Research on the Firm Spatial Distribution and Influencing Factors of the Service-Oriented Digital Industry in Yangtze River Delta

Abstract

1. Introduction

2. Research Process

2.1. Analysis Framework and Explanatory Variables

2.2. Research Data

2.3. Research Methods and Model Setting

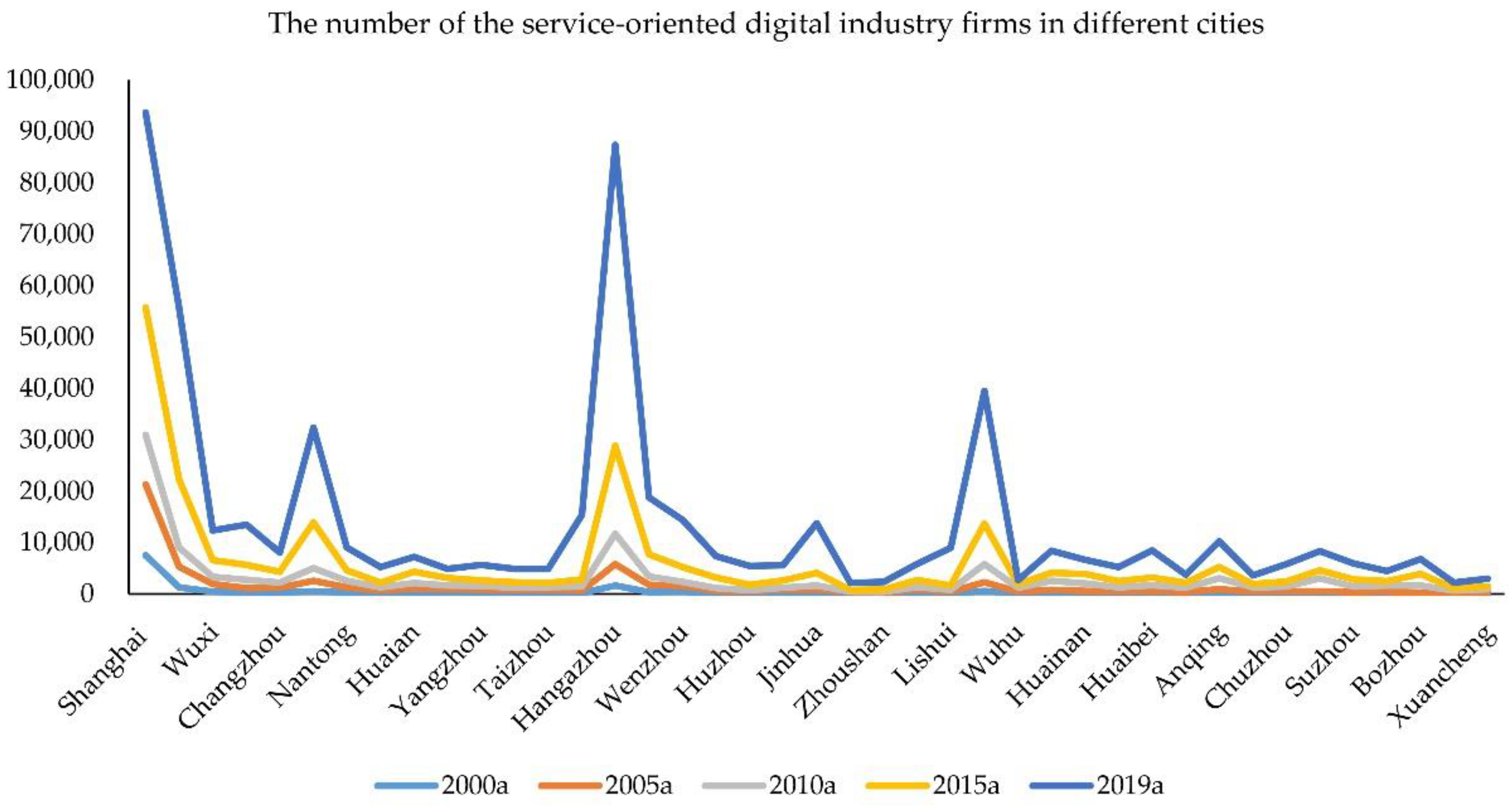

3. Spatial and Temporal Evolution Characteristics of the Total Number of Service-Oriented Digital Industries in the Yangtze River Delta

4. Regression Result Analysis

4.1. The Foundation of Socio-Economic Development

4.2. Location

4.3. Innovation Ability

4.4. Business Environment

5. Conclusions and Discussion

5.1. Conclusions

- (a)

- The service-oriented digital industry in the Yangtze River Delta has witnessed rapid growth and large changes in the total number of firms. In terms of provinces, the growth rates of each province and city are quite different. Among them, Anhui has the largest growth rate, the Zhejiang Province has the second largest growth rate, the Jiangsu Province has the third largest growth rate, and Shanghai has the smallest growth rate in the number of firms.

- (b)

- The number of the service-oriented digital industry firms in various cities in the Yangtze River Delta varies greatly, showing an obvious core–periphery structure. There are many enterprises in municipalities and provincial capitals, which are the core areas. The number of firms in non-provincial capital cities is small and they are marginal areas. The total number of firms has formed a high-value cluster area dominated by the estuary of the Yangtze River Delta, while the northwest of the Jiangsu Province, the northeast of the Anhui Province, and the southwest of the Zhejiang Province have all formed a low value cluster area. There are significant differences in the spatial differentiation of firms in different years. In 2000, the spatial pattern showed obvious differences between the east and the west, with a large number of firms in the eastern region and a small number in the western region and presented an obvious core–periphery structure. In 2005, the difference between east and west was more significant and the core–periphery structure was still obvious. In 2010, the difference between the east and the west slowed down, the core–periphery structure was significant and a high-value cluster with Shanghai as the center was formed. In 2015, the spatial pattern showed significant differences between the north and the south. With the Yangtze River as the boundary, there were more firms in the northern regions and less in the southern regions. In 2019, there was no obvious east–west difference or north–south difference and the core–periphery structure was still significant.

- (c)

- From the perspective of the influencing factors of the location selection of firms in the service-oriented digital industry, the basis of social and economic development, location, innovation ability, and business environment have different degrees of influence on the location choice of enterprises. Specifically, the per capita GDP, industrial structure upgrading, whether it is a municipality directly under the Central Government/provincial capital city, whether it has opened high-speed rail, information transmission, number of employees in the computer service industry, number of patent applications, Internet infrastructure level, and scientific fiscal expenditure have a significant positive impact on its location choice and the per capita total social consumer goods have a significant negative impact on its location choice.

5.2. Discussion

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- UNCTAD. Digital Economy Report 2019 Value Creation and Capture: Implication for Developing Countries; United Nations: New York, NY, USA, 2019; pp. 25–45. [Google Scholar]

- Jing, Q.P. The Emerging Digital economy; China Renmin University Press: Beijing, China, 1998; pp. 4–65. [Google Scholar]

- Mao, F.; Gao, Y.; Zhou, C. Evolution characteristics of spatial patterns of digital industry and its driving factors in the Yangtze River Economic Belt. Geogr. Res. 2022, 6, 1593–1609. [Google Scholar] [CrossRef]

- Chen, X.; Li, Y.; Song, L.; Wang, Y. Theoretical Framework and Research Prospect of Digital Economy. Manag. World 2022, 38, 208–224+213–216. [Google Scholar] [CrossRef]

- Wu, Y.; Wang, T. Research on the Statistical Definition and Industrial Classification of Digital Economy. Stat. Res. 2021, 38, 18–29. [Google Scholar] [CrossRef]

- Bukht, R.; Heeks, R. Defining, conceptualising and measuring the digital economy. Dev. Inform. Work. Pap. Ser. 2017, 68, 1–24. [Google Scholar] [CrossRef]

- National Bureau of Statistics. Statistical Classification of Digital Economy and Its Core Industries (2021). Available online: http://www.stats.gov.cn/xxgk/tjbz/gjtjbz/202106/t20210603_1818135.html (accessed on 27 May 2021).

- Zhang, X.; Wu, T. Research on spatial differentiation patterns of China’s provincial digital economy development. World Surv. Res. 2019, 10, 34–40. [Google Scholar] [CrossRef]

- Wang, B.; Tian, J.; Cheng, L. Spatial differentiation of digital economy and its influencing factors in China. Sci. Geogr. Sin. 2018, 38, 859–868. [Google Scholar] [CrossRef]

- Zhong, Y.; Mao, W. Spatial differentiation of digital economy and its influencing factors in the Yangtze River Economic Belt. J. Chongqing Univ. Soc. Sci. Ed. 2020, 26, 19–30. [Google Scholar] [CrossRef]

- Yuan, F.; Wei, Y.; Chen, W. Spatial agglomeration and new firm formation in the information and communication technology industry in Suzhou. Acta Geogr. Sin. 2010, 65, 153–163. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2010&filename=DLXB201002005&uniplatform=NZKPT&v=dwWPUfiS6rPWSiMw_TG_SERJ94d3Ug6j8HQ0b-tCUQK8_nAuQoMfGdooB13zfbIL (accessed on 1 June 2022).

- Lin, J.; Zhang, X.; Wang, M. Agglomeration and spatial evolution of the internet of things industry in Shanghai metropolitan. Hum. Geogr. 2017, 32, 131–137, 145. [Google Scholar] [CrossRef]

- Scott, A.J. Industrial organization and the logic of intra-metropolitan location: I. theoretical considerations. Econ. Geogr. 1983, 59, 233–250. [Google Scholar] [CrossRef]

- Wang, Z.; Mao, K.; Liu, X. An analysis for location factors that cause industrial agglomeration. Acta Geogr. Sin. 2005, 4, 567–576. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2005&filename=DLXB200504006&uniplatform=NZKPT&v=0-BIUiNLOgRaKQTE9Slmwk_4jdIf1lG8DizfeR9NhMFTZJHKZ0bdFTLIjp_5013t (accessed on 1 June 2022).

- Liu, Y.; Guo, Q.; He, C. Urban characteristics and firms’ location selection. Geogr. Res. 2016, 35, 1301–1313. [Google Scholar] [CrossRef]

- Liu, C.; Wang, Z.; Li, X. Spatial pattern evolution and location choice of internet startups: A case study of Hangzhou. Econ. Geogr. 2021, 41, 107–115. [Google Scholar] [CrossRef]

- Yang, F.; Du, D.; Duan, D. The intra-metropolitan location of R&D: Intensive manufacturing in Beijing and Shanghai. Sci. Geogr. Sin. 2017, 37, 492–501. [Google Scholar] [CrossRef]

- Deng, Z. Analysis of the advantages and disadvantages of China’s digital economy development based on the industrial division. Econ. Rev. J. 2020, 4, 67–76. [Google Scholar] [CrossRef]

- OECD. OECD Digital Economy Outlook 2015. Available online: https://www.oecd-ilibrary.org/science-and-technology/oecd-digital-economy-outlook-2015_9789264232440-en (accessed on 13 July 2021).

- Yao, Z. Regional marketization level and digital economic competition: Based on the analysis of digital economic index inter—provincial spatial distribution feature. Jianghan Trib. 2020, 12, 23–33. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2021&filename=JHLT202012003&uniplatform=NZKPT&v=cOhPE6mYQ1mtsRwmnCnYsfA7SAxSkXUUnHlQuN5C4g1dFryLoQy_99qDsSqmdHVx (accessed on 1 June 2022).

- Tian, J.; Wang, B.; Wang, S. Spatial differentiation of urban digital economic development and its causes in northeast China. Areal Res. Dev. 2019, 38, 16–21. [Google Scholar] [CrossRef]

- Wang, J.; She, G. Measurement and regional comparison of digital economy development level in China. China Bus. Mark. 2021, 8, 3–17. [Google Scholar] [CrossRef]

- Zhang, L.; Hu, B.; Wang, S. Research on the evolution mechanism and characteristics of digital economy. Stud. Sci. Sci. 2021, 39, 406–414. [Google Scholar] [CrossRef]

- Jiao, S.; Sun, Q. Research on the measurement of China’s digital economy development and its influencing factors. World Surv. Res. 2021, 7, 13–23. [Google Scholar] [CrossRef]

- Peng, W.; Han, D.; Yin, Y.; Yang, Y. Spatial Evolution and Integrated Development of Digital Economy in Beijing-Tianjin-Hebei Region. Econ. Geogr. 2022, 42, 136–143+232. [Google Scholar] [CrossRef]

- Cox, K.R. Location and Public Problems: A Political Geography of the Contemporary World; Maaroufa Press., Inc: Chicago, IL, USA, 1979; pp. 45–63. [Google Scholar]

- Zhang, W.J. The economics of Location; The Commercial Press: Beijing, China, 2022; pp. 221–235. [Google Scholar]

- Kang, J.J.; Wang, M.F. Spatial Pattern Evolution and Influencing Factors of Digital Economy Service Industry in Shanghai. Shanghai Econ. 2021, 4, 14–26. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2021&filename=SJIN202104003&uniplatform=NZKPT&v=-xEyXlyTYy6ryDCvXyj43CL8f9uSl-1KTwP6ZH9l8El2y0M1cXrdTQA_ZDAnxbrU (accessed on 1 June 2022).

- Kang, J.J.; Zhang, F.; Ning, Y.M. Value allocation and China’s evolving role in the global value chains of iPhone parts. Prog. Geogr. 2019, 38, 395–406. [Google Scholar] [CrossRef]

- Xu, W.; Zhou, J.; Liu, C. The impact of digital economy on urban carbon emissions: Based on the analysis of spatial effects. Geogr. Res. 2022, 41. [Google Scholar] [CrossRef]

- Li, Z.J.; Zhang, S.G.; Niu, Z.W.; Yuan, W.R.; Liu, Q. Theoretical logic, Comparative Analysis, and the Countermeasures of Doing Business Assessment in Chinese Cities. J. Manag. World 2021, 37, 98–112+118. [Google Scholar] [CrossRef]

- Zhou, W. Data Empowerment: The Theoretical Logic and Optimization Path of Digital Business Environment Construction. Truth Seek. 2022, 4, 30–42+110. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2022&filename=QUAK202204004&uniplatform=NZKPT&v=kXcfJTujshqzcGmen5WkpZwtjrn8t2ep19ofTb_fXHvSNAM21ksdtf3tYFs8NENn (accessed on 1 June 2022).

- Qiu, J.; Wang, M. The temporal-spatial differences and influencing factors of internet development in China since 2020. Areal Res. Dev. 2010, 29, 28–32, 38. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2010&filename=DYYY201005006&uniplatform=NZKPT&v=uemvkw4drAb38nIlu2OWyOuKM9ryLbl69EcxE7no7wr3I304FTPvc4QEFVF-cVLk (accessed on 1 June 2022).

- Xiao, F.; Lin, J.J. High-speed rail and high-tech industry evolution: Empirical evidence from China. Transportation Res. Interdiscip. Perspect. 2021, 10, 100358. [Google Scholar] [CrossRef]

- Jiao, J.; Wang, J.; Zhang, F. Roles of accessibility, connectivity and spatial interdependence in realizing the economic impact of high-speed rail: Evidence from China. Transp. Policy 2020, 91, 1–15. [Google Scholar] [CrossRef]

- Bai, J.; Jin, W.; Zhou, S. Proximity and Knowledge Spillovers: Evidence from the Introduction of New Airline Routes. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3851753 (accessed on 1 June 2022).

- Chen, X.; Miao, Z. Spatial distribution of digital economic growth dynamics and regional income. Acta Geogr. Sin. 2021, 76, 1882–1894. [Google Scholar] [CrossRef]

- Xiao, F.; Wang, J.; Yujin, H.; Hengyu, G. Exploring the spatial and scale variation of factors affecting the geography of high-tech enterprises in China. Geogr. Res. 2022, 41, 1338–1351. [Google Scholar] [CrossRef]

- Sun, C.; Song, X. Total factor productivity of marine economy in China in the era of digital economy. Prog. Geogr. 2021, 40, 1983–1998. [Google Scholar] [CrossRef]

- Li, W.; Zheng, M. Is it Substantive Innovation or Strategic Innovation?—Impact of Macroeconomic Policies on Micro-enterprises’ Innovation. Econ. Res. J. 2016, 51, 60–73. [Google Scholar]

- Zhou, X.; Cheng, L.; Wang, H. Is the higher the level of technological innovation, the better the financial performance of enterprises—Empirical study based on patent application data of Chinese pharmaceutical listed companies in 2016 Research. J. Financ. Res. 2012, 8, 166–179. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFD2012&filename=JRYJ201208016&uniplatform=NZKPT&v=0v72DW-iZqgtfXPH75E4A7J0gga3HjIueeLMNZ17OYMq8U4Gnb4lMRPlQaNHhCoV (accessed on 1 June 2022).

- Li, H. The Spatial Distribution Chaiacteristics of China Higher Education Institutions and Their Influential Factors. J. High. Educ. 2021, 42, 40–47. Available online: https://kns.cnki.net/kcms/detail/detail.aspx?dbcode=CJFD&dbname=CJFDLAST2021&filename=HIGH202104005&uniplatform=NZKPT&v=-4m9-EW7O9dPl5xrJBSSMp1ZuFuF9EIOQbKpyutpC_D8GFD-0FIR-hm7RzQPr0qB (accessed on 23 October 2022).

- LI, T.; Sun, G.; Cui, G. Digital industrialization and industrial digitization: Two-way linkage, industrial network characteristics, and digital economy development. Ind. Econ. Res. 2021, 4, 54–68. [Google Scholar] [CrossRef]

- Institute, T.R. How Much Is the Impact of Higher Education on the Sluggish Development of Digital Economy? Available online: https://36kr.com/p/1243914050620678 (accessed on 28 May 2021).

- BaiDu. Weiya’s Tax Evasion Case. Available online: https://baike.baidu.com/item/%E8%96%87%E5%A8%85%E9%80%83%E7%A8%8E%E6%A1%88/59551306?fr=aladdin (accessed on 20 December 2021).

- News, N. Digital Economy Enables Suqian to Develop in High Quality as a “Famous E-Commerce City”. Available online: https://www.sohu.com/a/551847449_412025 (accessed on 27 May 2022).

- Wu, F.; Hu, H.; Lin, H.; Ren, X. Enterprise Digital Transformation and Capital Market Performance:Empirical Evidence from Stock Liquidity. Manag. World 2021, 37, 130–144+110. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indicator System | Variable Name | Variable Name Abbreviation | Expected Symbol | |

|---|---|---|---|---|

| Social and economic development needs | Urban economic development level | GDP per capita | GDP | + |

| Upgrading of urban industrial structure | Proportion of added value of tertiary industry in GDP | IndustStruct | + | |

| Location | Municipality/provincial capital city | Dummy variable, whether it is a municipality/provincial capital city | City | + |

| High-speed rail | Dummy variable, whether there is high-speed railway in that year | Rail | + | |

| Innovation capability | Human capital innovation | Number of colleges and universities | University | + |

| Number of employees in information transmission and computer service industries | Employee | + | ||

| Technological innovation | Number of patent applications | Patent | + | |

| Business environment | Globalization level | Actually utilized foreign capital | Global | + |

| Marketization level | Proportion of state-owned firms | State-owned | − | |

| Market vitality | Total retail sales of consumer goods per capita | MarketVitality | + | |

| Policy environment | Scientific fiscal expenditure per capita | SciFiscal | + | |

| Infrastructure | Internet Infrastructure | Internet | + | |

| Ecological environment | PM2.5 concentration | PM2.5 | − |

| Variables | Variable Description (Unit) | Minimum | Maximum | Mean | Standard Deviation | Vif |

|---|---|---|---|---|---|---|

| Urban economic development level | GDP per capita (RMB 10,000/Person) | 0.110 | 15.879 | 4.498 | 3.757 | 4.36 |

| Upgrading of urban industrial structure | Proportion of added value of tertiary industry in GDP (%) | 25.19 | 72.73 | 41.186 | 8.179 | 2.24 |

| Municipality/provincial capital city | Virtual variable, whether it is a municipality/provincial capital city | 0 | 1 | 0.098 | 0.297 | 5.36 |

| High-speed rail | Dummy variable, whether there is high-speed railway in that year | 0 | 1 | 0.444 | 0.498 | 2.15 |

| Human capital innovation | Number of colleges and universities (Pieces) | 0 | 67 | 8.717 | 12.827 | 8.08 |

| Number of employees in information transmission and computer service industries (Person) | 700 | 417,680 | 14,826.190 | 45,728.130 | 4.33 | |

| Technological innovation | Number of patent applications (Pieces) | 0 | 173,586 | 11,167.560 | 23,481.500 | 5.37 |

| Globalization level | Actually utilized foreign capital (RMB 100 mn) | 0.081 | 1314.020 | 84.852 | 158.654 | 4.78 |

| Marketization level | Proportion of state-owned firms | 0 | 342 | 55.976 | 61.138 | 1.30 |

| Market vitality | Total retail sales of consumer goods per capita (RMB/Person) | 916.717 | 76,572.470 | 17,102.740 | 15,021.840 | 4.83 |

| Policy environment | Scientific fiscal expenditure per capita (RMB 10,000/Person) | 0.091 | 1689.132 | 221.185 | 327.526 | 3.44 |

| Infrastructure | Internet Infrastructure (%) | 0.002 | 2.334 | 0.421 | 0.438 | 2.48 |

| Ecological environment | PM2.5 concentration (um) | 20 | 78.885 | 48.281 | 12.217 | 1.19 |

| Variable | GDP | IndustStruct | Rail | City | University | Employee | Patent | Global | State-Owned | MarketVitality | SciFiscal | Internet | PM2.5 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| GDP | 1 | ||||||||||||

| IndustStruct | 0.443 *** | 1 | |||||||||||

| Rail | 0.690 *** | 0.291 *** | 1 | ||||||||||

| City | 0.230 *** | 0.400 *** | 0.103 | 1 | |||||||||

| University | 0.238 *** | 0.516 *** | 0.109 | 0.882 *** | 1 | ||||||||

| Employee | 0.367 *** | 0.643 *** | 0.169 *** | 0.502 *** | 0.664 *** | 1 | |||||||

| Patent | 0.544 *** | 0.610 *** | 0.236 *** | 0.382 *** | 0.544 *** | 0.761 *** | 1 | ||||||

| Global | 0.555 *** | 0.504 *** | 0.307 *** | 0.528 *** | 0.675 *** | 0.772 *** | 0.715 *** | 1 | |||||

| State-owned | −0.222 *** | −0.0187 | −0.202 *** | −0.055 | −0.002 | −0.005 | −0.009 | −0.107 | 1 | ||||

| MarketVitality | 0.622 *** | 0.591 *** | 0.360 *** | 0.237 *** | 0.301 *** | 0.503 *** | 0.693 *** | 0.392 *** | 0.109 | 1 | |||

| SciFiscal | 0.554 *** | 0.540 *** | 0.279 *** | 0.347 *** | 0.457 *** | 0.569 *** | 0.797 *** | 0.563 *** | 0.723 *** | 0.008 | 1 | ||

| Internet | 0.448 *** | 0.467 *** | 0.245 *** | 0.178 ** | 0.212 *** | 0.345 *** | 0.533 *** | 0.275 *** | 0.753 *** | 0.090 | 0.595 *** | 1 | |

| PM2.5 | 0.089 | 0.129 * | 0.146 ** | −0.065 | −0.055 | 0.0001 | 0.041 | −0.065 | 0.110 *** | −0.244 *** | 0.038 | 0.182 *** | 1 |

| Factors | Variables | Variable Description (Unit) | Coefficient | p Value 1 |

|---|---|---|---|---|

| Social and economic development needs | Urban economic development level | GDP per capita (RMB 10,000/Person) | 949.161 | 0.077 * |

| Upgrading of urban industrial structure | Proportion of added value of tertiary industry in GDP (%) | 1614.902 | 0.005 *** | |

| Location | Municipality/provincial capital city | Virtual variable, whether it is a municipality/provincial capital city | 6351.897 | 0.001 *** |

| High-speed rail | Dummy variable, whether there is high-speed railway in that year | 3131.287 | 0.000 *** | |

| Creativity | Human capital innovation | Number of colleges and universities (Pieces) | 161.934 | 0.862 |

| Number of employees in information transmission and computer service industries (Person) | 5455.717 | 0.000 *** | ||

| Technological innovation | Number of patent applications (Pieces) | 3958.436 | 0.000 *** | |

| Business environment | Globalization level | Actually utilized foreign capital (RMB 100 mn) | −875.896 | 0.119 |

| Marketization level | Proportion of state-owned firms | −217.985 | 0.483 | |

| Market vitality | Total retail sales of consumer goods per capita (RMB/Person) | −2399.919 | 0.004 *** | |

| Policy environment | Scientific fiscal expenditure per capita (RMB 10,000/Person) | 1251.263 | 0.025 ** | |

| Infrastructure | Internet infrastructure (%) | 1311.748 | 0.020 ** | |

| Ecological environment | PM2.5 concentration (um) | −530.066 | 0.258 | |

| Cons | - | - | −2589.54 | 0.001 *** |

| Factors | Variables | Positive Influence | Negative Influence |

|---|---|---|---|

| Social and economic development needs | Urban economic development level | √ | |

| Upgrading of urban industrial structure | √ | ||

| Location | Municipality/provincial capital city | √ | |

| High-speed rail | √ | ||

| Creativity | College and University | - | - |

| Employees in information transmission and computer service industries | √ | ||

| Technological innovation | √ | ||

| Business environment | Globalization level | - | - |

| Marketization level | - | - | |

| Market vitality | √ | ||

| Policy environment | √ | ||

| Infrastructure | √ | ||

| Ecological environment | - | - |

| Directions | Indicators | Strategic Goals | Tools |

|---|---|---|---|

| Social and economic development needs | Urban economic development level | Accelerate the development of digital industrialization and industry digitalization | Digital industrialization: enhance the innovation ability of key technologies (sensors, quantum information, etc.), improve the competitiveness of core industries, and cultivate new business forms and models (platform economy, etc.). Industrial digitalization: based on different industrial characteristics and differentiated needs, promote the all-round and full-chain digital transformation of traditional entrepreneurship and improve total factor productivity. |

| Upgrading of urban industrial structure | Advanced industrial structure promotes high-quality development of digital industry | Combine the industrial structure and resource endowment of cities in the Yangtze River Delta region, provide play to comparative advantages, and promote the development of service-oriented digital industry. | |

| Location | Municipality/provincial capital city | Create a new digital city (Shanghai, Haizhou, Nanjing, Hefei, etc.) | Deepen the construction of a new digital city, promote the integration and sharing of urban data and business collaboration, improve the urban comprehensive management service capacity, and improve the urban information model platform and operation management service platform. |

| High-speed rail | Strengthen the accessibility of urban high-speed rail network | Rebuild the new logistics system and strengthen the formation of the “high-speed rail + e-commerce” development model. Improve high-speed railway infrastructure. | |

| Innovation ability | College and University | Improving the innovation ability of colleges and universities | Deepen the development mode of universities, industry research cooperation, and implement the policy of double first-class universities and double first-class disciplines. |

| Employees in information transmission and computer service industries | Cultivate and own digital industry talents | Cultivate digital strategic management talents, in-depth analysis talents, product R&D talents, advanced manufacturing talents, digital operation talents, and digital marketing talents. Accelerate talent introduction policy (settlement, subsidy, and high-level person time). | |

| Technological innovation | Protection of intellectual property rights such as patents | Carry out research and practical exploration on intellectual property protection system in new fields and formats such as big data and artificial intelligence. Promote the implementation of data intellectual property protection projects. | |

| Business environment | Globalization level | Accelerate the globalization of digital industry | Promote the global development of emerging service capabilities such as data storage and intelligent computing. We will increase innovation in cooperation models in finance, logistics, e-commerce, and other fields, support digital firms in the Yangtze River Delta to “go global”, and actively participate in international cooperation. |

| Marketization level | Optimize the allocation of production factors of digital industry | Study data-right confirmation and classified and hierarchical management, smooth data transaction flow, realize market-oriented configuration of data elements, and promote transparency, standardization, and legalization of data-right confirmation, transaction, sharing, and protection. | |

| Market vitality | Strengthen market vitality and improve digital tax policy | Stimulate domestic market demand, strengthen cross sectoral and cross regional division of labor and collaboration, promote the collection, sharing, and utilization of regulatory data, and improve the openness, transparency, and rule of law of regulation. Strengthen tax supervision and inspection. | |

| Policy environment | Increase financial support | Focus on supporting a group of key firms with core technologies and invest in high-end chips, integrated circuits, artificial intelligence, and other key software and hardware technologies to tackle key problems. | |

| Infrastructure | Optimize and upgrade digital infrastructure | Speed up the construction of information network infrastructure. Promote the development of cloud network collaboration and computing network integration. Promote intelligent upgrading of infrastructure. | |

| Ecological environment | Accelerate ecological environment control | Governance of regional ecological environment and digital enabling ecological environment governance. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, J.; Fu, Y.; Zhang, B. Research on the Firm Spatial Distribution and Influencing Factors of the Service-Oriented Digital Industry in Yangtze River Delta. Sustainability 2022, 14, 14902. https://doi.org/10.3390/su142214902

Zhang J, Fu Y, Zhang B. Research on the Firm Spatial Distribution and Influencing Factors of the Service-Oriented Digital Industry in Yangtze River Delta. Sustainability. 2022; 14(22):14902. https://doi.org/10.3390/su142214902

Chicago/Turabian StyleZhang, Jing, Yuhan Fu, and Baifa Zhang. 2022. "Research on the Firm Spatial Distribution and Influencing Factors of the Service-Oriented Digital Industry in Yangtze River Delta" Sustainability 14, no. 22: 14902. https://doi.org/10.3390/su142214902

APA StyleZhang, J., Fu, Y., & Zhang, B. (2022). Research on the Firm Spatial Distribution and Influencing Factors of the Service-Oriented Digital Industry in Yangtze River Delta. Sustainability, 14(22), 14902. https://doi.org/10.3390/su142214902