The Impact of the Available Infrastructure on the Electric Vehicle Market in Poland and in EU Countries

Abstract

1. Introduction

2. Materials and Methods

2.1. Employment Scenario in Automotive Industry in Poland and Selected EU Member States

2.2. Car Market in Europe

2.3. Electric Car Infrastructure

2.4. Electric Car Infrastructure in Poland

2.5. Statistical Analysis

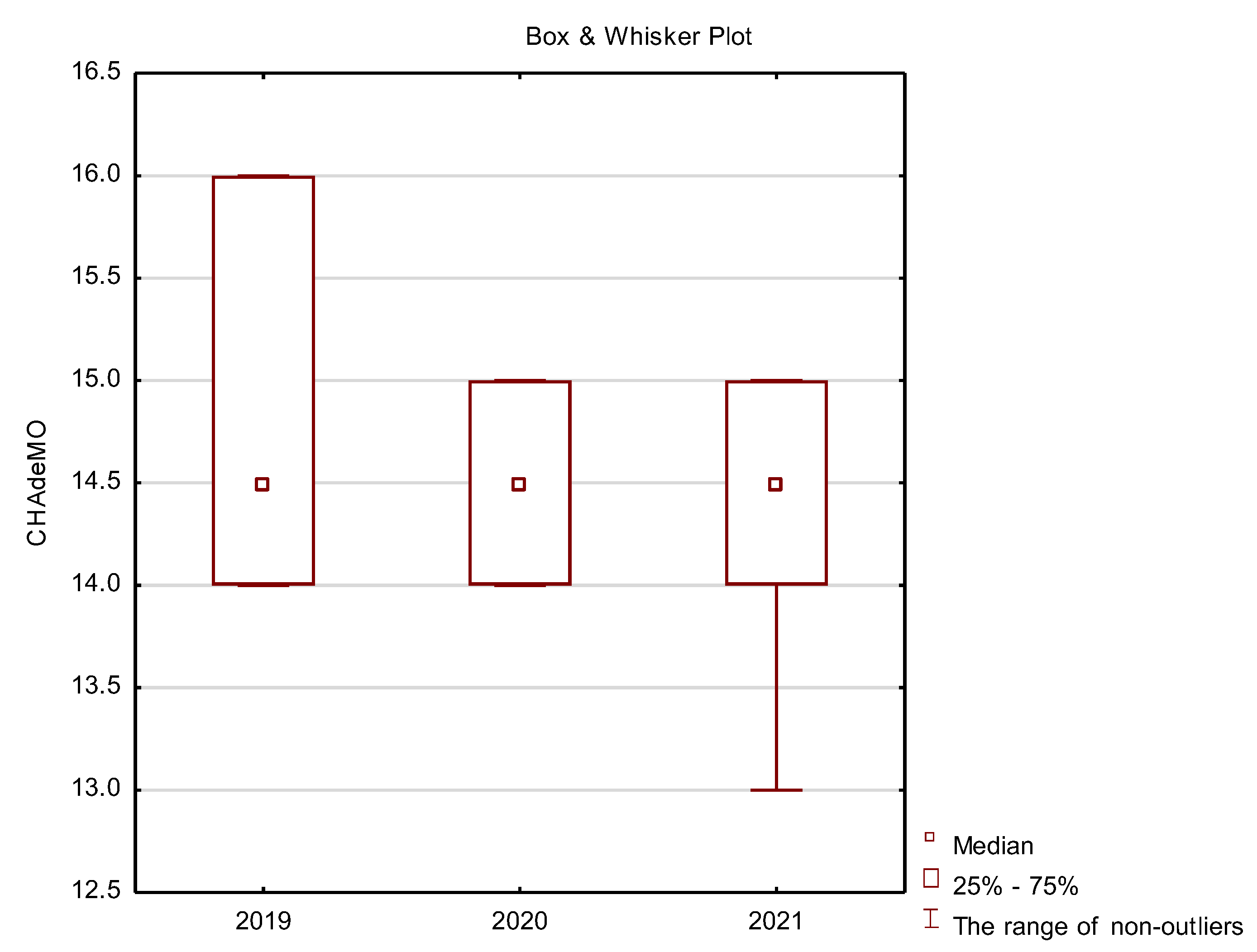

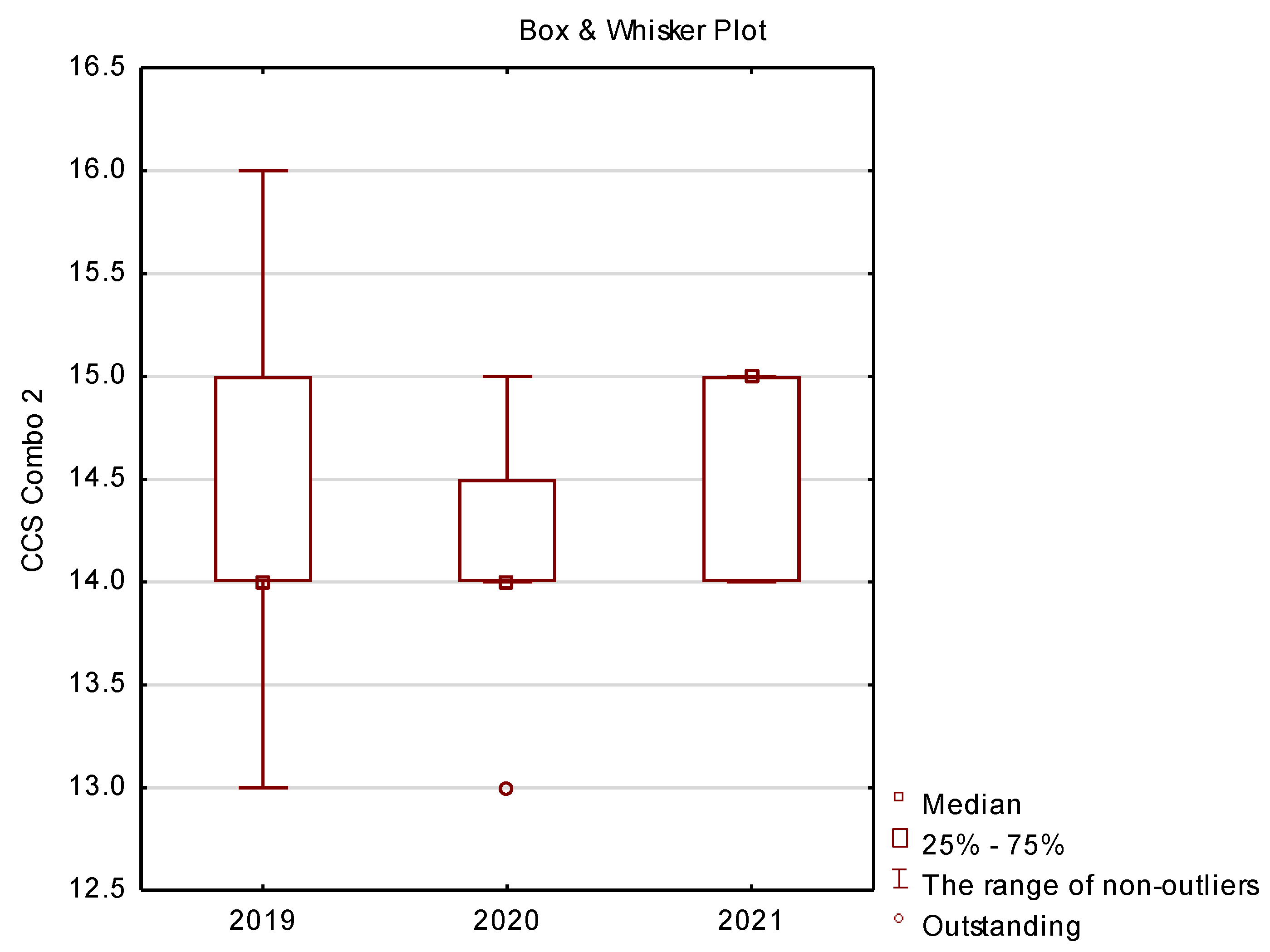

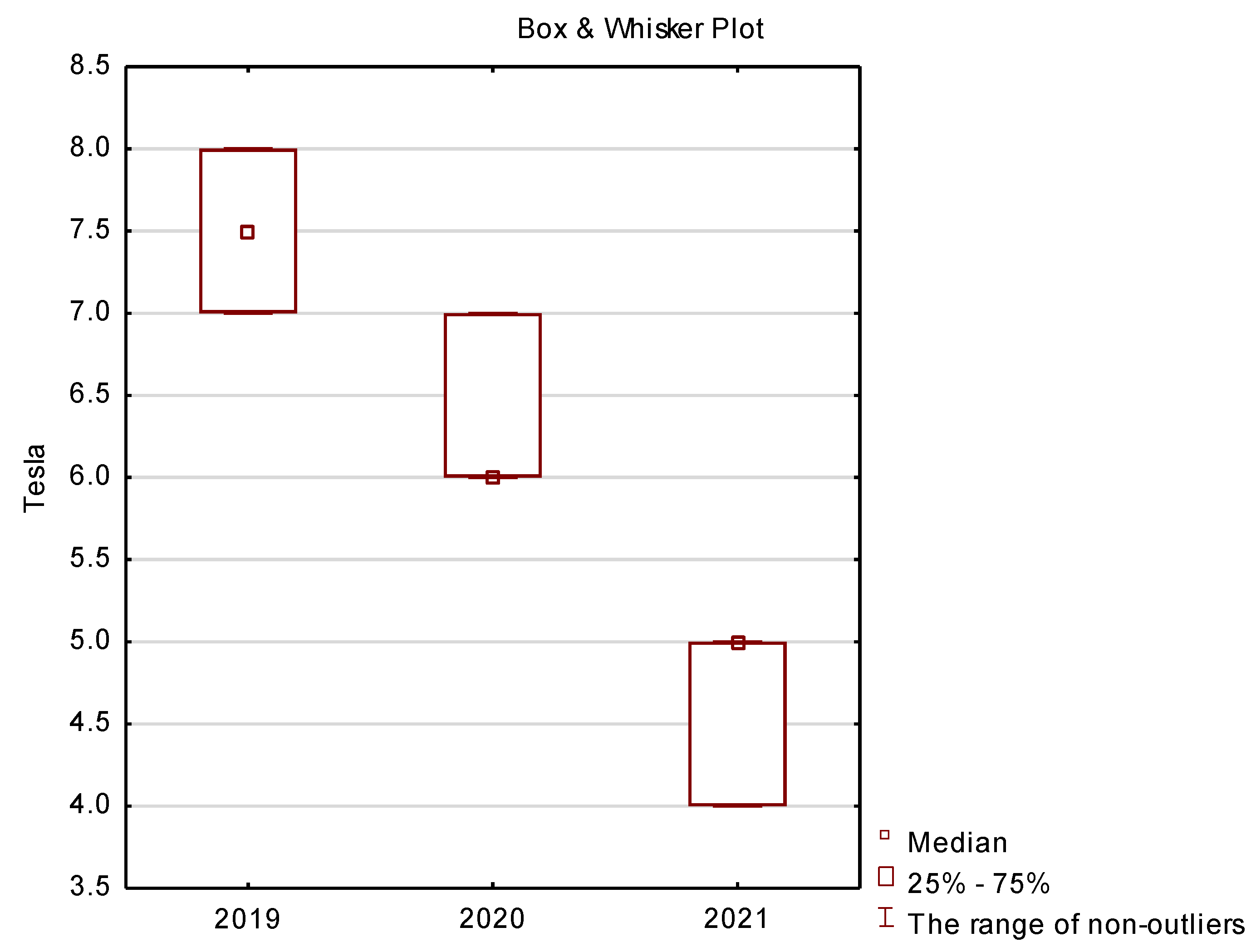

Statistical Analysis—Correlation Analysis between AC and DC Vehicle Charging Stations

3. Results

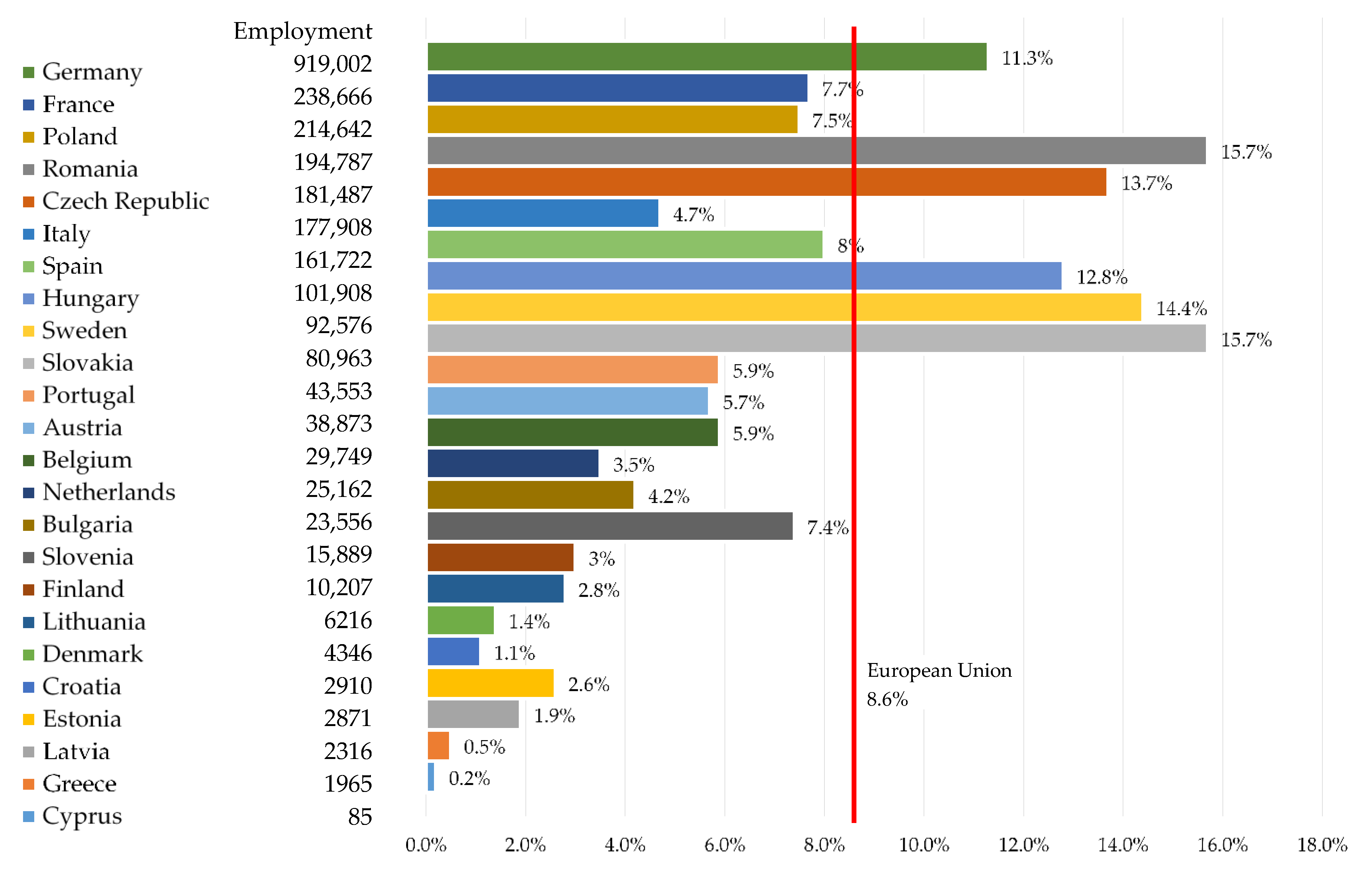

- At the end of 2021, there were 2,571,359 people employed in the automotive industry in the European Union, of which, 214,642 in Poland. Most people were employed in Germany—919,002 people.

- In the European Union and in Poland, the entire automotive sector is developing very dynamically. It is a significant employer and one of the largest branches of the economy. Currently, the automotive industry in Poland accounts for 8% of GDP and approx. 13.5% of export value. The automotive industry is currently undergoing the fourth industrial revolution. Technologies that help optimize production and artificial intelligence which drives the development of autonomous cars, have a key impact on the industry.

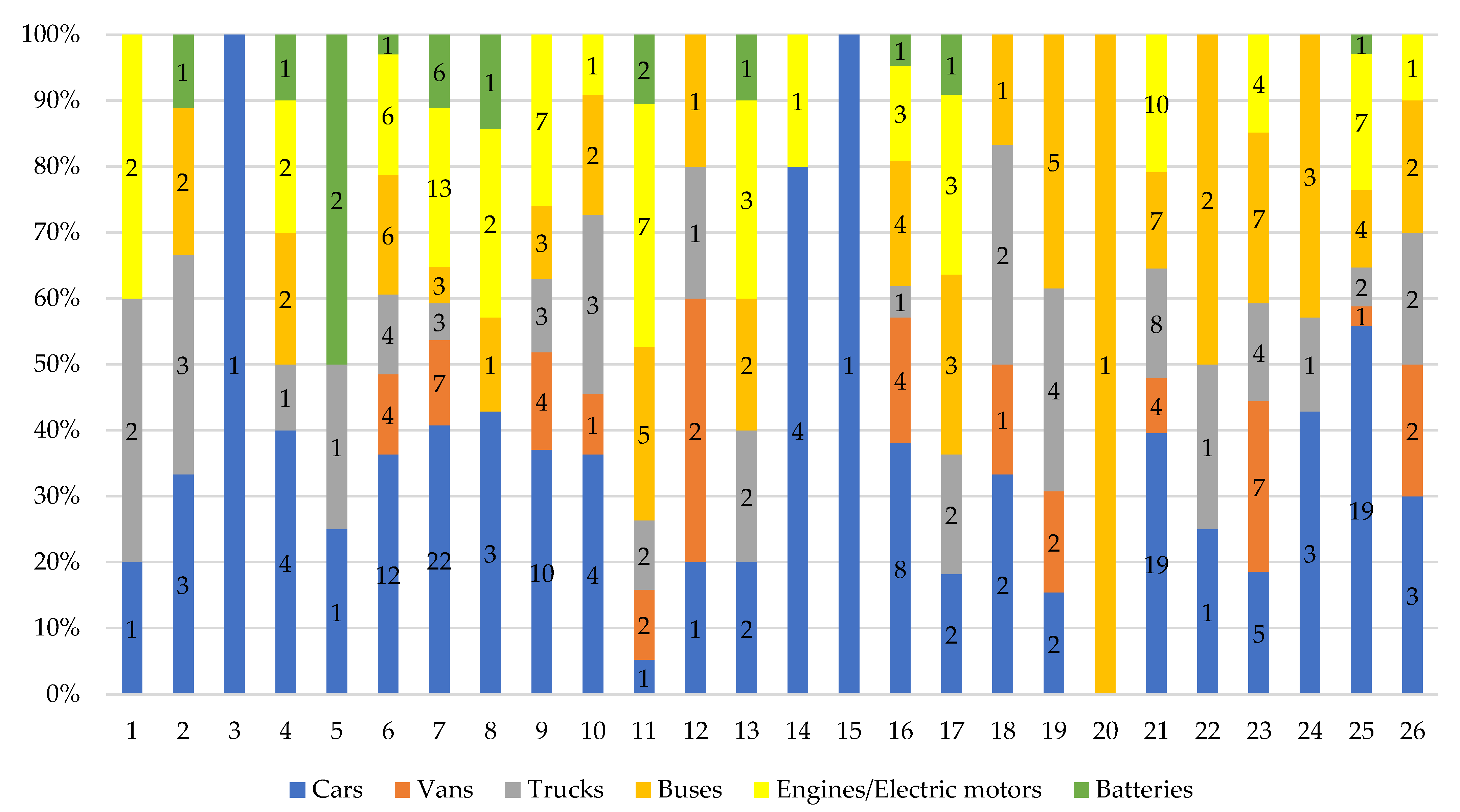

- In 2022, there are 301 car engine assembly and production plants operating in Europe, of which 194 are located in the European Union (EU-27). Most factories are located in Germany. Among the countries outside the EU, Russia should be mentioned with 33 factories producing cars and components.

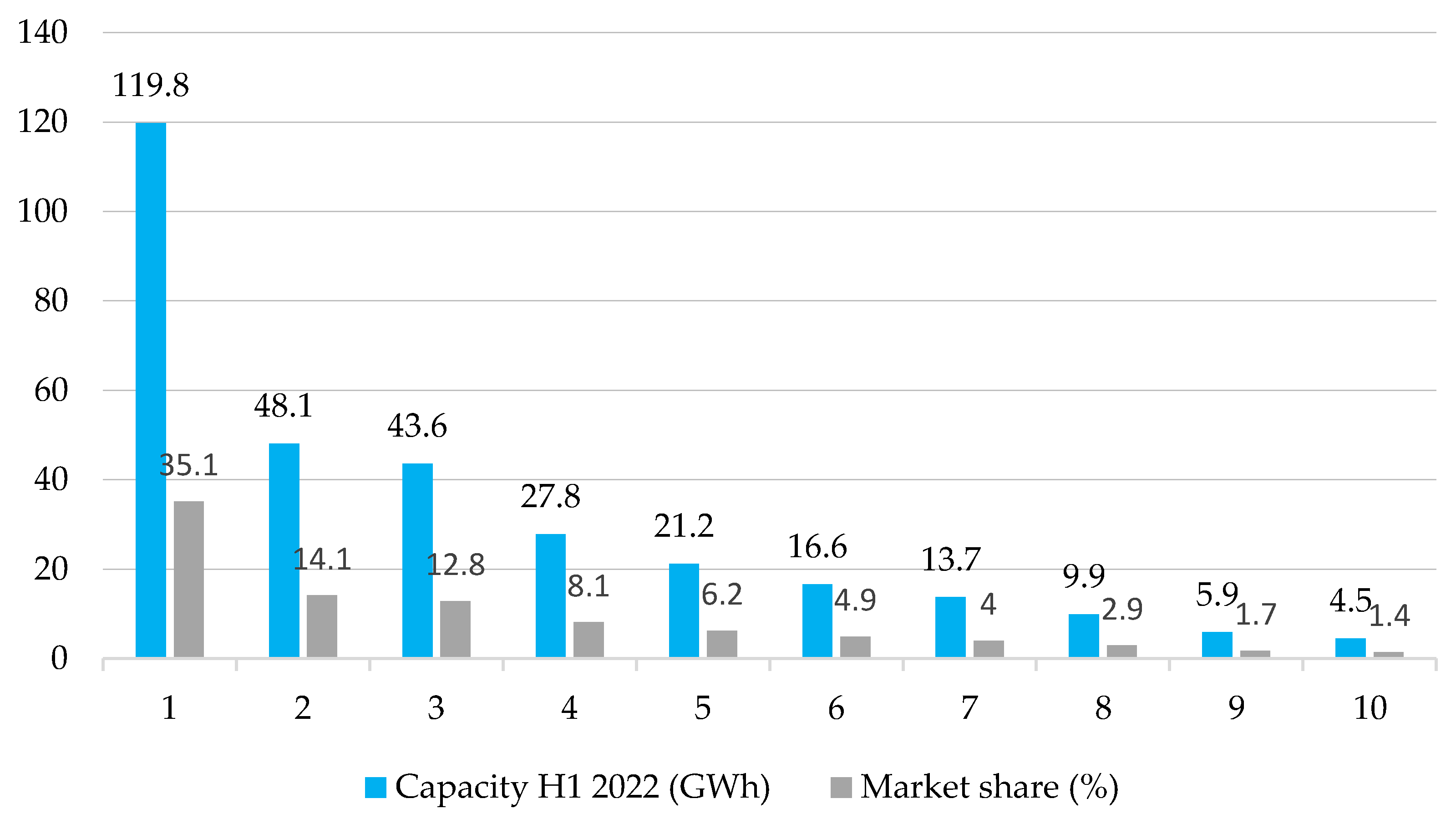

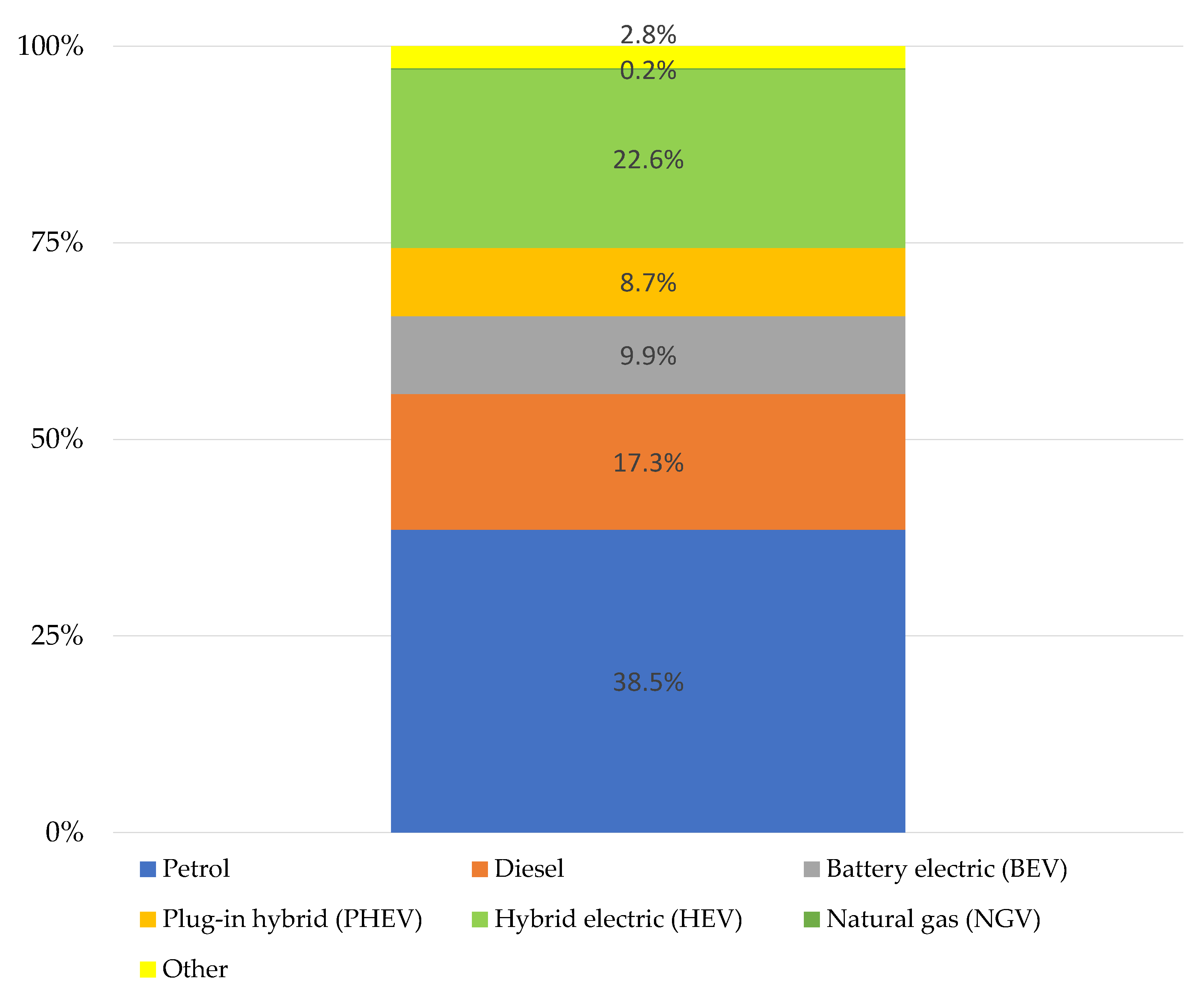

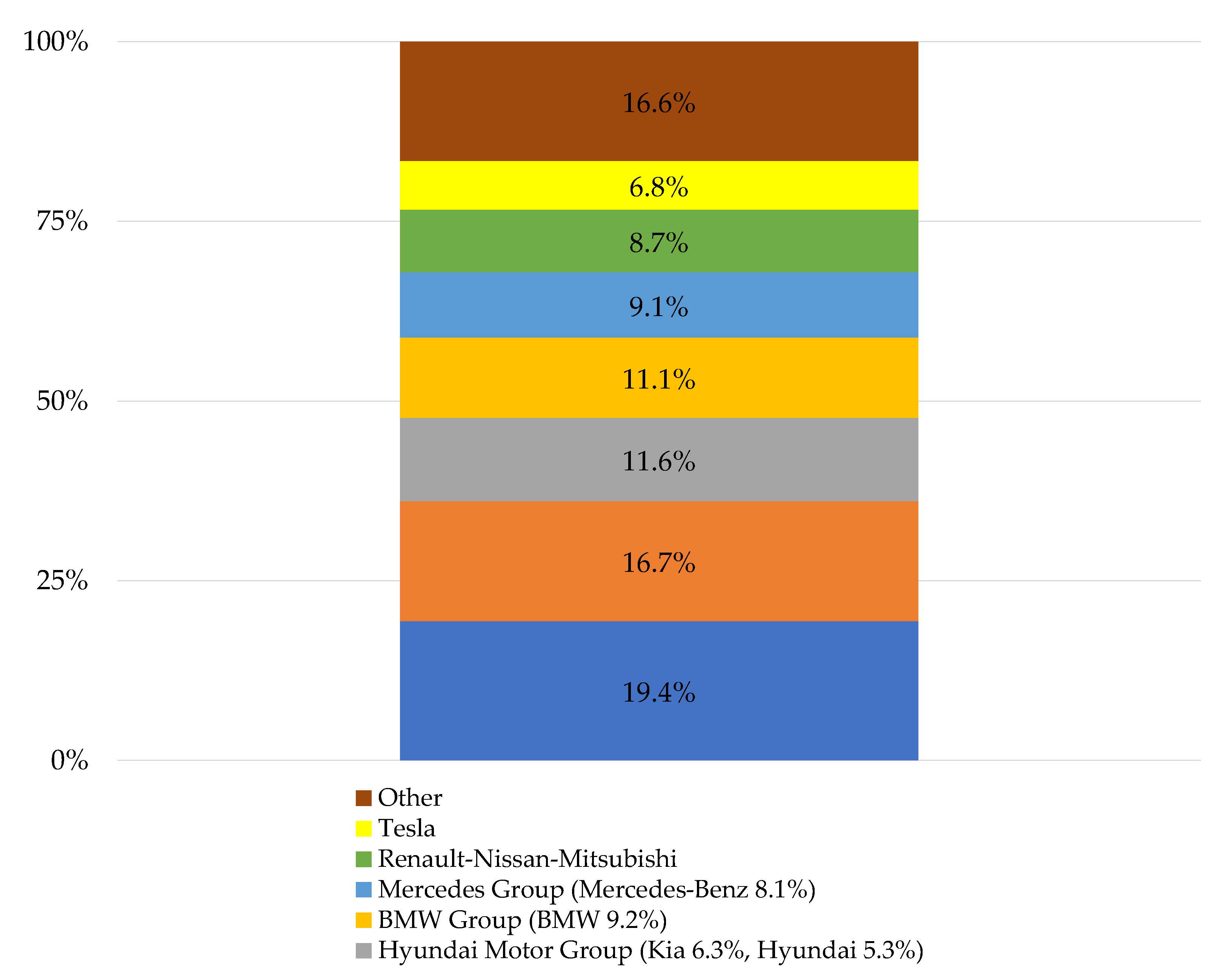

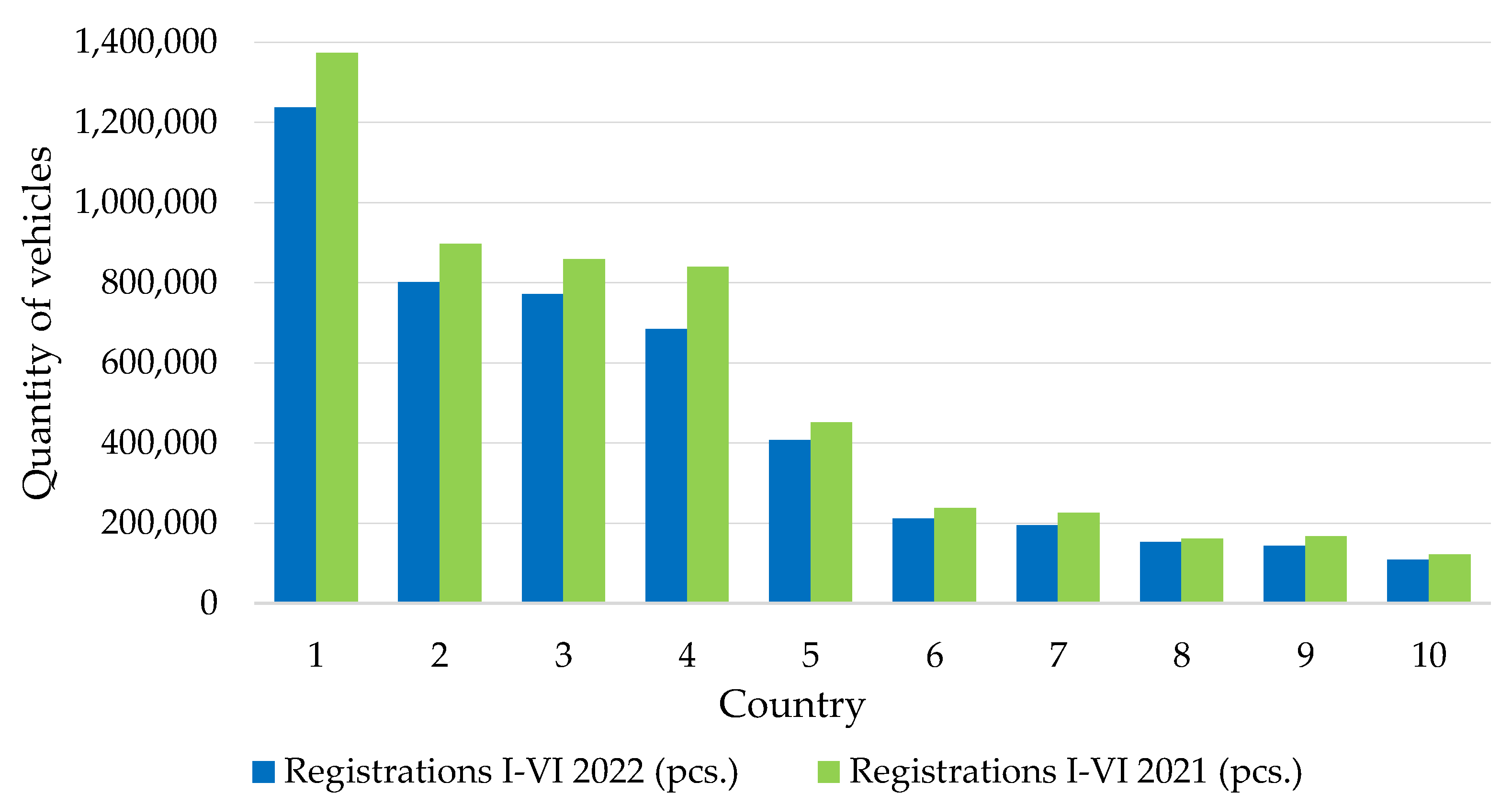

- In the first half of 2022, 5,027,547 new cars appeared in Europe, 13.7% less than in the same period of 2021. Sales of battery electric vehicles in the EU accounted for 9.9% of all passenger car registrations.

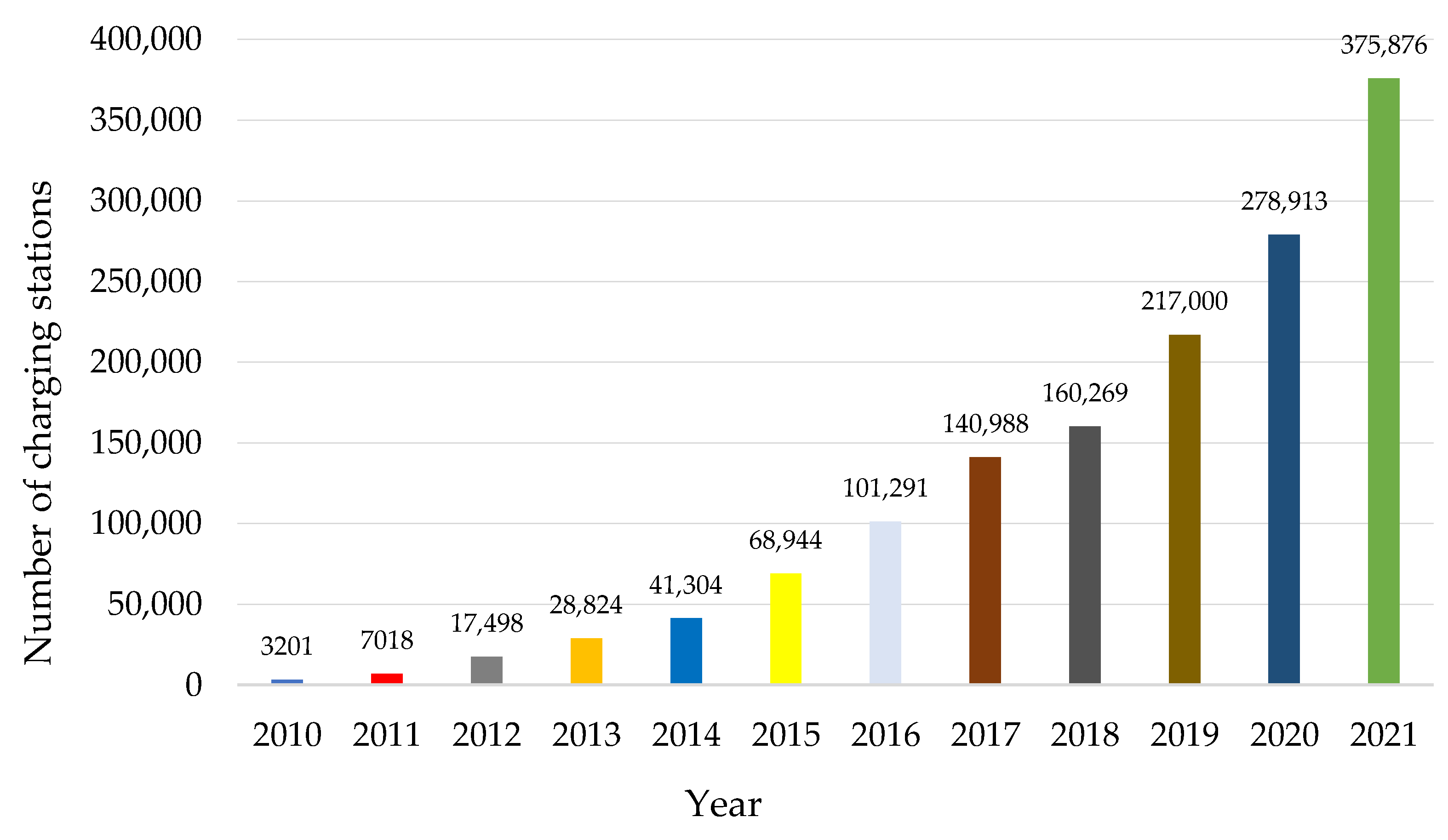

- In 2021, across Europe, there were over 380,000 charging outlets.

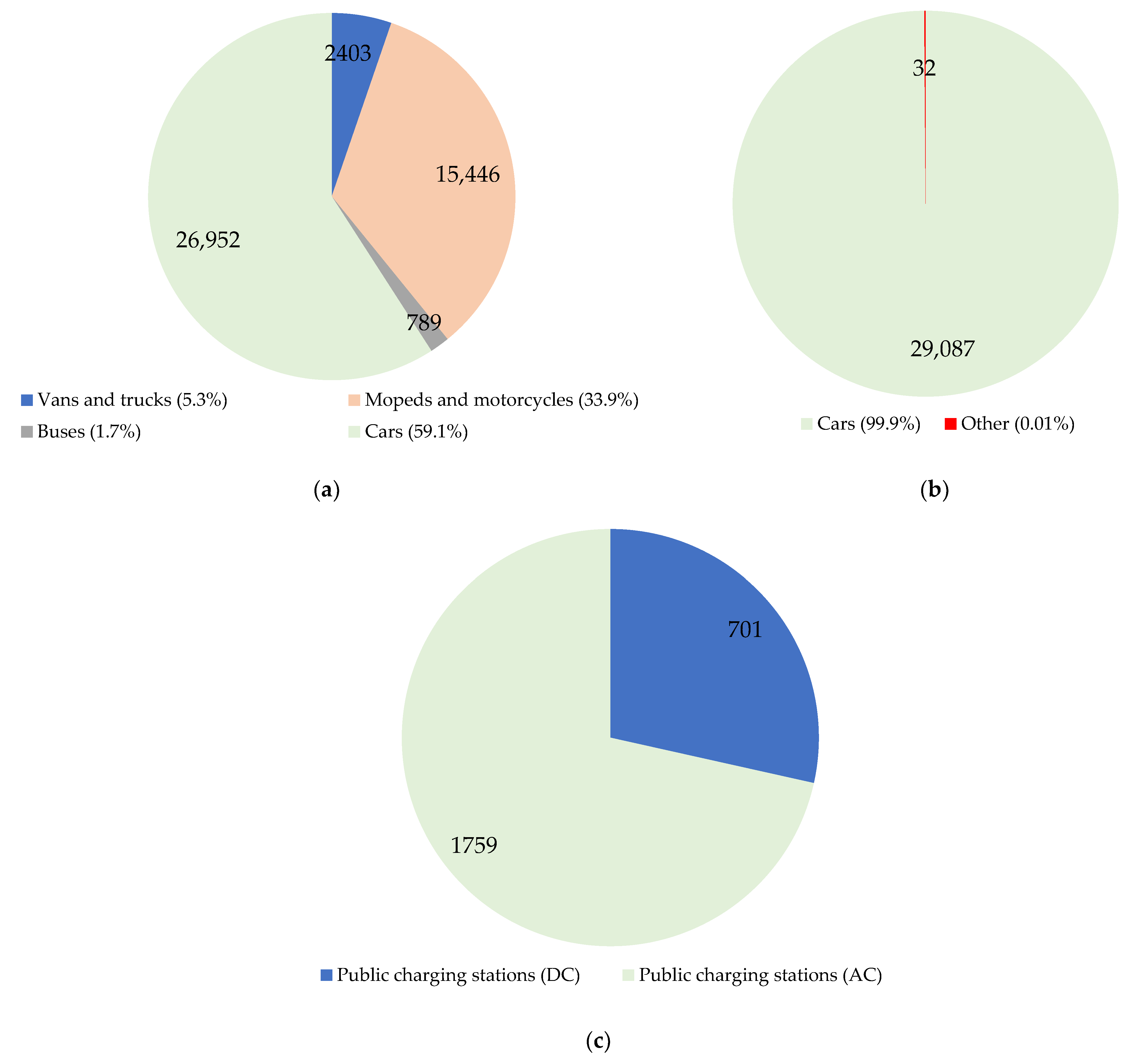

- In September 2022, there were 58,474 electric vehicles registered in Poland, including BEV (49%) and PHEV (51%). The fleet of electric buses in Poland has increased to 789 units.

- At the end of September 2022, there were 2460 charging stations in Poland for 58,474 electric vehicles.

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Papież, M.; Śmiech, S.; Frodyma, K. Does the European Union energy policy support progress in decoupling economic growth from emissions? Energy Policy 2022, 170, 113247. [Google Scholar] [CrossRef]

- Jakučionytė-Skodienė, M.; Krikštolaitis, R.; Liobikienė, G. The contribution of changes in climate-friendly behaviour, climate change concern and personal responsibility to household greenhouse gas emissions: Heating/cooling and transport activities in the European Union. Energy 2022, 246, 123387. [Google Scholar] [CrossRef]

- Barisa, A.; Rosa, M. A system dynamics model for CO2 emission mitigation policy design in road transport sector. Energy Procedia 2018, 147, 419–427. [Google Scholar] [CrossRef]

- Andrés, L.; Padilla, E. Driving factors of GHG emissions in the EU transport activity. Transport Policy 2018, 61, 60–74. [Google Scholar] [CrossRef]

- Haasz, T.; Vilchez, J.J.G.; Kunze, R.; Deane, P.; Fraboulet, D.; Fahl, U.; Mulholland, E. Perspectives on decarbonizing the transport sector in the EU-28. Energy Strategy Rev. 2018, 20, 124–132. [Google Scholar] [CrossRef]

- Sadik-Zada, E.R.; Gatto, A.; Scharfenstein, M. Sustainable management of lithium and green hydrogen and long-run perspectives of electromobility. Technol. Forecast. Soc. Change 2023, 186, 121992. [Google Scholar] [CrossRef]

- Zirganos, A.; Orfanou, F.; Vlahogianni, E.I.; Yannis, G. Evaluating good practices for the promotion of electromobility using multi criteria analysis methods. Case Stud. Transp. Policy 2022, 10, 1602–1610. [Google Scholar] [CrossRef]

- Jandásek, V.; Šimela, A.; Mücková, P.; Horák, B. Smart Grid and Electromobility. IFAC-PapersOnLine 2022, 55, 164–169. [Google Scholar] [CrossRef]

- Dzikuć, M.; Piwowar, A. Economic Aspects of Low Carbon Development. Energies 2022, 15, 5228. [Google Scholar] [CrossRef]

- Omahne, V.; Knez, M.; Obrecht, M. Social Aspects of Electric Vehicles Research—Trends and Relations to Sustainable Development Goals. World Electr. Veh. J. 2021, 12, 15. [Google Scholar] [CrossRef]

- Patel, A.R.; Tesoriere, G.; Campisi, T. Users’ Socio-economic Factors to Choose Electromobility for Future Smart Cities. In Computational Science and Its Applications—ICCSA 2022 Workshops, 1st ed.; ICCSA 2022. Lecture Notes in Computer Science; Gervasi, O., Murgante, B., Misra, S., Rocha, A.M.A.C., Garau, C., Eds.; Springer: Cham, Switzerland, 2022; Volume 13380, pp. 331–344. [Google Scholar] [CrossRef]

- Tucki, K.; Orynycz, O. Bioenergy and Biofuels. Sustainability 2021, 13, 9972. [Google Scholar] [CrossRef]

- Tucki, K.; Orynycz, O.; Mitoraj-Wojtanek, M. Perspectives for Mitigation of CO2 Emission due to Development of Electromobility in Several Countries. Energies 2020, 13, 4127. [Google Scholar] [CrossRef]

- Drábik, P.; Krnáčová, P. Socio-economic barriers and development opportunities of electromobility as key technological innovation of transportation. Int. J. Multidiscip. Bus. Sci. 2018, 4, 91–98. [Google Scholar]

- Mönnig, A.; Schneemann, C.; Weber, E.; Zika, G.; Helmrich, R. Electromobility 2035: Economic and Labour Market Effects through the Electrification of Powertrains in Passenger Cars, IAB-Discussion Paper, No. 8/2019, Institut für Arbeitsmarkt- und Berufsforschung (IAB), Nürnberg. Available online: https://www.econstor.eu/bitstream/10419/204855/1/1664536213.pdf (accessed on 10 December 2022).

- Pollák, F.; Vodák, J.; Soviar, J.; Markovič, P.; Lentini, G.; Mazzeschi, V.; Luè, A. Promotion of Electric Mobility in the European Union—Overview of Project PROMETEUS from the Perspective of Cohesion through Synergistic Cooperation on the Example of the Catching-Up Region. Sustainability 2021, 13, 1545. [Google Scholar] [CrossRef]

- Nur, A.I. The Limits of Indonesia’s Legal Framework for Electromobility: Regulatory and Sustainable Issues. Lentera Huk. 2022, 9, 211–236. [Google Scholar] [CrossRef]

- Feckova Skrabulakova, E.; Ivanova, M.; Rosova, A.; Gresova, E.; Sofranko, M.; Ferencz, V. On Electromobility Development and the Calculation of the Infrastructural Country Electromobility Coefficient. Processes 2021, 9, 222. [Google Scholar] [CrossRef]

- Skrúcaný, T.; Kendra, M.; Stopka, O.; Milojević, S.; Figlus, T.; Csiszár, C. Impact of the Electric Mobility Implementation on the Greenhouse Gases Production in Central European Countries. Sustainability 2019, 11, 4948. [Google Scholar] [CrossRef]

- Ovaere, M.; Proost, S. Cost-effective reduction of fossil energy use in the European transport sector: An assessment of the Fit for 55 Package. Energy Policy 2022, 168, 113085. [Google Scholar] [CrossRef]

- Poschmann, J.; Bach, V.; Finkbeiner, M. Are the EU climate ambitions reflected on member-state level for greenhouse gas reductions and renewable energy consumption shares? Energy Strategy Rev. 2022, 43, 100936. [Google Scholar] [CrossRef]

- Thiel, C.; Nijs, W.; Simoes, S.; Schmidt, J.; Van Zyl, A.; Schmid, E. The impact of the EU car CO2 regulation on the energy system and the role of electro-mobility to achieve transport decarbonization. Energy Policy 2016, 96, 153–166. [Google Scholar] [CrossRef]

- Cansino, J.M.; Sánchez-Braza, A.; Sanz-Díaz, T. Policy Instruments to Promote Electro-Mobility in the EU28: A Comprehensive Review. Sustainability 2018, 10, 25207. [Google Scholar] [CrossRef]

- Kupczyk, A.; Mączyńska, J.; Redlarski, G.; Tucki, K.; Bączyk, A.; Rutkowski, D. Selected Aspects of Biofuels Market and the Electromobility Development in Poland: Current Trends and Forecasting Changes. Appl. Sci. 2019, 9, 254. [Google Scholar] [CrossRef]

- Kallitsis, E.; Korre, A.; Kelsall, G.H. Life cycle assessment of recycling options for automotive Li-ion battery packs. J. Clean. Prod. 2022, 371, 133636. [Google Scholar] [CrossRef]

- Baldassarre, B.; Maury, T.; Mathieux, F.; Garbarino, E.; Antonopoulos, I.; Sala, S. Drivers and Barriers to the Circular Economy Transition: The Case of Recycled Plastics in the Automotive Sector in the European Union. Procedia CIRP 2022, 105, 37–42. [Google Scholar] [CrossRef]

- Tucki, K.; Orynycz, O.; Świć, A.; Mitoraj-Wojtanek, M. The Development of Electromobility in Poland and EU States as a Tool for Management of CO2 Emissions. Energies 2019, 12, 2942. [Google Scholar] [CrossRef]

- Tucki, K.; Krzywonos, M.; Orynycz, O.; Kupczyk, A.; Bączyk, A.; Wielewska, I. Analysis of the Possibility of Fulfilling the Paris Agreement by the Visegrad Group Countries. Sustainability 2021, 13, 8826. [Google Scholar] [CrossRef]

- Elektromobility Counter: A Significant Increase in the Number of Registrations of Electric Cars after Three Quarters of 2022. Available online: https://pspa.com.pl/2022/informacja/licznik-elektromobilnosci-znaczny-wzrost-liczby-rejestracji-samochodow-elektrycznych-po-trzech-kwartalach-2022-r/ (accessed on 17 November 2022).

- UL 2202—Standard for Safety for Electric Vehicle (EV) Charging System Equipment, Second Edition. Available online: https://www.intertek.com/automotive/electric-vehicle/evse/ul-2202/ (accessed on 7 December 2022).

- MET Certification. Available online: https://www.tde-lighttech.com/news/certification (accessed on 7 December 2022).

- The Electromobility Market is Growing—More and More Investments and Jobs. Available online: https://www.rynekelektryczny.pl/elektromobilnosc-w-polsce-statystyki-inwestycje-zatrudnienie/ (accessed on 17 November 2022).

- National Reconstruction Plan. Available online: https://www.gov.pl/web/planodbudowy (accessed on 7 December 2022).

- National Reconstruction Plan. Billion Goldes and New Taxes for Drivers. Available online: https://motopedia.otomoto.pl/krajowy-plan-odbudowy/ (accessed on 7 December 2022).

- Farsi, A.; Rosen, M.A. PEM fuel cell-assisted lithium ion battery electric vehicle integrated with an air-based thermal management system. Int. J. Hydrog. Energy 2022, 47, 35810–35824. [Google Scholar] [CrossRef]

- Rojas, O.E.; Khan, M.A. A review on electrical and mechanical performance parameters in lithium-ion battery packs. J. Clean. Prod. 2022, 378, 134381. [Google Scholar] [CrossRef]

- Greenpeace Report Troubleshoots China’s Electric Vehicles Boom, Highlights Critical Supply Risks for Lithium-ion Batteries. Available online: https://www.greenpeace.org/eastasia/press/6175/greenpeace-report-troubleshoots-chinas-electric-vehicles-boom-highlights-critical-supply-risks-for-lithium-ion-batteries/ (accessed on 17 November 2022).

- Vanderburgt, S.; Santos, R.M.; Chiang, Y.W. Is it worthwhile to recover lithium-ion battery electrolyte during lithium-ion battery recycling? Resour. Conserv. Recycl. 2022, 189, 106733. [Google Scholar] [CrossRef]

- Ali, H.; Khan, H.A.; Pecht, M. Preprocessing of spent lithium-ion batteries for recycling: Need, methods, and trends. Renew. Sustain. Energy Rev. 2022, 168, 112809. [Google Scholar] [CrossRef]

- Mishra, G.; Jha, R.; Meshram, A.; Singh, K.K. A review on recycling of lithium-ion batteries to recover critical metals. J. Environ. Chem. Eng. 2022, 10, 108534. [Google Scholar] [CrossRef]

- Raport EY. Power Sector Accelerating e-Mobility. Available online: https://assets.ey.com/content/dam/ey-sites/ey-com/pl_pl/news/2022/02/raport-ey/power-sector-accelerating-e-mobility-2022-ey-and-eurelectric-report.pdf (accessed on 17 November 2022).

- Raport. Electric Vehicle Charging Station Market by Application (Public, Private), Level of Charging, Charging Point Type, Infrastructure, Service Type, Installation, Electric Bus Charging, DC Fast Charging, IOT Connectivity and Region—Global Forecast to 2027. Available online: https://www.researchandmarkets.com/reports/5241528/electric-vehicle-charging-station-market-by (accessed on 17 November 2022).

- EV Readiness Index 2022. Available online: https://evmarketsreports.com/ev-readiness-index-2022-2/ (accessed on 17 November 2022).

- Sharing Economy. Available online: https://www.pwc.pl/pl/publikacje/2016/wspol-dziel-i-rzadz-sharing-economy.html (accessed on 7 December 2022).

- Electromobility is a Challenge for Car Sharing Companies. Available online: https://www.motofaktor.pl/elektromobilnosc-wyzwaniem-dla-firm-carsharingowych/ (accessed on 7 December 2022).

- Transport & Environment. Available online: https://www.transportenvironment.org/ (accessed on 17 November 2022).

- Report—Vehicles in Use, Europe 2022. Available online: https://www.acea.auto/publication/report-vehicles-in-use-europe-2022/ (accessed on 17 November 2022).

- Final Report. Evaluation of Primary Energy Factor Calculation Options for Electricity. Available online: https://ec.europa.eu/ (accessed on 17 November 2022).

- Renewable Energy Statistics. Available online: https://ec.europa.eu/eurostat/ (accessed on 17 November 2022).

- Climate for Poland—Poland for Climate: 1988-2018-2050. Available online: https://cop24.gov.pl/ (accessed on 17 November 2022).

- Progress of EU Transport Sector towards Its Environment and Climate objectives. Available online: https://www.eea.europa.eu/ (accessed on 17 November 2022).

- Tucki, K.; Orynycz, O.; Wasiak, A.; Świć, A.; Dybaś, W. Capacity market implementation in Poland: Analysis of a survey on consequences for the electricity market and for energy management. Energies 2019, 12, 839. [Google Scholar] [CrossRef]

- Eurostat: Unemployment Statistics. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Unemployment_statistics (accessed on 17 November 2022).

- Polish Automotive: 8 Percent. GDP and Continues to Grow. Available online: https://branden.biz/polski-automotive-8-proc-pkb-i-stale-rosnie/ (accessed on 17 November 2022).

- Will Electromobility Speed Up Poland’s Economic Development? Available online: https://pspa.com.pl/2022/raport/czy-elektromobilnosc-przyspieszy-rozwoj-gospodarczy-polski/?lang=en (accessed on 7 December 2022).

- Employment Trends in the EU Automotive Sector. Available online: https://www.acea.auto/figure/employment-trends-in-eu-automotive-sector/ (accessed on 17 November 2022).

- Romania, the Fourth Place in Europe in the Number of Employees in the Automotive Industry. Available online: https://www.romanianbusinessjournal.ro/romania-the-fourth-place-in-europe-in-the-number-of-employees-in-the-automotive-industry/ (accessed on 7 December 2022).

- ACEA Automobile Industry Pocket Guide 2021–2022. Available online: https://www.acea.auto/files/ACEA_Pocket_Guide_2021-2022.pdf (accessed on 7 December 2022).

- Poland is the Largest Exporter of Car Batteries in the EU. Available online: https://www.obserwatorfinansowy.pl/bez-kategorii/rotator/polska-najwiekszym-eksporterem-baterii-samochodowych-w-ue/ (accessed on 17 November 2022).

- Poland in Fifth Place in the Production of li-ion Batteries. Available online: https://poland.postsen.com/local/140987/Poland-in-fifth-place-in-the-production-of-li-ion-batteries.html (accessed on 7 December 2022).

- BloombergNEF: China Dominates Global Battery Supply Chain Again with Followers in Flux. Available online: https://www.energy-storage.news/bloombergnef-china-dominates-global-battery-supply-chain-again-with-followers-in-flux/ (accessed on 7 December 2022).

- Compendium of Electromobility. Available online: https://pfr.pl/dam/jcr:4ea38a9b-4781-42de-8a57-76e2ba4a424e/PFR_baterie_202207.pdf (accessed on 7 December 2022).

- Observatory for the Alternative Fuels Market. Poland is European Market Leader in the Production of Electric Buses. Available online: https://orpa.pl/polska-europejskim-liderem-produkcji-elektrycznych-autobusow/ (accessed on 7 December 2022).

- Interactive Map—Automobile Assembly and Production Plants in Europe. Available online: https://www.acea.auto/figure/interactive-map-automobile-assembly-and-production-plants-in-europe/ (accessed on 17 November 2022).

- E-car and Component Map of Europe. Available online: https://europe.autonews.com/e-car-and-component-map-europe (accessed on 17 November 2022).

- 2023 Outlook: US will Grow to be Next Battery Battlefield. Available online: https://www.digitimes.com/news/a20221130VL208/2023-ev-battery.html&chid=10 (accessed on 7 December 2022).

- CATL Holds 34.8% of Global Power Battery Market Share in H1. Available online: https://cnevpost.com/2022/08/02/catl-holds-34-8-of-global-power-battery-market-share-in-h1/ (accessed on 7 December 2022).

- CATL with a Market Share of 34.8%. Available online: https://napradzie.pl/2022/08/08/catl-z-348-udzialem-w-rynku-akumulatorow/ (accessed on 7 December 2022).

- ACEA. Passenger Car Registrations: −13.7% Five Months into 2022; −11.2% in May. Available online: https://www.acea.auto/pc-registrations/passenger-car-registrations-13-7-five-months-into-2022-11-2-in-may/ (accessed on 17 November 2022).

- BMW Group. At the Forefront of Electromobility: BMW Group Doubles Global Sales of Fully-Electric Vehicles in First Half-Year. Available online: https://www.press.bmwgroup.com/global/article/detail/T0402163EN/at-the-forefront-of-electromobility:-bmw-group-doubles-global-sales-of-fully-electric-vehicles-in-first-half-year?language=en (accessed on 17 November 2022).

- ACEA. New Passenger Car Registrations, by Market. Available online: https://www.acea.auto (accessed on 17 November 2022).

- Electromobility Map. Available online: https://mapaelektromobilnosci.pl/#pojazdy-elektryczne (accessed on 17 November 2022).

- PSPA. Meter of Electromobility: Poland Must Prepare for the Planned Ban on Registration of Internal Combustion Cars. Available online: https://pspa.com.pl/2022/informacja/licznik-elektromobilnosci-polska-musi-sie-przygotowac-na-planowany-zakaz-rejestracji-samochodow-spalinowych/?lang=en (accessed on 17 November 2022).

- IEA. lobal EV Outlook 2022. Available online: https://www.iea.org/reports/global-ev-outlook-2022 (accessed on 17 November 2022).

- Statista. Number of Electric Vehicle Charging Stations (AC+DC) in Poland from 2019 to 2022. Available online: https://www.statista.com/statistics/1301653/poland-charging-stations-for-electric-cars/ (accessed on 17 November 2022).

- Parchomenko, A.; Nelen, D.; Gillabel, J.; Vrancken, K.C.; Rechberger, H. Resource effectiveness of the European automotive sector—A statistical entropy analysis over time. Resour. Conserv. Recycl. 2021, 169, 105558. [Google Scholar] [CrossRef]

- Rezaei, H.; Abdollahi, S.E.; Abdollahi, S.; Filizadeh, S. Energy management strategies of battery-ultracapacitor hybrid storage systems for electric vehicles: Review, challenges, and future trends. J. Energy Storage 2022, 53, 105045. [Google Scholar] [CrossRef]

- Wang, Y.; Biswas, A.; Rodriguez, R.; Keshavarz-Motamed, Z.; Emadi, A. Hybrid electric vehicle specific engines: State-of-the-art review. Energy Rep. 2022, 8, 832–851. [Google Scholar] [CrossRef]

- Kandidayeni, M.; Trovão, J.P.; Soleymani, M.; Boulon, L. Towards health-aware energy management strategies in fuel cell hybrid electric vehicles: A review. Int. J. Hydrog. Energy 2022, 47, 10021–10043. [Google Scholar] [CrossRef]

- Fernández, R.A. Stochastic analysis of future scenarios for battery electric vehicle deployment and the upgrade of the electricity generation system in Spain. J. Clean. Prod. 2021, 316, 128101. [Google Scholar] [CrossRef]

- Lieutenant, K.; Borissova, A.V.; Mustafa, M.; McCarthy, N.; Iordache, I. Comparison of “Zero Emission” Vehicles with Petrol and Hybrid Cars in Terms of Total CO2 Release—A Case Study for Romania, Poland, Norway and Germany. Energies 2022, 15, 7988. [Google Scholar] [CrossRef]

- Vodovozov, V.; Aksjonov, A.; Petlenkov, E.; Raud, Z. Neural Network-Based Model Reference Control of Braking Electric Vehicles. Energies 2021, 14, 2373. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Manufacturer | ||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Country | BMW | BorgWarner | Bosch | Contemporary Amperex Technology (CATL) | Daimler-ACCUMOTIVE | Daimler | Ferrari | Fiat Chrysler | Ford of Europe | Hyundai-Kia | Jaguar Land Rover (Tata) | LG Chem | Magna Powertrain | Magna Steyr | Northvolt | PSA/Peugeot Citroen | Renault-Nissan-AvtoVAZ | Samsung SDI | SK Innovation | StreetScooter | Thunder Power | Toyota | VDL (Formerly Mitsubishi/NedCar) | VW Group | ZF Friedrichshafen | Zhejiang Geely (Volvo/London Electric Vehicle Company) |

| Austria | x | x | ||||||||||||||||||||||||

| Belgium | x | x | x | |||||||||||||||||||||||

| Czech Republic | x | |||||||||||||||||||||||||

| France | x | x | x | |||||||||||||||||||||||

| Germany | x | x | x | x | x | x | x | x | x | x | x | x | ||||||||||||||

| Hungary | x | x | x | |||||||||||||||||||||||

| Italy | x | x | ||||||||||||||||||||||||

| The Netherlands | x | x | ||||||||||||||||||||||||

| Poland | x | x | x | |||||||||||||||||||||||

| Romania | x | |||||||||||||||||||||||||

| Serbia | x | x | ||||||||||||||||||||||||

| Slovakia | x | x | x | x | ||||||||||||||||||||||

| Spain | x | x | x | |||||||||||||||||||||||

| Sweden | x | x | x | x | ||||||||||||||||||||||

| Turkey | x | x | x | |||||||||||||||||||||||

| UK | x | x | x | x | x | x | ||||||||||||||||||||

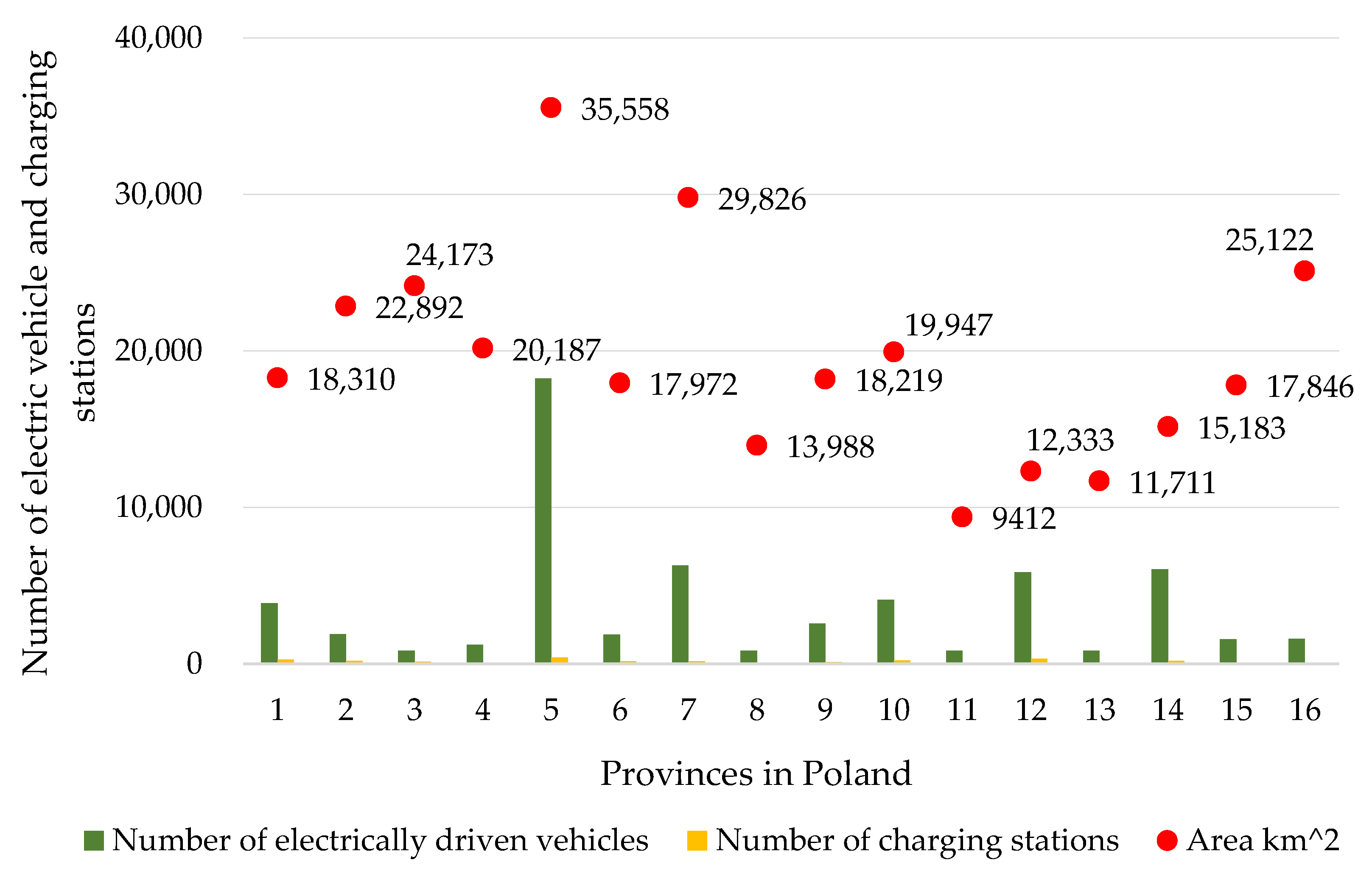

| Province | Area km2 | Number of Electrically Driven Vehicles | Number of Charging Stations | ||||

|---|---|---|---|---|---|---|---|

| Sum | BEV | PHEV | Sum | AC | DC | ||

| Pomorskie | 18,310 | 3885 | 1874 | 2011 | 263 | 198 | 65 |

| Zachodniopomorskie | 22,892 | 1893 | 845 | 1048 | 190 | 164 | 26 |

| Warmińsko-mazurskie | 24,173 | 836 | 381 | 455 | 139 | 126 | 13 |

| Podlaskie | 20,187 | 1214 | 632 | 582 | 52 | 32 | 20 |

| Mazowieckie | 35,558 | 18,237 | 9139 | 9098 | 413 | 326 | 87 |

| Kujawsko-pomorskie | 17,972 | 1883 | 805 | 1078 | 153 | 106 | 47 |

| Wielkopolskie | 29,826 | 6280 | 3186 | 3094 | 158 | 95 | 63 |

| Lubuskie | 13,988 | 848 | 423 | 425 | 51 | 27 | 24 |

| Łódzkie | 18,219 | 2581 | 1290 | 1291 | 109 | 44 | 65 |

| Dolnośląskie | 19,947 | 4089 | 1996 | 2093 | 224 | 164 | 60 |

| Opolskie | 9412 | 827 | 420 | 407 | 59 | 41 | 18 |

| Śląskie | 12,333 | 5856 | 2834 | 3022 | 323 | 233 | 90 |

| Świętokrzyskie | 11,711 | 846 | 488 | 358 | 31 | 24 | 7 |

| Małopolskie | 15,183 | 6032 | 3464 | 2568 | 197 | 126 | 71 |

| Podkarpackie | 17,846 | 1577 | 755 | 822 | 61 | 32 | 29 |

| Lubelskie | 25,122 | 1590 | 823 | 767 | 37 | 21 | 16 |

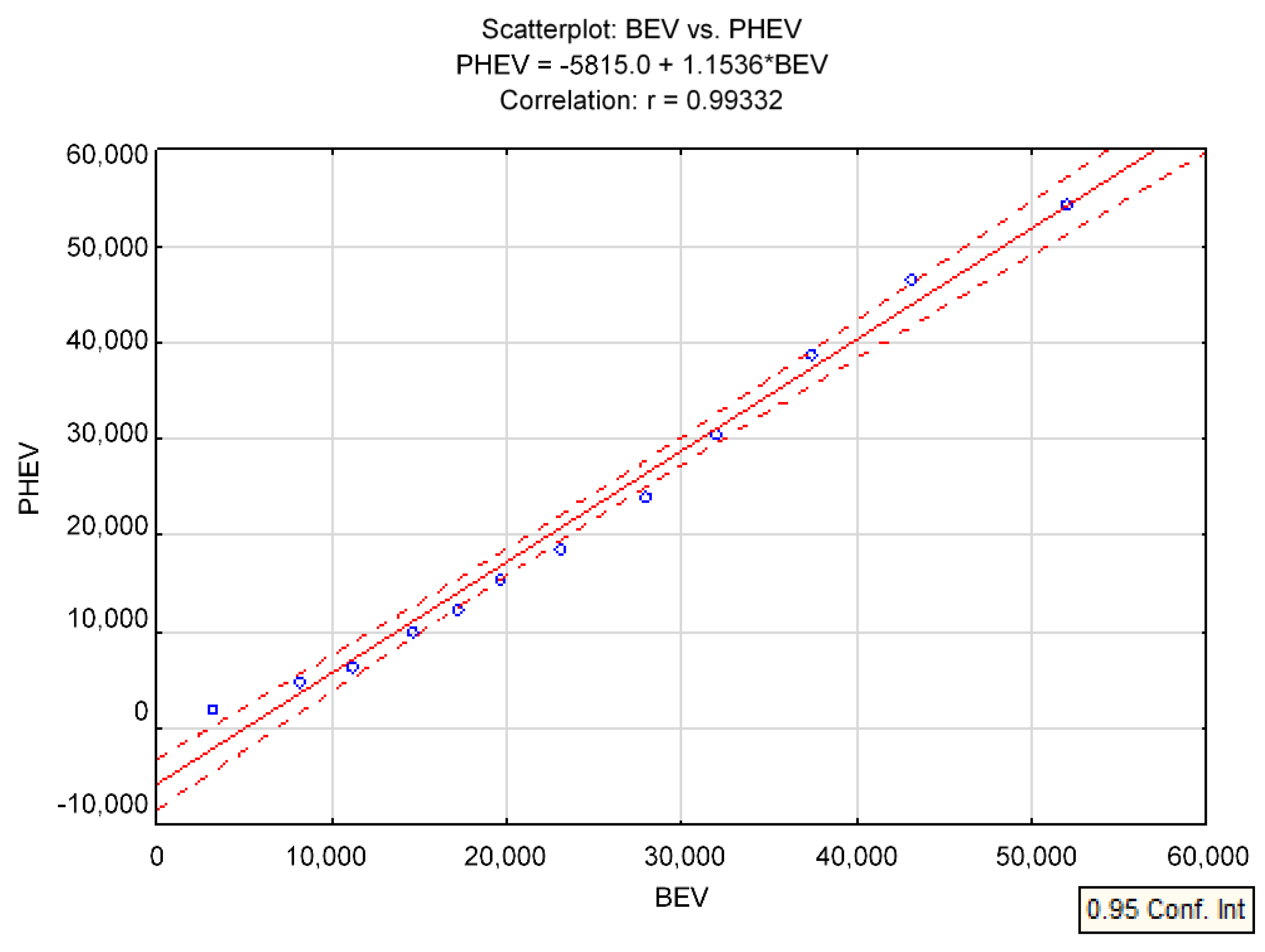

| Variable | Mean | Standard Deviation | Traditional Vehicles | PHEV | BEV |

|---|---|---|---|---|---|

| Traditional vehicles | 119,216 | 20,896.59 | 1 | −0.430761 | −0.455769 |

| PHEV | 22,004.2 | 17,184.83 | −0.430761 | 1 | 0.99332 |

| BEV | 24,115.6 | 14,797.29 | −0.455769 | 0.99332 | 1 |

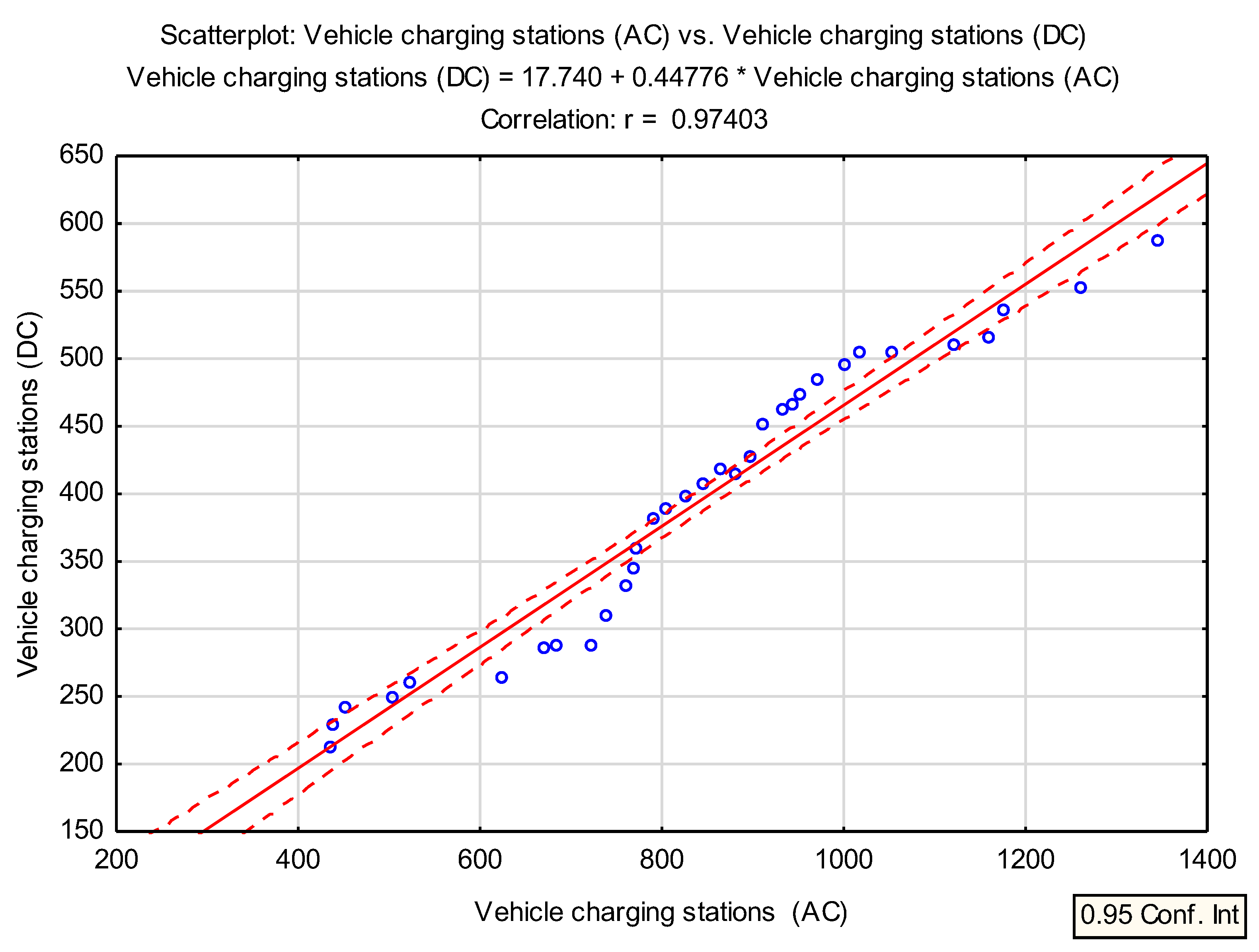

| Variable | Y-Vehicle Charging Stations—DC |

|---|---|

| X-Vehicle charging stations—AC | 0.974 |

| p = 0.00 |

| Variable | Mean | Std. Dev. | r (X, Y) | r2 | t | p | N | Constant Dep: Y | Slope Dep: Y | Constant Dep: X | Slope Dep: Y |

|---|---|---|---|---|---|---|---|---|---|---|---|

| X | 843.6970 | 231.8115 | |||||||||

| Y | 395.5152 | 106.5634 | 0.974033 | 0.948739 | 23.95313 | 0.0000 | 33 | 17.74039 | 0.447761 | 5.659202 | 2.118851 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tucki, K.; Orynycz, O.; Dudziak, A. The Impact of the Available Infrastructure on the Electric Vehicle Market in Poland and in EU Countries. Int. J. Environ. Res. Public Health 2022, 19, 16783. https://doi.org/10.3390/ijerph192416783

Tucki K, Orynycz O, Dudziak A. The Impact of the Available Infrastructure on the Electric Vehicle Market in Poland and in EU Countries. International Journal of Environmental Research and Public Health. 2022; 19(24):16783. https://doi.org/10.3390/ijerph192416783

Chicago/Turabian StyleTucki, Karol, Olga Orynycz, and Agnieszka Dudziak. 2022. "The Impact of the Available Infrastructure on the Electric Vehicle Market in Poland and in EU Countries" International Journal of Environmental Research and Public Health 19, no. 24: 16783. https://doi.org/10.3390/ijerph192416783

APA StyleTucki, K., Orynycz, O., & Dudziak, A. (2022). The Impact of the Available Infrastructure on the Electric Vehicle Market in Poland and in EU Countries. International Journal of Environmental Research and Public Health, 19(24), 16783. https://doi.org/10.3390/ijerph192416783