Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe

Abstract

1. Introduction

2. Literature Review

2.1. Theoretical Framework

2.2. Prior Research Discussion on the Relationship between Corporate Responsibility (CSR, CSP and ESG) and Performance

3. Hypotheses

4. Methods

4.1. Sample Collection

4.2. Variable Measurements

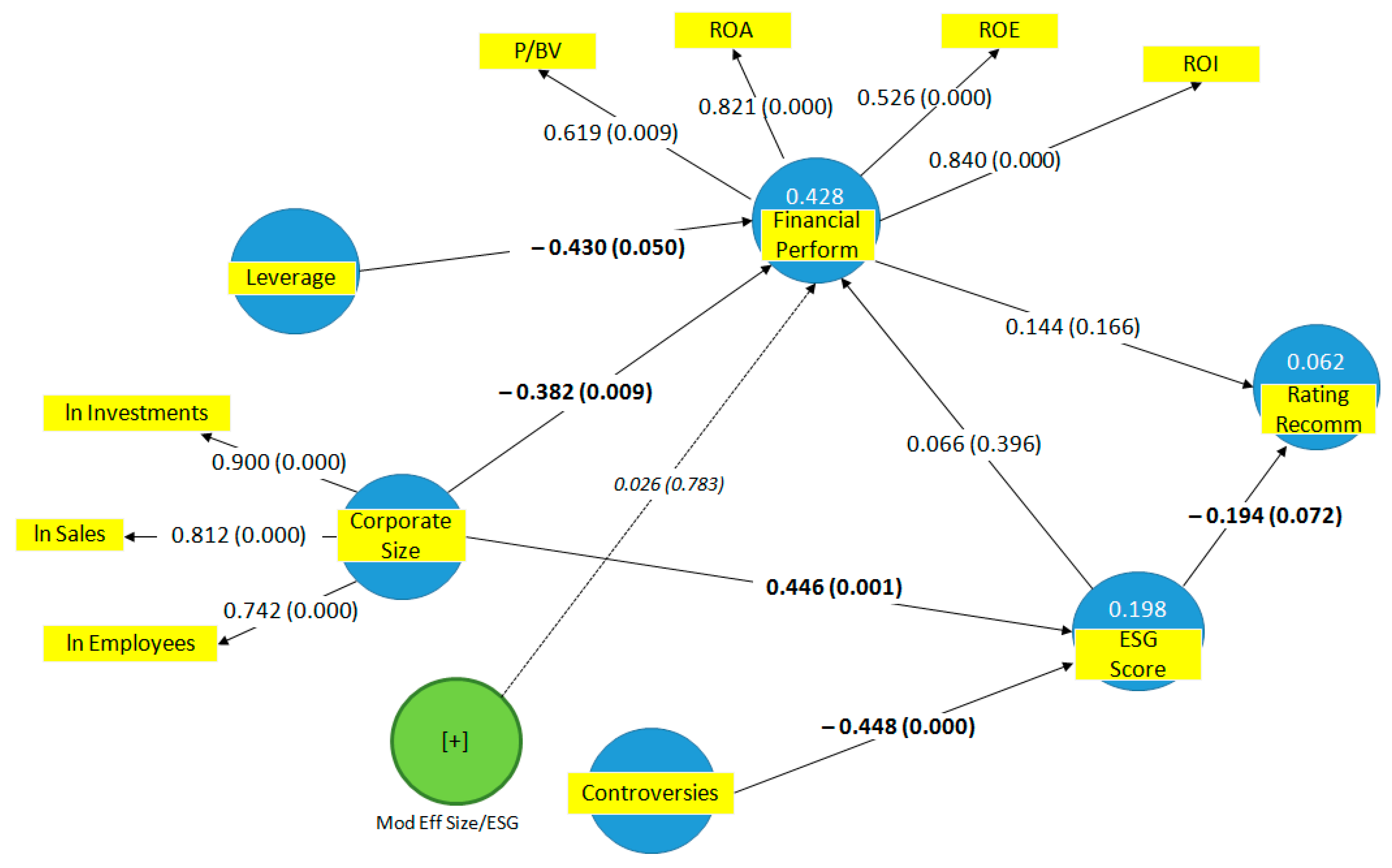

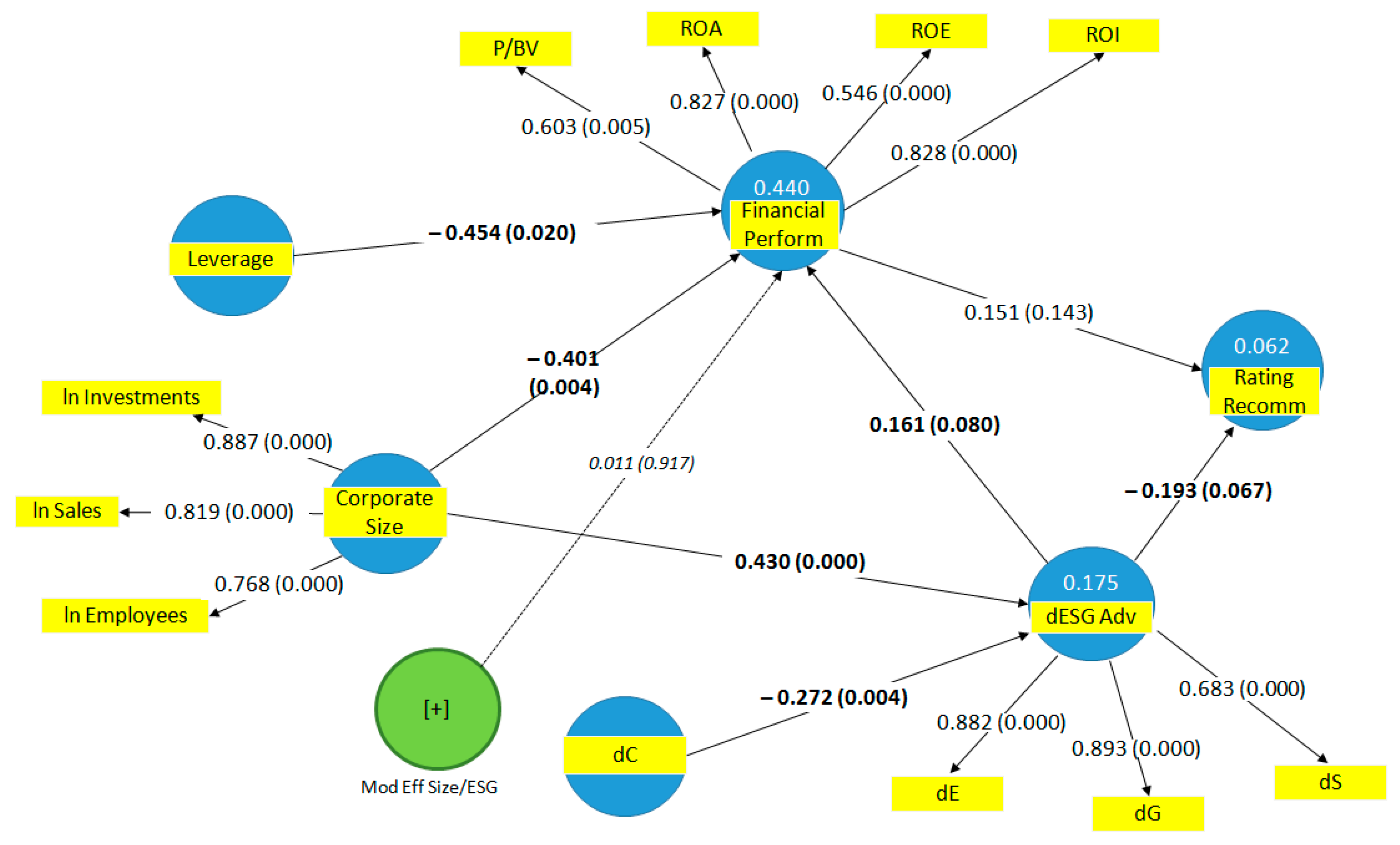

4.3. Models: Regression Analysis and ESG-Based Structural Equation Pattern to Test the Hypotheses

- MLR (Multiple Linear Regression) for the sample of European corporations (450 firm-year observations for the ‘post-crisis’ period 2014–2017), including the above-mentioned dummy and control variables (fixed-effects panel data model, after executing preliminary Breusch-Pagan, Lagrange-multiplier and Hausman tests to control for pooled and/or random effects);

- SEM (Structural Equations Model) performed by Partial Least Squares Path Modeling on the specific ESG sub-sample (analysed with regard to the 2016–2017 period due to the new regulatory framework set out at a European scale and the spread of ESG metrics, which would entail enhanced firm performance and evaluations [88]), in order to implement the analysed sub-variables with suitable vector clusters (latent variables: CS, ESG, and FMP, extracted from statistical projections and grouped by OLS). It is worth underlining that the SEM-PLS is a procedure increasingly being adopted in business and social sciences [89,90].

4.4. Results

5. Discussion of Findings and Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Deegan, C. Introduction: The legitimising effect of social and environmental disclosures—A theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Bassen, A.; Kovács, A.M. Environmental, Social and Governance Key Performance-Indicators from a Capital Market Perspective. Z. für Wirtsch.-und Unternehm.—J. Bus. Econ. Ethics 2008, 9, 182–192. [Google Scholar]

- Zanda, G. Fondamenti di Economia Aziendale; Giappichelli: Turin, Italy, 2015. [Google Scholar]

- Hummel, K.; Schlick, C. The relationship between sustainability performance and sustainability disclosure—Reconciling voluntary disclosure theory and legitimacy theory. J. Account. Public Policy 2016, 35, 455–476. [Google Scholar] [CrossRef]

- Clarkson, M.E. A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Griffin, J.J. Corporate social performance: Research directions for the 21st century. Bus. Soc. 2000, 39, 479–491. [Google Scholar] [CrossRef]

- Muller, A.; Kolk, A. Extrinsic and intrinsic drivers of corporate social performance: Evidence from foreign and domestic firms in Mexico. J. Manag. Stud. 2010, 47, 1–26. [Google Scholar] [CrossRef]

- Cooper, S. Corporate Social Performance: A Stakeholder Approach; Routledge: London, UK, 2017. [Google Scholar]

- Jones, T.M. Instrumental stakeholder theory: A synthesis of ethics and economics. Acad. Manag. Rev. 1995, 20, 404–437. [Google Scholar] [CrossRef]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2002. [Google Scholar]

- Porter, M.E.; Kramer, M.R. The Big Idea: Creating Shared Value. How to reinvent capitalism—And unleash a wave of innovation and growth. Harv. Bus. Rev. 2011, 89, 2–17. [Google Scholar]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strateg. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Jensen, J.C.; Berg, N. Determinants of traditional sustainability reporting versus integrated reporting. An institutionalist approach. Bus. Strategy Environ. 2012, 21, 299–316. [Google Scholar] [CrossRef]

- Adams, C.A. The international integrated reporting council: A call to action. Crit. Perspect. Account. 2015, 27, 23–28. [Google Scholar] [CrossRef]

- Sierra-García, L.; Zorio-Grima, A.; García-Benau, M.A. Stakeholder engagement, corporate social responsibility and integrated reporting: An exploratory study. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 286–304. [Google Scholar] [CrossRef]

- Simnett, R.; Huggins, A.L. Integrated reporting and assurance: Where can research add value? Sustain. Account. Manag. Policy J. 2015, 6, 29–53. [Google Scholar] [CrossRef]

- Maas, K.; Schalteggerand, S.; Crutzen, N. Integrating corporate sustainability assessment, management accounting, control, and reporting. J. Clean. Prod. 2016, 136, 237–248. [Google Scholar] [CrossRef]

- Elkington, J. Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environ. Qual. Manag. 1998, 8, 37–51. [Google Scholar] [CrossRef]

- Barman, E. Doing Well by Doing Good: A Comparative Analysis of ESG Standards for Responsible Investment. In Sustainability, Stakeholder Governance, and Corporate Social Responsibility; Emerald: Bingley, UK, 2018; Volume 38, pp. 289–311. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Perspective; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Freeman, R.E.; Harrison, J.S.; Wicks, A.C.; Parmar, B.; de Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Freeman, R.E.; Dmytriyev, S. Corporate Social Responsibility and Stakeholder Theory: Learning from Each Other. Symphonya. Emerg. Issues Manag. 2017, 2, 7–15. [Google Scholar]

- Bourghelle, D.; Hager, J.; Louche, C. The Integration of ESG Information into Investment Processes: Toward an Emerging Collective Belief? Working Paper; Vlerick Leuven Gent Management School: Ghent, Belgium, 2009. [Google Scholar]

- Van Duuren, E.; Plantinga, A.; Scholtens, B. ESG integration and the investment management process: Fundamental investing reinvented. J. Bus. Ethics 2016, 138, 525–533. [Google Scholar] [CrossRef]

- Tamimi, N.; Sebastianelli, R. Transparency among S&P 500 companies: An analysis of ESG disclosure scores. Manag. Decis. 2017, 55, 1660–1680. [Google Scholar]

- Waddock, S.A.; Graves, S.B. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Van Beurden, P.; Gössling, T. The worth of values—A literature review on the relation between corporate social and financial performance. J. Bus. Ethics 2008, 82, 407. [Google Scholar] [CrossRef]

- Kim, M.; Kim, Y. Corporate social responsibility and shareholder value of restaurant firms. Int. J. Hosp. Manag. 2014, 40, 120–129. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Porter, M.E. Towards a dynamic theory of strategy. Strateg. Manag. J. 1991, 12, 95–117. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Hammond, S.A.; Slocum, J.W. The impact of prior firm financial performance on subsequent corporate reputation. J. Bus. Ethics 1996, 15, 159–165. [Google Scholar] [CrossRef]

- Neville, B.A.; Bell, S.J.; Mengüç, B. Corporate reputation, stakeholders and the social performance-financial performance relationship. Eur. J. Mark. 2005, 39, 1184–1198. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Bird, R.; Hall, A.D.; Momentè, F.; Reggiani, F. What corporate social responsibility activities are valued by the market? J. Bus. Ethics 2007, 76, 189–206. [Google Scholar] [CrossRef]

- Weber, M. The business case for corporate social responsibility: A company-level measurement approach for CSR. Eur. Manag. J. 2008, 26, 247–261. [Google Scholar] [CrossRef]

- Flammer, C. Does corporate social responsibility lead to superior financial performance? A regression discontinuity approach. Manag. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef]

- Frooman, J. Socially irresponsible and illegal behavior and shareholder wealth: A meta-analysis of event studies. Bus. Soc. 1997, 36, 221–249. [Google Scholar] [CrossRef]

- Damodaran, A. Damodaran on Valuation: Security Analysis for Investment and Corporate Finance; John Wiley & Sons: Hoboken, NJ, USA, 2016; Volume 324. [Google Scholar]

- Friedman, M. Capitalism and Freedom: With the Assistance of Rose D. Friedman; University of Chicago Press: Chicago, IL, USA, 1962. [Google Scholar]

- Friedman, M. The social responsibility of the corporation is to increase its profits. N. Y. Times Mag. 1970, 13, 122–126. [Google Scholar]

- Moser, D.V.; Martin, P.R. A broader perspective on corporate social responsibility research in accounting. Account. Rev. 2012, 87, 797–806. [Google Scholar] [CrossRef]

- Mackey, A.; Mackey, T.B.; Barney, J.B. Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Acad. Manag. Rev. 2007, 32, 817–835. [Google Scholar] [CrossRef]

- Moon, J. The Social Responsibility of Business and New Governance. Gov. Oppos. 2002, 37, 385–408. [Google Scholar] [CrossRef]

- Caulkin, S. Good thinking, bad practice. The Observer, 7 April 2002. [Google Scholar]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Wang, H.; Choi, J.; Li, J. Too little or too much? Untangling the relationship between corporate philanthropy and firm financial performance. Organ. Sci. 2008, 19, 143–159. [Google Scholar] [CrossRef]

- Wu, M.L. Corporate social performance, corporate financial performance, and firm size: A meta-analysis. J. Am. Acad. Bus. 2006, 8, 163–171. [Google Scholar]

- Mishra, S.; Suar, D. Does corporate social responsibility influence firm performance of Indian companies? J. Bus. Ethics 2010, 95, 571–601. [Google Scholar] [CrossRef]

- Orlitzky, M. Does firm size confound the relationship between corporate social performance and firm financial performance? J. Bus. Ethics 2001, 33, 167–180. [Google Scholar] [CrossRef]

- Allouche, J.; Laroche, P. A meta-analytical investigation of the relationship between corporate social and financial performance. Revue de Gestion des Ressources Humaines 2005, 57, 18–41. [Google Scholar]

- Margolis, J.D.; Elfenbein, H.A.; Walsh, J.P. Does it pay to be good... and does it matter? A meta-analysis of the relationship between corporate social and financial performance. SSRN Electron. J. 2009. [Google Scholar] [CrossRef]

- Peiró-Signes, A.; Segarra-Oña, M.; Mondéjar-Jiménez, J.; Vargas-Vargas, M. Influence of the environmental, social and corporate governance ratings on the economic performance of companies: An overview. Int. J. Environ. Res. 2013, 7, 105–112. [Google Scholar]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Shaukat, A.; Qiu, Y.; Trojanowski, G. Board attributes, corporate social responsibility strategy, and corporate environmental and social performance. J. Bus. Ethics 2016, 135, 569–585. [Google Scholar] [CrossRef]

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R.J. Corporate Sustainability, Capital Markets, and ESG Performance. In Individual Behaviors and Technologies for Financial Innovations; Springer International Publishing AG: Cham, Switzerland, 2006; pp. 287–309. [Google Scholar]

- Hoepner, A.G.F.; McMillan, D.G. Research on ‘Responsible Investment’: An Influential Literature Analysis Comprising a Rating, Characterisation, Categorisation and Investigation; University of St. Andrews: St. Andrews, UK, 2009. [Google Scholar]

- Galbreath, J. ESG in focus: The Australian evidence. J. Bus. Ethics 2013, 118, 529–541. [Google Scholar] [CrossRef]

- Lokuwaduge, C.S.D.S.; Heenetigala, K. Integrating environmental, social and governance (ESG) disclosure for a sustainable development: An Australian study. Bus. Strategy Environ. 2017, 26, 438–450. [Google Scholar] [CrossRef]

- Landi, G.; Sciarelli, M. Towards a more ethical market: The impact of ESG rating on corporate financial performance. Soc. Responsib. J. 2018. [Google Scholar] [CrossRef]

- Brooks, C.; Oikonomou, I. The effects of environmental, social and governance disclosures and performance on firm value: A review of the literature in accounting and finance. Br. Account. Rev. 2018, 50, 1–15. [Google Scholar] [CrossRef]

- Murphy, D.; McGrath, D. ESG reporting–class actions, deterrence, and avoidance. Sustain. Account. Manag. Policy J. 2013, 4, 216–235. [Google Scholar] [CrossRef]

- Ling, A.; Forrest, S.; Lynch, M.; Fox, M. Global Food & Beverages: Integrating ESG; Goldman Sachs: New York, NY, USA, 2007. [Google Scholar]

- Melnyk, S.A.; Sroufe, R.P.; Calantone, R. Assessing the impact of environmental management systems on corporate and environmental performance. J. Oper. Manag. 2003, 21, 329–351. [Google Scholar] [CrossRef]

- Du Rietz, S. Information vs knowledge: Corporate accountability in environmental, social, and governance issues. Account. Audit. Account. J. 2018, 31, 586–607. [Google Scholar] [CrossRef]

- Li, Y.; Gong, M.; Zhang, X.Y.; Koh, L. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. Br. Account. Rev. 2018, 50, 60–75. [Google Scholar] [CrossRef]

- Bouslah, K.; Linares-Zegarra, J.; M’Zali, B.; Scholtens, B. CEO risk-taking incentives and socially irresponsible activities. Br. Account. Rev. 2018, 50, 76–92. [Google Scholar] [CrossRef]

- Velte, P. Women on management board and ESG performance. J. Glob. Responsib. 2016, 7, 98–109. [Google Scholar] [CrossRef]

- Manita, R.; Bruna, M.G.; Dang, R.; Houanti, L.H. Board gender diversity and ESG disclosure: Evidence from the USA. J. Appl. Account. Res. 2018, 19, 206–224. [Google Scholar] [CrossRef]

- Manes-Rossi, F.; Tiron-Tudor, A.; Nicolò, G.; Zanellato, G. Ensuring More Sustainable Reporting in Europe Using Non-Financial Disclosure—De Facto and De Jure Evidence. Sustainability 2018, 10, 1162. [Google Scholar] [CrossRef]

- Global Reporting Initiative (GRI) Global Sustainability Standards Board (GSSB) “Linking the GRI Standards and the European Directive on Non-Financial and Diversity Disclosure”. 2017. Available online: http://asvis.it/public/asvis/files/linkingGRI.pdf (accessed on 27 February 2019).

- Mervelskemper, L.; Streit, D. Enhancing Market Valuation of ESG Performance: Is Integrated Reporting Keeping its Promise? Bus. Strategy Environ. 2017, 26, 536–549. [Google Scholar] [CrossRef]

- Ohlson, J.A. Earnings, book values, and dividends in equity valuation. Contemp. Account. Res. 1995, 11, 661–687. [Google Scholar] [CrossRef]

- Eccles, R.G.; Serafeim, G.; Seth, D.; Ming, C.C.Y. The Performance Frontier: Innovating for a Sustainable Strategy: Interaction. Harv. Bus. Rev. 2013, 91, 17–18. [Google Scholar]

- Endrikat, J.; Guenther, E.; Hoppe, H. Making sense of conflicting empirical findings: A meta-analytic review of the relationship between corporate environmental and financial performance. Eur. Manag. J. 2014, 32, 735–751. [Google Scholar] [CrossRef]

- Pfeffer, J.; Salancik, G.R. The External Control of Organisations: A Resource Dependence Perspective; Harper & Row: New York, NY, USA, 1978. [Google Scholar]

- Chang, Y.K.; Oh, W.Y.; Jung, J.C.; Lee, J.Y. Firm size and corporate social performance: The mediating role of outside director representation. J. Leadersh. Organ. Stud. 2012, 19, 486–500. [Google Scholar] [CrossRef]

- Gooding, R.Z.; Wagner, J.A., III. A meta-analytic review of the relationship between size and performance: The productivity and efficiency of organizations and their subunits. Adm. Sci. Q. 1985, 30, 462–481. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2001, 24, 403–441. [Google Scholar] [CrossRef]

- Wisebrod, J.M. Social impact ratings: How to make responsible investment appealing. Finance Bien Commun. 2007, 27, 29–40. [Google Scholar] [CrossRef]

- Cohen, J.R.; Holder-Webb, L.; Zamora, V.L. Nonfinancial information preferences of professional investors. Behav. Res. Account. 2015, 27, 127–153. [Google Scholar] [CrossRef]

- Lefkovitz, D. Sustainability Atlas; Morningstar: Chicago, IL, USA, 2017. [Google Scholar]

- Onesti, T. ‘Fattori Ambientali’ e Comportamenti Contabili. Analisi Comparata dei Sistemi Contabili di Alcuni Paesi Industrializzati; Giappichelli: Turin, Italy, 1995. [Google Scholar]

- Aouadi, A.; Marsat, S. Do ESG controversies matter for firm value? Evidence from international data. J. Bus. Ethics 2016, 1, 1–21. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting. SSRN Electron. J. 2017. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

- Gelhard, C.; von Delft, S. The role of organizational capabilities in achieving superior sustainability performance. J. Bus. Res. 2016, 69, 4632–4642. [Google Scholar] [CrossRef]

- Mardani, A.; Streimikiene, D.; Zavadskas, E.K.; Cavalaro, F.; Nilashi, M.; Jusoh, A.; Zare, H. Application of Structural Equation Modeling (SEM) to Solve Environmental Sustainability Problems: A Comprehensive Review and Meta-Analysis. Sustainability 2017, 9, 1814. [Google Scholar] [CrossRef]

- Ağan, Y.; Kuzey, C.; Acar, M.F.; Açıkgöz, A. The relationships between corporate social responsibility, environmental supplier development, and firm performance. J. Clean. Prod. 2016, 112, 1872–1881. [Google Scholar] [CrossRef]

- Reverte, C.; Gómez-Melero, E.; Cegarra-Navarro, J.G. The influence of corporate social responsibility practices on organizational performance: Evidence from Eco-Responsible Spanish firms. J. Clean. Prod. 2016, 112, 2870–2884. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y.; Nassen, K.D. Representation of measurement error in marketing variables: Review of approaches and extension to three-facet designs. J. Econ. 1998, 89, 393–421. [Google Scholar] [CrossRef]

- Tseng, M.L.; Wu, W.W.; Lin, Y.H.; Liao, C.H. An exploration of relationships between environmental practice and manufacturing performance using the PLS path modeling. WSEAS Trans. Environ. Dev. 2008, 4, 487–502. [Google Scholar]

- Götz, O.; Liehr-Gobbers, K.; Krafft, M. Evaluation of structural equation models using the partial least squares (PLS) approach. In Handbook of Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 2010; pp. 691–711. [Google Scholar]

- Johansen, T.R. EU Regulation of Corporate Social and Environmental Reporting. Soc. Environ. Account. J. 2016, 36, 1–9. [Google Scholar] [CrossRef]

- Venturelli, A.; Caputo, F.; Leopizzi, R.; Pizzi, S. The state of art of Corporate Social Disclosure before the introduction of Non-financial reporting Directive: A cross country analysis. Soc. Responsib. J. 2018. [Google Scholar] [CrossRef]

- Muserra, A.L.; Papa, M.; Grimaldi, F. Exploring the legitimacy of EU directive on non-financial and diversity information: Evidence from italian preparers and auditors. In Proceedings of the Annual Congress, European Accounting Association, Milan, Italy, 30 May–1 June 2018. [Google Scholar]

- Frey, M. Agenda 2030 e ruolo delle imprese. Impresa Progetto 2018, 2, 1–9. [Google Scholar]

- Kang, J.S.; Chiang, C.F.; Huangthanapan, K.; Downing, S. Corporate social responsibility and sustainability balanced scorecard: The case study of family-owned hotels. Int. J. Hosp. Manag. 2015, 48, 124–134. [Google Scholar] [CrossRef]

- Gompers, P.; Ishii, J.; Metrick, A. Corporate governance and equity prices. Q. J. Econ. 2003, 118, 107–156. [Google Scholar] [CrossRef]

- Chen, K.H.; Metcalf, R.W. The relationship between pollution control record and financial indicators revisited. Account. Rev. 1980, 55, 168–177. [Google Scholar]

- Porter, M.E. Competitive advantage: Creating and Sustaining Superior Performance; The Free Press: New York, NY, USA, 1985. [Google Scholar]

- Grant, R.M. L’analisi Strategica per le Decisioni Aziendali; Il Mulino: Bologna, Italy, 2011. [Google Scholar]

- Sciarelli, S. La produzione del valore allargato quale obiettivo dell’etica nell’impresa. Finanza Marketing e Produzione 2002, 20, 5–17. [Google Scholar]

- Busco, C.; Izzo, M.F.; Granà, F. L’evoluzione del sistema di Corporate Rating. Lo Shared Value all’interno del Bilancio Integrato di un gruppo bancario. Rivista Italiana di Ragioneria e di Economia Aziendale 2018, 1–4, 16–36. [Google Scholar]

- Kassinis, G.I.; Soteriou, A.C. Greening the service profit chain: The impact of environmental management practices. Prod. Oper. Manag. 2003, 12, 386–403. [Google Scholar] [CrossRef]

- Chopra, S.; Wu, P.J. Eco-activities and operating performance in the computer and electronics industry. Eur. J. Oper. Res. 2016, 248, 971–981. [Google Scholar] [CrossRef]

- Brammer, S.; Brooks, C.; Pavelin, S. The stock performance of America’s 100 best corporate citizens. Q. Rev. Econ. Finance 2009, 49, 1065–1080. [Google Scholar] [CrossRef]

- Hoang, T. The Role of the Integrated Reporting in Raising Awareness of Environmental, Social and Corporate Governance (ESG) Performance. In Stakeholders, Governance and Responsibility; Emerald: Bingley, UK, 2018; pp. 47–69. [Google Scholar]

- International Federation of Accountants (IFAC); International Integrated Reporting Council (IIRC). Materiality in IR. Guidance for the Preparation of Integrated Reports, November, 2015. Available online: https://integratedreporting.org/wp-content/uploads/2015/11/1315_MaterialityinIR_Doc_4a_Interactive.pdf (accessed on 27 February 2019).

- London Stock Exchange Group. Revealing the Full Picture. Your Guide to ESG Reporting—Guidance for Issuers on the Integration of ESG into Investor Reporting and Communication. February 2017. Available online: https://www.lseg.com/sites/default/files/content/images/Green_Finance/ESG/2018/February/LSEG_ESG_report_January_2018.pdf (accessed on 27 February 2019).

- Oekom. Corporate Responsibility Review 2018. The Materiality and Impact of Sustainability Research. 2018. Available online: http://www.oekom-research.com/homepage/english/2018-04%20oekom%20CR%20Review-EN.pdf (accessed on 27 February 2019).

- Eccles, R.G.; Krzus, M.P.; Rogers, J.; Serafeim, G. The need for sector-specific materiality and sustainability reporting standards. J. Appl. Corp. Finance 2012, 24, 65–71. [Google Scholar] [CrossRef]

- Torelli, R.; Balluchi, F.; Furlotti, K. Il settore industriale come determinante della materialità nell’informativa volontaria: Analisi empirica nel contesto italiano. Rivista Italiana di Ragioneria e di Economia Aziendale 2018. [Google Scholar] [CrossRef]

- Baldini, M.; Dal Maso, L.; Liberatore, G.; Mazzi, F.; Terzani, S. Role of country-and firm-level determinants in environmental, social, and governance disclosure. J. Bus. Ethics 2018, 150, 79–98. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable | Mean | Median | Min | Max | Std.Dev. | Var. Coeff. |

|---|---|---|---|---|---|---|

| EMPL: employees | 10.353 | 87,114 | 40 | 625,796 | 108.253 | 1.045 |

| ln_EMPL | 10.738 | 11.375 | 3.689 | 13.3468 | 1.804 | 0.168 |

| SALES | 3.12e+007 | 2.04e+007 | 255,203 | 2.17e+008 | 3.58e+007 | 1.147 |

| ln_SALES | 16.636 | 16.836 | 12.450 | 19.197 | 1.259 | 0.076 |

| INV_CAP: Invested Capital | 1.85e+008 | 4.48e+007 | 1.37e+006 | 2.08e+009 | 3.64e+008 | 1.968 |

| ln_INV_CAP | 17.842 | 17.618 | 14.134 | 21.455 | 1.521 | 0.085 |

| FIN LEV.: leverage | 5.624 | 2.302 | 0.003 | 61.947 | 8.039 | 1.429 |

| ROS: Return on Sales | 0.163 | 0.127 | −1.255 | 0.697 | 0.164 | 1.003 |

| ROI: Return on Investment | 0.056 | 0.055 | −0.011 | 0.218 | 0.044 | 0.771 |

| ROA: Return on Asset | 0.040 | 0.033 | −0.133 | 0.369 | 0.051 | 1.275 |

| ROE: Return on Equity | 0.083 | 0.098 | −6.566 | 0.517 | 0.420 | 5.034 |

| CFOI: Cash flow to Inv. | 0.064 | 0.063 | −0.192 | 0.370 | 0.057 | 0.887 |

| P/BV: Price on Book Value | 2.707 | 2.094 | 0.350 | 14.705 | 2.214 | 0.818 |

| Analyst stock recomm | 2.441 | 2.400 | 1.700 | 3.700 | 0.393 | 0.161 |

| E: Environment (score) | 73.292 | 74.300 | 34.800 | 96.000 | 12.137 | 0.166 |

| S: Social (score) | 72.164 | 74.000 | 43.100 | 97.200 | 10.903 | 0.151 |

| G: Governance (score) | 69.247 | 70.000 | 36.900 | 88.000 | 10.090 | 0.146 |

| C: Controversies (score) | 2.536 | 3.000 | 1.000 | 5.000 | 0.842 | 0.332 |

| ESG _Tot (score) | 71.341 | 72.000 | 43.000 | 87.000 | 9.441 | 0.132 |

| dE: E score over industry | 1.232 | 1.217 | 0.642 | 1.738 | 0.226 | 0.183 |

| dS: S score over industry | 1.196 | 1.193 | 0.804 | 1.664 | 0.166 | 0.139 |

| dG: G score over industry | 1.109 | 1.116 | 0.625 | 1.488 | 0.156 | 0.141 |

| dC: C score over industry | 1.367 | 1.429 | 0.400 | 2.500 | 0.425 | 0.309 |

| ln_Emp | ln_Sal | ln_Inv. | Lev | ROI | ROA | ROE | CFOI | E | S | G | C | dE | dS | dG | dC | Recomm. | P/BV | ESG_T. | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ln_Emp. | 1 | 0.723 ** | 0.444 ** | 0.036 | −0.111 | −0.123 * | −0.017 | −0.118 | 0.26 ** | 0.110 | 0.215 ** | 0.402 ** | 0.280 ** | 0.180 ** | 0.287 ** | 0.288 ** | −0.507 ** | −0.087 | 0.235 ** |

| ln_Sal | 1 | 0.519 ** | −0.046 | −0.175 ** | −0.255 ** | −0.083 | −0.080 | 0.157 ** | 0.092 | 0.223 ** | 0.425 ** | 0.185 ** | 0.102 | 0.186 ** | 0.289 ** | −0.494 ** | −0.262 ** | 0.186 ** | |

| ln_Inv | 1 | 0.543 ** | −0.667 ** | −0.409 ** | −0.099 | −0.562 ** | 0.228 ** | 0.191 ** | 0.035 | 0.579 ** | 0.412 ** | −0.031 | 0.257 ** | 0.366 ** | −0.186 ** | −0.571 ** | 0.182 ** | ||

| Lev | 1 | −0.516 ** | −0.310 ** | −0.326 ** | −0.414 ** | 0.136 * | 0.145 * | −0.119 | 0.238 ** | 0.340 ** | 0.005 | 0.113 | 0.131 * | 0.086 | −0.100 | 0.069 | |||

| ROI | 1 | 0.562 ** | 0.169 ** | 0.759 ** | 0.005 | −0.169 ** | 0.058 | −0.331 ** | −0.178 ** | 0.041 | −0.098 | −0.091 | −0.014 | 0.658 ** | −0.041 | ||||

| ROA | 1 | 0.330 ** | 0.398 ** | 0.003 | −0.111 | 0.030 | −0.149 * | −0.078 | −0.002 | −0.046 | −0.032 | 0.115 | 0.377 ** | −0.034 | |||||

| ROE | 1 | 0.094 | 0.015 | −0.097 | −0.008 | −0.014 | 0.006 | −0.012 | 0.031 | 0.015 | 0.108 | 0.097 | −0.034 | ||||||

| CFOI | 1 | −0.059 | −0.128 * | 0.101 | −0.257 ** | −0.197 ** | 0.043 | −0.125 * | −0.055 | 0.014 | 0.534 ** | −0.037 | |||||||

| E | 1 | 0.553 ** | 0.591 ** | −0.179 ** | 0.868 ** | 0.466 ** | 0.628 ** | −0.185 ** | −0.161 ** | −0.027 | 0.860 ** | ||||||||

| S | 1 | 0.563 ** | −0.243 ** | 0.562 ** | 0.777 ** | 0.521 ** | −0.241 ** | −0.049 | −0.153 * | 0.839 ** | |||||||||

| G | 1 | −0.237 ** | 0.482 ** | 0.499 ** | 0.856 ** | −0.151 * | −0.313 ** | −0.034 | 0.827 ** | ||||||||||

| C | 1 | −0.030 | −0.119 | −0.104 | 0.818** | −0.232 ** | −0.287 ** | −0.275 ** | |||||||||||

| dE | 1 | 0.498 ** | 0.625 ** | −0.079 | −0.072 | −0.091 | 0.768 ** | ||||||||||||

| dS | 1 | 0.512 ** | −0.129 * | −0.109 | 0.055 | 0.691 ** | |||||||||||||

| dG | 1 | −0.129 * | −0.260 ** | −0.085 | 0.774 ** | ||||||||||||||

| dC | 1 | −0.200 ** | −0.069 | −0.244 ** | |||||||||||||||

| Recom. | 1 | −0.004 | −0.201 ** | ||||||||||||||||

| P/BV | 1 | −0.080 | |||||||||||||||||

| ESG_Tot | 1 |

| Coefficient | Std Error | T | p-Value | ||

|---|---|---|---|---|---|

| Const | 14.9869 | 2.0082 | 7.4628 | <0.00001 | *** |

| ln_EMPLOYEES | 0.2876 | 0.0695 | 4.1356 | 0.00004 | *** |

| ln_SALES | 0.2841 | 0.1344 | 2.1139 | 0.03508 | ** |

| ln_INVESTMENTS | −1.2544 | 0.1149 | −10.9180 | <0.00001 | *** |

| LEVERAGE | 0.1298 | 0.0253 | 5.1240 | <0.00001 | *** |

| DESG | 1.5565 | 0.3471 | 4.4844 | <0.00001 | *** |

| Regression Statistics | |||||

| Sum Squared Errors | 3395.202 | S.E. | 2.765 | Sum Squared Errors | |

| R-squared | 0.2257 | Adj. R-squared | 0.217 | R-squared | |

| F-test | 37.991 | p-value(F) | 0.000 | F-test | |

| Coefficient | Std Error | T | p-Value | ||

|---|---|---|---|---|---|

| Const | 17.6004 | 2.8577 | 6.1589 | <0.0000 | *** |

| ln_EMPLOYEES | 0.1738 | 0.0603 | 2.8804 | 0.0051 | *** |

| ln_SALES | 0.1523 | 0.1231 | 1.2371 | 0.2196 | |

| ln_INVESTMENTS | −1.1577 | 0.1594 | −7.2630 | <0.0000 | *** |

| LEVERAGE | 0.0804 | 0.0164 | 4.8945 | <0.0000 | *** |

| ESG_Tot | −0.0460 | 0.0348 | −1.3230 | 0.1895 | |

| dE | 2.1672 | 1.1564 | 1.8741 | 0.0645 | * |

| dS | −0.2671 | 0.8738 | 0.3057 | 0.7606 | |

| dG | 0.8368 | 1.0903 | 0.7671 | 0.4452 | |

| Regression Statistics | |||||

| Sum Squared Errors | 129.9269 | S.E. | 1.2588 | Sum Squared Errors | |

| R-squared | 0.5120 | Adj. R-squared | 0.4644 | R-squared | |

| F-test | 10.9266 | p-value(F) | 0.0000 | F-test | |

| y = ROI | y = ROA | y = ROE | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Coeffic. | p-Value | Coeffic. | p-Value | Coeffic. | p-Value | ||||

| Const | 0.3888 | <0.0000 | *** | 0.4528 | 0.0004 | *** | 0.3654 | 0.5316 | |

| ln_EMPLOYEES | 0.0052 | 0.0452 | ** | 0.0068 | 0.0423 | ** | 0.02876 | 0.2988 | |

| ln_SALES | 0.0033 | 0.4202 | −0.0168 | 0.0306 | ** | −0.2176 | 0.0888 | * | |

| ln_INVESTMENTS | −0.0248 | <0.0000 | *** | −0.0110 | 0.0062 | *** | 0.1856 | 0.1519 | |

| LEVERAGE | −0.0010 | 0.0351 | ** | −0.0019 | 0.0122 | ** | −0.0721 | 0.0620 | * |

| ESG_Tot | −0.0002 | 0.7911 | −0.0017 | 0.0771 | * | −0.0285 | 0.0411 | ** | |

| dE | 0.0518 | 0.0936 | * | 0.0923 | 0.0154 | ** | 1.039 | 0.0273 | ** |

| dS | −0.0360 | 0.0972 | * | −0.0598 | 0.0899 | * | 0.1070 | 0.7798 | |

| dG | 0.0019 | 0.9497 | 0.0706 | 0.0970 | * | 0.6152 | 0.0999 | * | |

| Regression Statistics | |||||||||

| R-squared | 0.5757 | 0.3744 | 0.5103 | ||||||

| S.E. | 0.0303 | 0.0418 | 0.5198 | ||||||

| Adj. R-squared | 0.5343 | 0.3134 | 0.4625 | ||||||

| p-value(F) | 0.000 | 0.0000 | 0.0938 | ||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Taliento, M.; Favino, C.; Netti, A. Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe. Sustainability 2019, 11, 1738. https://doi.org/10.3390/su11061738

Taliento M, Favino C, Netti A. Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe. Sustainability. 2019; 11(6):1738. https://doi.org/10.3390/su11061738

Chicago/Turabian StyleTaliento, Marco, Christian Favino, and Antonio Netti. 2019. "Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe" Sustainability 11, no. 6: 1738. https://doi.org/10.3390/su11061738

APA StyleTaliento, M., Favino, C., & Netti, A. (2019). Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe. Sustainability, 11(6), 1738. https://doi.org/10.3390/su11061738