A bank’s competitive attitude is majorly influenced by its risk-taking behavior; generally, banks with a higher risk-taking capability tend to be more competitive. However, such competitive nature without an efficient risk management framework often leads to insolvencies, which, in turn, may lead to ‘bank-run’, which is responsible for risk spillover onto the larger banking system, thereby resulting in systemic risk accumulation.

There are two major hypotheses that serve as a fulcrum around which the theory of banking competition stands—competition stability and competition fragility. While the former (i.e., competition stability) is based on two approaches (i.e., ‘too big to fail’ and the ‘risk-shifting paradigm’), the latter (i.e., competition fragility) revolves around the ‘franchise value hypothesis’.

1.3. Lerner Index and Its Extended Measure of Competition

The Lerner index is defined as the ratio of differences between price and marginal cost to price. This is a popular measure to estimate market power and is based on the static oligopoly theory. The Lerner index is based on the assumption that firms produce a single product. However, in today’s competitive environment, firms make multiple products, and banks are no exception; they too offer numerous products and services. Hence, the concept of the multi-product Lerner index (MPLI) evolved, where

Ten Kate and Kate (

2013) proposed a method to aggregate product by product elasticities instead of a group of products. Besides the above-mentioned drawback, there are other limitations of the Lerner index, which have been addressed and improved using the scale-corrected price-cost margin Lerner index (

Spierdijka and Zaourasa 2018), the copula-based stochastic frontier model (

Huang et al. 2017), the frontier-based measure using service line (

Bolt and Humphrey 2015), etc.

Clerides et al. (

2015) measured competition using three methods, namely the Lerner index, the adjusted Lerner index, and profit elasticity. They found that competition in the banking system was reduced from 1998 to 2006 but increased thereafter until 2008. Notably, the competition level was more for high-income regions but low in low-income countries. Thus, their study illuminated that with the approach of GFC, the banking system essentially became more competitive. Further,

Bolt and Humphrey (

2015), while examining competition for US banks, indicated that traditional measures such as the Lerner index, H-statistic, and HHI are not sufficient to assess bank competition. They suggested a frontier-based measure to estimate banking competition, using a service line capable of evaluating competition even with missing output and price data.

Huang et al. (

2017) proposed a method of estimating market power and cost efficiency in two markets using the copula-based stochastic frontier model. This method measures potential Lerner indices comprising of the Lerner index and marginal cost gap ratio. New Lerner indices are evaluated using three simultaneous equations consisting of cost frontier and two output price frontier equations.

Spierdijk and Zaouras (

2017) indicated that the positive value of the Lerner index highlights market power, but its magnitude cannot rightly justify the strength of the market power.

Spierdijka and Zaourasa (

2018) proposed a scale-corrected price-cost margin preferred over the traditional Lerner index, as a positive Lerner index may measure banks’ capability to earn non-negative profits over market power, especially in situations of economies of scale, when margin-cost pricing yields negative profits. This corrected Lerner index was empirically validated for US banks (2000–2014), showing significant market power for sample banks.

Huang et al. (

2018) jointly estimated market power and cost efficiency in a single step and used copula to incorporate the dependency between the two. The Lerner index is used to measure market power, while the stochastic frontier method assesses cost efficiency.

The network theory is used to examine the interconnectedness between the global and other systemically important institutions (

Andries et al. 2020). In fact, this theory is widely used to examine the contagion effect, resulting in systemic risk spillover. However, the network topology remains unexplored in assessing banking competition. In the past, several pieces of literature have indicated that a bank’s market power is influenced by size, capitalization, profitability, and phases of the economy (

Bikker et al. 2006;

Santoso et al. 2021;

Torre Olmo et al. 2021;

Apergis 2015).

Bikker et al. (

2006) implemented the extended version of Panzar–Rosse model to examine bank competition for 18,000 banks across 101 countries. They found that big-sized banks have more market power than small-sized banks.

Torre Olmo et al. (

2021) examined the impact of sustainable banking practices on the profitability and insolvency risks of 1236 banks from 48 countries. They noted that banks that operate in the market with a higher concentration have higher profitability. Bank capitalization has higher market power and thereby helps in enhancing stability (

Santoso et al. 2021).

Apergis (

2015) used the Panzar–Rosse model to examine banking competition for emerging economies during 2000 to 2012; they found a decrease in banking competition after GFC.

In India, banking competition is strong and is characterized by a monopolistic nature (

Li et al. 2019). This intense competition is due to various government policies that have promoted the same.

Bhattacharya and Das (

2003) highlighted a significant change in the market structure of banks during the early 1990s; interestingly, they remained majorly unaffected even with mergers during the latter part of the decade.

Prasad and Ghosh (

2005) stated that the Indian banking system is competitive with considerable revenue earnings, thereby indicating its monopolistic nature.

Arrawatia et al. (

2019) examined banking competition using the risk-adjusted Lerner index and found improvements in competition for Indian banks.

COVID-19 has hammered the global economy to a great extent.

Batool et al. (

2020) talked about massive economic fallouts due to the lockdowns that were imposed. They used Google trend data and examined the changes in the search patterns. They found that sectors such as transportation and accommodation were negatively impacted by the lockdowns; on the other hand, sectors such as freelance work, streaming services, and online deliveries showed an increase in Google searches.

Mehdiabadi et al. (

2020) illustrated the integration of Banking 4.0 with Industry 4.0. The authors highlighted that banks should match themselves with technology advancements and should be more customer-centric. They recommended that fourth-generation banks should work in association with knowledge-based companies to provide better-operating methods. Furthermore, while studying the stock market performance of 80 countries during COVID-19,

Burdekin and Harrison (

2021) found that there was a deterioration in stock market performance with an increase in the number of COVID-19 cases. Importantly, during this ongoing pandemic, banks should closely work with industries to improve the economy.

Extant literature has covered various methods to estimate market power. The most widely used technique is the Lerner index. However, literature has cited that such methods to have drawbacks (

Spierdijk and Zaouras 2017;

Bolt and Humphrey 2015;

Spierdijka and Zaourasa 2018) and hence has covered extended measures of the Lerner index. As banks operate in an interconnected environment, they are constantly faced with competition from network banks. Thus, it becomes imperative to examine competition from the perspective of the banking system at large. However, extant literature does not seem to have enough empirical evidence to factor in the ‘interconnectedness’ among banks while assessing competition. Therefore, we attempt to use the contemporary network theory to analyze banking competition, both at the system and the bank level. Ever since the GFC, India has witnessed several booms and busts within its own economy that have specifically impacted its banking system. Specifically, post-GFC, India did witness an economic upsurge, characterized by a high credit off-take. However, in early 2015, large amount of banking assets were declared non-performing with a handful of corporate defaults, raising questions on financial stability. Thus, it becomes a crucial research objective to examine whether lower banking competition leads to the sanctioning of loans at a high net-interest margin, which results in the curse of rapid growth in NPAs. Again, in early 2020, the ongoing COVID-19 pandemic posed a global challenge, with India being no exception. Therefore, there is an urgent need to understand banking competition during such rare global events encompassing public health turmoil.

In this context, we frame the following objectives:

- (1)

Estimate the Lerner index to examine the market power of banks.

- (2)

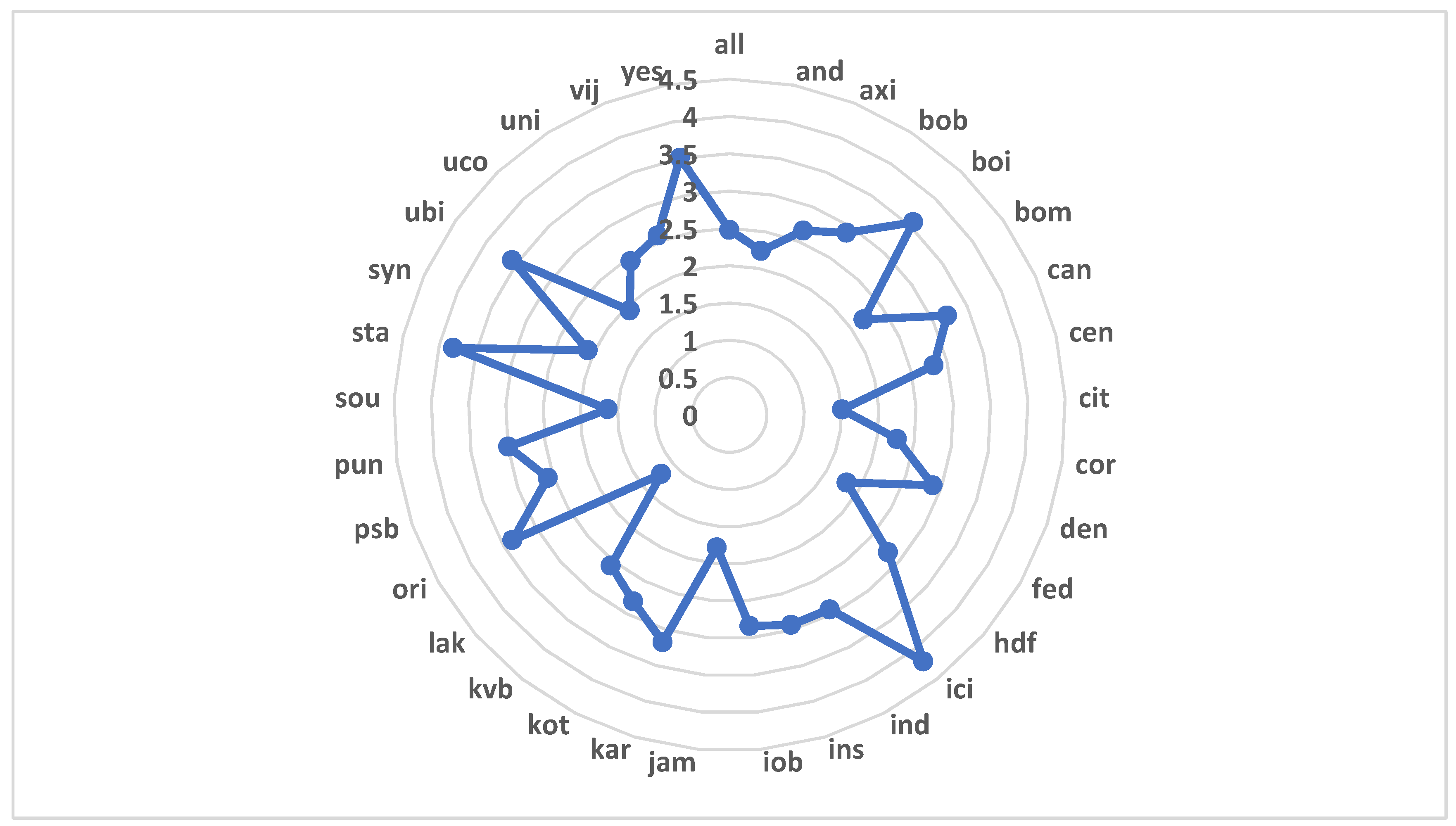

Construct a competitive network structure for the Indian banking system, estimate the system and nodal properties, and identify cluster formation using the page-rank algorithm.

- (3)

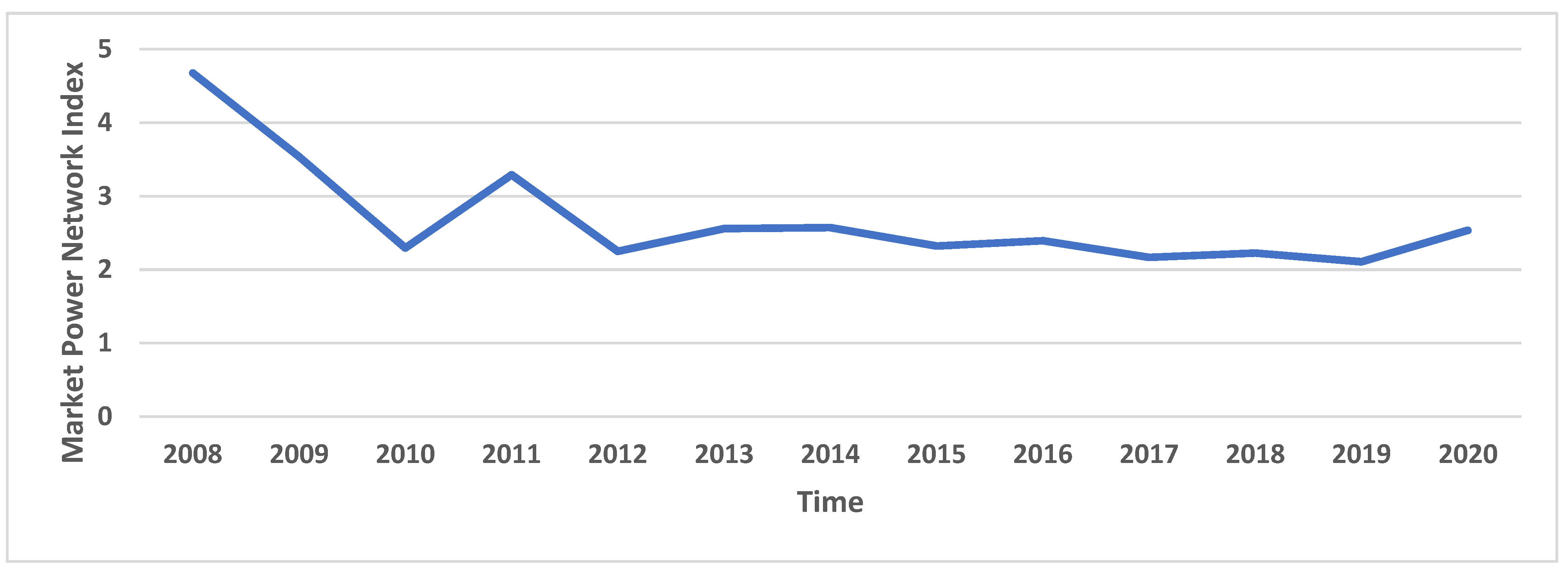

Develop a Market Power Network Index (MPNI), which measures the market power of banks by considering their operation within an interconnected environment.

The Indian banking system passed through a Non-Performing Loan (NPL) crisis in early 2015, as there were multiple corporate loans, which at that point were defaulted. In fact, even during the ongoing COVID-19 pandemic, we have witnessed a major economic slowdown with the banking system being no exception. Although network theory is widely used to examine the contagion effect, the method remains unexplored in the field of banking competition. Effectively, this is what motivated us to explore banking competition in India, using the contemporary network theory.

This paper built network structures for the Indian banking system, clearly showing the clusters of banks that were involved in competition. Network properties, namely centroid, average path length, distance of a node from the centroid, total number of connections in the inter-bank market, and network density are estimated and have the potential to explain banking competition. Our findings show that the estimated network properties indicate a lower level of competition during crisis periods. In effect, we used network properties to propose the Market Power Network Index (MPNI), which can be considered as an alternative method to assess banking competition. Interestingly, the MPNI showed the highest value during GFC followed by the COVID-19 pandemic, thereby indicating a lower level of competition during said periods. Further, we observed that big-sized, profitable, capital adequate, and public banks have higher market power.

The salience of this paper is that it is one of the first to examine banking competition using the Network Theory. Notably, the design implemented herein to examine banking competition using the contemporary network model has its own advantages, as it measures competition by considering the banking system at large, rather than assessing competition on a standalone basis.

The period of our study is from 2008 to 2020, covering the periods of the GFC (2008–2009), the high credit off-take period (2010–2014), the non-performing loan crisis (2015–2018), the pre-COVID-19 periods (2019), and the COVID-19 periods (2020). This broad timeframe enables us to examine the nature of banking competition during different time horizons. This would also enable us to scrutinize the market power of banks during rare events, such as the ongoing COVID-19 pandemic.

The remaining paper is organized as follows:

Section 2 discusses the methodology to construct a competitive network structure and proposes a new index to measure a bank’s market power.

Section 3 discusses the results of competitiveness among Indian banks, and the banking system overall; specifically, it focuses on different economic phases.

Section 4 concludes by providing policy implications while highlighting the future scope of the study.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}