Abstract

Although the increasing adoption of digital finance in recent years has exerted a wide-ranging influence on farmers’ consumption and production activities, many farmers in China still seriously suffer from digital financial exclusion. Few studies have documented the different impacts of e-commerce adoption characterized by online purchases and sales on farmers’ participation in the digital financial market measured by their engagement in digital payments, digital wealth management, and digital credit in rural China. Using survey data from 832 entrepreneurial households in rural China, we contribute to the literature by confirming that both online purchases and sales have a robust significant and positive impact on farmers’ participation in the digital financial market and that this impact on digital wealth management is successively larger than that on digital payments and digital credit, with the propensity score matching (PSM) method and instrument variable (IV) approach employed. We further discover that the impact of online purchases and sales on farmers’ participation in the digital financial market is significantly mediated by digital financial literacy. Moreover, the impact of online purchases and sales on farmers’ participation in the digital financial market is larger for those with high education levels, pursuing skills training, running new agricultural operation entities (i.e., family farms, professional cooperatives), and engaging in agricultural entrepreneurship. Our findings suggest that more effective measures to enhance adoption rates of online purchases and sales, innovation in rural market-oriented digital financial products and services, systematic training for farmers in e-commerce skills as well as digital financial literacy, and differentiated support measures for different groups of farmers to reduce the gap are urgently needed in China.

1. Introduction

With the emergence and rapid development of digital technology, a fundamental change has occurred around the world in the financial services industry, especially in terms of the manner in which people engage in the financial market. Digital finance, stemming from the effective integration of digital technology and finance, has gone through impressive development since 2013 in China [1]. The accelerating development of digital finance has gradually exerted a wide-ranging influence on people’s consumption and production activities in China [2]; this influence on rural residents in developing countries under a transition economy has recently aroused increasing concern among scholars as well as policy-makers [3]. In this context, the Chinese central government has given great policy priority to bolster digital finance in rural areas [2]. In spite of the increasing adoption rate of digital finance in recent years, many farmers in China still seriously suffer from digital financial exclusion [4], especially in terms of adopting the products and services of digital wealth management and digital credit [5,6]. Widespread exclusion from digital finance, which intensifies the Matthew effect of the rural financial market, has become a considerable barrier against the expansion of inclusive finance in rural areas in the digital economy era [7].

Little attention has yet been paid to the differences in the adoption of multiple digital financial products among rural residents brought by e-commerce adoption. Consumers’ demographic and socio-economic characteristics, and the regional financial environment, have been the primary focal points of previous research associated with their exclusion from individual digital financial products or services [8,9,10]. These discussions above have been mainly restricted to the traditional offline transaction scenes in the masses’ daily production and life. Indeed, for rural residents, the changes arising from using digital payments, digital wealth management, and digital credit have been increasingly prominent in the era of e-commerce [3], but the impact of e-commerce adoption on farmers’ usage of multiple digital financial products has been rarely discussed in existing studies.

Nowadays, the boom of e-commerce is widespread in rural areas in China, and a range of revenues brought about by e-commerce adoption has triggered much attention from scholars [11,12,13]. It is obvious that innovations in digital finance, like online payment technology, provide indispensable support for the effective functioning of e-commerce [4,14]. It also can be seen that the diffusion of e-commerce inevitably involves many financial issues with regard to payment transactions, credit accessibility, and capital management [15]. However, few studies have explored whether the e-commerce adoption for both online product sellers and purchasers can effectively relieve their exclusion from and increase their participation in the digital financial market, particularly in regard to digital wealth management and digital credit. Quantifying the causal relationship between farmers’ adoption of e-commerce and digital finance empirically faces challenges caused by omitted unobservable variables, sample self-selection, and reverse causality with cross-section data used. Therefore, with the propensity score matching (PSM) method and instrument variable (IV) approach employed to identify the causality and address endogeneity bias, we investigate whether e-commerce adoption by farmers drives their usage of multiple digital financial products. How does such an impact takes place, and which groups of farmers divided by their characteristics (e.g., education levels, skills training experience, occupation type) are most affected?

A comprehensive and adequate assessment of the impact of e-commerce adoption on farmers’ engaging in the digital financial market would not be accomplished without distinguishing the difference between online purchases and online sales [16]. Previous studies have primarily observed the effects of consumers’ online purchases, which include a lower degree of information asymmetry, less time and labor costs for transactions, and more economic benefits for the purchasers [17,18]. Meanwhile, some studies have highlighted the influence of producers’ online sales, which involve wider sales channels, a greater sales volume, and more sales flexibility for the sellers [19]. In view of the distinct differences between online purchases and online sales in essence [20], the difference between their impacts on the use of multiple digital financial products or services cannot be ignored. Additionally, due to the fact that purchasing the means of production and selling products are the two most critical and common economic activities infiltrating farmers’ entrepreneurship, it, therefore, makes more sense to concentrate on the relationship between entrepreneurial farmers’ e-commerce adoption and their usage of multiple digital financial products [21]. A farmer was defined as an entrepreneur if he or she established and was engaged in one of these activities: small handicraft operations, enterprise operations, farm operations, cooperative management, business services, etc.

Indeed, the use of digital financial products and services might be directly or indirectly related to transactions on e-commerce platforms. Digital payment services, such as WeChat, Alipay, and Bestpay, have become the main tools for farmers’ online transactions and consumption [3]. Moreover, digital wealth management resources, like Yu’e Bao, and apps about insurance, securities, and funds are effective management tools that benefit farmers’ capital reserves, liquidity management, and property appreciation [2]. Digital peer to peer (P2P) lending providers, for instance, Jing Dong Dai and Wang Nong Dai, and consumer loan products, like Ant Huabei and Jingdong Baitia, are becoming increasingly popular in China, as they provide important capital for farmers’ production and operations [22]. Jing Dong Dai and Jingdong Baitiao are provided by Jingdong Finance; Wang Nong Dai and Ant Huabei are provided by Alipay. Studies have suggested that conducting transactions online can facilitate the accumulation of internet knowledge and financial literacy for purchasers [23], which benefits for individuals’ financial market participation [21,24]. Therefore, we assume that digital financial literacy, reflecting a comprehensive level of consciousness, knowledge and ability related to digital finance in individuals’ human capital, would be a potential pathway through which e-commerce adoption stimulate farmers’ usage of digital financial products.

Our study aimed to ascertain the impact of e-commerce adoption on rural residents’ participation in the digital financial market and explore possible pathways for enhancing the inclusion of digital finance, which would provide useful suggestions for other developing countries. In general, our study contributed to the existing research in the following ways. First, rather than discussing general internet users and individual supplier and demander sides of online products, we concentrated on rural entrepreneurial farmers and emphasized both sellers’ and purchasers’ adoption of e-commerce and participation in the digital financial market. We elucidated the general and differential influence mechanism of e-commerce adoption characterized by online purchases and sales on farmers’ usage of multiple digital financial products. Second, taking potential endogeneity problems caused by sample self-selection bias, omitted unobservable variables, and reverse causality into consideration, we employed both the PSM method and IV approach to empirically dissect the different impacts of e-commerce adoption on farmers’ usage of digital payments, digital wealth management, and digital credit. Third, we shed light on the mediation effects of digital financial literacy on the relationship between online purchases as well as online sales on farmers’ usage of different digital financial products and services using mediation model. The heterogeneous effects across individual and family characteristics of farmers were taken into account.

The rest of this paper is organized as follows: Section 2 presents a review of previous literature on the topic as well as the hypotheses to be tested. Section 3 introduces the empirical strategies employed in the research. Section 4 describes the data and main variables considered. Section 5 presents and discusses the empirical results and is followed by the conclusions and implications in Section 6.

2. Literature Review and Hypothesis

2.1. Development of the Definition of Digital Finance

European and North American countries adopted the concepts of e-banking and e-finance early [15,25], which laid the foundations for Chinese scholars to put forward the concept of digital finance (internet finance). Few scholars and policy-makers have clearly distinguished between the concepts of digital finance and internet finance. Although no consensus has been reached on the definition of digital finance, scholars’ opinions on its core elements and basic attributes have become increasingly clear in China. For instance, research by Xie and Zou conceptualized internet finance as a third kind of financing pattern different from the other two kinds—indirect financing from commercial banks and direct financing from the capital market [26]. Wu further regarded internet finance as a new financial pattern built on the basis of internet thinking, internet platforms, and cloud data integration [27]. This formed a mainstream definition that was recognized by most scholars in China. The Institute of Digital Finance at Peking University championed the concept of digital finance and constructed an inclusive digital finance index, in which payments, loans, insurance, investments, and credit are conceptually taken into account. The Digital Inclusive Financial Index (2011–2018) was compiled by a research group at the Institute of Digital Finance at Peking University, https://jszx6.pku.edu.cn../../docs/2019-07/20190724210323477869.pdf, accessed on 20 April 2021.

Following existing studies, we define farmers’ participation in the digital financial market as the utilization of digital financial products and services (such as online payments, online credit, and online wealth management) in their daily lives, production, and operation activities. It is worth noting that digital finance has not changed the nature of the financial industry, and there are four main functions of consumer finance: payment, risk management, savings or investment, and credit [28]. Hence, we focus on three of these aspects for farmers participating in the digital financial market (digital payment, digital wealth management, and digital credit) in the context of rural China.

2.2. Nexus between Online Purchases and Participation in the Digital Financial Market

In recent years, consumers in China have shown an increasing interest in purchasing products through e-commerce platforms. The differences between online purchases and offline situations in terms of perceived search costs, price sensitivity, and response flexibility are the main reasons why consumers demonstrate higher purchase motivation in virtual markets [17,29].

The related existing studies have revealed that using the internet for buying activities had a positive effect on purchasers’ acceptance of internet banking services [8], which is just one form of digital payment service in China. A certain amount of liquid capital by producers is needed for online purchases, due to the fact that purchases of raw materials, production, and sales often taken place at different times [30]. The urgent demands for funds can directly prompt farmers to apply for quick loans through P2P platforms or use internet consumer loans for installment consumption [22]. Likewise, a long-term investment reserve fund by producers is essential for bulk purchases [30], thereby stimulating farmers’ demands for flexible and diverse digital wealth management products. In addition, the herding effect of social networks arising from online transactions would effectively help motivate farmers’ participation in the digital financial market [31]. As mentioned above, online purchases has been found to be positively related to individuals’ financial literacy [23], which would affect their management of personal finance [24,32], credit demand, and accessibility [21]. Therefore, the following hypotheses are proposed here:

Hypothesis 1:

Online purchases can increase farmers’ participation in the digital financial market measured by their participation in digital payments, digital wealth management, and digital credit.

Hypothesis 2:

Online purchases can affect farmers’ participation in the digital financial market through their digital financial literacy.

2.3. Nexus between Online Sales and Participation in the Digital Financial Market

Nowadays, there are mainly two kinds of online sales in China, friend circle sales and website sales. Friend circle sales aim at acquaintance and derivative networks based on WeChat, QQ, Weibo, and other social platforms (e.g., Tiktok, Kwai), while website sales rely on Tmall, Jingdong, Taobao, and other professional e-commerce websites. In China, WeChat is a mobile instant messenger application based on social relationships and was launched in 2010 by the Tencent Company. QQ is the largest and most used online service portal in China and was founded in November 1998 by the Tencent Company. Weibo is a Chinese microblogging website, which was launched by Sina Corporation in August 2009. Tiktok and Kwai are popular short video entertainment platforms. Friend circle sales integrate words, pictures, and videos into a marketing platform and carry out mass information transmission based on acquaintance networks and their derivatives to maximize the sale of products [33,34]. Additionally, the establishment of shopping guide websites helps to fully display the products sales information and gather target consumers [35], which can continuously increase e-marketing flexibility and effectiveness [36].

Previous studies have preliminary confirmed that using the internet for selling activities has had a positive effect on sellers’ acceptance of internet banking services [8], which is just one kind of digital payment service in China. It has been suggested that sellers’ engaging constantly in online sales activities increases their operating income and profit [19], which would enhance individuals’ adoption of online wealth management products and services [10]. Moreover, a certain amount of working capital for operators is needed for an increase in online sales scale [37], especially in the sales of seasonal agricultural products. For e-commerce households, access to credit would relieve their liquidity constraints, ensure orderly operations, and accelerate agricultural transformation [6,38]. In addition, it has been argued that financial literacy is positively related to individuals’ adoption of financial management and demand for credits [21,24,39]. The increase in online sales would effectively promote the precipitation and accumulation of internet knowledge, financial literacy, and improve online social relationships for the sellers [33]. This would be helpful for further reinforcing individuals’ trust in digital finance and inspiring their enthusiasm for accepting digital financial products or services [31]. Therefore, the following hypotheses are proposed in this study:

Hypothesis 3:

Online sales can enhance farmers’ participation in the digital financial market measured by their participation in digital payments, digital wealth management, and digital credit.

Hypothesis 4:

Online sales can influence farmers’ participation in the digital financial market through their digital financial literacy.

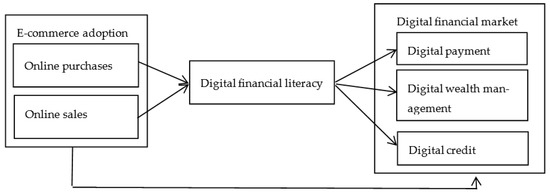

Based on the above literature review and hypothesis, the conceptual framework is schematically depicted in Figure 1.

Figure 1.

The conceptual framework.

3. Model Specification

3.1. Modelling the Adoption Decision of E-Commerce

According to the random utility decision model proposed by Becerril and Abdulai, individuals’ decision about whether to adopt internet technology depends on the utility the individual expects to derive from this adoption [40]. Farmer adoption occurs when the expected utility of using internet technology () is greater than the utility without using internet technology (), i.e., − > 0. The difference between the utility with and without e-commerce adoption may be denoted as a latent variable , so that indicates that the utility with e-commerce adoption exceeds the utility without adoption. Therefore, is not observable but can be expressed as a function of the observed characteristics and attributes, denoted as in a latent variable model, as follows:

In Equations (1) and (2), is a binary indicator variable that equals 1 if a farmer adopts online purchases () or sales () and is otherwise zero. is a vector of an all exogenous explanatory variable, including individual characteristics, household characteristics, and village characteristics. is a random disturbance item assumed to be normally distributed.

3.2. Modelling the Impacts of E-Commerce Adoption on Engaging in Digital Financial Market

According to the theory of behavioral finance, an individual’s participation decision in the financial market arises from their pursuing the maximum expected utility based on bounded rationality [28,41]. It is believed that farmers’ adoption of new technology, like e-commerce, would exert direct or indirect impacts on the measurement and comparison of the costs, benefits, and risks of participating in the traditional and new-type financial market.

To measure the impact of online purchases and sales on farmers’ participation in the digital financial market, we construct the baseline model as follows:

In Equation (3), is a dummy variable that equals 1 if the farmer participated in the digital financial market; respectively denotes farmers’ participation in digital payments, digital wealth management, and digital credit. is the control variable vector that affects the participation decisions of the farmer in the digital financial market, as shown in Table 1. represents the adoption of online purchases () or online sales () of the farmer . is a random disturbance item. The adoption of online purchases or sales could be endogenous variables in Equation (3), mainly due to omitted unobservable variables, reverse causality, and sample self-selection problems [42].

Table 1.

Definition and summary of variables.

3.3. PSM Method

Considering that whether farmers choose to adopt internet technology depends on their own internal and external conditions, their decisions about the e-commerce adoption () may be affected by certain unobservable factors, which are also related to the outcome variable (), resulting in a correlation between and . Therefore, there may be estimation bias due to sample self-selection problems if a binary probit or logit model is employed for the estimation of Equation (3). Given that there are no strict requirements for function form assumptions, parameter constraints, an error term distribution, or exogenous explanatory variables in the PSM method, this method has an obvious strength in dealing with sample self-selection [43]. Due to the limitation that PSM estimation cannot take the influence arising from unobservable factors into consideration, the Rosenbaum bound sensitivity analysis is employed to test the robustness of the estimation results.

According to the counterfactual analysis framework proposed by Rosenbaum and Rubin [44], we define the average treatment effect on the treated group (ATT) as follows:

In Equation (4), denotes the participation decision of the farmer in the digital financial market when farmers adopted online purchases (online sales), and denotes the participation decision of the farmer in the digital financial market when farmers did not adopt online purchases (online sales). measured the net impact of online purchases (online sales) on farmers’ participation in the digital financial market, that is, the difference between the probability of their participating in the digital financial market under the condition of adopting versus non-adopting online purchases (online sales). Additionally, is the actual result that can be directly observed, while is the counterfactual result that cannot be directly observed but can be constructed by the propensity score matching method. Following the research of Rosenbaum and Rubin, there are different matching algorithms in the PSM, and the trade-offs—in terms of bias and efficiency—of various methods are inconsistent [44,45]. If the estimation results of different matching methods are similar, this indicates that they are robust.

3.4. Instrument Variable Estimation

In order to address the potential endogeneity of online purchases and sales caused by omitted unobservable variables and reverse causality, we used the sample’s participation proportion in online purchases or sales from the same town (excluding the respondent) as a possible valid instrumental variable (IV). For the IV to be valid, it had to correlate with the endogenous variable and not affect the dependent variable through other mechanisms [42]. Farmers’ participation proportion in online purchases or sales from the same town (excluding the respondent) are undeniably related to the respondents’ behavior about online purchases or sales, with highly similarity in their social and economic characteristics. Regarding the exogeneity restriction, the respondents’ decisions about the usage of digital finance might not be affected by the participation proportion in online purchases or sales of others from the same town; therefore, the two requirements, correlation and exogeneity, for a valid instrument were likely to be satisfied. To check the endogeneity of online purchases or sales, Durbin–Wu–Hausman (DWH) tests were conducted by introducing an IV.

3.5. Mediation Model

According to the hierarchical regression model proposed by Baron and Kenny [46], we assigned the regression models of e-commerce adoption to usage of digital finance (see Equation (3)), e-commerce adoption to the digital financial literacy, and e-commerce adoption and the digital financial literacy to farmers’ usage of digital finance. The last two equations were expressed as follows:

where indicates the participation decisions in the digital financial market; is the digital financial literacy of the respondent . represents the adoption of online purchases () or sales () of the farmer . and are the parameters to be estimated. and are the random disturbance terms.

The mediation effect test procedures included the following steps: (1) test the significance of in Equation (3); if is significant, continue to test, otherwise stop the test. (2) test the significance of in Equation (5) and in Equation (6); if at least one is not significant, the Sobel test (step (4)) is needed to conduct further assessment. If and are significant, conduct step (3): test whether in Equation (6) is significant; if it is not significant, it means that is a complete intermediary variable, but if it is significant, and < , is a partial intermediary variable. (4) If the statistic of Sobel test is significant, there exists a mediation effect [46]. The Stata 15.0 software and the procedure sgmediation.ado were used for the Sobel test in the mediation effect test, with which the updated estimation command can be obtained. In general, the Sobel test has a better test effect than stepwise regression, but it also has the limitation of requiring the sampling distribution to be normal. In the future studies, we will use the bootstrap method with a better testing effect to obtain more convincing results.

4. Data and Variables

4.1. Data Source and Descriptive Statistics

Our data were based on a questionnaire survey conducted through face-to-face interviews in 2018 in rural China. Multi-stage cluster sampling procedures were performed. First, three provinces in the eastern and western parts of China were selected by taking the development of e-commerce and digital inclusive finance into consideration. Second, nine counties or districts in the selected provinces were selected by considering their development of e-commerce, geographical environment, and economic status. We selected three representative counties (Fuping, Pingluo, and Qingzhou) with higher levels of e-commerce activities, three representative counties (Nanzheng, Tongxin, and Shen) with average levels, and three counties (Gaoling, Shapotou, and Yinan) with poor levels. Fuping, Nanzheng, and Gaoling are located in Shaanxi; Shapotou, Tongxin, and Pingluo are located in Ningxia; and Shen, Qingzhou, and Yinan are located in Shandong. Third, three or four representative towns reflecting different economic levels were extracted from each selected county or district. From these, two or three representative villages were selected based on the same principle. Fourth, 15 to 20 rural households (mainly the decision-makers in economic activities) were selected from each selected village to interview. Prior to conducting the survey, we scouted various regions and tried to consult local town and village leaders, the staff of financial institutions, and the farmers.

Our research group selected 2000 farmers for interview. However, a small number of farmers directly refused to answer our questions or just finished part of the questions, resulting in many vacancies in the questionnaire items. After excluding the above observations with much missing data or outliers, we obtained 1947 valid questionnaires coming from 105 villages in 36 towns, nine counties (or districts), and three provinces. The representativeness of our sample is described as follows: firstly, according to the Report of Peking University Digital Inclusive Finance Index (2011~2018), Shandong, Shaanxi and Ningxia provinces were the representative provinces with high, average, and low development level of digital inclusive finance in China, respectively. In addition, the 42nd Statistical Report on the Development of China’s Internet showed that, as of June 2018, the proportion of using digital payment for Chinese Internet users increased to 78%, while the utilization rate of digital wealth management increased to 21%. The 42nd Statistical Report on the Development of China’s Internet can be accessed at http://www.cac.gov.cn/2018-08/20/c_1123296882.htm, accessed on 20 April 2021. The proportions of using digital payment and digital wealth management in our sample were 75% and 23%, respectively, which were in line with the results of the above report. Secondly, Shaanxi and Ningxia were the representative provinces of the growth-oriented e-commerce development mode (relatively fast growth rate but low level), while Shandong was the representative province of the relatively mature e-commerce development mode (relatively high level but slow growth rate) (The 2018 Report of China’s E-commerce Development Index can be accessed at http://www.lifangwang.net/detail.php?aid=145, accessed on 20 April 2021). Thirdly, our sample set covers agricultural ecosystems varying with different geographic environments, such as the Guanzhong Plain, Mountainous Area of Southern Shaanxi, Loess Plateau, and North China Plain, which means the use of e-commerce and digital finance by farmers and entrepreneurial activities of farmers may present regional differences. Based on the aforementioned reasons, our sample can fairly reflect good representativeness at the national level. As mentioned previously, considering that production and sale activities are the two most critical and common economic activities for farmers’ entrepreneurship [21], we focus on the online purchases and sales of entrepreneurial farmers rather than general farmers. We divided the sample into entrepreneurial farmers and non-entrepreneurial farmers. Agricultural and non-agricultural entrepreneurship were included in farmers’ entrepreneurial activities. Agricultural entrepreneurship refers to agro-economic activities, such as scale management or start-ups of new businesses or new organizations (e.g., family farms, professional cooperatives, and enterprises), in traditional agriculture, such as plantations, aquaculture, forestry, and fisheries. Non-agricultural entrepreneurship refers to the establishment of businesses in industrial sectors, such as processing, manufacturing, and construction, or engagement in non-agricultural economic activities in service industries, such as specialized services for agricultural production, retailing, wholesaling, accommodation, transportation, housekeeping, culture and entertainment, or medical and health services. Thus, an entrepreneurial sample of 832 was used for analysis. The samples from Shaanxi, Ningxia, and Shandong accounted for 37.92%, 36.23%, and 25.85% of the full entrepreneurial sample, respectively.

4.2. Dependent Variable

The dependent variable was farmers’ participation in the digital financial market, which was mainly measured by digital payments, digital wealth management, and digital credit. We asked every interviewee the following questions: “Have you used WeChat, Alipay, Tenpay, Bestpay, or other third-party payment software to conduct capital transactions?”; “Have you participated in P2P platforms as an investor, used Yu’e Bao, or invested insurance, securities, funds, etc. through apps?”; and “Have you participated in P2P platforms as a borrower, used small loan products (Jing Dong Dai, Wang Nong Dai, etc.) to obtain loan funds, or used consumer loan products (Ant Huabei, Jingdong Baitiao, Weipinhua, etc.) to realize consumption and pay by installment?” According to the answers to the above three questions, we successively identified farmers’ participation behaviors with respect to digital payments, digital wealth management, and digital credit.

As reported in Table 1, 75% of the respondents used digital payments, 23% used digital wealth management, and 10% used digital credit. Along with the popularity of WeChat and Alipay in rural China, digital payments are increasingly widely used by farmers. Meanwhile, due to farmers’ perceived riskiness of the digital financial market and limited knowledge reserve about digital finance [5,6], their participation rates in digital wealth management and digital credit were generally low. This is generally consistent with the statistic that only 7.60% and 11.10% households in China have access to credit and wealth management products online, respectively, in Li, Wu, and Xiao [4]. Indeed, it is reasonable that entrepreneurial farmers’ participation levels in the digital financial market would be higher than their counterparts, due to more capital transactions, wealth management, and credit demands for entrepreneurs.

4.3. Treatment Variables

The treatment variables were online purchases and online sales in entrepreneurship. To clearly identify farmers’ adoption of online purchases and online sales, we asked the respondents: “Did you use the internet for purchasing raw materials, machinery, and other means of production in your entrepreneurial activities”; “Did you use circles of friends on WeChat, QQ, and other social platforms (e.g., Weibo, Tiktok, Kwai) for selling products in your entrepreneurial activities?”; and “Did you use websites for selling products in your entrepreneurial activities?” If the answer for the first question was “yes,” the respondent was classified as an online purchaser. If at least one of the answers to the last two questions was “yes,” the respondent was classified as an online seller. As shown in Table 1, 23.47% of the sample took part in purchasing online, while 35.50% of the sample took part in selling online. As one statistic reported, the number of e-commerce users in rural China in 2019 reached 230 million, accounting for approximately 35% of the total rural population (this can be obtained from the Report of China Rural E-commerce Market, http://www.100ec.cn/zt/2019ncdsbg/ (accessed on 20 April 2021).). This implied that purchases and sales online have become an important supplement to traditional offline channels. Furthermore, through the means comparison (see Table A1 of Appendix A), we can preliminarily judge that those farmers who adopted online purchases or sales were more inclined to take part in the digital financial market.

4.4. Channel Variable

Farmers’ digital financial literacy was selected as the channel variable, which affected individuals’ perceptions of and intentions towards the products and services in the digital financial market. Previous studies have mainly used items related to interest rates, inflation, and risk diversification to measure individuals’ financial literacy [21,32,39]. With reference to the above research, we measured farmers’ digital financial literacy using six questions (as reported in Table 1), which emphasized interest rates, mortgage and guarantee requirements, credit, transaction cost, and financial security in the digital financial market. We calculated the respondents’ digital financial literacy using a scoring method based on whether answers to each item were correct (“Yes” for each item) or not, with the correct answer being given a score of 1, and other answers a 0. Using equal weights, we then obtained the digital financial literacy score for each respondent, which ranged from 0 to 6. As shown in Table 1, the average score for the digital financial literacy of respondents was 2.43, indicating a low average level of financial literacy among rural residents in China [3].

4.5. Control Variables

Based on the existing literature [8,9,10,20] and field experience, we controlled for the respondents’ individual characteristics (gender, age, education, risk propensity, internet learning ability, skill training experience, information access, time spent online per week), household characteristics (annual network fee, number of WeChat friends, financial network, new agricultural operation entities, entrepreneurship industry), village characteristics (distance to the nearest town, formal financial institution status, Taobao shops (Alibaba Group in China has cooperated with local governments to establish Taobao stores and service stations in rural areas to promote online products dissemination to the countryside as well as rural products access to the cities), and province dummies variables (Shaanxi, Ningxia). Table 1 presents the detailed definitions and descriptive statistics of the control variables.

From Table 1, it is clear that 78.22% of the respondents were male and had an average age of 44 years. Half of the respondents had only completed middle school, while 31.64% of them had attended high school or above. In terms of skill training experience, 53.23% of the respondents had taken some kind of training courses on business skills in the past. With regard to risk propensity, 15.45% of the respondents were open to risk, 56.88% were risk averse, and 27.66% were risk neutral. Of the respondents, 30.56% reported poor internet learning ability, while 53.26% believed that they could effectively learn and apply internet knowledge. Moreover, 57.34% of the farmers often obtained economic information from their friends through social platforms, such as QQ, WeChat, and Weibo. The respondents’ average time spent online was 14.53 h per week. Overall, the rural households surveyed paid an annual 727.88 RMB for network fees on average. About 68 friends, on average, were in frequent contact with each respondent on WeChat. Only 18.16% of the households had relatives or friends working at banks or credit cooperatives. Approximately 32.10% of the households were engaged in new agricultural operations, such as family farms, professional cooperatives, and agricultural enterprises. Furthermore, 39.22% of households conducted entrepreneurship in a non-agricultural industry. Regarding the village traits of each study village, the average distance from the selected villages to the nearest town was 5.06 km. The average number of formal financial institutions in each town was two. About 29.25% of the surveyed villages had Taobao shops established by individuals.

5. Empirical Results and Discussion

5.1. Determinants of the Adoption of Online Purchases and Sales

As reported in Table A2 of Appendix A, gender, education, internet learning ability, skill training experience, time spent online per week, new agricultural operation entities and entrepreneurship industry positively affected farmers’ online purchases at different significance levels, while distance to the nearest town had a negative and significant impact on their online purchases. The male participants were less skeptical about e-business, showed less web apprehensiveness, and were more satisfied with online shopping than their female counterparts [47]. Additionally, farmers with higher levels of education, greater internet learning capabilities, special training in business skills, and more time spent online would seek more freedom of products and services choice and control in their online shopping [17,48]. Additionally, farmers engaging in new agricultural operation entities (i.e., engagement in family farms, professional cooperatives) and non-agricultural entrepreneurship showed a greater demand for various new products with high technical content and low substitutability as well as fast and convenient transactions in online channels.

Moreover, gender, risk propensity, internet learning ability, skills training experience, information access, time spent online per week, annual network fee, new agricultural operation entities, entrepreneurship industry, and the existence of Taobao shops in the village positively affected farmers’ online sales. These findings are in line with the research of Chitura et al. [14] and Li et al. [49]. Moreover, farmers engaging in new agricultural operation entities involved in family farms and professional cooperatives and non-agricultural entrepreneurship were more inclined to sell products online to receive wider product promotions, a greater market share, and a higher sales profit.

5.2. Impact of E-Commerce Adoption on Usage of Digital Finance

5.2.1. The PSM Estimation Results

To ensure a good matching quality, we conducted both a balanced hypothesis test and a common support hypothesis test. As shown in Figure A1 of Appendix A, the common support interval of propensity scores for the online purchase adopters and non-adopters was from 0.0038 to 0.8263, while that for the online sales participants and non-participants was from 0.0528 to 0.8062. After matching with online purchases and online sales as treatment variables, pseudo-R2 decreased significantly from 0.159 and 0.177 to 0.004–0.025 and 0.003–0.031, respectively, and LR values decreased significantly from 143.30 and 191.17 to 2.14–13.68 and 2.26–15.30, respectively. The joint significance test of explanatory variables changed from the 1% significance level before matching to the 10% level without significance; the mean biases of explanatory variables decreased from 30.4% and 31.1% to within 15%, and the total bias reduced significantly. All the above results indicated that the sample matching effectively balanced the differences of explanatory variable distribution between the treatment group and the control group and minimized the problem of sample selection bias [44].

As shown in Table 2, both online purchases and online sales had a positive and significant impact on digital payments, digital wealth management, and digital credit for farmers. This finding is in line with Hojjati and Rabi [8] in that selling and buying online positively affects the adoption of internet banking, which can be extend to farmers’ utilization decisions about digital wealth management and digital credit. Specifically, farmers’ online purchases increased the likelihood of participating in digital payments, digital wealth management, and digital credit by an average of 7.16%, 8.97%, and 6.67%, respectively. Likewise, farmers’ online sales increased the probability of participating in digital payments, digital wealth management, and digital credit by an average of 9.28%, 10.59%, and 5.30%, respectively. Remarkably, we found that the impact of online purchases and sales on digital wealth management was larger than that on digital payments and digital credit. Moreover, the impact of farmers’ online sales on digital payments and digital wealth management was larger than that of online purchases; on the contrary, the impact of farmers’ online sales on their digital credit was smaller than that of online purchases.

Table 2.

PSM estimation of the impact of e-commerce adoption on usage of digital finance.

A possible explanation for this finding may be that wealth management behavior stems from the traditional saving culture in China. In fact, the precautionary saving rate of Chinese households has been one of the highest in recent decades around the world, with an imperfect social security system [50]. The main means of online wealth management for farmers discussed in this article was Yu’e Bao, which is an effective tool for cash management with value-added services. This financial product has been popular in China since it was launched in 2013 due to its advantages such as simple and clear process, low threshold, zero poundage, and flexible use [3,10]. The transaction and capital flow of online sales occur more frequently than that of online purchases, which causes farmers’ higher dependence on digital wealth management and digital payments for online sales. In addition, online purchases would stimulate farmers’ greater demand for digital credit than online sales.

5.2.2. The IV Estimation Results

The IV estimation results of online purchases and sales on farmers’ usage of digital finance are shown in Table 3. The t values of IV were all significant at the 1% level and the first-stage F-statistics in the IV probit regression were 27.27 and 46.60, suggesting that the IV was a strong instrument, since it exceeded the conventional “rule of thumb” of 10 for an F-statistic [42]. The DWH endogeneity tests all rejected the null hypothesis that online purchases or sales were exogenous at the 10% significance level. The results indicated that online purchases or sales had a positive and significant impact on farmers’ adoption of digital payments, digital wealth management, and digital credit, at least at the 10% level. Additionally, the positive impact of online purchases or sales on farmers’ adoption of digital wealth management was larger than that impact on digital payments and digital credit, which was ignored in the existing studies [5,6,8]. Hence, we concluded that our main aforementioned conclusions were still confirmed with mitigating potential endogeneity of online purchases and sales.

Table 3.

IV estimation of the impact of e-commerce adoption on digital finance usage.

5.3. Robustness Checks

5.3.1. Rosenbaum Bound Sensitivity Analysis

Since the influence arising from unobservable factors was not considered in the PSM estimation, we used the sensitivity analysis of treatment effect to do the robustness test. When the gamma coefficient, which refers to the effect of ignored and unobservable factors, is close to one, and the existing conclusion is no longer significant, the PSM estimation result is not robust; however, when the gamma coefficient is larger than one (usually close to two), and the existing conclusion becomes no longer significant, the result is relatively reliable [45]. Through the ATT sensitivity analysis results (the details are not reported here due to the space limitations), we clearly found that, when the gamma coefficient increased to 3.8 and 4.2, respectively, the impacts of online purchases and sales on farmers’ participation in the digital financial market were no longer significant. Therefore, the conclusions of our study were robust.

5.3.2. Superposition Effect

For further robustness testing, we took both online purchases and online sales as the treatment variable. As shown in Table A3 of Appendix A, the average treatment effects of both online purchases and online sales on the use of digital payments, digital wealth management, and digital credit were significantly positive—at least at the 10% significance level—and the average ATTs were 0.0776, 0.0890, and 0.0712, respectively. Those farmers who have more experience in online purchases and sales were inclined to have stronger demands for and more adoption of digital financial products and services [8]. In brief, the impact of both online purchases and sales on farmers’ usage of digital wealth management was successively greater than that on digital payments and digital credit, which was never discussed in the previous studies [8]. Therefore, the main conclusions above were robust.

5.4. Potential Impact Pathways

Table 4 summarizes the outcomes of the mediation effect test of digital financial literacy. According to the hierarchical regression model proposed by Baron and Kenny [46], we successively estimated the effect of online purchases and sales on participation in the digital financial market (Columns 1 to 3), the effect of online purchases and sales on digital financial literacy (Column 4), and the effect of online purchases and sales on participation in the digital financial market with digital financial literacy introduced (Columns 5 to 7).

Table 4.

The mediation effect of digital financial literacy.

Considering that digital financial literacy could be an endogenous variable due to measurement errors, omitted unobservable variables, and reverse causality, we use IV approach to address potential endogeneity of digital financial literacy. Following Bucher-Koenen and Lusardi [51], we used the average level of digital financial literacy in the respondents’ village (excluding the respondent) as a potentially valid instrumental variable (IV). On the one hand, farmers’ average level of digital financial literacy in the same village (excluding the respondent) was clearly related to the respondents’ digital financial literacy, due to a high similarity for respondents coming from the same village in terms of social and economic characteristics. On the other hand, farmers’ usage of digital finance might not have been affected by the average digital financial literacy of others coming from their villages; therefore, the two requirements, correlation and exogeneity, for a valid instrument were likely to be satisfied [42].

As shown in Columns (1) to (4), online purchases positively and significantly affected farmers’ digital payments, digital wealth management, digital credit, and digital financial literacy at the 10%, 1%, 5%, and 1% levels, with magnitudes of 0.0822, 0.0910, 0.0485, and 0.4987, respectively. Likewise, online sales were positively and significantly associated with farmers’ digital payments, digital wealth management, digital credit, and digital financial literacy at the 1%, 1%, 10%, and 1% levels, with magnitudes of 0.1028, 0.1151, 0.0634, and 0.4264, respectively. As presented in Columns (5) to (7), all the DWH endogeneity tests rejected the null hypothesis that digital financial literacy was exogenous at the 1% significance level. The first-stage F-statistic in the IV probit regression was 35.11 with a t-value of 6.35, verifying that the IV was a strong instrument [42]. The results indicated that online purchases had a positive and significant impact on farmers’ participation in digital payments, digital wealth management, and digital credit, with magnitudes of 0.0738, 0.0531, and 0.0337, respectively. Likewise, online sales had a positive and significant impact on farmers’ participation in digital payments, digital wealth management, and digital credit, with magnitudes of 0.0912, 0.0665, and 0.0342, respectively. A comparison of the marginal effects from only introducing online purchases or sales in Columns (1) to (3) and those from simultaneously introducing online purchases or sales and digital financial literacy in Columns (5) to (7) show that the former effects are larger. With reference to the mediation effect test procedures put forward by Baron and Kenny [46], we concluded that both online purchases and sales could affect farmers’ participation in the digital financial market through the partial mediation effect of digital financial literacy. Our findings expanded the existing research on the relationship between e-commerce adoption and individuals’ financial literacy [23], and the relationship between e-commerce adoption and online banking service utilization [8]. Furthermore, the Sobel test showed that 52.74%, 36.29%, and 58.56%, respectively, of the impacts between online purchases and farmers’ participation in digital payment, digital wealth management, and digital credit were mediated by digital financial literacy. Similarly, 27.62%, 25.84%, and 29.66%, respectively, of the impacts between online sales and farmers’ participation in digital payment, digital wealth management, and digital credit were mediated by digital financial literacy. These findings confirmed that farmers’ participation practice of both online purchase and online sales benefits for the accumulation of digital financial literacy [23], and then promotes their rational usage of digital financial products and services.

5.5. Heterogeneous Treatment Effects

Farmers’ education level, skills training experience, engaging in new agricultural operation entities (e.g., family farms, professional cooperatives), and entrepreneurial industries (agricultural and non-agricultural entrepreneurship) all have potential impacts on their adoption of e-commerce [17,49] and participation in the digital financial market [8,9]. Thus, they are regarded as group variables to explore the heterogeneous treatment effects across different groups. The results are displayed in Table 5.

Table 5.

Heterogeneity results of the impact of e-commerce adoption on usage of digital finance.

As reported in Columns (1) and (2), for farmers with a high level of education, online purchases or sales adoption could increase the propensity of using digital payments, digital wealth management and digital credit at least at a 10% significance level, while only the impact of online sales on digital payments was significant at a 10% level for farmers with a low education level. As shown in Columns (3) and (4), for those farmers with skills training experience, online purchases could facilitate their involvement in digital wealth management and digital credit at the 5% and 10% significance levels, respectively; online sales could lead to a high probability of using digital payments and digital wealth management at the 10% and 1% significance levels, respectively. As displayed in Columns (5) and (6), for the new agricultural operation entities, online purchases could promote their use of wealth management and access to credit through the internet at the 5% significance level, respectively; online sales could lead to a high probability of using digital payments and digital wealth management at the 10% and 1% significance levels, respectively. As reported in Columns (7) and (8), both online purchases and online sales showed a significant impact on participation in the digital financial market for farmers engaging in agricultural entrepreneurship.

Consequently, the group comparisons indicated that the marginal effects of online purchases and sales on farmers’ participation in the digital financial market were generally larger among farmers who had higher education levels, more skills training experience, were running new agricultural operation entities and were pursuing agriculture entrepreneurship. Reasons for such could be that higher education levels lead to a better understanding of the costs, benefits, and risks of digital financial products and a better ability to make good use of them [25]. Moreover, possessing business-related skills training would enhance farmers’ abilities to choose and adopt digital financial products and services, thus increasing their trust in digital finance [52]. In addition, there are more capital transactions, liquidity management, credit demand, and higher levels of risk tolerance and internet usage for new agricultural operation entities compared with traditional agricultural operators [38]. Agricultural entrepreneurs are more familiar with and show more dependence on the production and sales activities in the field of agriculture [53], which makes it relatively easier for them to participate in the digital financial market related to the agricultural field.

6. Conclusions and Implications

Few studies have documented the impacts of e-commerce adoption measured by online purchases and sales when explaining farmers’ digital financial exclusion [5,6]. Our results provide a new perspective on the relationship between the e-commerce adoption for both online products demanders and suppliers and their participation in the digital financial market in rural areas. Using survey data on 832 entrepreneurial farmers in rural China, we reveal that both online purchases and online sales have a significant and positive impact on farmers’ participation in the digital financial market. This effect on the usage of digital wealth management is successively larger than that on the usage of digital payments and digital credit. Moreover, the effect of online purchases and sales on farmers’ participation in the digital financial market could be consistently mediated by their digital financial literacy. The results further provide strong evidence for that the impact of online purchases and sales on farmers’ participation in the digital financial market is greater for those with high education levels, pursuing skills training, running new agricultural operation entities, and engaging in agricultural entrepreneurship.

Our study indicates that the driving role of e-commerce adoption both for online products suppliers and demanders on their engagement in the digital financial market should not be ignored in the digital economy era. Our findings also contribute to the literature by elucidating the differential influence of e-commerce adoption characterized by online purchases and sales on farmers’ usage of multiple digital financial products, represented by digital payments, digital wealth management, and digital credit. In addition, our discussion on the impact path of e-commerce adoption on the participation in digital financial market solicits further attention to farmers’ digital financial literacy, and other possible pathways. The heterogeneous effect of e-commerce adoption for different groups suggests that farmers’ participation gap in the digital financial market would be widened caused by e-commerce adoption.

This study provides beneficial practical implications as follows. First, our study suggests that both online purchases and online sales significantly increased farmers’ participation in the digital financial market. In order to relieve farmers’ digital financial exclusion, governments in China are expected to take more effective measures to enhance adoption rates of online purchases and sales technology, in particular for entrepreneurial farmers. Professional and systematic digital education relating to online purchases, online sales, online management, and other related content for different types of farmers is urgently needed for further enhancing their adaptability to new changes in the era of e-commerce. Additionally, the establishment of information support systems, such as internet infrastructure, logistics facilities, and e-commerce service platforms, should be constantly optimized. On the basis of this, the construction of e-commerce demonstration regions and Taobao villages should be continuously promoted.

Second, our findings also demonstrate that the impact of e-commerce adoption on farmers’ usage of various types of digital financial products is different, due to the difference in digital financial demands. Local financial institutions and the internet financial industry in China should actively strengthen the related investigation on different farmers’ requirements of digital financial market participation. It is an increasing trend among rural areas to accelerate market-oriented financial reforms and strengthen function-based regulation to foster the healthy and inclusive development of the digital financial market. The innovative design of digital financial products and services related to investment, wealth management, credit, and relevant intelligent terminals, should be strengthened for accelerating the digital financial inclusion in rural areas.

Third, more attention should be paid to the mediation role of digital financial literacy in the relationship between farmers’ online purchases and sales and their participation in the digital financial market. Government departments, financial institutions, schools, and social education resources in China should be actively encouraged to strengthen their systematic training of farmers’ financial knowledge, especially in the form of digital financial literacy. Moreover, farmers’ trust levels in the digital finance should be enhanced by promoting their overall digital financial literacy.

Fourth, our study further reveals that the effects of online purchases and sales on farmers’ adoption of digital payment, digital wealth management and digital credit vary across individual and family characteristics. The differences among farmers regarding education levels, production and operation types, and organizational forms should be fully considered when optimizing the supply of digital financial products and services. More effective measures should be taken to encourage more farmers to actively participate in skills training, expand their operation scale, and engage in new types of agricultural business entities. In order to reduce the gap in the usage of digital finance among farmers with different characteristics, more assistance should be given to the disadvantaged farmers.

Limitations still exist in this study, which drives us to pay attention to the improvement in aspects of sampling, empirical data, methods and impact mechanism in our future research. First, our study only used the survey data of farmers from three provinces of China for empirical analysis and was a lack of the survey of provinces from central China, which weakened the generalization of the research conclusions to a certain extent. To generalize our findings, we would conduct survey in central provinces and expand the sample to other provinces. Second, the cross-section data we used cannot capture the changes of participation decision in the digital financial market before and after e-commerce adoption, so there are obvious limitations in causality identification. Hence, we would try to establish panel data through longitudinal survey for further study. Third, we just tested the mediation effect of digital financial literacy when exploring the mechanism by e-commerce adoption affects farmers’ participation in the digital financial market. In future studies, we would discuss other pathways such as online social networks, income, and financial demand to extend our study.

It is worth noting that the epidemic of COVID-19 has a great impact on China’s agricultural production, sales, capital liquidity and the sustainability of small and micro enterprises in a certain period, but it also accelerates the digital transformation of the whole agricultural industry chain [54]. Since agriculture is the basic industry of China’s national economy and has the characteristics of weak industry vulnerable to natural risks and market risks, the improvement of the adoption rate of farmers’ e-commerce and participation degree of digital financial market will help to continuously improve the elasticity and efficiency of agricultural production. In the context of fighting against COVID-19, more and more farmers, especially entrepreneurial farmers, are actively using online purchase and sales technology to reduce information asymmetry and ensure the orderly operation of production and operation. This will also further promote farmers’ participation in the financial market from offline to online. Therefore, in further studies, it would be meaningful to explore the impact of COVID-19 on farmers’ e-commerce adoption and participation in the digital financial market.

Author Contributions

Conceptualization, L.S.; methodology, Y.P.; software, Y.P.; validation, L.S. and Y.P.; formal analysis, L.S.; investigation, L.S. and R.K.; resources, R.K.; data curation, L.S.; writing—original draft preparation, L.S. and Y.P.; writing—review and editing, L.S., Y.P. and Q.C.; supervision, R.K.; project administration, R.K. and L.S.; funding acquisition, R.K. and L.S. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by National Natural Science Foundation of China (NSFC) (grant numbers: 71773094 and 71903141), China Postdoctoral Science Foundation Project (grant number: 2020M680246), Humanities and Social Science Fund of Ministry of Education of China (grant number: 18YJC790125), and Natural Science Foundation Research Project of Shaanxi Province (grant number: 2020JQ-281).

Data Availability Statement

The datasets analyzed during the current study are not publicly available due to institutional restrictions but are available from the corresponding author on reasonable request.

Acknowledgments

L.L. contributed to the paper design, data collection, and writing. Y.L. contributed to the data analysis, paper review and revision. R.K. contributed to the paper revisions. Q.C. contributed to the language editing.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Definition and summary of variables(cont.).

Table A1.

Definition and summary of variables(cont.).

| Variables | Online Purchases | Online Sales | ||||

|---|---|---|---|---|---|---|

| Treatment | Control | T-Test | Treatment | Control | T-Test | |

| Digital payments | 0.90 (0.30) | 0.71 (0.45) | 0.19 *** | 0.91 (0.28) | 0.66 (0.47) | 0.25 *** |

| Digital wealth management | 0.41 (0.49) | 0.17 (0.38) | 0.24 *** | 0.38 (0.48) | 0.14 (0.35) | 0.24 *** |

| Digital credit | 0.19 (0.40) | 0.08 (0.26) | 0.11 *** | 0.17 (0.37) | 0.07 (0.25) | 0.10 *** |

| Digital financial literacy | 3.49 (0.13) | 2.11 (0.08) | 1.38 *** | 3.20 (0.11) | 2.02 (0.08) | 1.18 *** |

| Gender | 0.86 (0.35) | 0.75 (0.43) | 0.11 *** | 0.81 (0.39) | 0.76 (0.43) | 0.05 * |

| Age | 42.04 (9.01) | 45.24 (9.15) | −3.20 *** | 41.97 (8.89) | 45.87 (9.10) | 3.90 *** |

| Education | 10.43 (3.18) | 8.48 (3.25) | 1.95 *** | 9.92 (3.30) | 8.40 (3.24) | 1.52 *** |

| Risk propensity | 2.62 (1.08) | 2.44 (1.09) | 0.18 ** | 2.67 (1.10) | 2.38 (1.07) | 0.29 *** |

| Internet learning ability | 3.89 (1.15) | 3.19 (1.37) | 0.70 *** | 3.86 (1.15) | 3.07 (1.38) | 0.79 *** |

| Skills training experience | 0.69 (0.46) | 0.48 (0.50) | 0.21 *** | 0.63 (0.48) | 0.48 (0.50) | 0.15 *** |

| Information access | 0.73 (0.45) | 0.53 (0.50) | 0.20 *** | 0.78 (0.42) | 0.46 (0.50) | 0.32 *** |

| Time online | 19.79 (15.82) | 12.92 (12.56) | 6.87 *** | 19.44 (16.54) | 11.82 (10.96) | 7.62 *** |

| Annual network fee | 9.59 (9.05) | 6.57 (8.22) | 302.05 *** | 9.60 (8.64) | 6.00 (7.22) | 359.64 *** |

| Number of WeChat friends | 1.21 (2.13) | 0.52 (1.89) | 68.94 *** | 1.11 (2.50) | 0.45 (2.51) | 66.62 *** |

| Financial network | 0.23 (0.42) | 0.16 (0.37) | 0.07 ** | 0.23 (0.42) | 0.15 (0.36) | 0.08 *** |

| New agricultural operation entities | 0.47 (0.50) | 0.28 (0.45) | 0.19 *** | 0.42 (0.49) | 0.27 (0.44) | 0.15 *** |

| Entrepreneurship industry | 0.51 (0.50) | 0.36 (0.48) | 0.15 *** | 0.50 (0.50) | 0.33 (0.47) | 0.17 *** |

| Distance to town | 4.84 (3.58) | 5.76 (6.48) | −0.92 ** | 5.02 (3.58) | 5.12 (5.69) | −0.10 |

| Formal financial institution status | 2.18 (1.12) | 2.13 (1.15) | 0.05 | 2.10 (2.10) | 2.16 (1.19) | −0.06 |

| Taobao shops | 0.29 (0.45) | 0.26 (0.44) | 0.03 | 0.34 (0.47) | 0.26 (0.44) | 0.08 * |

| Shaanxi | 0.44 (0.50) | 0.36 (0.48) | 0.08 * | 0.43 (0.50) | 0.35 (0.48) | 0.08 ** |

| Ningxia | 0.29 (0.46) | 0.38 (0.49) | −0.09 ** | 0.30 (0.46) | 0.40 (0.49) | −0.10 *** |

| Observations | 195 | 637 | 295 | 537 | ||

Notes: mean values outside the parentheses with standard deviations in parentheses; * P < 0.1, ** P < 0.05, *** P < 0.01.

Table A2.

Determinants of adoption of online purchases and sales.

Table A2.

Determinants of adoption of online purchases and sales.

| Variables | Online Purchases | Online Sales |

|---|---|---|

| Gender | 0.4443 *** (0.1441) | 0.2190 * (0.1279) |

| Age | −0.0048 (0.0063) | −0.0081 (0.0059) |

| Education | 0.0570 *** (0.0185) | 0.0141 (0.0170) |

| Risk propensity | −0.0045 (0.0502) | 0.0756 * (0.0458) |

| Internet learning ability | 0.0786 * (0.0469) | 0.0970 ** (0.0436) |

| Skills training experience | 0.3054 *** (0.1187) | 0.2566 ** (0.1103) |

| Information access | 0.1199 (0.1200) | 0.5131 *** (0.1109) |

| Online time per week | 0.0134 *** (0.0040) | 0.0141 *** (0.0042) |

| Annual network fee | 0.0001 (0.0001) | 0.0002 ** (0.0001) |

| Number of WeChat friends | 0.0003 (0.0002) | 0.0003 (0.0002) |

| Financial network | 0.0529 (0.1341) | 0.0949 (0.1286) |

| New agricultural operation entities | 0.2581 ** (0.1260) | 0.2138 * (0.1183) |

| Entrepreneurship industry | 0.4153 *** (0.1143) | 0.3930 *** (0.1080) |

| Distance to the nearest town | −0.0337 ** (0.0151) | 0.0048 (0.0116) |

| Formal financial institution status | 0.0364 (0.0482) | 0.0028 (0.0450) |

| Taobao shops | −0.1260 (0.1313) | 0.2867 ** (0.1213) |

| Shaanxi | 0.0370 (0.1534) | 0.1051 (0.1429) |

| Ningxia | −0.0570 (0.1603) | 0.0588 (0.1477) |

| Observations | 832 | 832 |

| LR X2 | 143.30 *** | 191.17 *** |

Notes: standard errors in parentheses; * P < 0.1, ** P < 0.05, *** P < 0.01; Shandong was taken as the control group.

Table A3.

The superposition effect of both online purchases and sales.

Table A3.

The superposition effect of both online purchases and sales.

| Methods | Treated | Controls | ATT | Average ATTs | |

|---|---|---|---|---|---|

| Digital payments | NNM | 0.9357 | 0.8378 | 0.0980 *** (0.0350) | 0.0776 |

| CM | 0.9328 | 0.8571 | 0.0757 ** (0.0353) | ||

| NNMC | 0.9328 | 0.8535 | 0.0793 ** (0.0343) | ||

| KM | 0.9357 | 0.8697 | 0.0660 * (0.0383) | ||

| SM | 0.9362 | 0.8675 | 0.0687 ** (0.0316) | ||

| MM | 0.9362 | 0.8582 | 0.0780 * (0.0387) | ||

| Digital wealth management | NNM | 0.4286 | 0.3378 | 0.0908 * (0.0531) | 0.0890 |

| CM | 0.4254 | 0.3423 | 0.0831 * (0.0499) | ||

| NNMC | 0.4254 | 0.3345 | 0.0909 * (0.0525) | ||

| KM | 0.4286 | 0.3455 | 0.0831 * (0.0502) | ||

| SM | 0.4255 | 0.3429 | 0.0826 * (0.0498) | ||

| MM | 0.4256 | 0.3221 | 0.1035 ** (0.0547) | ||

| Digital credit | NNM | 0.2000 | 0.1153 | 0.0847 ** (0.0411) | 0.0712 |

| CM | 0.1940 | 0.1278 | 0.0662 * (0.0388) | ||

| NNMC | 0.1940 | 0.1218 | 0.0722 * (0.0405) | ||

| KM | 0.2000 | 0.1291 | 0.0709 * (0.0340) | ||

| SM | 0.1986 | 0.1319 | 0.0667 * (0.0390) | ||

| MM | 0.1986 | 0.1324 | 0.0662 * (0.0344) |

Notes: standard errors in parentheses; * P < 0.1, ** P < 0.05, *** P < 0.01. NNM denotes nearest neighbor matching; CM denotes caliper matching; NNMC denotes nearest neighbor matching with a caliper; KM denotes kernel matching; SM denotes spline matching; and MM denotes Mahalanobis matching.

Figure A1.

Propensity score density function of adopters and non-adopters of online purchases and sales.

References

- Liao, G.K.; Yao, D.Q.; Hu, Z.H. The spatial effect of the efficiency of regional financial resource allocation from the perspective of internet finance: Evidence from Chinese provinces. Emerg. Mark. Financ. Trade 2020, 56, 1–13. [Google Scholar] [CrossRef]

- Lei, Y. Policy Discussion of Internet Finance in China. BOFIT Policy Brief, Institute for Economies in Transition, Bank of Finland. 25 November 2014. Available online: https://helda.helsinki.fi/bof/bitstream/handle/123456789/13462/bpb1314%5b1%5d.pdf?sequence=1&isAllowed=y (accessed on 20 April 2021).

- Ren, B.Y.; Li, L.Y.; Zhao, H.M.; Zhou, Y.B. The financial exclusion in the development of digital finance: A study based on survey data in the JingJinJi rural area. Singap. Econ. Rev. 2018, 63, 65–82. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J.J. The impact of digital finance on household consumption: Evidence from China. Econ. Model. 2020, 86, 317–326. [Google Scholar] [CrossRef]

- Lenka, S.K.; Barik, R. Has expansion of mobile phone and internet use spurred financial inclusion in the SAARC countries? Financ. Innov. 2018, 4, 1–19. [Google Scholar] [CrossRef]

- Turvey, C.G.; Xiong, X. Financial inclusion, financial education, and e-commerce in rural China. Agribusiness 2017, 33, 279–285. [Google Scholar] [CrossRef]

- Zhang, Q.; Posso, A. Thinking inside the Box: A closer look at financial inclusion and household income. J. Dev. Stud. 2019, 55, 1616–1631. [Google Scholar] [CrossRef]

- Hojjati, S.N.; Rabi, A.R. Effects of Iranian online behavior on the acceptance of internet banking. J. Asian Bus. Stud. 2013, 7, 123–139. [Google Scholar] [CrossRef]

- Mu, H.L.; Lee, Y.C. Examining the influencing factors of third-party mobile payment adoption: A comparative study of Alipay and WeChat pay. J. Inform. Syst. 2017, 26, 257–294. [Google Scholar]

- Ren, J.Z.; Sun, H. Acceptance behavior of internet wealth management based on user risk perception: The case of Alibaba’s Yuebao. In Proceedings of the 2017 International Conference on Management Engineering, Software Engineering and Service Sciences, Wuhan, China, 14–16 January 2017. [Google Scholar]

- Lele, U.; Goswami, S. The fourth industrial revolution, agricultural and rural innovation, and implications for public policy and investments: A case of India. Agric. Econ. 2017, 48, 87–100. [Google Scholar] [CrossRef]

- Qi, J.Q.; Zheng, X.Y.; Guo, H.D. The formation of Taobao villages in China. China Econ. Rev. 2019, 53, 106–127. [Google Scholar] [CrossRef]

- Liu, M.; Zhang, Q.; Gao, S.; Huang, J.K. The spatial aggregation of rural e-commerce in China: An empirical investigation into Taobao Villages. J. Rural Stud. 2020, 80, 403–417. [Google Scholar] [CrossRef]

- Chitura, T.; Mupemhi, S.; Dube, T.; Bolongkikit, J. Barriers to electronic commerce adoption in small and medium enterprises: A critical literature review. J. Int. Bank. Commer. 2008, 13, 1–13. [Google Scholar]

- Malhotra, R.; Malhotra, D.K. The impact of internet and e-commerce on the evolving business models in the financial services industry. Int. J. Electron. Bus. 2006, 4, 56–82. [Google Scholar] [CrossRef]

- Patel, V.B.; Asthana, A.K.; Patel, K.J.; Patel, K.M. A study on adoption of e-commerce practices among the Indian farmers with specific reference to north Gujarat region. Inter. J. Commer. Bus. Manag. 2016, 9, 1–7. [Google Scholar] [CrossRef]

- Chiu, Y.P.; Lo, S.K.; Hsieh, A.Y.; Hwang, Y.J. Exploring why people spend more time shopping online than in offline stores. Comput. Hum. Behav. 2019, 95, 24–30. [Google Scholar] [CrossRef]

- Wu, L.Y.; Chen, K.Y.; Chen, P.Y.; Cheng, S.L. Perceived value, transaction cost, and repurchase-intention in online shopping: A relational exchange perspective. J. Bus. Res. 2014, 67, 2768–2776. [Google Scholar] [CrossRef]

- Baourakis, G.; Kourgiantakis, M.; Migdalas, A. The impact of e-commerce on agro-food marketing: The case of agricultural cooperatives, firms and consumers in Crete. Br. Food J. 2002, 104, 580–590. [Google Scholar] [CrossRef]

- Treiblmaier, H.; Pinterits, A.; Floh, A. Success factors of internet payment systems. Inter. J. Electron. Bus. 2008, 6, 369–385. [Google Scholar] [CrossRef]

- Xu, N.N.; Shi, J.Y.; Rong, Z.; Yuan, Y. Financial literacy and formal credit accessibility: Evidence from informal businesses in China. Financ. Res. Lett. 2020, 36, 101327. [Google Scholar] [CrossRef]

- Lee, S. Evaluation of mobile application in user’s perspective: Case of P2P lending apps in fintech industry. KSII Trans. Internet Inf. Syst. 2017, 11, 1105–1117. [Google Scholar]

- Lam, L.T.; Lam, M.K. The association between financial literacy and problematic internet shopping in a multinational sample. Addict. Behav. Rep. 2017, 6, 123–127. [Google Scholar] [CrossRef] [PubMed]

- Navickas, M.; Gudaitis, T.; Krajnakova, E. Influence of financial literacy on management of personal finances in a young household. Bus. Theory Pract. 2014, 15, 32–40. [Google Scholar] [CrossRef]

- Kolodinsky, J.M.; Hogarth, J.M.; Hilgert, M.A. The adoption of electronic banking technologies by US consumers. Inter. J. Bank Mark. 2004, 22, 238–259. [Google Scholar] [CrossRef]

- Xie, P.; Zou, C.W. Studies on the mode of internet finance. J. Financ. Res. 2012, 12, 11–22. [Google Scholar]

- Wu, X.Q. Internet finance: The logic of growth. Financ. Trade Econ. 2015, 2, 5–15. [Google Scholar]

- Tufano, P. Consumer finance. Annu. Rev. Financ. Econ. 2009, 1, 227–247. [Google Scholar] [CrossRef]

- Lo, S.K.; Hsieh, A.Y.; Chiu, Y.P. Why expect lower prices online? Empirical examination in online and store-based retailers. Inter. J. Electron. Commer. Stud. 2014, 5, 27–37. [Google Scholar] [CrossRef]

- Patnaik, B.C.M.; Sethy, P.K. An empirical study on NPAs in working capital loan of Gramya banks. TRANS Asian J. Mark. Manag. Res. 2013, 2, 1–13. [Google Scholar]

- Lee, E.; Lee, B. Herding behavior in online P2P lending: An empirical investigation. Electron. Commer. Res. Appl. 2012, 11, 495–503. [Google Scholar] [CrossRef]

- Van Rooij, M.; Lusardi, A.; Alessie, R. Financial literacy and stock market participation. J. Financ. Econ. 2011, 101, 449–472. [Google Scholar] [CrossRef]

- Yang, S.; Chen, S.X.; Li, B. The role of business and friendships on WeChat business: An emerging business model in China. J. Glob. Mark. 2016, 29, 174–187. [Google Scholar] [CrossRef]

- Lv, Z.P.; Jin, Y.; Huang, J.H. How do sellers use live chat to influence consumer purchase decisions in China? Electron. Commer. Res. Appl. 2018, 28, 102–113. [Google Scholar] [CrossRef]

- Bai, B.; Law, R.; Wen, I. The impact of website quality on customer satisfaction and purchase intentions: Evidence from Chinese online visitors. Int. J. Hosp. Manag. 2008, 27, 391–402. [Google Scholar] [CrossRef]

- Rahimnia, F.; Hassanzadeh, J.F. The impact of website content dimension and e-trust on e-marketing effectiveness: The case of Iranian commercial saffron corporations. Inf. Manag. 2013, 50, 240–247. [Google Scholar] [CrossRef]

- Panda, A. The status of working capital and its relationship with sales. Int. J. Commer. Manag. 2012, 22, 36–52. [Google Scholar] [CrossRef]

- Hu, L.; Lopez, R.A.; Zeng, Y. The impact of credit constraints on the performance of Chinese agricultural wholesalers. Appl. Econ. 2019, 51, 3864–3875. [Google Scholar] [CrossRef]

- Miller, M.; Godfrey, N.; Lévesque, B.; Stark, E. The Case for Financial Literacy in Developing Countries: Promoting Access to Finance by Empowering Consumers; World Bank, DFID, OECD and CGAP Joint Note: Washington, DC, USA, 2009. [Google Scholar]

- Becerril, J.; Abdulai, A. The impact of improved maize varieties on poverty in Mexico: A propensity score-matching approach. World Dev. 2010, 38, 1024–1035. [Google Scholar] [CrossRef]

- Morgan, P.J.; Long, T.Q. Financial literacy, financial inclusion, and savings behavior in Laos. J. Asian Econ. 2020, 68, 101197. [Google Scholar] [CrossRef]

- Staiger, D.; Stock, J.H. Instrumental Variables Regression with Weak Instruments. Econometrica 1997, 65, 557–586. [Google Scholar] [CrossRef]

- Heckman, J.J.; Vytlacil, E.J. Econometric evaluation of social programs, part II: Using the marginal treatment effect to organize alternative econometric estimators to evaluate social programs, and to forecast their effects in new environments. In Handbook of Econometrics; Elsevier: Amsterdam, The Netherlands, 2007; pp. 4875–5143. [Google Scholar]

- Rosenbaum, P.R.; Rubin, D.B. Constructing a control group using multivariate matched sampling methods that incorporate the propensity score. Am. Stat. 1985, 39, 33–38. [Google Scholar]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Biometrika 1983, 70, 41–55. [Google Scholar] [CrossRef]