From Niche to Market—An Agent-Based Modeling Approach for the Economic Uptake of Electro-Fuels (Power-to-Fuel) in the German Energy System

, and

, and

Abstract

1. Introduction

2. Current State of Affairs of P2F in Germany and Methodological Approach

- Reduction of investment costs

- High conversion efficiencies

- High utilization rates

- Reasonable legal framing conditions

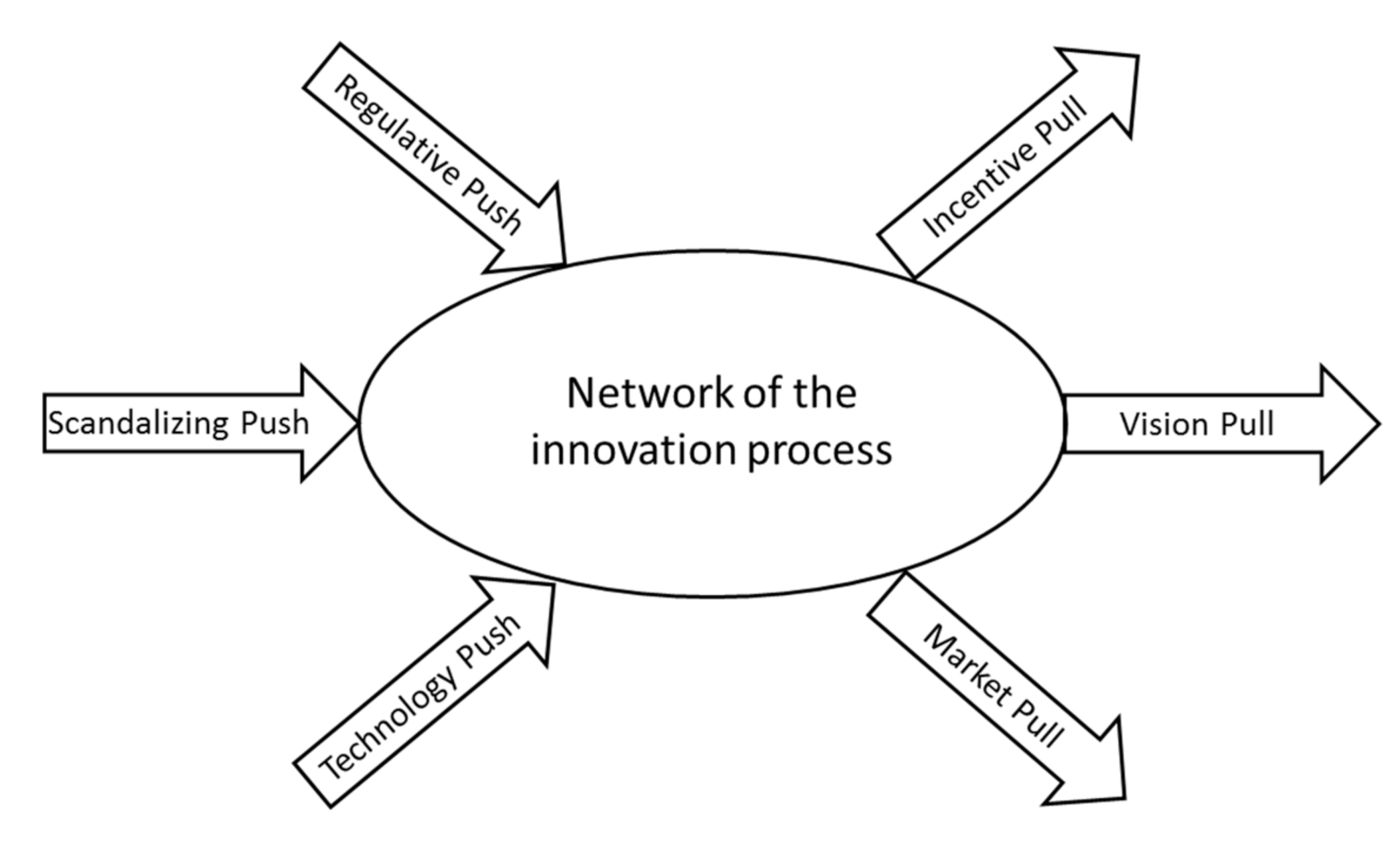

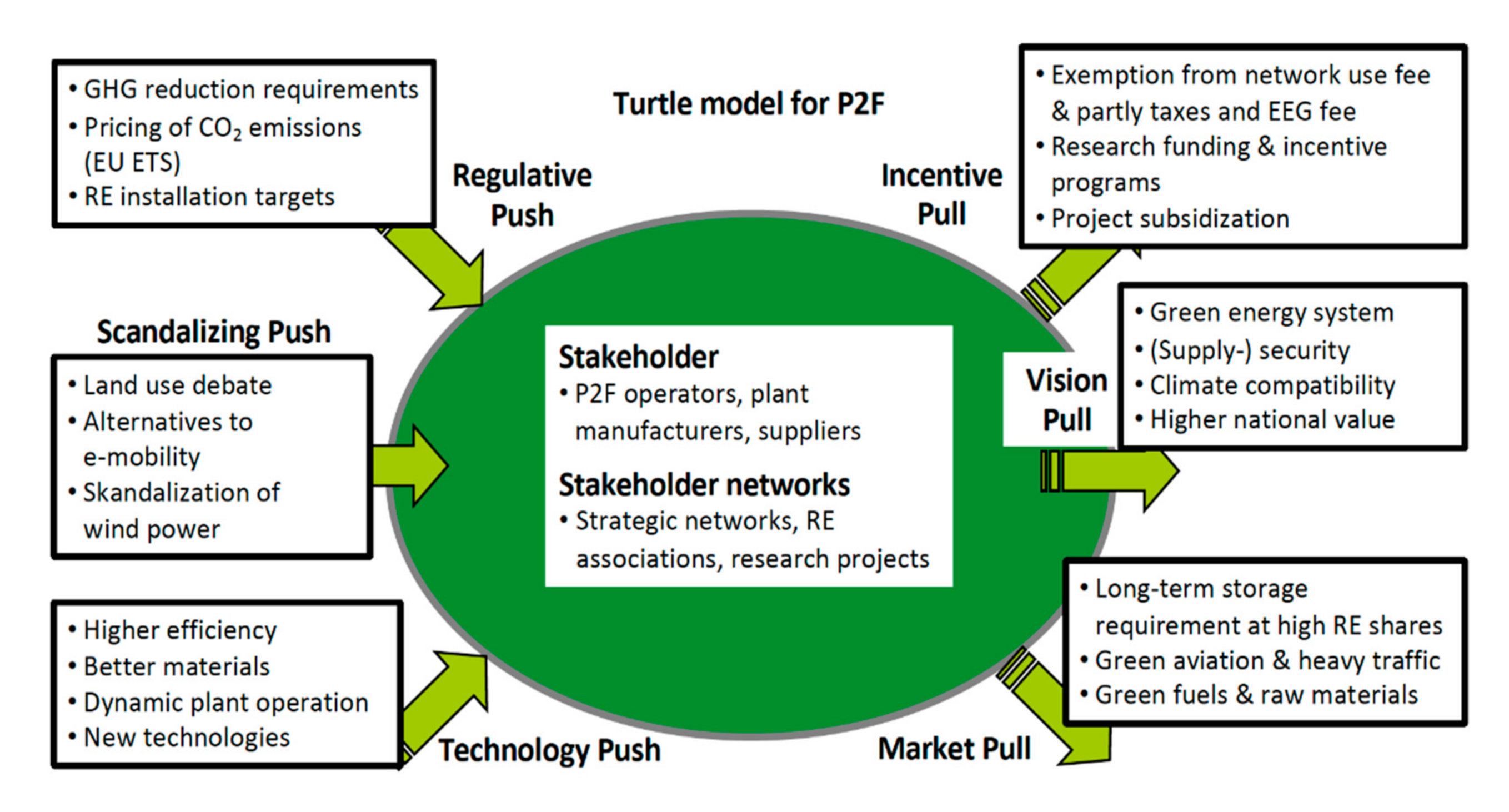

2.1. Defining Framing Conditions with the Help of the Turtle Model

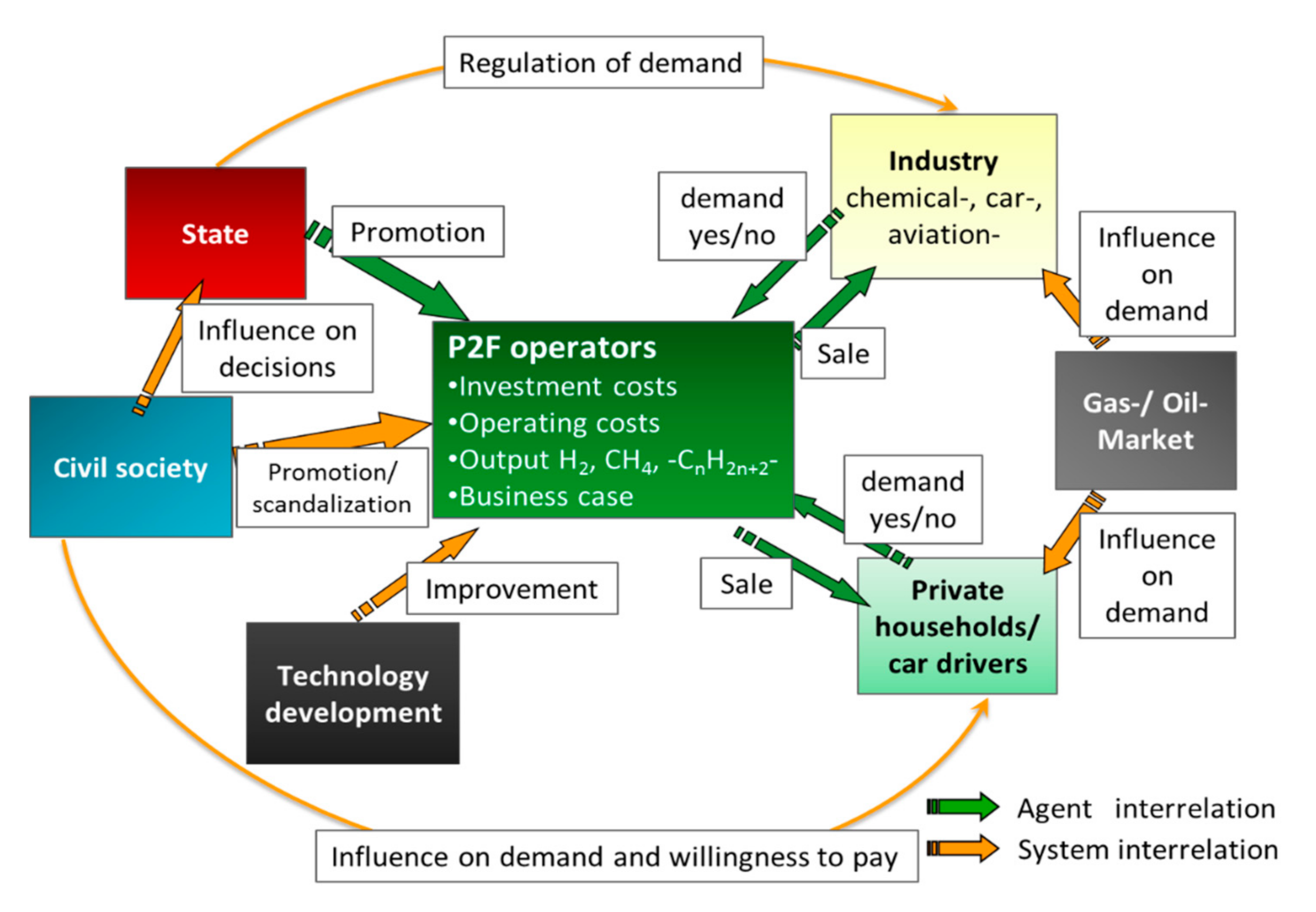

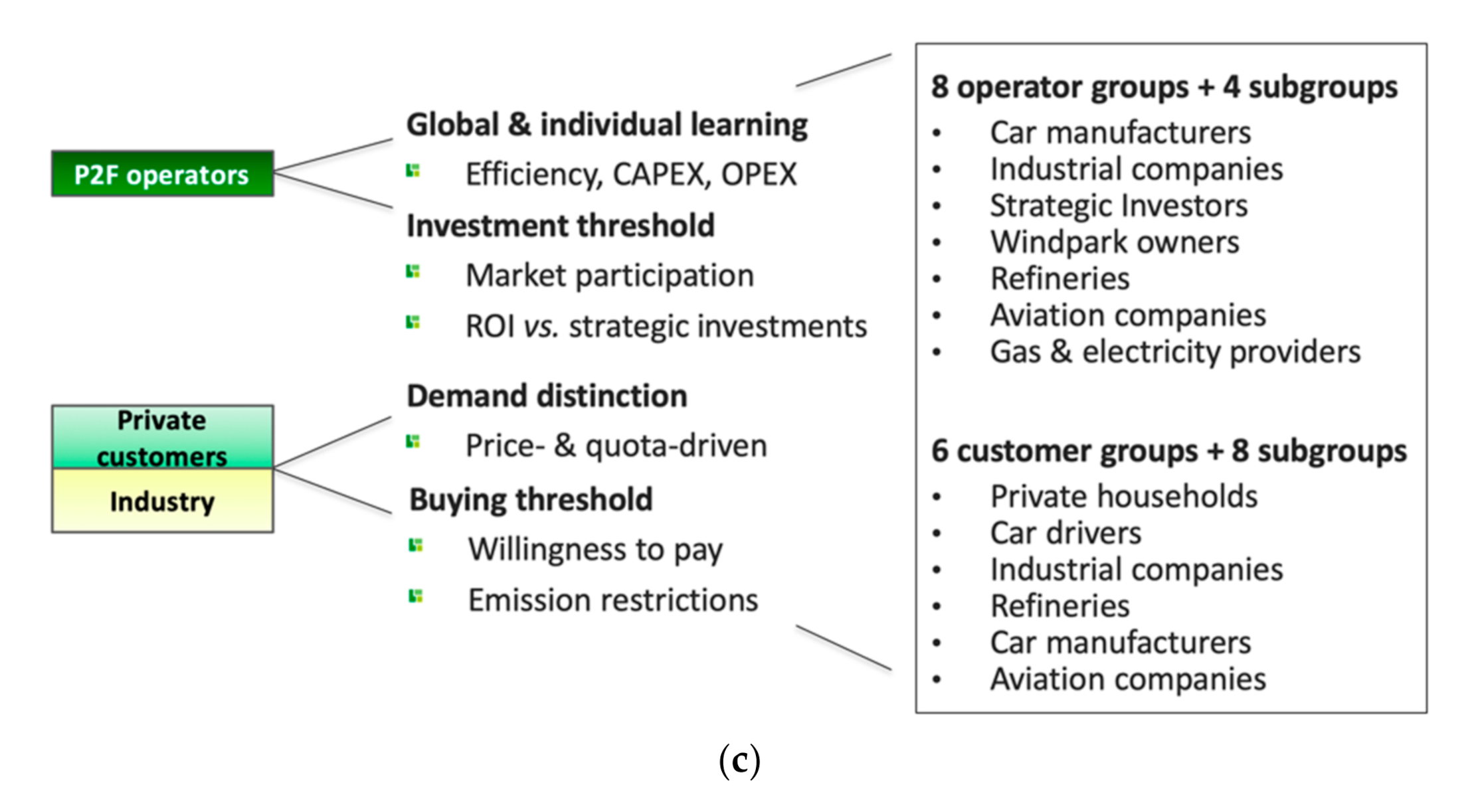

2.2. Conceptualization of the Agent-Based Model

2.3. General Model Description

3. Scenario Description with Consideration of Potential Markets and Legal Aspects for P2F

3.1. Legal Aspects

3.2. Description of Scenarios

4. Results and Discussion

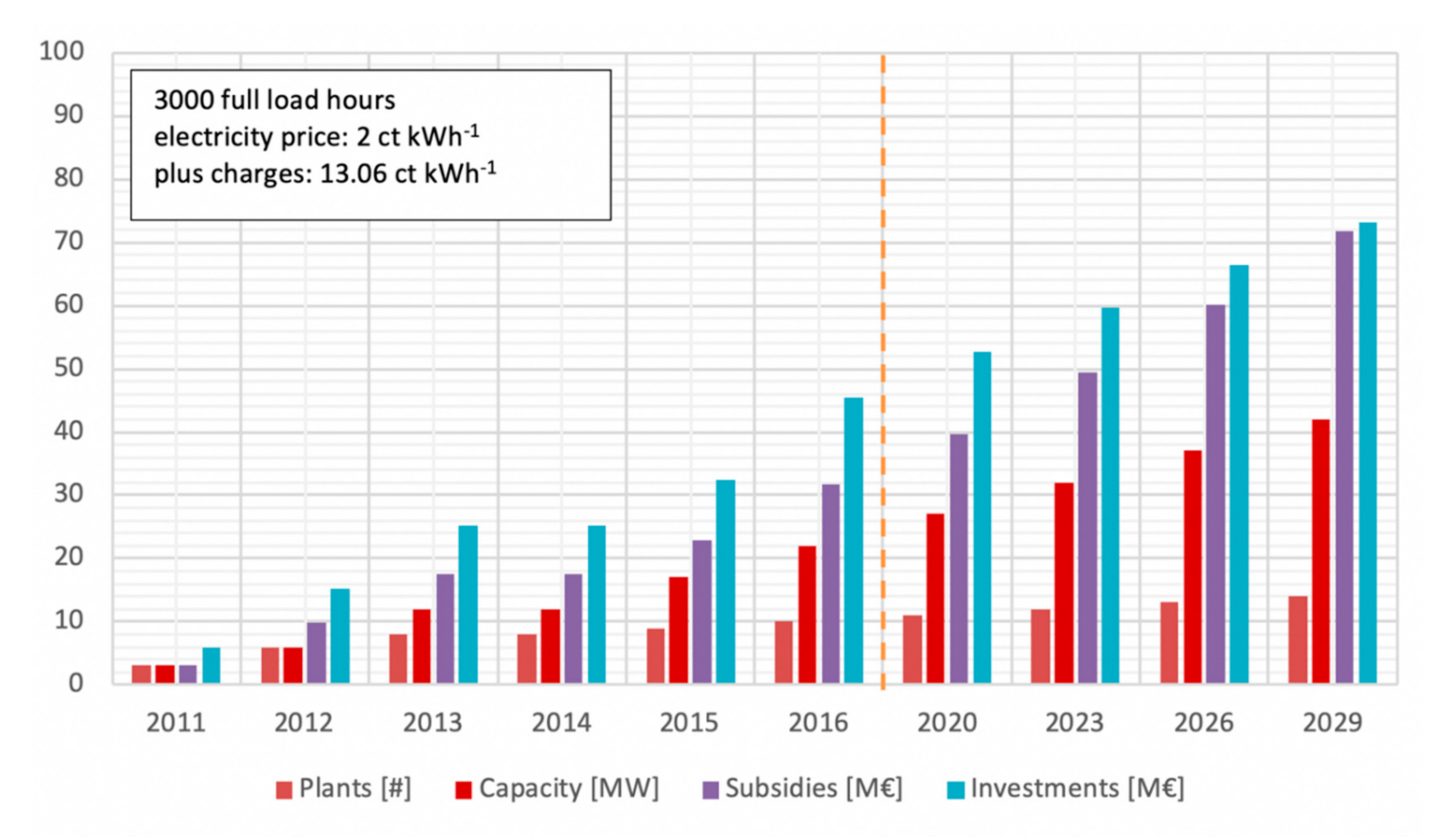

4.1. Model Calibration and Base Scenario

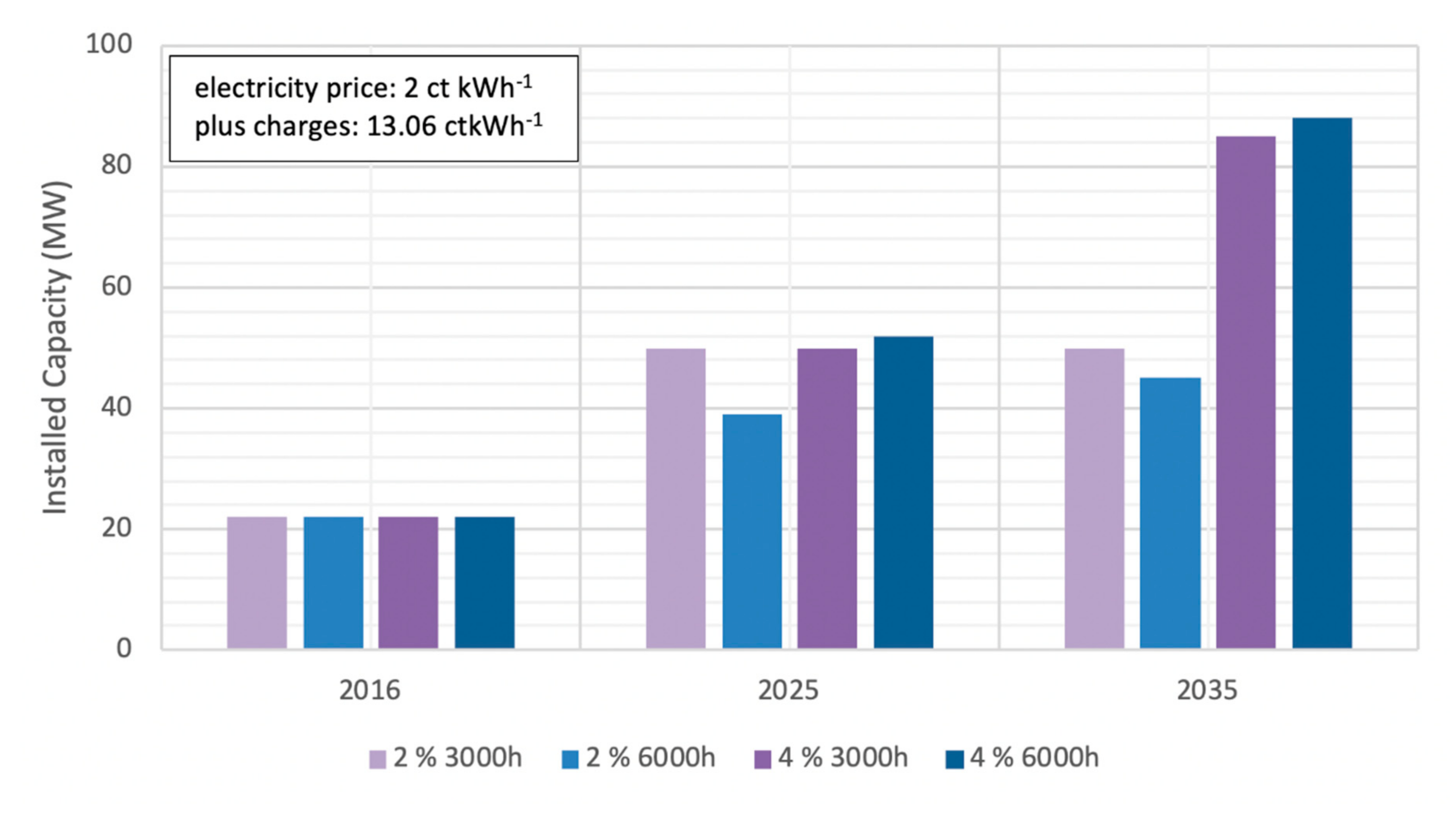

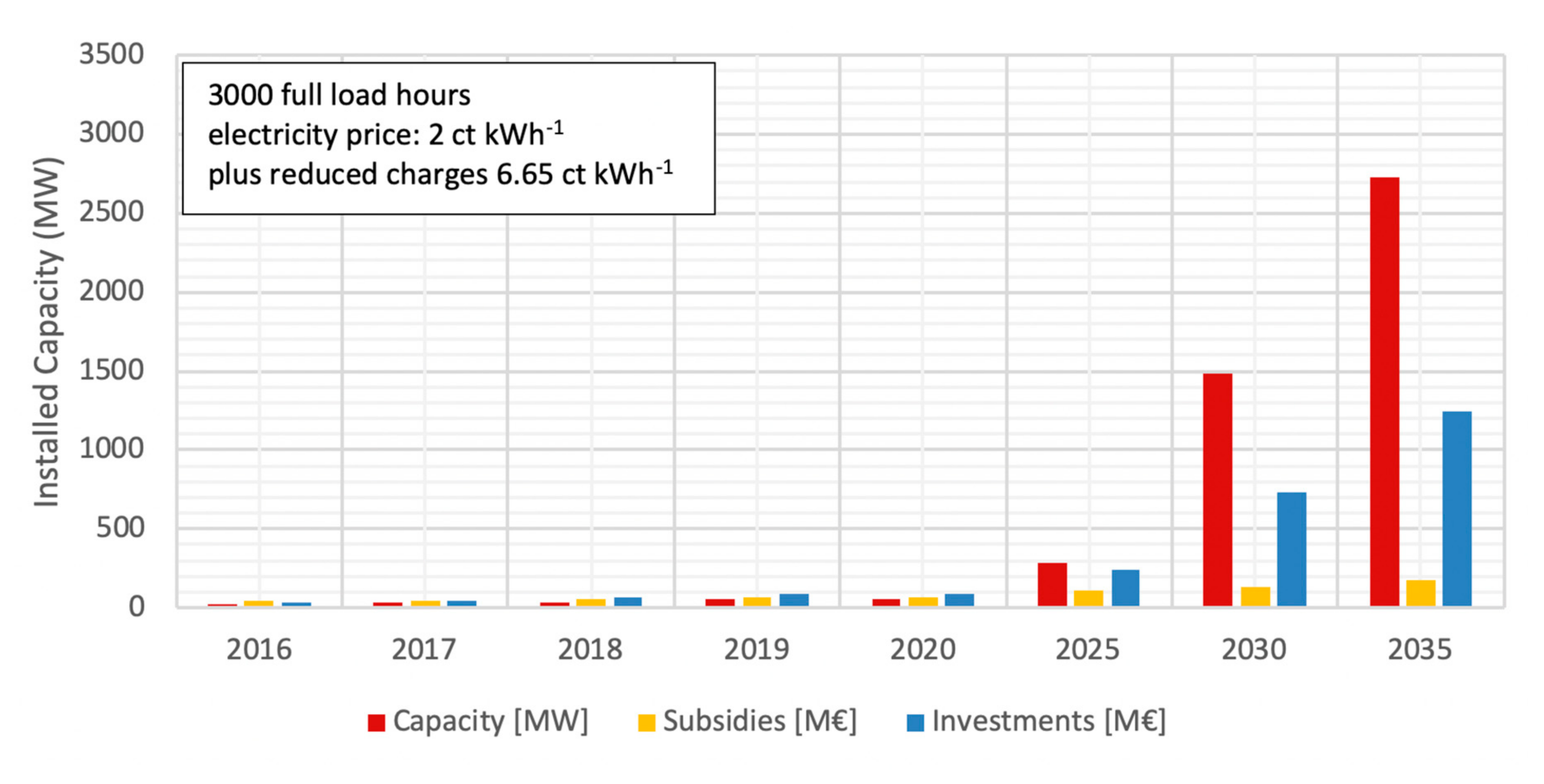

4.2. Moderate Policy Scenario

- ○

- Conventional energy price rise of 2% a−1

- ○

- Conventional energy price rise of 4% a−1

- ○

- 3000 full load hours in relation to electrolysis capacity

- ○

- 6000 full load hours in relation to electrolysis capacity

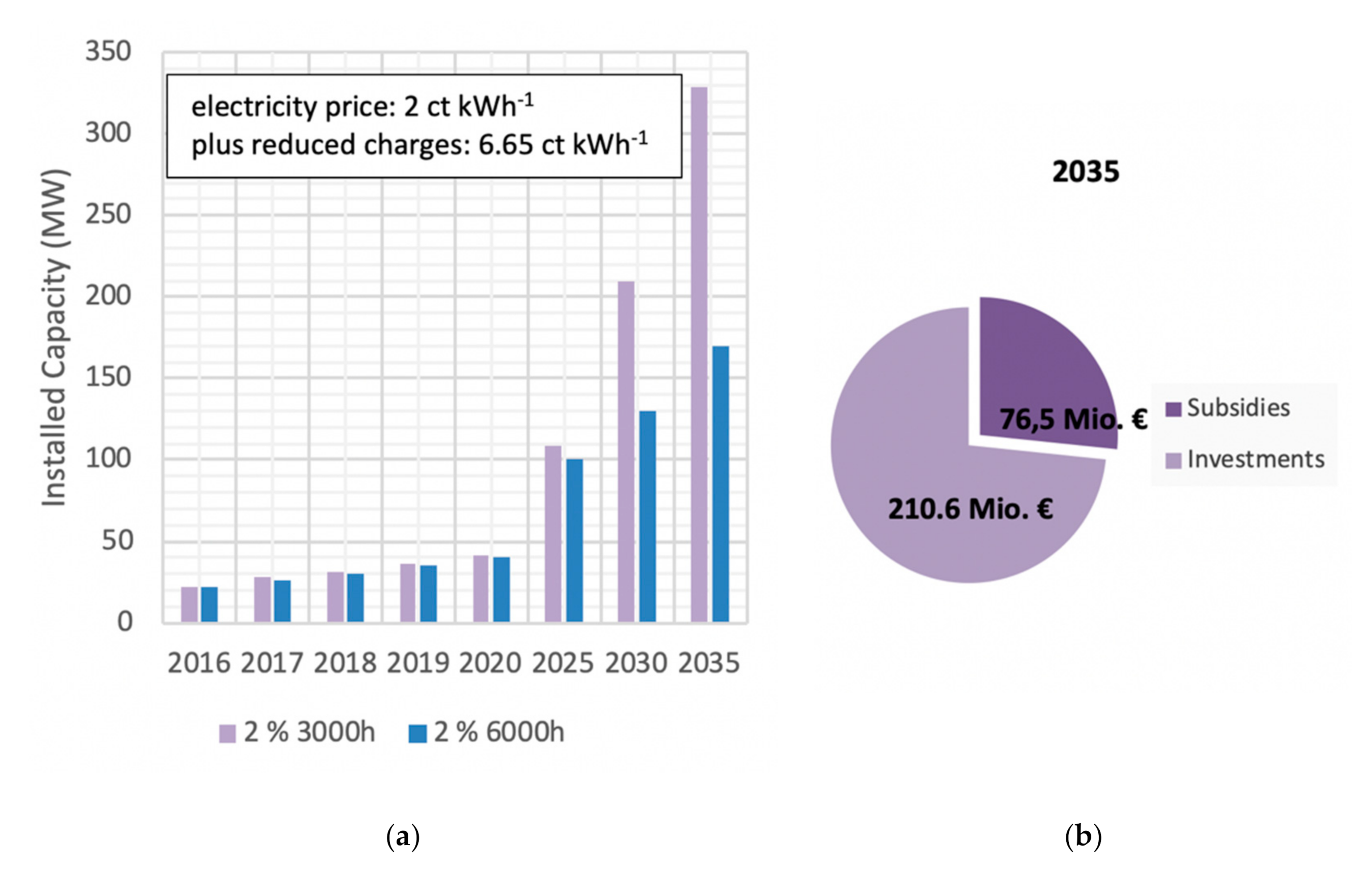

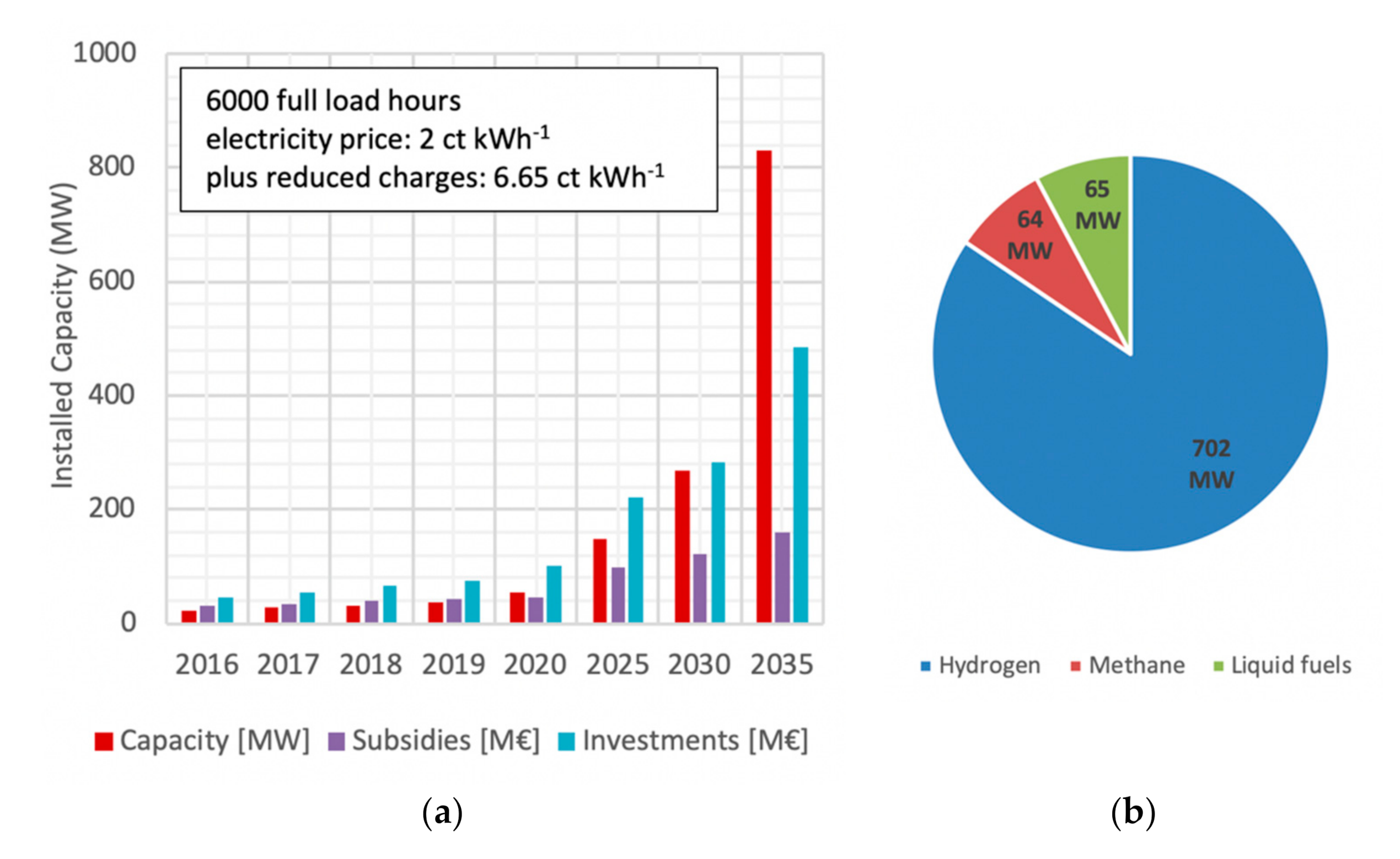

4.3. EnergiewendePlus (EW+) Scenario: Optimizing Parameters for an Ambitious Energy System Transformation

4.3.1. EEG—Fee Exemption

4.3.2. Biofuel Recognition

4.3.3. High Willingness-to-Pay

4.3.4. Strong Legal Regulations

- High EU ETS certificate price of 100 € ton CO₂−1 from 2021 on

- Strong start-up subsidization of 60 million € a−1 until 2025

- Strong GHG reduction quotas for industrial companies leading to a WTP of up to 30%.

4.4. Discussion of Model Results in Comparison to External Studies

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Operators | ||||

|---|---|---|---|---|

| Operator Group | Customer Base | Techs | Budget/Scale | Investment Criterion |

| Progressive Car Manufacturers | Mobility | All | Medium | Strategic |

| Conservative Car Manufacturers | Mobility | All | Large | Profitable |

| Progressive Industry | Industry | All | Medium | Strategic |

| Conservative Industry | Industry | All | Large | Profitable |

| Strategic P2F investor | Broad | All | Medium | Strategic |

| Wind park operators (big) | Broad | All | Medium | Profitable |

| Wind park operators (small) | Broad | P2H2/P2M | Small | Profitable |

| Electricity provider | Broad | P2H2/P2M | Medium | Profitable |

| Refinery-hydrogen investments | Refineries | P2H | Large | Strategic |

| Refinery—liquid investments | Refineries | P2L | Medium | Strategic |

| Progressive gas provider | Households | P2H2/P2M | Medium | Strategic |

| Conservative gas provider | Households | P2H2/P2M | Large | Profitable |

| Customers | ||||

| Customer Group | Substitute | Product | Potential Demand | Incentive |

| Green households | Hydrogen, methane | Gas | Medium | Willing to pay |

| Green+ households | Hydrogen, methane | Gas | Very small | Willing to pay |

| Green car drivers | Methane, liquid fuel | Liquid fuel | Small | Willing to pay |

| Fuel cell mobility | Hydrogen | Fossil hydrogen | Small | Willing to pay |

| Green H2 industry | Hydrogen | Fossil hydrogen | Small | Willing to pay |

| Green gas industry | Hydrogen, methane | Gas | Small | Willing to pay |

| Green liquid industry | Liquid fuel | Mineral oil | Small | Willing to pay |

| H2-oriented refineries | Hydrogen | Biofuel | Large | Quota |

| Liquid-oriented refineries | Liquid fuel | Biofuel | Large | Quota |

| Gas-based car industry | Methane | Biofuel | Medium | Quota |

| Liquid-based car industry | Liquid fuel | Biofuel | Medium | Quota |

| Subsidizer | ||||

| Subsidizer Group | Substitute | Subsidy per Year | ||

| Power-to-hydrogen subsidizer | Hydrogen | 3 million euro | ||

| Power-to-methane subsidizer | Methane | 3 million euro | ||

| Power-to-liquid subsidizer | Liquid fuel | 2 million euro | ||

| Technology Classes | ||||

| Technology Class | Initial Relative Investment Cost | Initial Efficiency | Pre-Existing (Input) Capacity | |

| Power-to-hydrogen | 1500 €/kW | 65% | 12 MW | |

| Power-to-methane | 3000 €/kW | 55% | 8 MW | |

| Power-to-liquid | 3500 €/kW | 50% | 1 MW | |

| Environment | ||||

| Environment Variable | Status | Initial Value | ||

| Fixed operating costs in % of investment | 4% | |||

| Individual relative fixed operating cost reduction per year of experience | 2% | |||

| Maximum individual relative fixed operating cost reduction | 20% | |||

| Tax per kWh related to legal status of P2F operators | End Consumer: | 0.1306 €/kWh | ||

| Energy-Intensive Industry: | 0.0765 €/kWh | |||

| Storage: | 0.0665 €/kWh | |||

| Locally produced RE: | 0.0254 €/kWh | |||

| Legal status of P2F operators | End Consumer | |||

| EU ETS certificate price | 6.5 €/tonCO2eq | |||

| Average utilization of renewable energy plants | 22% | |||

| Biofuels quota for refineries | 6% | |||

| Electricity price | 0.02 €/kWh | |||

References

- Umweltbundesamt (UBA). Zeitreihen zur Entwicklung der Erneuerbaren Energien in Deutschland, Dessau-Roßlau. 2020. Available online: https://www.erneuerbare-energien.de/EE/Navigation/DE/Service/Erneuerbare_Energien_in_Zahlen/Zeitreihen/zeitreihen.html (accessed on 20 October 2020).

- Bundesministerium für Umwelt, Naturschutz und Nukleare Sicherheit (BMUB). Climate Action Plan 2050 Berlin. 2016. Available online: https://www.bmu.de/fileadmin/Daten_BMU/Pools/Broschueren/klimaschutzplan_2050_en_bf.pdf (accessed on 20 October 2020).

- Kreyenberg, D.; Lischke, A.; Bergk, F.; Duennebeil, F.; Heidt, C.; Knoerr, W.; Raksha, T.; Schmidt, P.; Weindorf, W.; Naumann, K. Erneuerbare Energien im Verkehr Potenziale und Entwicklungsperspektiven Verschiedener Erneuerbarer Energieträger und Energieverbrauch der Verkehrsträger. Berlin. 2015. Available online: https://www.bmvi.de/SharedDocs/DE/Anlage/G/MKS/mks-kurzstudie-ee-im-verkehr.pdf?__blob=publicationFile (accessed on 20 October 2020).

- Lütkehus, I.; Adlunger, K.; Salecker, H. Potenzial der Windenergie an Land: Studie zur Ermittlung des Bundesweiten Flächen-und Leistungspotenzials der Windenergienutzung an Land Umweltbundesamt: Dessau-Roßlau, Germany. 2013. Available online: https://www.umweltbundesamt.de/sites/default/files/medien/378/publikationen/potenzial_der_windenergie.pdf (accessed on 20 October 2020).

- Agentur für Erneuerbare Energien (AfEE). Metaanalyse. Potenziale der Bioenergie. 2014. Available online: https://www.unendlich-viel-energie.de/presse/pressemitteilungen/nutzungspfade-der-bioenergie-gibt-es-den-koenigsweg (accessed on 20 October 2020).

- Brosowski, A.; Thrän, D.; Mantau, U.; Mahro, B.; Erdmann, G.; Adler, P.; Stinner, W.; Reinhold, G.; Hering, T.; Blanke, C. A review of biomass potential and current utilisation—Status quo for 93 biogenic wastes and residues in Germany. Biomass Bioenerg. 2016, 95, 257–272. [Google Scholar] [CrossRef]

- Deutscher Bundestag Sachstand. Die Einführung von Quoten für Biokraftstoff und von E 10-Benzin in Deutschland; Wissenschaftliche Dienste: Munich, Germany, 2017. [Google Scholar]

- Bergk, F.; Knörr, W. Klimaschutz im Verkehr: Neuer Handlungsbedarf nach dem Pariser Klimaschutzabkommen—Teilbericht des Projekts “Klimaschutzbeitrag des Verkehrs 2050“ Dessau-Roßlau. 2017. Available online: https://www.umweltbundesamt.de/sites/default/files/medien/1410/publikationen/2017-07-18_texte_45-2017_paris-papier-verkehr_v2.pdf (accessed on 20 October 2020).

- Nitsch, J. Die Energiewende nach COP 21-Aktuelle Szenarien der Deutschen Energieversorgung. Stuttgart. 2016. Available online: https://www.bee-ev.de/fileadmin/Publikationen/Studien/Joachim_Nitsch_Energiewende_nach_COP21.pdf (accessed on 20 October 2020).

- Quaschning, V. Sektorkopplung durch die Energiewende- Anforderungen an den Ausbau Erneuerbarer Energien zum Erreichen der Pariser Klimaschutzziele unter Berücksichtigung der Sektorkopplung. Berlin. 2016. Available online: https://www.volker-quaschning.de/publis/studien/sektorkopplung/Sektorkopplungsstudie.pdf (accessed on 20 October 2020).

- Bundesnetzagentur (BNetzA). Quartalsbericht zu Netz- und Systemsicherheitsmaßnahmen. Zweites bis Drittes Quartal 2018. Bonn. 2019. Available online: https://www.bundesnetzagentur.de/SharedDocs/Mediathek/Berichte/2019/Quartalsbericht_Q2Q3_2018.pdf?__blob=publicationFile&v=2 (accessed on 20 October 2020).

- Agora Energiewende Stromspeicher in der Energiewende-Untersuchung zum Bedarf an neuen Stromspeichern in Deutschland für den Erzeugungsausgleich, Systemdienstleistungen und im Verteilnetz Berlin. 2014. Available online: https://www.agora-energiewende.de/fileadmin2/Projekte/2013/speicher-in-der-energiewende/Agora_Speicherstudie_Web.pdf (accessed on 20 October 2020).

- Benndorf, R.; Bernicke, M.; Bertram, A. Greenhouse Gas Neutral Germany in 2050. Dessau-Roßlau. 2014. Available online: https://www.umweltbundesamt.de/sites/default/files/medien/378/publikationen/07_2014_climate_change_en.pdf (accessed on 20 October 2020).

- Purr, K.; Osiek, D.; Lange, M.; Adlunger, K.; Burger, A.; Hain, B.; Kuhnhenn, K.; Klaus, T.; Lehmann, H.; Monch, L.; et al. Integration of Power to Gas/ Power to Liquids into the Ongoing Transformation Process. Dessau-Roßlau. 2016. Available online: https://www.umweltbundesamt.de/sites/default/files/medien/377/publikationen/uba_position_powertoliquid_engl.pdf (accessed on 20 October 2020).

- Breyer, C.; Tsupari, E.; Tikka, V.; Vainikka, P. Power-to-Gas as an Emerging Profitable Business Through Creating an Integrated Value Chain. Energ. Proced. 2015, 73, 182–189. [Google Scholar] [CrossRef]

- Graves, C.R.; Ebbesen, S.D.; Mogensen, M.B.; Lackner, K.S. Sustainable hydrocarbon fuels by recycling CO2 and H2O with renewable or nuclear energy. Renew. Sustain. Energ. Rev. 2011, 15, 1–23. [Google Scholar] [CrossRef]

- König, D.H.; Baucks, N.; Dietrich, R.-U.; Wörner, A. Simulation and evaluation of a process concept for the generation of synthetic fuel from CO2 and H2. Energy 2015, 91, 833–841. [Google Scholar] [CrossRef]

- Golling, C.; Heuke, R.; Seidl, H.; Uhlig, J. Roadmap Power to Gas—Baustein einer Integrierten Energiewende. Berlin. 2017. Available online: https://www.powertogas.info/fileadmin/dena/Dokumente/Pdf/9215_Broschuere_Baustein_einer_Integrierten_Energiewende_Roadmap_Power_to_Gas.pdf (accessed on 20 October 2020).

- Bünger, U.; Michalski, J.Z. Ermittlung des volkswirtschaftlichen sowie des klimarelevanten Nutzens mittels Power-to-Gas-Eine Expertise für Open Grid Europe GmbH und Amprion GmbH—Endbericht. Ottobrunn. 2018. Available online: http://www.lbst.de/news/2018_docs/Studie_Sektorenkopplung_Kurzfassung.pdf (accessed on 20 October 2020).

- Schenuit, C.; Heuke, R.; Paschke, J. Potenzialatlas Power to Gas. Klimaschutz Umsetzen, Erneuerbare Energien Integrieren, Regionale Wertschöpfung Ermöglichen. Berlin. 2016. Available online: https://www.dena.de/fileadmin/dena/Dokumente/Pdf/9144_Studie_Potenzialatlas_Power_to_Gas.pdf (accessed on 20 October 2020).

- Bundesministerium für Verkehr, Bau und Stadtentwicklung (BMVBS). Globale und Regionale Räumliche Verteilung von Biomassepotenzialen. 2010. Available online: https://www.bbsr.bund.de/BBSR/DE/veroeffentlichungen/ministerien/bmvbs/bmvbs-online/2010/DL_ON272010.pdf?__blob=publicationFile&v=1 (accessed on 20 October 2020).

- Nitsch, J.; Pregger, T.; Naegler, T.; Heide, D.; de Tena, D.L.; Trieb, F.; Scholz, Y.; Nienhaus, K.; Gerhardt, N.; Sterner, M.; et al. Langfristszenarien und Strategien für den Ausbau der Erneuerbaren Energien in Deutschland bei Berücksichtigung der Entwicklung in Europa und Global. 2012, p. 345. Available online: https://www.dlr.de/dlr/Portaldata/1/Resources/bilder/portal/portal_2012_1/leitstudie2011_bf.pdf (accessed on 20 October 2020).

- Benndorf, R.; Bemicke, M.; Bertram, A.; Butz, W.; Dettling, F.; Drotleff, J.; Zietlow, B. Treibhausgasneutrales Deutschland im Jahr 2050. 2013. Available online: https://www.umweltbundesamt.de/sites/default/files/medien/376/publikationen/treibhausgasneutrales_deutschland_im_jahr_2050_langfassung.pdf (accessed on 20 October 2020).

- Blanck, R.; Kasten, P.; Hacker, F.; Mottschall, M. Treibhausgasneutraler Verkehr 2050: Ein Szenario zur zunehmenden Elektrifizierung und dem Einsatz stromerzeugter Kraftstoffe im Verkehr; Öko-Institut e.V: Berlin, Germany, 2013. [Google Scholar]

- Henning, H.-M.; Palzer, A. Was kostet die Energiewende?-Wege zur Transformation des deutschen Energiesystems bis 2050—Präsentation. Freiburg. 2015. Available online: https://www.ise.fraunhofer.de/content/dam/ise/de/documents/publications/studies/Fraunhofer-ISE-Studie-Was-kostet-die-Energiewende.pdf (accessed on 20 October 2020).

- Jean, M.D.S.; Baurens, P.; Bouallou, C.; Couturier, K. Economic assessment of a power-to-substitute-natural-gas process including high-temperature steam electrolysis. Int. J. Hydrog. Energ. 2015, 40, 6487–6500. [Google Scholar] [CrossRef]

- Müller-Syring, G.; Henel, M.; Köppel, W.; Mlaker, H.; Sterner, M.; Höcher, T. Entwicklung von modularen Konzepten zur Erzeugung, Speicherung und Einspeisung von Wasserstoff und Methan ins Erdgasnetz. 2013. Available online: https://www.dvgw.de/medien/dvgw/forschung/berichte/g1_07_10.pdf (accessed on 20 October 2020).

- Dierkes, M.; Hoffmann, U.; Marz, L. Leitbild und Technik: Zur Entstehung und Steuerung Technischer Innovationen; Ed. Sigma: Berlin, Germany, 1992. [Google Scholar]

- Lehr, U.; Lobbe, K. Umweltinnovationen-Anreize und Hemmnisse. Ökolog. Wirtschaf. Fachzeit. 1999, 14, 14. [Google Scholar] [CrossRef][Green Version]

- Fichter, K.; von Gleich, A.; Pfriem, R.; Siebenhüner, B. Theoretische Grundlagen für Klimaanpassungsstrategien. nordwest2050-Berichte. Nord. Ber. 2010, 2191–3218. [Google Scholar]

- Hemmelskamp, J. Umweltpolitik und Technischer Fortschritt: Eine Theoretische und Empirische Untersuchung der Determinanten von Umweltinnovationen; Springer-Verlag: Heidelberg, Germany, 2013; ISBN 978-3-662-13259-3. [Google Scholar]

- Ahrens, A.; Gleich, A. v Leitbilder in der Chemikalienentwicklung und Stoffpolitik (Bericht vom SubChem-Workshop). Hamburg. 2002. Available online: http://www.tecdesign.uni-bremen.de/subchem/pdf/Leitbild_Bericht_final_0803.pdf (accessed on 20 October 2020).

- Fichter, K. Einflussfaktoren: Das Gefüllte Schildkrötenmodell als Basiskonzept. 2006. Available online: https://www.yumpu.com/de/document/view/24208492/einflussfaktoren-das-gefa-1-4-llte-schildkratenmodell-als-borderstep (accessed on 20 October 2020).

- Stührmann, S.; von Gleich, A.; Brand, U.; Gößling-Reisemann, S. Mit dem Leitkonzept Resilienz auf dem Weg zu resilienteren Energieinfrastrukturen. Syst. Auf Innov. Tech. Tech. Berl. Ed. Sigma 2012, 181–192. [Google Scholar]

- Brand, U. Abschlussbericht zum Umsetzungsbaustein 1: “Schaffung von Gemeinsamer Identität und Verantwortung der Bewohner durch Energie-und Kosteneffiziente Sanierungs-und Entwicklungsplanung”—Teilprojekt: Analyse und Prozessbegleitende Untersuchung der Richtungsgebenden Einflussfaktoren; BMBF-Projekt ZukunftsWerkStadt Leutkirch, 2013. [Google Scholar]

- Wachsmuth, J.; Petschow, U.; Brand, U.; Fettke, U.; Pissarskoi, E.; Fuchs, G.; Dickel, S.; Kljajic, M. Richtungsgebende Einflussfaktoren im Spannungsfeld von Zentralen vs. de-zentralen Orientierungen bei der Energiewende und Ansatzpunkte für ein Leitkonzept Resilienz. 2015. Available online: http://www.resystra.de/files/publikationen/richtungsgebende-einflussfaktoren.master.pdf (accessed on 20 October 2020).

- Brand, U. Leitkonzepte Nachhaltigkeit und Resilienz als Richtungsgeber in Transformationsprozessen von Energiesystemen, Universität Bremen. 2016. Available online: http://www.resystra.de/files/publikationen/dissertation-von-urte-brand.master.pdf (accessed on 20 October 2020).

- Bundesministerium für Wirtschaft und Energie (BMWi). Hintergrundinformationen zur Besonderen Ausgleichsregelung- Antragsverfahren 2017 für Begrenzung der EEG-Umlage 2018. Berlin. 2018. Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Energie/hintergrundinformationen-zur-besonderen-ausgleichsregelung-antragsverfahren.pdf?__blob=publicationFile&v=24 (accessed on 20 October 2020).

- Van Dam, K.H.; Nikolic, I.; Lukszo, Z. Agent-Based Modelling of Socio-Technical Systems; Springer: Dordrecht, The Netherlands, 2013; ISBN 978-94-007-4932-0. [Google Scholar]

- Boudon, R. Beyond Rational Choice Theory. Annu. Rev. Sociol. 2003, 29, 1–21. [Google Scholar] [CrossRef]

- Bundesministerium für Wirtschaft und Energie (BMWi). Zahlen und Fakten Energiedaten-National und international Entwicklungen. 2015. Available online: https://www.foerderdatenbank.de/FDB/Content/DE/Download/Publikation/Energie/erneuerbare-energien-in-zahlen-2018.pdf?__blob=publicationFile&v=2 (accessed on 20 October 2020).

- Deutscher Wasserstoff- und Brennstoffzellenverband (DWV). Wasserstoffproduktion in Deutschland. 2015. Available online: https://www.dwv-info.de/wp-content/uploads/2015/06/20181128-Pos.-Papier-zu-Strukturwandel-final.pdf (accessed on 20 October 2020).

- Mineralölwirtschaftsverband (MWV). Jahresbericht 2015—Mineralöl-Zahlen 2014. 2015. Available online: https://www.mwv.de/wp-content/uploads/2016/06/mwv-publikationen-jahresberichte-mineraloelzahlen-2014-jahresbericht-2015.pdf (accessed on 20 October 2020).

- Union zur Förderung von Öl- und Proteinpflanzen e.V. (UFOP). Marktinformationen Ölsaaten und Biokraftstoffe. Berlin. 2015. Available online: https://www.ufop.de/files/9715/8107/4394/RZ_MI_0220.pdf (accessed on 20 October 2020).

- Bundesnetzagentur (BNetzA). Monitoringbericht 2015. Bonn. 2016. Available online: https://www.bundesnetzagentur.de/SharedDocs/Downloads/DE/Allgemeines/Bundesnetzagentur/Publikationen/Berichte/2015/Monitoringbericht_2015_BA.pdf?__blob=publicationFile (accessed on 20 October 2020).

- Brand, U.; Giese, B.; von Gleich, A.; Heinbach, K.; Ulrich, P.; Schnülle, C.; Stührmann, S.; Stührmann, T.; Thier, P.; Wachsmuth, J.; et al. Resiliente Gestaltung des Energiesystems am Beispiel der Transformationsoptionen “EE-Methan-System” und “Regionale Selbstversorgung”: Schlussbericht des vom BMBF geförderten Projektes RESYSTRA. 2017. Available online: http://www.resystra.de/files/publikationen/resystra-schlussbericht.master.pdf (accessed on 20 October 2020). [CrossRef]

- Ausfelder, F.; Beilmann, C.; Bertau, M.; Bräuninger, S.; Heinzel, A.; Hoer, R.; Koch, W.; Mahlendorf, F.; Metzelthin, A.; Peuckert, M.; et al. Energiespeicherung als Element einer sicheren Energieversorgung. Chem. Ing. Tech. 2015, 87, 17–89. [Google Scholar] [CrossRef]

- Fasihi, M.; Bogdanov, D.; Breyer, C. Techno-Economic Assessment of Power-to-Liquids (PtL) Fuels Production and Global Trading Based on Hybrid PV-Wind Power Plants. Energ. Proced. 2016, 99, 243–268. [Google Scholar] [CrossRef]

- Haarlemmer, G.; Boissonnet, G.; Peduzzi, E.; Setier, P.-A. Investment and production costs of synthetic fuels–A literature survey. Energy 2014, 66, 667–676. [Google Scholar] [CrossRef]

- Schiebahn, S.; Grube, T.; Robinius, M.; Tietze, V.; Kumar, B.; Stolten, D. Power to gas: Technological overview, systems analysis and economic assessment for a case study in Germany. Int. J. Hydro. Energ. 2015, 40, 4285–4294. [Google Scholar] [CrossRef]

- Schmidt, P.; Zittel, W.; Weindorf, W.; Rakasha, T.; Goericke, D. Renewables in transport 2050—Empowering a sustainable mobility future with zero emission fuels. In 16. Internationales Stuttgarter Symposium; Springer Science and Business Media LLC: Berlin, Germany, 2016; pp. 185–199. [Google Scholar]

- Stolten, D.; Emonts, B. Hydrogen Science and Engineering: Materials, Processes, Systems and Technology; Wiley-VCH Verlag GmbH & Co KGaA: Wheinheim, Germany, 2016; ISBN 978-3-527-33238-0. [Google Scholar]

- Tremel, A.; Wasserscheid, P.; Baldauf, M.; Hammer, T. Techno-economic analysis for the synthesis of liquid and gaseous fuels based on hydrogen production via electrolysis. Int. J. Hydro. Energ. 2015, 40, 11457–11464. [Google Scholar] [CrossRef]

- Ullrich, S. Übertragungsnetze. In Energietechnologien der Zukunft; Wietschel, M., Ullrich, S., Eds.; Lehrbuch; Springer Vieweg: Wiesbaden, Germany, 2015; pp. 267–322. ISBN 978-3-658-07128-8. [Google Scholar]

- Vanhoudt, W.; Barth, F.; Lanoix, J.; Neave, J.; Schmidt, P.; Weindorf, W.; Raksha, T.; Zerhusen, J.; Michalski, J. Power-to-Gas; Short Term and Long Term Opportunities to Leverage Synergies between the Electricity and Transport Sectors through Power-to-Hydrogen; Hinicio and LBST·Ludwig-Bölkow-Systemtechnik GmbH: Brussels, Belgium, 2016. [Google Scholar]

- Sterner, M.; Thema, M.; Eckert, F.; Lenck, T.; Götz, P. Bedeutung und Notwendigkeit von Windgas für die Energiewende in Deutschland, Forschungsstelle Energienetze und Energiespeicher (FENES) OTH Regensburg, Energy Brainpool, Studie im Auftrag von Greenpeace Energy, Regensburg, Hamburg, Berlin. 2015. Available online: https://www.greenpeace-energy.de/fileadmin/docs/pressematerial/Windgas-Studie_2015_FENES_GPE_lang.pdf (accessed on 20 October 2020).

- Albrecht, U.; Altmann, M.; Michalski, J.; Raksha, T.; Weindorf, W. Analyse der Kosten Erneuerbarer Gase; Bochum, Germany, 2013; ISBN 9783920328652. Available online: http://www.lbst.de/download/2014/20131217_BEE-PST_LBST_Studie_EEGase.pdf (accessed on 20 October 2020).

- Gregory, K.; Mislick, D.A. Nussbaum Cost Estimation—Methods and Tools; John Wiley & Sons: Hoboken, NJ, USA, 2015; ISBN 978-1-118-53613-1. [Google Scholar]

- Graf, F.; Götz, M.; Henel, M.; Schaaf, T.; Tichler, R. Technoökonomische Studie von Power-to-Gas-Konzepten Teilprojekte B-D Abschlussbericht. Bonn. 2014. Available online: https://www.dvgw.de/medien/dvgw/forschung/berichte/g3_01_12_tp_b_d.pdf (accessed on 20 October 2020).

- Bundesministerium für Wirtschaft und Energie (BMWi). Zahlen und Fakten Energiedaten—Nationale und Internationale Entwicklung. 2018. Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Energie/energieeffizienz-in-zahlen-2018.pdf%3F__blob%3DpublicationFile%26v%3D8 (accessed on 20 October 2020).

- Sargl, M.; Wolfsteiner, A.; Wittmann, G. Neue Weltklimaordnung: Emissionshandel zwischen Staaten mit schrittweiser Klimagerechtigkeit. Wirtschaftsdienst 2011, 91, 704–711. [Google Scholar] [CrossRef]

- Wronski, R.; Küchler, S.; Lückgr, H.; Schlegelmilch, K.; Duchene, K. Umsetzung eines CO2-Mindestpreises in Deutschland-Internationale Vorbilder und Möglichkeiten für die Ergänzung des Emissionshandels; Forum Ökologisch-Soziale Marktwirtschaft e.V. Berlin. 2014. Available online: https://foes.de/pdf/2014-10-FOES-CO2-Mindestpreis.pdf (accessed on 20 October 2020).

- Edenhofer, O.; Schmidt, C.M. Eckpunkte einer CO2-Preisreform: Gemeinsamer Vorschlag von Ottmar Edenhofer (PIK/MCC) und Christoph M. Schmidt (RWI); RePEc: 2018; Available online: http://www.rwi-essen.de/media/content/pages/publikationen/rwi-positionen/pos_072_eckpunkte_einer_co2-preisreform.pdf (accessed on 20 October 2020).

- De Clara, S.; Mayr, K. The EU ETS phase IV Reform: Implications for System Functioning and for the Carbon Price Signal. 2018. Available online: https://www.oxfordenergy.org/wpcms/wp-content/uploads/2018/09/The-EU-ETS-phase-IV-reform-implications-for-system-functioning-and-for-the-carbon-price-signal-Insight-38.pdf (accessed on 20 October 2020).

- European Energy Exchange (EEX) European Emission Allowances (EUA). Available online: https://www.eex.com/en/market-data/environmental-markets/spot-market/european-emission-allowances (accessed on 1 April 2020).

- International Energy Agency (IEA). Germany 2020–Country Report. 2020. Available online: https://www.iea.org/reports/germany-2020 (accessed on 20 October 2020).

- Bundesverband der Deutschen Bioethanolwirtschaft e.V. (BdBe). Presseinformation. Super E10: Akzeptanz und Wahrnehmung—Umfrageergebnis 2012. 2012. Available online: https://www.presseportal.de/pm/73390/2272715 (accessed on 20 October 2020).

- ADAC, e.V. ADAC Position zur Festlegung neuer Pkw CO 2-Grenzwerte post 2020. 2017. Available online: https://www.bundestag.de/resource/blob/561114/595b2167a4da0db5e89ec0946ba54af3/19-16-68-D_Anhoerung_CO2-Emissionen_ADAC-data.pdf (accessed on 20 October 2020).

- Bundesministerium für Umwelt, Naturschutz und Nukleare Sicherheit (BMU). Die EU-Verordnung zur Verminderung der CO2—Emissionen von Personenkraftwagen. 2009. Available online: https://www.bmu.de/fileadmin/bmu-import/files/pdfs/allgemein/application/pdf/eu_verordnung_co2_emissionen_pkw.pdf (accessed on 20 October 2020).

- European Parliament and the Council of the European Union Regulation (EU) No 333/2014 of the European Parliament and of the Council of 11 March 2014 Amending Regulation (EC) No 443/2009 to Define the Modalities for Reaching the 2020 Target to Reduce CO2 Emissions from New Passenger Cars. 2014. Available online: https://op.europa.eu/en/publication-detail/-/publication/5b971540-bc8f-11e3-86f9-01aa75ed71a1/language-en (accessed on 20 October 2020).

- Ploetner, K.O.; Rothfeld, R.; Urban, M.; Hornung, M.; Tay, G.; Oguntona, O. Technological and Operational Scenarios on Aircraft Fleet-Level towards ATAG and IATA 2050 Emission Targets. In Proceedings of the 17th AIAA Aviation Technology Integration, and Operations Conference, Denver, CO, USA, 5–9 June 2017; pp. 1–13. [Google Scholar]

- Naumann, K.; Oehmichen, K.; Zeymer, M.; Meisel, K.; Anfahrt, I.; Trainer, P. Monitoring Biokraftstoffsektor; DBFZ Deutsches Biomasseforschungszentrum: Leipzig, Germany, 2019; Available online: https://www.dbfz.de/fileadmin/user_upload/Referenzen/DBFZ_Reports/DBFZ_Report_11_4.pdf (accessed on 20 October 2020).

- International Air transport Association (IATA). IATA Sustainable Aviation Fuel Roadmap; Montreal—Geneva. 2015. Available online: https://www.iata.org/contentassets/d13875e9ed784f75bac90f000760e998/safr-1-2015.pdf (accessed on 20 October 2020).

- Fachagentur Nachwachsende Rohstoffe e.V. (FNR). FNR—Biokraftstoffe: Rahmenbedingungen. Available online: https://biokraftstoffe.fnr.de/kraftstoffe/rahmenbedingungen/ (accessed on 1 April 2020).

- Kolb, T.; Umesterung von Rapsöl zu Rapsmethylester (RME). Karlsruher Institut für Technologie (KIT), Engler-Bunte-Institut, Bereich I; Chemische Energieträger-Brennstofftechnologie (CEB). 2014. Available online: https://ceb.ebi.kit.edu/download/V1_RME_Synthese.pdf (accessed on 20 October 2020).

- Zah, R.; Gauch, M. Ökobilanz von Energieprodukten: Biotreibstoffen Schlussbericht Bern. 2007. Available online: https://www.academia.edu/22605305/Ökobilanz_von_Energieprodukten_Ökologische_Bewertung_von_Biotreibstoffen (accessed on 20 October 2020).

- ENCON. Potentialatlas für Wasserstoff—Analyse des Marktpotentials für Wasserstoff, der mit Erneuerbaren Strom Hergestellt Wird, im Raffineriesektor und im Zukünftigen Mobilitätssektor. 2018. Available online: https://www.innovationsforum-energiewende.de/fileadmin/user_upload/Potentialstudie-fuer-gruenen-Wasserstoff-in-Raffinerien.pdf (accessed on 20 October 2020).

- Grimm, N.; Holmeier, S.; Uhlig, J.; Weber, A.; Zoch, I. Power-to-Gas-Eine innovative Systemlösung auf dem Weg zur Marktreife. 2013. Available online: https://www.dena.de/fileadmin/dena/Dokumente/Pdf/9096_Fachbroschuere_Systemloesung_Power_to_Gas.pdf (accessed on 20 October 2020).

- Wilms, S.V.L.; Schäfer-Stradowsky, S.J.S.; Jahnke, P.G.T. Heutige Einsatzgebiete für Power Fuels—Factsheets zur Anwendung von Klimafreundlich Erzeugten Synthetischen Energieträgern. Berlin. 2018. Available online: https://www.dena.de/fileadmin/dena/Publikationen/PDFs/2019/181123_dena_PtX-Factsheets.pdf (accessed on 20 October 2020).

- Übertragungsnetzbetreiber (ÜNB). Prognose der EEG-Umlage 2019 nach EEV. 2018. Available online: https://www.netztransparenz.de/portals/1/Content/EEG-Umlage/EEG-Umlage%202019/20181015_Veröffentlichung%20EEG-Umlage%202019.pdf (accessed on 20 October 2020).

- Deutsche Energie-Agentur. Power to Gas: Chancen, Herausforderungen und Stellschrauben auf dem Weg zur Marktreife. 2015. Available online: https://www.dena.de/newsroom/publikationsdetailansicht/pub/fachbroschuere-systemloesung-power-to-gas/ (accessed on 20 October 2020).

- International Council on Clean Transportation (ICCT). Final Recast Renewable Energy Directive for 2021–2030 in the European Union. Brussels, Beijing, Berlin, San Francisco, Washington. 2018. Available online: https://theicct.org/publications/final-recast-renewable-energy-directive-2021-2030-european-union (accessed on 20 October 2020).

- Harks, E. Power-to-Gas-to-Refining (to Tank). Stromspeicher und Brücke zum Verkehr. 2015. Available online: https://www.innovationsforum-energiewende.de/fileadmin/user_upload/2015-10-IfE-P2G2R-BP-Harks-v4.pdf (accessed on 20 October 2020).

| Energy Carrier in Markets | Demand in TWh a−1 | Energy Carrier in Markets | Price in € kWh−1 |

|---|---|---|---|

| Natural Gas | Natural Gas | ||

| Private households | 289 | Private households | 0.072 |

| Industry | 225 | Industry | 0.036 |

| Transport | 2.47 | ||

| Mineral Oil | 0.073 | ||

| Hydrogen | |||

| Industry | 60 | Biofuels | |

| Traffic | 0.025 (Own assumptions based on registered fuel cell vehicles in Germany. Assumed fuel consumption: 1 kgH2 per 100 km. At 15,000 km a−1 the total consumption equals 25 GWh a−1.) | Gas | 0.08 |

| Diesel | 0.078 | ||

| Mineral Oil | Petrol | 0.07 | |

| Industry | 36 | ||

| Transport | 681 | Hydrogen | |

| Households | 157 | Industry | 0.06 (Own calculation of production costs for H2 via steam methane reformation at a gas price of 3 ct kWh−1.) |

| Transport | 0.28 (Price information of Clean Energy Partnership (CEP).) |

| 2015 | 2029 | |||

|---|---|---|---|---|

| Investment Costs [€ kW−1] | Production Costs [ct kWh−1] | Investment Costs [€ kW−1] | Production Costs [ct kWh−1] | |

| P2H2 | 1500 | 25.7 | 1292 | 23.6 |

| P2M | 3000 | 34.0 | 2630 | 30.4 |

| P2L | 3500 | 38.7 | 3500 | 38.7 |

| 2015 | 2029 | |||

|---|---|---|---|---|

| Investment Costs [€ kW−1] | Production Costs [ct kWh−1] | Investment Costs [€ kW−1] | Production Costs [ct kWh−1] | |

| P2H2 | 1500 | 25.7 | 520 | 12.8 |

| P2M | 3000 | 34.0 | 1000 | 15.4 |

| P2L | 3500 | 38.7 | 1000 | 15.4 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schnuelle, C.; Kisjes, K.; Stuehrmann, T.; Thier, P.; Nikolic, I.; von Gleich, A.; Goessling-Reisemann, S. From Niche to Market—An Agent-Based Modeling Approach for the Economic Uptake of Electro-Fuels (Power-to-Fuel) in the German Energy System. Energies 2020, 13, 5522. https://doi.org/10.3390/en13205522

Schnuelle C, Kisjes K, Stuehrmann T, Thier P, Nikolic I, von Gleich A, Goessling-Reisemann S. From Niche to Market—An Agent-Based Modeling Approach for the Economic Uptake of Electro-Fuels (Power-to-Fuel) in the German Energy System. Energies. 2020; 13(20):5522. https://doi.org/10.3390/en13205522

Chicago/Turabian StyleSchnuelle, Christian, Kasper Kisjes, Torben Stuehrmann, Pablo Thier, Igor Nikolic, Arnim von Gleich, and Stefan Goessling-Reisemann. 2020. "From Niche to Market—An Agent-Based Modeling Approach for the Economic Uptake of Electro-Fuels (Power-to-Fuel) in the German Energy System" Energies 13, no. 20: 5522. https://doi.org/10.3390/en13205522

APA StyleSchnuelle, C., Kisjes, K., Stuehrmann, T., Thier, P., Nikolic, I., von Gleich, A., & Goessling-Reisemann, S. (2020). From Niche to Market—An Agent-Based Modeling Approach for the Economic Uptake of Electro-Fuels (Power-to-Fuel) in the German Energy System. Energies, 13(20), 5522. https://doi.org/10.3390/en13205522