Political and Socioeconomic Factors That Determine the Financial Outcome of Successful Green Innovation

Abstract

1. Introduction

2. Literature Review

2.1. Financial Benefits of Corporate Environmentalism

2.2. Barriers of Green Technology-Related Innovation

2.3. Factors Explaining the Differences in Sustainability Efforts

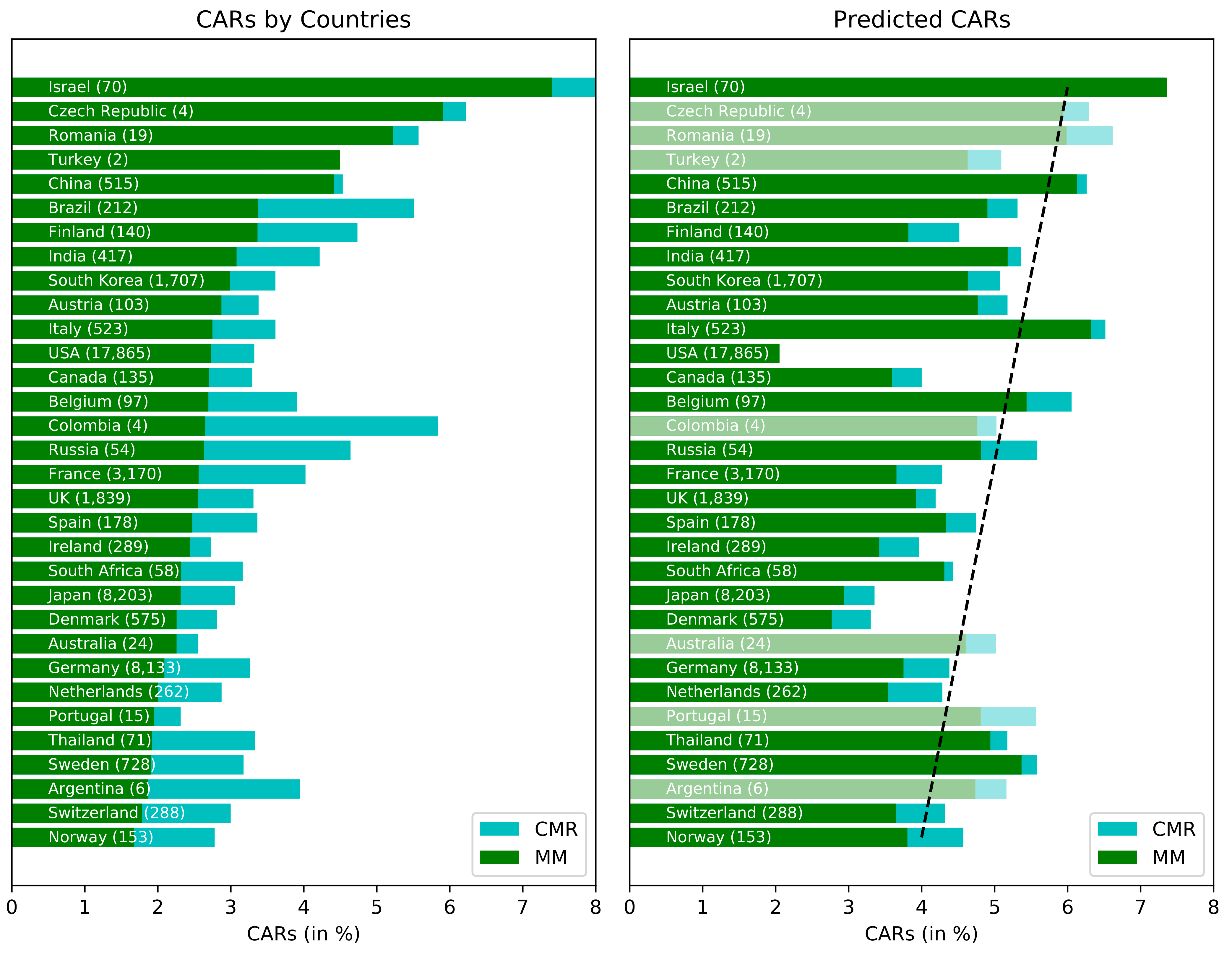

3. Materials and Methods

3.1. Construction of Dependent Variable

3.2. Description of Independent Variables

3.3. Exploratory Factor Analysis

3.4. Modeling and Regression Analysis

4. Results

4.1. Descriptive Statistics

4.2. Exploratory Factor Analysis

4.3. Regression Analysis

5. Discussion

6. Conclusions

6.1. Summary and Key Findings

6.2. Significance of This Work

6.3. Implications for Policymakers

6.4. Implications for Company Leaders

6.5. Research Limitations

6.6. Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| CAR | Cumulative abnormal returns |

| CMR | Constant mean return model (for event study analysis) |

| MM | Market model (for event study analysis) |

| R&D | Research and development |

| SMEs | Small and medium-sized enterprises |

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Mean | Std | Curtosis | Skewness | q.00 | q.25 | q.50 | q.75 | q1.0 | VIF | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| dependent | 1 | CAR (CMR) | 0.03 | 0.04 | 1737.75 | 20.63 | 0.00 | 0.00 | 0.00 | 0.00 | 3.75 | |

| 2 | CAR (MM) | 0.03 | 0.03 | 3329.71 | 32.45 | 0.00 | 0.00 | 0.00 | 0.00 | 3.82 | ||

| 3 | CAR (CMR, norm) | 0.37 | 0.17 | 1.06 | 0.72 | 0.00 | 0.03 | 0.04 | 0.05 | 1.36 | ||

| 4 | CAR (MM, norm) | 0.27 | 0.14 | 2.15 | 1.03 | 0.01 | 0.02 | 0.02 | 0.03 | 1.31 | ||

| independent | 1 | Oil price | 91.84 | 25.24 | −1.32 | −0.53 | 53.05 | 53.05 | 53.05 | 53.05 | 118.71 | 272.05 |

| 2 | Coal price | 91.45 | 23.64 | −0.81 | 0.30 | 56.79 | 56.79 | 56.79 | 56.79 | 136.21 | 65.34 | |

| 3 | Gas price | 10.77 | 3.28 | −0.71 | 0.63 | 2.76 | 3.71 | 6.53 | 6.53 | 16.75 | 346.49 | |

| 4 | Stock price | 86.62 | 155.93 | 15.64 | 3.96 | 2.03 | 2.91 | 3.26 | 3.58 | 938.13 | 2.21 | |

| 5 | Market cap | 1.51 | 1.31 | 1.76 | ||||||||

| 6 | EBIT | 1.37 | 1.38 | 2.06 | ||||||||

| 7 | GDP | 458.59 | ||||||||||

| 8 | GDP per capita | 16.84 | ||||||||||

| 9 | CTGCI | 2.85 | 0.42 | −0.98 | 0.73 | 2.04 | 2.38 | 2.38 | 2.38 | 3.60 | 35.81 | |

| 10 | WWGI (VOI) | 1.23 | 0.16 | −1.51 | −0.07 | 0.99 | 0.99 | 0.99 | 0.99 | 1.45 | 145.73 | |

| 11 | WWGI (STA) | 0.80 | 0.24 | 0.54 | −1.13 | 0.11 | 0.11 | 0.11 | 0.11 | 1.34 | 40.61 | |

| 12 | WWGI (GOV) | 1.59 | 0.14 | −1.25 | 0.10 | 1.34 | 1.34 | 1.34 | 1.34 | 1.81 | 42.93 | |

| 13 | WWGI (REG) | 1.37 | 0.26 | −1.58 | 0.29 | 1.02 | 1.02 | 1.02 | 1.02 | 1.86 | 409.21 | |

| 14 | WWGI (LAW) | 1.57 | 0.17 | −1.10 | 0.09 | 1.29 | 1.29 | 1.29 | 1.29 | 1.89 | 201.23 | |

| 15 | WWGI (COR) | 1.65 | 0.17 | −0.64 | −0.57 | 1.31 | 1.31 | 1.31 | 1.31 | 2.07 | 42.54 | |

| 16 | ADRI | 2.79 | 1.47 | −1.58 | −0.21 | 0.00 | 1.00 | 1.00 | 1.00 | 5.00 | ||

| 17 | NCDI (IDV) | 47.59 | 12.42 | −1.28 | 0.26 | 11.00 | 35.00 | 35.00 | 35.00 | 68.00 | ||

| 18 | NCDI (POW) | 61.18 | 13.34 | −0.83 | 0.22 | 46.00 | 46.00 | 46.00 | 46.00 | 90.00 | ||

| 19 | NCDI (MAS) | 73.65 | 18.77 | −1.22 | −0.14 | 43.00 | 43.00 | 43.00 | 43.00 | 95.00 | ||

| 20 | NCDI (UNC) | 76.51 | 17.06 | 0.05 | −0.90 | 35.00 | 35.00 | 35.00 | 35.00 | 94.00 | ||

| 21 | NCDI (LTO) | 79.21 | 12.01 | 0.69 | −1.40 | 21.00 | 36.00 | 51.00 | 51.00 | 88.00 | ||

| 22 | NCDI (IND) | 44.38 | 7.75 | 5.14 | 2.49 | 40.00 | 40.00 | 40.00 | 40.00 | 71.00 | ||

| 23 | IPRI (Overall) | 7.68 | 0.23 | 0.70 | -0.11 | 7.18 | 7.18 | 7.18 | 7.18 | 8.30 | 676.40 | |

| 24 | IPRI (Legal) | 7.73 | 0.36 | -0.81 | -0.36 | 6.97 | 6.97 | 6.97 | 6.97 | 8.40 | 101.40 | |

| 25 | IPRI (Physical) | 7.10 | 0.28 | 0.91 | 0.33 | 6.40 | 6.40 | 6.40 | 6.40 | 7.88 | 175.03 | |

| 26 | IPRI (Intellectual) | 8.20 | 0.22 | −0.10 | 0.28 | 7.80 | 7.80 | 7.80 | 7.80 | 8.74 | 168.47 | |

| 27 | IPRI (RuleOfLaw) | 7.99 | 0.32 | −1.43 | 0.00 | 7.50 | 7.50 | 7.50 | 7.50 | 8.61 | 97.40 | |

| 28 | IPRI (Pol.Stability) | 6.64 | 0.38 | 0.00 | −1.04 | 5.60 | 5.60 | 5.60 | 5.60 | 7.30 | 22.08 | |

| 29 | IPRI (Corr.Contr.) | 8.15 | 0.37 | −0.53 | −0.63 | 7.30 | 7.30 | 7.30 | 7.30 | 9.10 | 55.36 | |

| 30 | OECD (EPS) | 3.12 | 0.43 | 3.32 | −1.56 | 1.73 | 1.73 | 1.73 | 1.73 | 3.83 | inf | |

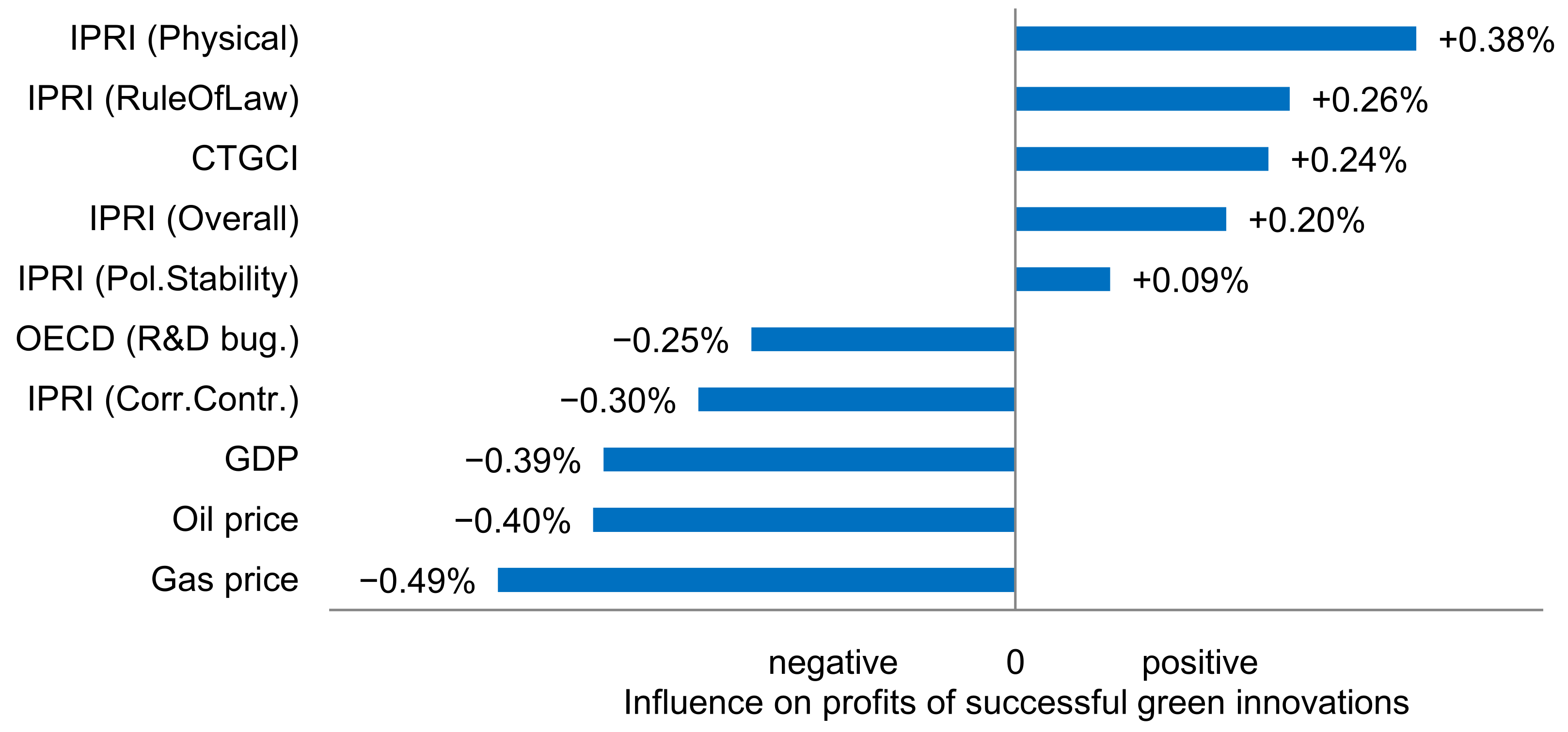

| 31 | OECD (RD bud.) | 2.81 | 0.49 | 0.25 | −1.07 | 1.58 | 1.58 | 1.58 | 1.58 | 3.37 | 735.45 | |

| 32 | OECD (Pub. RD) | 3.12 | 0.43 | 3.32 | −1.56 | 1.73 | 1.73 | 1.73 | 1.73 | 3.83 | inf | |

| Extracted Factors | Factor 1 (Cultural) | Factor 2 (Stability) | Factor 3 (Investor) | Factor 4 (Economic) | Factor 5 (Policy) | Factor 6 (Firm) | Factor 7 (Gover.) | ||

|---|---|---|---|---|---|---|---|---|---|

| Independent Variable | 1 | Oil price | −12.42 | −16.12 | −22.47 | 86.11 | 14.65 | 4.99 | −1.49 |

| 2 | Coal price | −60.71 | −9.64 | −7.19 | 69.73 | −7.09 | 5.53 | 5.48 | |

| 3 | Gas price | −72.09 | 3.52 | 3.87 | 51.34 | 35.44 | −0.78 | −4.06 | |

| 4 | Stock price | 46.81 | 26.79 | −44.01 | −13.45 | 15.66 | 8.39 | 10.53 | |

| 5 | Market cap | 3.79 | 14.24 | 9.11 | 00.02 | 28.94 | 65.70 | 24.02 | |

| 6 | EBIT | 32.92 | −4.95 | 7.25 | −11.80 | 37.08 | 58.68 | 22.49 | |

| 7 | GDP | −65.39 | 55.10 | 2.28 | −09.26 | 20.66 | 5.34 | −12.92 | |

| 8 | GDP per capita | 22.55 | −5.17 | −51.01 | 62.34 | −1.23 | 2.81 | −9.96 | |

| 9 | CTGCI | 66.36 | 45.23 | −2.31 | −02.69 | −18.69 | −6.50 | 17.01 | |

| 10 | WWGI (VOI) | 88.93 | 21.56 | −35.57 | 09.18 | 4.32 | 0.01 | −5.34 | |

| 11 | WWGI (STA) | −59.02 | 68.82 | −3.65 | 18.73 | 4.71 | −0.87 | −6.38 | |

| 12 | WWGI (GOV) | 7.88 | 66.62 | 35.69 | −37.50 | 24.48 | 3.31 | −27.15 | |

| 13 | WWGI (REG) | 87.01 | 43.15 | 4.24 | 04.11 | −3.83 | 5.20 | −17.55 | |

| 14 | WWGI (LAW) | 78.22 | 47.42 | 11.53 | −08.45 | 16.85 | 2.12 | −21.67 | |

| 15 | WWGI (COR) | 44.98 | 77.11 | −2.54 | 20.20 | 18.91 | 2.46 | −24.28 | |

| 16 | ADRI | −52.57 | −45.08 | 64.90 | 11.69 | −6.68 | 13.51 | −20.58 | |

| 17 | NCDI (IDV) | −57.59 | −72.50 | −1.26 | −22.09 | 15.02 | −11.64 | 13.24 | |

| 18 | NCDI (POW) | 94.09 | −28.93 | 7.34 | 8.90 | −11.05 | 1.63 | 0.70 | |

| 19 | NCDI (MAS) | −76.62 | 47.03 | 28.35 | 11.92 | −3.27 | 13.58 | −19.68 | |

| 20 | NCDI (UNC) | −88.51 | −17.93 | −21.29 | −23.19 | 18.56 | −12.35 | 13.45 | |

| 21 | NCDI (LTO) | −61.51 | 69.44 | −31.37 | −7.33 | 10.05 | −1.72 | 2.72 | |

| 22 | NCDI (IND) | 40.80 | −53.01 | 63.04 | 21.94 | −19.34 | 14.33 | −19.73 | |

| 23 | IPRI (Overall) | −4.46 | 82.34 | 44.26 | 20.29 | −13.28 | −10.09 | 25.41 | |

| 24 | IPRI (Legal) | 39.37 | 83.77 | 3.14 | 22.89 | −4.18 | −7.90 | 11.94 | |

| 25 | IPRI (Physical) | −18.49 | 50.41 | 53.33 | 21.01 | −29.48 | −5.79 | 35.84 | |

| 26 | IPRI (Intellectual) | −45.52 | 59.03 | 51.09 | 0.72 | −4.89 | −6.42 | 7.67 | |

| 27 | IPRI (RuleOfLaw) | 86.82 | 30.99 | −2.48 | 8.90 | −28.82 | −1.12 | 16.12 | |

| 28 | IPRI (Pol.Stability) | −53.28 | 72.41 | −16.56 | −11.61 | −7.30 | −4.38 | 7.80 | |

| 29 | IPRI (Corr.Contr.) | 57.78 | 67.90 | 11.21 | 4.05 | 33.35 | −14.91 | 1.65 | |

| 30 | OECD (EPS) | 47.00 | −35.90 | 32.89 | 12.58 | 63.25 | −28.75 | 12.07 | |

| 31 | OECD (RD bud.) | −72.35 | 60.00 | −23.77 | −13.54 | 18.29 | −1.62 | −3.97 | |

| 32 | OECD (Pub. RD) | 47.00 | −35.90 | 32.89 | 12.58 | 63.25 | −28.75 | 12.07 | |

| Model Nr. | (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|---|

| Regression Model | Linear | Linear | Truncated | Truncated | CRCH | CRCH | |

| CAR Estimation Model | CMR | MM | CMR | MM | CMR | MM | |

| 1 | Oil price | −0.22 *** (0.05) | −0.48 *** (0.04) | −0.24 *** (0.06) | −0.58 *** (0.05) | −0.17 ** (0.05) | −0.40 *** (0.04) |

| 2 | Coal price | 0.03 (0.04) | −0.13 *** (0.03) | 0.04 (0.05) | −0.16 *** (0.04) | 0.07 (0.04) | −0.08 ** (0.03) |

| 3 | Gas price | −0.48 *** (0.05) | −0.55 *** (0.03) | −0.53 *** (0.05) | −0.67 *** (0.04) | −0.43 *** (0.05) | −0.49 *** (0.03) |

| 4 | Stock price | −0.18 *** (0.02) | −0.51 *** (0.02) | −0.21*** (0.03) | −0.62 *** (0.02) | −0.17 *** (0.02) | −0.48 *** (0.02) |

| 5 | Market cap | −1.66 *** (0.17) | −1.97 *** (0.12) | −1.88 *** (0.19) | −2.45 *** (0.15) | −1.51 *** (0.17) | −1.75 *** (0.12) |

| 6 | EBIT | −1.57 *** (0.15) | −1.89 *** (0.11) | −1.77 *** (0.17) | −2.34 *** (0.14) | −1.44 *** (0.16) | −1.69 *** (0.11) |

| 7 | GDP | −0.60 *** () | −0.42 *** () | −0.67 *** () | −0.51 *** () | −0.57 *** () | −0.39 *** () |

| 8 | GDP per capita | ** () | −0.18 *** () | 0.02 *** () | −0.21 *** () | 0.03 *** () | −0.16 *** () |

| 9 | CTGCI | 0.47 *** (0.02) | 0.27 *** (0.02) | 0.53 *** (0.03) | 0.33 *** (0.02) | 0.44 *** (0.02) | 0.24 *** (0.02) |

| 10 | WWGI (VOI) | −0.03 *** () | −0.17 *** () | −0.02 *** () | −0.21 *** () | −0.03 *** () | −0.18 *** () |

| 11 | WWGI (STA) | −0.22 *** () | −0.16 *** () | −0.24 *** () | −0.18 *** () | −0.20 *** () | −0.14 *** () |

| 12 | WWGI (GOV) | −0.0084 *** (0.01) | -0.38 *** (0.01) | −0.95 *** (0.02) | −0.46 *** (0.01) | −0.84 *** (0.01) | −0.38 *** () |

| 13 | WWGI (REG) | −0.32 *** () | −0.14 *** () | −0.36 *** () | −0.17 *** () | −0.32 *** () | −0.16 *** () |

| 14 | WWGI (LAW) | −0.57 *** () | −0.34 *** () | −0.63 *** () | −0.40 *** () | −0.57 *** () | −0.34 *** () |

| 15 | WWGI (COR) | −0.64 *** () | −0.47 *** () | −0.71 *** () | −0.56 *** () | −0.62 *** () | −0.45 *** () |

| 16 | ADRI | −0.55 *** () | −0.04 *** () | −0.62 *** () | −0.06 *** () | −0.52 *** () | −0.01 *** () |

| 17 | NCDI (IDV) | 0.34 *** (0.02) | 0.21 *** (0.01) | 0.38 *** (0.02) | 0.25 *** (0.02) | 0.32 *** (0.02) | 0.20 *** (0.01) |

| 18 | NCDI (POW) | 0.14 *** (0.01) | 0.10 *** () | 0.15 *** (0.01) | 0.13 *** (0.01) | 0.12 *** (0.01) | 0.09 *** () |

| 19 | NCDI (MAS) | −0.64 *** () | −0.26 *** () | −0.71 *** () | −0.31 *** () | −0.60 *** () | −0.22 *** () |

| 20 | NCDI (UNC) | 0.28 *** (0.02) | 0.09 *** (0.01) | 0.31 *** (0.02) | 0.11 *** (0.02) | 0.27 *** (0.02) | 0.09 *** (0.01) |

| 21 | NCDI (LTO) | −0.09 *** () | −0.20 *** () | −0.09 *** () | −0.24 *** () | −0.07 *** () | −0.19 *** () |

| 22 | NCDI (IND) | −0.38 *** () | 0.06 *** () | −0.43 *** (0.01) | 0.07 *** (0.01) | −0.37 *** () | 0.07 *** () |

| 23 | IPRI (Overall) | 0.35 *** (0.08) | 0.21 *** (0.06) | 0.39 *** (0.09) | 0.26 *** (0.07) | 0.34 *** (0.08) | 0.20 *** (0.05) |

| 24 | IPRI (Legal) | 0.19 *** (0.05) | (0.03) | 0.21 *** (0.05) | 0.02 (0.04) | 0.18 *** (0.05) | (0.03) |

| 25 | IPRI (Physical) | 0.57 *** (0.09) | 0.38 *** (0.06) | 0.63 *** (0.10) | 0.47 *** (0.08) | 0.56 *** (0.08) | 0.38 *** (0.06) |

| 26 | IPRI (Intellectual) | 0.01 (0.04) | 0.15 *** (0.03) | 0.01 (0.04) | 0.19 *** (0.03) | 0.01 (0.04) | 0.14 *** (0.02) |

| 27 | IPRI (RuleOfLaw) | 0.48 *** (0.03) | 0.28 *** (0.02) | 0.54 *** (0.03) | 0.35 *** (0.02) | 0.46 *** (0.03) | 0.26 *** (0.02) |

| 28 | IPRI (Pol.Stability) | 0.18 *** () | 0.11 *** () | 0.20 *** () | 0.14 *** () | 0.18 *** () | 0.09 *** () |

| 29 | IPRI (Corr.Contr.) | −0.19 *** (0.04) | −0.30 *** (0.03) | −0.22 *** (0.05) | −0.35 *** (0.04) | −0.20 *** (0.04) | −0.30 *** (0.03) |

| 30 | OECD (EPS) | −0.02 (0.07) | −0.27 *** (0.05) | −0.03 (0.07) | −0.32 *** (0.06) | −0.05 (0.06) | −0.26 *** (0.05) |

| 31 | OECD (RD bud.) | −0.26 *** (0.01) | −0.26 *** (0.01) | −0.29 *** (0.02) | −0.32 *** (0.01) | −0.24 *** (0.01) | −0.25 *** () |

| 32 | OECD (Pub. RD) | −0.02 (0.07) | −0.27 *** (0.05) | −0.03 (0.07) | −0.32 *** (0.06) | −0.05 (0.06) | −0.26 *** (0.05) |

References

- Criscuolo, C.; Menon, C. Environmental policies and risk finance in the green sector: Cross-country evidence. Energy Policy 2015, 83, 38–56. [Google Scholar] [CrossRef]

- Orsato, R.J. When Does it Pay to be Green? In Sustainability Strategies; Springer: Berlin/Heidelberg, Germany, 2009; pp. 3–22. [Google Scholar]

- Clemens, B. Economic incentives and small firms: Does it pay to be green? J. Bus. Res. 2006, 59, 492–500. [Google Scholar] [CrossRef]

- Friedman, M. The social responsibility of business is to increase its profits. New York Times Magazine, 13 September 1970; 33–36. [Google Scholar]

- Porter, M.E.; Van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Farza, K.; Ftiti, Z.; Hlioui, Z.; Louhichi, W.; Omri, A. Does it pay to go green? The environmental innovation effect on corporate financial performance. J. Environ. Manag. 2021, 300, 113695. [Google Scholar] [CrossRef] [PubMed]

- Stefan, A.; Paul, L. Does it pay to be green? A systematic overview. Acad. Manag. Perspect. 2008, 22, 45–62. [Google Scholar] [CrossRef]

- Hoff, P. Greentech Innovation and Diffusion: A Financial Economics and Firm-Level Perspective; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2012. [Google Scholar]

- Chertow, M.R. Accelerating Commercialization of Environmental Technology in the United States: Theory and Case Studies. Ph.D. Thesis, Yale University, New Haven, CT, USA, 2000. [Google Scholar]

- Enzensberger, N.; Wietschel, M.; Rentz, O. Policy instruments fostering wind energy projects—A multi-perspective evaluation approach. Energy Policy 2002, 30, 793–801. [Google Scholar] [CrossRef]

- Samad, G.; Manzoor, R. Green growth: Important determinants. Singap. Econ. Rev. 2015, 60, 1550014. [Google Scholar] [CrossRef]

- Akomea-Frimpong, I.; Adeabah, D.; Ofosu, D.; Tenakwah, E.J. A review of studies on green finance of banks, research gaps and future directions. J. Sustain. Financ. Invest. 2021, 1–24. [Google Scholar] [CrossRef]

- D’Orazio, P.; Popoyan, L. Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies? Ecol. Econ. 2019, 160, 25–37. [Google Scholar] [CrossRef]

- Ziolo, M.; Filipiak, B.Z.; Bąk, I.; Cheba, K. How to design more sustainable financial systems: The roles of environmental, social, and governance factors in the decision-making process. Sustainability 2019, 11, 5604. [Google Scholar] [CrossRef]

- Immel, M.; Kiesel, F.; Hachenberg, B.; Schiereck, D. Green bonds: Shades of green and brown. J. Asset Manag. 2021, 22, 96–109. [Google Scholar] [CrossRef]

- Bieliński, T.; Mosionek-Schweda, M. Green bonds as a financial instrument for environmental projects funding. Unia Eur. 2018, 248, 13–21. [Google Scholar]

- Cumming, D.J.; Leboeuf, G.; Schwienbacher, A. Crowdfunding cleantech. Energy Econ. 2017, 65, 292–303. [Google Scholar] [CrossRef]

- Petruzzelli, A.M.; Natalicchio, A.; Panniello, U.; Roma, P. Understanding the crowdfunding phenomenon and its implications for sustainability. Technol. Forecast. Soc. Change 2019, 141, 138–148. [Google Scholar] [CrossRef]

- Bento, N.; Gianfrate, G.; Groppo, S.V. Do crowdfunding returns reward risk? Evidences from clean-tech projects. Technol. Forecast. Soc. Change 2019, 141, 107–116. [Google Scholar] [CrossRef]

- Gaddy, B.E.; Sivaram, V.; Jones, T.B.; Wayman, L. Venture capital and cleantech: The wrong model for energy innovation. Energy Policy 2017, 102, 385–395. [Google Scholar] [CrossRef]

- Mrkajic, B.; Murtinu, S.; Scalera, V.G. Is green the new gold? Venture capital and green entrepreneurship. Small Bus. Econ. 2019, 52, 929–950. [Google Scholar] [CrossRef]

- Tolliver, C.; Fujii, H.; Keeley, A.R.; Managi, S. Green innovation and finance in Asia. Asian Econ. Policy Rev. 2021, 16, 67–87. [Google Scholar] [CrossRef]

- Vaccarini, K.; Spigarelli, F.; Tavoletti, E. European Green Tech FDI in China: The Role of Culture; Technical Report; c.MET05: Ferrara, Italy, 2016. [Google Scholar]

- Mazzucato, M.; Semieniuk, G. Financing renewable energy: Who is financing what and why it matters. Technol. Forecast. Soc. Change 2018, 127, 8–22. [Google Scholar] [CrossRef]

- Palmquist, S.; Bask, M. Market dynamics of buyout acquisitions in the renewable energy and cleantech sectors: An event study approach. Renew. Sustain. Energy Rev. 2016, 64, 271–278. [Google Scholar] [CrossRef]

- Laurens, P.; Le Bas, C.; Schoen, A.; Lhuillery, S. Technological contribution of MNEs to the growth of energy-greentech sector in the early post-Kyoto period. Environ. Econ. Policy Stud. 2016, 18, 169–191. [Google Scholar] [CrossRef][Green Version]

- Fink, J. Phoenix, the Role of the University, and the Politics of Green-Tech. In Sustainability in America’s Cities; Springer: Berlin/Heidelberg, Germany, 2011; pp. 69–90. [Google Scholar]

- Fink, J.H. Contrasting governance learning processes of climate-leading and-lagging cities: Portland, Oregon, and Phoenix, Arizona, USA. J. Environ. Policy Plan. 2019, 21, 16–29. [Google Scholar] [CrossRef]

- Giudici, G.; Guerini, M.; Rossi-Lamastra, C. The creation of cleantech startups at the local level: The role of knowledge availability and environmental awareness. Small Bus. Econ. 2019, 52, 815–830. [Google Scholar] [CrossRef]

- Dulin, C. Improving the French GreenTech Ecosystem to Better Support GreenTech Startups. Master’s Thesis, Aalto University, Espoo, Finland, 2021. [Google Scholar]

- Çinar, S.; Yilmazer, M. Determinants of Green Technologies in Developing Countries. İşle. İktisat Çalışmaları Derg. 2021, 9, 155–167. [Google Scholar]

- Cumming, D.; Henriques, I.; Sadorsky, P. ‘Cleantech’venture capital around the world. Int. Rev. Financ. Anal. 2016, 44, 86–97. [Google Scholar] [CrossRef]

- Li, K.; Lin, B. Impact of energy technology patents in China: Evidence from a panel cointegration and error correction model. Energy Policy 2016, 89, 214–223. [Google Scholar] [CrossRef]

- Miao, C.; Fang, D.; Sun, L.; Luo, Q. Natural resources utilization efficiency under the influence of green technological innovation. Resour. Conserv. Recycl. 2017, 126, 153–161. [Google Scholar] [CrossRef]

- Liu, N.; Liu, C.; Xia, Y.; Da, B. Examining the coordination between urbanization and eco-environment using coupling and spatial analyses: A case study in China. Ecol. Indic. 2018, 93, 1163–1175. [Google Scholar] [CrossRef]

- Han, H.; Li, H.; Zhang, K. Spatial-temporal coupling analysis of the coordination between urbanization and water ecosystem in the Yangtze River Economic Belt. Int. J. Environ. Res. Public Health 2019, 16, 3757. [Google Scholar] [CrossRef]

- Ariken, M.; Zhang, F.; Chan, N.W. Coupling coordination analysis and spatio-temporal heterogeneity between urbanization and eco-environment along the Silk Road Economic Belt in China. Ecol. Indic. 2021, 121, 107014. [Google Scholar] [CrossRef]

- Russo, M.V. The emergence of sustainable industries: Building on natural capital. Strateg. Manag. J. 2003, 24, 317–331. [Google Scholar] [CrossRef]

- Dickel, P. Exploring the role of entrepreneurial orientation in clean technology ventures. Int. J. Entrep. Ventur. 2018, 10, 56–82. [Google Scholar] [CrossRef]

- Laurens, P.; Le Bas, C.; Lhuillery, S. Firm specialization in clean energy technologie: The influence of path dependence and technological diversification. Rev. Econ. Ind. 2018, 4, 73–106. [Google Scholar]

- Laurens, P.; Le Bas, C.; Lhuillery, S.; Schoen, A. The determinants of cleaner energy innovations of the world’s largest firms: The impact of firm learning and knowledge capital. Econ. Innov. New Technol. 2017, 26, 311–333. [Google Scholar] [CrossRef]

- Song, M.; Wang, S.; Zhang, H. Could environmental regulation and R&D tax incentives affect green product innovation? J. Clean. Prod. 2020, 258, 120849. [Google Scholar]

- Tödtling, F.; Trippl, M. Regional innovation policies for new path development–beyond neo-liberal and traditional systemic views. Eur. Plan. Stud. 2018, 26, 1779–1795. [Google Scholar] [CrossRef]

- Costa, J. Carrots or sticks: Which policies matter the most in sustainable resource management? Resources 2021, 10, 12. [Google Scholar] [CrossRef]

- Banerjee, S.B. Corporate environmentalism: The construct and its measurement. J. Bus. Res. 2002, 55, 177–191. [Google Scholar] [CrossRef]

- Chrun, E.; Dolšak, N.; Prakash, A. Corporate environmentalism: Motivations and mechanisms. Annu. Rev. Environ. Resour. 2016, 41, 341–362. [Google Scholar] [CrossRef]

- Karpf, A.; Mandel, A. Does It Pay to Be Green? 2017. Available online: https://ssrn.com/abstract=2923484 (accessed on 22 October 2017).

- Miller, N.; Spivey, J.; Florance, A. Does green pay off? J. Real Estate Portf. Manag. 2008, 14, 385–400. [Google Scholar] [CrossRef]

- Hart, S.L.; Ahuja, G. Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Bus. Strategy Environ. 1996, 5, 30–37. [Google Scholar] [CrossRef]

- Acemoglu, D.; Akcigit, U.; Hanley, D.; Kerr, W. Transition to clean technology. J. Polit. Econ. 2016, 124, 52–104. [Google Scholar] [CrossRef]

- Owen, R.; Brennan, G.; Lyon, F. Enabling investment for the transition to a low carbon economy: Government policy to finance early stage green innovation. Curr. Opin. Environ. Sustain. 2018, 31, 137–145. [Google Scholar] [CrossRef]

- Bithas, K. Sustainability and externalities: Is the internalization of externalities a sufficient condition for sustainability? Ecol. Econ. 2011, 70, 1703–1706. [Google Scholar] [CrossRef]

- Andreoni, J. Why free ride?: Strategies and learning in public goods experiments. J. Public Econ. 1988, 37, 291–304. [Google Scholar] [CrossRef]

- Zhang, F.; Zhang, Z.; Xue, Y.; Zhang, J.; Che, Y. Dynamic green innovation decision of the supply chain with innovating and free-riding manufacturers: Cooperation and spillover. Complexity 2020, 2020, 8937847. [Google Scholar] [CrossRef]

- De Marchi, V. Environmental innovation and R&D cooperation: Empirical evidence from Spanish manufacturing firms. Res. Policy 2012, 41, 614–623. [Google Scholar]

- Kenney, M. Venture capital investment in the greentech industries: A provocative essay. In Handbook of Research on Energy Entrepreneurship; Edward Elgar Publishing: Cheltenham, UK, 2011. [Google Scholar]

- Chapman, T. Evidence for a Speculative Bubble in the Clean Energy Sector. Ph.D. Thesis, University of Sheffield, Sheffield, UK, 2007. [Google Scholar]

- Hegeman, P.D.; Sørheim, R. Why do they do it? Corporate venture capital investments in cleantech startups. J. Clean. Prod. 2021, 294, 126315. [Google Scholar] [CrossRef]

- Polzin, F.; Egli, F.; Steffen, B.; Schmidt, T.S. How do policies mobilize private finance for renewable energy?—A systematic review with an investor perspective. Appl. Energy 2019, 236, 1249–1268. [Google Scholar] [CrossRef]

- Polzin, F. Mobilizing private finance for low-carbon innovation—A systematic review of barriers and solutions. Renew. Sustain. Energy Rev. 2017, 77, 525–535. [Google Scholar] [CrossRef]

- Portney, K.E. Local sustainability policies and programs as economic development: Is the new economic development sustainable development? Cityscape 2013, 15, 45–62. [Google Scholar]

- Spencer-Oatey, H.; Franklin, P. What is Culture. A Compilation of Quotations. GlobalPAD Core Concepts. 2012, pp. 1–22. Available online: https://warwick.ac.uk/fac/soc/al/globalpad-rip/openhouse/interculturalskills_old/global_pad_-_what_is_culture.pdf (accessed on 22 October 2021).

- Hofstede, G. Culture’s Consequences: International Differences in Work-Related Values; Sage: Thousand Oaks, CA, USA, 1984; Volume 5. [Google Scholar]

- Marra, A.; Antonelli, P.; Pozzi, C. Emerging green-tech specializations and clusters—A network analysis on technological innovation at the metropolitan level. Renew. Sustain. Energy Rev. 2017, 67, 1037–1046. [Google Scholar] [CrossRef]

- Dickel, P. The impact of protectability and proactiveness on the environmental performance of new ventures. Corp. Gov. Int. J. Bus. Soc. 2017, 17, 117–133. [Google Scholar] [CrossRef]

- Riehl, K.; Kiran, A.S.; Narender, M. Capturing GreenTech-related Commercial Activities of Listed Companies. Glob. Bus. Rev. 2022, forthcoming. [Google Scholar]

- Fama, E.F.; Fisher, L.; Jensen, M.; Roll, R. The adjustment of stock prices to new information. Int. Econ. Rev. 1969, 10, 1–21. [Google Scholar] [CrossRef]

- Campbell, J.Y.; Lo, A.W.; MacKinlay, A.C.; Whitelaw, R.F. The econometrics of financial markets. Macroecon. Dyn. 1998, 2, 559–562. [Google Scholar] [CrossRef]

- Warner, J.; Brown, S. Measuring security price performance. J. Financ. Econ. 1980, 8, 205–258. [Google Scholar]

- Hofstede, G.; Hofstede, G.J.; Minkov, M. Cultures and Organizations: Software of the Mind; Mcgraw-Hill: New York, NY, USA, 2005; Volume 2. [Google Scholar]

- Kaufmann, D.; Kraay, A.; Mastruzzi, M. The Worldwide Governance Indicators: Methodology and Analytical Issues; World Bank Policy Research Working Paper; World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Botta, E.; Koźluk, T. Measuring Environmental Policy Stringency in OECD Countries; OECD: Paris, France, 2014. [Google Scholar] [CrossRef]

- Porta, R.L.; Lopez-de Silanes, F.; Shleifer, A.; Vishny, R.W. Law and finance. J. Political Econ. 1998, 106, 1113–1155. [Google Scholar] [CrossRef]

- Liu, F.T.; Ting, K.M.; Zhou, Z.H. Isolation forest. In Proceedings of the 2008 Eighth IEEE International Conference on Data Mining, Pisa, Italy, 15–19 December 2008; pp. 413–422. [Google Scholar]

- Liu, F.T.; Ting, K.M.; Zhou, Z.H. Isolation-based anomaly detection. Acm Trans. Knowl. Discov. Data (TKDD) 2012, 6, 1–39. [Google Scholar] [CrossRef]

- Kennedy, P. A Guide to Econometrics; John Wiley & Sons: Hoboken, NJ, USA, 2008. [Google Scholar]

- Tucker, L.; MacCallum, R. Exploratory Factor Analysis: A Book Manuscript. 2012. Available online: http://www.unc.edu/~rcm/book/factornew.htm (accessed on 22 October 2017).

- Bartlett, M.S. Properties of sufficiency and statistical tests. Proc. R. Soc. Lond. Ser. A Math. Phys. Sci. 1937, 160, 268–282. [Google Scholar]

- Kaiser, H.F. An index of factorial simplicity. Psychometrika 1974, 39, 31–36. [Google Scholar] [CrossRef]

- Guttman, L. Some necessary conditions for common-factor analysis. Psychometrika 1954, 19, 149–161. [Google Scholar] [CrossRef]

- Kaiser, H.F.; Dickman, K.W. Analytic determination of common factors. Am. Psychol. 1959, 14, 425. [Google Scholar]

- Saunders, D.R. The rationale for an “oblimax” method of transformation in factor analysis. Psychometrika 1961, 26, 317–324. [Google Scholar] [CrossRef]

- Heckman, J.J. The common structure of statistical models of truncation, sample selection and limited dependent variables and a simple estimator for such models. Ann. Econ. Soc. Meas. 1976, 5, 475–492. [Google Scholar]

- Messner, J.W.; Mayr, G.J.; Zeileis, A. Heteroscedastic Censored and Truncated Regression with crch. R J. 2016, 8, 173. [Google Scholar] [CrossRef]

- Shaphiro, S.; Wilk, M. An analysis of variance test for normality. Biometrika 1965, 52, 591–611. [Google Scholar] [CrossRef]

- Massey, F.J., Jr. The Kolmogorov-Smirnov test for goodness of fit. J. Am. Stat. Assoc. 1951, 46, 68–78. [Google Scholar] [CrossRef]

- Breusch, T.S.; Pagan, A.R. A simple test for heteroscedasticity and random coefficient variation. Econometrica 1979, 47, 1287–1294. [Google Scholar] [CrossRef]

- Goldfeld, S.M.; Quandt, R.E. Some tests for homoscedasticity. J. Am. Stat. Assoc. 1965, 60, 539–547. [Google Scholar] [CrossRef]

- Fligner, M.A.; Killeen, T.J. Distribution-free two-sample tests for scale. J. Am. Stat. Assoc. 1976, 71, 210–213. [Google Scholar] [CrossRef]

- Levene, H. Contributions to Probability and Statistics—Essays in Honor of Harold Hotelling; Springer: Berlin/Heidelberg, Germany, 1960; pp. 278–292. [Google Scholar]

- R Core Team. R: A Language and Environment for Statistical Computing; R Foundation for Statistical Computing: Vienna, Austria, 2021. [Google Scholar]

- Wilkinson, G.; Rogers, C. Symbolic description of factorial models for analysis of variance. J. R. Stat. Soc. Ser. C Appl. Stat. 1973, 22, 392–399. [Google Scholar] [CrossRef]

- Chambers, J.; Hastie, T. Linear models. In Statistical Models; Wadsworth & Brooks/Cole: Pacific Grove, CA, USA, 1992; Chapter 4. [Google Scholar]

- Croissant, Y.; Zeileis, A. Truncreg: Truncated Gaussian Regression Models, R Package Version 0.2-4. 2016. Available online: https://CRAN.R-project.org/package=truncreg (accessed on 22 October 2021).

- Messner, J.W.; Zeileis, A.; Broecker, J.; Mayr, G.J. Probabilistic wind power forecasts with an inverse power curve transformation and censored regression. Wind Energy 2014, 17, 1753–1766. [Google Scholar] [CrossRef]

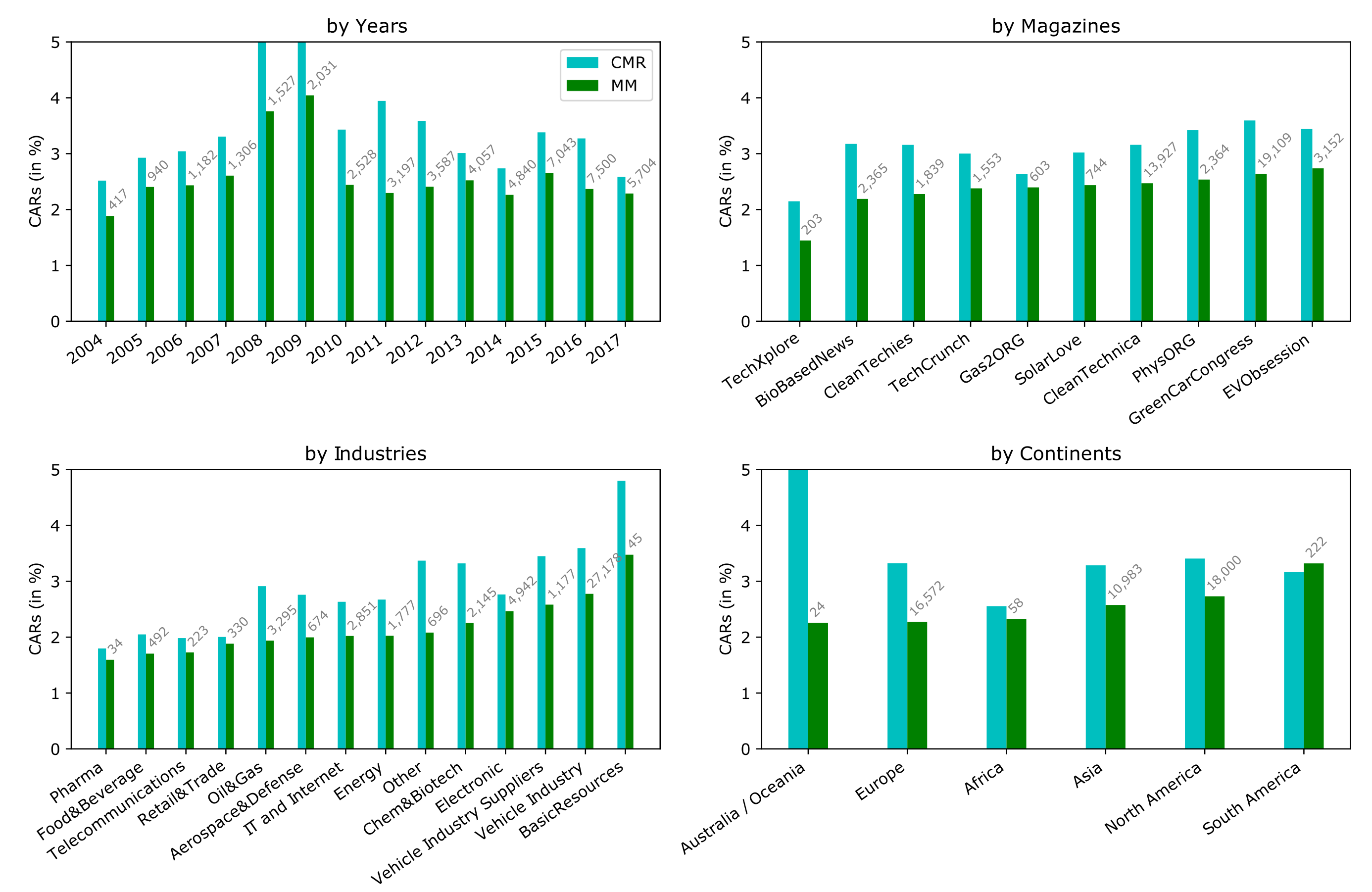

| Magazine | URL | # Events |

|---|---|---|

| GreenCarCongress | https://www.greencarcongress.com/ | 19,321 |

| BioBasedNews | https://news.bio-based.eu/ | 2408 |

| TechCrunch | https://www.techcrunch.com/ | 1586 |

| PhysORG | https://www.phys.org/ | 2441 |

| TechXplore | https://www.techxplore.com/ | 204 |

| CleanTechnica | https://www.cleantechnica.com/ | 14,291 |

| CleanTechies | https://www.cleantechies.com/ | 1786 |

| EVObsession | https://www.evobsession.com/ | 3207 |

| Gas2ORG | https://www.gas2.org/ | 654 |

| SolarLove | https://www.solarlove.org/ | 726 |

| Total | 46,624 |

| Factor | Interpretation | Eigenvalues |

|---|---|---|

| (Cum.var.expl.) | (Selected Dominant Independent Variables) | (VIF) |

| 1 | Cultural factors | 11.0862 |

| (34.41%) | NCDI (POW, 94%; UNC, 88%; MAS, 78%) | (1.00011) |

| 2 | Stability, Rule of Law | 8.2045 |

| (59.79%) | IPRI (Legal, 84%; Overall, 82%, Pol. Stability, 73%) | (1.00003) |

| 3 | Investor Rights and Indulgence | 3.0202 |

| (68.86%) | ADRI (61%), NCDI (IND, 62%) | (1.00025) |

| 4 | Economic factors | 2.6975 |

| (76.85%) | Oil (87%) and Coal (69%) price, GDP p.c. (60%) | (1.00021) |

| 5 | Environmental Policy | 1.9901 |

| (82.69%) | OECD (EPS, 62%; Pub. R&D, 62%) | (1.00418) |

| 6 | Firm-Specific factors | 1.3825 |

| (86.14%) | Market cap (66%), EBIT (58%) | (1.01140) |

| 7 | Governance factors | 0.9461 |

| (88.73%) | WWGI (GOV, 27%; COR, 23%; LAW 23%) | (1.00744) |

| Model Nr. | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Regression Model | Linear | Linear | Truncated | Truncated | CRCH | CRCH |

| CAR Estimation Model | CMR | MM | CMR | MM | CMR | MM |

| (Intercept) | 36.42 *** (0.17) | 27.13 *** (0.12) | 35.33 *** (0.20) | 25.18 *** (0.17) | 35.95 *** (0.17) | 26.32 *** (0.12) |

| Factor 1 | (0.02) | −0.05 *** (0.01) | 0.01 (0.02) | −0.07 *** (0.01 | (0.01) | −0.06 *** (0.01) |

| Factor 2 | −0.18 *** (0.02) | −0.16 *** (0.01) | −0.20 *** (0.02) | −0.19 *** (0.02) | −0.17 *** (0.02) | −0.17 *** (0.01) |

| Factor 3 | −0.30 *** (0.06) | 0.06 (0.04) | −0.35 *** (0.06) | 0.07 (0.05) | −0.30 *** (0.06) | 0.06 (0.04) |

| Factor 4 | −0.02 (0.06) | −0.21 *** (0.05) | −0.01 (0.07) | −0.24*** (0.06) | 0.02 (0.06) | −0.15 *** (0.04) |

| Factor 5 | −1.19 *** (0.09) | −1.44 *** (0.06) | −1.34 *** (0.10) | −1.77 *** (0.08) | −1.14 *** (0.09) | −1.33 *** (0.06) |

| Factor 6 | −2.28 *** (0.14) | −2.24 *** (0.10) | −2.56 *** (0.15) | −2.79 *** (0.12) | −2.07 *** (0.14) | −1.99 *** (0.10) |

| Factor 7 | 0.96 *** (0.19) | −0.24 * (0.14) | 1.06 *** (0.21) | −0.31 * (0.17) | 0.97 *** (0.19) | −0.16 (0.13) |

| F-test | 88.65 *** | 182.98 *** | 111.63 *** | 269.35 *** | 77.81 *** | 154.19 *** |

| (k, n) | (7, 9706) | (7, 12,897) | (7, 9706) | (7, 12,897) | (7, 9706) | (7, 12,897) |

| R square (%) | 5.89 | 8.64 | 6.01 | 9.04 | 5.52 | 6.75 |

| R squareAdj (%) | 5.84 | 8.59 | 5.96 | 8.99 | 5.47 | 6.70 |

| Residual Analysis—Normal Distribution | ||||||

| — Shapiro Wilk (%) | 95.29 *** | 96.64 *** | 95.25 *** | 97.17 *** | 95.08 *** | 96.43 *** |

| — Kolmogorov Smirnov (%) | 36.90 *** | 39.00 *** | 37.21 *** | 39.40 *** | 37.12 *** | 39.41 *** |

| Residual Analysis—Homoscedasticity | ||||||

| — Breusch-Pagan LM | 313.2 *** | 302.85 *** | 289.22 *** | 228.06 *** | 310.27 *** | 298.64 *** |

| — Breusch-Pagan F | 45.83 *** | 44.28 *** | 42.24 *** | 33.15 *** | 45.39 *** | 43.65 *** |

| — Goldfeld-Quandt (%) | 84.25 | 87.16 | 84.18 | 86.32 | 84.07 | 86.76 |

| — Fligner-Killeen | 18.62 *** | 12.27 *** | 17.93 *** | 10.82 *** | 18.93 *** | 13.14 *** |

| — Levene | 19.23 *** | 13.43 *** | 18.59 *** | 11.76 *** | 19.74 *** | 14.32 *** |

| Residual Analysis—Correlation | ||||||

| — with factors (%) | 1.85 | 5.23 | 0.75 | 0.74 | ||

| — with predictions (%) | −2.65 | −7.19 | 1.42 | 2.46 | ||

| — with true CARs (%) | 66.50 | 95.37 | 68.25 | 67.80 | 92.97 | 96.10 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Riehl, K.; Kiesel, F.; Schiereck, D. Political and Socioeconomic Factors That Determine the Financial Outcome of Successful Green Innovation. Sustainability 2022, 14, 3651. https://doi.org/10.3390/su14063651

Riehl K, Kiesel F, Schiereck D. Political and Socioeconomic Factors That Determine the Financial Outcome of Successful Green Innovation. Sustainability. 2022; 14(6):3651. https://doi.org/10.3390/su14063651

Chicago/Turabian StyleRiehl, Kevin, Florian Kiesel, and Dirk Schiereck. 2022. "Political and Socioeconomic Factors That Determine the Financial Outcome of Successful Green Innovation" Sustainability 14, no. 6: 3651. https://doi.org/10.3390/su14063651

APA StyleRiehl, K., Kiesel, F., & Schiereck, D. (2022). Political and Socioeconomic Factors That Determine the Financial Outcome of Successful Green Innovation. Sustainability, 14(6), 3651. https://doi.org/10.3390/su14063651