Public Pressure, Environmental Policy Uncertainty, and Enterprises’ Environmental Information Disclosure

Abstract

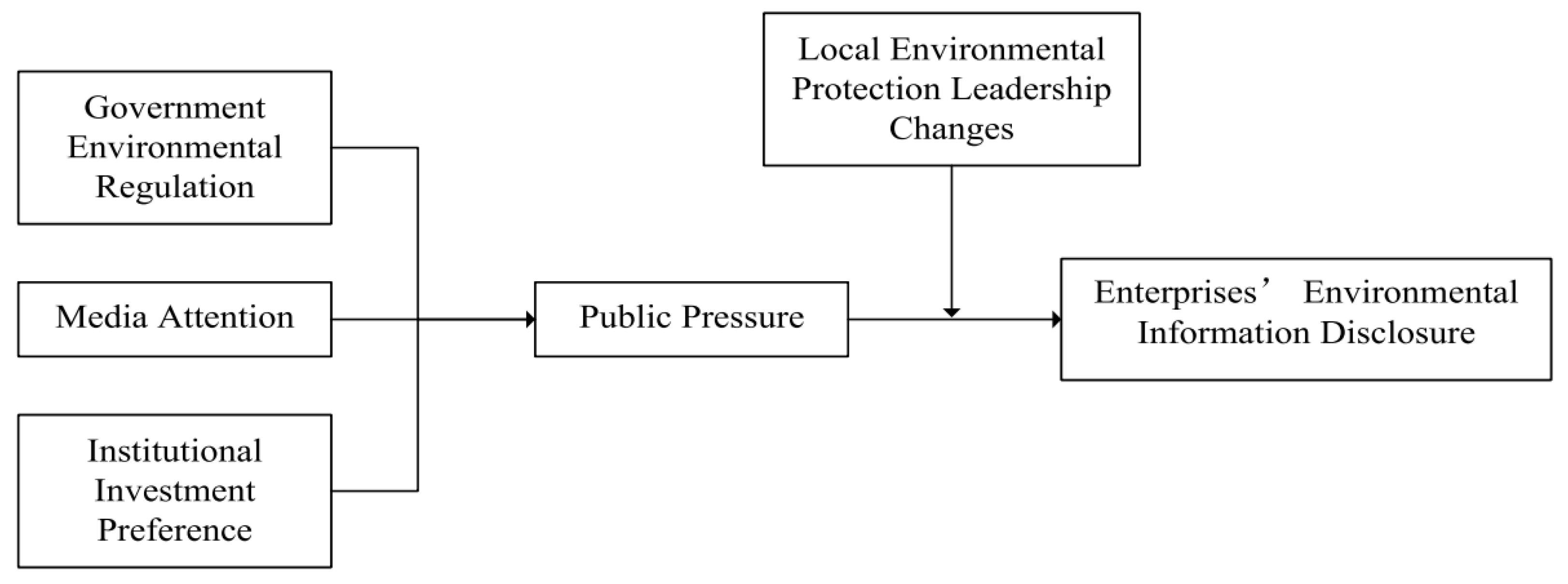

:1. Introduction

- What is the correlation between government environmental regulation or media attention and the EEID?

- What is the correlation between institutional investment preferences and the EEID?

- How are local environmental protection leadership changes and increased public pressure on the EEID related?

- How may local environmental protection leadership change moderate the relationship between public pressure and the EEID?

2. Literature Review and Hypothesis Development

2.1. Public Pressure and the EEID

2.2. Government Environmental Regulation and the EEID

2.3. Media Attention and the EEID

2.4. Institutional Investment Preference and the EEID

2.5. Regulatory Role of the Change of Local Environmental Protection Leadership

3. Study Design

3.1. Samples and Data

3.2. Definition of Variables

3.2.1. Explained Variable (The Level of the EEID)

3.2.2. Explanatory Variables

Government Environmental Regulation

Media Attention

Institutional Investment Preference

3.2.3. Moderating Variables: Local Environmental Leadership Changes

Transfer Mode

Age

Source of Origin

3.2.4. Control Variables

3.3. Regression Model

4. Results and Analysis

4.1. Descriptive Statistics and Correlation Analysis

4.2. Analysis of Regression Results

4.2.1. Public Pressure and the EEID

4.2.2. The Moderating Effect of Changes in Local Environmental Protection Officials

4.3. Robustness Test

4.3.1. Change the Measurement Method of the Explained Variable

4.3.2. To Control the Impact of the Change of Governor and Provincial Party Secretary

5. Conclusions and Enlightenment

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- He, P.; Shen, H.; Zhang, Y.; Ren, J. External Pressure, Corporate Governance, and Voluntary Carbon Disclosure: Evidence from China. Sustainability 2019, 11, 2901. [Google Scholar] [CrossRef] [Green Version]

- Fan, Y.; Xia, M.; Zhang, Y.; Chen, Y. The influence of social embeddedness on organizational legitimacy and the sustainability of the globalization of the sharing economic platform: Evidence from Uber China. Resour. Conserv. Recycl. 2019, 151, 104490. [Google Scholar] [CrossRef]

- Dai, X.; Zhu, Z.; Zeng, X.; Luo, F. Research on Environmental Protection and Fire Safety in Furniture Industry Cluster Construction. Furnit. Inter. Des. 2020, 2020, 42–44. [Google Scholar]

- Qian, W.; Xu, P.; Wang, L. A review on the polyester fiber recycling and its environmental impact assessment. Adv. Text. Technol. 2021, 29, 22–26. [Google Scholar]

- Liang, J.; Cheng, W. Research on status and dilemma of sustainable clothing consumption behavior. J. Silk 2020, 57, 18–25. [Google Scholar]

- Yuan, X.-B.; Liu, Y.-T.; Chen, N.; Wu, Y.-Z.; Liu, Y.-J.; Sun, A.-K. Research Progress on Green Packaging Materials. Packag. Eng. 2022, 43, 87–94. [Google Scholar] [CrossRef]

- Wang, T.; Zhao, B. Research on the Design of Household Garbage Can Based on the Concept of Environmental Protection Design. Furnit. Inter. Des. 2020, 04, 68–70. [Google Scholar]

- Luo, W.; Guo, X.; Zhong, S.; Wang, J. Environmental information disclosure quality, media attention and debt financing costs: Evidence from Chinese heavy polluting listed companies. J. Clean. Prod. 2019, 231, 268–277. [Google Scholar] [CrossRef]

- Kathyayini, K.R.; Carol, A.T.; Laurence, H.L. Corporate Governance and Environmental Reporting: An Australian Study. Int. J. Bus. Soc. 2012, 12, 143–163. [Google Scholar]

- Bo, B.C.; Doowon, L.; Jim, P. An analysis of Australian company carbon emission disclosures. Pac. Account. Rev. 2013, 25, 58–79. [Google Scholar]

- Gary, F.P.; Andrea, M.R. Does the Voluntary Adoption of Corporate Governance Mechanisms Improve Environmental Risk Disclosures? Evidence from Greenhouse Gas Emission Accounting. J. Bus. Ethics 2014, 125, 637–666. [Google Scholar]

- Richard, L.; Gray, R. Social and Environmental Accounting and Organizational Change. Soc. Environ. Account. J. 2014, 34, 81–86. [Google Scholar]

- Julie, C.; Muftah, M.N. Institutional investor influence on global climate change disclosure practices. Aust. J. Manag. 2012, 37, 169–186. [Google Scholar]

- Zhang, Y.-J.; Liu, J.-Y. Overview of research on carbon information disclosure. Front. Eng. Manag. 2020, 7, 47–62. [Google Scholar] [CrossRef]

- Darrell, W.; Schwartz, B.N. Environmental disclosures and public policy pressure. J. Account. Public Policy 1997, 16, 125–154. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Islam, M.A.; Deegan, C. Media pressures and corporate disclosure of social responsibility performance information: A study of two global clothing and sports retail companies. Account. Bus. Res. 2010, 40, 131–148. [Google Scholar] [CrossRef]

- Wang, X.; Xu, X.; Wang, C. Public pressure, social reputation, inside governance and firm environmental information disclosure: The evidence from Chinese listed manufacturing firms. Nankai Bus. Rev. 2013, 16, 82–91. [Google Scholar]

- Hammami, A.; Zadeh, M.H. Audit quality, media coverage, environmental, social, and governance disclosure and firm investment efficiency. Int. J. Account. Inf. Manag. 2020, 28, 45–72. [Google Scholar] [CrossRef]

- Christopher, T.; Hutomo, S.; Monroe, G. Voluntary environmental disclosure by Australian listed mineral mining companies: An application of stakeholder theory. Int. J. Account. Bus. Soc. 1997, 5, 42–66. [Google Scholar]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Li, L.; Liu, Q.; Tang, D.; Xiong, J. Media reporting, carbon information disclosure, and the cost of equity financing: Evidence from China. Environ. Sci. Pollut. Res. 2017, 24, 9447–9459. [Google Scholar] [CrossRef]

- Carroll, C.E.; McCombs, M. Agenda-setting effects of business news on the public’s images and opinions about major corporations. Corp. Reput. Rev. 2003, 6, 36–46. [Google Scholar] [CrossRef]

- Chen, X.; Yunhe, H.U. Analysis of public concern on traditional dyeing and printing techniques based on Baidu index. J. Silk 2020, 57, 41108. [Google Scholar]

- Gray, S.J.; Vint, H.M. The impact of culture on accounting disclosures: Some international evidence. Asia-Pac. J. Account. 1995, 2, 33–43. [Google Scholar] [CrossRef]

- Kaymak, T.; Bektas, E. Corporate Social Responsibility and Governance: Information Disclosure in Multinational Corporations. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 555–569. [Google Scholar] [CrossRef]

- Schnatterly, K.; Shaw, K.W.; Jennings, W.W. Information advantages of large institutional owners. Strateg. Manag. J. 2008, 29, 219–227. [Google Scholar] [CrossRef]

- Petersen, H.L.; Vredenburg, H. Morals or economics? Institutional investor preferences for corporate social responsibility. J. Bus. Ethics 2009, 90, 1. [Google Scholar] [CrossRef]

- Ruf, B.M.; Muralidhar, K.; Brown, R.M.; Janney, J.J.; Paul, K. An empirical investigation of the relationship between change in corporate social performance and financial performance: A stakeholder theory perspective. J. Bus. Ethics 2001, 32, 143–156. [Google Scholar] [CrossRef]

- Neubaum, D.O.; Zahra, S.A. Institutional ownership and corporate social performance: The moderating effects of investment horizon, activism, and coordination. J. Manag. 2006, 32, 108–131. [Google Scholar] [CrossRef]

- Huang, J.; Zhou, C.-N. Empirical Research on the Impact of Ownership Structure and Management Behavior on the Environmental Disclosure: Evidence from Heavy Polluting Industries Listed in Shanghai Stock Exchange. China Soft Sci. 2012, 1, 133–143. [Google Scholar]

- Li, D.D.; Feng, M.; Long, S.; Yuan, G.; Zhou, P.; Li, Y. Proactive Macroeconomic Management. In Economic Lessons from China’s Forty Years of Reform and Opening-Up; Springer: Singapore, 2021; pp. 183–251. [Google Scholar] [CrossRef]

- Chunfang, C. Between the Transfer of the Political Power and the Corporate Investment: The Logic of China. Manag. World 2013, 1, 143–157. (In Chinese) [Google Scholar]

- Fraser, J.; Quail, R.; Simkins, B. Enterprise Risk Management: Today’s Leading Research and Best Practices for Tomorrow’s Executives; John Wiley & Sons: San Francisco, CA USA, 2010; Volume 3. [Google Scholar]

- Chuang, S.-P.; Huang, S.-J. The effect of environmental corporate social responsibility on environmental performance and business competitiveness: The mediation of green information technology capital. J. Bus. Ethics 2018, 150, 991–1009. [Google Scholar] [CrossRef]

- Dai, L.; Ngo, P. Political uncertainty and accounting conservatism. Eur. Account. Rev. 2021, 30, 277–307. [Google Scholar] [CrossRef]

- Cailou, J.; Fuyu, Z.; Chong, W. Environmental information disclosure, political connections and innovation in high-polluting enterprises. Sci. Total Environ. 2021, 764, 144248. [Google Scholar] [CrossRef]

- Cai, R.; Lv, T.; Deng, X. Evaluation of Environmental Information Disclosure of Listed Companies in China’s Heavy Pollution Industries: A Text Mining-Based Methodology. Sustainability 2021, 13, 5415. [Google Scholar] [CrossRef]

- Kaolei, G.; Rui, Z. Corporate Reputation and Earnings Management: Efficient Contract Theory or Rent-Seeking Theory. Account. Res. 2019, 59–64. [Google Scholar]

- Mao, Y.; Wang, J. Is green manufacturing expensive? Empirical evidence from China. Int. J. Prod. Res. 2019, 57, 7235–7247. [Google Scholar] [CrossRef]

- Yu, L.; Zhang, W.; Bi, Q.; Dong, J. Environmental Policy Uncertainty and Corporate Environmental Information Disclosure: Evidence from the Turnover of Local Environmental Protection Directors. J. Shanghai Univ. Financ. Econ. 2020, 22, 35–50. [Google Scholar]

- Hu, J.; Long, W.; Song, X.; Tang, T. The driving force in corporate environmental governance: Turnover of environmental protection department directors as an indicator. Nankai Bus. Rev. Int. 2020, 11, 253–282. [Google Scholar] [CrossRef]

- Wu, D.; Zhu, S.; Memon, A.A.; Memon, H. Financial Attributes, Environmental Performance, and Environmental Disclosure in China. Int. J. Environ. Res. Public Health 2020, 17, 8796. [Google Scholar] [CrossRef]

- Wu, H.; Li, Y.; Hao, Y.; Ren, S.; Zhang, P. Environmental decentralization, local government competition, and regional green development: Evidence from China. Sci. Total Environ. 2020, 708, 135085. [Google Scholar] [CrossRef]

- Chen, C.; Jiang, D.; Li, W.; Song, Z. Does analyst coverage curb executives’ excess perks? Evidence from Chinese listed firms. Asia-Pac. J. Account. Econ. 2022, 29, 329–343. [Google Scholar] [CrossRef]

{kind=link}

| First Level Indicators | Secondary Indicators |

|---|---|

| Strategy and goal of environmental protection | The environmental system, policy, and objective |

| Environmental risk prevention and emergency system | |

| Environmental action and performance | Environmental protection investment (equipment purchase) and environmental protection technology development of enterprises |

| Environmental protection expenses such as sewage discharge costs and labor expenditure | |

| Discharge and compliance of pollutants | |

| Operation of environmental protection facilities | |

| Resource-saving and resource consumption | |

| Environmental subsidies and penalties | Government grants, financial subsidies, and tax relief related to environmental protection |

| Secondary indicators |

| Variable Type | Variable Name | Symbol | Calculation Method |

|---|---|---|---|

| Explained variable | level | EID | According to the method of this paper, the score of the EEID is measured |

| Explanatory variable | Government environmental regulation | GR | Pollution Information Transparency Index |

| Media attention | Media | ln (total number of news reports in that year + 1) | |

| Institutional investment preference | Share | The shareholding ratio of institutional investors | |

| Moderating variables | Change of local environmental leadership | COE | If the director of the DoEE of the province where the enterprise is registered changes, the value is 1; otherwise, it is 0 |

| Transfer mode | Promote | If the director of the DoEE takes office through promotion, the value will be 1; if he is transferred, demoted, or unchanged, the value will be 0 | |

| Age | Age | If the director of the DoEE is less than or equal to 55 years old at the time of change, the value is 1; if he is more than 55 years old and there is no change, the value is 0 | |

| Source area | Origin | If the enterprise is not located in the city before the new director of the DoEE takes office and belongs to the non-source area, the value is 1, otherwise 0 | |

| control variable | Gender | Gender | When the gender of the director of the DoEE is female, the value is 1, otherwise 0 |

| Educational level | Edu | When the education background of the director of the DoEE is master or above, the value is 1, otherwise 0 | |

| Enterprise-scale | Size | Natural logarithm of total assets at the end of the period | |

| Financial leverage | Debt | (total liabilities at the end of the period/total assets at the end of the period) × 100% | |

| Profitability | ROA | (net profit / average total assets) × 100% | |

| Nature of property rights | Type | If the company is a state-owned controlling shareholder, the assignment is 1, otherwise 0 | |

| Ownership concentration | CR10 | The sum of the shareholding ratio of the top ten shareholders | |

| Company growth rate | Growth | (difference of primary business income between the current period and the previous period/primary business income of the previous period) × 100% | |

| Change of provincial Party Secretary | COS | If the secretary of the provincial Party committee of the province where the enterprise is registered changes, the value is 1; otherwise, it is 0 | |

| Change of governor | COG | If the governor of the province where the enterprise is registered changes, the value is 1; otherwise, it is 0 |

| Variable | Number of Samples | Average | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|

| EEID level | 2280 | 7.117 | 3.897 | 0 | 17 |

| Government environmental regulation | 2280 | 57.84 | 13.06 | 30.40 | 82.40 |

| Media attention | 2280 | 3.340 | 1.326 | 0 | 6.400 |

| Institutional investment preference | 2280 | 46.31 | 22.68 | 0.00318 | 91.61 |

| Change of local environmental leadership | 2280 | 0.263 | 0.440 | 0 | 1 |

| Transfer mode | 2280 | 0.200 | 0.400 | 0 | 1 |

| Age | 2280 | 0.238 | 0.426 | 0 | 1 |

| Source Region | 2280 | 0.221 | 0.415 | 0 | 1 |

| Gender | 2280 | 0.157 | 0.364 | 0 | 1 |

| educational level | 2280 | 0.686 | 0.464 | 0 | 1 |

| Change of provincial Party Secretary | 2280 | 0.258 | 0.438 | 0 | 1 |

| Change of governor | 2280 | 0.303 | 0.460 | 0 | 1 |

| Enterprise scale | 2280 | 22.80 | 1.365 | 20.48 | 26.04 |

| Financial leverage (%) | 2280 | 43.89 | 20.34 | 2.889 | 87.32 |

| Profitability (%) | 2280 | 3.813 | 5.596 | −12.37 | 17.12 |

| Nature of property rights | 2280 | 0.491 | 0.500 | 0 | 1 |

| Ownership concentration (%) | 2280 | 57.76 | 14.90 | 29.24 | 88.76 |

| Company growth rate (%) | 2280 | 8.945 | 23.26 | −36.25 | 75.75 |

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EID | 1 | |||||||||||||||||

| GR | 0.047 ** | 1 | ||||||||||||||||

| Media | 0.196 *** | −0.049 ** | 1 | |||||||||||||||

| Share | 0.206 *** | 0.007 | 0.298 *** | 1 | ||||||||||||||

| COE | 0.057 *** | 0.005 | 0.021 | 0.027 | 1 | |||||||||||||

| Promote | 0.036 * | 0.021 | 0.044 ** | 0.030 | 0.839 *** | 1 | ||||||||||||

| Age | 0.063 *** | 0.052 ** | 0.028 | 0.019 | 0.937 *** | 0.751 *** | 1 | |||||||||||

| Origin | 0.044 ** | 0.019 | 0.018 | 0.018 | 0.892 *** | 0.726 *** | 0.836 *** | 1 | ||||||||||

| Gender | −0.059 *** | 0.129 *** | −0.053 ** | −0.097 *** | −0.001 | 0.066 *** | −0.038 * | 0.005 | 1 | |||||||||

| Edu | 0.024 | 0.133 *** | −0.041 ** | −0.036 * | 0.151 *** | 0.155 *** | 0.117 *** | 0.133 *** | 0.293 *** | 1 | ||||||||

| COS | 0.039 * | −0.015 | 0.017 | 0.008 | 0.249 *** | 0.133 *** | 0.247 *** | 0.259 *** | −0.087 *** | 0.026 | 1 | |||||||

| COG | −0.008 | 0.051 ** | 0.029 | −0.002 | 0.105 *** | 0.149 *** | 0.095 *** | 0.090 *** | 0.050 ** | 0.023 | 0.353 *** | 1 | ||||||

| Size | 0.335 *** | 0.026 | 0.486 *** | 0.535 *** | 0.048 ** | 0.049 ** | 0.037 * | 0.024 | −0.089 *** | 0.013 | 0.017 | 0.011 | 1 | |||||

| Debt | 0.138 *** | −0.194 *** | 0.156 *** | 0.193 *** | 0.025 | 0.020 | 0.009 | −0.009 | −0.108 *** | −0.041 ** | 0.014 | −0.018 | 0.490 *** | 1 | ||||

| ROA | 0.044 ** | 0.133 *** | 0.124 *** | 0.049 ** | 0.016 | 0.007 | 0.022 | 0.035 * | 0.076 *** | 0.065 *** | 0.034 | 0.027 | 0.023 | −0.424 *** | 1 | |||

| Type | 0.211 *** | −0.173 *** | 0.201 *** | 0.421 *** | 0.041 ** | 0.043 ** | 0.029 | −0.001 | −0.167 *** | −0.107 *** | 0 | −0.014 | 0.382 *** | 0.264 *** | −0.128 *** | 1 | ||

| CR10 | 0.103 *** | 0.072 *** | 0.190 *** | 0.627 *** | 0.019 | 0.020 | 0.019 | 0.016 | −0.035 * | 0.051 ** | 0.015 | 0.035 * | 0.449 *** | 0.058 *** | 0.141 *** | 0.176 *** | 1 | |

| Growth | 0.033 | 0.109 *** | 0.026 | 0.001 | 0.113 *** | 0.105 *** | 0.105 *** | 0.097 *** | 0.047 ** | 0.043 ** | 0.133 *** | 0.198 *** | 0.050 ** | −0.025 | 0.324 *** | −0.114 *** | 0.048 ** | 1 |

| Variable | EEID Level | ||||

|---|---|---|---|---|---|

| M1 | M2 | M3 | M4 | M5 | |

| gr | 0.032 *** | 0.033 *** | 0.033 *** | 0.033 *** | 0.033 *** |

| (7.71) | (7.90) | (7.87) | (7.84) | (7.76) | |

| media | −0.014 | ||||

| (−0.28) | |||||

| share | 0.006 * | 0.006 * | 0.006 * | 0.006 * | 0.006 * |

| (1.79) | (1.87) | (1.88) | (1.84) | (1.87) | |

| coe | 0.110 * | ||||

| (1.82) | |||||

| promote | 0.141 ** | ||||

| (2.15) | |||||

| age | 0.097 | ||||

| (1.58) | |||||

| origin | 0.140 ** | ||||

| (2.21) | |||||

| gr * coe | 0.006 | ||||

| (1.25) | |||||

| gr * promote | 0.007 | ||||

| (1.43) | |||||

| gr * age | 0.008 * | ||||

| (1.71) | |||||

| gr * origin | 0.002 | ||||

| (0.32) | |||||

| share * coe | 0.006 ** | ||||

| (2.52) | |||||

| share * promote | 0.007 ** | ||||

| (2.44) | |||||

| share * age | 0.007 *** | ||||

| (2.69) | |||||

| share * origin | 0.006 ** | ||||

| (2.42) | |||||

| gender | 0.157 | 0.150 | 0.174 | 0.158 | |

| (1.31) | (1.25) | (1.45) | (1.32) | ||

| edu | −0.098 | −0.096 | −0.083 | −0.114 | |

| (−1.21) | (−1.23) | (−1.04) | (−1.42) | ||

| size | 0.459 *** | 0.448 *** | 0.450 *** | 0.447 *** | 0.446 *** |

| (4.40) | (4.29) | (4.31) | (4.29) | (4.27) | |

| debt | −0.003 | −0.003 | −0.003 | −0.003 | −0.003 |

| (−0.90) | (−0.77) | (−0.82) | (−0.75) | (−0.80) | |

| roa | 0.005 | 0.006 | 0.006 | 0.006 | 0.006 |

| (0.67) | (0.78) | (0.79) | (0.79) | (0.76) | |

| type | −0.123 | −0.135 | −0.118 | −0.133 | −0.125 |

| (−0.44) | (−0.48) | (−0.42) | (−0.47) | (−0.44) | |

| cr10 | −0.012 * | −0.011 * | −0.011 * | −0.011 * | −0.011 * |

| (−1.88) | (−1.84) | (−1.85) | (−1.82) | (−1.86) | |

| growth | 0.004 *** | 0.004 *** | 0.004 *** | 0.004 *** | 0.004 *** |

| (3.28) | (3.01) | (2.96) | (3.03) | (3.07) | |

| R-squared | 0.296 | 0.302 | 0.302 | 0.303 | 0.301 |

| F | 63.51 | 48.86 | 48.99 | 49.04 | 48.77 |

| Variable | The EEID Level (Standard) | The EEID Level | |||

|---|---|---|---|---|---|

| M6 | M7 | M8 | M9 | M10 | |

| gr | 0.008 *** | 0.009 *** | 0.028 *** | 0.032 *** | 0.028 *** |

| (7.71) | (7.90) | (6.61) | (7.54) | (6.65) | |

| media | −0.004 | ||||

| (−0.28) | |||||

| share | 0.002 * | 0.002 * | 0.006 * | 0.006 * | 0.007 * |

| (1.79) | (1.87) | (1.90) | (1.81) | (1.95) | |

| coe | 0.028 * | 0.057 | 0.066 | 0.080 | |

| (1.82) | (0.95) | (1.09) | (1.33) | ||

| gr * coe | 0.001 | 0.003 | 0.002 | 0.006 | |

| (1.25) | (0.74) | (0.42) | (1.26) | ||

| share * coe | 0.002 ** | 0.006 ** | 0.006 ** | 0.006 ** | |

| (2.52) | (2.39) | (2.38) | (2.47) | ||

| gender | 0.040 | 0.187 | 0.224 * | 0.143 | |

| (1.31) | (1.56) | (1.86) | (1.20) | ||

| edu | −0.025 | −0.065 | −0.103 | −0.056 | |

| (−1.21) | (−0.81) | (−1.27) | (−0.70) | ||

| cos | 0.162 ** | 0.261 *** | |||

| (2.47) | (4.19) | ||||

| cog | 0.296 *** | 0.347 *** | |||

| (4.65) | (5.76) | ||||

| size | 0.118 *** | 0.115 *** | 0.369 *** | 0.406 *** | 0.385 *** |

| (4.40) | (4.29) | (3.54) | (3.90) | (3.71) | |

| debt | −0.001 | −0.001 | −0.000 | −0.002 | −0.001 |

| (−0.90) | (−0.77) | (−0.11) | (−0.51) | (−0.18) | |

| roa | 0.001 | 0.001 | 0.009 | 0.006 | 0.009 |

| (0.67) | (0.78) | (1.24) | (0.89) | (1.24) | |

| type | −0.032 | −0.035 | −0.113 | −0.127 | −0.114 |

| (−0.44) | (−0.48) | (−0.40) | (−0.45) | (−0.41) | |

| cr10 | −0.003 * | −0.003 * | −0.010 * | −0.010 * | −0.010 * |

| (−1.88) | (−1.84) | (−1.66) | (−1.71) | (−1.72) | |

| growth | 0.001 *** | 0.001 *** | 0.003 ** | 0.004 *** | 0.003 ** |

| (3.28) | (3.01) | (1.99) | (2.73) | (2.02) | |

| R-squared | 0.296 | 0.302 | 0.317 | 0.309 | 0.314 |

| F | 63.51 | 48.86 | 46.51 | 47.44 | 48.76 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, D.; Memon, H. Public Pressure, Environmental Policy Uncertainty, and Enterprises’ Environmental Information Disclosure. Sustainability 2022, 14, 6948. https://doi.org/10.3390/su14126948

Wu D, Memon H. Public Pressure, Environmental Policy Uncertainty, and Enterprises’ Environmental Information Disclosure. Sustainability. 2022; 14(12):6948. https://doi.org/10.3390/su14126948

Chicago/Turabian StyleWu, Die, and Hafeezullah Memon. 2022. "Public Pressure, Environmental Policy Uncertainty, and Enterprises’ Environmental Information Disclosure" Sustainability 14, no. 12: 6948. https://doi.org/10.3390/su14126948

APA StyleWu, D., & Memon, H. (2022). Public Pressure, Environmental Policy Uncertainty, and Enterprises’ Environmental Information Disclosure. Sustainability, 14(12), 6948. https://doi.org/10.3390/su14126948