The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry

Abstract

1. Introduction

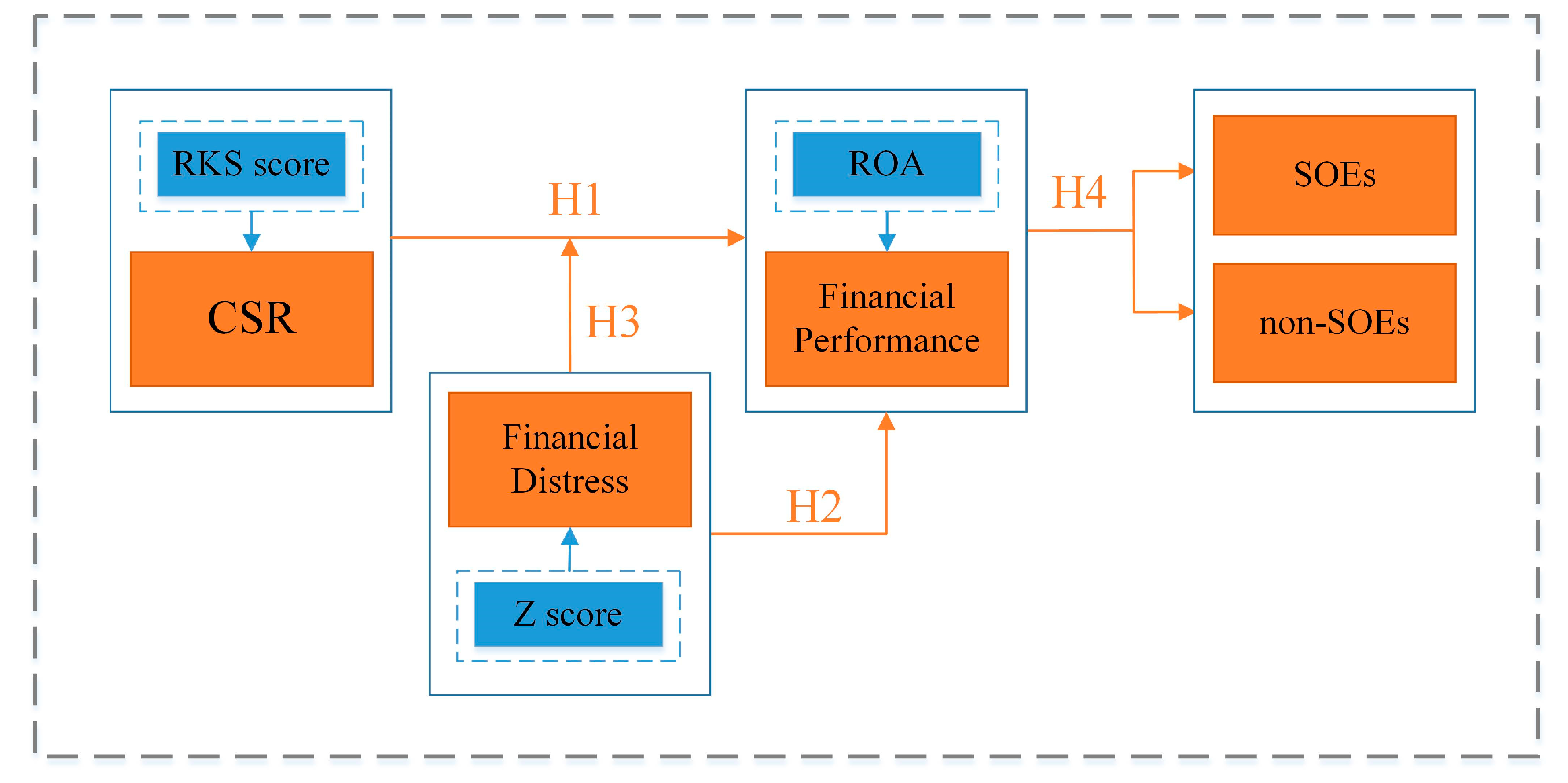

2. Literature Reviews and Hypotheses

2.1. CSR in China

2.2. Relationship between CSR and CFP

2.3. Relationship between Financial Distress and CFP

3. Measurement of Variance and Model Construction

3.1. Measurement of CSR

3.2. Measurement of CFP

3.3. Measurement of Financial Distress

3.4. Model Construction

4. Sample and Data

5. Empirical Results

5.1. Regression Results

5.2. Addition Test of SOEs and Non-SOEs

5.3. Robustness Tests

5.4. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Jamali, D. The case for strategic corporate social responsibility in developing countries. Bus. Soc. Rev. 2007, 112, 1–27. [Google Scholar] [CrossRef]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does it pay to be good. And does it matter? A meta-analysis of the relationship between corporate social and financial performance. SSRN Electron. J. 2009. [Google Scholar] [CrossRef]

- Wang, K.; Sewon, O.; Claiborne, M.C. Determinants and consequences of voluntary disclosure in an emerging market: Evidence from China. J. Int. Account. Audit. Tax. 2008, 17, 14–30. [Google Scholar] [CrossRef]

- Freeman, R.E. The politics of stakeholder theory: Some future directions. Bus. Ethics Q. 1994, 4, 409–421. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A. Corporate social responsibility as a conflict between shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Harrison, J.S.; Wicks, A.C. Stakeholder theory, value, and firm performance. Bus. Ethics Q. 2013, 23, 97–124. [Google Scholar] [CrossRef]

- Connelly, B.L.; Certo, S.T.; Ireland, R.D.; Reutzel, C.R. Signaling theory: A review and assessment. J. Manag. 2010, 37, 39–67. [Google Scholar] [CrossRef]

- Bae, S.M.; Masud, A.K.; Kim, J.D. A Cross-country investigation of corporate governance and corporate sustainability disclosure: A signaling theory perspective. Sustainability 2018, 10, 2611. [Google Scholar] [CrossRef]

- Uyar, A.; Karaman, A.S.; Kılıç, M. Is corporate social responsibility reporting a tool of signaling or greenwashing? Evidence from the worldwide logistics sector. J. Clean. Prod. 2020, 253, 119997. [Google Scholar] [CrossRef]

- Nguyen, P.-A.; Kecskés, A.; Mansi, S. Does corporate social responsibility create shareholder value? The importance of long-term investors. J. Bank. Financ. 2020, 112, 105217. [Google Scholar] [CrossRef]

- Lu, W.; Chau, K.W.; Wang, H.; Pan, W. A decade’s debate on the nexus between corporate social and corporate financial performance: A critical review of empirical studies 2002–2011. J. Clean. Prod. 2014, 79, 195–206. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Rupp, D.E.; Williams, C.A.; Ganapathi, J. Putting the S back in corporate social responsibility: A multilevel theory of social change in organizations. Acad. Manag. Rev. 2007, 32, 836–863. [Google Scholar] [CrossRef]

- Capon, N.; Farley, J.U.; Hoenig, S. Determinants of financial performance: A meta-analysis. Manag. Sci. 1990, 36, 1143–1159. [Google Scholar] [CrossRef]

- Männasoo, K.; Maripuu, P.; Hazak, A. Investments, credit, and corporate financial distress: Evidence from Central and Eastern Europe. Emerg. Mark. Financ. Trade 2018, 54, 677–689. [Google Scholar] [CrossRef]

- Feng, L.; Zhang, X.; Zhou, K. Current problems in China’s manufacturing and countermeasures for industry 4.0. EURASIP J. Wirel. Commun. Netw. 2018, 2018, 90. [Google Scholar] [CrossRef]

- Cheng, S.; Lin, K.Z.; Wong, W. Corporate social responsibility reporting and firm performance: Evidence from China. J. Manag. Gov. 2015, 20, 503–523. [Google Scholar] [CrossRef]

- Lin, L.; Hung, P.-H.; Chou, D.-W.; Lai, C.W. Financial performance and corporate social responsibility: Empirical evidence from Taiwan. Asia Pac. Manag. Rev. 2019, 24, 61–71. [Google Scholar] [CrossRef]

- Kao, E.H.C.; Yeh, C.-C.; Wang, L.-H.; Fung, H.-G. The relationship between CSR and performance: Evidence in China. Pac. Basin Financ. J. 2018, 51, 155–170. [Google Scholar] [CrossRef]

- Schmidpeter, R.; Stehr, C. A history of research on CSR in China: The obstacles for the implementation of CSR in emerging markets. In Sustainable Development and CSR in China: A Multi-Perspective Approach; Schmidpeter, R., Lu, H., Stehr, C., Huang, H., Eds.; Springer International Publishing: Cham, Switzerland, 2015; pp. 1–11. [Google Scholar]

- Marquis, C.P.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef]

- Kuo, L.; Yeh, C.-C.; Yu, H.-C. Disclosure of corporate social responsibility and environmental management: Evidence from China. Corp. Soc. Responsib. Environ. Manag. 2011, 19, 273–287. [Google Scholar] [CrossRef]

- Gong, Y.; Ho, K.-C. Does corporate social responsibility matter for corporate stability? Evidence from China. Qual. Quant. 2017, 52, 2291–2319. [Google Scholar] [CrossRef]

- Timothy, M.D. Is the socially responsible corporation a myth? The good, the bad, and the ugly of corporate social responsibility. Acad. Manag. Persp. 2009, 23. [Google Scholar] [CrossRef]

- Scholtens, B. A note on the interaction between corporate social responsibility and financial performance. Ecol. Econ. 2008, 68, 46–55. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance–financial performance link. Strat. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Quéré, B.P.; Nouyrigat, G.; Baker, C.R. A bi-directional examination of the relationship between corporate social responsibility ratings and company financial performance in the European context. J. Bus. Ethics 2015, 148, 527–544. [Google Scholar] [CrossRef]

- Duque-Grisales, E.; Aguilera-Caracuel, J. Environmental, Social and Governance (ESG) scores and financial performance of multilatinas: Moderating effects of geographic international diversification and financial slack. J. Bus. Ethics 2019, 1–20. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. Corporate governance and firm value: The impact of corporate social responsibility. J. Bus. Ethics 2011, 103, 351–383. [Google Scholar] [CrossRef]

- Adegbite, E.; Guney, Y.; Kwabi, F.; Tahir, S. Financial and corporate social performance in the UK listed firms: The relevance of non-linearity and lag effects. Rev. Quant. Financ. Account. 2018, 52, 105–158. [Google Scholar] [CrossRef]

- Inekwe, J.; Jin, Y.; Valenzuela, M.R. The effects of financial distress: Evidence from US GDP growth. Econ. Model. 2018, 72, 8–21. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure; Springer: Berlin/Heidelberg, Germany, 1979; pp. 163–231. [Google Scholar]

- Jandik, T.; Makhija, A.K. Debt, debt structure and corporate performance after unsuccessful takeovers: Evidence from targets that remain independent. J. Corp. Financ. 2005, 11, 882–914. [Google Scholar] [CrossRef]

- Agostini, M. Corporate Financial Distress: A Roadmap of the Academic Literature Concerning its Definition and Tools of Evaluation; Springer: Berlin/Heidelberg, Germany, 2018; pp. 5–47. [Google Scholar]

- Tan, T.K. Financial distress and firm performance: Evidence from the Asian financial crisis. J. Financ. Account. 2012, 11, 1. [Google Scholar]

- Bouslah, K.; Kryzanowski, L.; M’Zali, B. Social performance and firm risk: Impact of the financial crisis. J. Bus. Ethics 2016, 149, 643–669. [Google Scholar] [CrossRef] [PubMed]

- Goss, A.; Roberts, G.S. The impact of corporate social responsibility on the cost of bank loans. J. Bank. Financ. 2011, 35, 1794–1810. [Google Scholar] [CrossRef]

- Oikonomou, I.; Brooks, C.; Pavelin, S. The impact of corporate social performance on financial risk and utility: A longitudinal analysis. Financ. Manag. 2012, 41, 483–515. [Google Scholar] [CrossRef]

- Chollet, P.; Sandwidi, B.W. CSR engagement and financial risk: A virtuous circle? International evidence. Glob. Financ. J. 2018, 38, 65–81. [Google Scholar] [CrossRef]

- See, G. Harmonious society and Chinese CSR: Is there really a link? J. Bus. Ethics 2008, 89, 1–22. [Google Scholar] [CrossRef]

- Li, W.; Zhang, R. Corporate social responsibility, ownership structure, and political interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- He, Y.; Chiu, Y.-H.; Zhang, B. The impact of corporate governance on state-owned and non-state-owned firms efficiency in China. N. Am. J. Econ. Financ. 2015, 33, 252–277. [Google Scholar] [CrossRef]

- Chang, L.; Li, W.; Lu, X. Government engagement, environmental policy, and environmental performance: Evidence from the most polluting Chinese listed firms. Bus. Strat. Environ. 2013, 24, 1–19. [Google Scholar] [CrossRef]

- Ma, L.; Liang, J. The effects of firm ownership and affiliation on government’s target setting on energy conservation in China. J. Clean. Prod. 2018, 199, 459–465. [Google Scholar] [CrossRef]

- Makni, R.; Francoeur, C.; Bellavance, F. Causality between corporate social performance and financial performance: Evidence from Canadian firms. J. Bus. Ethics 2008, 89, 409–422. [Google Scholar] [CrossRef]

- Cho, S.Y.; Lee, C.; Pfeiffer, R.J. Corporate social responsibility performance and information asymmetry. J. Acc. Public Policy 2013, 32, 71–83. [Google Scholar] [CrossRef]

- Du, X.; Chang, Y.; Zeng, Q.; Du, Y.; Pei, H. Corporate environmental responsibility (CER) weakness, media coverage, and corporate philanthropy: Evidence from China. Asia Pac. J. Manag. 2015, 33, 551–581. [Google Scholar] [CrossRef]

- McGuinness, P.B.; Vieito, J.P.; Wang, M. The role of board gender and foreign ownership in the CSR performance of Chinese listed firms. J. Corp. Financ. 2017, 42, 75–99. [Google Scholar] [CrossRef]

- Fischer, T.M.; Sawczyn, A.A. The relationship between corporate social performance and corporate financial performance and the role of innovation: Evidence from German listed firms. J. Manag. Control 2013, 24, 27–52. [Google Scholar] [CrossRef]

- Jacobs, B.; Kraude, R.; Narayanan, S. Operational productivity, corporate social performance, financial performance, and risk in manufacturing firms. Prod. Oper. Manag. 2016, 25, 2065–2085. [Google Scholar] [CrossRef]

- Petitjean, M. Eco-friendly policies and financial performance: Was the financial crisis a game changer for large US companies? Energy Econ. 2019, 80, 502–511. [Google Scholar] [CrossRef]

- O’Sullivan, J.; Mamun, A.; Hassan, M.K. The relationship between board characteristics and performance of bank holding companies: Before and during the financial crisis. J. Econ. Financ. 2015, 40, 438–471. [Google Scholar] [CrossRef]

- Esteban-Sanchez, P.; de La Cuesta-Gonzalez, M.; Paredes-Gazquez, J.D. Corporate social performance and its relation with corporate financial performance: International evidence in the banking industry. J. Clean. Prod. 2017, 162, 1102–1110. [Google Scholar] [CrossRef]

- Liu, T.; Zhang, Y.; Liang, D. Can ownership structure improve environmental performance in Chinese manufacturing firms? The moderating effect of financial performance. J. Clean. Prod. 2019, 225, 58–71. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Definition | ||

|---|---|---|

| Dependent variable | ROA | Return on assets. |

| Independent variable | CSR | Corporate social responsibility. |

| Z | Financial distress. | |

| Control variables | Lev | Asset-liability ratio. |

| Growth | Operating revenue growth rate. | |

| CR | Current ratio. | |

| CASH | Cash ratio. | |

| SLACK | Redundant resources. |

| Code | Description of the Industry | Number of Firms |

|---|---|---|

| C13 | Agricultural and sideline food processing. | 5 |

| C14 | Food manufacturing. | 9 |

| C15 | Wine, beverage, and refined tea manufacturing. | 17 |

| C17 | Textile industry. | 6 |

| C18 | Textile and garment industry. | 1 |

| C19 | Leather, fur, feathers, and their products and footwear. | 1 |

| C21 | Furniture manufacturing. | 2 |

| C22 | Paper and paper products industry. | 9 |

| C23 | The printing and recording media reproduction industry. | 1 |

| C25 | Petroleum processing, coking, and nuclear fuel processing industries. | 10 |

| C26 | Chemical raw material and chemical product manufacturing. | 33 |

| C27 | Pharmaceutical manufacturing. | 29 |

| C28 | Chemical fiber manufacturing. | 4 |

| C29 | Rubber and plastic products manufacturing. | 6 |

| C30 | Non-metallic mineral products industry. | 20 |

| C31 | Ferrous metal smelting and rolling industry. | 17 |

| C32 | Non-ferrous metal smelting and rolling processing industry. | 31 |

| C33 | Metal products industry. | 4 |

| C34 | General equipment manufacturing. | 15 |

| C35 | Special equipment manufacturing. | 26 |

| C36 | Automobile manufacturing. | 10 |

| C37 | Manufacturing of railway, shipping, aerospace, and other transport equipment. | 17 |

| C38 | Electrical machinery and equipment manufacturing. | 21 |

| C39 | Manufacturing of computers, communications, and other electronic equipment. | 45 |

| C40 | Instrument and meter manufacturing. | 2 |

| Year | ||||||

|---|---|---|---|---|---|---|

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| Number of samples | 234 | 242 | 236 | 251 | 240 | 242 |

| % privately control | 24% | 24% | 25% | 24% | 24% | 24% |

| % state owned | 76% | 76% | 75% | 76% | 76% | 76% |

| Variables | Obs | Min | Max | Mean | Std. |

|---|---|---|---|---|---|

| CSR | 1445 | 22.80 | 89.00 | 40.74 | 11.11 |

| ROA | 1445 | −0.59 | 0.34 | 0.03 | 0.07 |

| Z | 1445 | −1.82 | 64.57 | 4.46 | 4.98 |

| LEV | 1445 | 0.04 | 1.35 | 0.51 | 0.20 |

| GROWTH | 1445 | −1.72 | 37.26 | 0.28 | 1.29 |

| CR | 1445 | 0.09 | 21.72 | 1.75 | 1.73 |

| CASH | 1445 | 0.00 | 11.04 | 0.50 | 0.80 |

| SLACK | 1445 | 0.00 | 0.63 | 0.16 | 0.11 |

| ROA | CSR | Z | LEV | GROWTH | CR | CASH | SLACK | |

|---|---|---|---|---|---|---|---|---|

| ROA | 1 | |||||||

| CSR | 0.126 ** (0.000) | 1 | ||||||

| Z | 0.307 ** (0.001) | −0.088 * (0.001) | 1 | |||||

| LEV | 0.470 ** (0.000) | 0.065 ** (0.014) | 0.647 ** (0.000) | 1 | ||||

| GROWTH | −0.007 (0.798) | −0.064 (0.016) | 0.23 ** (0.000) | −0.031 (0.245) | 1 | |||

| CR | −0.206 ** (0.000) | 0.084 * (0.001) | 0.759 ** (0.000) | −0.618 ** (0.000) | 0.152 ** (0.000) | 1 | ||

| CASH | −0.222 ** (0.000) | −0.022 (0.407) | 0.654 ** (0.000) | 0.533 ** (0.000) | 0.046 (0.082) | 0.813 ** (0.000) | 1 | |

| SLACK | 0.249 (0.000) | 0.059 * (0.026) | 0.315 ** (0.033) | −0.231 ** (0.000) | −0.005 (0.845) | 0.337 ** (0.000) | 0.566 ** (0.000) | 1 |

| ROA | ROA | ROA | |

|---|---|---|---|

| Z | 0.001636 *** (3.19) | ||

| CSR | 0.000835 *** (6.14) | 0.000610 *** (3.99) | |

| Z * CSR | 0.0000663 *** (4.98) | ||

| LEV | −0.189454 *** (−1.78) | −0.175630 *** (−16.63) | −0.168616 *** (−16.02) |

| GROWTH | 0.000487 (0.41) | −0.000751 (−0.61) | −0.000463 (−0.39) |

| CR | −0.004984 *** (−2.95) | −0.007944 *** (−4.32) | −0.007898 *** (−4.45) |

| CASH | −0.00636 * (−1.76) | −0.006985 * (−1.77) | −0.008492 ** (−2.21) |

| SLACK | 0.124342 *** (7.20) | 0.127508 *** (7.31) | 0.120164 *** (7.00) |

| c | 0.085587 *** (9.75) | 0.110319 *** (14.78) | 0.079318 *** (9.02) |

| R2 | 28.40 | 27.04 | 29.62 |

| ROA | ROA | ROA | |

|---|---|---|---|

| ROA(−1) | 0.051833 * (1.78) | 0.036528 (1.13) | 0.031554 (1.23) |

| Z | 0.001550 *** (6.51) | ||

| CSR | 0.000633 * (1.73) | 0.000391 (1.24) | |

| Z * CSR | 0.0000431 *** (6.81) | ||

| SLACK | 0.108036 *** (3.04) | 0.094030 *** (2.65) | 0.084684 *** (2.65) |

| LEV | −0.192969 *** (−6.52) | −0.219352 *** (−6.84) | −0.184631 *** (−7.00) |

| GROWTH | 0.011206 *** (2.70) | 0.010059 *** (3.11) | 0.011686 *** (3.71) |

| CASH | −0.004360 ** (−2.29) | −0.008017 *** (−3.24) | −0.006718 *** (−3.68) |

| CR | 0.002052 ** (2.25) | 0.000902 (−0.76) | 0.119127 (0.10) |

| AR(2) | 0.45 | 0.49 | 0.36 |

| Subsample of SOEs | Subsample of Non-SOEs | ||||||

|---|---|---|---|---|---|---|---|

| ROA | ROA | ROA | ROA | ROA | ROA | ||

| Z | 0.001008 * (1.72) | Z | 0.002827 *** (2.82) | ||||

| CSR | 0.000995 *** (6.40) | 0.000808 *** (4.96) | CSR | 0.000746 *** (2.77) | 0.000481 * (1.72) | ||

| Z * CSR | 0.0000563 ***(3.69) | Z * CSR | 0.0000803 *** (3.16) | ||||

| LEV | −0.180429 *** (−17.31) | −0.171356 *** (−14.63) | −0.161199 *** (−13.78) | LEV | −0.176687 *** (−7.32) | −0.151143 *** (−5.97) | −0.151784 *** (−6.05) |

| GROWTH | 9.15 ** (0.078) | 0.001095 ** (−0.86) | −0.001016 ** (−0.84) | GROWTH | 0.015026 ** (2.38) | 0.01591 ** (2.51) | 0.01713 *** (2.73) |

| CR | −0.004067 * (−1.82) | −0.006388 *** (−2.66) | −0.006306 *** (−2.74) | CR | −0.018418 *** (−3.06) | −0.025898 *** (−4.01) | −0.024732 *** (−3.94) |

| CASH | 0.008810 ** (−2.22) | −0.009172 ** (−2.26) | −0.011121 *** (−2.79) | CASH | 0.015153 (1.03) | 0.013142 ** (0.89) | 0.012502 (0.86) |

| SLACK | −0.145391 *** (7.91) | 0.151733 *** (8.12) | 0.140534 *** (7.67) | SLACK | 0.022083 (0.48) | 0.05899 *** (1.25) | 0.051937 (1.12) |

| c | 0.063469 *** (6.60) | 0.098077 *** (12.09) | 0.056495 *** (5.80) | c | 0.115678 *** (6.53) | 0.122965 *** (7.52) | 0.103635 *** (5.79) |

| R2 | 31.19 | 28.81 | 32.04 | R2 | 22.20 | 22.26 | 24.43 |

| ROA | ROA | ROA | |

|---|---|---|---|

| Z | 0.001975 ** (2.45) | ||

| CSR | 0.000625 *** (3.12) | 0.000289 (1.35) | |

| Z * CSR | 9.07 *** (4.14) | ||

| LEV | −0.172577 *** (−11.54) | −0.150618 *** (−9.1) | −0.138578 *** (−8.21) |

| GROWTH | 0.000974 (0.49) | 0.000158 (0.08) | 0.000665 (0.34) |

| CR | −0.001366 (−0.38) | −0.006446 (−1.62) | −0.008123 ** (−2.07) |

| CASH | −0.009584 (−1.26) | −0.004128 (−0.53) | −0.001574 (−0.2) |

| SLACK | 0.135023 *** (5.65) | 0.125659 *** (5.16) | 0.11451 *** (4.75) |

| c | 0.080803 *** (6.14) | 0.093791 *** (8.08) | 0.072212 *** (5.49) |

| R2 | 27.15 | 26.70 | 29.16 |

| ROA | ROA | ROA | |

|---|---|---|---|

| Z | 0.001783 ** (3.19) | ||

| CSR | 0.000977 *** (4.72) | 0.000731 *** (3.35) | |

| Z * CSR | 0.0000693 *** (3.37) | ||

| LEV | −0.174023 *** (−11.14) | −0.157773 *** (−9.38) | −0.153876 *** (−9.27) |

| GROWTH | −0.0000723 (−0.05) | −0.001653 (−0.99) | −0.001436 (−0.93) |

| CR | −0.005143 ** (−2.3) | −0.008664 *** (−3.41) | −0.008335 *** (−3.45) |

| CASH | −0.002361 * (−0.4) | −0.001177 (−0.2) | −0.005407 (−0.92) |

| SLACK | 0.083492 *** (3.07) | 0.082441 *** (2.98) | 0.081329 *** (3.01) |

| c | 0.075141 *** (5.55) | 0.106561 *** (9.33) | 0.070954 *** (5.26) |

| R2 | 23.93 | 21.73 | 25.34 |

| ROAt | ROAt | ROAt | |

|---|---|---|---|

| Zt−1 | 0.001699 *** (2.67) | ||

| CSRt-1 | 0.000714 *** (4.23) | 0.000479 *** (2.73) | |

| Z * CSRt-1 | 0.0000708 *** (4.34) | ||

| LEVt−1 | −0.132277 *** (−11.22) | −0.116898 *** (−9.08) | −0.10915 *** (−8.49) |

| GROWTHt−1 | 0.002394 (0.93) | 0.00211 (0.82) | 0.002603 (1.02) |

| CRt-1 | −0.002472 (−1.18) | −0.005184 ** (−2.32) | −0.005246 ** (−2.41) |

| CASHt-1 | −0.005076 (−1.08) | −0.005736 (−1.21) | −0.007391 (−1.58) |

| SLACKt-1 | 0.093125 *** (4.49) | 0.096336 *** (4.63) | 0.088342 *** (4.29) |

| c | 0.060465 *** (5.65) | 0.078396 *** (8.46) | 0.052203 *** (4.84) |

| R2 | 15.74 | 14.96 | 17.11 |

| EPS | EPS | EPS | |

|---|---|---|---|

| Z | 0.011241 * (1.74) | ||

| CSR | 0.014912 *** (8.83) | 0.012719 *** (7.17) | |

| Z * CSR | 0.000645 *** (3.89) | ||

| LEV | −1.657791 *** (−13.71) | −1.546731 *** (−11.61) | −1.455025 *** (−11.1) |

| GROWTH | 0.000892 (0.06) | −0.011116 (−0.72) | −0.008356 (−0.56) |

| CR | −0.013444 (−0.64) | −0.041711 ** (−1.8) | −0.041802 ** (−1.89) |

| CASH | −0.202457 *** (−4.23) | −0.194576 *** (−3.96) | −0.218573 *** (−4.58) |

| SLACK | 1.947439 *** (9.08) | 2.039097 *** (9.27) | 1.906784 *** (8.92) |

| c | 0.436359 *** (4.00) | 0.971364 *** (10.32) | 0.375361 *** (3.43) |

| R2 | 21.32 | 22.14 | 17.23 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, L.; Shao, Z.; Yang, C.; Ding, T.; Zhang, W. The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry. Sustainability 2020, 12, 6799. https://doi.org/10.3390/su12176799

Wu L, Shao Z, Yang C, Ding T, Zhang W. The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry. Sustainability. 2020; 12(17):6799. https://doi.org/10.3390/su12176799

Chicago/Turabian StyleWu, Liu, Zhen Shao, Changhui Yang, Tao Ding, and Wan Zhang. 2020. "The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry" Sustainability 12, no. 17: 6799. https://doi.org/10.3390/su12176799

APA StyleWu, L., Shao, Z., Yang, C., Ding, T., & Zhang, W. (2020). The Impact of CSR and Financial Distress on Financial Performance—Evidence from Chinese Listed Companies of the Manufacturing Industry. Sustainability, 12(17), 6799. https://doi.org/10.3390/su12176799