of individual i largely satisfies the linearity assumption. Building upon this, it is necessary to further test the DID effect of the confounder, i.e., testing whether the confounder in the model “” is affected by the SCP policy—that is, whether it meets the exogeneity assumption.

{kind=link}

{kind=link}

{kind=link}

| (1) | (2) | |

|---|---|---|

| DID | 1.4323 *** | 1.215 ** |

| (0.5166) | (0.5009) | |

| Control variables | Uncontrolled | Controlled |

| Year fixed effects | Controlled | Controlled |

| City fixed effects | Controlled | Controlled |

| Obs | 1648 | 1648 |

| R2 | 0.9941 | 0.9944 |

4.2.2. Evaluating the Effect of Covariates on SCP

4.2.3. Dynamic Heterogeneity Test

| Lagged Covariates | (1) | (2) |

|---|---|---|

| 1 Time Period | 2 Time Periods | |

| GDP per capita | 0.0208 | 0.0634 |

| (0.0318) | (0.0674) | |

| Share of secondary industry | −0.0007 | 0.0011 |

| (0.0022) | (0.0021) | |

| Share of tertiary industry | −0.0014 | 0.0004 |

| (0.0021) | (0.0021) | |

| Human capital index | −0.0034 | −0.0045 |

| (0.0031) | (0.0035) | |

| Population density | −0.0329 | −0.0474 ** |

| (0.0256) | (0.0213) | |

| Percentage of Govt. Spending on Sci. & Tech. | 0.0137 | −0.0082 |

| (0.0141) | (0.0102) | |

| Per capita telecommunications usage | 0.0285 | 0.0084 |

| (0.0193) | (0.0146) | |

| The average number of mobile phones per capita in the city | −0.0003 | −0.0004 |

| (0.0006) | (0.0006) | |

| The number of Internet connected devices per capita in the city | −0.0007 | −0.0013 |

| (0.001) | (0.0013) | |

| Average wage of employed workers | 0.0106 | −0.0158 |

| (0.0472) | (0.0625) | |

| Per capita foreign direct investment | 0.0123 | 0.0014 |

| (0.0076) | (0.0081) | |

| Year fixed effect | Controlled | Controlled |

| City fixed effect | Controlled | Controlled |

| _cons | −0.3918 | −0.3781 |

| (0.5344) | (0.801) | |

| Observations | 1442 | 1236 |

| R2 | 0.748 | 0.8429 |

4.2.4. The Adjustment for Pre-Existing Trends

4.2.5. The Adjustment for Systematic Bias

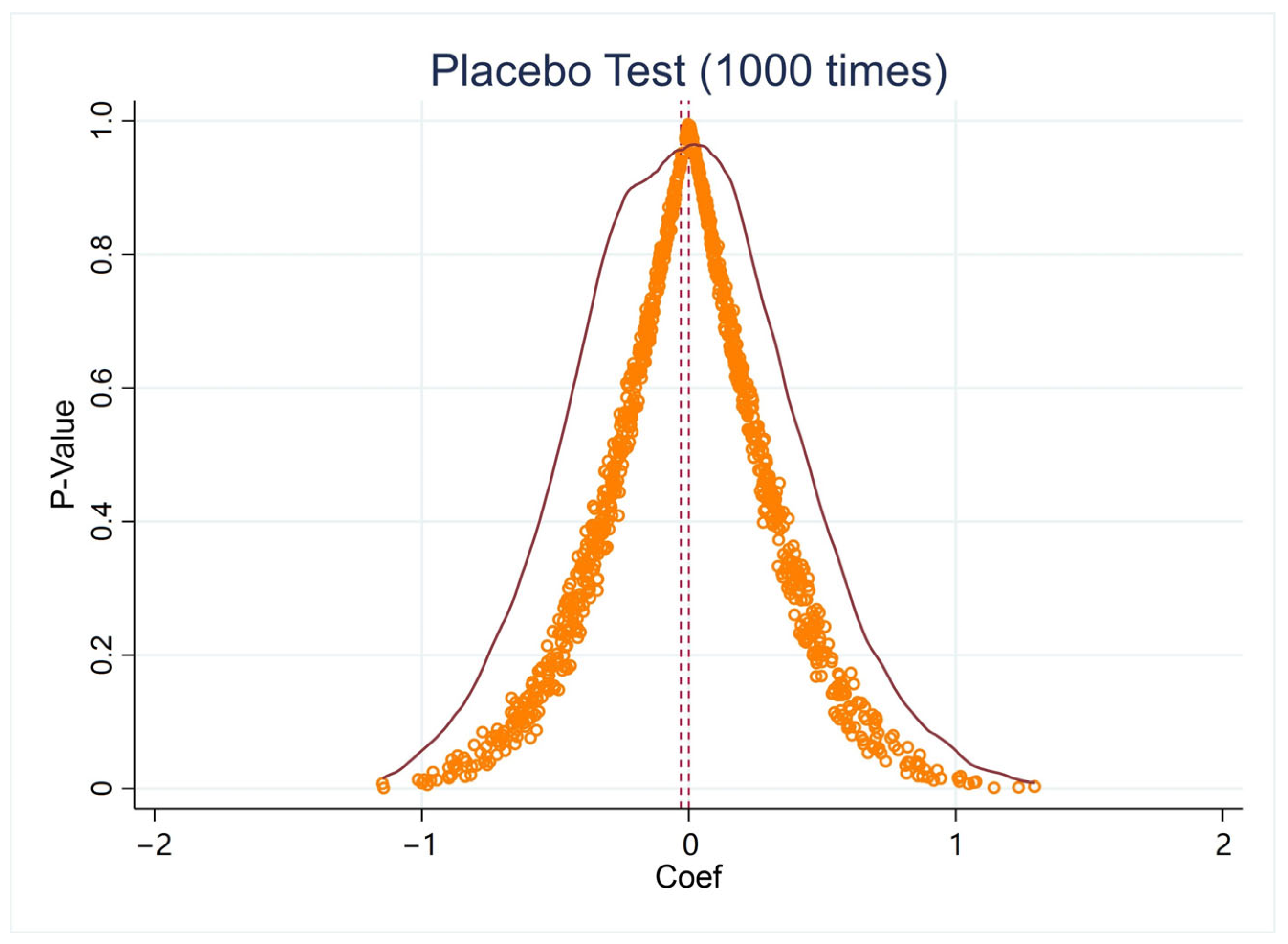

4.2.6. Placebo Tests for Randomly Generated Treatment and Control Groups

4.3. Heterogeneity Analysis for the Effect of SCP on DIF

4.4. Spatial Effects of SCP on DIF

4.4.1. Assessing Diffusion Effects of SCP

4.4.2. Selection of Spatial Econometric Model

| (1) | (2) | |

|---|---|---|

| 0~20 km | 3.9887 *** | 3.9396 *** |

| (1.1908) | (1.2404) | |

| 20~40 km | 4.897 ** | 4.1732 * |

| (2.1494) | (2.2268) | |

| 40~60 km | 2.2232 * | 1.7372 |

| (1.1769) | (1.1966) | |

| 60~80 km | 1.7448 | 1.5448 |

| (1.137) | (1.1346) | |

| 80~100 km | 2.211 | 1.6389 |

| (1.4349) | (1.4297) | |

| Control variables | Uncontrolled | Controlled |

| Year fixed effects | Controlled | Controlled |

| City fixed effects | Controlled | Controlled |

| Obs | 2280 | 2280 |

| R2 | 0.9946 | 0.9946 |

4.4.3. Regression Analysis of Fixed Effects in SDM

5. Discussion

- (1)

- The main content of smart city construction is to enhance the digital and information-based infrastructure of the city. However, the development of smart cities driven by government initiatives has not advanced the degree of digitization observed in inclusive finance spearheaded by the Ant Group. At the very least, there is no statistically significant correlation between the two. Hence, while the Chinese government-led smart city construction also involves digitization, this digitization is not aimed at facilitating the expansion of large private capital.

- (2)

- Smart city construction in China directly affects rural residents and marginalized groups and seeks to promote digital development in grassroots governments. In recent years, the most significant digital transformation undergone by Chinese society is the continual reduction of the urban–rural gap in infrastructure development, such as internet access [8]. However, compared to the results of this study, there was no significant difference in the population coverage of DIF between SCP pilot cities and non-pilot cities. These findings indicate that the objectives of the government and large private capital do not entirely align.

- (3)

- The content of smart city construction does not include the monetary fund business, credit business, insurance business, investment business, and credit services of the digital finance industry. However, the results of this study show that the depth of DIF usage of these businesses in SCP pilot cities has significantly increased compared to non-SCP pilot cities. The possible reason for this is that large private capital utilized SCP to develop DIF. The acquisition of DIF services entails significant technical complexity, where users’ knowledge base, financial awareness, and digital literacy play a pivotal role. These elements serve as critical gateways for accessing digital financial resources [48,49]. Additionally, the development of smart cities creates a favorable environment for promoting the digital literacy of residents, either directly or indirectly [50,51]. Therefore, under the influence of the market economy, SCP promotes the development of DIF indirectly, especially in increasing its depth of use.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Shkarlet, S.; Dubyna, M.; Zhuk, O. Determinants of the financial services market functioning in the era of the informational economy development. Balt. J. Econ. Stud. 2018, 4, 349–357. [Google Scholar] [CrossRef]

- Pazarbasioglu, C.; Mora, A.G.; Uttamchandani, M.; Natarajan, H.; Feyen, E.; Saal, M. Digital Financial Services; World Bank: Washitington, DC, USA, 2020; pp. 1–54. Available online: https://pubdocs.worldbank.org/en/230281588169110691/Digital-Financial-Services.pdf (accessed on 10 March 2023).

- Durai, T.; Stella, G. Digital Finance and its Impact on Financial Inclusion. J. Emerg. Technol. Innov. Res. 2019, 6, 122–127. [Google Scholar]

- Situ, P. Microfinance in China and Development Opportunities. Consultant Report, October, German Technical Cooperation (GTZ). 2003. Available online: https://www.findevgateway.org/sites/default/files/publications/files/mfg-en-paper-microfinance-in-china-and-development-opportunities-oct-2003.pdf (accessed on 15 March 2023).

- Yeung, G. Chinese state-owned commercial banks in reform: Inefficient and yet credible and functional? J. Chin. Gov. 2021, 6, 198–231. [Google Scholar] [CrossRef]

- Boiarynova, K.; Popelo, O.; Tulchynska, S.; Gritsenko, S.; Prikhno, I. Conceptual Foundations of Evaluation and Forecasting of Innovative Development of Regions. Period. Polytech. Soc. Manag. Sci. 2022, 30, 167–174. [Google Scholar] [CrossRef]

- Gruin, J.; Knaack, P. Not just another shadow bank: Chinese authoritarian capitalism and the ‘developmental’ promise of digital financial innovation. New Political Econ. 2020, 25, 370–387. [Google Scholar] [CrossRef]

- China Internet Network Information Center [CNNIC]. The 49th Statistical Report on China’s Internet Development. 2022. Available online: https://www.cnnic.com.cn/IDR/ReportDownloads/202204/P020220424336135612575.pdf (accessed on 15 March 2023).

- Chang, S.E.; Luo, H.L.; Chen, Y. Blockchain-enabled trade finance innovation: A potential paradigm shift on using letter of credit. Sustainability 2019, 12, 188. [Google Scholar] [CrossRef]

- Perzanowski, A.; Schultz, J. The End of Ownership: Personal Property in the Digital Economy; MIT Press: Cambridge, MA, USA, 2016. [Google Scholar]

- Anttiroiko, A.V.; Valkama, P.; Bailey, S.J. Smart cities in the new service economy: Building platforms for smart services. AI Soc. 2014, 29, 323–334. [Google Scholar] [CrossRef]

- Bagloee, S.A.; Heshmati, M.; Dia, H.; Ghaderi, H.; Pettit, C.; Asadi, M. Blockchain: The operating system of smart cities. Cities 2021, 112, 103104. [Google Scholar] [CrossRef]

- The State Council of the People’s Republic of China. Xi Jinping Presided over the 38th Collective Study of the Political Bureau of the CPC Central Committee and Delivered an Important Speech. 30 April 2022. Available online: http://www.gov.cn/xinwen/2022-04/30/content_5688268.htm (accessed on 20 May 2023).

- Lin, C.S. State, capital, and space in China in an age of volatile globalization. Environ. Plan. A 2000, 32, 455–471. [Google Scholar] [CrossRef]

- Zhao, Z.J.; Su, G.; Li, D. The rise of public-private partnerships in China. J. Chin. Gov. 2018, 3, 158–176. [Google Scholar] [CrossRef]

- Liu, Z.; Guo, J.E.; Wang, S.; Liu, H. Government incentive strategies and private capital participation in China’s Shale gas development. Appl. Econ. 2018, 50, 51–64. [Google Scholar] [CrossRef]

- Arora, R.U. Financial sector development and smart cities: The Indian case. Sustain. Cities Soc. 2018, 42, 52–58. [Google Scholar] [CrossRef]

- Visvizi, A.; Lytras, M.D.; Damiani, E.; Mathkour, H. Policy making for smart cities: Innovation and social inclusive economic growth for sustainability. J. Sci. Technol. Policy Manag. 2018, 9, 126–133. [Google Scholar] [CrossRef]

- Papa, C.; Rossi, N. Smart Cities and Sustainable Finance. Eur. J. Islam. Financ. 2022, 9, 18–26. [Google Scholar]

- Langley, P.; Leyshon, A. Platform capitalism: The intermediation and capitalization of digital economic circulation. Financ. Soc. 2017, 3, 11–31. [Google Scholar] [CrossRef]

- Chen, B.; Zhu, H. Has the Digital Economy Changed the Urban Network Structure in China?—Based on the Analysis of China’s Top 500 New Economy Enterprises in 2020. Sustainability 2022, 14, 150. [Google Scholar] [CrossRef]

- Hu, Q.; Zheng, Y. Smart city initiatives: A comparative study of American and Chinese cities. J. Urban Aff. 2021, 43, 504–525. [Google Scholar] [CrossRef]

- Smart, E.C.; Cooperation, G.C. Comparative study of smart cities in Europe and China. In Current Chinese Economic Report Series; Springer: Berlin/Heidelberg, Germany, 2014. [Google Scholar]

- Shen, L.; Huang, Z.; Wong, S.W.; Liao, S.; Lou, Y. A holistic evaluation of smart city performance in the context of China. J. Clean. Prod. 2018, 200, 667–679. [Google Scholar] [CrossRef]

- Yu, W.; Xu, C. Developing smart cities in China: An empirical analysis. Int. J. Public Adm. Digit. Age (IJPADA) 2018, 5, 76–91. [Google Scholar] [CrossRef]

- Lardy, N. Markets over Mao: The Rise of Private Business in China; Columbia University Press: New York, NY, USA, 2014. [Google Scholar]

- Ozili, P.K. Financial inclusion research around the world: A review. Forum Soc. Econ. 2021, 50, 457–479. [Google Scholar] [CrossRef]

- Allen, F.; Qian, J.Q.; Gu, X. An overview of China’s financial system. Annu. Rev. Financ. Econ. 2017, 9, 191–231. [Google Scholar] [CrossRef]

- Bakır, C.; Çoban, M. How can a seemingly weak state in the financial services industry act strong? The role of organizational policy capacity in monetary and macroprudential policy. New Perspect. Turk. 2019, 61, 71–96. [Google Scholar] [CrossRef]

- Tkachuk, I.; Kobelia, M.; Popelo, O.; Zhavoronok, A.; Vinnychuk, O. Modelling financial influence of political and oligarchic interests of governed-sponsored enterprises on the creation and implementation of the financial policy in the state. J. Hyg. Eng. Des. 2023, 42, 271–279. [Google Scholar]

- Shen, Q.; Wu, R.; Pan, Y.; Feng, Y. The effectiveness of smart city policy on pollution reduction in China: New evidence from a quasi-natural experiment. Environ. Sci. Pollut. Res. 2023, 30, 52841–52857. [Google Scholar] [CrossRef]

- Institute of Digital Finance at Peking University. Peking University Digital Financial Inclusion Index (2011–2020). April 2021. Available online: http://nsd.pku.edu.cn/docs/20221017131046905230.pdf (accessed on 22 May 2023).

- Ji, Y.; Shi, L.; Zhang, S. Digital finance and corporate bankruptcy risk: Evidence from China. Pac.-Basin Financ. J. 2022, 72, 101731. [Google Scholar] [CrossRef]

- Lv, P.; Xiong, H. Can FinTech improve corporate investment efficiency? Evidence from China. Res. Int. Bus. Financ. 2022, 60, 101571. [Google Scholar] [CrossRef]

- Ahmad, M.; Majeed, A.; Khan, M.A.; Sohaib, M.; Shehzad, K. Digital financial inclusion and economic growth: Provincial data analysis of China. China Econ. J. 2021, 14, 291–310. [Google Scholar] [CrossRef]

- Chen, M. Research on Threshold Effect of Digital Inclusive Finance and Regional Urban-rural Income Gap. Front. Econ. Manag. 2021, 2, 255–262. [Google Scholar]

- Ant Group. 2023. Available online: https://www.antgroup.com/#company-profile (accessed on 15 January 2023).

- MOHURD (Ministry of Housing and Urban-Rural Development). A Notice on Conducting National Pilot Smart Cities [Guan Yu Kai Zhan Guo Jia ZhiHui Cheng Shi Shi Dian Gong Zuo De Tong Zhi]. 2012. Available online: www.mohurd.gov.cn/wjfb/201212/t20121204_212182.html (accessed on 15 January 2023).

- Abadie, A. Semiparametric difference-in-differences estimators. Rev. Econ. Stud. 2005, 72, 1–19. [Google Scholar] [CrossRef]

- Athey, S.; Imbens, G.W. The state of applied econometrics: Causality and policy evaluation. J. Econ. Perspect. 2017, 31, 3–32. [Google Scholar] [CrossRef]

- PKU-DFIIC. The Peking University Digital Financial Inclusion Index of China (2011–2020) [PDF]. Institute of Digital Finance Peking University. 2021. Available online: https://idf.pku.edu.cn/docs/20210421101507614920.pdf (accessed on 18 March 2023). (In Chinese).

- Bertrand, M.; Mullainathan, S. Pyramids. J. Eur. Econ. Assoc. 2003, 1, 478–483. [Google Scholar] [CrossRef]

- Beck, T.; Levine, R.; Levkov, A. Big Bad Banks? The Winners and Losers from Bank Deregulation in the United States. J. Financ. 2010, 65, 1637–1667. [Google Scholar] [CrossRef]

- Moser, P.; Voena, A. Compulsory Licensing: Evidence from the Trading with the Enemy Act. Am. Econ. Rev. 2012, 102, 396–427. [Google Scholar] [CrossRef]

- Blundell, R.; Dias, M.C. Evaluation methods for non-experimental data. Fisc. Stud. 2000, 21, 427–468. [Google Scholar] [CrossRef]

- Heyman, F.; Sjöholm, F.; Tingvall, P.G. Is there really a foreign ownership wage premium? Evidence from matched employer-employee data. J. Int. Econ. 2007, 73, 355–376. [Google Scholar] [CrossRef]

- Zenios, C.V.; Zenios, S.A.; Agathocleous, K.; Soteriou, A.C. Benchmarks of the efficiency of bank branches. Interfaces 1999, 29, 37–51. [Google Scholar] [CrossRef]

- Poon, W.C. Users’ adoption of e-banking services: The Malaysian perspective. J. Bus. Ind. Mark. 2008, 23, 59–69. [Google Scholar] [CrossRef]

- Mohammadyari, S.; Singh, H. Understanding the effect of e-learning on individual performance: The role of digital literacy. Comput. Educ. 2015, 82, 11–25. [Google Scholar] [CrossRef]

- Kummitha, R.K.R.; Crutzen, N. How do we understand smart cities? An evolutionary perspective. Cities 2017, 67, 43–52. [Google Scholar] [CrossRef]

- OECD. Smart Cities and Inclusive Growth: Building on the Outcomes of the 1st OECD Roundtable on Smart Cities and Inclusive Growth. 2020. Available online: https://www.oecd.org/cfe/cities/OECD_Policy_Paper_Smart_Cities_and_Inclusive_Growth.pdf (accessed on 15 January 2023).

- Zygiaris, S. Smart city reference model: Assisting planners to conceptualize the building of smart city innovation ecosystems. J. Knowl. Econ. 2013, 4, 217–231. [Google Scholar] [CrossRef]

- Charnock, G. Challenging new state spatialities: The open Marxism of Henri Lefebvre. Antipode 2010, 42, 1279–1303. [Google Scholar] [CrossRef]

- Harvey, D. The political economy of public space. In The Politics of Public Space; Routledge: Abingdon, UK, 2013; pp. 23–188. [Google Scholar]

- Harvey, D. Neoliberalism and the City. Stud. Soc. Justice 2007, 1, 2–13. [Google Scholar] [CrossRef]

- Kitchin, R.; Cardullo, P.; Di Feliciantonio, C. Citizenship, justice, and the right to the smart city. In The Right to the Smart City; Emerald Publishing Limited: Bingley, UK, 2019; pp. 1–24. [Google Scholar] [CrossRef]

| First-Level Dimension | Second-Level Dimension | Specific Indicators | |

|---|---|---|---|

| Coverage | Account coverage | Number of Alipay accounts per 10,000 people | |

| Proportion of Alipay users with linked bank cards | |||

| Average number of bank cards linked to each Alipay account | |||

| Usage depth | Payment service | Number of payments per capita | |

| Per capita payment amount | |||

| active users to the total active users per year | |||

| Monetary Fund Business | Number of Yu’e Bao purchases per capita | ||

| Amount of Yu’e Bao purchased per capita | |||

| Number of Yu’e Bao purchasers per 10,000 Alipay users | |||

| Credit business | Personal consumption loans | Number of internet consumption loan users per 10,000 Alipay adult users | |

| Number of loans per capita | |||

| Loan amount per capita | |||

| Small and micro-business loans | Number of internet small & micro-business loan users per 10,000 Alipay adult users | ||

| Average number of loans per small and micro-business | |||

| Average loan amount for small and micro-businesses | |||

| Insurance business | Number of insured users per 10,000 Alipay users | ||

| Number of insurance policies per capita | |||

| Insurance amount per capita | |||

| Investment Business | Alipay users in online investment and wealth management per 10,000 people | ||

| Number of investments per capita | |||

| Per capita investment amount | |||

| Credit services | Per capita call times of natural person credit | ||

| Number of credit-based service users per 10,000 Alipay users | |||

| Degree of digitization | Mobile | Proportion of mobile payment transactions | |

| Proportion of mobile payment amount | |||

| Affordability | Average loan interest rate for small and micro-businesses | ||

| Average personal loan interest rate | |||

| Credit | Proportion of Huabei payments | ||

| Proportion of Huabei payment amount | |||

| Proportion of Sesame Credit’s deposit-free transactions | |||

| Proportion of Sesame Credit’s deposit-free amount | |||

| Convenience | Proportion of user QR code payments | ||

| Proportion of the amount paid by user QR code | |||

| Variable | Observations | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Digital Financial Inclusion Index | 1648 | 151.634 | 61.000 | 17.020 | 284.910 |

| Logarithm of GDP per capita (USD) | 1648 | 8.642 | 0.668 | 6.266 | 13.765 |

| Proportion of GDP from the secondary industry (%) | 1648 | 47.973 | 11.102 | 13.570 | 89.340 |

| Proportion of GDP from the tertiary industry (%) | 1648 | 42.441 | 101.525 | 10.150 | 80.980 |

| Human capital level (% of the population with a certain level of education or training) | 1648 | 18.829 | 6.960 | 0.523 | 62.303 |

| Logarithm of population density (person/km2) | 1648 | 7.988 | 0.718 | 5.733 | 9.397 |

| Proportion of fiscal expenditure on science and technology (% of total government spending) | 1648 | 0.885 | 1.298 | 0.002 | 20.414 |

| Logarithm of telecom business volume per capita (USD) | 1648 | 4.622 | 0.830 | 0.524 | 9.688 |

| The average number of mobile phones per capita in the city | 1648 | 0.914 | 0.433 | 0.111 | 3.303 |

| The number of Internet connected devices per capita in the city | 1648 | 0.185 | 0.144 | 0.035 | 1.489 |

| Logarithm of per capita salary of employed workers (USD) | 1648 | 6.379 | 0.872 | 4.262 | 9.785 |

| Logarithm of per capita foreign direct investment (USD) | 1648 | 5.189 | 2.056 | −1.820 | 9.403 |

| (1) | (2) | |

|---|---|---|

| DID | 3.0482 ** | 2.6283 ** |

| (1.1979) | (1.1763) | |

| Control variables | Uncontrolled | Controlled |

| Year fixed effects | Controlled | Controlled |

| City fixed effects | Controlled | Controlled |

| Time trend term × Treatment group dummy variable | Controlled | Controlled |

| Obs | 1648 | 1648 |

| R2 | 0.9941 | 0.9944 |

| (1) | (2) | |

|---|---|---|

| DID | 1.4277 *** | 1.0288 ** |

| (0.5002) | (0.4962) | |

| Control variables | Uncontrolled | Controlled |

| Year fixed effects | Controlled | Controlled |

| City fixed effects | Controlled | Controlled |

| Obs | 1572 | 1572 |

| R2 | 0.9946 | 0.9948 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Coverage | Depth of Use | Degree of Digitization | ||||

| DID | 0.1914 | −0.2474 | 2.3111 *** | 2.2925 *** | 3.9309 * | 4.084 * |

| (0.4692) | (0.4443) | (0.8754) | (0.8669) | (2.2213) | (2.1819) | |

| Control variables | Uncontrolled | Controlled | Uncontrolled | Controlled | Uncontrolled | Controlled |

| Year fixed effects | Controlled | Controlled | Controlled | Controlled | Controlled | Controlled |

| City fixed effects | Controlled | Controlled | Controlled | Controlled | Controlled | Controlled |

| Obs | 1648 | 1648 | 1648 | 1648 | 1648 | 1648 |

| R2 | 0.9943 | 0.9949 | 0.9867 | 0.9871 | 0.9285 | 0.9300 |

| Weight Matrix Type | (1) | (2) | (3) |

|---|---|---|---|

| Geographical Distance | Economic | Proximity | |

| DID | 2.0766 ** | 1.5206 *** | 5.8274 *** |

| (0.9574) | (0.6243) | (2.2153) | |

| Control variables | Controlled | Controlled | Controlled |

| Fixed effects | Controlled | Controlled | Controlled |

| ρ | 1.3047 *** | 0.8926 *** | 0.6362 *** |

| (0.0498) | (0.0127) | (0.0505) | |

| 28.3547 *** | 21.7206 *** | 130.8168 *** | |

| (3.5165) | (2.4903) | (29.8918) | |

| Obs | 1648 | 1648 | 1648 |

| R2 | 0.0355 | 0.9429 | 0.0523 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lin, J.; Chen, X.; Yan, G. How Smart City Construction Affects Digital Inclusive Finance in China: From the Perspective of the Relationship between Government and Large Private Capital. Sustainability 2023, 15, 9035. https://doi.org/10.3390/su15119035

Lin J, Chen X, Yan G. How Smart City Construction Affects Digital Inclusive Finance in China: From the Perspective of the Relationship between Government and Large Private Capital. Sustainability. 2023; 15(11):9035. https://doi.org/10.3390/su15119035

Chicago/Turabian StyleLin, Jinlong, Xiaoxiao Chen, and Guiquan Yan. 2023. "How Smart City Construction Affects Digital Inclusive Finance in China: From the Perspective of the Relationship between Government and Large Private Capital" Sustainability 15, no. 11: 9035. https://doi.org/10.3390/su15119035

APA StyleLin, J., Chen, X., & Yan, G. (2023). How Smart City Construction Affects Digital Inclusive Finance in China: From the Perspective of the Relationship between Government and Large Private Capital. Sustainability, 15(11), 9035. https://doi.org/10.3390/su15119035