Perceived Internal Audit Quality and External Auditors’ Attributes in Iranian and Iraqi Banks

Abstract

1. Introduction

2. Literature Review

3. Hypothesis Development

3.1. External Auditors’ Competency and Perceived Internal Audit Quality

3.2. External Auditors’ Independence and Perceived Internal Audit Quality

3.3. External Audit Methodologies and Perceived Internal Audit Quality

4. Research Methodology

4.1. Research Method

4.2. Research Population

4.3. Sample and Data Collection

4.4. Research Variables

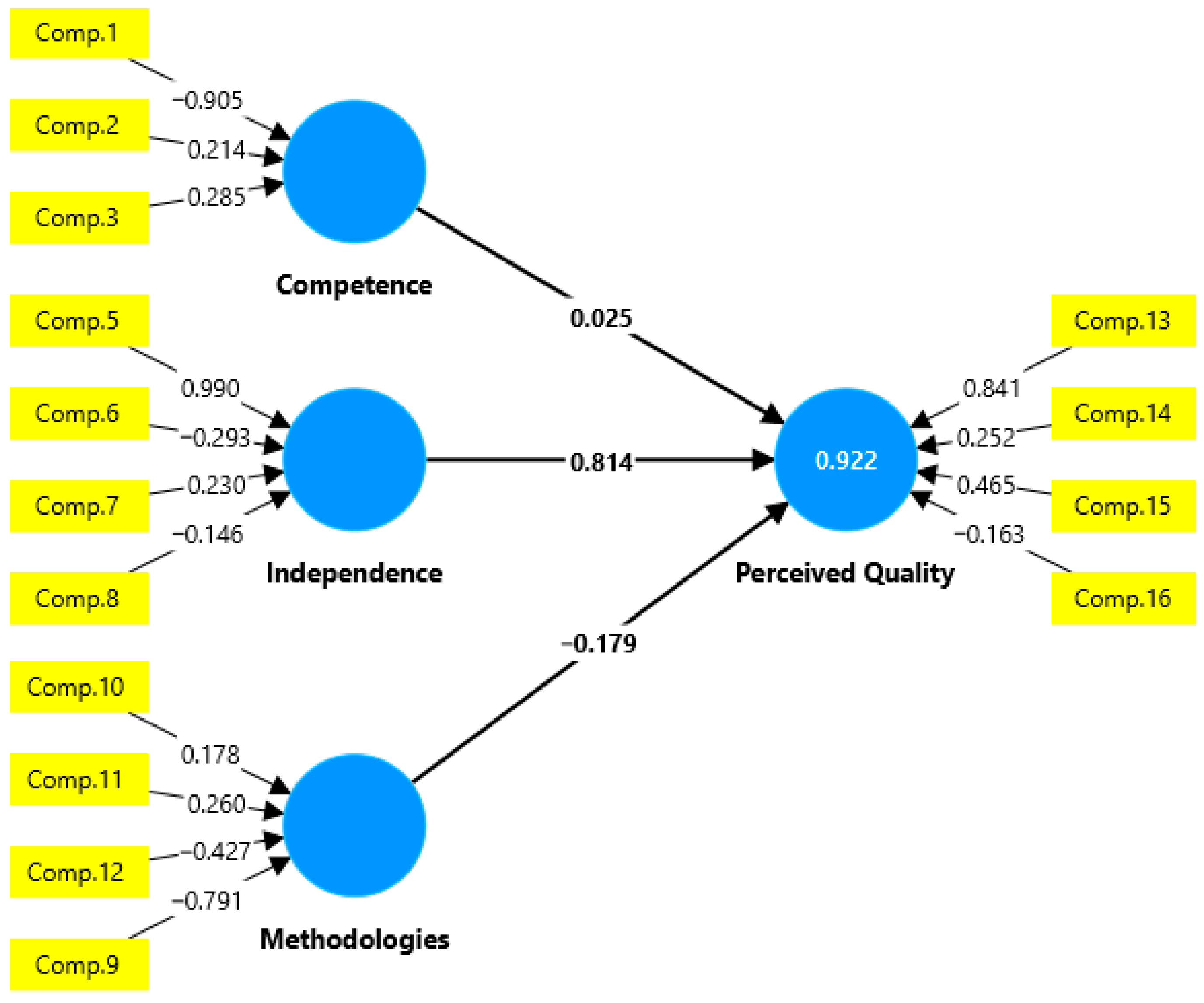

5. Results

Robustness Test

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abbott, L. J., Parker, S., & Peters, G. F. (2012). Audit fee reductions from internal audit-provided assistance: The incremental impact of internal audit characteristics. Contemporary Accounting Research, 29(1), 94–118. [Google Scholar] [CrossRef]

- Abdi, H., & Williams, L. J. (2010). Principal component analysis. Wiley Interdisciplinary Reviews: Computational Statistics, 2(4), 433–459. [Google Scholar] [CrossRef]

- Abdullah, R., Ismail, Z., & Smith, M. (2018). Audit committees’ involvement and the effects of quality in the internal audit function on corporate governance. International Journal of Auditing, 22(3), 385–403. [Google Scholar] [CrossRef]

- AL Fayi, S. M. (2022). Internal audit quality and resistance to pressure. Journal of Money and Business, 2(1), 57–69. [Google Scholar] [CrossRef]

- ALbawwat, I. E., AL-HAJAIA, M. E., & AL FRIJAT, Y. S. (2021). The Relationship Between Internal Auditors’ Personality Traits, Internal Audit Effectiveness, and Financial Reporting Quality: Empirical Evidence from Jordan. The Journal of Asian Finance, Economics and Business, 8(4), 797–808. [Google Scholar]

- Alhazmi, A. H. J., Islam, S., & Prokofieva, M. (2024). The Impact of Changing External Auditors, Auditor Tenure, and Audit Firm Type on the Quality of Financial Reports on the Saudi Stock Exchange. Journal of Risk and Financial Management, 17(9), 407. [Google Scholar] [CrossRef]

- Aliu, M., Okpanachi, J., & Mohammed, N. (2018). Auditor’s independence and audit quality: An empirical study. Accounting and Taxation Review, 2(2), 15–27. [Google Scholar]

- Al-Olimat, N. H., & Al Shbail, M. O. (2021). The mediating effect of external audit quality on the relationship between corporate governance and creative accounting. International Journal of Financial Research, 12(1), 149–157. [Google Scholar] [CrossRef]

- Andiola, L. M., Downey, D. H., & Westermann, K. D. (2020). Examining climate and culture in audit firms: Insights, practice implications, and future research directions. Auditing: A Journal of Practice & Theory, 39(4), 1–29. [Google Scholar]

- Appelbaum, D. A., Kogan, A., & Vasarhelyi, M. A. (2018). Analytical procedures in external auditing: A comprehensive literature survey and framework for external audit analytics. Journal of Accounting Literature, 40(1), 83–101. [Google Scholar] [CrossRef]

- Arel, B., Beaudoin, C. A., & Cianci, A. M. (2012). The impact of ethical leadership, the internal audit function, and moral intensity on a financial reporting decision. Journal of Business Ethics, 109(2012), 351–366. [Google Scholar] [CrossRef]

- Bae, G. S., Choi, S. U., Lamoreaux, P. T., & Lee, J. E. (2021). Auditors’ fee premiums and low-quality internal controls. Contemporary Accounting Research, 38(1), 586–620. [Google Scholar] [CrossRef]

- Basel Committee. (2012). The Internal Audit Function in Bank-Basel Committee on Banking Supervision. Bank for International Settlements. Available online: http://www.bis.org/publ/bcbs223.pdf (accessed on 1 February 2024).

- Boskou, G., Kirkos, E., & Spathis, C. (2019). Classifying internal audit quality using textual analysis: The case of auditor selection. Managerial Auditing Journal, 34(8), 924–950. [Google Scholar] [CrossRef]

- Deribe, W. J., & Regasa, D. G. (2014). Factors determining internal audit quality: Empirical evidence from Ethiopian commercial banks. Research Journal of Finance and Accounting, 5(23), 86–95. [Google Scholar]

- Erasmus, L., & Coetzee, P. (2018). Drivers of stakeholders’ view of internal audit effectiveness: Management versus audit committee. Managerial Auditing Journal, 33(1), 90–114. [Google Scholar] [CrossRef]

- Gramling, A. A., & Vandervelde, S. D. (2006). Assessing internal audit quality. Internal Auditing, 21(3), 26. [Google Scholar]

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. [Google Scholar] [CrossRef]

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. [Google Scholar] [CrossRef]

- Hamza, M., & Damak-Ayadi, S. (2023). The perception of audit quality among financial statements users, preparers and auditors, in Tunisia. Accounting and Management Information Systems, 22(2), 202–224. [Google Scholar] [CrossRef]

- Hazaea, S. A., Tabash, M. I., Khatib, S. F., Zhu, J., & Al-Kuhali, A. A. (2020). The impact of internal audit quality on financial performance of Yemeni commercial banks: An empirical investigation. The Journal of Asian Finance, Economics and Business, 7(11), 867–875. [Google Scholar] [CrossRef]

- Herdiati, M. F., Yusnaini, Y., & Wahyudi, T. (2023). The Effect of Independence, Role Conflict, and Internal-External Auditor Relationship on Audit Quality: Case at Universities in Indonesia. Journal of Economics, Finance and Management Studies, 6(7), 3197–3205. [Google Scholar] [CrossRef]

- Jiang, L., André, P., & Richard, C. (2018). An international study of internal audit function quality. Accounting and Business Research, 48(3), 264–298. [Google Scholar] [CrossRef]

- Jöreskog, K. G. (1970). A general method for estimating a linear structural equation system. ETS Research Bulletin Series, 1970(2), i-41. [Google Scholar] [CrossRef]

- Khalil, S., & Nehme, R. (2023). Performance evaluations and junior auditors’ attitude to audit behavior: A gender and culture comparative study. Meditari Accountancy Research, 31(2), 239–257. [Google Scholar] [CrossRef]

- KPMG. (2014). Guide to audit quality and the external auditor. KPMG. Available online: https://assets.kpmg.com/content/dam/kpmg/pdf/2014/08/KPMG-NZ-Guide-to-audit-quality-and-external-auditor.pdf (accessed on 1 February 2024).

- Lenz, R., & Hahn, U. (2015). A synthesis of empirical internal audit effectiveness literature pointing to new research opportunities. Managerial Auditing Journal, 30(1), 5–33. [Google Scholar] [CrossRef]

- Mansouri, A., Pirayesh, R., & Salehi, M. (2009). Audit competence and audit quality: Case in emerging economy. International Journal of Business and Management, 4(2), 17–25. [Google Scholar] [CrossRef]

- Mashayekhi, B., Ghasemi Dashtaki, S., & Ahmadi, H. (2024). Banks’ financial performance analysis: An experience from an Islamic economy. Journal of Islamic Accounting and Business Research. [Google Scholar] [CrossRef]

- Mashayekhi, B., Jalali, F., & Rezaee, Z. (2022). The role of stakeholders’ perception in internal audit status: The case of Iran. Journal of Accounting in Emerging Economies, 12(4), 589–614. [Google Scholar] [CrossRef]

- Mashayekhi, B., Samavat, M., & Jahangard, A. (2023). Reviewing the Internal Audit Literature in the Public Sector: A Bibliometrics Analysis. Governmental Accounting, 9(2), 207–226. [Google Scholar]

- Mat Zain, M., Zaman, M., & Mohamed, Z. (2015). The Effect of Internal Audit Function Quality and Internal Audit Contribution to External Audit on Audit Fees. International Journal of Auditing, 19(3), 134–147. [Google Scholar] [CrossRef]

- Mazza, T., & Azzali, S. (2015). Effects of internal audit quality on the severity and persistence of controls deficiencies. International Journal of Auditing, 19(3), 148–165. [Google Scholar] [CrossRef]

- Messier, W. F., Jr., Reynolds, J. K., Simon, C. A., & Wood, D. A. (2011). The effect of using the internal audit function as a management training ground on the external auditor’s reliance decision. The Accounting Review, 86(6), 2131–2154. [Google Scholar] [CrossRef]

- Noordin, N. A., Hussainey, K., & Hayek, A. F. (2022). The use of artificial intelligence and audit quality: An analysis from the perspectives of external auditors in the UAE. Journal of Risk and Financial Management, 15(8), 339. [Google Scholar] [CrossRef]

- Nurdiono, N., & Gamayuni, R. R. (2018). The effect of internal auditor competency on internal audit quality and its implication on the accountability of local government. European Research Studies Journal, 21(4), 426–434. [Google Scholar] [CrossRef]

- Okechukwu, O., & Ene, E. C. (2023, February). Effect of auditor’s independence on audit quality of quoted consumer goods companies in Nigeria [Conference session]. 7th Annual International Academic Conference on Accounting and Finance Disruptive Technology: Accounting Practices, Financial and Sustainability Reporting, RIVERS State University of Science and Technology, Port Harcourt, Nigeria. [Google Scholar]

- Pizzini, M., Lin, S., & Ziegenfuss, D. E. (2015). The impact of internal audit function quality and contribution on audit delay. Auditing, 34(1), 25–58. [Google Scholar] [CrossRef]

- Prawitt, D. F., Smith, J. L., & Wood, D. A. (2009). Internal audit quality and earnings management. Accounting Review, 84(4), 1255–1280. [Google Scholar] [CrossRef]

- Rezaee, Z. (2005). Causes, consequences, and deterence of financial statement fraud. Critical Perspectives on Accounting, 16(3), 277–298. [Google Scholar] [CrossRef]

- Rogers, S., & Johnson, J. (2023). Auditors Abound: The Differences Between Internal and External Audit. Available online: https://www.jgacpa.com/auditors-abound (accessed on 1 February 2024).

- Samagaio, A., & Felício, T. (2023). The determinants of internal audit quality. European Journal of Management and Business Economics, 32(4), 417–435. [Google Scholar] [CrossRef]

- Saporta, G., & Keita, N. N. (2009). Principal component analysis: Application to statistical process control. Data Analysis, 1–23. [Google Scholar]

- Sarstedt, M., Ringle, C. M., & Hair, J. F. (2021). Partial least squares structural equation modeling. In Handbook of market research (pp. 587–632). Springer. [Google Scholar]

- Stewart, J., & Subramaniam, N. (2010). Internal audit independence and objectivity: Emerging research opportunities. Managerial Auditing Journal, 25(4), 328–360. [Google Scholar] [CrossRef]

- The Institute of Internal Auditors (IIA). (2015). Global Internal Audit Competency Framework. Institute of Internal Auditors (IIA). Available online: https://docs.ifaci.com/wp-content/uploads/2018/03/the-iia-global-internal-audit-competency-framework-2013.pdf (accessed on 1 March 2024).

- The Institute of Internal Auditors (IIA). (2024). Quality Assessment Manual: Chapter 4. Available online: https://www.theiia.org/globalassets/documents/quality/quality-assessment-manual-chapter-4.pdf (accessed on 1 March 2024).

- Usman, R., Rohman, A., & Ratmono, D. (2023). The relationship of internal auditors’ characteristics with external auditors’ reliance and its impact on audit efficiency: Empirical evidence from Indonesian government institutions. Cogent Business & Management, 10(1), 2191781. [Google Scholar]

- Waheed, A. A., & Sfan, A. M. D. (2024). Evaluating Internal Audit Quality (Evidence From Iraq). International Journal of Economics, Management and Accounting, 1(4), 230–257. [Google Scholar] [CrossRef]

- Wehrhahn, C., & Velte, P. (2024). The relationship between audit committees, external auditors, and internal control systems: A literature review and a research agenda. Journal of Financial Reporting and Accounting. ahead-of-print. [Google Scholar] [CrossRef]

- Zhang, C., Shah, S., Lau, Y. W., & Ngalim, S. M. (2024). The impact of independence, auditors’ competence and information technology usage on internal audit quality: Empirical evidence from chinese commercial banks. Corporate Ownership & Control, 21(3), 18–30. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Part A | Related References |

|---|---|

| Independent Variables: Characteristics of External Auditors | |

| Competency | |

| The external auditor has extensive experience in internal auditing. | KPMG (2014) |

| The external auditor possesses in-depth knowledge of organizational activities. | KPMG (2014) |

| The external auditor holds a professional designation in accountancy or a qualification in internal auditing. | IIA (2024) |

| The external auditor has a track record of satisfactory past interactions with internal auditors. | Wehrhahn and Velte (2024) |

| The external auditor complies with codified professional norms of conduct and professional standards promulgated by the internal audit. | IIA (2024) |

| Independence | |

| The external auditor operates in a completely independent manner. | KPMG (2014) |

| The external auditor can execute audit activities without any interference or influence from the organization. | KPMG (2014) |

| The external auditor has free access to the organization’s information and data necessary for the audit. | IIA (2024) |

| The external auditor is free to include any findings in their audit report and communicate them directly to the responsible parties. | Wehrhahn and Velte (2024) |

| The external auditor requires the approval of the audit committee and/or the board of directors for the completion of audit work. | KPMG (2014) |

| Audit Methodologies | |

| The external auditor uses tools, techniques, programs, step-by-step approaches, and best-practice examples of deliverables. | IIA (2024) |

| The external auditor successfully passes external assessments performed by an independent internal audit-certified reviewer and complies with specific quality assessment criteria. | IIA (2024) |

| The external auditor incorporates modern technology, including computer data tools and specific software, into the audit process. | Wehrhahn and Velte (2024) |

| The external auditor cooperates with the internal audit department of the organization for a quality external audit. | Wehrhahn and Velte (2024) |

| Periodic meetings between the external auditor and the internal auditor improve the quality of internal audits. | KPMG (2014) |

| Part B | |

| Dependent Variables: Perceived Quality of Internal Audits | |

| Audit Procedures | |

| Internal auditors have appropriate and relevant training enabling them to audit all of the organization’s systems. | IIA (2024) |

| Internal auditors intervene in all organizational units and all questions. | Wehrhahn and Velte (2024) |

| Internal auditors regularly monitor measures taken to correct problems encountered. | KPMG (2014) |

| Internal auditors have regular and direct working relationships with the managing director and the management team. | Wehrhahn and Velte (2024) |

| Internal auditors have free access to the organization’s information and data, which they can download and examine. | IIA (2024) |

| Reporting Practices | |

| Internal auditors are free to include any findings in their audit reports and communicate them directly to responsible parties. | KPMG (2014) |

| The internal audit work requires the approval of the audit committee and/or the board of directors. | Wehrhahn and Velte (2024) |

| Internal auditors comply with codified professional norms of conduct and professional standards. | IIA (2024) |

| Internal audit reports provide clear and actionable recommendations. | Wehrhahn and Velte (2024) |

| Internal auditors follow up on recommendations to ensure implementation and effectiveness. | IIA (2024) |

| Overall Effectiveness | |

| The internal audit department’s work is considered high quality by external auditors. | Wehrhahn and Velte (2024) |

| The internal audit department operates independently and without influence from other departments. | KPMG (2014) |

| The internal audit department ensures the organization’s strategic goals and objectives are met. | IIA (2024) |

| The internal audit department’s findings and recommendations lead to meaningful improvements in organizational processes. | Wehrhahn and Velte (2024) |

| The internal audit department is perceived as a valuable asset by the organization’s management. | KPMG (2014) |

| Component Matrix a | |

|---|---|

| External Auditor Competency | 0.987 |

| External Auditor Independence | 0.987 |

| External Audit Methodologies | 0.987 |

| Internal Audit Procedures | 0.987 |

| Reporting Practices | 0.980 |

| Overall Effectiveness of Internal Audit | 0.980 |

| Extraction Method: Principal Component Analysis. | |

| a. 1 components extracted. | |

| Variables | Number of Items | Cronbach Alpha |

|---|---|---|

| External Auditor Competency | 5 | 0.832 |

| External Auditor Independence | 5 | 0.796 |

| External Audit Methodologies | 5 | 0.809 |

| Internal Audit Procedures | 5 | 0.757 |

| Reporting Practices | 5 | 0.878 |

| Overall Effectiveness of Internal Audit | 5 | 0.833 |

| Variable | 1 | 2 | 3 | 4 |

|---|---|---|---|---|

| Age | 18–24 | 25–34 | 35–44 | 45 and above |

| Gender | Male | Female | ||

| Position | Internal Auditor | Senior External Auditor | Audit Committee members | Manager |

| Education | BA | MA | Ph.D. |

| Age | Frequency | Percent | Position | Frequency | Percent |

|---|---|---|---|---|---|

| 1 | 29 | 13.43 | 1 | 68 | 31.48 |

| 2 | 76 | 35.19 | 2 | 125 | 57.87 |

| 3 | 74 | 34.26 | 3 | 14 | 6.48 |

| 4 | 37 | 17.13 | 4 | 9 | 4.17 |

| Total | 216 | 100 | Total | 216 | 100 |

| Education | Frequency | Percent | Gender | Frequency | Percent |

| 1 | 155 | 71.76 | 1 | 153 | 70.83 |

| 2 | 37 | 17.13 | 2 | 63 | 29.17 |

| 3 | 24 | 11.11 | Total | 216 | 100 |

| Total | 216 | 100 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mashayekhi, B.; Mohammed, Y. Perceived Internal Audit Quality and External Auditors’ Attributes in Iranian and Iraqi Banks. J. Risk Financial Manag. 2025, 18, 3. https://doi.org/10.3390/jrfm18010003

Mashayekhi B, Mohammed Y. Perceived Internal Audit Quality and External Auditors’ Attributes in Iranian and Iraqi Banks. Journal of Risk and Financial Management. 2025; 18(1):3. https://doi.org/10.3390/jrfm18010003

Chicago/Turabian StyleMashayekhi, Bita, and Yousif Mohammed. 2025. "Perceived Internal Audit Quality and External Auditors’ Attributes in Iranian and Iraqi Banks" Journal of Risk and Financial Management 18, no. 1: 3. https://doi.org/10.3390/jrfm18010003

APA StyleMashayekhi, B., & Mohammed, Y. (2025). Perceived Internal Audit Quality and External Auditors’ Attributes in Iranian and Iraqi Banks. Journal of Risk and Financial Management, 18(1), 3. https://doi.org/10.3390/jrfm18010003