Knowledge Mapping of Corporate Financial Performance Research: A Visual Analysis Using Cite Space and Ucinet

Abstract

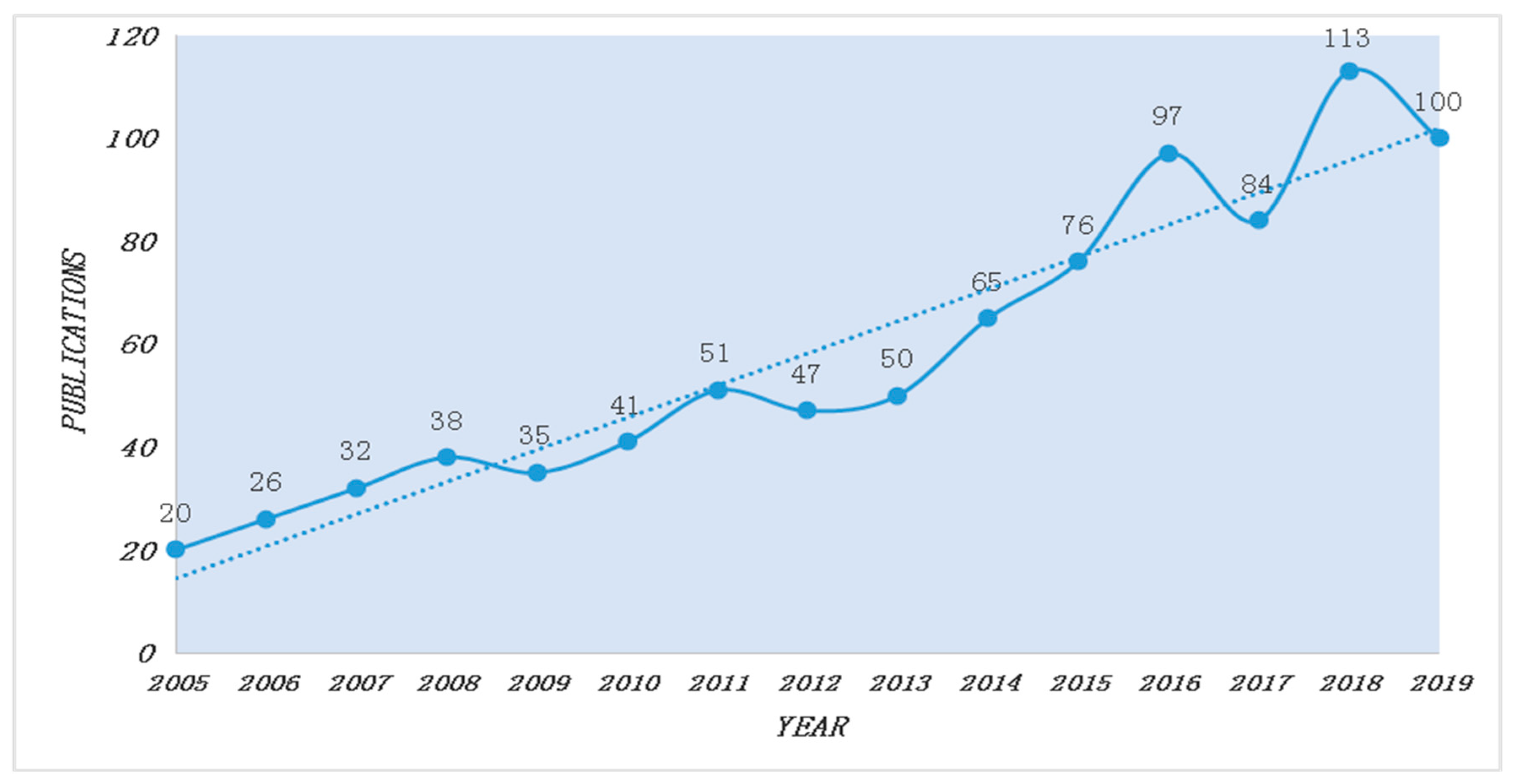

1. Introduction and Scope of Review

2. Method and Data Description

3. Results and Analysis

3.1. Mapping and Analysis of Countries

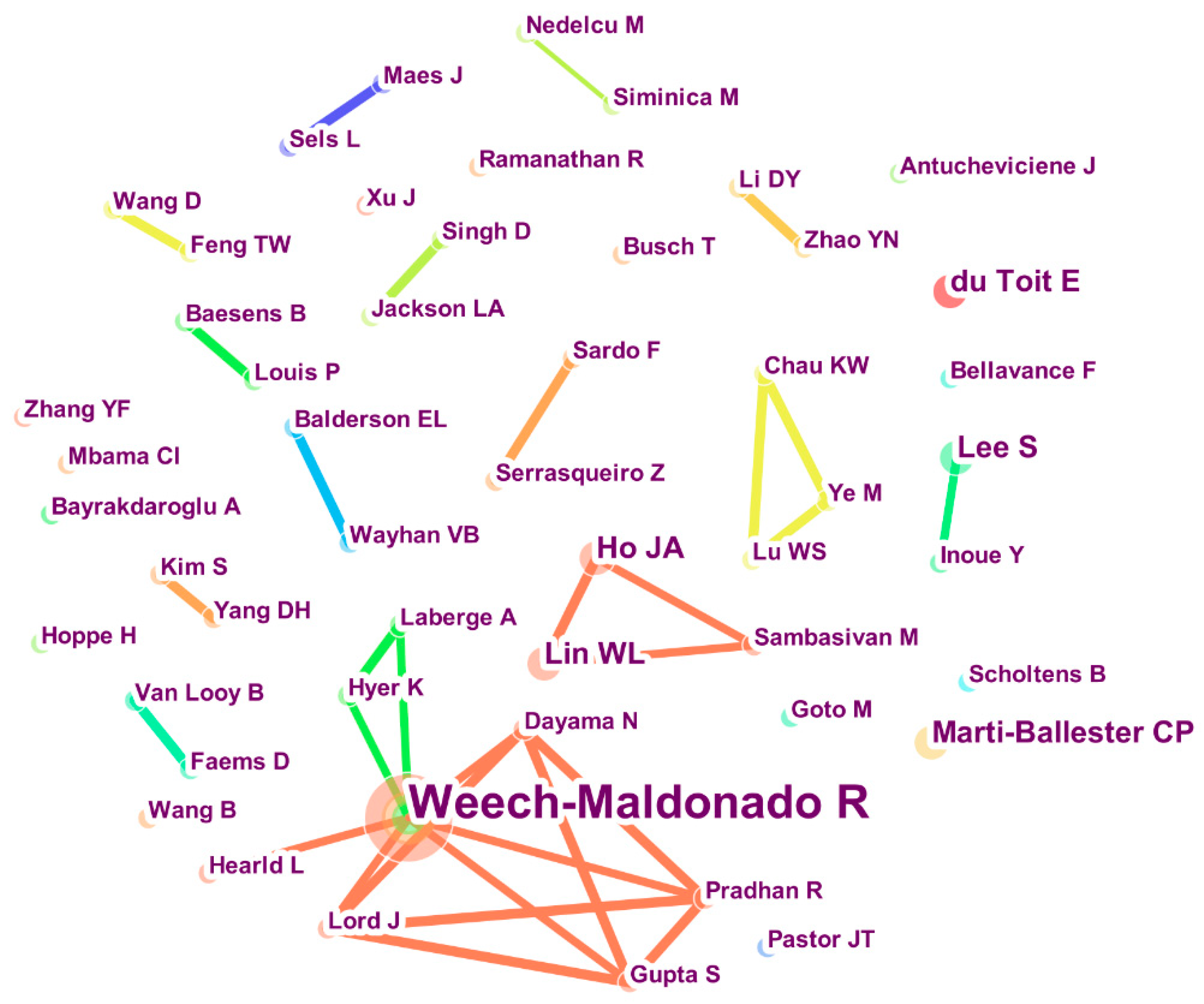

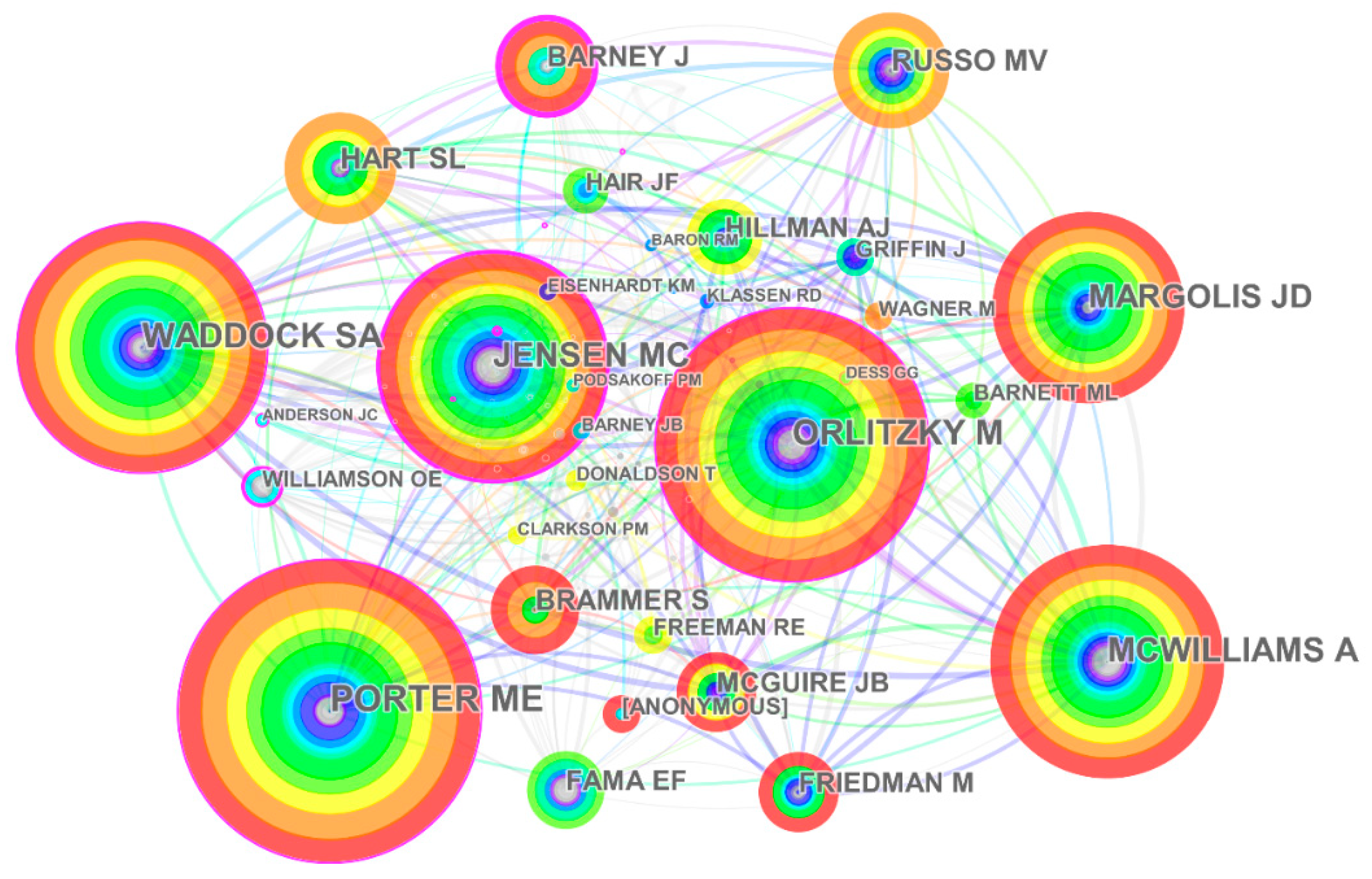

3.2. Mapping and Analysis of Authors and Cited Authors

3.3. Mapping and Analysis of Journals

3.4. Mapping and Analysis of Keywords

3.4.1. High-Frequency Keywords

3.4.2. Extraction of Financial Performance Based on Keywords

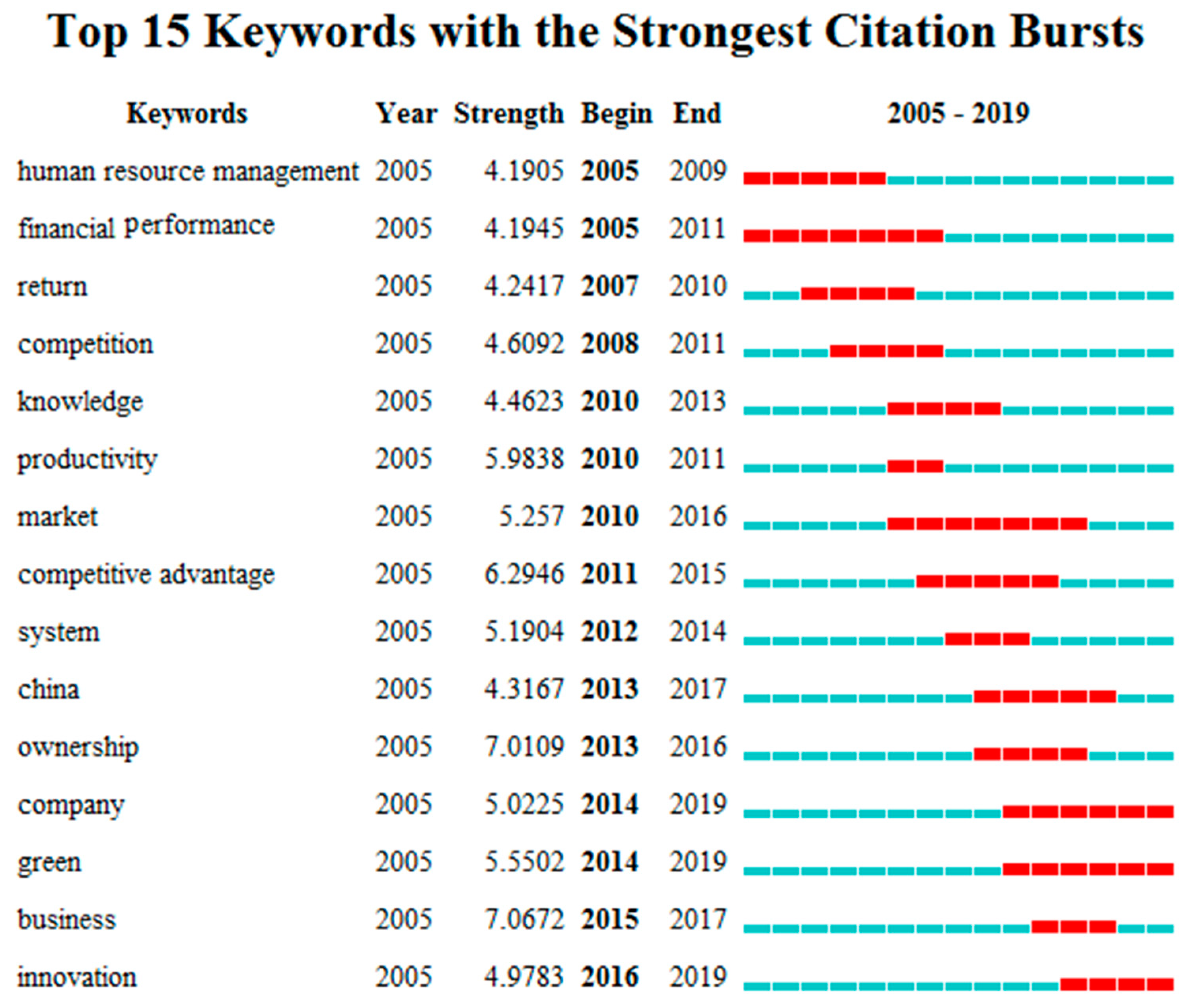

3.4.3. Theme Evolution Trend Based on Keywords

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Taylor, F.W. The Principles of Scientific Management; Harper & Brothers: New York, NY, USA, 1911. [Google Scholar]

- Johnson, H.T. Management Accounting in an Early Integrated Industrial: E. I. duPont de Nemours Powder Company, 1903–1912. Bus. Hist. Rev. 1975, 49, 184–204. [Google Scholar] [CrossRef]

- Beaver, W.; Kettler, P.; Scholes, M. The association between market determined and accounting determined risk measures. Account. Rev. 1970, 45, 654–682. [Google Scholar]

- Vernon, J.M. Market Structure and Industrial Performance; Allyn and Bacon: Boston, MA, USA, 1972. [Google Scholar]

- Dalton, D.R.; Todor, W.D.; Spendolini, M.J.; Fielding, G.J.; Porter, L.W. Organization structure and performance: A critical review. Acad. Manag. Rev. 1980, 5, 49–64. [Google Scholar] [CrossRef]

- Capon, N.; Jhon, U.; Farley, J.M.H. Corporate Financial Performance and the Role of Envirnoment, Strategy, and Organization; Columbia University Working Paper; Columbia University: New York, NY, USA, 1987. [Google Scholar]

- Gale, B.T.; Branch, B.S. Concentration versus market share: Which determines performance and why does it matter. Antitrust Bull. 1982, 27, 83. [Google Scholar]

- Capon, N.; Farley, J.U.; Hoenig, S. Determinants of financial performance: A meta-analysis. Manag. Sci. 1990, 36, 1143–1159. [Google Scholar] [CrossRef]

- Chandler, A. The Continental Bank Middle Market Roundtable. J. Appl. Corp. Financ. 1991, 4, 6–29. [Google Scholar]

- Stern, J.M.; Stewart, G.B., III; Chew, D.H. The EVA® financial management system. J. Appl. Corp. Financ. 1995, 8, 32–46. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Using the Balanced Scorecard as a Strategic Management System; Harvard Business Review: Boston, MA, USA, 1996. [Google Scholar]

- Lenz, R.T. ‘Determinants’ of organizational performance: An interdisciplinary review. Strateg. Manag. J. 1981, 2, 131–154. [Google Scholar] [CrossRef]

- White, R.E.; Hamermesh, R.C. Toward a model of business unit performance: An integrative approach. Acad. Manag. Rev. 1981, 6, 213–223. [Google Scholar] [CrossRef]

- Arlow, P.; Gannon, M.J. Social responsiveness, corporate structure, and economic performance. Acad. Manag. Rev. 1982, 7, 235–241. [Google Scholar] [CrossRef]

- Venkatraman, N.; Ramanujam, V. Measurement of business performance in strategy research: A comparison of approaches. Acad. Manag. Rev. 1986, 11, 801–814. [Google Scholar] [CrossRef]

- Zahra, S.A.; Pearce, J.A. Boards of directors and corporate financial performance: A review and integrative model. J. Manag. 1989, 15, 291–334. [Google Scholar] [CrossRef]

- Orlitzky, M.; Benjamin, J.D. Corporate social performance and firm risk: A meta-analytic review. Bus. Soc. 2001, 40, 369–396. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Callan, S.J.; Thomas, J.M. Corporate financial performance and corporate social performance: An update and reinvestigation. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 61–78. [Google Scholar] [CrossRef]

- Wang, Q.; Dou, J.; Jia, S. A meta-analytic review of corporate social responsibility and corporate financial performance: The moderating effect of contextual factors. Bus. Soc. 2016, 55, 1083–1121. [Google Scholar] [CrossRef]

- Otlet, P. Traité de Documentation: Le Livre Sur le Livre, Théorie et Pratique; Editiones Mundaneum: Bruxelles, Belgium, 1934. [Google Scholar]

- Pritchard, A. Statistical bibliography or bibliometrics. J. Doc. 1969, 25, 348–349. [Google Scholar]

- Chen, C. CiteSpace II: Detecting and visualizing emerging trends and transient patterns in scientific literature. J. Am. Soc. Inf. Sci. Technol. 2006, 57, 359–377. [Google Scholar] [CrossRef]

- Borgatti, S.P.; Everett, M.G.; Freeman, L.C. Ucinet for Windows: Software for social network analysis. Harvard MA Anal. Technol. 2002, 88. [Google Scholar]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Does it pay to be really good? Addressing the shape of the relationship between social and financial performance. Strateg. Manag. J. 2012, 33, 1304–1320. [Google Scholar] [CrossRef]

- Inoue, Y.; Lee, S. Effects of different dimensions of corporate social responsibility on corporate financial performance in tourism-related industries. Tour. Manag. 2011, 32, 790–804. [Google Scholar] [CrossRef]

- Flammer, C. Does corporate social responsibility lead to superior financial performance? A regression discontinuity approach. Manage. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Sofian, S.; Saeidi, P.; Saeidi, S.P.; Saaeidi, S.A. How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation, and customer satisfaction. J. Bus. Res. 2015, 68, 341–350. [Google Scholar] [CrossRef]

- Post, C.; Byron, K. Women on boards and firm financial performance: A meta-analysis. Acad. Manag. J. 2015, 58, 1546–1571. [Google Scholar] [CrossRef]

- Qiu, Y.; Shaukat, A.; Tharyan, R. Environmental and social disclosures: Link with corporate financial performance. Br. Account. Rev. 2016, 48, 102–116. [Google Scholar] [CrossRef]

- Lin, C.; Sanders, K.; Sun, J.; Shipton, H.; Mooi, E.A. From customer-oriented strategy to organizational financial performance: The role of human resource management and customer-linking capability. Br. J. Manag. 2016, 27, 21–37. [Google Scholar] [CrossRef]

- Herzallah, A.M.; Gutiérrez-Gutiérrez, L.; Munoz Rosas, J.F. Total quality management practices, competitive strategies and financial performance: The case of the Palestinian industrial SMEs. Total Qual. Manag. Bus. Excell. 2014, 25, 635–649. [Google Scholar] [CrossRef]

- Peng, C.-W.; Yang, M.-L. The effect of corporate social performance on financial performance: The moderating effect of ownership concentration. J. Bus. Ethics 2014, 123, 171–182. [Google Scholar] [CrossRef]

- Stewart, G. Supply-chain operations reference model (SCOR): The first cross-industry framework for integrated supply-chain management. Logist. Inf. Manag. 1997. [Google Scholar] [CrossRef]

- Pyke, D.; Johnson, M. Supply Chain Management: Integration and Globalization in the Age of eBusiness. SSRN Electron. J. 2001. [Google Scholar] [CrossRef]

- Huang, S.H.; Sheoran, S.K.; Keskar, H. Computer-assisted supply chain configuration based on supply chain operations reference (SCOR) model. Comput. Ind. Eng. 2005, 48, 377–394. [Google Scholar] [CrossRef]

- Flynn, B.; Wu, S.; Melnyk, S. Operational capabilities: Hidden in plain view. Bus. Horiz. 2010, 53, 247–256. [Google Scholar] [CrossRef]

- Torres, I.; Gutierrez Gutierrez, L.; Ruiz-Moreno, A. Boosting sustainability and financial performance: The role of supply chain controversies. Int. J. Prod. Res. 2018, 1–16. [Google Scholar] [CrossRef]

- Pomering, A.; Dolnicar, S. Assessing the Prerequisite of Successful CSR Implementation: Are Consumers Aware of CSR Initiatives? J. Bus. Ethics 2009, 85, 285–301. [Google Scholar] [CrossRef]

- Vanhamme, J.; Lindgreen, A.; Reast, J.; Popering, N. To Do Well by Doing Good: Improving Corporate Image Through Cause-Related Marketing. J. Bus. Ethics 2012, 109. [Google Scholar] [CrossRef]

- Heidary Dahooie, J.; Zavadskas, E.K.; Vanaki, A.S.; Firoozfar, H.R.; Lari, M.; Turskis, Z. A new evaluation model for corporate financial performance using integrated CCSD and FCM-ARAS approach. Econ. Res. Istraživanja 2019, 32, 1088–1113. [Google Scholar] [CrossRef]

- Miroshnychenko, I.; Barontini, R.; Testa, F. Green practices and financial performance: A global outlook. J. Clean. Prod. 2017, 147, 340–351. [Google Scholar] [CrossRef]

- Vu, M.-C.; Phan, T.; Le, N. Relationship between board ownership structure and firm financial performance in transitional economy: The Vietnamese transition. Res. Int. Bus. Financ. 2017, 45. [Google Scholar] [CrossRef]

- Liao, Z. Corporate culture, environmental innovation and financial performance. Bus. Strateg. Environ. 2018, 27. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Source | Web of Science; ACM; Scopus |

|---|---|

| Citation indexes | SCIE; SSCI; CPCI-S; CPCI-SSH |

| Years | January 2005 to September 2019 |

| Searching terms | Ti = (“financial performance” or “financial performance evaluation” or “financial efficiency”) |

| Sample size | 875 |

| Study(Frequency) | Research Question | Method/Data | Findings |

|---|---|---|---|

| Surroca et al. (543) | Taking a firm’s intangible resources in mediating the relationship between corporate responsibility and financial performance | A database comprising 599 companies from 28 countries | There is no direct relationship between corporate responsibility and financial performance, merely an indirect relationship that relies on the mediating effect of a firm’s intangible resources |

| Uotila et al. (303) | The relationship between exploration, exploitation, and financial performance | Analysis of S&P 500 Corporations | There is an inverted U-shaped relationship between the relative share of explorative orientation and financial performance. This relationship is positive, moderated by the R&D intensity of the industry in which the firm operates |

| Wang et al. (250) | The relationship between corporate philanthropy and corporate financial performance | Empirical analyses using data on Chinese firms listed on stock exchanges from 2001 to 2006 | The positive philanthropy–performance relationship is stronger for firms with greater public visibility and for those with better past performance, as philanthropy by these firms gains more positive stakeholder responses |

| Barnett et al. (249) | The relationship between social and financial performance | Studies contrasting analysis | Firms with low CSP have higher CFP than firms with moderate CSP, but firms with high CSP have the highest CFP |

| Saeidi et al. (213) | Considering sustainable competitive advantage, reputation, and customer satisfaction as three probable mediators in the relationship between corporate social responsibility (CSR) and firm performance | 205 Iranian manufacturing and consumer product firms | Only reputation and competitive advantage mediate the relationship between CSR and firm performance. A role for CSR in indirectly promoting firm performance through enhancing reputation and competitive advantage, while improving the level of customer satisfaction |

| Post et al. (202) | The relationship between women on boards and firm financial performance | A meta-analysis of 140 Studies | Female board representation is positively related to accounting returns and this relationship is more positive in countries with stronger shareholder protections, perhaps because shareholder protections motivate boards to use the different knowledge, experience, and values that each member brings. |

| Inoue et al. (198) | Effects of different dimensions of corporate social responsibility on corporate financial performance in tourism-related industries | none | Disaggregating CSR into five dimensions based on voluntary corporate activities for five primary stakeholder issues: (1) employee relations, (2) product quality, (3) community relations, (4) environmental issues, and (5) diversity issues. Finds that each dimension had a differential effect on both short-term and future profitability and that such financial impacts varied across the four industries |

| Flammer (160) | The effect of shareholder proposals related to corporate social responsibility (CSR) on financial performance | A regression discontinuity approach | The adoption of close call CSR proposals leads to positive announcement returns and superior accounting performance, implying that these proposals are value-enhancing. |

| Qiu et al. (83) | The link between a firm’s environmental and social disclosures and its profitability and market value | none | Firms with greater economic resources make more extensive disclosures that yield net positive economic benefits. |

| Lu et al. (68) | Review systematically quantifies the CSR–CFP link in a meta-analytic framework | 119 effect sizes from 42 studies | This study proposes that CSR in the developed world, with a relatively mature institutional system and efficient market mechanism, will be more visible than CSR in the developing world. The results show that the CSR–CFP relationship is stronger for firms from advanced economies than for firms from developing economies. |

| Total Publication | Countries/Territories | Total Publication | Countries/Territories |

|---|---|---|---|

| 309 | USA | 41 | TAIWAN |

| 87 | PEOPLE’S R CHINA | 34 | GERMANY |

| 67 | SPAIN | 27 | CANADA |

| 60 | ENGLAND | 25 | SOUTH KOREA |

| 51 | AUSTRALIA | 20 | NETHERLANDS |

| Author | Publications | Institution | Year of First Publication |

|---|---|---|---|

| Weech-Maldonado, R | 11 | Univ Alabama Birmingham | 2012 |

| Lee, S | 6 | Penn State Univ | 2011 |

| Menachemi, N | 5 | Univ Alabama Birmingham | 2006 |

| Pink, GH | 5 | Univ N Carolina | 2007 |

| du Toit, E | 4 | Univ Pretoria | 2007 |

| Earnhart, D | 4 | Univ Kansas | 2006 |

| Goto, M | 4 | Cent Res Inst Elect Power Ind | 2009 |

| Hyer, K | 4 | Univ Alabama Birmingham | 2012 |

| Marti-Ballester, CP | 4 | Univ Autonoma Barcelona | 2015 |

| Pradhan, R | 4 | Univ Arkansas Med Sci | 2012 |

| Przychodzen, J | 4 | Univ Deusto | 2015 |

| Przychodzen, W | 4 | Univ Deusto | 2015 |

| Scholtens, B | 4 | Univ Groningen | 2008 |

| Siminica, M | 4 | Univ Craiova | 2015 |

| Singal, M | 4 | Virginia Tech | 2013 |

| Wang, D | 4 | Monash Univ | 2015 |

| Wang, HL | 4 | Hong Kong Univ Sci & Technol | 2008 |

| Wang, YJ | 4 | Lan Yang Inst Technol | 2008 |

| Yu, WT | 4 | Univ E Anglia | 2013 |

| Cited Author | Frequency | Cited Author | Frequency | Cited Author | Frequency |

|---|---|---|---|---|---|

| Porter ME | 185 | Barney J | 58 | Freeman RE | 24 |

| Orlitzky M | 168 | Brammer S | 55 | Barnett ML | 23 |

| Waddock SA | 155 | Friedman M | 52 | Williamson OE | 22 |

| Mcwilliams A | 146 | Fama EF | 51 | Wagner M | 17 |

| Jensen MC | 142 | Mcguire JB | 51 | Donaldson T | 13 |

| Margolis JD | 121 | Hillman AJ | 48 | Clarkson PM | 12 |

| Russo MV | 74 | Hair JF | 29 | Eisenhardt KM | 11 |

| Hart SL | 69 | Griffin J | 25 | Klassen RD | 11 |

| Sr. No. | Journals | Publications |

|---|---|---|

| 1 | Sustainability | 44 |

| 2 | Journal of Business Ethics | 34 |

| 3 | Journal of Cleaner Production | 34 |

| 4 | Business Strategy and the Environment | 18 |

| 5 | Journal of Business Research | 16 |

| 6 | International Journal of Production Economics | 15 |

| 7 | Corporate Social Responsibility and Environmental Management | 14 |

| 8 | Total Quality Management & Business Excellence | 14 |

| 9 | Health Care Management Review | 11 |

| 10 | Journal of Operations Management | 10 |

| 11 | Strategic Management Journal | 10 |

| Journal | Frequency | Editor in Chief | Scope |

|---|---|---|---|

| Strategic Management Journal | 2052 | Sendil Ethiraj | The journal publishes original material concerned with all aspects of strategic management. |

| The Academy of Management Journal | 1705 | Guclu Atinc | AMJ is ranked among the top five most influential and frequently cited management journals, publishing original ideas, theories, empirical testing. |

| Journal of Business Ethics | 1583 | R. Edward Freeman | The journal only publishes original articles from a wide variety of methodological and disciplinary perspectives concerning ethical issues related to business that bring something new or unique to the discourse in their field. |

| Academy of Management Review | 1307 | Jay Barney | The articles are often grounded in “normal science disciplines” of economics, psychology, sociology, or social psychology, as well as nontraditional perspectives, such as the humanities. |

| Journal of Operations Management | 757 | Suzanne de Treville | General topic area: Operations management in process, manufacturing, and service organizations; operations strategy and policy; product and service design and development; technology management for operations; multi-site operations management; capacity planning and analysis; operations planning, scheduling and control; project management; human resource management for operations, etc. |

| Journal of Marketing | 748 | V. Kumar | Studies which can lead in the development, dissemination, and implementation of marketing concepts, practice, and information; and probe and promote the use of marketing concepts by business, not-for-profit, and other institutions for the betterment of society. |

| Journal of Management | 718 | David G. Allen | The journal publishes original scholarly articles related to the study of management and organization from any area within the domain of management: organizational behavior, organizational theory; human resources management; business strategy and theory; internationalization; interdisciplinary, including both theoretical and empirical approaches. |

| Journal of Financial Economics | 698 | G. William Schwert | The journal is a peer-reviewed academic journal covering theoretical and empirical topics in financial economics. |

| Management Science | 623 | David Simchi-Levi | The journal scope includes articles that address management issues with tools from foundational fields such as computer science, economics, mathematics, operations research, political science, psychology, sociology, and statistics, as well as cross-functional, multidisciplinary research that reflects the diversity of the management science professions. |

| The Journal of Finance | 576 | Stefan Nagel | The journal publishes leading research across all the major fields of financial research. |

| Number | Keywords | Frequency | Number | Keywords | Frequency |

|---|---|---|---|---|---|

| 1 | financial performance | 334 | 25 | corporate sustainability | 9 |

| 2 | corporate social responsibility | 89 | 26 | event study | 9 |

| 3 | corporate financial performance | 67 | 27 | nursing homes | 9 |

| 4 | firm performance | 35 | 28 | SMEs | 9 |

| 5 | corporate governance | 33 | 29 | endogeneity | 8 |

| 6 | corporate social performance | 31 | 30 | manufacturing | 8 |

| 7 | performance | 29 | 31 | quality management | 8 |

| 8 | environmental performance | 26 | 32 | stakeholder management | 8 |

| 9 | sustainable development | 25 | 33 | Tobin’s q | 8 |

| 10 | China | 21 | 34 | data envelopment analysis | 7 |

| 11 | profitability | 18 | 35 | emerging markets | 7 |

| 12 | sustainability | 16 | 36 | hospitals | 7 |

| 13 | supply chain management | 15 | 37 | microfinance | 7 |

| 14 | intellectual capital | 14 | 38 | operational performance | 7 |

| 15 | meta-analysis | 14 | 39 | ownership | 7 |

| 16 | environmental management | 13 | 40 | panel data | 7 |

| 17 | innovation | 13 | 41 | social responsibility | 7 |

| 18 | stakeholder theory | 13 | 42 | stakeholder engagement | 7 |

| 19 | customer satisfaction | 12 | 43 | board composition | 6 |

| 20 | corporate environmental performance | 11 | 44 | disclosure | 6 |

| 21 | resource-based view | 11 | 45 | family firms | 6 |

| 22 | financial efficiency | 10 | 46 | information technology | 6 |

| 23 | ownership structure | 10 | 47 | social performance | 6 |

| 24 | agency theory | 9 | 48 | stakeholders | 6 |

| Degree | Betweenness | Closeness | |||

|---|---|---|---|---|---|

| Nodes | Degree | Nodes | Degree | Nodes | Degree |

| financial performance | 46 | financial performance | 480.13 | hospitals | 94 |

| corporate social responsibility | 30 | corporate social responsibility | 95.71 | nursing homes | 93 |

| corporate financial performance | 22 | firm performance | 46.86 | event study | 91 |

| firm performance | 20 | corporate governance | 37.22 | intellectual capital | 91 |

| corporate governance | 20 | corporate financial performance | 35.75 | financial efficiency | 90 |

| sustainable development | 17 | environmental performance | 24.59 | operational performance | 90 |

| corporate social performance | 16 | sustainable development | 21.53 | quality management | 90 |

| environmental performance | 15 | China | 17.69 | innovation | 89 |

| performance | 14 | performance | 17.50 | disclosure | 89 |

| China | 14 | manufacturing | 12.87 | information technology | 89 |

| Cluster-ID | Clusters | Main Including Labels |

|---|---|---|

| #0 | corporate atmosphere | human resource management, care, perception, organizational climate, cost, customer satisfaction |

| #1 | ownership concentration | ownership structure, corporate performance, small business, profitability, innovation |

| #2 | diversity assessment | strategic management, competitive advantage, shareholder value, diversity, international diversification, personality |

| #3 | supply chain management | supply chain management, antecedent, product development, linkage |

| #4 | the corporate financial performance indicator system | corporate social responsibility, corporate financial performance, empirical analysis, time series |

| #5 | financial performance quality management framework | total quality management, organizational performance, market orientation, financial performance, award |

| #6 | stakeholder theory | Ownership, social responsibility, perspective, china, stakeholder theory |

| #7 | corporate social responsibility | Business, director, market, contract, acquisition, valuation |

| #8 | risk and decision-making | Earning, quality, trust, determinant, risk, choice |

| #9 | environmental management | Environment, impact, health care, pollution benefit, green, certification |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xue, W.; Li, H.; Ali, R.; Rehman, R.U. Knowledge Mapping of Corporate Financial Performance Research: A Visual Analysis Using Cite Space and Ucinet. Sustainability 2020, 12, 3554. https://doi.org/10.3390/su12093554

Xue W, Li H, Ali R, Rehman RU. Knowledge Mapping of Corporate Financial Performance Research: A Visual Analysis Using Cite Space and Ucinet. Sustainability. 2020; 12(9):3554. https://doi.org/10.3390/su12093554

Chicago/Turabian StyleXue, Wuzhao, Hua Li, Rizwan Ali, and Ramiz Ur Rehman. 2020. "Knowledge Mapping of Corporate Financial Performance Research: A Visual Analysis Using Cite Space and Ucinet" Sustainability 12, no. 9: 3554. https://doi.org/10.3390/su12093554

APA StyleXue, W., Li, H., Ali, R., & Rehman, R. U. (2020). Knowledge Mapping of Corporate Financial Performance Research: A Visual Analysis Using Cite Space and Ucinet. Sustainability, 12(9), 3554. https://doi.org/10.3390/su12093554