Performance of US and European Exchange Traded Funds: A Base Point-Slack-Based Measure Approach

,

,  ,

,

Abstract

1. Introduction

2. Methodology

3. Data and Assumptions

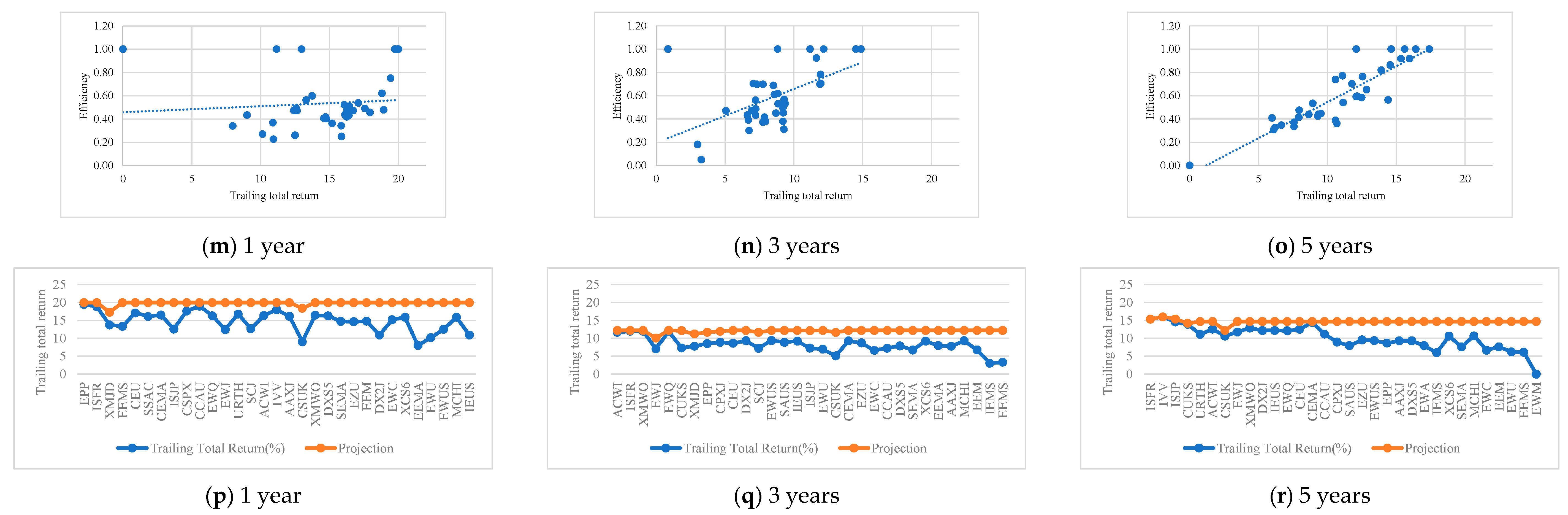

4. Results

4.1. Results for the Complete Set of ETFs

4.2. Results by Region

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| DMU | ETF | Home | Index Followed | Launch | Legal Structure |

|---|---|---|---|---|---|

| IVV | iShares core S&P 500 ETF | US | S&P 500 | 15/05/2000 | ETF |

| CSPX | iShares Core S&P 500 UCITS ETF | Ireland | S&P 500 | 19/05/2010 | UCITS ETF |

| EWU | iShares MSCI United Kingdom ETF | US | MSCI United Kingdom | 12/03/1996 | ETF |

| CSUK | iShares MSCI United Kingdom UCITS ETF | Ireland | MSCI United Kingdom | 12/01/2010 | UCITS ETF |

| EWQ | iShares MSCI France ETF | US | MSCI France | 12/03/1996 | ETF |

| ISFR | iShares MSCI France UCITS ETF | Ireland | MSCI France | 05/09/2014 | UCITS ETF |

| URTH | iShares MSCI World EFT | US | MSCI World | 10/01/2012 | ETF |

| XMWO | XTRACKERS MSCI World UCITS ETF 1C | Ireland | MSCI World | 22/07/2014 | UCITS ETF |

| EWJ | iShares MSCI Japan ETF | US | MSCI Japan | 12/03/1996 | ETF |

| XMJD | Xtrackers MSCI Japan UCITS ETF 1C | Luxembourg | MSCI Japan | 09/01/2007 | UCITS ETF |

| EEMA | iShares MSCI Emergent Market Asia ETF | US | MSCI Emergent Market Asia | 08/02/2012 | ETF |

| CEMA | iShares MSCI Emergent Asia UCITS ETF | Ireland | MSCI Emergent Market Asia | 06/08/2010 | UCITS ETF |

| MCHI | iShares MSCI China ETF | US | MSCI China | 29/03/2011 | ETF |

| XCS6 | Xtrackers MSCI China UCITS ETF 1C | Luxembourg | MSCI China | 24/06/2010 | UCITS ETF |

| EWC | iShares MSCI Canada ETF | US | MSCI Custom Capped Canada | 12/03/1996 | ETF |

| CCAU | iShares MSCI Canada UCITS ETF | Ireland | MSCI Canada | 12/01/2010 | UCITS ETF |

| EEM | iShares MSCI Emerging Markets ETF | US | MSCI Emerging Markets Index (SM) | 07/04/2003 | ETF |

| SEMA | iShares MSCI EM UCITS ETF USD (Acc) | Ireland | MSCI Emerging Markets Index (SM) | 25/09/2009 | UCITS ETF |

| EZU | iShares MSCI EMU ETF | US | MSCI MEU | 25/07/2000 | ETF |

| CEU | iShares MSCI EMU UCITS ETF | Ireland | MSCI MEU | 12/01/2010 | UCITS ETF |

| EPP | iShares MSCI Pacific ex Japan ETF | US | MSCI Pacific ex-Japan Index | 25/10/2001 | ETF |

| CPXJ | iShares Core MSCI Pacific ex-Japan UCITS ETF | Ireland | MSCI Pacific ex-Japan Index | 12/01/2010 | UCITS ETF |

| EWA | iShares MSCI Australia ETF | US | MSCI Australia Index | 12/03/1996 | ETF |

| SAUS | iShares MSCI Australia UCITS ETF | Ireland | MSCI Australia Index | 22/01/2010 | UCITS ETF |

| ACWI | iShares MSCI ACWI ETF | US | MSCI ACWI Index | 26/03/2008 | ETF |

| SSAC | iShares MSCI ACWI UCITS ETF | Ireland | MSCI ACWI Index | 21/10/2011 | UCITS ETF |

| SCJ | iShares MSCI Japan Small-Cap ETF | US | MSCI Japan Small Cap Index | 20/12/2007 | ETF |

| ISJP | iShares MSCI Japan Small Cap UCITS ETF | Ireland | MSCI Japan Small Cap Index | 09/05/2008 | UCITS ETF |

| EWUS | iShares MSCI United Kingdom Small-Cap ETF | US | MSCI United Kingdom Small Cap Index | 25/01/2012 | ETF |

| CUKS | iShares MSCI UK Small Cap UCITS ETF | Ireland | MSCI United Kingdom Small Cap Index | 01/07/2009 | UCITS ETF |

| EWM | iShares MSCI Malaysia ETF | US | MSCI Malaysia Index | 12/03/1996 | ETF |

| LG6 | Xtrackers MSCI Malaysia UCITS ETF 1C | Luxembourg | MSCI Malaysia TRN INDEX | 24/06/2010 | UCITS ETF |

| EEMS | iShares MSCI Emerging Markets Small-Cap ETF | US | MSCI Emerging Markets Small Cap Index | 16/08/2011 | ETF |

| IEMS | iShares MSCI EM Small Cap UCITS ETF | Ireland | MSCI Emerging Markets Small Cap Index | 06/03/2009 | UCITS ETF |

| IEUS | iShares MSCI Europe Small-Cap ETF | US | MSCI Europe Small Cap Index | 12/11/2007 | ETF |

| DX2J | Xtrackers MSCI Europe Small Cap UCITS ETF 1C | Luxembourg | MSCI Europe Small Cap Index | 17/01/2008 | UCITS ETF |

| AAXJ | iShares MSCI All Country Asia ex Japan ETF | US | MSCI AC Asia ex Japan Index | 13/08/2008 | ETF |

| DXS5 | Xtrackers MSCI AC Asia ex Japan Swap UCITS ETF 1C | Luxembourg | MSCI AC Asia ex Japan Index | 20/01/2009 | UCITS ETF |

| Inputs | Beta | Standard Deviation (%) | ||||

|---|---|---|---|---|---|---|

| DMU | 1 Year | 3 Years | 5 Years | 1 Year | 3 Years | 5 Years |

| IVV | 1 | 1 | 1 | 17 | 12.07 | 11.92 |

| CSPX | 0.98 | 0.99 | 0.99 | 15.17 | 11.4 | 11.29 |

| EWU | 1.01 | 0.93 | 0.95 | 14.46 | 12.01 | 13.14 |

| CSUK | 1.02 | 1.04 | 1.05 | 10.66 | 10.48 | 10.47 |

| EWQ | 1.04 | 1.1 | 1.04 | 15.38 | 14 | 14.37 |

| ISFR | 0.96 | 0.95 | 0.96 | 11.53 | 11.76 | 11.91 |

| URTH | 1.09 | 0.89 | 0.86 | 15.54 | 11.21 | 11.65 |

| XMWO | 1.06 | 1.02 | 1 | 16.28 | 11.54 | 11.81 |

| EWJ | 0.84 | 0.82 | 0.87 | 12.72 | 10.7 | 12.3 |

| XMJD | 1.02 | 1.01 | 1.02 | 10.44 | 9.94 | 11.53 |

| EEMA | 1.09 | 1.17 | 1.09 | 16.13 | 14.76 | 15.46 |

| CEMA | 0.99 | 1.01 | 1 | 12.22 | 12.72 | 14.49 |

| MCHI | 1.52 | 1.45 | 1.39 | 23.04 | 19.44 | 21.12 |

| XCS6 | 1.02 | 1.01 | 1 | 23.57 | 19.66 | 21.24 |

| EWC | 1.17 | 0.9 | 0.92 | 18.04 | 13.28 | 14.68 |

| CCAU | 0.98 | 0.99 | 1 | 15.38 | 12.19 | 13.1 |

| EEM | 1.09 | 1.16 | 1.13 | 15.91 | 14.18 | 15.65 |

| SEMA | 1 | 1 | 1 | 15.9 | 14.21 | 15.65 |

| EZU | 1.08 | 1.15 | 1.09 | 15.42 | 14.2 | 14.74 |

| CEU | 1 | 1 | 1 | 14.04 | 12.04 | 13.98 |

| EPP | 0.85 | 0.86 | 0.99 | 12.88 | 11.47 | 14.02 |

| CPXJ | 1 | 1 | 1 | 10.34 | 10.88 | 13.17 |

| EWA | 0.67 | 0.7 | 0.92 | 10.97 | 10.98 | 14.5 |

| SAUS | 1 | 1 | 1 | 10.52 | 11.82 | 14.08 |

| ACWI | 1.09 | 0.92 | 0.89 | 15.37 | 11.28 | 11.74 |

| SSAC | 1 | 1 | 1 | 12.7 | 9.92 | 10.43 |

| SCJ | 0.83 | 0.86 | 0.74 | 13.69 | 11.65 | 11.53 |

| ISJP | 0.99 | 1 | 1 | 11.42 | 11.14 | 11.72 |

| EWUS | 1.21 | 1.06 | 0.99 | 18.86 | 14.67 | 16.46 |

| CUKS | 1.25 | 0.96 | 0.99 | 13.17 | 11.1 | 11.32 |

| EWM | 0.24 | 0.62 | 0.76 | 7.07 | 11.84 | 15.01 |

| EEMS | 0.76 | 0.97 | 0.97 | 12.48 | 13.09 | 14.4 |

| IEMS | 0.93 | 0.98 | 0.99 | 9.42 | 11.86 | 13.93 |

| IEUS | 1.16 | 1.14 | 1.03 | 16.81 | 14 | 14.58 |

| DX2J | 106 | 1.03 | 1.01 | 16.56 | 12.4 | 13.61 |

| AAXJ | 1.1 | 1.16 | 1.09 | 16.35 | 14.67 | 15.4 |

| DXS5 | 1.02 | 1.01 | 1 | 16.7 | 14.89 | 15.48 |

| Average | 1.00 | 1.00 | 0.99 | 14.44 | 12.69 | 13.83 |

| Minimum | 0.24 | 0.62 | 0.74 | 7.07 | 9.92 | 10.43 |

| Maximum | 1.52 | 1.45 | 1.39 | 23.57 | 19.66 | 21.24 |

| Outputs | Jensen’s Alpha | Sharpe Ratio | Trailing Total Return (%) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| DMU | 1 Year | 3 Years | 5 Years | 1 Years | 3 Years | 5 Years | 1 Year | 3 Years | 5 Years |

| IVV | −0.03 | −0.03 | −0.04 | 0.74 | 1.08 | 0.83 | 14.29 | 14.87 | 10.73 |

| CSPX | −0.05 | −0.07 | −0.09 | 0.8 | 1.03 | 1.27 | 13.92 | 14.5 | 10.37 |

| EWU | −4.39 | −0.54 | −2.52 | 0.34 | 0.48 | 0.06 | 6.48 | 6.93 | 0.97 |

| CSUK | −1.44 | −1.13 | −1.32 | 0.47 | 0.47 | 0.52 | 5.35 | 5.06 | 5.35 |

| EWQ | 1.03 | 3.1 | 3 | 0.7 | 0.75 | 0.46 | 12.62 | 11.88 | 6.85 |

| ISFR | 0.52 | 1.49 | 1.54 | 0.97 | 0.86 | 0.99 | 15.16 | 11.93 | 10.1 |

| URTH | 1.06 | 4.47 | 4.2 | 0.72 | 0.94 | 0.62 | 13.07 | 12.16 | 5.85 |

| XMWO | −0.34 | 0.42 | 0.52 | 0.68 | 0.89 | 0.59 | 12.75 | 11.95 | 7.61 |

| EWJ | −0.96 | 0.21 | 3.02 | 0.54 | 0.54 | 0.49 | 8.76 | 7.05 | 6.54 |

| XMJD | 0.37 | −0.49 | −1.2 | 0.67 | 0.5 | 0.93 | 10.08 | 7.75 | 11.18 |

| EEMA | 0.34 | −0.88 | 0.58 | 0.65 | 0.48 | 0.28 | 4.32 | 7.93 | 12.16 |

| CEMA | −1.02 | −0.75 | −0.69 | 0.82 | 0.45 | 0.6 | 12.79 | 9.22 | 9.18 |

| MCHI | −2.39 | −0.74 | 1.63 | 0.51 | 0.47 | 0.31 | 12.21 | 9.27 | 5.44 |

| XCS6 | −0.8 | −0.67 | −0.6 | 0.5 | 0.46 | 0.3 | 12.19 | 9.19 | 5.36 |

| EWC | −0.78 | −0.5 | −1.78 | 0.56 | 0.42 | 0.1 | 11.53 | 6.61 | 1.42 |

| CCAU | −0.08 | −0.22 | −0.22 | 0.64 | 0.37 | 0.45 | 15.28 | 7.21 | 5.9 |

| EEM | −0.7 | −1.97 | −1.47 | 0.6 | 0.41 | 0.16 | 11.12 | 6.74 | 2.34 |

| SEMA | −0.73 | −0.64 | −0.58 | 0.59 | 0.41 | 0.16 | 11.06 | 6.69 | 2.34 |

| EZU | −0.83 | −0.12 | 0.43 | 0.6 | 0.54 | 0.29 | 10.94 | 8.69 | 4.29 |

| CEU | 0.65 | 0.4 | 0.37 | 1 | 0.78 | 0.59 | 13.43 | 8.58 | 7.25 |

| EPP | 5.27 | 1.37 | −0.17 | 1.03 | 0.62 | 0.23 | 15.78 | 8.5 | 3.41 |

| CPXJ | −0.15 | −0.11 | −0.13 | 1.31 | 0.61 | 0.63 | 16.1 | 8.83 | 3.7 |

| EWA | 7.19 | 2.65 | −0.56 | 1.23 | 0.67 | 0.18 | 16.29 | 8.81 | 2.69 |

| SAUS | −0.35 | −0.31 | −0.35 | 1.3 | 0.57 | 0.53 | 16.35 | 8.85 | 2.71 |

| ACWI | 0.67 | 3.78 | 3.61 | 0.7 | 0.89 | 0.57 | 12.68 | 11.63 | 7.31 |

| SSAC | −0.14 | −0.14 | −0.21 | 0.83 | 0.87 | 1.05 | 12.42 | 11.17 | 6.85 |

| SCJ | −0.52 | 0.19 | 6.06 | 0.53 | 0.51 | 0.74 | 8.99 | 7.21 | 9.4 |

| ISJP | −0.35 | −0.36 | −0.38 | 0.63 | 0.46 | 1.14 | 8.92 | 7.22 | 9.32 |

| EWUS | −3.45 | 1.22 | 0.88 | 0.42 | 0.57 | 0.26 | 8.84 | 9.36 | 4.1 |

| CUKS | 8 | 3.62 | 2.5 | 0.56 | 0.64 | 0.75 | 7.51 | 7.31 | 8.67 |

| EWM | −8.02 | −4.34 | −7.92 | −0.82 | −0.01 | −0.35 | −3.65 | 0.85 | −5.24 |

| EEMS | 0.56 | −4.15 | −2.53 | 0.62 | 0.18 | 0.06 | 9.65 | 3.27 | 0.87 |

| IEMS | −0.53 | −1.12 | −0.46 | 0.78 | 0.1 | 0.39 | 9.32 | 3 | 0.74 |

| IEUS | −4.72 | 0.41 | 3.16 | 0.36 | 0.58 | 0.46 | 7.27 | 9.19 | 6.94 |

| DX2J | −0.46 | −0.19 | −0.14 | 0.62 | 0.76 | 0.75 | 7.24 | 9.28 | 6.93 |

| AAXJ | 0.55 | −1 | 0.31 | 0.66 | 0.47 | 0.27 | 12.47 | 7.74 | 4.06 |

| DXS5 | −0.75 | −0.63 | −0.67 | 0.65 | 0.47 | 0.27 | 12.59 | 7.85 | 4.06 |

| Average | −0.21 | 0.06 | 0.21 | 0.66 | 0.58 | 0.48 | 10.98 | 8.49 | 5.61 |

| Minimum | −8.02 | −4.34 | −7.92 | −0.82 | −0.01 | −0.35 | −3.65 | 0.85 | −5.24 |

| Maximum | 8 | 4.47 | 6.06 | 1.31 | 1.08 | 1.27 | 16.35 | 14.87 | 12.16 |

| DMU | 1 Year | 3 Years | 5 Years | Number of Times as Benchmark (1 Year) | Number of Times as Benchmark (3 Years) | Number of Times as Benchmark (5 Years) | Home |

|---|---|---|---|---|---|---|---|

| IVV | 0.41 | 1.00 | 0.66 | US | |||

| CSPX | 0.44 | 1.00 | 1.00 | 5 | Ireland | ||

| EWU | 0.24 | 0.44 | 0.32 | US | |||

| CSUK | 0.45 | 0.50 | 0.69 | Ireland | |||

| EWQ | 0.45 | 0.66 | 0.58 | US | |||

| ISFR | 0.56 | 0.73 | 0.85 | Ireland | |||

| URTH | 0.44 | 1.00 | 0.81 | 31 | US | ||

| XMWO | 0.39 | 0.63 | 0.61 | Ireland | |||

| EWJ | 0.45 | 0.70 | 0.69 | US | |||

| XMJD | 0.58 | 0.70 | 0.66 | Luxembourg | |||

| EEMA | 0.40 | 0.34 | 0.42 | US | |||

| CEMA | 0.46 | 0.39 | 0.50 | Ireland | |||

| MCHI | 0.22 | 0.27 | 0.35 | US | |||

| XCS6 | 0.31 | 0.33 | 0.36 | Luxembourg | |||

| EWC | 0.33 | 0.41 | 0.34 | US | |||

| CCAU | 0.42 | 0.39 | 0.51 | Ireland | |||

| EEM | 0.37 | 0.26 | 0.32 | US | |||

| SEMA | 0.38 | 0.36 | 0.37 | Ireland | |||

| EZU | 0.37 | 0.41 | 0.43 | US | |||

| CEU | 0.50 | 0.60 | 0.55 | Ireland | |||

| EPP | 0.73 | 0.67 | 0.43 | US | |||

| CPXJ | 1.00 | 0.58 | 0.56 | 1 | Ireland | ||

| EWA | 1.00 | 1.00 | 0.40 | 32 | 3 | US | |

| SAUS | 0.91 | 0.48 | 0.51 | Ireland | |||

| ACWI | 0.43 | 0.92 | 0.76 | US | |||

| SSAC | 0.48 | 1.00 | 1.00 | 6 | 2 | Ireland | |

| SCJ | 0.45 | 0.54 | 1.00 | 34 | US | ||

| ISJP | 0.48 | 0.46 | 0.85 | Ireland | |||

| EWUS | 0.23 | 0.50 | 0.43 | US | |||

| CUKS | 1.00 | 0.77 | 0.79 | Ireland | |||

| EWM | 1.00 | 1.00 | 0.00 | 2 | US | ||

| EEMS | 0.55 | 0.04 | 0.30 | US | |||

| IEMS | 1.00 | 0.16 | 0.47 | Ireland | |||

| IEUS | 0.19 | 0.46 | 0.58 | US | |||

| DX2J | 0.38 | 0.53 | 0.57 | Luxembourg | |||

| AAXJ | 0.41 | 0.33 | 0.41 | US | |||

| DXS5 | 0.38 | 0.38 | 0.40 | Luxembourg |

| Model DEA 1 | 1 Year | 3 Years | 5 Years | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | |

| Efficient DMUs | ||||||||||||

| Beta | 0.82 | 0.38 | 0.24 | 1.25 | 0.87 | 0.17 | 0.62 | 1.00 | 0.91 | 0.15 | 0.74 | 1.00 |

| Standard deviation | 10.19 | 2.23 | 7.07 | 13.17 | 11.24 | 0.76 | 9.92 | 12.07 | 11.08 | 0.58 | 10.43 | 11.53 |

| Alpha | 9.33 | 6.56 | 0.01 | 16.03 | 4.77 | 2.99 | 0.00 | 8.81 | 9.85 | 3.59 | 7.72 | 13.99 |

| Sharpe | 1.43 | 0.86 | 0.00 | 2.13 | 0.77 | 0.41 | 0.00 | 1.09 | 1.37 | 0.27 | 1.09 | 1.62 |

| Efficiency | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 |

| Inefficient DMUs | ||||||||||||

| Beta | 1.03 | 0.13 | 0.76 | 1.52 | 1.02 | 0.12 | 0.82 | 1.45 | 1.00 | 0.10 | 0.76 | 1.39 |

| Standard deviation | 15.10 | 3.10 | 10.44 | 23.57 | 12.97 | 2.26 | 9.94 | 19.66 | 14.08 | 2.36 | 10.47 | 21.24 |

| Alpha | 7.58 | 1.73 | 3.31 | 13.30 | 4.33 | 1.55 | 0.19 | 8.12 | 7.99 | 2.19 | 0.01 | 12.13 |

| Sharpe | 1.49 | 0.20 | 1.16 | 2.12 | 0.55 | 0.18 | 0.11 | 0.90 | 0.79 | 0.30 | 0.00 | 1.49 |

| Efficiency | 0.43 | 0.14 | 0.19 | 0.91 | 0.48 | 0.19 | 0.04 | 0.92 | 0.51 | 0.19 | 0.00 | 0.85 |

| (a) Correlation with Efficiency (M1) | ||||

| Input/output | 1 year | 3 years | 5 years | Bigger |

| Beta | −0.52 | −0.53 | −0.19 | 3 years |

| Standard Deviation | −0.74 | −0.55 | −0.70 | 1 year |

| Jensen’s Alpha | 0.40 | 0.50 | 0.64 | 5 years |

| Sharpe ratio | 0.20 | 0.64 | 0.91 | 5 years |

| (b) Correlation with efficiency (M2) | ||||

| Input/output | 1 year | 3 years | 5 years | Bigger |

| Beta | −0.51 | −0.52 | −0.07 | 3 years |

| Standard Deviation | −0.70 | −0.53 | −0.60 | 1 year |

| Jensen’s Alpha | 0.41 | 0.51 | 0.56 | 5 years |

| Trailing total return | 0.11 | 0.51 | 0.86 | 5 years |

| (c) Correlation with efficiency (M3) | ||||

| Input/output | 1 year | 3 years | 5 years | Maior |

| Beta | −0.64 | −0.51 | −0.09 | 1 year |

| Standard Deviation | −0.75 | −0.51 | −0.61 | 1 year |

| Sharpe ratio | 0.29 | 0.69 | 0.86 | 5 years |

| Trailing total return | 0.22 | 0.56 | 0.89 | 5 years |

| (d) Correlation with efficiency (M4) | ||||

| Input/output | 1 year | 3 years | 5 years | Maior |

| Beta | −0.51 | −0.51 | −0.08 | 1 year |

| Standard Deviation | −0.73 | −0.52 | −0.63 | 1 year |

| Jensen’s Alpha | 0.39 | 0.50 | 0.55 | 5 years |

| Sharpe ratio | 0.23 | 0.66 | 0.86 | 5 years |

| Trailing total return | 0.09 | 0.54 | 0.89 | 5 years |

| DMU | 1 Year | 3 Years | 5 Years | Number of Times as Benchmark (1 Year) | Number of Times as Benchmark (3 Years) | Number of Times as Benchmark (5 Years) | Home |

|---|---|---|---|---|---|---|---|

| IVV | 0.44 | 1.00 | 0.90 | US | |||

| CSPX | 0.46 | 1.00 | 1.00 | Ireland | |||

| EWU | 0.23 | 0.46 | 0.34 | US | |||

| CSUK | 0.39 | 0.45 | 0.83 | Ireland | |||

| EWQ | 0.47 | 0.73 | 0.61 | US | |||

| ISFR | 0.58 | 0.75 | 0.84 | Ireland | |||

| URTH | 0.46 | 1.00 | 0.75 | 31 | US | ||

| XMWO | 0.41 | 0.64 | 0.61 | Ireland | |||

| EWJ | 0.44 | 0.70 | 0.71 | US | |||

| XMJD | 0.57 | 0.78 | 1.00 | 2 | Luxembourg | ||

| EEMA | 0.30 | 0.37 | 1.00 | 2 | US | ||

| CEMA | 0.47 | 0.47 | 0.52 | Ireland | |||

| MCHI | 0.23 | 0.32 | 0.38 | US | |||

| XCS6 | 0.33 | 0.39 | 0.39 | Luxembourg | |||

| EWC | 0.35 | 0.44 | 0.36 | US | |||

| CCAU | 0.47 | 0.48 | 0.52 | Ireland | |||

| EEM | 0.38 | 0.28 | 0.34 | US | |||

| SEMA | 0.40 | 0.40 | 0.39 | Ireland | |||

| EZU | 0.38 | 0.45 | 0.46 | US | |||

| CEU | 0.50 | 0.56 | 0.55 | Ireland | |||

| EPP | 0.76 | 0.69 | 0.45 | US | |||

| CPXJ | 1.00 | 0.61 | 0.47 | 1 | Ireland | ||

| EWA | 1.00 | 1.00 | 0.43 | 32 | 3 | US | |

| SAUS | 1.00 | 0.52 | 0.42 | Ireland | |||

| ACWI | 0.45 | 0.92 | 0.76 | US | |||

| SSAC | 0.48 | 1.00 | 1.00 | 6 | 2 | Ireland | |

| SCJ | 0.45 | 0.56 | 1.00 | 32 | US | ||

| ISJP | 0.46 | 0.50 | 0.60 | Ireland | |||

| EWUS | 0.23 | 0.56 | 0.46 | US | |||

| CUKS | 1.00 | 0.71 | 0.80 | Ireland | |||

| EWM | 1.00 | 1.00 | 0.00 | 3 | US | ||

| EEMS | 0.54 | 0.04 | 0.31 | US | |||

| IEMS | 0.83 | 0.27 | 0.36 | Ireland | |||

| IEUS | 0.19 | 0.50 | 0.61 | US | |||

| DX2J | 0.34 | 0.52 | 0.53 | Luxembourg | |||

| AAXJ | 0.43 | 0.36 | 0.44 | US | |||

| DXS5 | 0.40 | 0.42 | 0.42 | Luxembourg |

| Model DEA 2 | 1 Year | 3 Years | 5 Years | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | |

| Efficient DMUs | ||||||||||||

| Beta | 0.83 | 0.39 | 0.24 | 1.25 | 0.87 | 0.17 | 0.62 | 1.00 | 0.97 | 0.13 | 0.74 | 1.09 |

| Standard deviation | 10.41 | 2.19 | 7.07 | 13.17 | 11.24 | 0.76 | 9.92 | 12.07 | 12.05 | 1.96 | 10.43 | 15.46 |

| Alfa | 9.36 | 6.54 | 0.01 | 16.03 | 4.77 | 2.99 | 0.00 | 8.81 | 8.96 | 2.88 | 6.73 | 13.99 |

| TTR | 14.17 | 8.78 | 0.00 | 20.00 | 10.39 | 5.18 | 0.85 | 14.87 | 15.24 | 2.03 | 12.10 | 17.41 |

| Efficiency | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 |

| Inefficient DMUS | ||||||||||||

| Beta | 1.03 | 0.13 | 0.76 | 1.52 | 1.02 | 0.12 | 0.82 | 1.45 | 1.00 | 0.10 | 0.76 | 1.39 |

| Standard deviation | 15.06 | 3.16 | 9.42 | 23.57 | 12.97 | 2.26 | 9.94 | 19.66 | 14.11 | 2.38 | 10.47 | 21.24 |

| Alfa | 7.58 | 1.73 | 3.31 | 13.30 | 4.33 | 1.55 | 0.19 | 8.12 | 8.01 | 2.25 | 0.01 | 12.13 |

| TTR | 14.70 | 2.89 | 7.97 | 19.43 | 8.13 | 2.13 | 3.00 | 11.95 | 10.18 | 3.32 | 0.01 | 15.98 |

| Efficiency | 0.43 | 0.13 | 0.19 | 0.83 | 0.51 | 0.18 | 0.04 | 0.92 | 0.52 | 0.19 | 0.00 | 0.90 |

| DMU | 1 Year | 3 Years | 5 Years | Number of Times as Benchmark (1 Year) | Number of Times as Benchmark (3 Years) | Number of Times as Benchmark (5 Years) | Home |

|---|---|---|---|---|---|---|---|

| IVV | 0.54 | 1.00 | 0.88 | 18 | US | ||

| CSPX | 0.59 | 1.00 | 1.00 | 14 | 32 | Ireland | |

| EWU | 0.38 | 0.50 | 0.30 | US | |||

| CSUK | 0.46 | 0.44 | 0.70 | Ireland | |||

| EWQ | 0.53 | 0.66 | 0.53 | US | |||

| ISFR | 0.75 | 0.86 | 0.90 | Ireland | |||

| URTH | 0.52 | 1.00 | 0.72 | 10 | US | ||

| XMWO | 0.51 | 0.83 | 0.66 | Ireland | |||

| EWJ | 0.53 | 0.70 | 0.66 | US | |||

| XMJD | 0.65 | 0.63 | 1.00 | 1 | Luxembourg | ||

| EEMA | 0.33 | 0.41 | 1.00 | US | |||

| CEMA | 0.64 | 0.49 | 0.63 | Ireland | |||

| MCHI | 0.33 | 0.34 | 0.32 | US | |||

| XCS6 | 0.40 | 0.41 | 0.38 | Luxembourg | |||

| EWC | 0.42 | 0.45 | 0.32 | US | |||

| CCAU | 0.57 | 0.41 | 0.54 | Ireland | |||

| EEM | 0.47 | 0.36 | 0.31 | US | |||

| SEMA | 0.48 | 0.38 | 0.33 | Ireland | |||

| EZU | 0.47 | 0.47 | 0.40 | US | |||

| CEU | 0.63 | 0.64 | 0.60 | Ireland | |||

| EPP | 0.77 | 0.70 | 0.39 | US | |||

| CPXJ | 1.00 | 0.64 | 0.54 | Ireland | |||

| EWA | 1.00 | 1.00 | 0.38 | 32 | 3 | US | |

| SAUS | 1.00 | 0.57 | 0.47 | Ireland | |||

| ACWI | 0.52 | 0.91 | 0.72 | US | |||

| SSAC | 0.62 | 1.00 | 1.00 | 6 | 1 | Ireland | |

| SCJ | 0.52 | 0.58 | 1.00 | 10 | US | ||

| ISJP | 0.55 | 0.49 | 0.90 | Ireland | |||

| EWUS | 0.35 | 0.51 | 0.39 | US | |||

| CUKS | 0.42 | 0.60 | 0.77 | Ireland | |||

| EWM | 1.00 | 1.00 | 0.00 | 2 | US | ||

| EEMS | 0.60 | 0.19 | 0.28 | US | |||

| IEMS | 1.00 | 0.14 | 0.38 | Ireland | |||

| IEUS | 0.35 | 0.50 | 0.53 | US | |||

| DX2J | 0.40 | 0.64 | 0.66 | Luxembourg | |||

| AAXJ | 0.49 | 0.40 | 0.38 | US | |||

| DXS5 | 0.50 | 0.43 | 0.66 | Luxembourg |

| Model DEA 3 | 1 Year | 3 Years | 5 Years | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | |

| Efficient DMUs | ||||||||||||

| Beta | 0.77 | 0.32 | 0.24 | 1.00 | 0.87 | 0.17 | 0.62 | 1.00 | 0.97 | 0.13 | 0.74 | 1.09 |

| Standard deviation | 9.66 | 1.56 | 7.07 | 10.97 | 11.24 | 0.76 | 9.92 | 12.07 | 12.05 | 1.96 | 10.43 | 15.46 |

| Alfa | 2.07 | 0.91 | 0.49 | 2.62 | 0.77 | 0.41 | 0.00 | 1.09 | 1.20 | 0.37 | 0.63 | 1.62 |

| TTR | 14.54 | 8.66 | 0.00 | 20.00 | 10.39 | 5.18 | 0.85 | 14.87 | 15.24 | 2.03 | 12.10 | 17.41 |

| Efficiency | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 |

| Inefficient DMUs | ||||||||||||

| Beta | 1.04 | 0.14 | 0.76 | 1.52 | 1.02 | 0.12 | 0.82 | 1.45 | 1.00 | 0.10 | 0.76 | 1.39 |

| Standard deviation | 15.18 | 3.01 | 10.44 | 23.57 | 12.97 | 2.26 | 9.94 | 19.66 | 14.11 | 2.38 | 10.47 | 21.24 |

| Alfa | 1.96 | 0.16 | 1.65 | 2.34 | 0.55 | 0.18 | 0.11 | 0.90 | 0.78 | 0.30 | 0.00 | 1.49 |

| TTR | 14.64 | 2.94 | 7.97 | 19.43 | 8.13 | 2.13 | 3.00 | 11.95 | 10.18 | 3.32 | 0.01 | 15.98 |

| Efficiency | 0.51 | 0.11 | 0.33 | 0.77 | 0.53 | 0.18 | 0.14 | 0.91 | 0.52 | 0.21 | 0.00 | 0.90 |

| DMU | 1 Year | 3 Years | 5 Years | Number of Times as Benchmark (1 Year) | Number of Times as Benchmark (3 Years) | Number of Times as Benchmark (5 Years) | Home |

|---|---|---|---|---|---|---|---|

| IVV | 0.46 | 1.00 | 0.92 | US | |||

| CSPX | 0.49 | 1.00 | 1.00 | 3 | Ireland | ||

| EWU | 0.27 | 0.47 | 0.33 | US | |||

| CSUK | 0.43 | 0.47 | 0.74 | Ireland | |||

| EWQ | 0.48 | 0.70 | 0.59 | US | |||

| ISFR | 0.62 | 0.78 | 0.92 | Ireland | |||

| URTH | 0.47 | 1.00 | 0.77 | 31 | US | ||

| XMWO | 0.43 | 0.71 | 0.65 | Ireland | |||

| EWJ | 0.47 | 0.70 | 0.70 | US | |||

| XMJD | 0.60 | 0.70 | 1.00 | 2 | Luxembourg | ||

| EEMA | 0.34 | 0.38 | 1.00 | US | |||

| CEMA | 0.51 | 0.45 | 0.56 | Ireland | |||

| MCHI | 0.25 | 0.31 | 0.36 | US | |||

| XCS6 | 0.34 | 0.38 | 0.39 | Luxembourg | |||

| EWC | 0.36 | 0.43 | 0.35 | US | |||

| CCAU | 0.48 | 0.43 | 0.54 | Ireland | |||

| EEM | 0.40 | 0.30 | 0.33 | US | |||

| SEMA | 0.42 | 0.39 | 0.37 | Ireland | |||

| EZU | 0.41 | 0.45 | 0.45 | US | |||

| CEU | 0.54 | 0.61 | 0.58 | Ireland | |||

| EPP | 0.75 | 0.69 | 0.44 | US | |||

| CPXJ | 1.00 | 0.62 | 0.53 | Ireland | |||

| EWA | 1.00 | 1.00 | 0.41 | 31 | 3 | US | |

| SAUS | 1.00 | 0.53 | 0.47 | Ireland | |||

| ACWI | 0.46 | 0.92 | 0.76 | US | |||

| SSAC | 0.52 | 1.00 | 1.00 | 6 | 2 | Ireland | |

| SCJ | 0.47 | 0.56 | 1.00 | 32 | US | ||

| ISJP | 0.49 | 0.49 | 0.86 | Ireland | |||

| EWUS | 0.26 | 0.53 | 0.44 | US | |||

| CUKS | 1.00 | 0.70 | 0.82 | Ireland | |||

| EWM | 1.00 | 1.00 | 0.00 | 2 | US | ||

| EEMS | 0.56 | 0.05 | 0.31 | US | |||

| IEMS | 1.00 | 0.18 | 0.41 | Ireland | |||

| IEUS | 0.23 | 0.50 | 0.59 | US | |||

| DX2J | 0.37 | 0.57 | 0.60 | Luxembourg | |||

| AAXJ | 0.44 | 0.37 | 0.43 | US | |||

| DXS5 | 0.42 | 0.42 | 0.42 | Luxembourg |

| Model DEA 4 | 1 Year | 3 Years | 5 Years | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | |

| Efficient DMUs | ||||||||||||

| Beta | 0.85 | 0.35 | 0.24 | 1.25 | 0.87 | 0.17 | 0.62 | 1.00 | 0.97 | 0.13 | 0.74 | 1.09 |

| Standard deviation | 10.25 | 2.00 | 7.07 | 13.17 | 11.24 | 0.76 | 9.92 | 12.07 | 12.05 | 1.96 | 10.43 | 15.46 |

| Alfa | 9.05 | 5.90 | 0.01 | 16.03 | 4.77 | 2.99 | 0.00 | 8.81 | 8.96 | 2.88 | 6.73 | 13.99 |

| TTR | 1.55 | 0.82 | 0.00 | 2.13 | 0.77 | 0.41 | 0.00 | 1.09 | 1.20 | 0.37 | 0.63 | 1.62 |

| Efficiency | 13.97 | 7.87 | 0.00 | 20.00 | 10.39 | 5.18 | 0.85 | 14.87 | 15.24 | 2.03 | 12.10 | 17.41 |

| Inefficient DMUs | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 |

| Beta | ||||||||||||

| Standard deviation | 1.03 | 0.13 | 0.76 | 1.52 | 1.02 | 0.12 | 0.82 | 1.45 | 1.00 | 0.10 | 0.76 | 1.39 |

| Alfa | 15.25 | 3.04 | 10.44 | 23.57 | 12.90 | 2.27 | 9.94 | 19.66 | 14.11 | 2.38 | 10.47 | 21.24 |

| TTR | 7.58 | 1.76 | 3.31 | 13.30 | 4.36 | 1.57 | 0.19 | 8.12 | 8.01 | 2.25 | 0.01 | 12.13 |

| Efficiency | 1.47 | 0.17 | 1.16 | 1.85 | 0.55 | 0.18 | 0.11 | 0.90 | 0.78 | 0.30 | 0.00 | 1.49 |

| DMU efficient | 14.76 | 2.92 | 7.97 | 19.43 | 8.14 | 2.17 | 3.00 | 11.95 | 10.18 | 3.32 | 0.01 | 15.98 |

| Beta | 0.44 | 0.11 | 0.23 | 0.75 | 0.51 | 0.18 | 0.05 | 0.92 | 0.53 | 0.21 | 0.00 | 0.92 |

| Model DEA 1US | 1 Year | 3 Years | 5 Years | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | |

| Efficient DMUs | ||||||||||||

| Beta | 0.46 | 0.30 | 0.24 | 0.67 | 0.81 | 0.15 | 0.62 | 1.00 | 0.87 | 0.18 | 0.74 | 1.00 |

| Standard deviation | 9.02 | 2.76 | 7.07 | 10.97 | 11.36 | 0.58 | 10.70 | 12.07 | 11.73 | 0.28 | 11.53 | 11.92 |

| Alfa | 7.61 | 10.76 | 0.01 | 15.22 | 4.94 | 3.32 | 0.00 | 8.81 | 10.94 | 4.31 | 7.89 | 13.99 |

| TTR | 1.03 | 1.45 | 0.00 | 2.05 | 0.65 | 0.42 | 0.00 | 1.09 | 1.14 | 0.06 | 1.09 | 1.18 |

| Efficiency | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 |

| Inefficient DMUs | ||||||||||||

| Beta | 1.05 | 0.18 | 0.76 | 1.52 | 1.06 | 0.16 | 0.86 | 1.45 | 1.00 | 0.14 | 0.76 | 1.39 |

| Standard deviation | 15.89 | 2.57 | 12.48 | 23.04 | 13.76 | 2.06 | 11.28 | 19.44 | 14.66 | 2.14 | 11.65 | 21.12 |

| Alfa | 7.48 | 2.35 | 3.31 | 13.30 | 4.36 | 1.99 | 0.19 | 8.12 | 8.16 | 2.99 | 0.01 | 12.13 |

| TTR | 1.43 | 0.16 | 1.16 | 1.85 | 0.54 | 0.16 | 0.19 | 0.90 | 0.61 | 0.23 | 0.00 | 0.97 |

| Efficiency | 0.39 | 0.13 | 0.19 | 0.73 | 0.45 | 0.21 | 0.04 | 0.92 | 0.45 | 0.19 | 0.00 | 0.81 |

| Model DEA 1EUR | 1 Year | 3 Years | 5 Years | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | Mean | Stand. Deviation | Minimum | Maximum | |

| Efficient DMUs | ||||||||||||

| Beta | 1.04 | 0.15 | 0.93 | 1.25 | 0.98 | 0.02 | 0.95 | 1.00 | 0.99 | 0.02 | 0.96 | 1.00 |

| Standard deviation | 11.12 | 1.62 | 9.42 | 13.17 | 11.05 | 0.80 | 9.92 | 11.76 | 11.24 | 0.61 | 10.43 | 11.91 |

| Alfa | 9.99 | 4.05 | 7.50 | 16.03 | 5.57 | 1.77 | 4.20 | 7.96 | 8.86 | 1.31 | 7.72 | 10.43 |

| TTR | 1.73 | 0.32 | 1.38 | 2.13 | 0.86 | 0.16 | 0.65 | 1.04 | 1.37 | 0.21 | 1.10 | 1.62 |

| Efficiency | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 | 1.00 | 0.00 | 1.00 | 1.00 |

| Inefficient DMUS | ||||||||||||

| Beta | 1.01 | 0.03 | 0.98 | 1.06 | 1.01 | 0.02 | 0.98 | 1.04 | 1.01 | 0.01 | 0.99 | 1.05 |

| Standard deviation | 14.40 | 3.54 | 10.44 | 23.57 | 12.56 | 2.44 | 9.94 | 19.66 | 13.88 | 2.60 | 10.47 | 21.24 |

| Alfa | 7.64 | 0.54 | 6.59 | 8.68 | 3.93 | 0.47 | 3.21 | 4.76 | 7.51 | 0.51 | 6.61 | 8.45 |

| TTR | 1.55 | 0.22 | 1.29 | 2.12 | 0.53 | 0.20 | 0.11 | 0.90 | 0.91 | 0.26 | 0.51 | 1.49 |

| Efficiency | 0.73 | 0.12 | 0.52 | 0.98 | 0.58 | 0.17 | 0.19 | 0.89 | 0.64 | 0.14 | 0.40 | 0.92 |

| Correlation with Efficiency US (M1) | Correlation with Efficiency Europe (M1) | ||||||||

| Input/output | 1 year | 3 years | 5 years | Bigger | Input/output | 1 year | 3 years | 5 years | Bigger |

| Beta | −0.86 | −0.66 | −0.25 | 1 year | Beta | 0.02 | −0.31 | −0.25 | 3 years |

| Standard deviation | −0.82 | −0.67 | −0.62 | 1 year | Standard deviation | −0.77 | −0.46 | −0.77 | 5 years |

| Jensen’s Alfa | 0.34 | 0.50 | 0.80 | 5 years | Jensen’s Alfa | 0.45 | 0.69 | 0.53 | 3 years |

| Sharpe ratio | −0.09 | 0.48 | 0.97 | 5 years | Sharpe ratio | 0.66 | 0.91 | 0.92 | 5 years |

| Correlation with efficiency US (M2) | Correlation with efficiency Europe (M2) | ||||||||

| Input/output | 1 year | 3 years | 5 years | Bigger | Input/output | 1 year | 3 years | 5 years | Bigger |

| Beta | −0.83 | −0.63 | −0.11 | 1 year | Beta | −0.02 | −0.40 | −0.06 | 3 years |

| Standard deviation | −0.80 | −0.64 | −0.48 | 1 year | Standard deviation | −0.61 | −0.45 | −0.73 | 5 years |

| Jensen’s Alfa | 0.35 | 0.52 | 0.75 | 5 years | Jensen’s Alfa | 0.44 | 0.69 | 0.40 | 3 years |

| Trailing total return | −0.03 | 0.36 | 0.95 | 5 years | Trailing total return | 0.47 | 0.77 | 0.86 | 5 years |

| Correlation with efficiency US (M3) | Correlation with efficiency Europe (M3) | ||||||||

| Input/output | 1 year | 3 years | 5 years | Bigger | Input/output | 1 year | 3 years | 5 years | Bigger |

| Beta | −0.86 | −0.67 | −0.13 | 1 year | Beta | −0.60 | −0.36 | −0.09 | 1 year |

| Standard deviation | −0.82 | −0.69 | −0.50 | 1 year | Standard deviation | −0.59 | −0.40 | −0.72 | 5 years |

| Jensen’s Alfa | −0.10 | 0.47 | 0.87 | 5 years | Jensen’s Alfa | 0.83 | 0.89 | 0.94 | 5 years |

| Trailing total return | −0.03 | 0.31 | 0.94 | 5 years | Trailing total return | 0.66 | 0.77 | 0.84 | 5 years |

| Correlation with efficiency US (M4) | Correlation with efficiency Europe (M4) | ||||||||

| Input/output | 1 year | 3 years | 5 years | Bigger | Input/output | 1 year | 3 years | 5 years | Bigger |

| Beta | −0.85 | −0.64 | −0.13 | 1 year | Beta | −0.01 | −0.31 | −0.12 | 3 years |

| Standard deviation | −0.82 | −0.65 | −0.50 | 1 year | Standard deviation | −0.67 | −0.42 | −0.75 | 5 years |

| Jensen’s Alfa | 0.34 | 0.51 | 0.74 | 5 years | Jensen’s Alfa | 0.45 | 0.69 | 0.42 | 3 years |

| Sharpe ratio | −0.08 | 0.49 | 0.87 | 5 years | Sharpe ratio | 0.70 | 0.91 | 0.91 | 3 and 5 years |

| Trailing total return | −0.05 | 0.35 | 0.94 | 5 years | Trailing total return | 0.39 | 0.78 | 0.84 | 5 years |

| 1 | ETF LG6, which is domiciled in Luxembourg, is excluded from the analysis due to a lack of data for the period under analysis. |

| 2 | These measures will be further explained in Section 3. |

| 3 | Irish funds are the abbreviation for Irish Funds Industry Association, which is an association that aims to support, complement, and develop the funds industry in Ireland. |

| 4 | ALFI represents the face and voice of asset management in Luxembourg and the investment fund community. |

References

- Acharya, Satya Ranjan, Amit Kumar Dwivedi, and Bhumika Darshak Panchal. 2015. Application od Data Envelopment analysis on Indian Gold ETFs. International Journal of Business Continuity and Risk Management 6: 147–61. [Google Scholar] [CrossRef]

- Admati, Anat R., and Stephen A. Ross. 1985. Measuring Investment Performance in a Rational Expectations Equilibrium Model. The Journal of Business 53: 1–26. [Google Scholar] [CrossRef]

- Banker, Rajiv D., Abraham Charnes, and William Wager Cooper. 1984. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science 30: 1078–92. [Google Scholar] [CrossRef]

- Basso, Antonella, and Stefania Funari. 2001. A data envelopment analysis approach to measure mutual fund performance. European Journal of Operational Research 135: 477–92. [Google Scholar] [CrossRef]

- Basso, Antonella, and Stefania Funari. 2007. DEA models for ethical and non ethical mutual funds with negative data. Mathematics and Methods in Economics Finance 2: 21–40. [Google Scholar]

- Basso, Antonella, and Stefania Funari. 2014. Constant and variable returns to scale DEA models for socially responsible investment funds. European Journal of Operational Research 235: 775–83. [Google Scholar] [CrossRef]

- Basso, Antonella, and Stefania Funari. 2016. DEA performance assessment of mutual funds. In Data Envelopment Analysis. Boston: Springer, pp. 229–87. [Google Scholar] [CrossRef]

- Blitz, David, and Joop Huij. 2012. Evaluating the performance of global emerging markets equity exchange-traded funds. Emerging Markets Review 13: 149–58. [Google Scholar] [CrossRef]

- Bowes, Jordan, and Marcel Ausloos. 2021. Financial Risk and Better Returns through smart beta exchange-traded funds? Journal of Risk and Financial Management 14: 283. [Google Scholar] [CrossRef]

- Charnes, Abraham, William W. Cooper, and Edwardo Rhodes. 1978. Measuring the efficiency of decision making units. European Journal of Operational Research 2: 429–44. [Google Scholar] [CrossRef]

- Choi, Hyung-Suk, and Daiki Min. 2017. Efficiency of well-diversified portfolios: Evidence from data envelopment analysis. Omega 73: 104–13. [Google Scholar] [CrossRef]

- Choi, Yoon K. 1995. The sensitivity in tests of the efficiency of a portfolio and portfolio performance measurement. Quarterly Review of Economics and Finance 35: 187–206. [Google Scholar] [CrossRef]

- Chu, Jacky, Frank Chen, and Philip Leung. 2010. ETF performance measurement-Data envelopment analysis. Paper present at 2010 7th International Conference on Service Systems and Service Management, Proceedings of ICSSSM’, Tokyo, Japan, June 28–30, vol. 10, pp. 173–78. [Google Scholar] [CrossRef]

- Dragomirescu-Gaina, Catalin, Emilios Galariotis, and Dionisis Philippas. 2021. Chasing the ‘green bandwagon’ in times of uncertainty. Energy Policy 151: 112190. [Google Scholar] [CrossRef]

- Galagedera, Don UA, and Param Silvapulle. 2002. Australian mutual fund performance appraisal using data envelopment analysis. Managerial Finance 28: 60–73. [Google Scholar] [CrossRef]

- Gastineau, Gary L. 2001. Exchange-Traded Funds. The Journal of Portfolio Management 27: 88–96. [Google Scholar] [CrossRef]

- Golany, Boaz, and Yaakov Roll. 1989. An application procedure for DEA. Omega 17: 237–50. [Google Scholar] [CrossRef]

- Gouveia, Maria, Elisabete Duarte Neves, Luís Cândido Dias, and Carlos Henggeler Antunes. 2018. Performance evaluation of Portuguese mutual fund portfolios using the value-based DEA method. Journal of the Operational Research Society 69: 1628–39. [Google Scholar] [CrossRef]

- Graham, J. Edward, Carlos Lassala, and Belén Ribeiro Navarrete. 2020. Influences on mutual fund performance: Comparing US and Europe using qualitative comparative analysis. Economic research-Ekonomska istraživanja 33: 3049–70. [Google Scholar] [CrossRef]

- Gregoriou, Greg N. 2006. Optimisation of the largest US mutual funds using data envelopment analysis. Journal of Asset Management 6: 445–55. [Google Scholar] [CrossRef]

- Gregoriou, Greg N., and Stephen C. Henry. 2015. Undesirable outputs in commodities trading advisers: A data envelopment analysis approach. Journal of Wealth Management 17: 85–92. [Google Scholar] [CrossRef]

- Henriques, Carla Oliveira, and Maria Elisabete Duarte Neves. 2019. A multiobjective interval portfolio framework for supporting investor’s preferences under different risk assumptions. Journal of the Operational Research Society 70: 1639–61. [Google Scholar] [CrossRef]

- Henriques, Carla Oliveira, Maria Elisabete Neves, Licínio Castelão, and Duc Khuong Nguyen. 2022. Assessing the performance of exchange traded funds in the energy sector: A hybrid DEA multiobjective linear programming approach. Annals of Operations Research 313: 341–66. [Google Scholar] [CrossRef] [PubMed]

- Hill, Joanne M., Dave Nadig, and Matt Hougan. 2015. A Comprehensive Guide to Exchange-Traded Funds (ETFs). Charlottesville: CFA Institute Research Foundation. [Google Scholar] [CrossRef]

- Ippolito, Richard A. 1989. Efficiency with costly information: A study of mutual fund performance, 1965–1984. The Quarterly Journal of Economics 104: 1–23. [Google Scholar] [CrossRef]

- Isakov, Vsevolod. 2019. Performance Appraisal of Exchange-Traded Funds using Clustering and Data Envelopment analysis (Xetra, Germany). Master’s thesis, LUT School of Business and Management, Lappeenranta, Finland. [Google Scholar]

- Jensen, Michael C. 1968. The Performance of Mutual Funds in the Period 1945–1964. The Journal of Finance 23: 389–416. [Google Scholar] [CrossRef]

- Kerstens, Kristiaan, and Ignace Van de Woestyne. 2011. Negative data in DEA: A simple proportional distance function approach. Journal of the Operational Research Society 62: 1413–19. [Google Scholar] [CrossRef]

- Kiymaz, Halil. 2019. Factors influencing SRI fund performance. Journal of Capital Markets Studies 3: 68–81. [Google Scholar] [CrossRef]

- Kostovetsky, Leonard. 2003. Index mutual funds and exchange-traded funds. Journal of Portfolio Management 29: 80–92. [Google Scholar] [CrossRef]

- Lettau, Martin, and Markus Pelger. 2020. Factors that fit the time series and cross-section of stock returns. The Review of Financial Studies 33: 2274–325. [Google Scholar] [CrossRef]

- Lobato, Manuel, Javier Rodríguez, and Herminio Romero. 2021. A volatility-match approach to measure performance: The case of socially responsible exchange-traded funds (ETFs). The Journal of Risk Finance 22: 34–43. [Google Scholar] [CrossRef]

- Murthi, B. P. S., Yoon K. Choi, and Preyas Desai. 1997. Efficiency of mutual funds and portfolio performance measurement: A non-parametric approach. European Journal of Operational Research 98: 408–18. [Google Scholar] [CrossRef]

- Navratil, Robert, Stephen Taylor, and Jan Vecer. 2021. On equity market inefficiency during the COVID-19 pandemic. International Review of Financial Analysis 77: 101820. [Google Scholar] [CrossRef]

- Neves, Maria Elisabete Duarte, Carla Manuela Fernandes, and Pedro Coimbra Martins. 2019. Are ETFs good vehicles for diversification? New evidence for critical investment periods. Borsa Istanbul Review 19: 149–57. [Google Scholar] [CrossRef]

- Osterhoff, Friedrich, and Christoph Kaserer. 2016. Determinants of tracking error in German ETFs–the role of market liquidity. Managerial Finance 42: 417–37. [Google Scholar] [CrossRef]

- Portela, Silva, Emmanuel Thanassoulis, and Gary Simpson. 2004. Negative data in DEA: A directional distance approach applied to bank branches. Journal of the Operational Research Society 55: 1111–21. [Google Scholar] [CrossRef]

- Poterba, James M., and John B. Shoven. 2002. Exchange-traded Funds: A New Investment Option for Taxable Investors. American Economic Review 92: 422–27. [Google Scholar] [CrossRef]

- Prasanna, P. Krishna. 2012. Performance of Exchange-Traded Funds in India. International Journal of Business and Management 7: 122. [Google Scholar] [CrossRef]

- Proença, C., E. Neves, M. Gouveia, and M. Madaleno. 2023. Technological, healthcare and consumer: Influence of COVID-19. Operational Research, unpublished. [Google Scholar]

- Roll, Richard. 1978. Ambiguity when performance is measured by the securities market line. The Journal of Finance 33: 1051–69. [Google Scholar] [CrossRef]

- Sharp, John A., Wang Meng, and Wei Liu. 2007. A modified slacks-based measure model for data envelopment analysis with “natural” negative outputs and inputs. Journal of the Operational Research Society 58: 1672–77. [Google Scholar] [CrossRef]

- Sharpe, William F. 1966. Mutual Fund Performance, Part 2: Supplement on Security Prices. The Journal of Business 39: 119–38. [Google Scholar] [CrossRef]

- Tone, Kaoru. 2001. Slacks-Based measure of efficiency. European Journal of Operational Research 130: 498–509. [Google Scholar] [CrossRef]

- Tone, Kaoru, Tsung-Sheng Chang, and Chen-Hui Wu. 2019. Handling negative data in slacks-based measure data envelopment analysis models. European Journal of Operational Research 282: 926–35. [Google Scholar] [CrossRef]

- Tsolas, Ioannis E. 2019. Utility exchange traded fund performance evaluation. A comparative approach using grey relational analysis and data envelopment analysis Modelling. International Journal of Financial Studies 7: 67. [Google Scholar] [CrossRef]

- Tsolas, Ioannis E. 2022. Performance Evaluation of Utility Exchange-Traded Funds: A Super-Efficiency Approach. Journal of Risk and Financial Management 15: 318. [Google Scholar] [CrossRef]

- Tsolas, Ioannis E., and Vincent Charles. 2015. Green exchange-traded fund performance appraisal using slacks-based DEA models. Operational Research 15: 51–77. [Google Scholar] [CrossRef]

- Zopounidis, Constantin, Michael Doumpos, and Panos M. Pardalos, eds. 2010. Handbook of Financial Engineering. Berlin: Springer Science & Business Media, vol. 18. [Google Scholar]

| Models | Input | Output |

|---|---|---|

| DEA 1 (M1) | Beta and standard deviation | Jensen’s Alpha and Sharpe ratio |

| DEA 2 (M2) | Beta and standard deviation | Jensen’s Alpha and trailing total return |

| DEA 3 (M3) | Beta and standard deviation | Sharpe ratio and total trailing return |

| DEA 4 (M4) | Beta and standard deviation | Jensen’s Alpha, Sharpe ratio, and trailing total return |

| Models | Period | Input | Output | Efficient ETFs Global | US Efficient ETFs | EUR Efficient ETFs |

|---|---|---|---|---|---|---|

| M1 | 1 Year | Beta Standard deviation | Jensen’s Alpha Sharpe ratio | EWA, EWM, CPXJ, CUKS, IEMS | EWA, EWM | CPXJ, CUKS, IEMS, ISFR |

| 3 Years | IVV, URTH, EWA, EWM, CSPX, SSAC | IVV, URTH, EWA, EWM, EWJ | CSPX, CUKS, ISFR | |||

| 5 Years | SCJ, CSPX, SSAC | SCJ, IVV | CSPX, SSAC CUKS, ISFR | |||

| M2 | 1 Year | Beta Standard deviation | Jensen’s Alpha trailing total return | EWA, EWM, CPXJ, CUKS, and IEMS | EWA, EWM | CPXJ, CUKS, SAUS, ISFR, IEMS |

| 3 Years | IVV, URTH, EWA, EWM, CSPX, SSAC | IVV, URTH, EWA, EWM, EWJ | CSPX, SSAC CUKS, ISFR | |||

| 5 Years | EEMA, SCJ, CSPX, SSAC, XMJD | EEMA, SCJ, IVV | CSPX, SSAC, CUKS, ISFR, XMJD | |||

| M3 | 1 Year | Beta Standard deviation | Sharpe ratio, trailing total return | EWA, EWM, CPXJ, CUKS, IEMS | EWA, EWM | CPXJ, IEMS, SAUS, ISFR |

| 3 Years | IVV, URTH, EWA, EWM, CSPX, SSAC | IVV, URTH, EWA, EWM, EWJ | CSPX, SSAC CUKS, ISFR | |||

| 5 Years | EEMA, SCJ, CSPX, SSAC XMJD | EEMA, SCJ, IVV | CSPX, SSAC, XMJD, ISFR | |||

| M4 | 1 Year | Beta Standard deviation | Jensen’s Alpha Sharpe ratio Trailing total return | EWA, EWM, CPXJ, | EWA, EWM | CPXJ, SAUS, IEMS, CUKS, ISFR |

| 3 Years | IVV, URTH, EWA, EWM, CSPX, SSAC | IVV, URTH, EWA, EWM, EWJ | CSPX, SSAC CUKS, ISFR | |||

| 5 Years | EEMA, SCJ, CSPX, SSAC, XMJD | EEMA, SCJ, IVV | CSPX, SSAC, XMJD, ISFR, CUKS |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Henriques, C.O.; Neves, M.E.; Conceição, J.A.; Vieira, E.S. Performance of US and European Exchange Traded Funds: A Base Point-Slack-Based Measure Approach. J. Risk Financial Manag. 2023, 16, 130. https://doi.org/10.3390/jrfm16020130

Henriques CO, Neves ME, Conceição JA, Vieira ES. Performance of US and European Exchange Traded Funds: A Base Point-Slack-Based Measure Approach. Journal of Risk and Financial Management. 2023; 16(2):130. https://doi.org/10.3390/jrfm16020130

Chicago/Turabian StyleHenriques, Carla O., Maria E. Neves, Jeremias A. Conceição, and Elisabete S. Vieira. 2023. "Performance of US and European Exchange Traded Funds: A Base Point-Slack-Based Measure Approach" Journal of Risk and Financial Management 16, no. 2: 130. https://doi.org/10.3390/jrfm16020130

APA StyleHenriques, C. O., Neves, M. E., Conceição, J. A., & Vieira, E. S. (2023). Performance of US and European Exchange Traded Funds: A Base Point-Slack-Based Measure Approach. Journal of Risk and Financial Management, 16(2), 130. https://doi.org/10.3390/jrfm16020130