Does CSR Influence Firm Performance Indicators? Evidence from Chinese Pharmaceutical Enterprises

Abstract

1. Introduction

Product-Related Incidents in Chinese Pharmaceuticals

2. Literature Review and Hypotheses Development

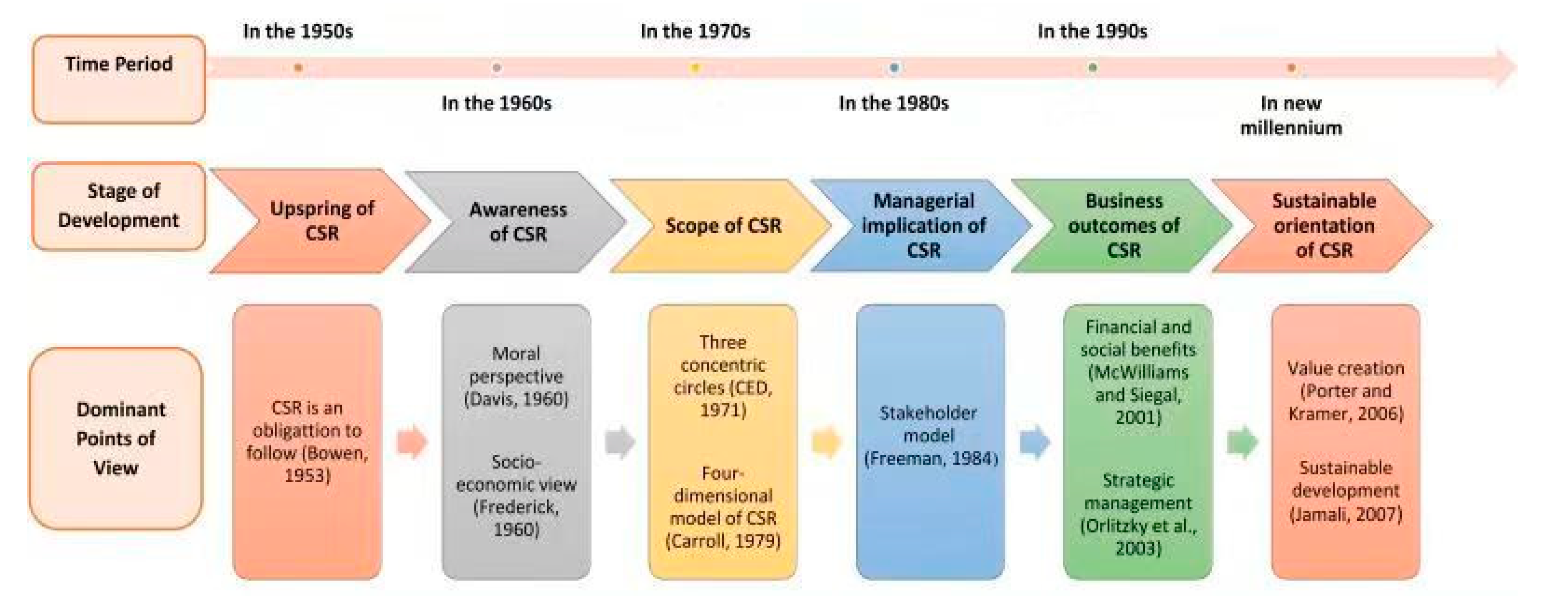

2.1. Evolution of CSR

2.2. CSR in China

2.3. Stakeholder Theory in Explaining CSR Dimensions

2.4. Hypotheses Development

3. Research Design

3.1. Sample Selection

3.2. Variables of the Study

CSR

3.3. Firm Performance and Other Control Variables

4. Results and Discussions

4.1. Descriptive Statistics

4.2. Overall CSR and Firm Performance

4.3. Impact of Individual CSR Dimensions on Firm Performance

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| S/N | Code | Name of the Company | S/N | Code | Name of the Company |

|---|---|---|---|---|---|

| 1 | 000004 | CAU Technology | 64 | 300049 | Fu-rui Pharmaceutical |

| 2 | 000078 | Neptunus Group | 65 | 300110 | Huaren Pharmaceutical |

| 3 | 000153 | BBCA Pharmaceutical | 66 | 300119 | Ruipu Biological |

| 4 | 000403 | Shenghua Pharmaceutical | 67 | 300122 | Zhifei Biological |

| 5 | 000423 | Dongeejiao Group | 68 | 300138 | CCGB Biological |

| 6 | 000513 | Livzon Pharmaceutical | 69 | 300142 | Walvax Biotechnology |

| 7 | 000518 | Sihuan Biological | 70 | 300158 | Zhengdong Group |

| 8 | 000538 | Yunnai baiyao | 71 | 300181 | Zuoli Pharmaceutical |

| 9 | 000545 | Jinpu Group | 72 | 300194 | Fuan Pharmaceutical |

| 10 | 000590 | Guhan Group | 73 | 300199 | Hanyu Biological |

| 11 | 000597 | Northeast Pharmaceutical | 74 | 300204 | Staidson Bio-pharmaceutical |

| 12 | 000606 | Shenzhou Yiqiao | 75 | 300239 | Dongbao Biological |

| 13 | 000623 | Jilin Aodong Medical | 76 | 300254 | CY Pharmaceutical |

| 14 | 000650 | Renhe Pharmaceutical | 77 | 300255 | CSBIO Group |

| 15 | 000661 | Changchun Gaoxin | 78 | 300267 | Erkang Pharmaceutical |

| 16 | 000739 | Apeloa Pharmaceutical | 79 | 300289 | Leadman Biological |

| 17 | 000756 | Xinhua Pharmaceutical | 80 | 300294 | Boya Pharmaceutical |

| 18 | 000766 | Tonghua Jinma | 81 | 600062 | DCPC Pharmaceutical |

| 19 | 000788 | PKU Health care | 82 | 600079 | HumanWell Healthcare |

| 20 | 000915 | Sd-Wit Group | 83 | 600129 | Taiji Group |

| 21 | 000919 | Jinlin Pharmaceutical | 84 | 600161 | Tiantan Biological |

| 22 | 000952 | Guangji Pharmaceutical | 85 | 600195 | CAHIC Group |

| 23 | 000989 | JZT Pharmaceutical | 86 | 600196 | Fosun Pharmaceutical |

| 24 | 000990 | Chengzhi Group | 87 | 600201 | Jinyu Bio-technology |

| 25 | 000999 | 999 Pharmaceutical | 88 | 600211 | Tibet Pharmaceutical |

| 26 | 002001 | NHU group | 89 | 600222 | Tailong Pharmaceutical |

| 27 | 002004 | Huapont Life Science | 90 | 600252 | Zhongheng Group |

| 28 | 002007 | Hualan Biological | 91 | 600267 | Hisun Pharmaceutical |

| 29 | 002020 | Jinxin Pharmaceutical | 92 | 600276 | Hengrui Medicine |

| 30 | 002022 | Kehua Biological | 93 | 600285 | Lingrui Pharmaceutical |

| 31 | 002030 | Daan Gene | 94 | 600329 | Zhongxin Pharmaceutical |

| 32 | 002038 | Shuanglu Pharmaceutical | 95 | 600332 | BYS Pharmaceutical |

| 33 | 002099 | Hisoar Pharmaceutical | 96 | 600351 | Yabao Pharmaceutical |

| 34 | 002107 | Wohua Pharmaceutical | 97 | 600380 | Joincare |

| 35 | 002118 | Zixin Pharmaceutical | 98 | 600420 | Shyndec Pharmaceutical |

| 36 | 002166 | Layn Biological | 99 | 600422 | KPC Pharmaceutical |

| 37 | 002198 | Jiaying Pharmaceutical | 100 | 600436 | Pien Tze Huang |

| 38 | 002219 | Hengkang Medical | 101 | 600466 | BRC Group |

| 39 | 002252 | Shanghai RAAS | 102 | 600479 | Qianjin Pharmaceutical |

| 40 | 002275 | Sanjin Pharmaceutical | 103 | 600488 | Tianyao Pharmaceutical |

| 41 | 002287 | Cheezheng Pharmaceutical | 104 | 600513 | Lianghuang Group |

| 42 | 002294 | Salubris Pharmaceutical | 105 | 600518 | Kangmei Pharmaceutical |

| 43 | 002317 | ZS Pharmaceutical | 106 | 600521 | Huahai Pharmaceutical |

| 44 | 002332 | Xianju Pharmaceutical | 107 | 600530 | Onlly Group |

| 45 | 002349 | Jinghua Pharmaceutical | 108 | 600535 | Tasly Group |

| 46 | 002370 | Yatai Pharmaceutical | 109 | 600557 | Kanion Pharmaceutical |

| 47 | 002393 | Lisheng Pharmaceutical | 110 | 600572 | Conba Group |

| 48 | 002399 | Hepalink Pharmaceutical | 111 | 600594 | Yibai Pharmaceutical |

| 49 | 002412 | Hansen Pharmaceutical | 112 | 600613 | Shengqi Pharmaceutical |

| 50 | 002422 | Kelun Pharmaceutical | 113 | 600664 | Hayao Pharmaceutical |

| 51 | 002424 | Bailing Pharmaceutical | 114 | 600671 | HZTM Pharmaceutical |

| 52 | 002433 | Pibao Pharmaceutical | 115 | 600750 | Jiangzhong Pharmaceutical |

| 53 | 002437 | Gloria Pharmaceutical | 116 | 600771 | Guangyuyuan |

| 54 | 002550 | Qianhong Bio-pharma | 117 | 600781 | Furen Pharmaceutical |

| 55 | 002566 | Yisheng Pharmaceutical | 118 | 600789 | Lukang Pharmaceutical |

| 56 | 002603 | Yiling Pharmaceutical | 119 | 600803 | ENN Group |

| 57 | 002644 | Foci Pharmaceutical | 120 | 600812 | Huabei Pharmaceutical |

| 58 | 002653 | Haisco Pharmaceutical | 121 | 600829 | RMTT Pharmaceutical |

| 59 | 300006 | Laimei Pharmaceutical | 122 | 600867 | Dongbao Pharmaceutical |

| 60 | 300009 | Anke Biological | 123 | 600869 | Zhihui Group |

| 61 | 300016 | Beilu Pharmaceutical | 124 | 600976 | Jianmin Group |

| 62 | 300026 | Chasesun Pharmaceutical | 125 | 600993 | Mayinglong |

| 63 | 300039 | Kaibao Pharmaceutical |

References

- Amran, A.; Fauzi, H.; Purwanto, Y.; Darus, F.; Yusoff, H.; Zain, M.M.; Naim, D.M.A.; Nejati, M. Social responsibility disclosure in Islamic banks: A comparative study of Indonesia and Malaysia. J. Financ. Rep. Account. 2017, 15, 99–115. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Lin, L.W. Corporate social responsibility in China: Window dressing or structural change. Berkeley J. Int. Law 2010, 28, 64–100. [Google Scholar]

- Zhu, Q.; Liu, J.; Lai, K. Corporate social responsibility practices and performance improvement among Chinese national state-owned enterprises. Int. J. Prod. Econ. 2016, 171, 417–426. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Brammer, S.; Millington, A. Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar] [CrossRef]

- Hillman, A.; Keim, G. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? an institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Surroca, J.; Tribo, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef]

- Ann, T.N.; Wayne, O.; Rob, H. Capabilities, proactive CSR and financial performance in SMEs: Empirical evidence from Australian manufacturing industry sector. J. Bus. Ethics 2012, 109, 483–500. [Google Scholar]

- Ducassy, I. Does corporate social responsibility pay off in times of crisis? An alternate perspective on the relationship between financial and corporate social performance. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 157–167. [Google Scholar] [CrossRef]

- Tang, L.; Gallagher, C.C.; Bie, B. Corporate social responsibility communication through corporate websites: A comparison of leading corporations in the United States and China. Int. J. Bus. Commum. 2015, 52, 205–227. [Google Scholar] [CrossRef]

- Zhang, W.; Xue, J. Economically motivated food fraud and adulteration in China: An analysis based on 1553 media reports. Food Control 2016, 67, 192–198. [Google Scholar] [CrossRef]

- Smith, A.D. Corporate social responsibility practices in the pharmaceutical industry. Bus. Strateg. Ser. 2008, 9, 306–315. [Google Scholar] [CrossRef]

- Esteban, D. Strengthening corporate social responsibility in the pharmaceutical industry. J. Med. Mark. 2008, 8, 77–79. [Google Scholar] [CrossRef]

- Lin, X.F.; Xiao, D.D.; Liu, W.J.; Liu, C.J. The analysis and model reconstruction of corporate social responsibility in Chinese pharmaceutical companies. Med. Soc. 2011, 24, 368–371. (In Chinese) [Google Scholar]

- Wang, X.Q.; Xu, P. The empirical study on CSR for Pharmaceutical firms based on stakeholder theory. Stud. Ind. Econ. 2011, 7, 97–98. (In Chinese) [Google Scholar]

- China Food and Drug Administration. The News of Drug-Related Product Accidents. Available online: http://samr.cfda.gov.cn/WS01/CL0412/ (accessed on 30 March 2019).

- Bichta, C. Corporate socially responsible (CSR) practices in the context of Greek industry. Corp. Soc. Responsib. Environ. Manag. 2003, 10, 12–24. [Google Scholar] [CrossRef]

- Frederick, W.C. The growing concern over social responsibility. Calif. Manag. Rev. 1960, 2, 54–61. [Google Scholar] [CrossRef]

- Davis, K. Can business afford to ignore social responsibility. Calif. Manag. Rev. 1960, 2, 70–76. [Google Scholar] [CrossRef]

- Johnson, H.L. A berkeley view of business and society. Calif. Manag. Rev. 1973, 16, 95–100. [Google Scholar] [CrossRef]

- Committee for Economic Development. Social Responsibility of Business Corporations; Research and Business Policy Committee: New York, NY, USA, 1971. [Google Scholar]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pittman: Boston, MA, USA, 1984. [Google Scholar]

- Matten, D.; Crane, A.; Chapple, W. Behind the mask: Revealing the true face of corporate citizenship. J. Bus. Ethics 2003, 45, 109–120. [Google Scholar] [CrossRef]

- Doane, D. The myth of CSR: The problem with assuming that companies can do well while also doing good is that markets don’t really work that way. Stanf. Soc. Innov. Rev. 2005, 3, 22–29. [Google Scholar]

- Orlitzky, M.; Rynes, S.L.; Schmidt, F.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Mohr, L.A.; Webb, D.J.; Harris, K.E. Do Consumers expect companies to be socially responsible? The impact of corporate social responsibility on buying behavior. J. Consum. Aff. 2001, 35, 45–72. [Google Scholar] [CrossRef]

- Jamali, D. The case for strategic corporate social responsibility in developing countries. Bus. Soc. Rev. 2007, 112, 1–27. [Google Scholar] [CrossRef]

- Crane, A.; Matten, D. Business Ethics: Managing Corporate Citizenship and Sustainability in the Age of Globalization; Oxford University Press: Oxford, UK, 2007. [Google Scholar]

- Griesse, M.A. The geographic, political, and economic context for corporate social responsibility in Brazil. J. Bus. Ethics 2007, 73, 21–37. [Google Scholar] [CrossRef]

- Alkhatib, J.A.; Rawwas, M.Y.; Vitell, S.J. Organizational ethics in developing countries: A comparative analysis. J. Bus. Ethics 2004, 55, 309–322. [Google Scholar]

- Chen, H.; Wang, X. Corporate social responsibility and corporate financial performance in China: An empirical research from Chinese firms. Corp. Gov. 2011, 11, 361–370. [Google Scholar] [CrossRef]

- Visser, W. Corporate Citizenship in a Development Perspective; Copenhagen Business School Press: Copenhagen, Denmark, 2006. [Google Scholar]

- Ministry of Commerce of China. Chinese Company Law; Ministry of Commerce of China: Beijing, China, 1994.

- Ministry of Commerce of China. Chinese Company Law; Ministry of Commerce of China: Beijing, China, 2006.

- State-Owned Assets Supervision and Administration Commission of the State Council (SASAC). Guidance for Social Responsibility Implementation for the Stated-Owned Enterprise; SASAC: Beijing, China, 2008.

- State-Owned Assets Supervision and Administration Commission of the State Council. Guide on the SOEs’ Better Performance of CSR; SASAC: Beijing, China, 2016.

- Shanghai Stock Exchange (SHSE). Guide on Environmental Information Disclosure; SHSE: Shanghai, China, 2018. [Google Scholar]

- Maignan, I.; Ferrell, O.C.; Hult, G.T.M. Corporate citizenship in two countries: The case of the United States and France. J. Bus. Ethics 2000, 23, 283–297. [Google Scholar] [CrossRef]

- Crilly, D.; Zollo, M.; Hansen, M.T. Faking it or muddling through? Understanding decoupling in response to stakeholder pressures. Acad. Manag. J. 2012, 55, 1429–1448. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Jones, T.M. Instrumental stakeholder theory: A synthesis of ethics and economics. Acad. Manag. Rev. 1995, 20, 404–437. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Hou, T.C.T. The relationship between corporate social responsibility and sustainable financial performance: Firm-level evidence from Taiwan. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 19–28. [Google Scholar] [CrossRef]

- Lu, R.X.A.; Lee, P.K.C.; Cheng, T.C.E. Socially responsible supplier development: Construct development and measurement validation. Int. J. Prod. Econ. 2012, 140, 160–167. [Google Scholar] [CrossRef]

- Wood, D.J.; Jones, R.E. Stakeholder mismatching: A theoretical problem in empirical research on corporate social performance. Int. J. Organ. Anal. 1995, 3, 229–267. [Google Scholar] [CrossRef]

- Weiss, J.W. Business Ethics: A Stakeholder and Issues Management Approach; South-Western College Publications: Cincinnati, OH, USA, 2008. [Google Scholar]

- Pan, X.; Sha, J.; Zhang, H.; Ke, W. Relationship between Corporate Social Responsibility and Financial Performance in the Mineral Industry: Evidence from Chinese Mineral Firms. Sustainability 2014, 6, 4077–4101. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Branco, M.C.; Rodrigues, L.L. Corporate social responsibility and resource-based perspective. J. Bus. Ethics 2006, 69, 111–132. [Google Scholar] [CrossRef]

- Hart, S.L.; Ahuja, G. Does it pay to be green? An empirical examination of the relationship between emission reduction and firm performance. Bus. Strateg. Environ. 1996, 5, 30–37. [Google Scholar] [CrossRef]

- Wu, W.; Liu, Y.; Chin, T.; Zhu, W. Will green CSR enhance innovation? A perspective of public visibility and firm transparency. Int. J. Environ. Res. Public Health 2018, 15, 268. [Google Scholar] [CrossRef] [PubMed]

- Jiang, X.; Akbar, A. Does increased representation of female executives improve corporate environmental investment? Evidence from China. Sustainability 2018, 10, 4750. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. Quality of management and quality of stakeholder relations: Are they synonymous? Bus. Soc. 1997, 36, 250–279. [Google Scholar] [CrossRef]

- Ma, A.Y.; Jiang, Z.H.; Li, W. The relationship between CSR and financial performance: An empirical study for food and drinking companies. Commun. Financ. Account. 2015, 33, 109–111. (In Chinese) [Google Scholar]

- Hexun CSR Evaluation System. Available online: http://stock.hexun.com/2013/gsshzr/index.html (accessed on 19 January 2019).

- Xiong, B.; Lu, W.; Skitmore, M.; Chau, K.W.; Ye, M. Virtuous nexus between corporate social performance and financial performance: A study of construction enterprises in China. J. Clean. Prod. 2016, 129, 223–233. [Google Scholar] [CrossRef]

- Lee, E.; Walker, M.; Zeng, C.C. Do Chinese state subsidies affect voluntary corporate social responsibility disclosure? J. Account. Public Policy 2017, 36, 179–200. [Google Scholar] [CrossRef]

- Zhong, M.; Xu, R.; Liao, X.; Zhang, S. Do CSR ratings converge in China? A comparison between RKS and Hexun scores. Sustainability 2019, 11, 3921. [Google Scholar] [CrossRef]

- Tang, P.; Yang, S.; Boehe, D. Ownership and corporate social performance in China: Why geographic remoteness matters. J. Clean. Prod. 2018, 197, 1284–1295. [Google Scholar] [CrossRef]

- Zheng, G.; Wang, S.; Xu, Y. Monetary stimulation, bank relationship and innovation: Evidence from China. J. Bank. Financ. 2018, 89, 237–248. [Google Scholar] [CrossRef]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar]

- Ullmann, A. Data in search of a theory: A critical examination of the relationships among social performance, social disclosure, and economic performance. Acad. Manag. Rev. 1985, 10, 540–577. [Google Scholar]

- Branch, B. Misleading Accounting: The Danger and the Potential; Working paper; University of Massachusetts: Amherst, MA, USA, 1983. [Google Scholar]

- Sial, M.; Zheng, C.; Cherian, J.; Gulzar, M.; Thu, P.; Khan, T.; Nguyen, V. Does corporate social responsibility mediate the relation between boardroom gender diversity and firm performance of Chinese listed companies? Sustainability 2018, 10, 3591. [Google Scholar] [CrossRef]

- The State Council of China, Labor Contract Law of China. Available online: http://www.gov.cn/flfg/2008-09/19/content_1099500.htm (accessed on 19 September 2008).

- Laan, G.V.D.; Ees, H.V.; Witteloostuijn, A.V. Corporate social and financial performance: An extended stakeholder theory, and empirical test with accounting measures. J. Bus. Ethics 2008, 79, 299–310. [Google Scholar] [CrossRef]

| Date | Incident | Consequence |

|---|---|---|

| 2019 | Explosion in glutamine manufacturing line of Shenhua Pharma in Jiangsu Province. | Eight persons were severely injured, one person died. |

| 2018 | Injurious hydrophobia vaccine made by Changsheng Pharma in the Jilin Province. | All vaccines were not sold yet, 15 criminals including senior management were arrested. |

| 2017 | False DPT (Diphtheria, Pertussis, Tetanus) vaccine made by Changsheng Pharma in the Jilin Province. | 252,600 vaccines confiscated in the Shangdong Province. |

| 2017 | Misleading advertising for eye drops by SPAS. | There was a significant drop in share price by 40% within a week. |

| 2016 | Injurious vaccine made by an illegal medical factory in the Shandong Province | Vaccines spread into over 10 provinces and some children were infected. |

| 2014 | Counterfeit drugs to treat diabetes manufactured in the Henan Province. | Several patients were affected. |

| 2013 | Injurious vaccine from Kangtai Pharma in the Guangdong Province. | Seven newborn babies died. Deaths were suspected to be caused by the vaccine. |

| 2012 | Toxic capsules made by Hengtai Pharma in the Jiangsu Province. | Thirteen batches of capsules had excessive chromium. |

| 2011 | Plasticizer scandal in Taiwan. | It spread to 294 companies and a total of 973 different products. |

| 2009 | Poor quality of Coptis chinensis injection in the Heilongjiang Province. | One death was reported in this incident. |

| 2008 | Injurious vaccine made by Huawei Pharma in the Shanxi Province. | One death was reported in this incident. |

| 2006 | Visible particles existed in glucose and sodium chloride injections in the Hebei Province. | Nine patients were affected and adverse reactions occurred. |

| Dimension of CSR Performance | Second-Class Measures | Third-Class Measures |

|---|---|---|

| Shareholders (weight ratio: 30%) | Profitability (10%) | ROE (2%) |

| ROA (2%) | ||

| Return of sales (2%) | ||

| Cost margin (1%) | ||

| EPS (2%) | ||

| Retained earnings per share (1%) | ||

| Debt paying (3%) | Quick ratio (0.5%) | |

| Liquidity ratio (0.5%) | ||

| Cash ratio (0.5%) | ||

| Equity ratio (0.5%) | ||

| Asset-liability ration (1%) | ||

| Return (8%) | Dividend capital ratio (2%) | |

| Dividend yield (3%) | ||

| Bonus share allocation ratio of profit (3%) | ||

| Credit (5%) | Number of penalties by stock exchange (5%) | |

| Innovation (4%) | R & D expenditure (1%) | |

| Concept of technological innovation (1%) | ||

| The number of items of technological innovation (2%) | ||

| Employees (weight ratio: 15%, 10% in consumption sector) | Performance (5%) | Per capita incomes of workers (4%) |

| Training of staff (1%) | ||

| Safety (5%) | Periodic security check (2%) | |

| Safety training (3%) | ||

| Caring for employees (5%) | Policy of caring (1%) | |

| Number of caring (2%) | ||

| Caring payments (2%) | ||

| Customers and suppliers (weight ratio: 15%, 10% in consumption sector) | Product quality (7%) | Policy of quality management (3%) |

| Quality management system certificate (4%) | ||

| Customer service (3%) | Customer satisfaction survey (3%) | |

| Mutual good faith (5%) | Vendor fair competition (3%) | |

| Anti-bribery training (2%) | ||

| Environment (weight ratio: 20%, 30% in manufacturing sector, 10% in service sector) | Environmental governance (20%) | Policy of environmental protection (2%) |

| Environmental management system certificate (3%) | ||

| Environmental investment amount (5%) | ||

| Number of types of sewage (5%) | ||

| Number of types of green energy (5%) | ||

| Society (weight ratio: 20%, 30% in service sector, 10% in manufacturing sector) | Contribution (20%) | Tax (10%) |

| Donation amount (10%) |

| Variables | Measurement |

|---|---|

| CSR-SHA | CSR performance on shareholders dimension was extracted from Hexun CSR database. |

| CSR-EMP | CSR performance on employees dimension was extracted from Hexun CSR database. |

| CSR-CUST & SUP | CSR performance on customers and suppliers dimension was extracted from Hexun CSR database. |

| CSR-ENV | CSR performance on the environment dimension was extracted from Hexun CSR database. |

| CSR-SOC | CSR performance on society’s dimension was extracted from Hexun CSR database. |

| CSR | The sum of score of five CSR dimensions extracted from Hexun CSR database |

| Tobin’s Q | Tobin’s Q = total market value of firm/total assets value of firm |

| ROA | Return on assets = net income/total average assets |

| ROE | Return on equity = net income/total average equity |

| EPS | Earnings per share = (net income − preferred dividends)/weighted average shares outstanding |

| LNTA | Natural logarithm of total assets |

| Variables | No. of Observations | Median | Mean | Min. | Max. | S.D. | Skewness |

|---|---|---|---|---|---|---|---|

| Tobin’s Q | 875 | 2.689 | 3.242 | 0 | 16.854 | 2.232 | 1.798 |

| ROA | 875 | 0.660 | 0.069 | −0.298 | 0.494 | 0.641 | 0.204 |

| ROE | 875 | 0.095 | 0.106 | −0.911 | 6.918 | 0.256 | 21.848 |

| EPS | 875 | 0.417 | 0.550 | −1.148 | 4.100 | 0.593 | 1.960 |

| CSR | 875 | 24.7500 | 29.5180 | −11.4600 | 87.2200 | 17.8389 | 1.2651 |

| CSR-SHA | 875 | 57.567 | 54.174 | −11.433 | 92.333 | 20.466 | −0.749 |

| CSR-EMP | 875 | 12.300 | 22.874 | 0 | 100.000 | 26.016 | 1.582 |

| CSR-CUST & SUP | 875 | 0 | 14.560 | 0 | 100.000 | 32.215 | 1.809 |

| CSR-ENV | 875 | 0 | 10.400 | 0 | 100.000 | 23.642 | 2.026 |

| CSR-SOC | 875 | 28.350 | 30.789 | −50.000 | 85.000 | 16.489 | −0.431 |

| LNTA | 875 | 21.669 | 21.716 | 19.032 | 25.0187 | 1.002 | 0.143 |

| Tobin’s Q | ROA | ROE | EPS | LNTA | CSR | CSR-SHA | CSR-EMP | CSR-CUST & SUP | CSR-ENV | CSR-SOC | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Tobin’s Q | 1 | ||||||||||

| ROA | 0.350 ** | 1 | |||||||||

| ROE | 0.091 ** | 0.483 ** | 1 | ||||||||

| EPS | 0.072 * | 0.616 ** | 0.260 ** | 1 | |||||||

| LNTA | 0-.380 ** | 0.067 * | 0.015 | 0.326 ** | 1 | ||||||

| CSR | −0.024 | 0.377 ** | 0.032 * | 0.424 ** | 0.294 ** | 1 | |||||

| CSR-SHA | 0.155 ** | 0.693 ** | 0.222 ** | 0.590 ** | 0.272 ** | 0.610 ** | 1 | ||||

| CSR-EMP | 0.003 | 0.248 ** | 0.164 ** | 0.309 ** | 0.226 ** | 0.879 ** | 0.330 ** | 1 | |||

| CSR-CUST & SUP | 0.006 | 0.216 ** | 0.142 ** | 0.240 ** | 0.197 ** | 0.911 ** | 0.289 ** | 0.912 ** | 1 | ||

| CSR-ENV | −0.015 | 0.199 ** | 0.114 ** | 0.247 ** | 0.205 ** | 0.902 ** | 0.286 ** | 0.883 ** | 0.964 ** | 1 | |

| CSR-SOC | −0.080 * | 0.114 ** | 0.075 * | 0.097 ** | 0.135 ** | 0.499 ** | 0.157 ** | 0.298 ** | 0.332 ** | 0.335 ** | 1 |

| Dependent Variables | ||||

|---|---|---|---|---|

| Tobin’s Q | ROA | ROE | EPS | |

| Independent variable | ||||

| CSR | −0.0345 *** | 0.0009 *** | 0.0033 * | 0.0059 *** |

| Control variable | ||||

| Size | −2.2433 *** | −0.0071 | −0.1025 *** | 0.1051 ** |

| Constant | 51.1818 *** | 0.1981 | 2.2582 *** | −1.9091 * |

| Adjusted R2 | 0.6523 | 0.5296 | 0.3973 | 0.6707 |

| F-statistics | 12.8926 *** | 8.3383 *** | 7.0462 *** | 14.2751 *** |

| Durbin–Watson | 2.2095 | 1.8129 | 2.3988 | 1.1661 |

| Dependent Variables | ||||

|---|---|---|---|---|

| Tobin’s Q | ROA | ROE | EPS | |

| Independent Variable | ||||

| Shareholders (CSR-SHA) | 0.0038 ** | 0.0016 *** | 0.0026 *** | 0.0105 *** |

| Employees (CSR-EMP) | −0.0017 | 0.0001 *** | 0.0012 *** | 0.0005 * |

| Customers and suppliers (CSR-CUST & SUP) | −0.0014 | 0.0001 ** | 0.0008 *** | 0.0001 |

| The environment (CSR-ENV) | −0.0016 | 0.0001 ** | 0.0009 *** | 0.0002 |

| Society (CSR-SOC) | −0.0023 | 0.0001 ** | 0.0004 *** | 0.0010 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, M.; Bento, P.; Akbar, A. Does CSR Influence Firm Performance Indicators? Evidence from Chinese Pharmaceutical Enterprises. Sustainability 2019, 11, 5656. https://doi.org/10.3390/su11205656

Yang M, Bento P, Akbar A. Does CSR Influence Firm Performance Indicators? Evidence from Chinese Pharmaceutical Enterprises. Sustainability. 2019; 11(20):5656. https://doi.org/10.3390/su11205656

Chicago/Turabian StyleYang, Minghui, Paulo Bento, and Ahsan Akbar. 2019. "Does CSR Influence Firm Performance Indicators? Evidence from Chinese Pharmaceutical Enterprises" Sustainability 11, no. 20: 5656. https://doi.org/10.3390/su11205656

APA StyleYang, M., Bento, P., & Akbar, A. (2019). Does CSR Influence Firm Performance Indicators? Evidence from Chinese Pharmaceutical Enterprises. Sustainability, 11(20), 5656. https://doi.org/10.3390/su11205656